Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

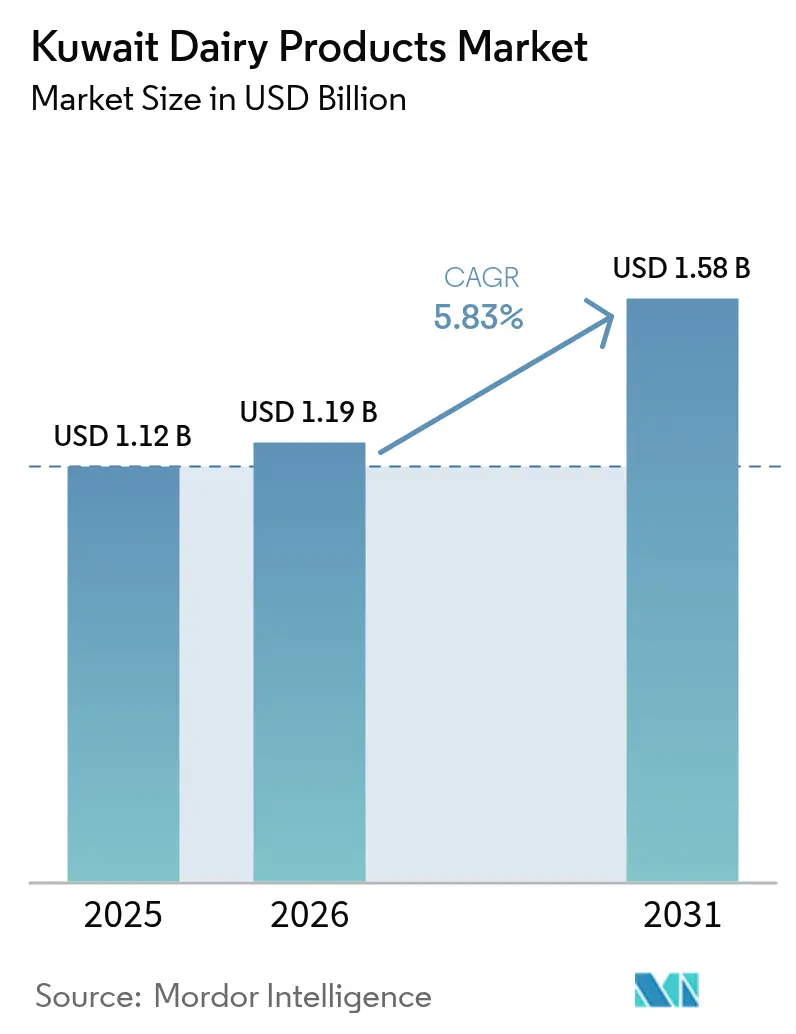

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

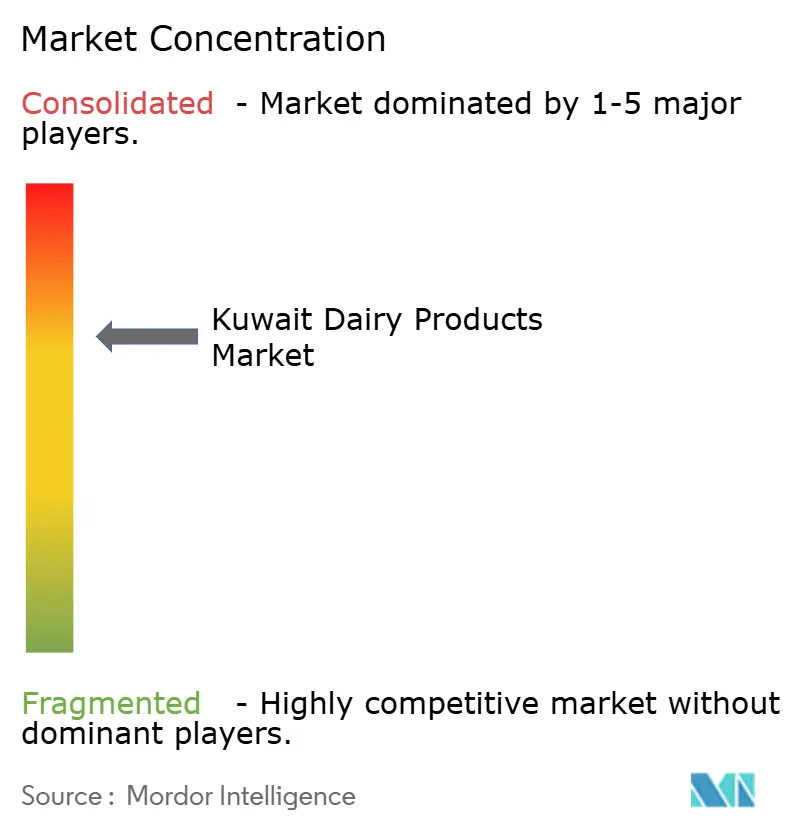

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kuwait Dairy Products Market Analysis by Mordor Intelligence

The Kuwait dairy products market size is expected to grow from USD 1.12 billion in 2025 to USD 1.19 billion in 2026 and is forecast to reach USD 1.58 billion by 2031 at 5.83% CAGR over 2026-2031. This solid growth is anchored in rising household incomes, population expansion, and policy-driven efforts to curb the country’s 88-89% import dependence. Strategic food-security investments, a front-of-pack traffic-light labeling mandate, and incentives for local herd expansion are reshaping supply-demand fundamentals. Simultaneously, technology upgrades in aseptic filling and lighter PET packaging are compressing logistics costs and extending shelf life, while camel-milk ventures introduce a functional-nutrition angle that differentiates Kuwait from neighboring GCC markets. Consolidation remains pronounced, with a handful of regional majors and two entrenched local producers accounting for most retail shelf space and food-service contracts.

Key Report Takeaways

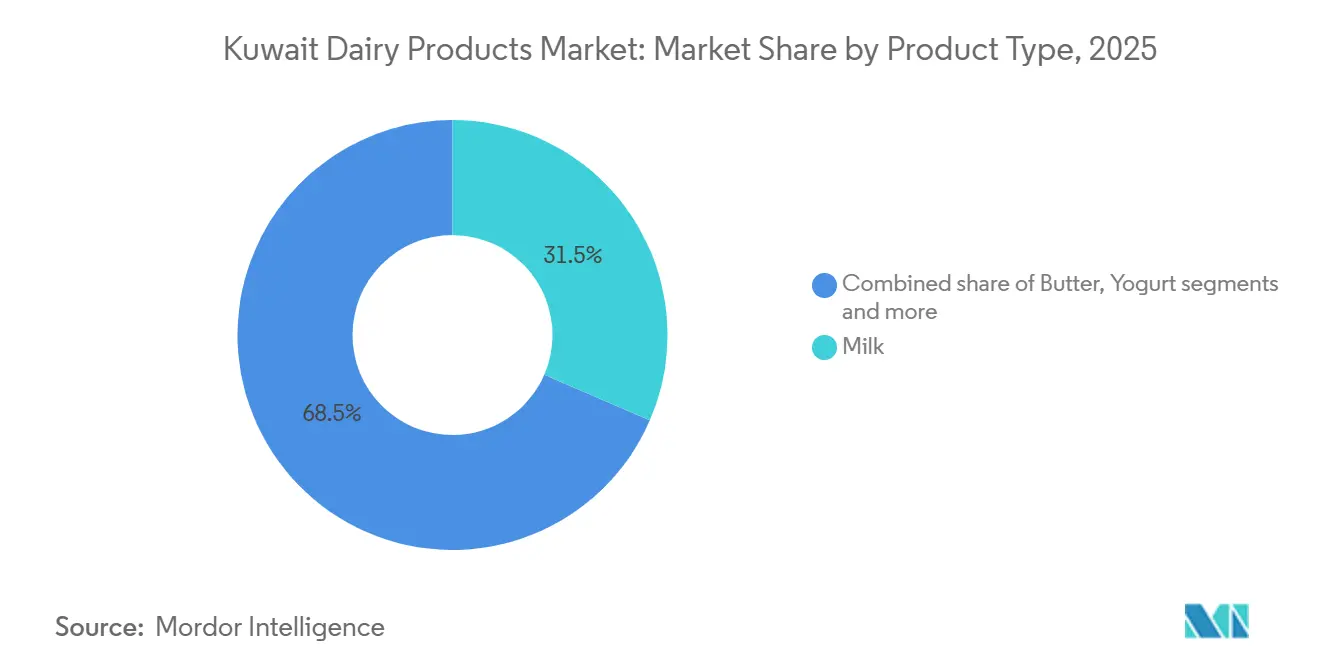

- By product type, milk commanded 31.49% of Kuwait dairy products market share in 2025, whereas yogurt is forecast to post a 6.14% CAGR through 2031, outperforming every other category.

- By source, cow milk represented 78.49% of the Kuwait dairy products market size in 2025; camel milk is set to expand at a 7.93% CAGR between 2026 and 2031.

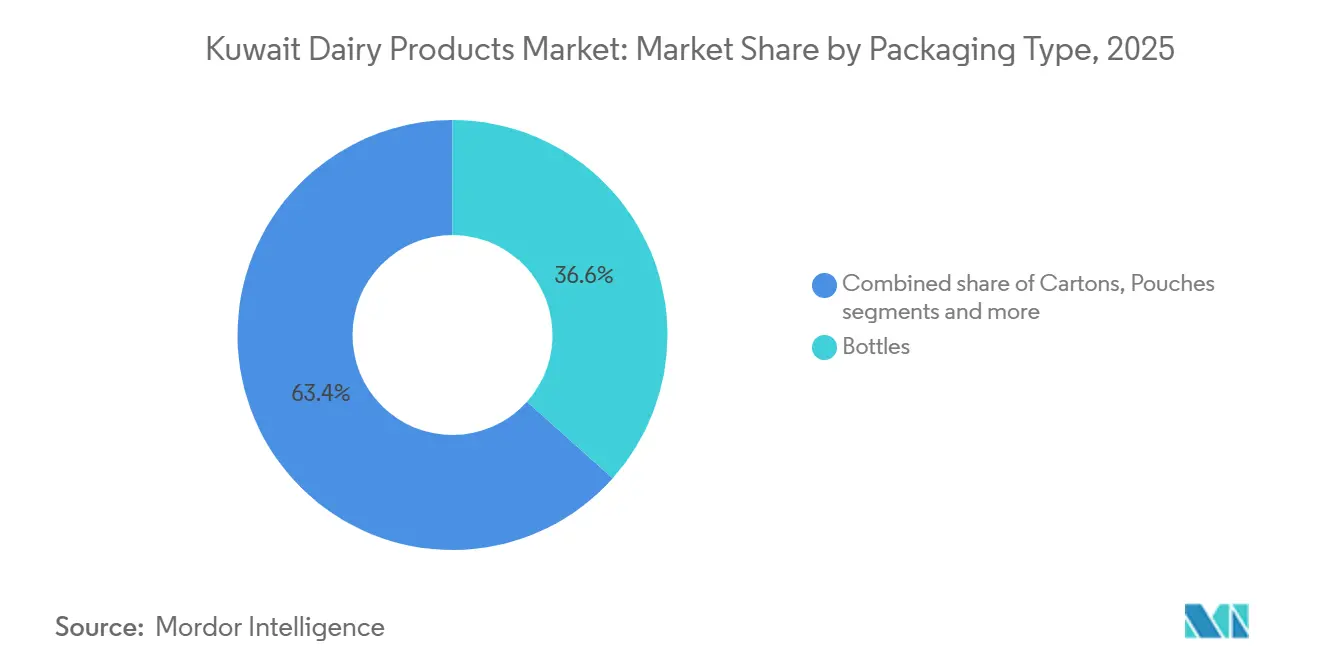

- By packaging, bottled formats held 36.61% of 2025 revenue, while tubs and cups are projected to grow fastest at a 6.94% CAGR to 2031.

- By distribution channel, off-trade dominated with a 94.81% share in 2025; nonetheless, on-trade is expected to advance at a 6.81% CAGR as hotel and restaurant demand rebounds.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Dairy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness increasing demand for nutritious and fortified dairy products | +1.2% | Kuwait national | Medium term (2-4 years) |

| Growing demand for organic, functional, and probiotic dairy products | +1.0% | Kuwait urban centers, expatriate segments | Medium term (2-4 years) |

| Increasing working population driving demand for convenient dairy products | +0.9% | Kuwait national, particularly Kuwait City metro | Short term (≤ 2 years) |

| Advancements in dairy processing and packaging improving shelf life | +0.7% | Kuwait national, GCC supply chain | Long term (≥ 4 years) |

| Growth of foodservice and hospitality sectors increasing dairy consumption | +0.6% | Kuwait City, coastal resort zones | Medium term (2-4 years) |

| Government regulations supporting food safety and product quality | +0.5% | Kuwait national | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness increasing demand for nutritious and fortified dairy products

In Kuwait, a surge in health consciousness is propelling the demand for nutritious and fortified dairy products. As consumers become increasingly aware of the pivotal role diet plays in overall health, they're gravitating towards dairy items enriched with essential vitamins, minerals, and probiotics. Health-conscious and younger demographics are particularly favoring products like fortified milk, low-fat yogurt, and functional dairy beverages. Concerns about immunity, bone health, and digestive wellness further bolster the appetite for these value-added dairy products. In response, manufacturers are rolling out offerings with enhanced calcium, vitamin D, and reduced sugar content, aligning closely with shifting consumer preferences. Moreover, a rise in fitness trends and a heightened awareness of preventive healthcare are fueling the regular consumption of these nutrient-rich dairy items. This collective shift towards healthier dietary choices is driving robust growth in Kuwait's dairy market.

Growing demand for organic, functional, and probiotic dairy products

The growing demand for organic, functional, and probiotic dairy products is emerging as a key driver of the Kuwait dairy products market, supported by increasing consumer focus on preventive health and nutrition. Consumers are increasingly seeking dairy products perceived as natural, minimally processed, and beneficial for digestive and overall health. Functional dairy items such as probiotic yogurt, fortified milk, and low-sugar dairy beverages are gaining traction among health-conscious consumers. In 2024, the International Diabetes Federation reported that 25.6% of adults in Kuwait are living with diabetes, which has further encouraged consumers to shift toward healthier and nutritionally balanced food choices[1]Source: International Diabetes Federation, "Diabetes in Kuwait (2024)", idf.org. This has led to rising demand for products with reduced sugar content and added health benefits. Dairy manufacturers are responding by expanding organic and functional product portfolios to meet evolving dietary preferences.

Advancements in dairy processing and packaging improving shelf life

Advancements in dairy processing and packaging technologies are significantly contributing to the growth of the Kuwait dairy products market by improving product quality and extending shelf life. Modern processing techniques such as ultra-high temperature (UHT) treatment and advanced pasteurization help maintain nutritional value while allowing longer storage periods. Improved packaging solutions, including aseptic packaging and resealable containers, enhance product safety and convenience for consumers. These innovations reduce product spoilage and support efficient distribution across retail channels, particularly in a market reliant on consistent cold chain management. Longer shelf life also enables manufacturers and retailers to optimize inventory management and reduce wastage. Additionally, convenient and portable packaging formats are aligning with evolving consumer preferences for on-the-go consumption.

Growth of foodservice and hospitality sectors increasing dairy consumption

The growth of the foodservice and hospitality sectors is significantly contributing to rising dairy consumption in Kuwait, driven by increasing demand from restaurants, hotels, cafés, and quick-service outlets. Dairy products such as milk, cheese, cream, butter, and yogurt are widely used in beverages, desserts, and prepared food offerings, supporting consistent demand from the foodservice industry. The expansion of café culture and specialty beverage outlets has further increased the use of dairy-based ingredients, particularly in coffee and dessert segments. Tourism growth is also strengthening this trend, as higher visitor inflows support increased dining-out activity. International inbound tourism expenditure in Kuwait reached USD 2,883.68 million in 2024, marking a 15.31% increase compared to USD 2,500.75 million in 2023, reflecting stronger hospitality sector performance[2]Source: Statbase, “International inbound tourism expenditure- Kuwait”, statbase.org . This rise in tourism-related spending continues to boost dairy usage across hotels and foodservice establishments. As the hospitality sector expands further, dairy consumption through commercial channels is expected to grow steadily.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and operational costs impacting profitability | -0.8% | Kuwait national, particularly domestic producers | Short term (≤ 2 years) |

| High dependency on imports increasing supply risks and price volatility | -0.7% | Kuwait national, GCC supply chain | Medium term (2-4 years) |

| Stringent regulatory requirements delaying product introductions | -0.4% | Kuwait national, import compliance | Medium term (2-4 years) |

| Supply chain and logistics challenges affecting availability | -0.5% | Kuwait national, Red Sea trade routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production and operational costs impacting profitability

High production and operational costs remain a key restraint for the Kuwait dairy products market, affecting profitability across the value chain. Dairy producers face rising expenses related to feed, energy, labor, transportation, and cold chain maintenance, all of which increase overall production costs. The country’s climatic conditions also require significant investment in cooling systems and advanced farm management practices, further adding to operational expenses. Dependence on imported raw materials and feed ingredients exposes manufacturers to global price fluctuations and supply chain uncertainties. These cost pressures often limit pricing flexibility, particularly in a competitive retail environment where consumers remain price sensitive. Smaller producers are especially vulnerable, as they may lack economies of scale to absorb rising costs. As a result, sustained increases in operational expenses continue to challenge profit margins and market expansion.

High dependency on imports increasing supply risks and price volatility

High dependency on imports remains a significant restraint for the Kuwait dairy products market, increasing exposure to supply disruptions and price volatility. Kuwait relies heavily on imported dairy products, raw materials, and feed ingredients due to limited domestic agricultural capacity and climatic constraints. Fluctuations in global dairy prices, transportation costs, and exchange rates can directly impact product pricing and availability in the local market. Supply chain disruptions caused by geopolitical tensions or logistical challenges further increase uncertainty for manufacturers and retailers. This reliance on imports also limits the ability of local producers to maintain stable production costs and long-term pricing strategies. Sudden increases in import costs may be passed on to consumers, affecting demand in price-sensitive segments. Consequently, import dependency continues to pose challenges to market stability and profitability within Kuwait’s dairy sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yogurt Innovation Outpaces Traditional Milk

Milk accounted for the largest share of the Kuwait dairy products market in 2025, representing 31.49% of total revenue, supported by its strong position as a staple product in daily consumption. The category benefits from consistent household demand, as milk is widely used across different age groups and dietary habits. High consumption frequency, combined with its use in beverages, cooking, and food preparation, continues to sustain stable sales volumes. The availability of various product formats, including fresh, long-life, flavored, and fortified milk, further supports category expansion. Additionally, strong distribution through supermarkets, convenience stores, and modern retail channels ensures widespread accessibility. Local dairy producers continue to invest in quality improvements and product innovation, reinforcing milk’s dominant position within the overall dairy market.

Yogurt is projected to be the fastest-growing segment in the Kuwait dairy products market, with an expected CAGR of 6.14% through 2031, outperforming other dairy categories. Growth in this segment is largely driven by increasing consumer awareness of digestive health and the perceived benefits of probiotic-rich products. Changing dietary preferences toward healthier and lighter food options are encouraging higher yogurt consumption among younger and health-conscious consumers. Manufacturers are expanding product offerings through flavored variants, low-fat options, and functional yogurt products to attract a broader consumer base. The rising popularity of convenient snack formats and on-the-go consumption is also contributing to demand growth.

By Source: Camel Milk Disrupts Cow-Dominated Market

Cow milk held the dominant position in the Kuwait dairy products market in 2025, accounting for 78.49% of the total market share. Its strong market presence is supported by widespread consumer familiarity, consistent availability, and established supply chains across the country. Cow milk remains a staple product in daily diets due to its affordability, nutritional value, and versatility in household consumption as well as foodservice applications. The availability of multiple product variants, including fresh, long-life, low-fat, and fortified options, further strengthens its market penetration. Local dairy companies continue to invest in processing efficiency and distribution expansion to maintain steady supply and competitive pricing.

Camel milk is projected to be the fastest-growing segment in the Kuwait dairy products market, expected to expand at a CAGR of 7.93% between 2026 and 2031. Increasing consumer interest in functional and specialty dairy products is driving demand for camel milk, which is often perceived as offering unique nutritional and health benefits. Growing awareness regarding lactose sensitivity and alternative dairy options is also encouraging consumers to explore camel milk products. Producers are increasingly introducing flavored and value-added camel milk offerings to attract a wider consumer base. Additionally, rising premiumization trends and cultural preference for traditional dairy sources in the region are supporting market growth.

By Packaging Type: Single-Serve Formats Gain Ground

By 2025, bottled packaging is set to command a substantial 36.61% share of the market. This stronghold is largely due to the convenience it provides consumers, coupled with a distribution infrastructure adeptly tailored for glass and plastic bottles. Bottled packaging is the go-to choice for liquid dairy products, including milk and flavored drinks, thanks to its durability, transport ease, and freshness preservation. Moreover, the ubiquitous presence of bottled products in retail channels bolsters its market stance. The segment is riding the wave of rising demand for ready-to-drink dairy beverages, perfectly aligning with Kuwait's fast-paced consumer lifestyle. Innovations in bottle designs, especially lightweight and eco-friendly variants, are further amplifying the allure of bottled packaging.

Conversely, the tubs and cups segment is on an upward trajectory, eyeing a robust CAGR of 6.94% in the coming years. This surge is a testament to shifting consumer inclinations towards portion-controlled packaging and a heightened appetite for premium yogurt offerings. Tubs and cups are the preferred choice for their convenience in single-serving sizes, catering to both the on-the-go consumer and health enthusiasts prioritizing portion control. The segment's ascent is bolstered by design and material innovations, amplifying both product appeal and functionality. This makes it a pivotal player in Kuwait's dairy products arena. Furthermore, the surging demand for flavored and probiotic yogurts, predominantly housed in tubs and cups, is propelling this segment's growth.

By Distribution Channel: Off-Trade Dominance Masks On-Trade Momentum

Off-trade channels accounted for the largest share of the Kuwait dairy products market in 2025, representing 94.81% of total sales. This dominance is primarily driven by strong consumer preference for purchasing dairy products through supermarkets, hypermarkets, convenience stores, and other retail outlets. The wide availability of dairy products, frequent promotional activities, and competitive pricing strategies in retail channels continue to support high sales volumes. Additionally, increasing household consumption and the convenience of bulk purchasing contribute to the strong performance of off-trade distribution. The expansion of modern retail infrastructure and improved cold chain logistics further enhance product accessibility and shelf availability.

On-trade channels are projected to be the fastest-growing distribution segment in the Kuwait dairy products market, expected to register a CAGR of 6.81% between 2026 and 2031. Growth in this segment is supported by the expansion of foodservice establishments, including restaurants, cafes, hotels, and quick-service outlets. Rising dining-out trends and increasing demand for dairy-based beverages and desserts are contributing to higher dairy usage within the foodservice sector. The recovery and growth of tourism and hospitality activities are also supporting increased consumption through on-trade channels. Additionally, menu innovation and the growing popularity of specialty coffee and dairy-based drinks are creating new opportunities for dairy suppliers.

Geography Analysis

The Kuwait dairy products market is primarily driven by high urban concentration and strong purchasing power, which support consistent demand for both staple and value-added dairy products. The country’s population is largely concentrated in urban areas such as Kuwait City and surrounding metropolitan regions, enabling efficient distribution through modern retail channels. Supermarkets and hypermarkets dominate dairy sales due to their extensive product assortment and strong cold chain infrastructure. Additionally, the presence of a large expatriate population contributes to diverse consumption patterns, increasing demand for a wide range of dairy products including milk, yogurt, cheese, and flavored dairy beverages. High per capita income levels further encourage the consumption of premium and imported dairy products. According to the World Bank, Kuwait's GDP per capita hit USD 32,717.7 in 2024[3]Source: World Bank, "Economic Indicators-GDP-Percapita", worldbank.org.

Regional demand within Kuwait is also influenced by lifestyle patterns and evolving consumer preferences toward convenience-oriented food products. Busy urban lifestyles and rising workforce participation have increased demand for ready-to-consume and on-the-go dairy products, particularly in densely populated residential and commercial areas. Modern retail expansion and the growing penetration of convenience stores are improving product accessibility across different regions. Furthermore, increasing awareness of health and nutrition is supporting demand for functional dairy products such as low-fat milk, probiotic yogurt, and fortified dairy items. Local dairy producers are strategically strengthening distribution networks to ensure product freshness and availability across the country.

The foodservice and hospitality sector also plays an important role in shaping geographical demand for dairy products, particularly in commercial hubs and high-traffic urban zones. Hotels, restaurants, cafes, and quick-service restaurants generate steady demand for dairy ingredients used in beverages, desserts, and prepared foods. Growth in café culture and specialty coffee outlets has increased the use of milk and cream-based products, especially in urban centers. Additionally, government initiatives supporting food security and local production have encouraged investments in domestic dairy processing facilities, reducing reliance on imports in certain categories. Distribution efficiency supported by well-developed logistics infrastructure allows dairy products to reach consumers quickly across the country.

Competitive Landscape

In Kuwait's dairy market, regional powerhouses compete fiercely for dominance, standing shoulder to shoulder with established locals and emerging niche players. The market remains consolidated, with a handful of key players sharing the leadership spotlight. Almarai, a regional behemoth, harnesses its vast scale and operational efficiencies to stay ahead. Meanwhile, local entities like Kuwait Dairy Company and Kuwait Danish Dairy leverage their deep-rooted understanding of the domestic landscape and robust distribution networks. This competitive tapestry mirrors broader trends in the GCC, where larger entities reap the benefits of economies of scale in processing and distribution, while local producers adeptly align with consumer preferences and navigate regulatory landscapes.

In Kuwait's dairy arena, competitive dynamics are increasingly shaped by strategic moves emphasizing vertical integration and stringent supply chain oversight. With Kuwait's heavy reliance on imports and the looming challenge of water scarcity curtailing local production expansion, companies are honing their supply chains for optimal efficiency and reliability. A pronounced focus on cold chain logistics underscores this commitment, ensuring the preservation of product quality and freshness, especially for perishables. The burgeoning e-commerce landscape further nudges companies to bolster their online visibility and delivery prowess, meeting the rising appetite for fresh food deliveries. Such strategies not only tackle logistical hurdles but also prime companies to seize burgeoning market prospects.

Moreover, firms are broadening their horizons by rolling out premium dairy products, aligning with shifting consumer tastes. These upscale offerings not only promise heftier profit margins amidst fluctuating input costs but also resonate with a global trend: consumers' readiness to invest more for superior, value-added products. This premiumization strategy not only carves out a distinct niche in a crowded marketplace but also cultivates brand loyalty and broadens the customer base. In essence, Kuwait's dairy market landscape is a delicate dance of harnessing scale advantages while deftly navigating local nuances, all in pursuit of sustained growth and resilience amidst challenges.

Kuwait Dairy Products Industry Leaders

-

Kuwait United Dairy Company

-

The Almarai Company

-

Al Safat Fresh Dairy Co.

-

Kuwait Danish Dairy Company

-

Kuwait Dairy Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kuwait Dairy Company launched a comprehensive brand revamp under new management. The refreshed identity features a modern logo, redesigned packaging, and a fresh tagline: "Home of Fresh Milk". This new slogan emphasizes KDCow’s commitment to quality, purity, and support for local farms. The updated packaging uses a color-coded system for easy product identification, with the signature KDCow blue taking center stage.

- July 2024: Puck introduced its first-ever limited-time flavor: Zaatar Cream Cheese. The company has designed these jars with a modern 450g packaging and made them available at select retailers across the Middle East, including in Kuwait.

- June 2024: Kuwait Danish Dairy Company launched a new ice cream line named “Good for Me”. This fresh offering contains no added sugar, making it a healthier choice compared to the company's classic ice creams. Shoppers can savor three enticing flavors: vanilla, strawberry, and chocolate.

Kuwait Dairy Products Market Report Scope

A dairy product is defined as milk and any foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk. The kuwait dairy products market is segmented by product type, source, packaging type and distribution channel. By product type, the market is segmented by milk, cheese, yogurt, butter, cream and other product types. By source, the market is segmented by cow milk, camel milk and goat and sheep milk. Based on packaging type, the market is segmented by bottles, cartons, pouches, tubs and cups and other packaging types. By distribution channel, the market is segmented into off-trade and on-trade channels. For each segment, the market sizing and forecasting have been done in value terms (USD) and volume terms (Tons).

By Product Type

| Milk |

| Cheese |

| Yogurt |

| Butter |

| Cream |

| Other Product Types |

By Source

| Cow Milk |

| Camel Milk |

| Goat and Sheep Milk |

By Packaging Type

| Bottles |

| Cartons |

| Pouches |

| Tubs and Cups |

| Other Packaging Types |

By Distribution Channel

| On-Trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience/ Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| By Product Type | Milk | |

| Cheese | ||

| Yogurt | ||

| Butter | ||

| Cream | ||

| Other Product Types | ||

| By Source | Cow Milk | |

| Camel Milk | ||

| Goat and Sheep Milk | ||

| By Packaging Type | Bottles | |

| Cartons | ||

| Pouches | ||

| Tubs and Cups | ||

| Other Packaging Types | ||

| By Distribution Channel | On-Trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience/ Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How large will the Kuwait dairy products market be by 2031?

The market is projected to reach USD 1.58 billion by 2031, expanding at a 5.83% CAGR from 2026.

Which product category is growing fastest?

Yogurt leads with a forecast 6.14% CAGR, driven by probiotic and high-protein innovations.

What share do on-trade channels hold today?

On-trade channels account for just over 5% of 2025 value but are the fastest-growing segment at 6.81% CAGR.

Why is camel milk gaining traction?

Clinical findings on glycemic control and official “Year of the Camel” branding are propelling a 7.93% CAGR for camel milk through 2031.

How are packaging innovations shaping growth?

Lightweight PET bottles and electron-beam sterilization extend shelf life and cut freight costs, supporting a shift toward single-serve formats.

Page last updated on: