Clearing Houses And Settlements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

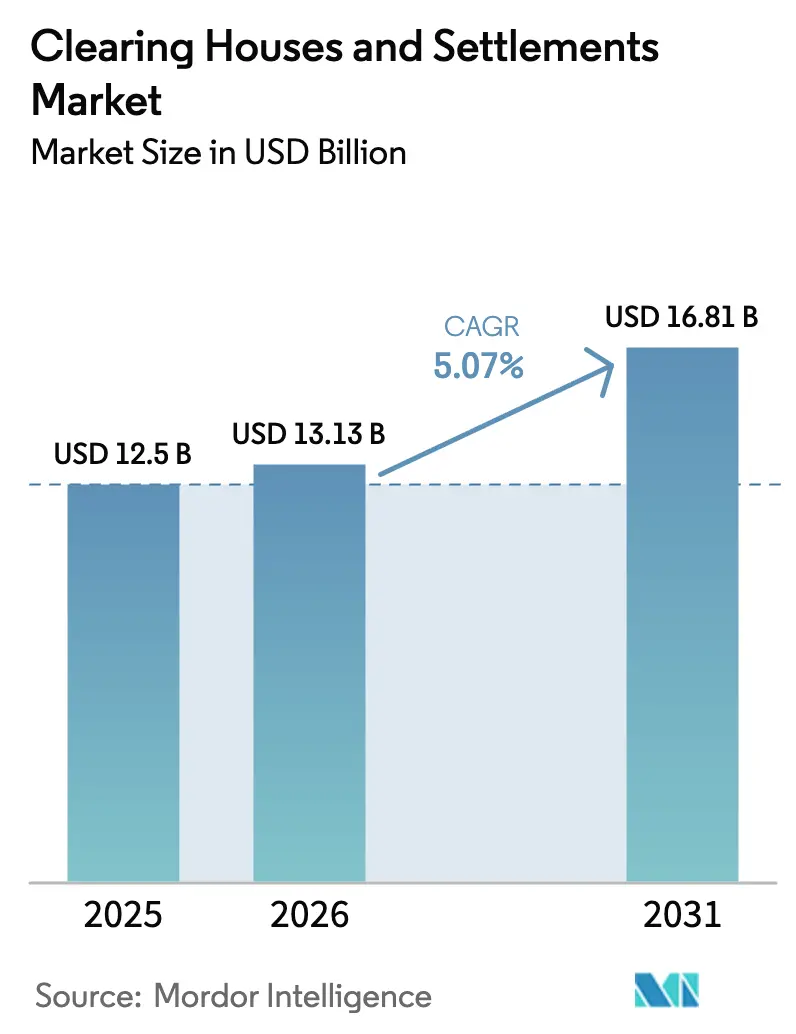

| Market Size (2026) | USD 13.13 Billion |

| Market Size (2031) | USD 16.81 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

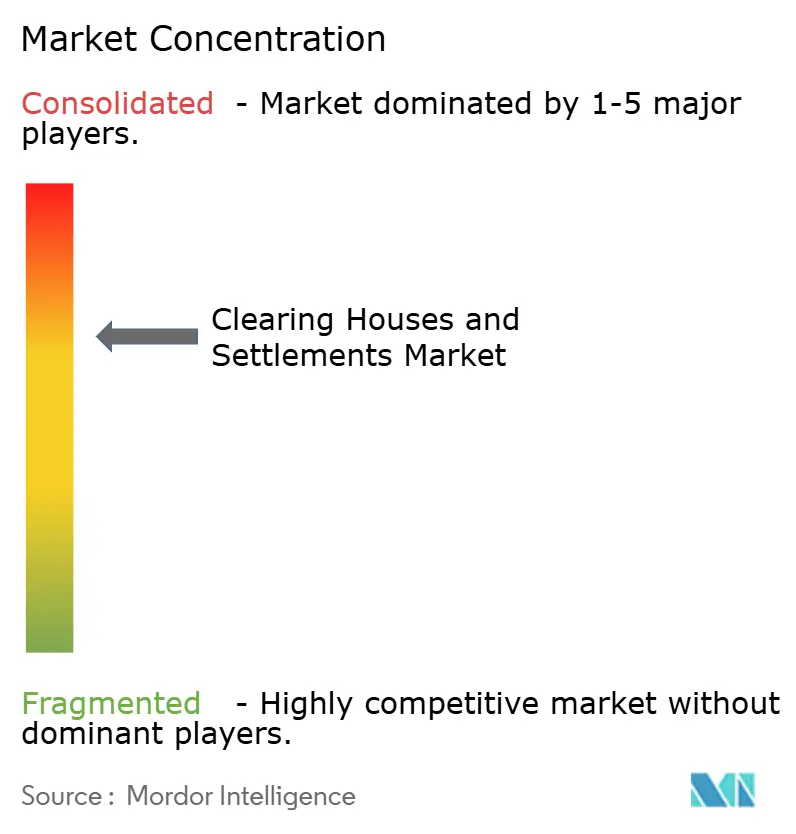

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clearing Houses And Settlements Market Analysis by Mordor Intelligence

The Clearing Houses And Settlements Market size is expected to grow from USD 12.5 billion in 2025 to USD 13.13 billion in 2026 and is forecast to reach USD 16.81 billion by 2031 at 5.07% CAGR over 2026-2031.

Electronic trading and high-frequency activity continue to increase throughput requirements and tighten operating tolerances across post-trade routes in 2026, with European TARGET Services reporting a significant rise in volumes in 2024 that has cascaded into capacity upgrades and resiliency programs in the current period. Outward clearing houses consolidate their lead by absorbing more cross-border flows through multilateral netting. They are poised to benefit from United States Treasury central clearing deadlines that mobilize large daily cash and repo volumes into central counterparties. TARGET2 remains the anchor of large-value euro payments while TIPS accelerates instant settlement adoption, setting the standard for real-time processing at scale in 2026. Regional dynamics show North America holding the largest 2025 share while Europe leads in growth as ISO 20022 and instant payments converge under the Eurosystem’s consolidated platforms.

Key Report Takeaways

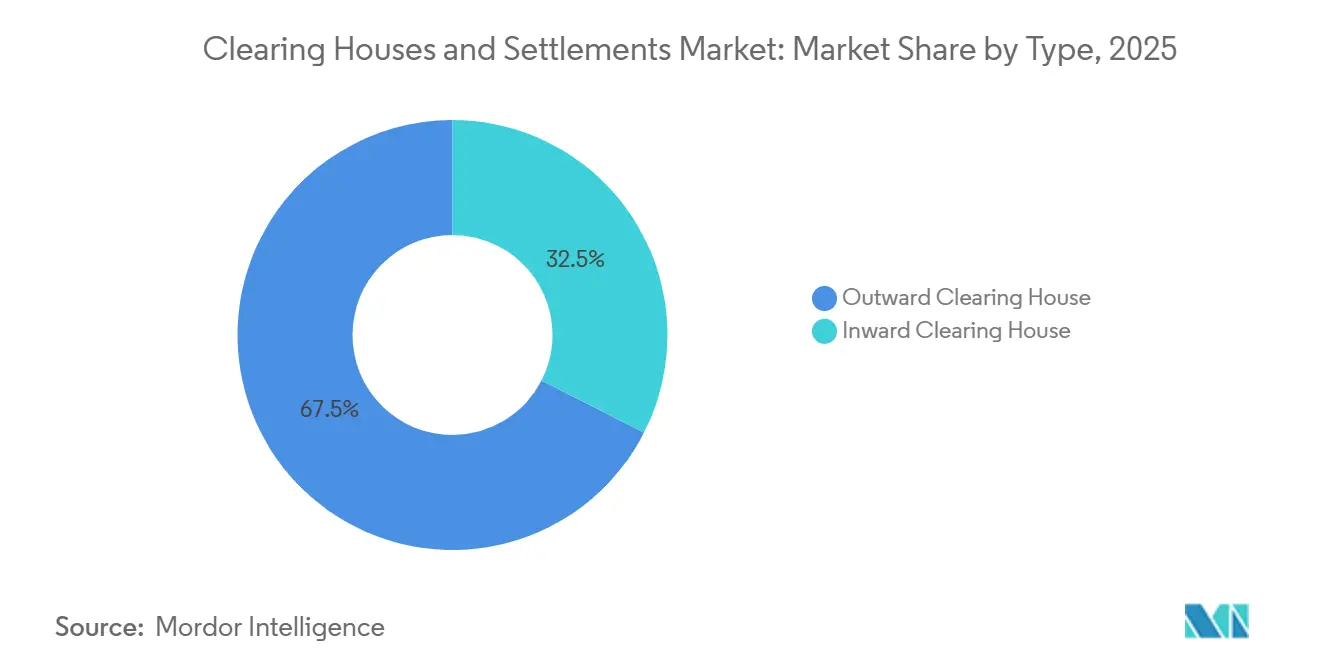

- By type, outward clearing houses led with 67.50% revenue share of the clearing houses and settlements market in 2025 and are the fastest growing at a 5.82% CAGR through 2031.

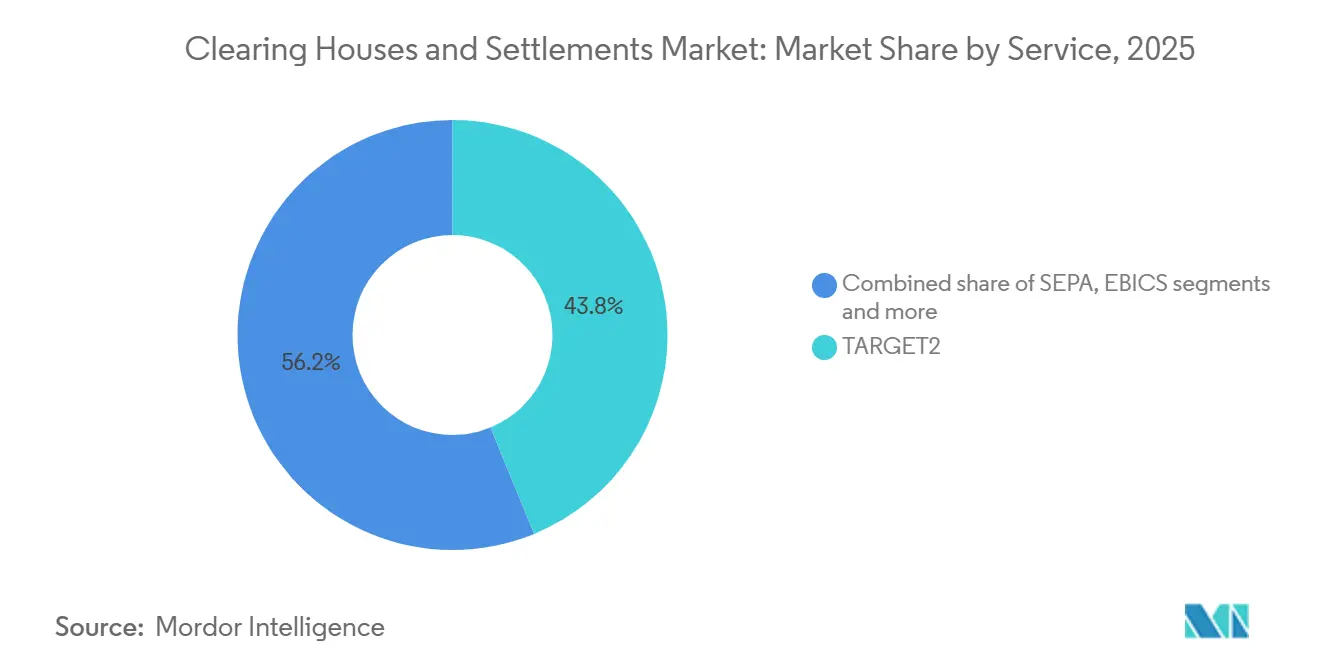

- By service, TARGET2 held a 43.80% share of the clearing houses and settlements market in 2025 and is advancing at a 7.43% CAGR to 2031.

- By geography, North America accounted for a 34.65% share of the clearing houses and settlements market size in 2025, while Europe recorded the highest projected CAGR at 6.65% through 2031.

- A small group of leading clearing members handles most client activity in United States CCPs, but the global concentration of clearing houses and settlements market remains limited due to the presence of regional infrastructures and new entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clearing Houses And Settlements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global trading activity, with rising electronic and high-volume transactions increasing demand for efficient clearing and settlement infrastructure | +1.2% | Global | Medium term (2-4 years) |

| Regulatory emphasis on central clearing, driven by post-financial-crisis reforms aimed at reducing systemic risk and enhancing market transparency | +1.5% | North America and the EU | Long term (≥ 4 years) |

| Advancements in clearing technologies, including AI, blockchain, and automation, are improving processing speed, accuracy, and operational efficiency | +0.9% | Global | Short term (≤ 2 years) |

| Increase in cross-border and derivatives trading, requiring interoperable, resilient clearing systems across jurisdictions | +1.1% | Global, early gains in APAC and EU | Medium term (2-4 years) |

| Heightened focus on counterparty risk management, as market volatility accelerates the adoption of centralized clearing mechanisms | +0.8% | Global | Short term (≤ 2 years) |

| Expansion of electronic and high-frequency trading platforms is driving the need for scalable, high-capacity settlement solutions | +0.7% | North America and APAC core | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Global Trading Activity Driving Clearing Infrastructure Demand

Electronic channels and algorithmic trading amplify daily volumes, pushing clearing operators to scale capacity or risk bottlenecks, with TARGET Services processing over 1.66 billion transactions in 2024 amid a 201.8% volume surge. TARGET2-Securities settles 202.6 million securities transactions valued at USD 292.7 trillion (EUR 248.9 trillion) in 2024, reinforcing the shift toward centralized platforms for harmonized cross-border settlement[1]https://www.ecb.europa.eu/press/targetservar/html/ecb.targetservar2024.en.html. . The U.S. Treasury clearing mandate channels up to USD 4 trillion in daily transactions toward central clearing by mid-2027, with aggregate margins at a key U.S. CCP reaching USD 96.3 billion by June 30, 2025. Japan Securities Clearing Corporation sets record interest-rate swap clearing in 2024, signaling the depth of rate hedging flows consolidating at central counterparties. South Korea’s KRX reports strong growth in derivatives activity and OTC clearing balances above USD 2 trillion, indicating the capacity shift that comes with electronic trading intensity. The instant payment expansion continues as the FedNow Service reports 2.5 million quarterly transactions worth USD 307.3 billion in Q3 2025, showcasing the real-time settlement trajectory[2]https://www.frbservices.org/resources/financial-services/fednow/quarterly-volume-value-stats.

Regulatory Emphasis on Central Clearing Reduces Systemic Risk

United States rules finalized in 2023 extend central clearing to cash Treasury and repo transactions with compliance dates on December 31, 2026, and June 30, 2027, which elevates transparency and aggregate margining discipline. Only 37% of dealer repo was centrally cleared as of Q4 2024, leaving USD 2.4 trillion in bilateral activity exposed to settlement frictions that clearing aims to address. EMIR REFIT lifts reporting granularity to 204 fields, while United States bank interest-rate derivatives show higher central clearing penetration at 48.1% notional by Q1 2025 from 32.5% in Q4 2024, underscoring regulatory impact on standardization. European CDS markets reached high clearing penetration by 2023, which aligns with the broader post-crisis emphasis on standardized products entering CCPs under EMIR oversight. India’s corporate bond settlement through exchange-linked clearing grows yet remains shallow relative to developed markets, highlighting room for standardization and deeper post-trade adoption. Convergence under CPMI-IOSCO PFMI and the EU’s cyber risk frameworks sustains harmonized expectations for resilience and data integrity that increasingly guide global FMI operations.

Advancements in Clearing Technologies Enhance Operational Efficiency

Tokenization trials, AI-based risk models, and automation reshape processing quality and timelines as jurisdictions test wholesale DLT integration and improve throughput through real-time decisioning. The Eurosystem ran 27 trials across nine countries and settled USD 1.88 billion (EUR 1.6 billion) in tokenized wholesale transactions, reinforcing the feasibility of interoperable DLT architectures for production-grade settlement. Clearstream validated a two-hour recovery with real-time data mirroring across geographically separated data centers, demonstrating how synchronized redundancy supports critical operations. EBA CLEARING’s RT1 scales to millions of instant payments daily with sustained low rejection rates and peak-hour throughput above 1,000 transactions per second, reflecting robust API-led scaling. Brazil’s PIX expands to 156 million individuals and 15.2 million organizations by late 2024, handling 6.4 billion transactions monthly through standardized APIs that interconnect banks and wallets[3]https://www.bcb.gov.br/en/financialstability/spi_en. Collateral mobility evolves as LME Clear accepts high-quality assets, including gold and eligible sovereign debt, which reduces funding friction across margin calls.

Increase in Cross-border and Derivatives Trading Requires Interoperable Clearing

Global cross-border payment value exceeds USD 190 trillion in 2024, yet one-quarter of corridors still impose costs above 3%, which accelerates demand for standardized messaging, interoperability, and netting efficiency in 2026[4]https://www.bancaditalia.it/pubblicazioni/interventi-governatore/integov2025/20251209-panetta/index.html. The Eurosystem’s instant settlement via TIPS grows 402.2% to 1.35 billion transactions in 2024, which validates the real-time model for retail and corporate flows that span borders within the region. APAC clearing depth rises as Japan’s JSCC advances swap clearing and South Korea’s OTC clearing balances exceed USD 2 trillion, reflecting derivative product growth and hedging intensity. Hong Kong’s OTC Clear clears USD interest-rate swaps at a faster clip in H1 2025, while the CCASS platform maintains high settlement efficiency for cash equities. As ISO 20022 and consolidated platforms harmonize operations, European infrastructure exhibits scalable cross-border capability that underpins liquidity and reduces reconciliation overhead. The clearing houses and settlements market increasingly depend on multi-rail compatibility with RTGS, instant, and securities platforms to sustain cross-border velocity without raising operational risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High collateral and capital requirements, raising operational costs, and limiting participation by smaller market players | -0.9% | Global, acute in EMDEs | Medium term (2-4 years) |

| Rising regulatory and compliance complexity, with evolving global standards increasing implementation and monitoring burdens | -0.7% | North America and the EU | Long term (≥ 4 years) |

| Escalating cybersecurity risks necessitate continuous investment in secure infrastructure for high-value transaction systems | -0.6% | Global | Short term (≤ 2 years) |

| Dependence on legacy clearing infrastructure constrains scalability and slows integration with next-generation technologies | -0.5% | North America and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Collateral and Capital Requirements Constrain Market Entry

Aggregate clearing fund requirements for United States government securities rise to USD 96.3 billion by June 30, 2025, with increases distributed across members in line with risk profiles, which raises barriers to entry for smaller firms. Minimum default fund contributions and net capital thresholds, such as those at LME Clear, restrict direct clearing participation to well-capitalized institutions that can supply eligible collateral. Adjustments in collateral eligibility and percentages at regional CCPs, including Saudi Arabia’s Muqassa, provide flexibility yet do not fully offset USD liquidity constraints across smaller participants. Large projected margin increases related to Treasury clearing timelines push smaller broker-dealers toward sponsored access arrangements that dilute economics and control. OTC positions in India’s corporate bond space remain outside centralized clearing in significant size, which sustains bilateral risk and diffusion of liquidity. The clearing houses and settlements market, therefore, sees a widening divide between large participants with diverse eligible collateral and smaller firms managing constrained capital stacks.

Rising Regulatory and Compliance Complexity Increases Implementation Burdens

The EU’s DORA regime in force in 2025, mandates near real-time incident reporting, periodic threat-led penetration tests, and oversight of critical third-party ICT providers, which requires governance and staffing changes across clearing operators. EMIR REFIT expands derivatives reporting to 204 fields while early rejection rates improve only after extensive recalibration, which underscores the learning curve for multi-jurisdictional reporting. Persistently elevated data-quality issues around outstanding trades and valuations limit supervisory visibility and increase the cost of reconciliation for market participants. Australia’s CHESS batch settlement incident in December 2024 resulted in operational risk downgrades that forced a comprehensive uplift of governance and contingency frameworks. ISO 20022 migrations by central banks and RTGS operators demand software changes and retraining that consume project resources ahead of regional deadlines. The clearing houses and settlements market must maintain parallel compliance processes for local cyber reporting and international standards, escalating administrative overhead for cross-border operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Outward Clearing Houses Propel Risk Mitigation and Netting Efficiencies

Outward clearing houses held a 67.50% share in 2025 and are projected to grow at a 5.82% CAGR through 2031, supported by multilateral netting that compresses gross obligations and reduces funding stress across borders. Liquidity benefits carry into day-to-day operations because outward platforms settle large-value payments and wholesale transactions while pooling exposures across jurisdictions for efficient offset. EURO1 settled 45.77 million payments worth USD 53.4 trillion (EUR 45.4 trillion) in 2024 and operates as a complementary multilateral net system that ultimately settles final balances in TARGET2, which optimizes participant liquidity profiles. Mandated U.S. Treasury central clearing positions outward venues to receive USD 4 trillion in daily activity by 2027, which will further institutionalize netting and margin efficiency at scale.

Inward clearing houses focus on domestic payment, and securities flows with risk models suited to national market structures, which aligns with lower collateral needs and simpler operational expectations. India’s exchange-linked clearing for corporate bonds processes sizable trade counts, although the dominance of private placements outside centralized venues limits penetration for inward routes. Hong Kong’s CCASS shows how disciplined netting can materially relieve liquidity even in domestic environments, with stock and funds netting ratios above 98% and 88%, respectively, in late 2025. As outward venues add features like AI-enhanced risk analytics and DLT pilots, inward models gradually adapt to interoperable standards to maintain continuity of settlement and collateral processes. With regulatory frameworks incentivizing centralized risk and consistent margining, outward platforms remain the primary channel for cross-border risk aggregation within the clearing houses and settlements market.

By Service: TARGET2 Dominates Large-Value Payments While TIPS Accelerates Instant Settlement Adoption

TARGET2 accounted for 43.80% of service-type share in 2025 and is forecast to expand at 7.43% annually through 2031, confirming its anchor role across euro large-value payment flows. It processed 108 million transactions worth EUR 463.7 trillion in 2024, while T2S handled 202.6 million securities transactions valued at EUR 248.9 trillion, reinforcing harmonized post-trade flows across the currency union. TIPS volume surged 402.2% to 1.35 billion transactions in 2024 and has been extended to new currencies across the Nordics, shaping the real-time standard for both retail and commercial use. The clearing houses and settlements market gains from this modular stack, which allows participants to coordinate liquidity across RTGS and instant payment rails with consistent messaging and service expectations.

SEPA instruments and supporting infrastructures round out euro retail payments, with STEP2 SCT posting higher volumes and SDD maintaining double-digit billions of transactions in 2024. RT1 instant payments surpassed 1.1 billion in 2024 with strong growth into 2025, which aligns with the Instant Payments Regulation that enforces reachability deadlines for euro institutions. EURO1 complements TARGET2 through multilateral netting with final settlement conducted in T2, which refines liquidity stewardship for major banks. National activity within the TARGET ecosystem, such as Portugal’s cross-border flows and T2 volume, shows how the consolidated European post-trade stack supports both domestic and pan-European operations. Verification of Payee features extends to RT1 and STEP2, adding fraud prevention to instant and batch channels without sacrificing speed. As a result, TARGET2 and its companion services continue to anchor the clearing houses and settlements market across the region’s high-value and instant segments.

Geography Analysis

North America held 34.65% of the clearing houses and settlements market in 2025, supported by the breadth of Federal Reserve services and the scale of U.S. Treasury transactions. The National Settlement Service processed USD 28.3 trillion in 2024 with average daily settlements of USD 112.6 billion, which reinforces the region’s foundation for large-value and net settlement workflows. FedNow adds real-time capability with 2.5 million transactions totaling USD 307.3 billion in Q3 2025, reflecting fast integration by institutions across the country. Centrally cleared derivatives notional rose in Q1 2025, fueled by interest-rate hedging, which supports wider CCP adoption across U.S. banks. The SEC’s Treasury clearing timelines intensify competition among approved and prospective CCPs as the pathway for USD 4 trillion in daily activity shifts toward central clearing. Canada’s and Mexico’s infrastructures extend the region’s footprint with established real-time and batch systems, including Mexico’s SPEI and adjunct payment identifiers that fuel digital usage.

Europe delivers the fastest growth at a 6.65% CAGR through 2031, underpinned by the convergence of TARGET Services, ISO 20022 harmonization, and the Instant Payments Regulation. Clearstream drives high settlement efficiency under T2S with day-end delivery-versus-payment performance near completion, and auto-collateralization supports resilient funding in peak periods. LCH and ICE Clear Europe operate as Tier 2 CCPs under ESMA, which consolidates supervisory alignment across OTC rate, credit, and listed derivatives in the region. France’s central bank participates in cross-border tokenization initiatives under central bank coordination, which points to future interoperability of clearing and settlement for wholesale transactions. National case studies such as Portugal’s T2 activity confirm the breadth of adoption across member states in the consolidated Eurosystem stack. As DORA takes effect, incumbents with scaled cyber programs gain an advantage in compliance and readiness.

Asia-Pacific shows heterogeneous maturity, from Japan’s record swap clearing at JSCC to rapid OTC growth in South Korea and strong instant-payment penetration in markets like India. Hong Kong’s CCASS posts 99.89% T+2 efficiency while OTC Clear’s derivative volumes rise sharply in H1 2025, which reflects both equity and derivatives system strength. India’s corporate bond market retains liquidity challenges in secondary trading despite expanding issuance, which highlights continued reliance on bilateral channels and room for clearing adoption. Australia clears high volumes in OTC derivatives and cash equities, though post-incident oversight has tightened expectations and remediation across ASX systems. Singapore’s FX turnover above SGD 1.5 trillion per day strengthens regional liquidity and supports collateral optimization via advanced execution and risk tools. In South America, Brazil’s PIX leads adoption with billions of monthly transactions and broad participation by households and firms, catalyzing cashless growth. Chile’s RTGS and card usage metrics show a clear shift toward digital flows with high per-capita payment usage. Africa and the Middle East see strong activity in the GCC and South Africa, with the UAE’s platform transitions and South Africa’s turnover growth pointing to resilient infrastructures.

Mordor Intelligence provides coverage of the clearing houses and settlements market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The clearing houses and settlements market presents moderate consolidation with five Title VIII-designated financial market utilities in the United States providing central clearing across cash and derivatives, including CME, FICC, NSCC, ICE Clear Credit, and OCC. FICC historically monopolized U.S. Treasury cash and repo clearing, though new approval for CME Securities Clearing introduces competition for the flow that will become subject to mandatory central clearing. Prospective entrants continue to position for participation ahead of the 2026 and 2027 compliance dates, which could increase innovation and fee competition. Concentration risk remains a supervisory focus because the top ten clearing members process more than 80% of client transactions at United States venues, which amplifies correlated exposures during stress.

Europe’s clearing and depository infrastructure centers on LCH Limited and ICE Clear Europe as Tier 2 CCPs under ESMA, with Euroclear and Clearstream as dominant CSDs and SIX entities serving Swiss and pan-European needs. EBA CLEARING’s EURO1, STEP2, and RT1 processed 22.62 billion transactions worth USD 83.8 trillion (EUR 71.3 trillion) in 2024, with RT1 instant payments up 32% to 1.107 billion, a proxy for the region’s rapid adoption of instant settlement. In APAC, JSCC doubled its yen interest-rate swap clearing year over year in 2024, while Hong Kong’s OTC Clear expanded USD IRS clearing and opened new collateral channels, including China Government Bonds.

Strategic moves in 2025 include CME’s regulatory approval to clear cash Treasuries and repo in the United States, which challenges an incumbent monopoly and signals a multi-CCP environment for the world’s deepest government bond market. LCH’s introduction of ZARONIA-based swaps broadens emerging currency coverage and shows how CCPs extend product scope to capture new hedging needs. HKEX’s expansion of eligible collateral for OTC Clear deepens linkages with onshore China and reduces collateral fragmentation across client portfolios. Compliance and resilience expectations under PFMI, DORA, and U.S. cyber standards continue to shape investment priorities across operations, technology, and third-party oversight.

Clearing Houses And Settlements Industry Leaders

Depository Trust & Clearing Corporation (DTCC)

Euroclear Group

LCH Limited (London Stock Exchange Group / LSEG)

Clearstream (Deutsche Börse Group)

CME Clearing (CME Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: CME Securities Clearing, Inc. received approval from the Securities and Exchange Commission to clear cash Treasury securities and repurchase agreements, ending the Fixed Income Clearing Corporation's monopoly and introducing competition to reduce fees and drive innovation in the USD 6 trillion daily U.S. Treasury market.

- September 2024: LCH introduces clearing for Overnight Index Swaps benchmarked to the South African Rand Overnight Index Average, becoming the first central counterparty to offer this capability and expanding emerging market currency coverage.

- June 2025: Following the CHESS batch settlement failure disruption of securities clearing for thousands. The Australian Securities and Investments Commission and the Reserve Bank of Australia initiated an inquiry into ASX Limited, examining its governance, capabilities, and risk management frameworks.

- March 2025: Hong Kong’s OTC Clear begins accepting China Government Bonds and Policy Bank Bonds held through Bond Connect as margin collateral for all derivative transactions, deepening onshore-offshore integration.

Global Clearing Houses And Settlements Market Report Scope

A clearing house is an intermediary between buyers and sellers of financial instruments. It is an agency or separate corporation of a futures exchange responsible for settling trading accounts, clearing trades, collecting and maintaining margin monies, regulating delivery, and reporting trading data.

A complete background analysis of the clearing houses and settlements market, which includes an assessment of the national accounts, economy, employment, and emerging market trends by segments, significant changes in the market dynamics, and a market overview, is covered in the report. The clearing houses and settlements market is segmented by type (outward clearing house, inward clearing house), by service (TARGET2, SEPA, EBICS), by other services (EURO1, CCBM), and by geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The report offers market size and forecasts for the Global Clearing Houses and Settlements Market in value (USD billion) for all the above segments.

| Outward Clearing House |

| Inward Clearing House |

| TARGET2 | |

| SEPA | |

| EBICS | |

| Other Services | EURO1 |

| CCBM |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Type | Outward Clearing House | |

| Inward Clearing House | ||

| By Service | TARGET2 | |

| SEPA | ||

| EBICS | ||

| Other Services | EURO1 | |

| CCBM | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the clearing houses and settlements market size in 2026 and the expected growth to 2031?

The clearing houses and settlements market size is USD 13.13 billion in 2026 and is projected to reach USD 16.81 billion by 2031 at a 5.07% CAGR.

Which segment leads the clearing houses and settlements market by type in 2026?

Outward clearing houses lead with 67.50% share in 2025 and maintain the fastest trajectory at a 5.82% CAGR through 2031.

What service type holds the largest share in the clearing houses and settlements market?

TARGET2 held 43.80% share in 2025 and advances at a 7.43% CAGR through 2031.

Which region is growing the fastest in the clearing houses and settlements market?

Europe records the fastest growth with a 6.65% CAGR through 2031, driven by TARGET Services consolidation and ISO 20022 migration.

What regulatory changes are most impactful for clearing houses through 2027?

The SEC’s Treasury clearing rules for cash and repo transactions drive central clearing adoption with deadlines in late 2026 and mid 2027, raising margin and operational capacity needs.

How are instant payments shaping the clearing houses and settlements market?

TIPS and FedNow expand instant payments, with TIPS volumes surging 402.2% in 2024 and FedNow scaling to USD 307.3 billion in Q3 2025 value, which raises expectations for always-on settlement.

Page last updated on: