Cluster Headache Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

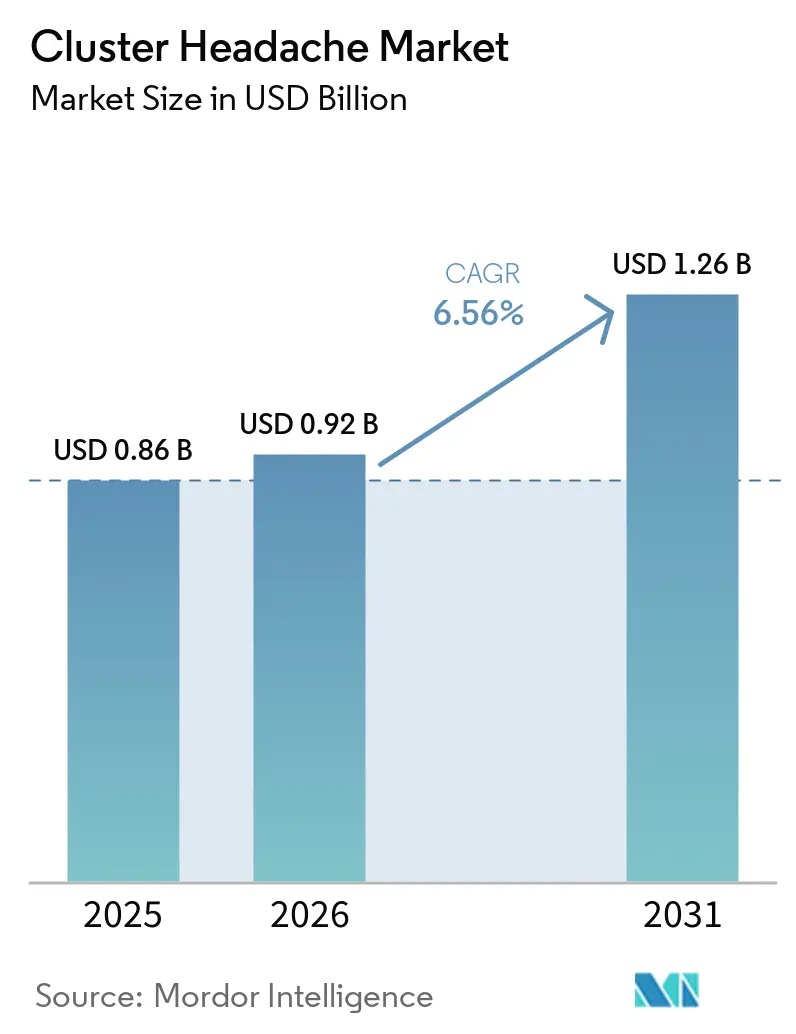

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

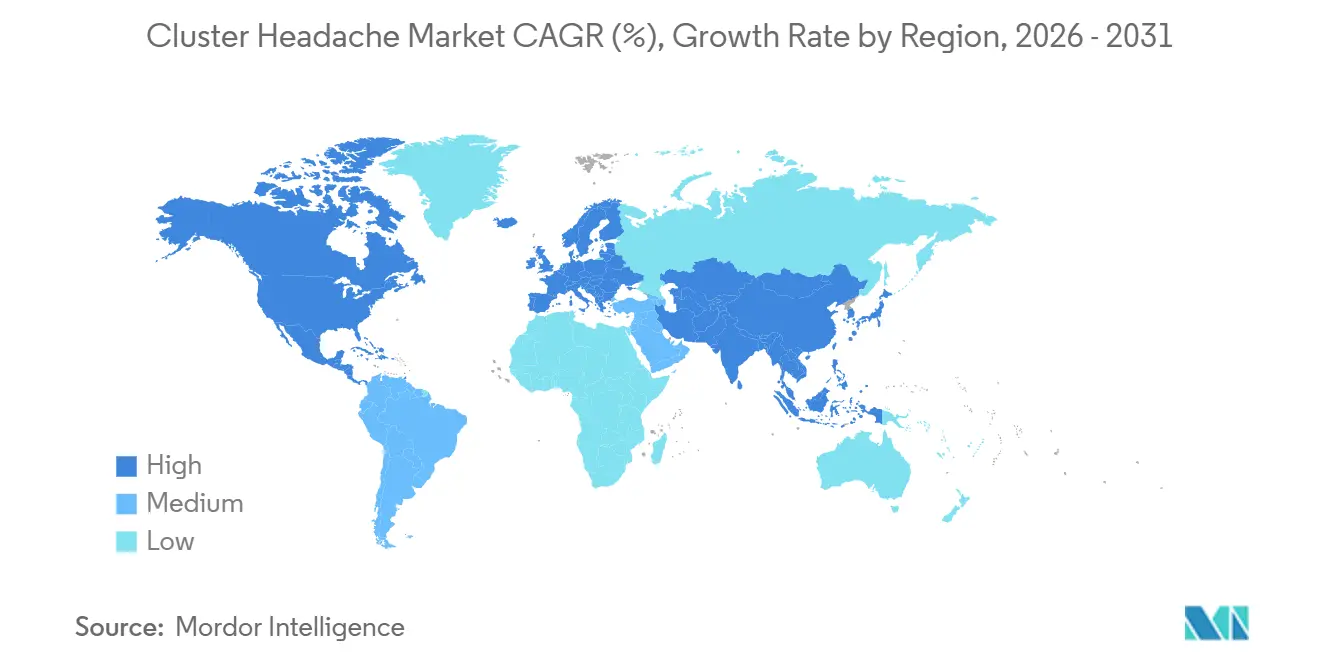

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

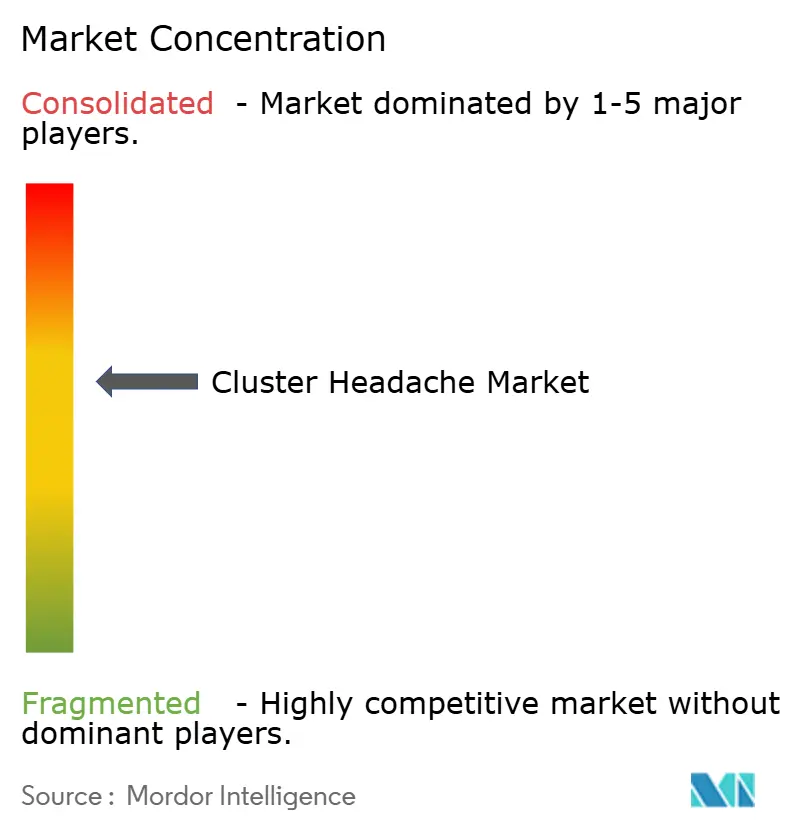

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cluster Headache Market Analysis by Mordor Intelligence

The Cluster Headache Market size is expected to increase from USD 0.86 billion in 2025 to USD 0.92 billion in 2026 and reach USD 1.26 billion by 2031, growing at a CAGR of 6.56% over 2026-2031.

The cluster headache market is witnessing growth driven by the increasing adoption of calcitonin gene-related peptide (CGRP) monoclonal antibodies, expanded reimbursement for home-use neuromodulation, and advancements in point-of-care biomarker tests, which are reducing diagnostic delays. While triptans and high-flow oxygen remain dominant in acute care, payer acceptance of biologics and vagus-nerve stimulators is expanding, particularly across North America and the European Union. Additionally, large-scale AI initiatives that integrate electronic health records with wearable biosensors are accelerating specialist referrals, addressing the average six-year delay between symptom onset and accurate diagnosis. Competitive rivalry remains moderate, as only one CGRP mAb, galcanezumab, holds a disease-specific indication, creating opportunities for implantable stimulators and gepants to differentiate based on safety and convenience.

Key Report Takeaways

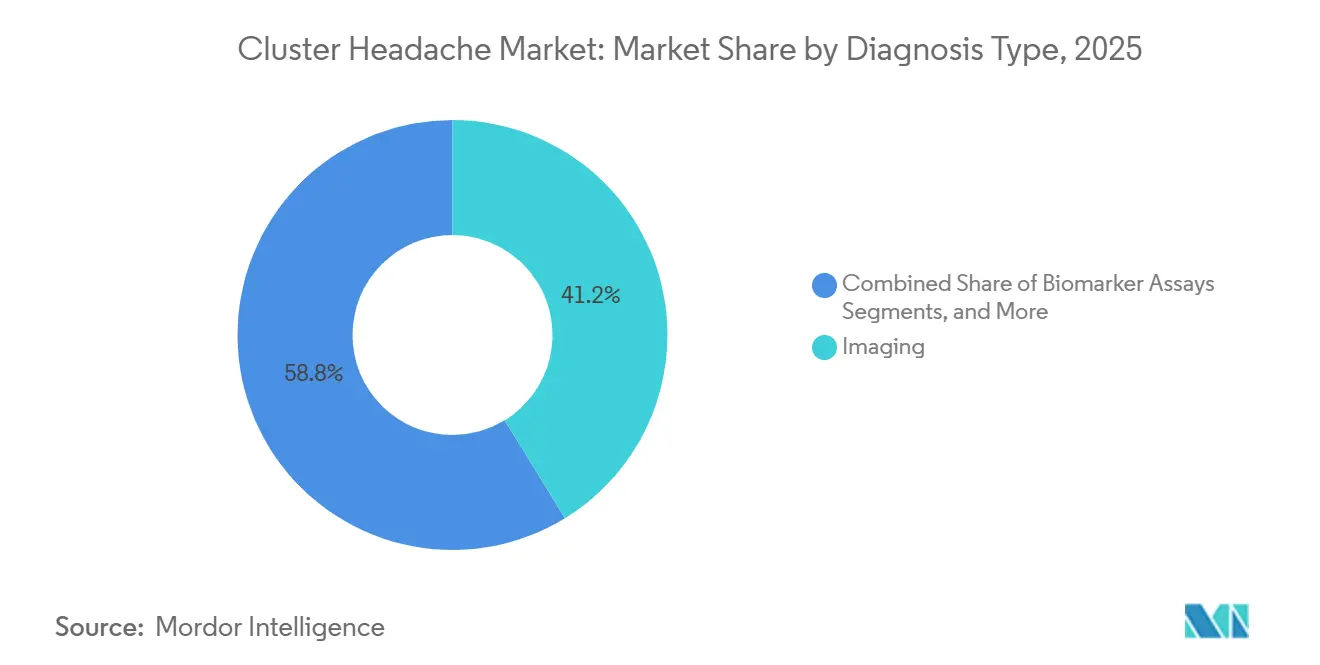

- By diagnosis type, imaging led with 41.23% of cluster headache market share in 2025, while biomarker assays are projected to grow at an 8.10% CAGR through 2031.

- By treatment type, acute care captured 65.44% revenue in 2025; preventive therapy is advancing at a 7.60% CAGR on the back of CGRP mAb adoption.

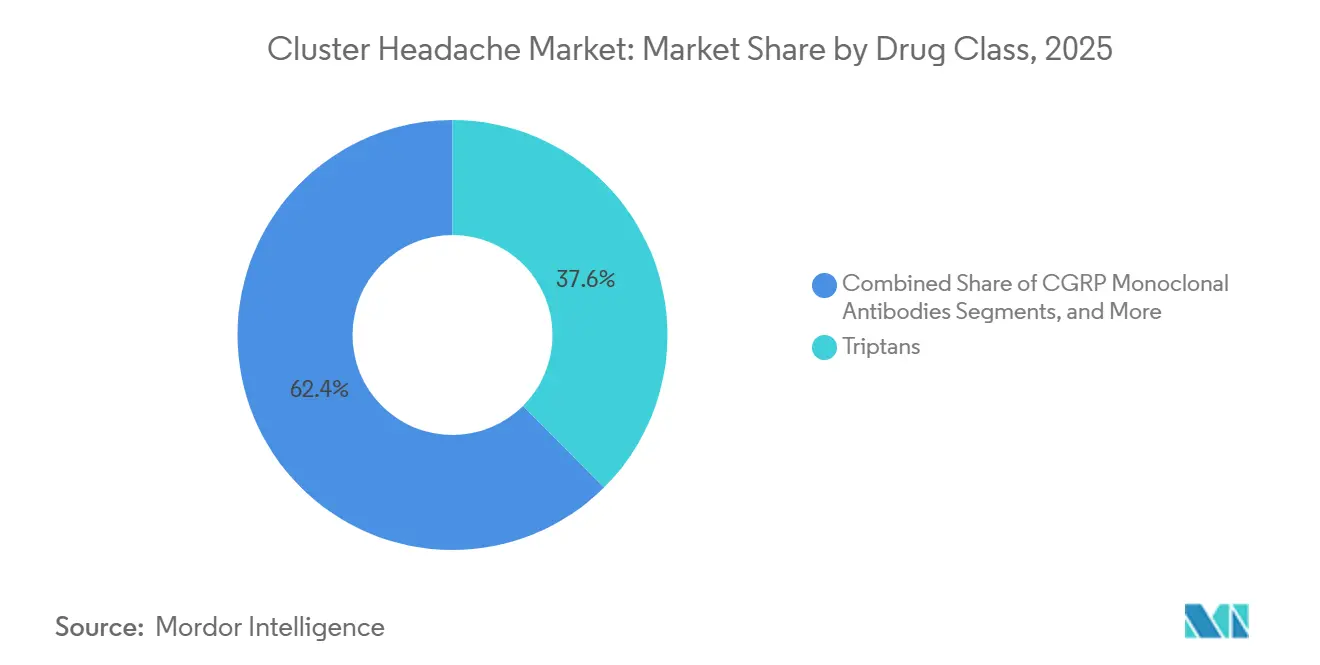

- By drug class, triptans held 37.56% of the cluster headache market size in 2025, yet CGRP mAbs are expanding at a 9.40% CAGR to 2031.

- By route, injectables commanded 41.54% in 2025, whereas neuromodulation devices are forecast to grow at 8.80% owing to home-use vagus-nerve stimulation.

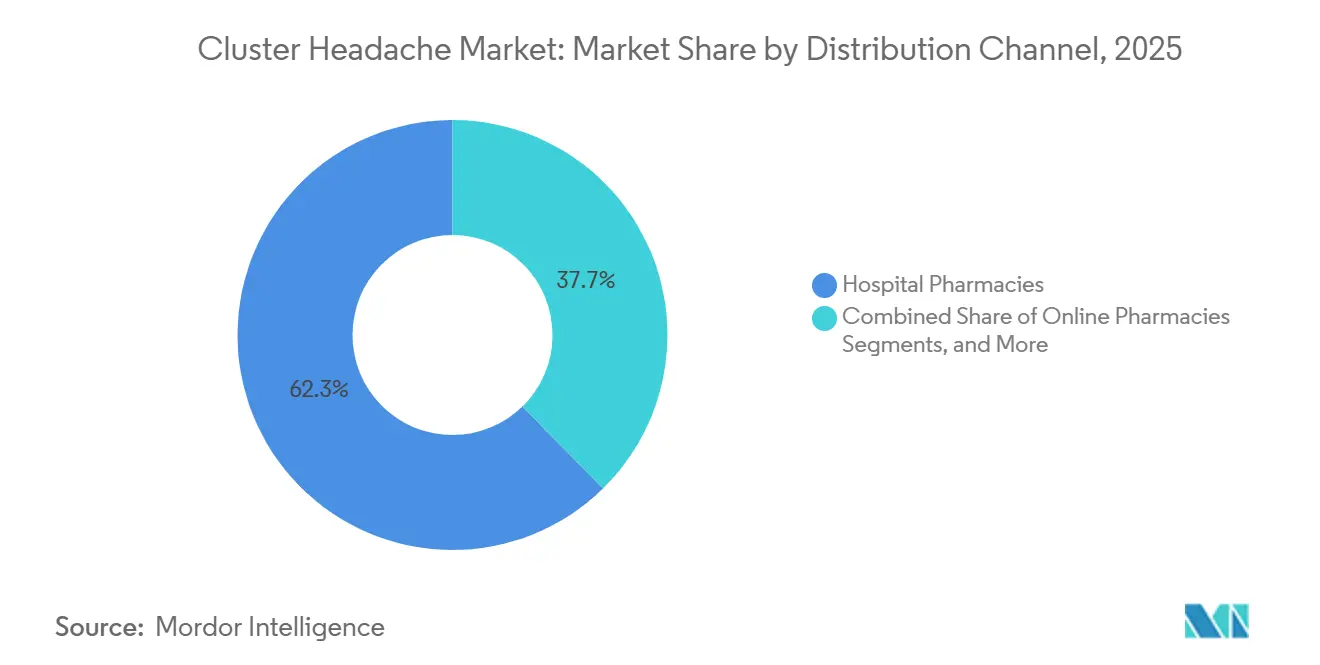

- By distribution channel, hospital pharmacies generated 62.34% revenue during 2025; online pharmacies are rising at a 7.55% CAGR as specialty drugs migrate to home delivery.

- By patient type, episodic disease delivered 78.67% of revenue in 2025, yet chronic cluster headache is growing 8.30% annually on the strength of orphan-drug programs.

- By geography, North America accounted for 42.67% revenue in 2025, while Asia-Pacific is projected to expand at an 8.50% CAGR to 2031 as regulatory harmonization improves access.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Cluster Headache Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Diagnosed Patient Population | 1.9% | North America & EU5, pilot programs in Japan & South Korea | Long term (≥ 4 years) |

| Expansion of targeted biologics & novel therapeutics | 1.8% | Global, with early adoption in North America & EU5 | Medium term (2-4 years) |

| Home-use non-invasive vagus nerve stimulation uptake | 1.2% | North America & EU5, expanding to APAC | Short term (≤ 2 years) |

| AI-powered wearable headache-diary analytics | 0.9% | North America & EU5, pilot programs in Japan & South Korea | Long term (≥ 4 years) |

| Orphan-drug reimbursements & rising healthcare spend | 1.1% | Global, with policy momentum in North America, EU5, and select APAC markets | Medium term (2-4 years) |

| CGRP Point-of-Care Biomarker Assays Accelerate Diagnosis | 1.2% | North America & EU5, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Targeted Biologics & Novel Therapeutics

Galcanezumab, the only CGRP monoclonal antibody approved for episodic cluster headaches, demonstrated a 71.4% responder rate by week 3 in pivotal studies. Organon expanded its commercialization efforts to 11 new markets in 2024 through a USD 22.5 million deal, reflecting payers' willingness to reimburse orphan indications.'[1]American Headache Society, “The Workforce Gap in Headache Medicine,” americanheadachesociety.org The 2025 ALLEVIATE trial for eptinezumab did not meet its primary endpoint but indicated potential delayed benefits, suggesting a shift by payers toward sustained-response benchmarks. Fremanezumab’s futility stop highlights the variability in biologics, reinforcing the importance of attack-frequency-based enrichment arms. A 2026 meta-analysis confirmed superior short-term efficacy in episodic diseases, guiding future trial designs toward subtype stratification.

Home-Use Non-Invasive Vagus Nerve Stimulation Uptake

GammaCore, after receiving U.S. clearance for acute use in 2017 and preventive use in 2018, was endorsed in 2019 for its cost-saving potential, with projected annual savings of GBP 450 (USD 570) per patient. The PREVA study demonstrated a reduction of 5.9 attacks per week compared to 2.1 with a sham, along with a 57% decrease in abortive medication usage. Salvia BioElectronics secured USD 60 million in 2025 to develop ultra-thin implants with AI-controlled stimulation, achieving Breakthrough Device status. Europe’s CLUSTERSENSE initiative is integrating biosensors with closed-loop stimulators to reduce time-to-relief to under five minutes.[2]The Journal of Headache and Pain, “Preventive therapy with galcanezumab for two consecutive cluster bouts,” thejournalofheadacheandpain.biomedcentral.comIn South Korea, reimbursement policies still require 12 months of failed oral prevention before coverage, delaying access to neuromodulation solutions.

AI-Powered Wearable Headache-Diary Analytics

The mBrain study identified physiological signatures from 35 chronic cluster attacks, enabling algorithms to differentiate them from migraines and paving the way for predictive alerts. Head.AI, utilizing a GPT-4o core, achieved 89.5% diagnostic accuracy based on ICHD-3 criteria, significantly reducing misclassification rates from 49% to 10.5%.[3]The American Journal of Managed Care, “The Current Landscape of CGRP Inhibitor Coverage,” ajmc.com A rapid 32-minute CGRP immunoassay with a 9 pg/mL detection limit enables same-visit confirmation of suspected attacks. Tear-fluid CGRP testing, offering non-invasive sampling and tolerance for processing delays, simplifies workflows in primary care. Norway’s MI-HEAD initiative is combining genetic markers with EHR data to predict verapamil response, signaling a shift toward precision prevention strategies.

Orphan-Drug Reimbursements & Rising Healthcare Spend

Headache disorders impose an economic burden of over USD 78 billion annually in the U.S., emphasizing the need for early intervention in cluster headaches. The 2025 HEADACHE Act aims to allocate federal funding for telehealth, training, and registries to address diagnostic delays in rural areas. Lobe Sciences raised USD 6 million in 2025 under orphan-drug regulations to develop its psilocin analog L-130, targeting a seven-year exclusivity period for chronic conditions. In Europe, high-flow oxygen is reimbursed in 12 countries, covering 63% of the population, though inconsistent access to injectable triptans drives some patients toward less effective intranasal alternatives. A specialist density of 0.21 per 100,000 population shows limited correlation with the adoption of novel agents, indicating that marketing strategies continue to influence prescribing patterns.

Restraints Impact Analysis of Cluster Headache Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of headache specialists & diagnostic delays | -0.8% | Global, acute in North America, rural APAC, and MEA | Medium term (2-4 years) |

| Cardiovascular safety flags for long-acting CGRP Mabs | -0.6% | Global, with heightened scrutiny in the EU5 and Japan | Short term (≤ 2 years) |

| High therapy cost burden on payers & patients | -0.7% | Global, acute in North America | High term (3-5 years) |

| Limited neuromodulation reimbursement outside NA/EU5 | -0.5% | Global, rural APAC, and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Headache Specialists & Diagnostic Delays

With only 564 board-certified headache specialists available, the U.S. faces a significant shortfall compared to the required 3,700 to 4,500. This shortage results in average wait times of 30 days for adults and delays of up to six months for pediatric patients. Misdiagnosis affects nearly half of the patients, extending their care pathway by six years and increasing emergency department visits. Rural Americans, facing longer travel distances, often journey 70 to 81 miles for specialist consultations, exacerbating existing socioeconomic disparities. While the HEADACHE Act aims to enhance telehealth funding, inconsistent reimbursement policies across states limit its adoption. Expanding the workforce alone may not be sufficient to drive CGRP mAb adoption without concurrent payer reforms and continuous education initiatives.

Cardiovascular Safety Flags for Long-Acting CGRP mAbs

A 2025 review identified blood-pressure spikes associated with erenumab, prompting regulatory warnings about hypertension and Raynaud’s phenomenon for all drugs in this class. Galcanezumab's updated labeling in 2025 highlighted the potential for hypertension onset within a week of injection, leading to stricter prior-authorization requirements. While pooled analyses indicated no significant increase in major adverse cardiovascular events, real-world variations have heightened payer caution, particularly in markets like Japan and South Korea, where two-year surveillance is mandatory. New payer policies, such as requiring a full-year trial of oral preventives followed by a six-month washout before approving CGRP mAbs, are slowing their adoption in commercial plans. These developments are shifting prescriber preferences toward neuromodulation and reversible gepants, which offer shorter systemic exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cluster Headache Market Segment Analysis

By Diagnosis Type:

Biomarker Assays Compress the Diagnostic OdysseyIn 2025, imaging captured 41.23% of the cluster headache market, driven by the widespread use of MRI and CT scans to eliminate secondary causes. Biomarker assays, supported by ultra-rapid CGRP tests delivering results in just 32 minutes, are expected to grow at an annual rate of 8.10% through 2031, significantly reducing diagnostic delays. While clinical evaluations based on ICHD-3 criteria remain the primary diagnostic method, a 49% misdiagnosis rate highlights the critical need for objective biomarkers. Tear-fluid assays demonstrate resilience against preanalytical degradation, while genetic panels remain confined to research due to low penetrance and limited therapeutic applications.

By Treatment Type:

Preventive Therapy Gains as CGRP mAbs MatureIn 2025, acute treatments, led by oxygen and subcutaneous sumatriptan, accounted for 65.44% of the revenue. Preventive therapies are projected to grow at a 7.60% CAGR through 2031, as CGRP mAbs shift the clinical approach toward long-term attack suppression. Corticosteroid bridges and occipital nerve blocks serve as transitional solutions but lack the scale of acute and preventive segments. GammaCore's dual functionality in both acute and preventive treatment is driving interest in hybrid therapeutic strategies.

By Drug Class:

CGRP mAbs Outpace Legacy Agents Despite Safety ScrutinyIn 2025, triptans, supported by the rapid 15-minute onset of subcutaneous sumatriptan, represented 37.56% of the cluster headache market. CGRP mAbs are projected to expand at a growth rate of 9.40% through 2031, supported by increasing payer coverage following multi-region agreements. Verapamil remains the first-line oral preventive treatment, but adherence is hindered by the need for dose-dependent cardiac monitoring. Lithium and ergot derivatives continue to play niche roles due to safety and monitoring requirements, creating opportunities for biologics and gepants to gain market share.

By Route of Administration:

Neuromodulation Devices Redefine DeliveryIn 2025, injectables accounted for 41.54% of the revenue, while home-use stimulators are forecast to grow at 8.80%, driven by cost savings and patient preference for needle-free options. Oral formulations dominate chronic prevention but face adherence challenges due to the need for electrocardiogram and serum-level monitoring. Inhaled oxygen remains the first-line treatment for acute care but faces supply challenges in remote areas, where concentrator shortages persist.

By Distribution Channel:

Online Pharmacies Extend ReachIn 2025, hospital pharmacies generated 62.34% of sales, as many attacks begin in emergency settings where injectable triptans and oxygen are readily available. Online platforms are growing at an annual rate of 7.55%, integrating teleconsultations with specialty-drug deliveries, effectively addressing access challenges in rural areas. Retail outlets manage the majority of oral preventives but face obstacles related to prior authorizations and lab-test logistics. Academic specialty clinics provide multidisciplinary care but are predominantly located in urban areas.

By Patient Type:

Chronic Disease Draws Orphan-Drug CapitalEpisodic cases, supported by therapies such as galcanezumab and GammaCore, accounted for 78.67% of revenue in 2025. Chronic cluster headaches are growing at an annual rate of 8.30%, attracting investment as companies leverage orphan drug incentives and real-world data demonstrating durable responses. Phase 2 studies on rimegepant and psilocin analogs are targeting chronic populations underserved by current biologics, signaling potential market shifts once efficacy is established.

Geography Analysis

North America Cluster Headache Market

North America's cluster headache market benefits from extensive Medicare and commercial coverage for treatments such as galcanezumab and gammaCore. This advantage is further supported by a well-established network of specialists in metropolitan areas. However, rural regions continue to face significant challenges in accessing care. The implementation of the HEADACHE Act could allocate funding to telehealth initiatives, aiming to address these geographic disparities and improve access to treatment. Additionally, the United States is actively fostering innovation, as evidenced by the numerous investigator-initiated trials focusing on gepants. These developments highlight the region's commitment to advancing treatment options and addressing unmet needs in the market.

Europe Cluster Headache Market

In Europe, the market is driven by harmonized clinical guidelines and a strong emphasis on cost-effectiveness. The endorsement of vagus-nerve stimulation by regulatory bodies has influenced reimbursement policies across key markets, including Germany, France, and Nordic countries. Moreover, Europe is positioning itself as a leader in advanced medical technologies, with initiatives such as the development of AI-enabled closed-loop neuromodulation systems. These advancements are expected to enhance treatment outcomes, improve patient care, and drive the adoption of innovative solutions across the region.

APAC Cluster Headache Market

The Asia-Pacific region is undergoing a transition from fragmented regulatory frameworks to unified standards under ASEAN and ICH guidelines. While South Korea's step-edit policies present barriers to the immediate adoption of biologics, Japan's stringent two-year post-marketing surveillance process generates robust safety data, fostering greater confidence in the long-term use of these treatments. In China, although CGRP monoclonal antibodies are not yet included in the National Reimbursement Drug List, pilot programs in select cities are exploring innovative value-based contracting models. These initiatives could pave the way for broader adoption and integration of advanced therapies, driving growth and improving patient outcomes in the region.

Competitive Landscape

The cluster headache market demonstrates a moderate level of concentration. Galcanezumab and gammaCore dominate the biologic and device segments, respectively, while verapamil and triptans continue to serve as foundational treatments in traditional pharmacotherapy. In 2024, Organon expanded the geographic footprint of galcanezumab by adding 11 new territories, reflecting a deliberate strategy to enhance market presence. Salvia BioElectronics is advancing next-generation implantable devices by integrating AI-driven pain recognition technology. The company has successfully raised USD 60 million to support pivotal clinical trials, which are expected to conclude by 2027.

Challenges faced by Lundbeck with eptinezumab highlight the significant clinical risks inherent in this market. Similar setbacks have driven companies to adopt more targeted approaches, such as subtype-specific enrichment strategies, to improve outcomes. Lobe Sciences is focusing on the development of psychedelic analogs for the treatment of chronic diseases, aiming to secure seven-year market exclusivity through orphan drug designation. Meanwhile, the Mayo Clinic is conducting studies on rimegepant for both episodic and chronic cluster headaches, positioning it as a potential oral treatment option with rapid dose adjustability.

Innovators in artificial intelligence, including companies like Head.AI and Empatica, are entering into data-licensing partnerships with device manufacturers to create integrated, closed-loop ecosystems. These collaborations are expected to shift competitive dynamics by prioritizing data-driven personalization and long-term patient adherence. This trend is likely to raise entry barriers for traditional market players that lack advanced digital capabilities, further intensifying competition within the sector.

Cluster Headache Industry Leaders

Eli Lilly & Company

Amgen Inc.

Teva Pharmaceutical

electroCore Inc.

Lundbeck A/S

- *Disclaimer: Major Players sorted in no particular order

Cluster Headache Market Companies Covered in this Report

- Abbvie

- Amgen

- AstraZeneca

- Cipla

- Dr. Reddy’s Laboratories

- electroCore, Inc.

- Eli Lilly and Company

- Endo International

- GE HealthCare Technologies Inc.

- Hikma Pharmaceuticals

- Impel NeuroPharma, Inc.

- Johnson & Johnson

- Koninklijke Philips

- Lundbeck A/S

- Magstim Company Ltd.

- Nevro

- Novartis

- Otsuka

- Pfizer

- Salvia BioElectronics B.V.

- Satsuma Pharmaceuticals, Inc.

- Siemens Healthineers

- Teva Pharmaceutical Industries

- UCB

- Upsher-Smith Laboratories

- WraSer Pharmaceuticals, LLC

Recent Industry Developments in Cluster Headache Market

- January 2026: Karolinska Institutet received SEK 1.1 million (USD 0.11 million) for a three-year project mapping heredity, sex, sleep, and circadian rhythms in cluster headache patients.

- May 2025: United States: The FDA cleared Brekiya, the first DHE autoinjector, for acute treatment of migraine and cluster headaches, enabling at-home administration of hospital-grade therapy.

- May 2025: Lundbeck published ALLEVIATE results showing eptinezumab failed its week-1–2 endpoint but hit week-3 responder targets, reshaping payer efficacy criteria.

- February 2025: Lobe Sciences raised USD 6 million to advance psilocin analog L-130 through orphan-drug designation for chronic cluster headache.

Global Cluster Headache Market Report Scope

As per the scope of the report, cluster headaches are rare, extremely severe, one-sided head pains, often called "suicide headaches," characterized by burning, sharp pain (often around one eye) lasting 15 minutes to 3 hours, with daily, intense, 1-3 hour cycles. Diagnosis relies on clinical history of attacks (often involving restlessness) and neurological exams, while treatments focus on rapid abortion with 100% oxygen or triptans and prevention via verapamil.

The cluster headache market is segmented by diagnosis type, treatment type, drug class, route of administration, distribution channel, patient type, and geography. By diagnosis type, the market includes clinical assessment, imaging (MRI and CT), biomarker assays, wearable neuro-physiological monitoring, and genetic testing. By treatment type, the market is segmented into acute treatment, preventive treatment, and transitional therapy. By drug class, the market is categorized into triptans, CGRP monoclonal antibodies, ergot alkaloids, calcium-channel blockers (e.g., verapamil), and lithium carbonate & miscellaneous. By route of administration, the market is segmented into oral, injectable, intranasal, inhalation (medical oxygen), and neuromodulation devices. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, specialty clinics, and home healthcare providers. By patient type, the market is categorized into episodic cluster headache and chronic cluster headache. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

Segmentation Overview

| Clinical Assessment | |

| Imaging | MRI |

| CT | |

| Biomarker Assays | |

| Wearable Neuro-physiological Monitoring | |

| Genetic Testing |

| Acute Treatment |

| Preventive Treatment |

| Transitional Therapy |

| Triptans |

| CGRP Monoclonal Antibodies |

| Ergot Alkaloids |

| Calcium-Channel Blockers (Verapamil) |

| Lithium Carbonate & Miscellaneous |

| Oral |

| Injectable |

| Intranasal |

| Inhalation (Medical Oxygen) |

| Neuromodulation Device |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Clinics |

| Home Healthcare Providers |

| Episodic Cluster Headache |

| Chronic Cluster Headache |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnosis Type | Clinical Assessment | |

| Imaging | MRI | |

| CT | ||

| Biomarker Assays | ||

| Wearable Neuro-physiological Monitoring | ||

| Genetic Testing | ||

| By Treatment Type | Acute Treatment | |

| Preventive Treatment | ||

| Transitional Therapy | ||

| By Drug Class | Triptans | |

| CGRP Monoclonal Antibodies | ||

| Ergot Alkaloids | ||

| Calcium-Channel Blockers (Verapamil) | ||

| Lithium Carbonate & Miscellaneous | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Intranasal | ||

| Inhalation (Medical Oxygen) | ||

| Neuromodulation Device | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Specialty Clinics | ||

| Home Healthcare Providers | ||

| By Patient Type | Episodic Cluster Headache | |

| Chronic Cluster Headache | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cluster headache market in 2031?

The cluster headache market is forecast to reach USD 1.26 billion by 2031, reflecting a 6.56% CAGR from 2026 to 2031.

Which segment is growing fastest within current treatment options?

Preventive therapy is expanding at a 7.60% CAGR thanks to broader reimbursement for CGRP monoclonal antibodies.

How large is imagings share of the cluster headache market?

Imaging contributed 41.23% of cluster headache market share in 2025, making it the largest diagnostic modality.

Which region will see the quickest growth to 2031?

Asia-Pacific is projected to grow at an 8.50% CAGR as regulatory harmonization speeds approvals and specialist training improves diagnosis.

Why are neuromodulation devices gaining traction?

Home-use vagus nerve stimulators such as gammaCore deliver acute and preventive benefits without systemic drug exposure, and NICE estimates annual savings of USD 570 per patient.

What impedes faster biologic uptake worldwide?

Cardiovascular safety flags for long-acting CGRP mAbs have triggered stricter prior-authorization rules, extending time to therapy initiation.

Page last updated on: