Citizen Services AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

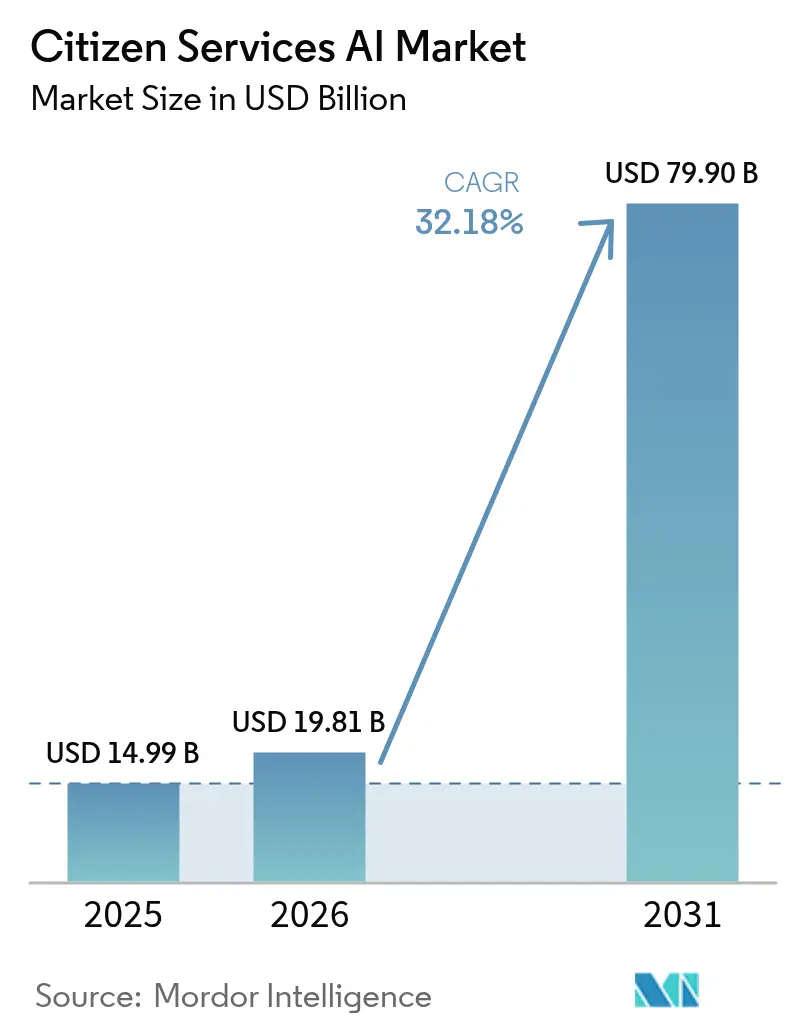

| Market Size (2026) | USD 19.81 Billion |

| Market Size (2031) | USD 79.9 Billion |

| Growth Rate (2026 - 2031) | 32.18% CAGR |

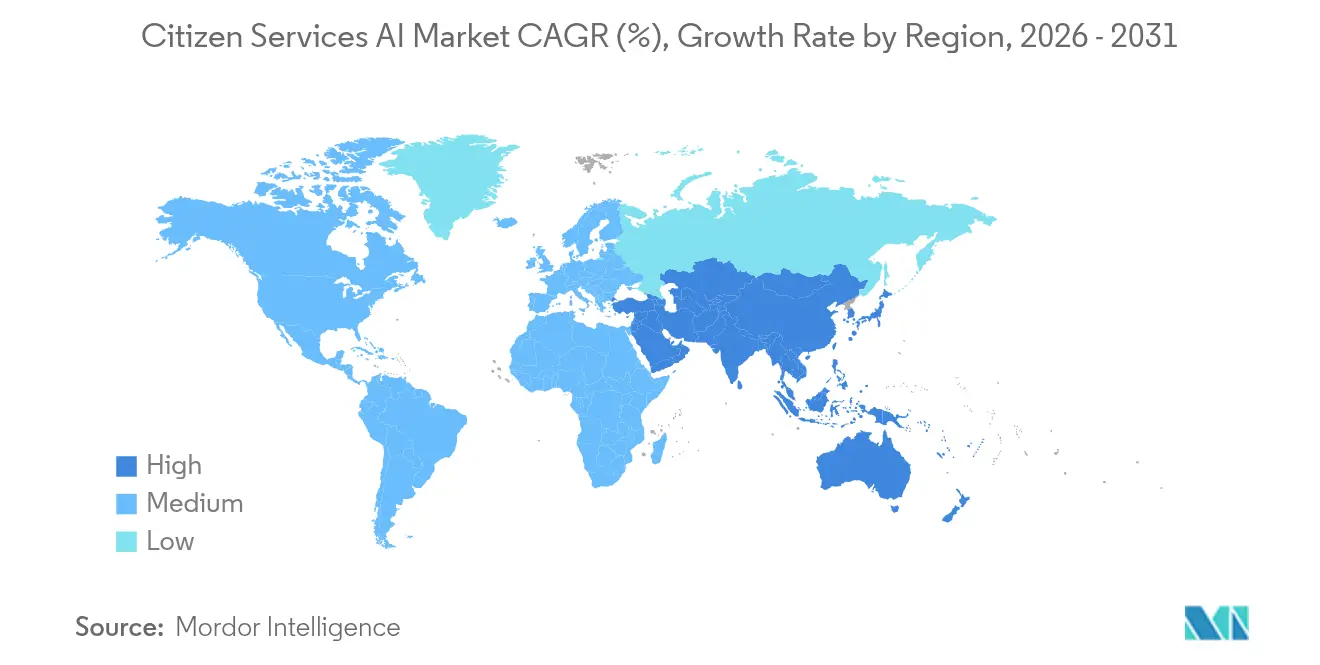

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Citizen Services AI Market Analysis by Mordor Intelligence

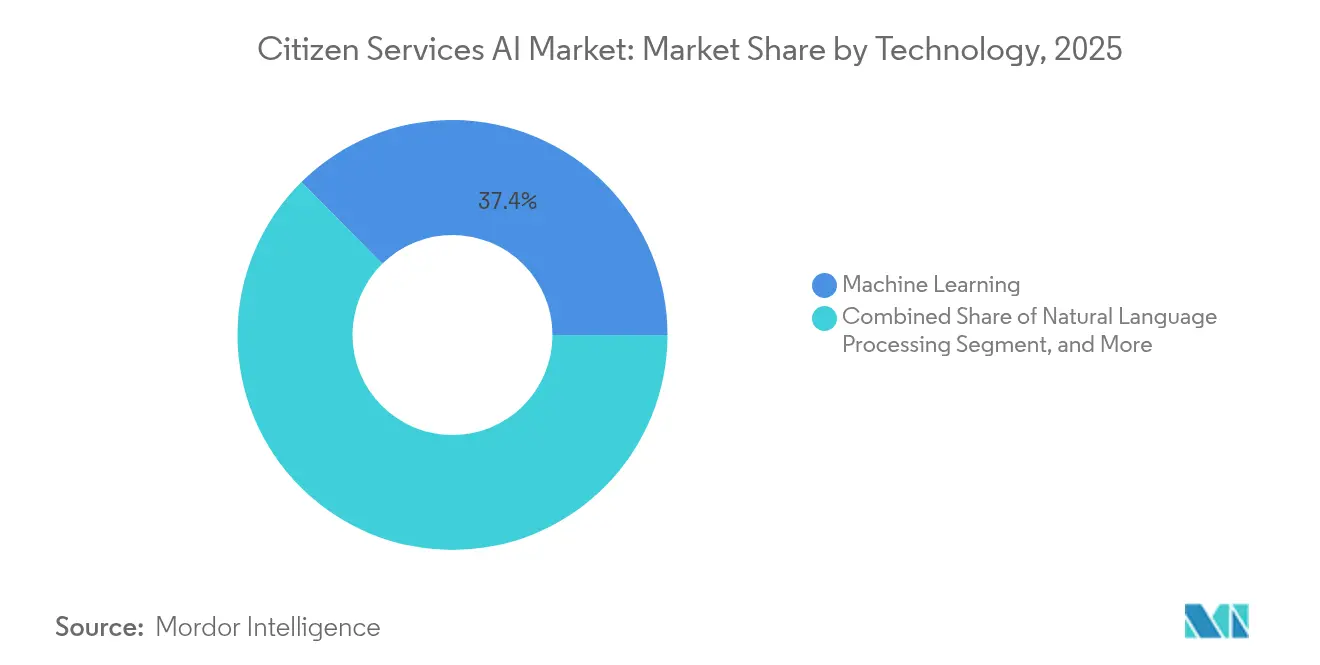

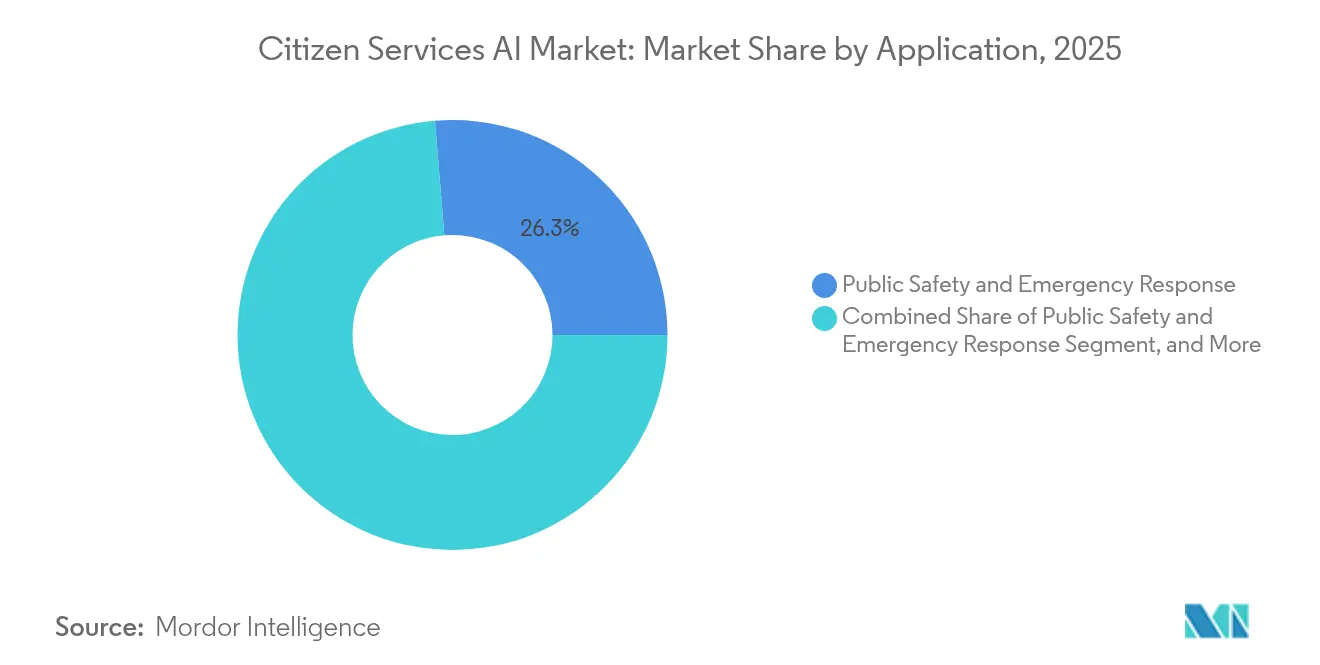

The Citizen services AI market size is expected to grow from USD 14.99 billion in 2025 to USD 19.81 billion in 2026 and is forecast to reach USD 79.9 billion by 2031 at 32.18% CAGR over 2026-2031. This swift rise illustrates how governments are replacing reactive workflows with predictive, autonomous public-service delivery. Federal agencies alone allocated USD 5.6 billion to AI programs between fiscal years 2022-2024, and the Biden administration has requested a further USD 3 billion for federal AI modernization in 2025. Rising sovereign-AI mandates, Section 508 accessibility rules, and the spread of low-code platforms jointly accelerate adoption, while integrated cloud suites make large-scale deployments feasible. North America controls 46% of the Citizen services AI market, yet Asia-Pacific is advancing at a 37% CAGR as large national AI investments, such as South Korea’s USD 735 billion sovereign-AI program, gather pace. Machine-learning tools still lead with 38% share, but generative AI is scaling at 38% growth as agencies lean on conversational interfaces to boost citizen engagement. [1]Camille Busette, “The evolution of artificial intelligence (AI) spending by the U.S. government,” Brookings, brookings.edu

Key Report Takeaways

- By technology, machine learning held 37.40% of the Citizen services AI market share in 2025, while generative AI is projected to grow at a 36.2% CAGR through 2031.

- By component, solutions and platforms captured 61.20% of the Citizen services AI market size in 2025; managed services are forecast to expand at a 34.4% CAGR.

- By deployment model, cloud accounted for 70.10% of the Citizen services AI market size in 2025, whereas hybrid and edge deployments are rising at a 37.5% CAGR.

- By application, public safety and emergency response commanded a 26.30% share of the Citizen services AI market size in 2025, while citizen engagement is advancing at a 37.8% CAGR.

- By end-user tier, state and provincial agencies led with a 34.20% share of the Citizen services AI market in 2025; county and municipal governments record the highest projected CAGR at 36.6%.

- By geography, North America dominated with 45.30% revenue share in 2025; Asia-Pacific is forecast to post a 35.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Citizen Services AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing public sector funding earmarked for AI modernization | +8.50% | Global, with North America and EU leading | Medium term (2-4 years) |

| Mandates for digital accessibility and inclusive citizen engagement | +6.20% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Advances in low-code / no-code AI platforms enabling rapid deployment | +7.10% | Global, particularly beneficial for smaller municipalities | Short term (≤ 2 years) |

| Integration of 5G and edge computing for real-time civic services | +4.80% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Adoption of AI digital twins for urban planning and infrastructure | +3.90% | Global, with early gains in smart cities | Long term (≥ 4 years) |

| Rise of AI-powered proactive social safety-net interventions | +2.70% | North America and EU, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing public sector funding earmarked for AI modernization

Federal AI spending rose 177% in small-business set-asides between 2018-2023, transforming AI from pilot projects into core infrastructure. The National Security Commission on AI recommends annual non-defense spending of USD 32 billion by 2026 to secure continued momentum. Executive Order 14110 now requires every federal agency to appoint a chief AI officer, embedding sustained budgets and accountability. California alone draws from USD 138.9 billion in overall SLED IT budgets for 2025 deployments. These moves signal that reliable, multi-year funding has become a structural driver rather than an isolated event.[2] U.S. General Services Administration, “Govwide ITVMO Small-Business Assessments Artificial Intelligence,” gsa.gov

Mandates for digital accessibility and inclusive citizen engagement

Section 508 compliance pushes agencies to design AI that serves diverse language and ability needs; 24% of U.S. residents speak a language other than English at home, heightening demand for multilingual assistants. The Biden administration’s AI order prioritizes equity, turning accessibility from a compliance box into a growth catalyst. Singapore’s government chatbot, which lets residents contact any civil servant via Facebook Messenger, shows how AI democratizes access to officials. Agencies therefore invest in real-time translation, voice navigation, and adaptive interfaces to expand service reach while cutting call-center costs.

Advances in low-code / no-code AI platforms enabling rapid deployment

Low-code AI reduces technical barriers, letting agencies prototype in weeks rather than quarters. Montana’s Department of Justice built DMV chatbots despite tight budgets, proving small teams can launch enterprise-grade services. Vendors such as ServiceNow integrate Microsoft Copilot and domain-specific models so workflows, data policies, and security controls are pre-configured, shortening learning curves. Standardized playbooks, like the U.S. Department of Energy’s Generative AI Reference Guide, further cut time-to-value by codifying best practices in governance and ethics.

Integration of 5G and edge computing for real-time civic services

Edge processing keeps latency in the millisecond range, critical for traffic optimization, public-safety video analytics, and disaster response. Pittsburgh’s AI traffic lights trimmed emissions 21% while cutting journey times 26%, showing the tangible impact of local inference. U.S. federal agencies are now urged to invest in GPU-accelerated edge nodes to meet surging AI workloads, and multicloud strategies ensure that sensitive data remains sovereign while still tapping hyperscale compute burst capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget volatility and fiscal austerity cycles in municipalities | -4.30% | Global, particularly affecting smaller municipalities | Short term (≤ 2 years) |

| Public skepticism over algorithmic transparency and privacy | -3.80% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| Fragmented legacy data architectures hampering AI training | -5.10% | Global, more severe in older government systems | Medium term (2-4 years) |

| Shortage of domain-specific annotated datasets for civic use-cases | -2.90% | Global, with variations by local language and context | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget volatility and fiscal austerity cycles in municipalities

Smaller jurisdictions often operate on annual, cash-constrained budgets that make multiyear AI projects difficult to sustain. Wake County, North Carolina paid SAS USD 707,587 since 2018 to automate property assessments, yet similar outlays are the first cut during downturns. Only 24% of state CIOs report mature data-governance frameworks for generative AI, underscoring resource limitations that extend well beyond software licensing. Competitive federal grant programs cushion some risk, but their episodic nature forces agencies to favour short-term ROI over systemic transformation. [3]Zachary Eanes, “North Carolina County Uses AI for Property Revaluations,” The News & Observer, govtech.com

Public scepticism over algorithmic transparency and privacy

Citizens question opaque automated decisions that affect benefits, licenses, or public safety. The U.K. Government’s GPT-4o chatbot faced criticism for hallucinated answers, highlighting accuracy concerns. In the United States, lawmakers raised alarms after an AI-driven review cancelled more than 650 Department of Veterans Affairs contracts, reinforcing demands for explainable AI. Agencies must now budget for robust model-audit tools and public engagement programs, lengthening deployment cycles and increasing costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Machine learning’s maturity meets generative AI disruption

Machine learning accounted for 37.40% of the Citizen services AI market in 2025 as agencies relied on predictive analytics for fraud detection, infrastructure monitoring, and permit backlogs. Its dominance stems from proven toolkits, pre-trained models, and a decade of incremental policy guidelines that derisk procurement. Yet generative AI and large language models are expanding at a 36.2% CAGR, propelled by rising demand for conversational interfaces that handle routine inquiries without staff intervention. The Social Security Administration’s employee-facing chatbot illustrates how natural-language tools streamline internal workflows. Computer-vision AI, bolstered by Costa Mesa’s manhole-inspection pilot, is also scaling as video archives become a rich data source for infrastructure analytics. Facial recognition retains a foothold in border control and secure facility access even as regulators impose tighter guardrails. Cutting-edge techniques such as federated and reinforcement learning enter pilot stages, especially inside defense agencies pursuing sovereign data strategies. Together, these shifts suggest that machine learning will remain foundational, but generative AI will gradually command higher budget shares through 2031, reshaping value capture across the Citizen services AI market.

Generative-AI momentum is visible in procurement notices stipulating large-language-model integration, multilingual output, and retrieval-augmented generation. OpenAI’s USD 200 million Department of Defense award indicates federal appetite for frontier models aligned with classified-data controls. As agencies invest in synthetic-data generation to offset annotation shortfalls, model-training cycles shorten and broaden use-case coverage. Specialized hardware accelerators, from NVIDIA H100 GPUs to Intel Habana Gaudi 3 chips, enter agency spending plans to sustain compute-hungry fine-tunes. Although generative AI currently represents a smaller slice of the Citizen services AI market size, its rapidly growing install base positions it to overtake several traditional analytics categories by the decade’s close.

By Component: Integrated solutions pull ahead of point products

Solutions and platforms captured 61.20% of the Citizen services AI market size in 2025 as agencies gravitated toward unified suites that bundle orchestration, model catalogues, and governance dashboards. This preference results from procurement simplification: a single authority-to-operate certificate covers multiple functions, reducing compliance overhead. ServiceNow’s Digital Government Transformation Suite exemplifies this trend, embedding a workflow data fabric, AI agents, and asset-management tools into a single, FedRAMP-authorized stack. Managed services, projected to grow at a 34.4% CAGR, appeal to local governments that lack in-house data-science talent; the Department of Homeland Security’s DHSChat serves 19,000 staff via a centrally managed generative AI backbone.Professional services remain critical for change management, risk assessments, and staff training, while hardware accelerators resurface due to the increasing demand for edge and on-premises workloads. Vendors pursue vertical partnerships with Oracle, Palantir, and Microsoft, as well as ServiceNow, to combine infrastructure, analytics, and domain templates in one sale. That integration drives longer contract durations, locking in incremental module sales and raising switching costs. Consequently, platform consolidation is set to deepen, reinforcing the primacy of end-to-end suites in the Citizen services AI market.

By Deployment Model: Cloud still leads, sovereignty drives hybrid surge

Cloud deployments accounted for 70.10% of the Citizen services AI market in 2025 given their near-instant scalability and pay-as-you-go economics. FedRAMP and StateRAMP certifications further speed procurement, turning commercial SaaS products into compliant government workloads. Yet hybrid and edge architectures are advancing at a 37.5% CAGR, driven by data-sovereignty rules and real-time use cases. Nutanix reports that agencies increasingly spread workloads across three or more hyperscalers to avoid vendor lock-in while keeping sensitive datasets on-premises. Oracle-Palantir sovereign clouds exemplify this shift by combining dedicated regions with policy-based data egress controls.Edge nodes stationed in intersections, patrol vehicles, or utility substations push inference closer to the event source, slashing latency for traffic lights, gun-shot detection, and wildfire alerts. Agencies adopt lightweight container orchestration to synchronize edge models with cloud-based retraining pipelines, preserving model accuracy without compromising localized decision making. As policy makers refine data-classification regimes, hybrid architectures will likely become the de facto blueprint, reshaping spending mixes within the Citizen services AI market.

By Application: Public safety remains anchor, citizen engagement scales fastest

Public safety and emergency response held 26.30% of the Citizen services AI market size in 2025 owing to long-standing investments in predictive policing, 911 call triage, and disaster-response simulation. AI traffic-optimization in Las Vegas cut crashes 17%, illustrating strong ROI in life-critical contexts. Simultaneously, contact-center automation for benefits inquiries or permit status drives the citizen-engagement segment’s 37.8% CAGR. Amarillo’s digital assistant “Emma” serves non-English-speaking residents, reducing call-center hold times and improving service ratings.

Healthcare, social services, and utilities follow closely behind as agencies use AI to predict Medicaid churn, allocate shelter beds, or proactively dispatch repair crews. Tax and revenue departments modernize fraud detection through anomaly-scanning algorithms. Environmental regulators test AI-based inspections that flag violations via drone footage, expanding the “other applications” bucket. These diverse opportunities ensure continued broad-based demand across the Citizen services AI market.

By End-User Tier: States dominate volume; municipalities post top growth

State and provincial agencies commanded a 34.20% share of the Citizen services AI market in 2025, leveraging larger IT budgets and broad statutory mandates. Durham County’s rollout of Moveworks chatbots across 30 departments demonstrates how mid-tier governments follow state templates to fast-track transformation. Municipalities, however, are expanding at a 36.6% CAGR as cloud subscriptions and low-code builders make sophisticated tools accessible without dedicated data centers.

Federal-level entities focus on mission-critical, often classified workloads, driving demand for on-prem secure enclaves. Government-owned enterprises such as public utilities experiment with AI for predictive maintenance and customer self-service. Successful county pilots feed state policy toolkits, which subsequently inform federal guidelines. This virtuous cycle strengthens collective momentum within the Citizen Services AI market.

Geography Analysis

North America’s 45.30% revenue share in 2025 reflects USD 5.6 billion in federal AI outlays since 2022, and statewide programs ranging from California’s multi-sector pilots to Oklahoma’s procurement optimization drive. Federal roadmaps, such as DHS’s AI blueprint, align pilot projects for immigration training and hazard mitigation. Municipal innovations from Seattle’s AI traffic signal timing to Spokane County’s body-camera analytics show that local governments actively shape adoption curves.

Asia-Pacific records the fastest regional CAGR at 35.6% through 2031. South Korea’s USD 735 billion sovereign-AI program, Japan’s USD 100 million generative-AI supercomputer, and Singapore’s nation-wide chatbots illustrate multi-country commitment to domestic AI ecosystems. In China, algorithm-regulation mandates are reshaping supplier go-to-market strategies, while Australia’s USD 101.2 million AI-adoption fund aims to create 1.2 million tech jobs by 2030, extending demand beyond federal agencies into education and healthcare.

Europe adopts a governance-led approach, developing comprehensive AI procurement guidelines that emphasize transparency and accountability. The U.K.’s chatbot demonstrates early-stage execution issues that regulators aim to correct through revised service-level metrics. Israel and the UAE incubate smart-city pilots, South Africa tests grant-management bots, and Brazil drafts an AI-governance framework. These diverse trajectories suggest no single blueprint but a spectrum of localized growth paths across the Citizen services AI market.

Competitive Landscape

The Citizen Services AI market is moderately fragmented. Hyperscalers, including Microsoft, Amazon, and Google, dominate infrastructure, while ServiceNow, IBM, Oracle, and Palantir lead in application platforms. Vendors increasingly secure FedRAMP High or StateRAMP authorizations to access public budgets. Oracle’s partnership with Palantir enables Foundry to run within regulated sovereign-cloud regions, thereby addressing data-residency rules for defense clients. ServiceNow’s expanded ties with Microsoft and Google integrate AI agents directly into 365 and Google Workspace, embedding capabilities where government knowledge workers already operate.

Niche entrants carve white-space positions. Ordinal AI provides retrieval-augmented generation tailored to city charters and municipal codes, offering source-linked answers that alleviate transparency concerns. Anthropic’s Claude Gov targets national-security users with air-gapped model-hosting. OpenAI’s USD 200 million defense deal underscores how AI-native firms bypass traditional integrators by pursuing direct Agency-Other-Transaction agreements.

Strategic moves center on joint reference architectures, sovereign-cloud capacity reservations, and industry-specific accelerators. Hardware specialists NVIDIA and Intel court agencies with secure multi-instance GPU partitions that enforce workload isolation. Consulting arms of Deloitte and Accenture assist change management but increasingly bundle proprietary accelerators, blurring lines between service and software. These dynamics keep switching costs high but encourage modular, standards-based interfaces across the Citizen services AI market.

Citizen Services AI Industry Leaders

Microsoft Corporation

ServiceNow, Inc.

Amazon Web Services, Inc.

International Business Machines Corporation

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: OpenAI secured a USD 200 million U.S. Department of Defense contract to prototype frontier AI systems for national-security missions.

- June 2025: Anthropic released Claude Gov models with classified-data safeguards now deployed inside multiple U.S. agencies.

- May 2025: C3 AI received a USD 450 million contract modification from the U.S. Air Force for its PANDA predictive-analytics program.

- March 2025: ServiceNow launched its Digital Government Transformation Suite aimed at the USD 125 billion annual government IT spend.

Global Citizen Services AI Market Report Scope

The study of the citizen service AI market has considered varied offerings from the vendors global based technology such as machine learning, face recognition, natural language processing, etc. for a wide range of applications in the citizen service sector, globally.

| Machine Learning |

| Natural Language Processing |

| Computer Vision and Image Processing |

| Generative AI and Large Language Models |

| Facial and Biometric Recognition |

| Other AI Techniques |

| Solutions / Platforms | |

| Services | Professional Services |

| Managed Services | |

| Hardware Accelerators |

| Cloud |

| On-premises |

| Hybrid and Edge |

| Traffic and Transportation Management |

| Public Safety and Emergency Response |

| Healthcare and Social Services |

| Utilities and Smart Infrastructure |

| Citizen Engagement and Contact Centers |

| Taxation and Revenue Management |

| Other Applications |

| Federal / National Agencies |

| State and Provincial Agencies |

| County and Municipal Governments |

| Government-Owned Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Computer Vision and Image Processing | ||

| Generative AI and Large Language Models | ||

| Facial and Biometric Recognition | ||

| Other AI Techniques | ||

| By Component | Solutions / Platforms | |

| Services | Professional Services | |

| Managed Services | ||

| Hardware Accelerators | ||

| By Deployment Model | Cloud | |

| On-premises | ||

| Hybrid and Edge | ||

| By Application | Traffic and Transportation Management | |

| Public Safety and Emergency Response | ||

| Healthcare and Social Services | ||

| Utilities and Smart Infrastructure | ||

| Citizen Engagement and Contact Centers | ||

| Taxation and Revenue Management | ||

| Other Applications | ||

| By End-User | Federal / National Agencies | |

| State and Provincial Agencies | ||

| County and Municipal Governments | ||

| Government-Owned Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Citizen services AI market?

The Citizen services AI market reached USD 19.81 billion in 2026 and is projected to grow to USD 79.9 billion by 2031 at a 32.18% CAGR.

Which region leads spending on citizen-service AI solutions?

North America held 45.30% of global revenue in 2025, driven by substantial U.S. federal and state investments.

Which application is expanding fastest?

Citizen engagement and contact-center automation is the fastest-growing application segment, advancing at a 37.8% CAGR through 2031.

Why are hybrid and edge deployments gaining popularity?

Agencies adopt hybrid and edge architectures to keep sensitive data sovereign and to support real-time services such as traffic management that require ultra-low latency.

Who are the leading platform vendors in this market?

ServiceNow, IBM, Oracle, Microsoft, and Palantir dominate the platform layer, while cloud infrastructure is led by Microsoft Azure, Amazon Web Services, and Google Cloud.

What is the main barrier to wider adoption of AI in government?

The leading barriers are budget volatility in smaller jurisdictions, public concerns about algorithmic transparency, and fragmented legacy data architectures that complicate model training.

Page last updated on: