Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

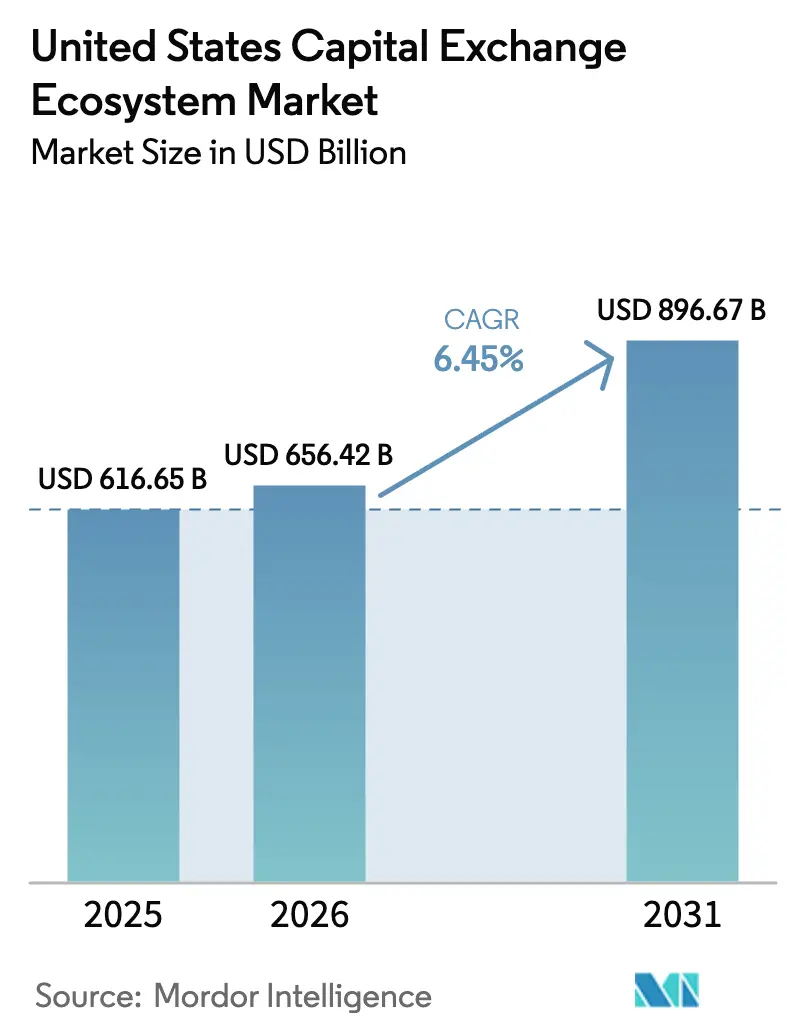

| Base Year Market Size (2025) | USD 616.65 Billion |

| Market Size (2026) | USD 656.42 Billion |

| Market Size (2031) | USD 896.67 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Capital Exchange Ecosystem Market Analysis by Mordor Intelligence

United States Capital Exchange Ecosystem market size in 2026 is estimated at USD 656.42 billion, growing from 2025 value of USD 616.65 billion with 2031 projections showing USD 896.67 billion, growing at 6.45% CAGR over 2026-2031. Solid growth reflects sustained algorithmic‐trading adoption, deeper institutional demand for sophisticated execution services, and a revitalized IPO pipeline that is lifting fee pools across asset classes. The Federal Reserve’s policy-normalization cycle first curtailed margin-driven volumes, yet subsequent rate volatility propelled derivative hedging and bond trading, adding fresh revenue streams for venue operators. Exchanges are upgrading core systems to enable 24/7 order matching, consolidated data feeds, and tokenized security workflows, thereby improving transparency and reinforcing platform stickiness. Zero-commission brokerage models are swelling retail participation, which is prompting exchanges to launch fractional shares, tailored analytics, and extended trading windows that preserve engagement while smoothing intraday liquidity patterns. Regionally, leadership remains anchored in the Northeast, but the West’s fast-growing technology ecosystem is recasting the competitive landscape and catalyzing national innovation cycles.

Key Report Takeaways

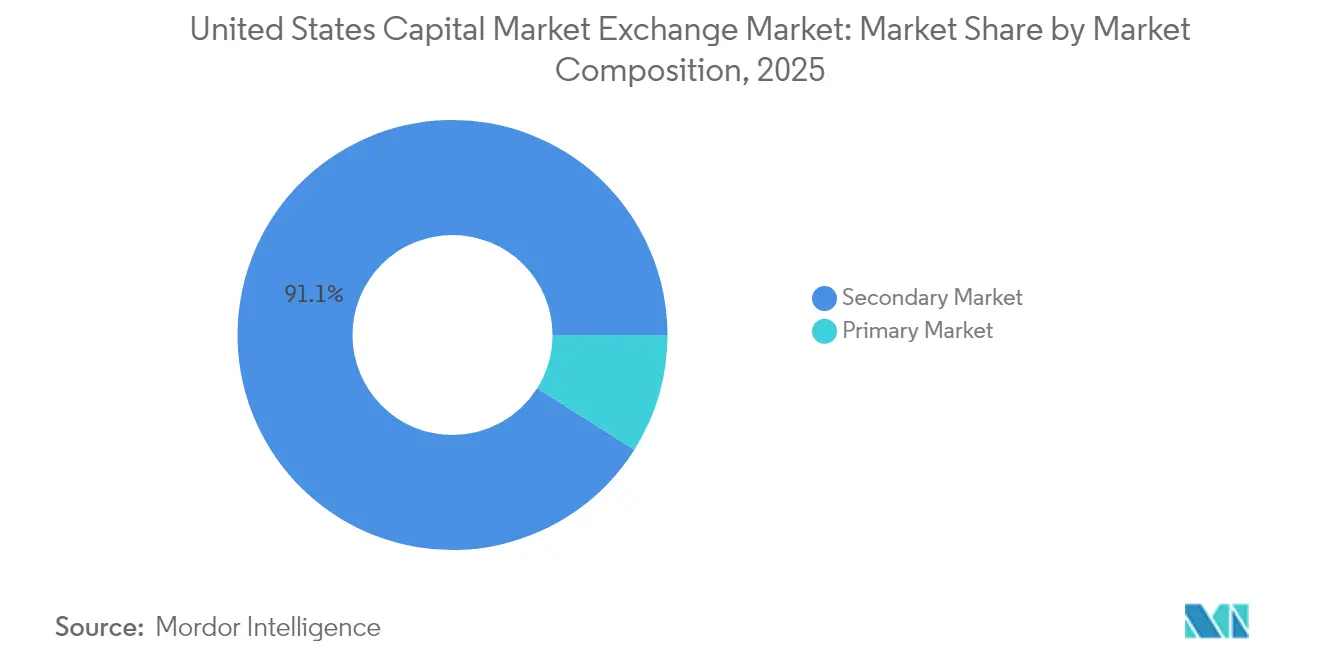

- By market composition, the secondary segment held 91.05% of the United States capital market exchange market share in 2025, while the primary segment is forecast to rise at a 6.11% CAGR through 2031.

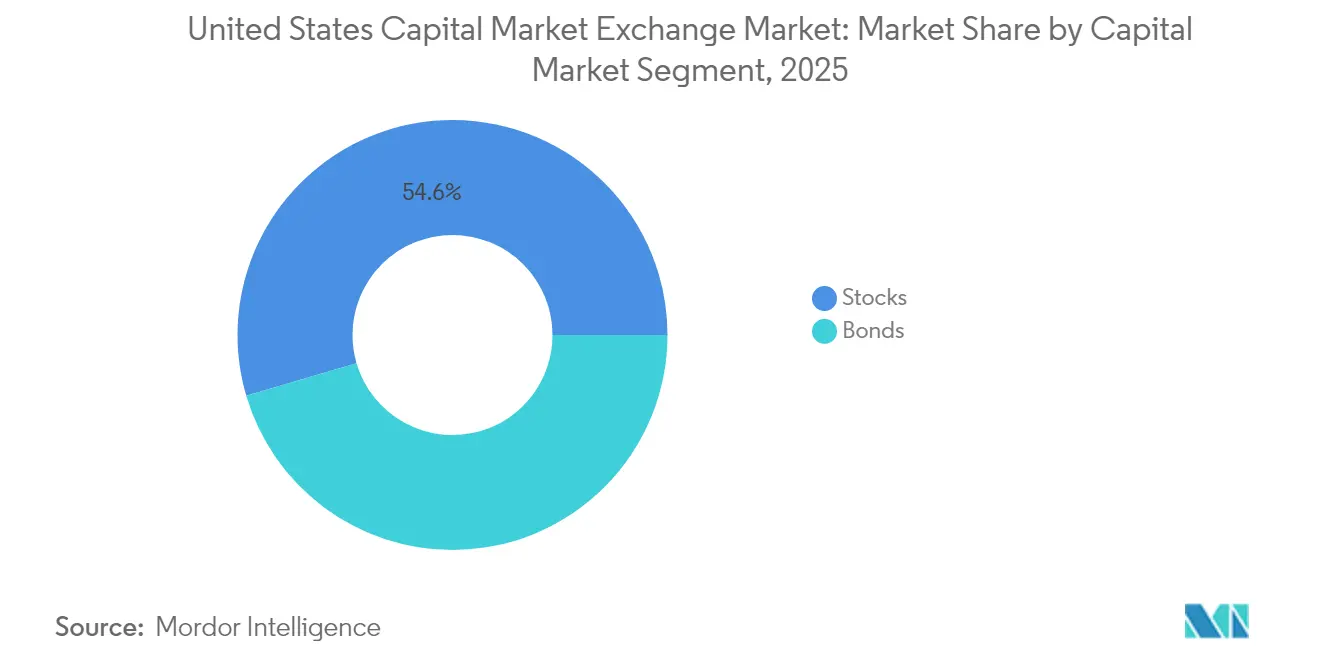

- By capital-market segment, stocks captured 54.55% of the United States capital market exchange market size in 2025, whereas bonds are positioned to expand at a 4.12% CAGR to 2031.

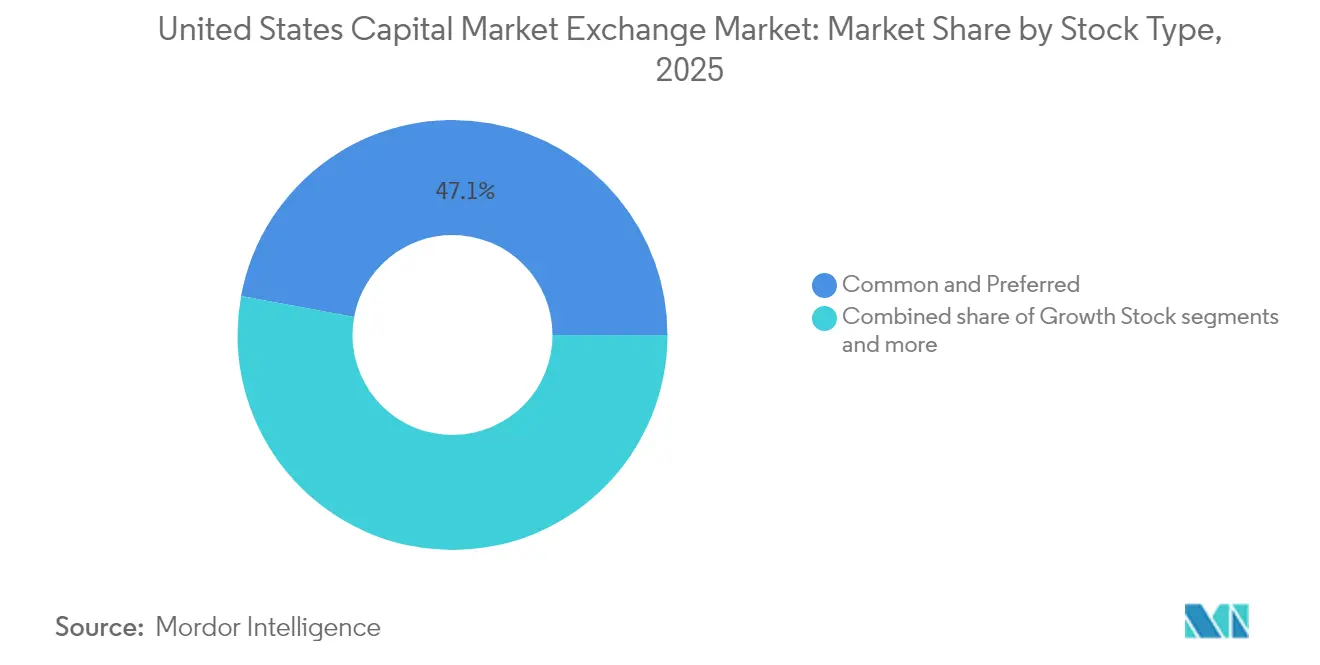

- By stock type, common and preferred shares represented 47.10% of the United States capital market exchange market size in 2025; growth stocks are projected to climb at an 8.75% CAGR through 2031.

- By bond type, government securities commanded a 36.55% share of the United States capital market exchange market in 2025, while corporate bonds are advancing at a 5.79% CAGR between 2026 and 2031.

- By geography, the Northeast commanded a 31.20% share of the United States capital market exchange market in 2025, while the West is advancing at a 5.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Capital Exchange Ecosystem Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream shift to algorithmic trading | +2.1% | National, with concentration in the Northeast and the West | Medium term (2-4 years) |

| Fed monetary policy normalization | +1.8% | National, with varying regional impacts | Short term (≤ 2 years) |

| Rising ESG-linked issuance | +1.4% | National, led by the West and the Northeast | Long term (≥ 4 years) |

| Surge in retail participation via zero-commission trading | +1.7% | National, with higher adoption in the South and West | Medium term (2-4 years) |

| Tokenization of securities enabling 24/7 trading | +0.9% | National, early adoption in the West | Long term (≥ 4 years) |

| Consolidated Tape implementation boosting transparency | +0.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mainstream shift to algorithmic trading

Algorithmic strategies now govern a majority of the United States equity executions, compelling exchanges to refine microsecond-level latency and scale messaging capacity to accommodate surging quote traffic. Sub-dollar shares doubled to 24% of total equity volume in May 2025, signalling that machine-learning models are harvesting liquidity pockets once overlooked by traditional desks[1]Federal Reserve Bank of Boston, “New England Economic Conditions Through April 22, 2025,” bostonfed.org . Market makers are investing heavily in artificial-intelligence decision engines and quantum-inspired analytics to preserve edge as spreads compress. Cloud-hosted algo toolkits are democratizing access, allowing small firms to compete head-on with bulge-bracket players, which intensifies price competition and tightens retail execution quality. Exchanges are answering with richer depth-of-book feeds, flexible order types, and co-location expansions that attract latency-sensitive participants.

Fed monetary policy normalization

Rate increases initially reduced speculative leverage but soon stoked demand for risk-management instruments and electronic bond venues, with Treasury and SOFR futures gaining open interest as duration hedges. The Northeast posted faster GDP growth in 2024 than the national average despite tighter policy, highlighting regional resilience. Exchanges expanded fixed-income matching and broadened derivative listings to capture volatility-driven turnover. Higher yields sparked corporate refinancings that invigorated primary-debt issuance and diversified fee flows beyond equities. Venue operators are also layering inflation-protection tools to meet asset-owner hedging mandates in the new rate environment.

Rising ESG-linked issuance

ESG criteria have migrated from niche to mainstream, boosting green-bond supply across technology, healthcare, and industrial borrowers. Venues now stream tagged sustainability metrics in real time by partnering with ratings providers, enabling algorithm screens aligned to specific governance thresholds. SEC climate-disclosure proposals accelerate institutional mandates, pushing exchanges to create dedicated ESG trading segments and carbon-intensity indices[2]MEMX, “Sub-Dollar Trading, Options Market Share, and More,” memx.com . Product innovation spans sustainability-linked bond futures and option overlays that let investors express thematic convictions with capital efficiency.

Surge in retail participation via zero-commission trading

The adoption of commission-free trading models has significantly accelerated the growth of new accounts, resulting in a notable increase in message traffic and a shift in trade sizes toward smaller transactions executed during extended trading hours. Brokerage firms are utilizing advanced machine-learning algorithms to optimize payment-for-order-flow mechanisms, focusing on achieving price improvements while maintaining a zero-fee structure. Retail-heavy securities are exhibiting heightened intraday volatility, prompting exchanges to implement enhanced limit-up/limit-down mechanisms and introduce fractional-share trading programs to ensure market stability and orderly operations. On a regional level, the South and West regions demonstrate the highest levels of retail trading activity, driven by factors such as population growth and increased adoption of technological advancements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty for digital-asset securities | -1.2% | National, with varying state-level approaches | Medium term (2-4 years) |

| Cybersecurity threats to exchange operations | -0.8% | National, with a higher risk in major financial centres | Short term (≤ 2 years) |

| Escalating market-data fee disputes | -0.6% | National, with concentration in the Northeast and the West | Medium term (2-4 years) |

| Liquidity fragmentation across ATS venues | -0.5% | National, with primary impact on equity markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory uncertainty for digital-asset securities

The United States exchanges are navigating a complex and evolving regulatory framework established by the SEC, which categorizes digital assets into utility tokens, security tokens, and stablecoins. This segmentation requires the implementation of multiple compliance frameworks and the establishment of legal risk mitigation strategies, increasing operational complexity. Although the approval of Bitcoin ETFs has provided limited regulatory clarity, the absence of definitive registration pathways for tokenized-equity models continues to impede their broader adoption and integration into the financial ecosystem. This regulatory uncertainty places domestic exchanges at a competitive disadvantage, as offshore competitors operating under more stable regulatory environments are better positioned to capture market growth, potentially constraining revenue diversification opportunities for the US-based platforms. Additionally, prolonged delays in the SEC’s comment periods are extending capital expenditure cycles for digital-wallet custody infrastructure, further inflating operational cost structures and impacting profitability.

Cybersecurity threats to exchange operations

Malicious actors are increasingly employing distributed denial-of-service (DDoS) attacks, ransomware payloads, and supply-chain vulnerabilities to target critical components such as matching engines and data fabric within financial systems. In high-frequency trading environments, even brief outages measured in microseconds can result in substantial financial losses due to slippage, thereby elevating systemic risk thresholds. Regulatory requirements from the SEC mandate detailed incident reporting within four business days, which intensifies reputational risks and drives up insurance premiums for affected entities. To mitigate these challenges, exchanges are prioritizing investments in advanced security measures, including zero-trust perimeter frameworks, AI-powered anomaly detection systems, and geographically distributed hot-standby data centres to ensure operational continuity. Despite these efforts, residual risks persist, representing a significant operational constraint that requires ongoing strategic management and resource allocation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Market Composition: Secondary Market Dominance Drives Innovation

The secondary arena held 91.05% of the United States capital market exchange market share in 2025, underscoring mature liquidity and robust electronic infrastructure. Venues continuously migrate core systems to cloud-native architectures that scale elastically during peak quote bursts, ensuring consistent latency for algorithmic participants. Alternative trading systems siphon block flow by offering anonymity and midpoint price improvement, yet public exchanges defend franchise positions through innovative order types such as auction-only crosses and retail liquidity programs. The primary segment is projected to post a 6.11% CAGR through 2031 as direct listings, SPAC conversions, and venture-stage IPOs proliferate, reflecting corporate enthusiasm for equity-based financing amid technology disruption.

Technology roadmaps reveal a shift toward continuous trading that will blur the boundary between issuance and secondary turnover. Nasdaq’s 24-hour framework hinges on synchronized clearing, surveillance, and corporate-action workflows targeting full rollout by late 2026 . Primary issuers could adopt multiple pricing windows within a day, enhancing capital-raising speed and global investor access. The United States capital market exchange market benefits as data-feed subscriptions and order-handling fees scale with time-zone expansion, bolstering top-line resilience.

By Capital Market Segment: Equity Leadership Amid Fixed-Income Renaissance

Stocks contributed 54.55% of overall activity in 2025, buoyed by ETF arbitrage, retail day-trading, and index-rebalancing flows that sustain deep two-sided markets. Derivative overlays such as options, gamma hedging, and delta-one swaps magnify equity volumes, providing venues with stable transaction-fee annuities. Bonds are projected to grow 4.12% annually through 2031 as rate volatility invites tactical allocation shifts and electronification dismantles historic voice-broker dominance. Institutional desks leverage auto-RFQ protocols to source all-to-all liquidity, compressing corporate-bond bid-ask spreads and lifting executed ticket counts.

Regionally disparate inflation trends influence asset-mix decisions: shelter-driven Northeast CPI elevates demand for Treasury hedges, while booming Southern employment lifts equity risk appetite. ESG overlays broaden both segments, with exchanges listing green-bond ETFs and low-carbon equity baskets to satisfy sustainability mandates. As multiproduct venues integrate matching for cash, derivatives, and financing, cross-margin efficiency attracts larger portfolios, helping cement the United States capital market exchange market as the global liquidity benchmark.

By Stock Type: Growth Stocks Lead Innovation-Driven Rally

Growth stocks are expected to climb at an 8.75% CAGR to 2031, outpacing defensive cohorts as investors concentrate on artificial intelligence, cloud, and cybersecurity themes. The top-ten constituents now represent over 30% of S&P 500 capitalization, reviving debates about systemic concentration and index methodology. Common and preferred securities, holding 47.10% share, retain foundational status for dividend stability and governance rights that underpin liability-matching institution strategies.

Quantitative investment approaches exploit factor volatility to toggle exposures between value, quality, and momentum baskets, driving turnover and providing liquidity across capitalization tiers. Exchanges support thematic segmentation by launching sector-specific listing categories and tailored data files, further reinforcing their role as innovation hubs. Active-share ETPs and option-enhanced wrappers diversify revenue streams while deepening tradeable instruments for growth exposures.

By Bond Type: Corporate Bonds Gain Momentum Amid Diversification

Government securities maintained a 36.55% share of fixed-income value in 2025, anchoring the yield curve and serving as macro hedge vehicles during volatility spikes. Corporate issuance, however, is poised for a 5.79% CAGR, fuelled by refinancing needs and investors’ search for incremental spread pickup. ESG-linked corporate structures, including step-up coupons tied to emissions targets, proliferate across investment-grade and high-yield tiers, attracting dedicated sustainability funds.

Electronification of dealer workflows supports auto-executable odd-lot corporates, broadening access for smaller asset managers and wealth platforms. The Consolidated Audit Trail’s extension into bonds bolsters surveillance and investor confidence, which in turn lifts liquidity. Municipal borrowing benefits from infrastructure-bill disbursements, while mortgage-backed activity benefits from algorithmically optimized duration hedging as prepayment speeds fluctuate. Together, these trends reinforce diversified fee inflows for the United States capital market exchange.

Geography Analysis

The Northeast retained a 31.20% share in 2025 due to its dense concentration of broker-dealers, asset managers, and regulatory talent pools. April 2025 unemployment reached 4.2%, converging on national levels, while core inflation hovered near 3%, driven by high shelter costs that pressured real wages . Office market vacancies in Boston and New York climbed, spawning distressed-debt trading opportunities and heightening REIT turnover that secures fee revenue for exchanges. Fintech sandboxes in Massachusetts and New York accelerate regulatory-compliant pilots for tokenized securities and T+0 settlement, reinforcing regional leadership in market-structure innovation.

The West is forecast to expand at a 5.11% CAGR through 2031, propelled by Silicon Valley venture activity, abundant engineering talent, and a pipeline of growth-stage IPOs. Regional venues pioneer crypto-equity hybrids, continuous matching, and high-bandwidth cloud gateways that handle the large message footprints typical of algorithmic quoting. Demographic inflows to California, Washington, and Utah sustain entrepreneurial ecosystems that demand capital-formation services, while tech employee liquidity programs feed secondary-market trading volumes.

Southern and Midwestern hubs offer diversification and cost advantages that underpin national stability. Population migration to Texas and Florida is driving SME listings, municipal-bond issuance, and increased derivative hedging related to energy markets. Midwest exchanges leverage agricultural futures heritage to expand cross-asset clearing, attracting corporate treasury desks that hedge raw-material exposures alongside FX and interest-rate risk. Distributed dual-site data centers located across these regions reinforce overall United States capital market exchange market resilience and demonstrably reduce single-point-of-failure risk.

Competitive Landscape

The United States capital market exchange market exhibits moderate concentration, with five primary venues controlling a significant share of 2024 turnover. NYSE, Nasdaq, and Cboe compete through latency-optimized infrastructures, diverse listing packages, and strategic acquisitions that expand service coverage in derivatives and digital assets. Challenger platforms such as MEMX, IEX, and the Long-Term Stock Exchange target fee compression and transparency gaps, capturing incremental share as buy-side routing logic prioritizes cost-effective (“maker-taker neutral”) venues.

Technology differentiation remains the chief battleground. Nasdaq’s AWS partnership accelerates data analytics and reduces time-to-market for product launches, while NYSE leverages ICE’s global commodity reach to cross-sell futures connectivity. Consolidated Audit Trail compliance and T+1 settlement cycles elevate fixed-cost baselines, potentially triggering niche-venue consolidation or cooperative resource sharing. Exchanges also vie for sustainability leadership by offering ESG-badge visibility, discounted listing fees for verified green issuers, and climate-risk analytics that embed directly into order-routing dashboards.

White-space expansion focuses on 24/7 trading and tokenization. NYSE Texas launched as an ETP listing venue in May 2025, signaling geographic expansion as legacy brands localize services to capture regional sponsorship. Over the forecast window, leadership will rest with operators that bundle issuance, trading, data, and post-trade utilities in unified SaaS frameworks, ultimately raising switching costs and deepening customer engagement.

United States Capital Exchange Ecosystem Industry Leaders

New York Stock Exchange (NYSE)

Nasdaq, Inc.

Cboe Global Markets

OTC Markets Group

Investors Exchange (IEX)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nasdaq detailed the rollout of its 24-hour trading framework, marking a major platform expansion that will add continuous order-matching and overnight clearing capabilities.

- April 2025: NYSE filed rule changes to expand its Virtual Control Circuit connectivity service between the Mahwah data center and trading floors, an infrastructure upgrade that extends bandwidth and lowers latency for members.

- March 2025: NYSE Texas officially opened as a new primary listing venue for exchange-traded products, widening Intercontinental Exchange’s geographic footprint and product shelf in the United States.

- June 2024: MEMX expanded its product lineup by launching an electronic options marketplace that quickly captured 3.1% of U.S. regular electronic options volume, underscoring successful new-product penetration.

United States Capital Exchange Ecosystem Market Report Scope

The capital market exchange ecosystem includes an ecosystem of markets in which debt or equity-backed securities are bought and sold. These are carried out on various platforms known as a stock exchanges. A complete analysis of the US Capital Market Exchange Ecosystem, which includes an assessment of emerging trends, significant changes in market dynamics, and a market overview is covered in the report. The US Capital Market Exchange Ecosystem is Segmented by Type of Market (Primary Market and Secondary Market), by Financial Instruments (Debt and Equity), and by Investors (Retail Investors and Institutional Investors). The report offers market size and forecasts for the US Capital Market Exchange Ecosystem in value (USD Million) for all the above segments.

By Market Composition

| Primary Market |

| Secondary Market |

By Capital Market Segment

| Stocks |

| Bonds |

By Stock Type

| Common & Preferred Stock |

| Growth Stock |

| Value Stock |

| Defensive Stock |

By Bond Type

| Government Bonds |

| Corporate Bonds |

| Municipal Bonds |

| Mortgage Bonds |

| Other Bond Types |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Market Composition | Primary Market |

| Secondary Market | |

| By Capital Market Segment | Stocks |

| Bonds | |

| By Stock Type | Common & Preferred Stock |

| Growth Stock | |

| Value Stock | |

| Defensive Stock | |

| By Bond Type | Government Bonds |

| Corporate Bonds | |

| Municipal Bonds | |

| Mortgage Bonds | |

| Other Bond Types | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the projected value of the United States capital market by 2031?

Forecasts place the United States capital market exchange market size at USD 896.67 billion by 2031, reflecting a 6.45% CAGR from 2026 levels.

Which trading venue segment currently dominates transaction activity?

The secondary segment leads with 91.05% market share, underlining its deep liquidity and mature electronic infrastructure.

Which U.S. region is experiencing the fastest expansion in exchange activity?

The West is projected to grow at a 5.11% CAGR through 2031, supported by Silicon Valley’s technology ecosystem and venture-driven IPO pipelines.

Why are corporate bonds gaining traction with investors?

Rising corporate issuance, ESG-linked financing structures, and the shift to electronic dealer workflows are driving a 5.79% CAGR in corporate-bond turnover.

How are exchanges adapting to rapid growth in retail trading?

Platforms are adding fractional-share functionality, extended hours, richer educational analytics, and refined order types to accommodate smaller lots and maintain execution quality

What technology initiative could most transform U.S. exchange competition?

Broad adoption of 24/7 trading infrastructure and tokenized security settlement is poised to reshape market access and settlement cycles over the next five years.

Page last updated on: