Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.39 Billion |

| Market Size (2026) | USD 5.92 Billion |

| Market Size (2031) | USD 8.46 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Specialty Fertilizer Market Analysis by Mordor Intelligence

The China specialty fertilizer market size is projected to grow from USD 5.39 billion in 2025 to USD 5.92 billion in 2026 and is forecast to reach USD 8.46 billion by 2031, registering a CAGR of 7.40% during 2026–2031. Strong policy support, rapid expansion of protected horticulture, digital sales channels, and carbon credit pilots are driving demand away from traditional NPK products towards high-efficiency products. Liquid formulations dominate due to widespread fertigation systems, while controlled-release innovations accelerate on the back of biodegradability mandates. Supply chains are shifting to direct-to-farmer platforms that compress margins yet expand geographic reach, and manufacturers with in-house agronomic services are capturing premium positioning.

Key Report Takeaways

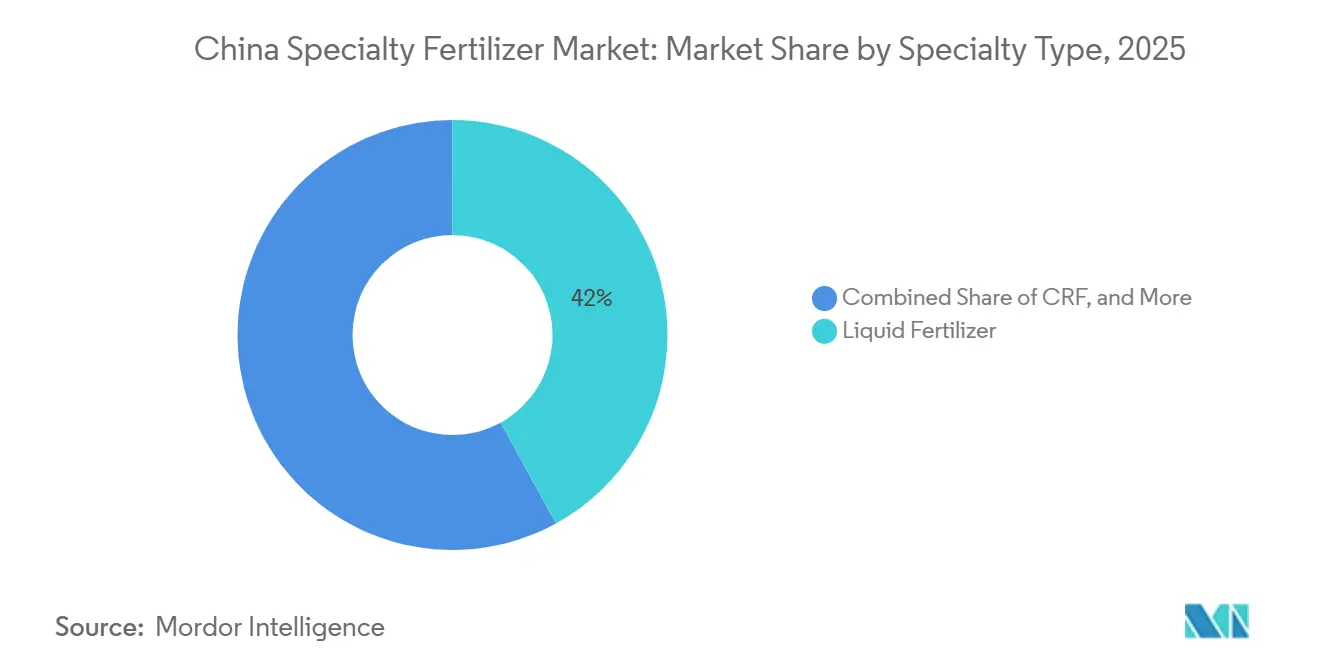

- By Specialty Type, liquid fertilizers held the largest segment, accounting for 42.0% of the China specialty fertilizer market share in 2025, while controlled-release fertilizers are the fastest-growing segment, projected to register a CAGR of 9.2% during 2026–2031.

- By Application Mode, fertigation led the market, accounting for 47.0% of the China specialty fertilizer market size in 2025, whereas soil application is the fastest-growing segment, projected to grow at an 8.1% CAGR during 2026–2031.

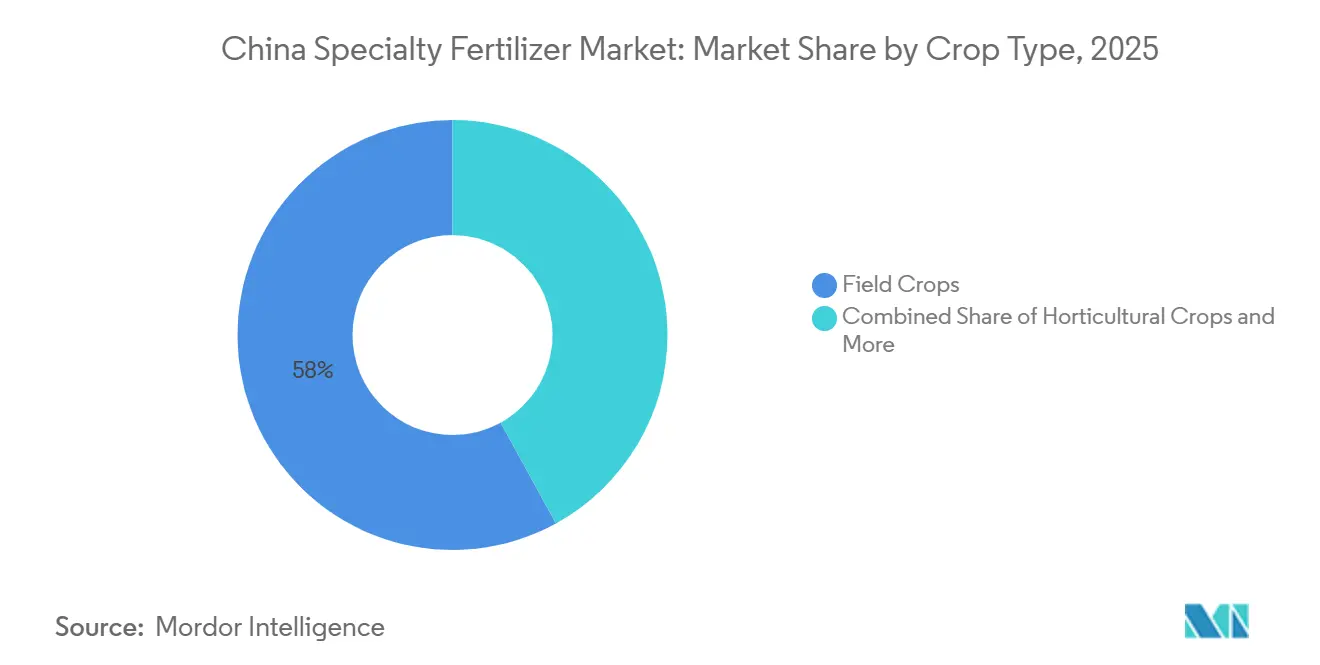

- By Crop Type, field crops held the largest share, accounting for 58.0% of the China specialty fertilizer market in 2025, while horticultural crops are the fastest-growing segment, projected to advance at a CAGR of 9.0% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Specialty Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for high-efficiency fertilizers | +1.5% | National, strongest in Shandong, Henan, Jiangsu | Medium term (2-4 years) |

| Expansion of protected horticulture and greenhouse cultivation | +1.2% | Coastal provinces and Xinjiang | Long term (≥ 4 years) |

| Rising adoption of fertigation and precision irrigation systems | +1.8% | Water-scarce northern regions | Medium term (2-4 years) |

| Shift of tea and specialty cash crops toward customized nutrient blends | +1.1% | Fujian, Zhejiang, Yunnan | Long term (≥ 4 years) |

| E-commerce direct-to-farmer channels reducing distribution friction | +0.9% | Nationwide, fastest in central China | Short term (≤ 2 years) |

| Carbon-footprint linked ag-input credit pilots accelerating coated fertilizer demand | +1.3% | Guangdong, Beijing, and Shanghai pilots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for High-Efficiency Fertilizers

Central and provincial subsidy schemes reimburse up to 30% of controlled-release fertilizer costs, fundamentally altering adoption economics for commercial growers and cooperatives. The Ministry of Agriculture's 2024 policy framework extends these incentives through 2027, targeting 15 million hectares of high-efficiency fertilizer application across major grain-producing regions[1]Source: Ministry of Agriculture and Rural Affairs, “Agricultural Modernization and High-Efficiency Fertilizer Policies,” MOA.GOV.CN. This policy architecture creates a two-tier market where subsidized operations achieve cost parity with conventional fertilizers, while unsubsidized smallholders face persistent price barriers. The subsidy structure supports domestic manufacturers by requiring the use of locally sourced nutrient inputs, facilitating technology transfer, and enhancing production capacity within China.

Expansion Of Protected Horticulture and Greenhouse Cultivation

China's protected horticulture area expanded to 4.2 million hectares in 2024, with plastic-film greenhouses and solar greenhouses driving 85% of this growth, creating concentrated demand for water-soluble and liquid fertilizer formulations. Xinjiang's greenhouse vegetable production alone increased 23% year-over-year, supported by government initiatives to diversify the region's agricultural output beyond cotton. This expansion pattern generates localized supply chain opportunities, as greenhouse operators require frequent, small-batch deliveries of specialized nutrient solutions that traditional bulk fertilizer distributors cannot efficiently serve. The trend toward year-round production cycles in controlled environments necessitates precise nutrient timing, favoring suppliers with technical advisory capabilities.

Rising Adoption of Fertigation and Precision Irrigation Systems

Precision fertigation systems integrate with drip irrigation infrastructure across 8.7 million hectares in northern China, where water scarcity drives adoption of nutrient-efficient application methods. Hebei Province leads implementation with 1.3 million hectares under fertigation, achieving 25% fertilizer use reduction while maintaining yields, according to provincial agricultural authorities. This transformation creates demand for liquid fertilizers and water-soluble formulations specifically engineered for injection systems, while traditional granular products lose relevance in these high-efficiency operations. Equipment manufacturers increasingly bundle fertilizer recommendations with irrigation hardware, creating integrated value propositions that favor specialty fertilizer suppliers with technical partnerships.

Shift of Tea and Specialty Cash Crops Toward Customized Nutrient Blends

Specialty crop producers in Fujian, Zhejiang, and Yunnan provinces increasingly adopt customized nutrient blends tailored to specific cultivars and soil conditions, moving beyond generic NPK formulations toward micronutrient-enriched solutions. Tea gardens covering 3.1 million hectares now utilize specialized formulations that optimize polyphenol content and leaf quality, with premium producers paying 40% premiums for targeted nutrition programs. This trend extends to fruit orchards and vegetable operations targeting export markets, where trace element management directly impacts product quality and certification compliance. Regional agricultural research institutes collaborate with fertilizer manufacturers to develop crop-specific formulations, creating barriers to entry for suppliers lacking local R&D capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher per-ton cost versus conventional fertilizers | -0.8% | Central and Western provinces | Short term (≤ 2 years) |

| Stringent environmental regulations on polymer coatings | -0.6% | Coastal regions enforce most tightly | Medium term (2-4 years) |

| Limited field-level agronomic advisory for smallholders | -0.4% | Fragmented rural areas | Long term (≥ 4 years) |

| Microplastic concerns in green-food certification schemes | -0.3% | Export-oriented production zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Per-Ton Cost Versus Conventional Fertilizers

Specialty fertilizers command prices 1.5 to 3 times higher than conventional NPK, creating adoption barriers for China's 200 million smallholder farming households with average landholdings below 0.6 hectares. Despite government subsidies covering 30% of costs for eligible operations, the absolute price differential remains prohibitive for farmers operating on thin margins, particularly in less-developed central and western provinces where agricultural incomes lag coastal regions. This cost structure creates a bifurcated market where large commercial operations and cooperatives drive specialty fertilizer adoption, while the numerically dominant smallholder segment relies on conventional products. The pricing gap widens during commodity price downturns, as farmers prioritize immediate cost reduction over long-term soil health benefits.

Stringent Environmental Regulations on Polymer Coatings

New GB national standards (Guobiao Standards) implemented in 2024 establish biodegradability requirements for polymer coatings used in controlled-release fertilizers, restricting certain polyethylene and polyurethane formulations that dominated earlier product generations [2]Source: Standardization Administration of China, “GB Standards for Fertilizer Environmental Compliance 2024,” SAC.GOV.CN. Manufacturers must demonstrate 60% coating degradation within 24 months under field conditions, forcing reformulation of existing products and increasing raw material costs by 12-18%. Eastern coastal provinces enforce these standards more rigorously than inland regions, creating compliance complexity for national suppliers. The regulatory framework favors companies with advanced polymer chemistry capabilities while disadvantaging smaller manufacturers relying on commodity coating materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specialty Type: CRF Innovation Drives Future Growth

Liquid fertilizers maintain the largest market share at 42.0% of the China specialty fertilizer market size in 2025, supported by established fertigation infrastructure. Liquid fertilizers account for a significant share of the market, offering advantages such as easy plant absorption and compatibility with various application methods, including irrigation and spraying systems. The SRF segment, while smaller in market share, plays a crucial role in providing sustained nutrient release over extended periods, particularly beneficial for long-duration crops. This segmentation pattern reflects underlying agricultural practices and infrastructure development, creating targeted market opportunities for specialized suppliers.

Controlled-release fertilizers emerge as the fastest-growing specialty type at 9.2% CAGR through 2031, driven by government carbon credit pilots and precision agriculture adoption. The CRF segment benefits from technological advances in polymer coating chemistry, with manufacturers developing biodegradable alternatives that meet environmental regulations while maintaining precise nutrient release. Water-soluble fertilizers are well-suited for greenhouse and hydroponic applications, particularly in protected horticulture operations that require precise nutrient control. Regional preferences vary significantly: northern provinces favor CRF for grain production efficiency, while southern regions emphasize liquid formulations for intensive vegetable cultivation.

By Application Mode: Soil Application Gains Momentum

Fertigation emerged as the dominant application mode in China specialty fertilizer market, commanding approximately 47.0% market share in 2025. This significant market position can be attributed to the growing adoption of irrigation agricultural practices and precision agriculture techniques across the country. The segment's prominence is further strengthened by its ability to effectively address challenges such as water scarcity and nutrient deficiencies through minimal water use and precise nutrient delivery. Regulatory compliance factors increasingly influence application mode selection, as GB standards for fertilizer application efficiency favor methods that demonstrate reduced environmental impact and improved nutrient utilization.

Soil application methods are growing at a 8.1% CAGR through 2031, driven by increasing awareness of soil nutrient deficiencies and the adoption of advanced controlled-release fertilizer technologies. This segment is particularly gaining traction due to its effectiveness in strengthening plant root systems and providing sustained nutrient release. The growing popularity of controlled-release fertilizers (CRFs) and slow-release fertilizers (SRFs) is bolstering this segment's expansion, as these products enhance nitrogen use efficiency while reducing excessive nitrogen applications.The soil application segment benefits from advances in variable-rate application equipment and GPS-guided spreaders that optimize nutrient placement without requiring irrigation infrastructure investments.

By Crop Type: Horticultural Surge Reshapes Demand

Field crops maintain a 58.0% of the China specialty fertilizer market share in 2025 due to China's grain security priorities. This segment's prominence is primarily driven by the extensive cultivation of staple crops such as rice, maize, and wheat, which collectively account for over 90% of the nation's food production. The segment's dominance is further reinforced by China's focus on food security and self-sufficiency, which has led to increased adoption of specialty fertilizers to enhance crop yields. Water-soluble and liquid fertilizers are particularly popular in this segment, as these formulations effectively address nutrient deficiencies during critical growth stages. The segment's strength is also attributed to the country's vast agricultural landscape, where field crops occupy about 70.8% of the total cultivated land, with major cultivation zones spread across provinces such as Heilongjiang, Hunan, Jiangxi, and other key agricultural provinces.

Horticultural crops accelerate at 9.0% CAGR through 2031, reflecting dietary transitions toward higher-value produce and corresponding premium fertilization practices. The horticultural segment drives demand for specialized micronutrient formulations and precise application timing, creating opportunities for suppliers with crop-specific expertise and technical advisory capabilities. This segment encompasses a wide range of crops, including vegetables, fruits, and commercial flowers, each requiring specific nutrient management strategies. The segment's importance is underscored by China's position as the world's largest producer of fruits and vegetables, with major growing regions spread across diverse climatic zones. The adoption of horticultural fertilizers in horticultural crops is driven by the need for quality produce, export requirements, and the growing trend toward protected cultivation methods like greenhouse systems and poly houses, where precise nutrient management is essential for optimal yields and quality.

Geography Analysis

China's specialty fertilizer market exhibits pronounced regional variations reflecting agricultural practices, economic development levels, and infrastructure capabilities across provinces. Eastern coastal provinces, including Shandong, Jiangsu, and Guangdong, lead adoption with nearly half of the national specialty fertilizer consumption in 2025, driven by intensive horticulture, advanced irrigation infrastructure, and proximity to manufacturing centers. These regions benefit from higher agricultural incomes, better extension services, and stronger environmental compliance enforcement that favors specialty products over conventional alternatives. Shandong, being one of the major specialty fertilizer-consuming provinces, is supported by its position as China's largest vegetable producer and early adopter of precision agriculture technologies.

Northern provinces demonstrate rapid growth in controlled-release fertilizer adoption, with Hebei, Henan, and Inner Mongolia collectively expanding specialty fertilizer use by 18% annually through precision grain production initiatives. Water scarcity in these regions drives fertigation system adoption, creating concentrated demand for liquid and water-soluble formulations compatible with drip irrigation infrastructure. Government subsidies for high-efficiency fertilizers achieve higher uptake rates in northern grain-producing areas, where large-scale operations and agricultural cooperatives can efficiently navigate subsidy application processes. The region's focus on food security and sustainable intensification aligns with specialty fertilizer value propositions, supporting continued market expansion.

Central and western provinces represent emerging growth opportunities despite current lower adoption rates, as infrastructure development and income growth gradually overcome cost barriers to specialty fertilizer use. Xinjiang's rapid greenhouse expansion creates localized demand spikes for specialized nutrients, while Yunnan's tea and flower cultivation drives customized formulation requirements. Government development programs targeting these regions include agricultural modernization components that favor specialty fertilizer adoption, though implementation timelines extend beyond the current forecast period. Regional supply chain challenges in these areas create opportunities for manufacturers with efficient distribution networks and local technical support capabilities.

Competitive Landscape

The China specialty fertilizer market maintains moderate fragmentation with the top players including Hebei Woze Wufeng Biological Technology Co., Ltd, Yara International ASA, ICL Group Ltd, Henan XinlianXin Chemicals Group Company Limited, and Hebei Monband Water Soluble Fertilizer Co. Ltd. Strategic patterns emphasize vertical integration and technical service capabilities, with leading companies investing in agronomic advisory services, digital agriculture platforms, and direct farmer relationships to differentiate beyond product specifications. Patent activity intensifies around biodegradable coating technologies and precision application systems, reflecting regulatory pressures and sustainability demands that favor companies with advanced R&D capabilities over commodity producers.

A mix of large diversified chemical conglomerates and specialized fertilizer manufacturers characterizes the competitive landscape. While consolidation activities are relatively limited, companies are forming strategic alliances and joint ventures to enhance their market presence. Local manufacturers are increasingly partnering with international companies to access advanced fertilizer technologies and expand their product portfolios, while global players are collaborating with domestic firms to strengthen their distribution networks and market reach.

Success in the Chinese specialty fertilizer market increasingly depends on developing innovative products that address specific regional crop needs while maintaining cost-effectiveness. Companies need to invest in research and development to create products that improve nutrient efficiency and reduce environmental impact. Building strong relationships with agricultural extension services and implementing farmer education programs are becoming crucial for market penetration. Additionally, establishing efficient supply chains and developing digital platforms for technical support and product selection guidance are essential for maintaining competitive advantage.

China Specialty Fertilizer Industry Leaders

Yara International ASA

ICL Group Ltd

Henan XinlianXin Chemicals Group Company Limited

Hebei Monband Water Soluble Fertilizer Co. Ltd

Hebei Woze Wufeng Biological Technology Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Yara International established a joint venture with Sinochem Fertilizer to develop precision agriculture solutions combining specialty fertilizers with digital advisory services, targeting large-scale grain operations and agricultural cooperatives across northern China.

- August 2024: ICL Group announced a USD 170 million five-year distribution agreement with AMP Holdings to expand specialty water-soluble fertilizer availability across China's high-value crop segments, targeting greenhouse vegetables and fruit production with technical advisory support and customized nutrient programs.

- October 2023: Hebei Monband launched a water-soluble fertilizer product line specifically formulated for tea cultivation, targeting premium tea-growing regions in Fujian and Zhejiang provinces with micronutrient-enriched formulations.

China Specialty Fertilizer Market Report Scope

The China Specialty Fertilizer Market is Segmented by Speciality Type (CRF, Liquid Fertilizer, SRF, and Water Soluble), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

Speciality Type

| CRF | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

| Speciality Type | CRF | Polymer Coated |

| Polymer-Sulfur Coated | ||

| Others | ||

| Liquid Fertilizer | ||

| SRF | ||

| Water Soluble | ||

| Application Mode | Fertigation | |

| Foliar | ||

| Soil | ||

| Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf & Ornamental |

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms