Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

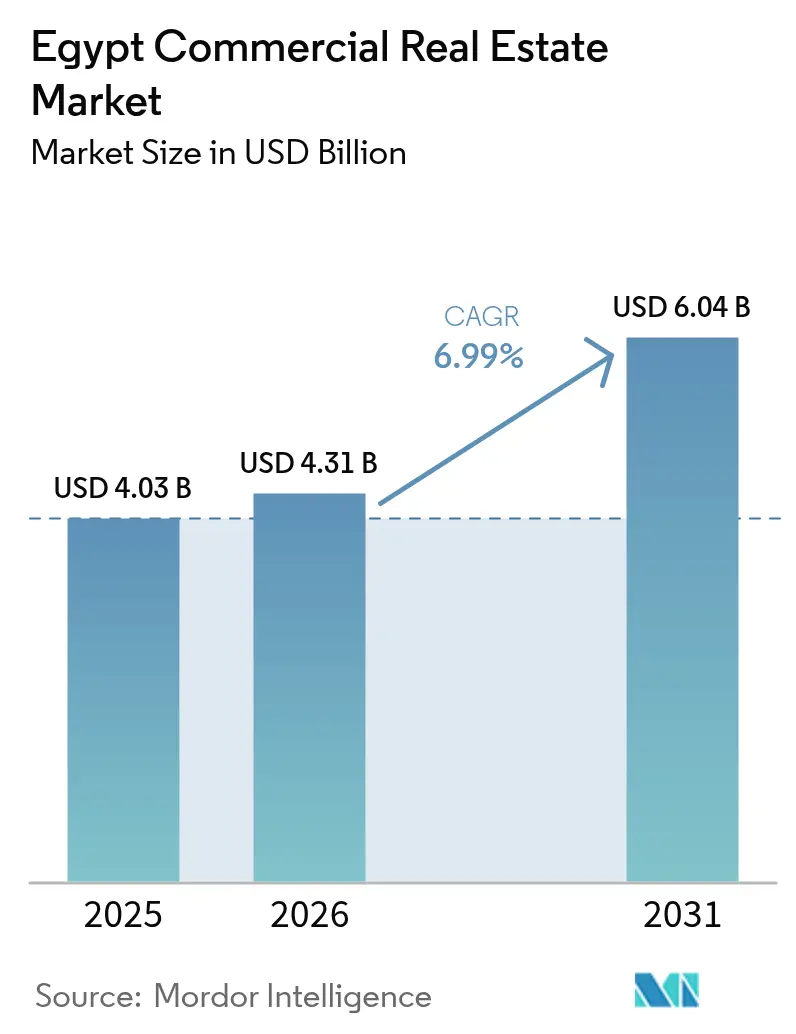

| Base Year Market Size (2025) | USD 4.03 Billion |

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 6.04 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Commercial Real Estate Market Analysis by Mordor Intelligence

Egypt commercial real estate market size in 2026 is estimated at USD 4.31 billion, growing from 2025 value of USD 4.03 billion with 2031 projections showing USD 6.04 billion, growing at 6.99% CAGR over 2026-2031. Robust infrastructure spending, liberalized land‐ownership laws, and record foreign direct investment are reshaping the sector’s demand profile, especially around the New Administrative Capital and the Suez Canal Economic Zone. Corporate relocations, tourism recovery, and surging e-commerce volumes are broadening asset-class appeal while diversified funding channels sustain development momentum despite a high-interest-rate environment. Currency stabilization prospects and hard-currency lease structures further improve the Egypt commercial real estate market’s risk-adjusted returns for global investors. Simultaneously, sustainability mandates and smart-city frameworks are forcing landlords to upgrade inventories to maintain competitive positioning.

Key Report Takeaways

- By property type, offices commanded 43.02% of the Egypt commercial real estate market share in 2025, whereas retail assets are projected to expand at a 9.60% CAGR through 2031.

- By business model, the rental segment held 73.62% of the Egypt commercial real estate market size in 2025, while sales transactions are advancing at an 8.44% CAGR to 2031.

- By end-user, corporate and SME occupiers accounted for 69.94% of overall demand in 2025; household participation is climbing at a 9.18% CAGR through 2031.

- By geography, Greater Cairo retained 60.05% share of the Egypt commercial real estate market in 2025, yet secondary locations are accelerating at an 11.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Commercial Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mega-projects (New Admin Capital, SCZone) | +2.1% | New Administrative Capital, Suez Canal Economic Zone | Short term (≤ 2 years) |

| Rapid population growth & urbanisation pressures | +1.8% | Greater Cairo, Alexandria, Giza | Long term (≥ 4 years) |

| Tourism-led demand for hospitality & retail assets | +1.2% | North Coast, Red Sea, Greater Cairo | Medium term (2-4 years) |

| Booming e-commerce boosts logistics & last-mile hubs | +0.9% | Greater Cairo, Alexandria, industrial zones | Medium term (2-4 years) |

| Near-shoring of EU manufacturing to Egyptian free-zones | +0.7% | Suez Canal Economic Zone, industrial free zones | Long term (≥ 4 years) |

| Green-building incentives & sustainability mandates | +0.4% | New Administrative Capital, Greater Cairo | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mega-Projects Establish New Commercial Epicenters

The USD 58 billion New Administrative Capital and the expanding Suez Canal Economic Zone exemplify state-led urban catalysts that anchor private investment. Ministry relocations instantly populate office districts, while logistics parks like Mercedes-Benz’s Sokhna hub validate industrial take-up. Such integrated ecosystems lower investor risk by guaranteeing early-stage occupancy and infrastructure readiness. Fiscal incentives and streamlined permitting under the Golden Licence program further compress project gestation periods, supporting rapid absorption. These mega-projects hence recalibrate supply–demand balances, elevating the Egypt commercial real estate market into a regional node for governmental, industrial, and service activities[1]Ministry of Housing, “New Administrative Capital Project Factsheet,” moh.gov.eg.

Rapid Population Growth & Urbanization Pressures

Egypt’s demographic expansion is compelling developers to pioneer satellite cities such as the 170,000-acre New Administrative Capital designed for 6.5 million residents. This distributed urban model lessens congestion in central Cairo and sparks demand for integrated office, retail, and logistics complexes that operate as self-contained economic ecosystems. Projects like the 1.5 Million Feddan scheme couple agricultural expansion with industrial-zone creation, widening commercial footprints beyond legacy corridors. As populations shift, mixed-use projects that bundle civic, residential, and commercial functions gain a structural demand advantage. Consequently, the Egypt commercial real estate market is evolving toward polycentric growth nodes that diversify risk and enhance tenant optionality.

Tourism-Led Demand For Hospitality & Retail Assets

Egypt leads Africa’s hotel pipeline with 143 properties under development, and global brands such as Hilton plan to triple their local portfolios. The USD 150 billion Ras El-Hekma mega-project targets 8 million annual visitors, catalyzing mixed retail and entertainment formats that serve both tourists and residents. Lifestyle hotel concepts and experiential shopping centers are proliferating to satisfy new traveler preferences, spawning secondary demand for logistics, food-service, and warehousing facilities. As visitor numbers climb, transitional spending across dining, transport, and leisure reinforces rental resilience in adjacent retail corridors. The tourism rebound therefore multiplies revenue streams beyond direct hospitality returns, deepening the Egypt commercial real estate market’s diversification.

Booming E-Commerce Transforms Logistics Requirements

National platforms such as the Nafeza single-window system and Advanced Cargo Information streamline customs clearance, enabling faster last-mile delivery decisions. AD Ports Group’s 20 km² KEZAD East Port Said Zone integrates bonded warehousing with fulfillment operations, serving both international trade and domestic online retail. Demand is shifting toward modern distribution centers that combine cross-docking, temperature-controlled storage, and returns processing capabilities. Developers that can deliver Grade-A space near population clusters secure premium rents and longer leases. As digital penetration climbs, e-commerce continues to unlock a material share of the Egypt commercial real estate market’s future pipeline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-digit inflation & high financing costs | -1.4% | National, with acute impact in Greater Cairo | Short term (≤ 2 years) |

| Egyptian-pound volatility vs. hard-currency rents | -0.8% | National, particularly affecting foreign investors | Medium term (2-4 years) |

| Escalating construction input costs | -0.6% | National, concentrated in major development zones | Short term (≤ 2 years) |

| Land-title & registration inefficiencies | -0.3% | National, with regional variations in processing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Double-Digit Inflation Pressures Development Economics and Tenant Affordability

Annual inflation above 25% forces the Central Bank to uphold a 28.25% overnight lending rate, driving construction loan pricing into double digits. Developers either delay launches or pivot to presales and partnership financing to preserve margins. Operating costs also climb: utility tariffs rose 43.6% year-over-year, and commercial rents increased 12.7%, squeezing tenant affordability. Prime assets with hard-currency leases sustain occupancy, but secondary stock witnesses elevated churn. Over time, price normalization and alternative funding vehicles should stabilize capital costs within the Egypt commercial real estate market.

Currency Volatility Creates Investment Uncertainty Despite Fundamental Strengths

Three devaluations since 2024 expanded the USD/EGP corridor, prompting investors to prefer dollar-indexed leases. Goldman Sachs now pegs the pound as 30% undervalued, yet policy signaling remains a market-sentiment swing factor. Banks face capital-adequacy erosion, tempering construction-loan appetite. Nevertheless, a USD 35 billion UAE commitment in Ras El-Hekma and augmented IMF backing uplift foreign-currency liquidity, hinting at medium-term exchange-rate stabilization. Until clarity emerges, sponsors hedge via offshore debt and hard-currency presales within the Egypt commercial real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Offices Dominate While Retail Surges

Offices secured 43.02% of the Egypt commercial real estate market share in 2025, buoyed by the relocation of 14 ministries and more than 48,000 staff to the New Administrative Capital. Grade-A towers like Infinity Tower (160 meters, LEED Platinum-targeted) are 70% complete and pre-leased to multinational tenants demanding environmentally certified space. The segment benefits from long leases, ancillary service demand, and government anchor occupancy that de-risks vacancy exposure. Meanwhile, retail assets are projected to post a 9.60% CAGR through 2031, the fastest across property types, as tourism rebounds and lifestyle centers such as Cairo Festival City Mall (USD 566.7 million) reopen with flagship tenants. Developers are blending experiential formats food halls, entertainment clusters, and digital storefronts to attract spending and extend dwell times.

The logistics sub-category gains structural support from Egypt’s trade ambitions. Mercedes-Benz’s Sokhna logistics park and AD Ports Group’s USD 120 million KEZAD zone illustrate the pivot toward build-to-suit facilities proximate to multimodal corridors. Industrial assets within the “Others” bucket tap near-shoring demand, especially from EU manufacturers leveraging duty-free access. Rising land prices in coastal projects such as Ras El-Hekma encourage vertical mixed-use clustering, spreading risk across retail, hospitality, and office stacks. Consequently, the Egypt commercial real estate market size for logistics is expected to widen its revenue slice as e-commerce consolidates share.

By Business Model: Rental Predominance Under Tight Credit

Rental agreements captured 73.62% of the Egypt commercial real estate market size in 2025 owing to high borrowing costs and corporate preferences for operational flexibility. Institutional financiers support this model: a USD 343.3 million facility for Palm Hills’ Badya and a USD 138 million loan for SODIC’s Karmell were structured around stabilized rental cash flows. Tenants gravitate toward hard-currency denominated leases to hedge inflation, further reinforcing landlord income security. The sales pathway, however, is quickening at an 8.44% CAGR to 2031 after the 2024 Desert Land Law amendment removed foreign-ownership caps, sparking offshore interest in strata titles and bulk acquisitions. As rent control reforms phase in 20-fold increases over five years, some occupiers may pivot to ownership once price parity emerges.

Hybrid models are also germinating. Sale-and-leaseback deals enable corporates to unlock capital while retaining operational control, and profit-sharing arrangements align developer and retailer incentives in new lifestyle malls. This flexibility supports transaction diversity, ultimately expanding liquidity channels in the Egypt commercial real estate market.

By End-User: Corporate Demand Leads, Households Accelerate

Corporate and SME occupiers generated 69.94% of total take-up in 2025, underpinned by headquarter moves, manufacturing expansion in free zones, and rising demand for tech-ready space. Multinationals impose ESG and health-safety standards, nudging developers toward smart building management systems and renewable power integration. Household and high-net-worth investors, although smaller, are growing at a 9.18% CAGR as liberalized ownership and fintech mortgage solutions improve accessibility. GCC investors, funneling USD 115 billion since 2021, often co-invest with local partners, blending regional liquidity with on-ground expertise.

Institutional capital remains active: Egypt’s M&A volume climbed 21% with USD 46.1 billion in FDI during 2024, and sovereign funds increasingly anchor development vehicles targeting green and social infrastructure. This diversified buyer base underpins resilience across the Egypt commercial real estate industry’s demand spectrum.

Geography Analysis

Greater Cairo’s unified metropolitan area, inclusive of the 170,000-acre New Administrative Capital, maintained 60.05% of Egypt commercial real estate market share in 2025 thanks to its governmental, financial, and consumer density. The Forbes International Tower’s hydrogen-powered blueprint signals the city’s ambition to set regional sustainability benchmarks, helping prime offices secure pre-leases from ESG-driven multinationals. Retail remains robust: Cairo Festival City Mall reopened after a USD 566.7 million upgrade featuring Egypt’s inaugural IKEA and a new Carrefour hypermarket, reaffirming the capital’s dominance as an entry point for global brands.

Secondary cities are outpacing in growth. Alexandria leverages Hutchison Ports’ USD 700 million terminal expansion to attract trade-linked warehousing and distribution projects, pushing coastal logistics absorption to record highs. Giza, abutting both historical Cairo and the New Administrative Capital, offers cost-effective plots for light industrial estates servicing the enlarged metropolis. Enhanced transport linkages and land price arbitrage support its double-digit leasing momentum.

The Rest-of-Egypt corridor—spanning North Coast, Red Sea, and SCZone clusters—records an 11.20% CAGR through 2031 anchored by mega-projects. The USD 150 billion Ras El-Hekma city targets 8 million tourists yearly, fueling integrated hospitality, retail, and entertainment demand while doubling nearby land values. Talaat Moustafa Group’s USD 21 billion SouthMED development secured USD 1.25 billion bookings in 12 hours, demonstrating deep appetite for premium coastal assets. SCZone continues to draw industrial pipelines, with 274 projects worth USD 8.3 billion commissioned within 33 months, embedding a diversified economic base that widens the Egypt commercial real estate market’s geographic spread.

Competitive Landscape

Local champions such as Talaat Moustafa Group, Palm Hills, and SODIC retain scale advantages in land banking and regulatory navigation, yet cross-border capital inflows are reshaping bargaining dynamics. UAE-based Modon’s mandate to steer the Ras El-Hekma masterplan illustrates the rising prevalence of joint ventures blending domestic execution with foreign financing. Portfolio diversification around government mega-projects yields lower vacancy risk, and early mover positioning near the New Administrative Capital or SCZone generates quasi-captive demand corridors.

Technology and ESG differentiation mark the new battleground. The Infinity Tower’s LEED Platinum pursuit and the Iconic Tower’s ECOPlanet cement showcase how green credentials translate into rent premiums and brand equity. Proptech platforms offering digital leasing, tenant-experience apps, and energy-optimization analytics gain traction as landlords chase operational efficiency. Firms lacking upgrade capital could become acquisition targets, sparking consolidation that tightens supply of Grade-A space within the Egypt commercial real estate market.

Regulatory enforcement under Law 175 (2022) empowers the Egyptian Competition Authority to scrutinize mergers, maintaining a moderately fragmented field. Niche disruptors focusing on specialized logistics hubs, cold storage, or flexible office suites broaden product diversity, while alternative lenders bridge financing gaps left by risk-averse banks. This eclectic mix sustains competitive tension yet fosters innovation beneficial to occupiers across the Egypt commercial real estate industry[3]Egyptian Competition Authority, “Merger Control Law 175 (2022) Application,” eca.org.eg.

Egypt Commercial Real Estate Industry Leaders

Amer Group

Orascom Construction PLC

Palm Hills Developments

The Arab Contractors

Talaat Moustafa Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AD Ports Group and the Suez Canal Economic Zone signed a 50-year concession to design, build, and operate the 20 km² KEZAD East Port Said Zone as a fully integrated industrial-logistics hub. The partnership will oversee infrastructure, utilities, and tenant onboarding to transform Port Said into a premier transshipment and manufacturing gateway.

- May 2025: AD Ports committed USD 120 million for Phase 1, fast-tracking 2.8 km² of KEZAD East with quay upgrades, warehousing shells, and road links. The upfront spend accelerates SCZONE’s bid to rank among the world’s top trade corridors by 2030.

- March 2025: Modon Holding and Elsewedy Industrial Development agreed to co-develop a 10 million m² industrial city in Ras El-Hekma focused on cement, steel, and prefab plants. The project is expected to create 20,000 jobs and supply critical materials to North Coast mega-projects, adding a sizable lift to Egypt’s GDP.

- December 2024: Hilton announced plans to triple its Egypt footprint by adding 25 hotels, raising its pipeline to more than 40 properties nationwide. The expansion brings lifestyle flags Tapestry Collection and Curio Collection to the country and is projected to generate 5,000 hospitality jobs.

Egypt Commercial Real Estate Market Report Scope

Commercial real estate is a property that has the potential to generate profit through capital gain or rental income. Commercial real estate (CRE) is only used for business-related activities or to offer a workspace instead of being utilized as a residence, which would fall under the residential real estate category. Most frequently, renters lease commercial real estate to conduct businesses that generate cash.

Egypt's commercial real estate market is segmented by type (offices, retail, industrial and logistics, hospitality, and multi-family) and key cities (Cairo, Alexandria, Giza, Port Said, and the Rest of Egypt). The report offers market sizes and forecasts in value (USD) for all the above segments.

By Property Type

| Offices |

| Retail |

| Logistics |

| Others (industrial real estate, hospitality real estate, etc.) |

By Business Model

| Sales |

| Rental |

By End-user

| Individuals / Households |

| Corporates & SMEs |

| Others |

By Geography

| Cairo |

| Alexandria |

| Giza |

| Rest of Egypt |

| By Property Type | Offices |

| Retail | |

| Logistics | |

| Others (industrial real estate, hospitality real estate, etc.) | |

| By Business Model | Sales |

| Rental | |

| By End-user | Individuals / Households |

| Corporates & SMEs | |

| Others | |

| By Geography | Cairo |

| Alexandria | |

| Giza | |

| Rest of Egypt |

Key Questions Answered in the Report

What is the current value of the Egypt commercial real estate market?

The Egypt commercial real estate market size is USD 4.31 billion in 2026 and is forecast to reach USD 6.04 billion by 2031.

Which property type leads demand?

Offices account for 43.02% of 2025 market share thanks to ministry relocations and multinational expansions.

Which segment is growing fastest?

Retail assets are projected to post a 9.60% CAGR through 2031 on the back of tourism recovery and lifestyle mall rollouts.

How is inflation affecting the sector?

Double-digit inflation and a 28.25% policy rate raise financing and operating costs, yet hard-currency leases help cushion prime assets.

What role do mega-projects play?

Government initiatives such as the New Administrative Capital and SCZone create new commercial hubs, drawing private investment and diversifying geographic demand.

Page last updated on: