China Solid-State Drive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

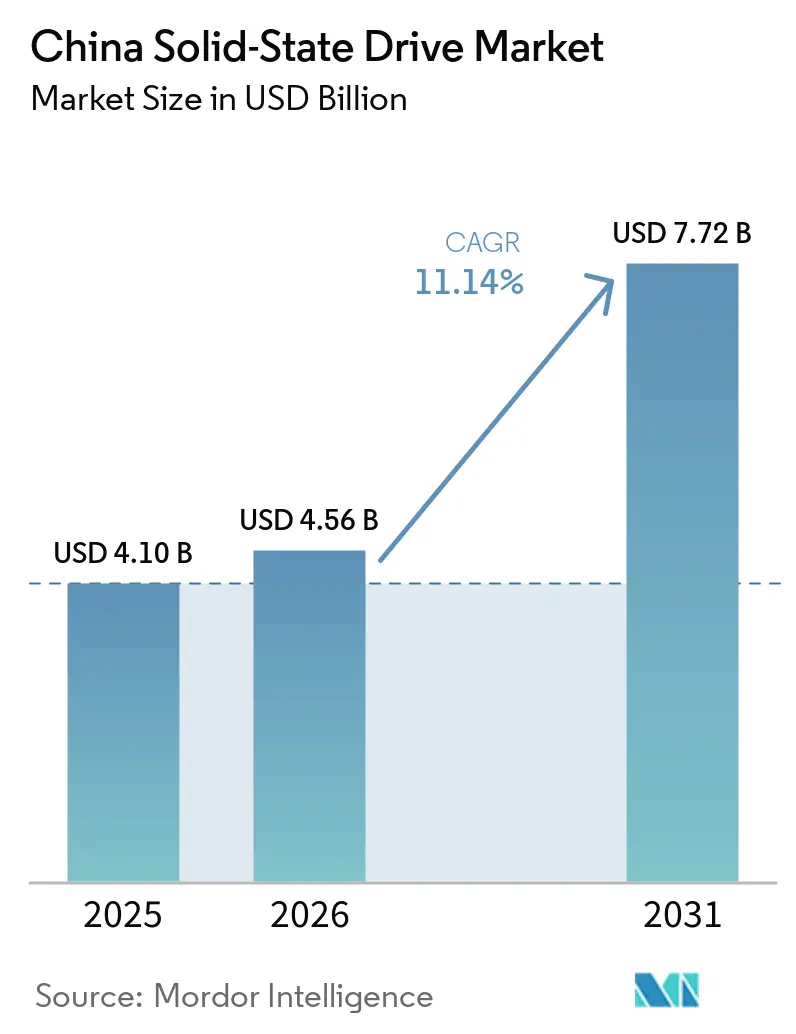

| Base Year Market Size (2025) | USD 4.10 Billion |

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 7.72 Billion |

| Growth Rate (2026 - 2031) | 11.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Solid-State Drive Market Analysis by Mordor Intelligence

The China solid-state drive market size is expected to grow from USD 4.10 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 7.72 billion by 2031 at 11.14% CAGR over 2026-2031. A national push to build more than 20 smart computing centers, combined with the government-backed East-Data-West-Compute program, underpins steady demand for high-performance PCIe/NVMe storage that can feed AI training clusters at scale. Domestic NAND breakthroughs, such as YMTC’s 232-layer Xtacking 4.0, amplify supply security goals while narrowing the technology gap with global leaders. A rapid shift from HDD to SSD in consumer devices, coupled with localization of controller IP, is broadening the revenue base beyond enterprise accounts. Meanwhile, hyperscale and colocation operators are standardizing on emerging E1.S form factors to lower power envelopes and raise rack density. The China solid-state drive market therefore benefits from synchronized policy support, rising AI workloads, and an appetite for advanced interfaces that satisfy latency-sensitive applications. [1]Data Center Knowledge Staff, “China Plans 20 Smart Computing Centers to Hit 300 Exaflops,” Data Center Knowledge, datacenterknowledge.com

Key Report Takeaways

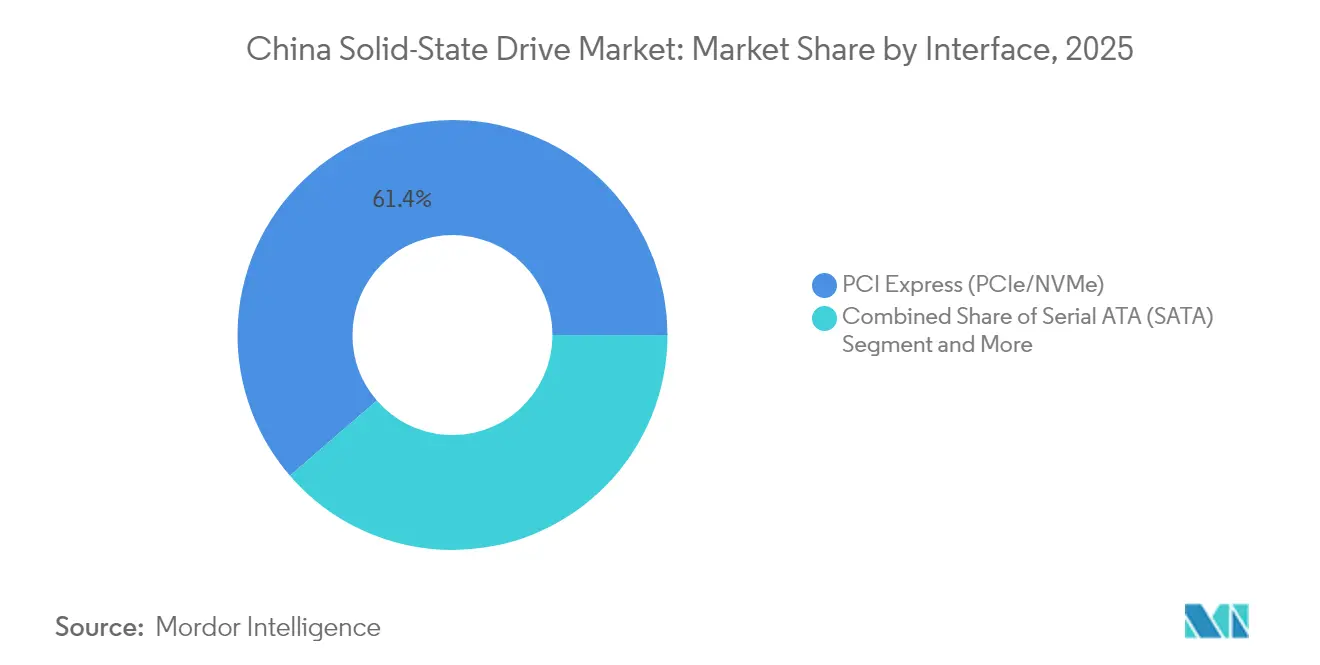

- By interface, PCIe/NVMe held 61.35% of the China solid-state drive market share in 2025 and is rising at a 14.32% CAGR through 2031.

- By form factor, M.2 captured 47.20% revenue share in 2025, while U.2/E1.S is projected to expand at a 15.55% CAGR to 2031.

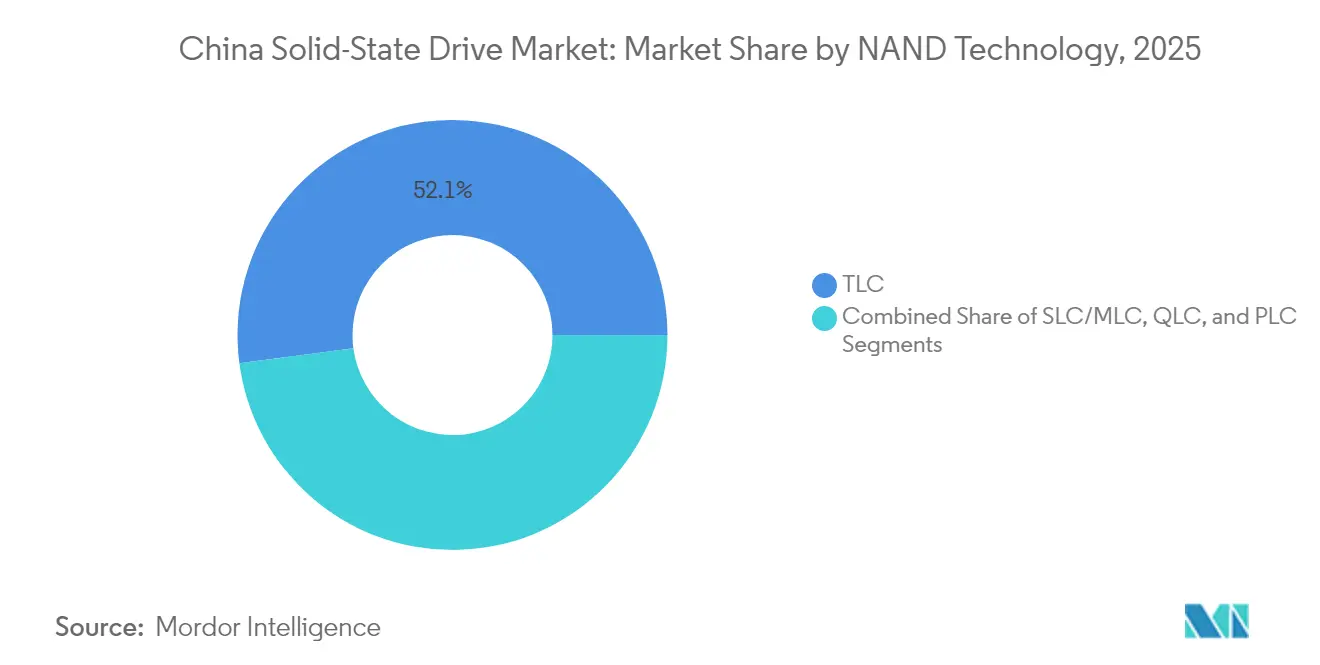

- By NAND technology, TLC accounted for 52.10% of the China solid-state drive market size in 2025; QLC is advancing at an 17.92% CAGR through 2031.

- By application, enterprise deployments represented 57.40% of the market in 2025 and are growing at a 14.74% CAGR.

- By end-user, hyperscale and colocation data centers recorded the fastest CAGR at 16.95% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with China representing one among them. The global report on solid state drive (ssd) market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

China Solid-State Drive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-centre expansion for AI workloads | +3.2% | Beijing-Tianjin-Hebei, Yangtze River Delta, Guangdong-Hong Kong-Macao | Medium term (2-4 years) |

| Shift from HDD to SSD in consumer devices | +2.8% | Tier 1 cities nationwide | Short term (≤ 2 years) |

| “East-Data-West-Compute” build-out | +2.1% | Western clusters: Guizhou, Inner Mongolia, Gansu, Ningxia | Long term (≥ 4 years) |

| Localization of NAND supply chain | +1.9% | Hubei and Jiangsu fabs | Medium term (2-4 years) |

| Edge and in-storage processing for IIoT | +1.4% | Jiangsu, Zhejiang, Guangdong industrial belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-centre Expansion for AI Workloads

China’s AI computing footprint is on track to exceed 300 exaflops by 2025, lifting SSD capacity requirements for model training servers from 30 TB today to 100 TB by decade-end. Kingsoft Cloud’s KS3 Extreme Speed deployment, built on Solidigm QLC devices, already sustains 1 Tbps per petabyte—100× faster than comparable HDD arrays. Inference workloads are expanding even faster, with storage demand forecast to reach 447 exabytes by 2030. Cloud providers are switching to domestically packaged PCIe 5.0 NVMe SSDs to secure supply amid export controls. As a result, the China solid-state drive market enjoys a direct volume lift from every incremental rack of AI servers commissioned. [2]Solidigm Engineering Team, “Kingsoft Cloud Achieves 1 Tbps/ PB With QLC SSDs,” Solidigm, solidigm.com

Shift from HDD to SSD in Consumer Devices

Consumer adoption of SSD-equipped laptops and desktops is accelerating as content-creation workloads move to 4K and 8K formats. Samsung’s Xi’an plant rebounded to 70% utilization in 2024, stabilizing local NAND supply for smartphone OEMs. Domestic player UNIS now ships PCIe 5.0 drives at 14.9 GB/s, narrowing the performance gap with international alternatives while offering cost relief to channel partners. Though pandemic-era PC weakness tempered retail pricing, controlled production schedules signal firmer conditions in late 2025, sustaining the China solid-state drive market’s consumer channel.

East-Data-West-Compute” Government Build-out

The national plan to route eastern data traffic to renewable-rich western sites mobilizes RMB 400-500 billion in infrastructure spend across eight hub nodes. Guizhou and Inner Mongolia are granting subsidized electricity to anchor tenants like Tencent, provided latency budgets stay below 20 ms. Such constraints necessitate high-speed SSD caches for real-time workloads, creating bundled procurement opportunities for domestic vendors. The policy also diversifies the China solid-state drive market beyond coastal metros, lifting long-term volumes in inland provinces.

Localization of NAND Supply Chain

YMTC is processing nearly 500,000 wafers per month on home-grown tooling, and its 232-layer QLC die now leads the world in bit density at 19.8 Gb/mm². Baidu, Alibaba, Tencent, and Huawei have each signed multi-year supply agreements with local module partners to hedge against export-control risk. Although YMTC posted a short-term loss in 2024, fresh capital injections and IP gains underscore a structural pivot toward self-reliance. These developments insulate the China solid-state drive industry from external price shocks and reinforce the broader China solid-state drive market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NAND price-cycle volatility | –2.3% | Nationwide, linked to global supply | Short term (≤ 2 years) |

| Export-control limits on advanced tools | –1.8% | Domestic fabs at 1x nm nodes | Medium term (2-4 years) |

| Power-supply caps for hyperscale DCs | –1.1% | Eastern metros and western hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

NAND Price-cycle Volatility

Spot prices swung sharply in 2024 as weak laptop demand met elevated fab utilization at Kioxia and Western Digital. Chinese tier-2 SSD brands faced squeezed margins, delaying controller upgrades and tightening promotional budgets. Forward contracts with YMTC are emerging as a hedge, but inventory misalignment can still hinder near-term sell-in volumes across the China solid-state drive market.

Export-control Limits on Advanced Tools

The Bureau of Industry and Security’s 2024 rules halted shipments of leading-edge EUV and high-aspect etchers, slowing domestic progress below 1x nm nodes. YMTC and peer fabs have teamed with local equipment makers, yet deposition uniformity and defect control challenges remain. The cost penalty for work-arounds risks dampening the premium tier of the China solid-state drive industry until localized tooling matures. [3]Source: Holland & Knight Trade Group, “U.S. Adds Advanced Chip Tools to Chinese Export Curbs,” Holland & Knight, hklaw.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Interface: PCIe/NVMe Dominance Accelerates Enterprise Adoption

PCIe/NVMe devices accounted for 61.35% of the China solid-state drive market size in 2025 and are on pace for a 14.32% CAGR, propelled by AI clusters that demand low-latency throughput. Enterprise buyers favour PCIe 4.0 and 5.0 lanes to cut training time on transformer models, lifting blended ASPs for domestic suppliers. SATA maintains a toehold in entry-level notebooks, but its share slides each quarter as consumers migrate to PCIe-based laptops. SAS continues in legacy mission-critical arrays where dual-port reliability trumps raw speed. Interface upgrades therefore remain a centerpiece of product differentiation across the China solid-state drive market.

Second-generation PCIe 5.0 controllers from Innogrit and Maxio add co-processing blocks for on-drive AI caching. As ODMs qualify these chips at cloud scale, the China solid-state drive industry unlocks fresh performance tiers without sacrificing power budgets. PCIe 6.0 roadmaps promise double-digit efficiency gains, aligning with the national goal of curbing data-center emissions. These advances reinforce China’s ambition to climb the storage value chain while enlarging export potential for indigenous IP blocks.

By Form Factor: M.2 Leads While U.2/E1.S Emerges for Hyperscale

M.2 modules held 47.20% of the China solid-state drive market share in 2025, favoured by OEMs for thin-and-light designs. Yet the U.2/E1.S category is forecast to grow 15.55% annually through 2031 as hyperscalers prioritize serviceability and airflow in AI racks. E1.S drives support 25 W envelopes, easing thermal throttling in PCIe 5.0 deployments. Their hot-swap convenience accelerates failure recovery, a key metric in cloud SLAs.

Converters from 2.5-inch bays to EDSFF trays are underway at Alibaba’s Zhangbei campus, signalling a migration path for brownfield sites. Meanwhile, add-in-card SSDs retain a niche in specialized accelerator nodes where bandwidth saturation overrides density concerns. Collectively, the form-factor shift exemplifies how rack-level design choices ripple across the China solid-state drive market supply chain.

By NAND Technology: TLC Dominance with QLC Acceleration

TLC drives contributed 52.10% of the China solid-state drive market size in 2025, balancing endurance with economics for mainstream workloads. QLC volumes, though smaller, are compounding at 17.92% as cloud archives and AI data lakes prize cost per bit. YMTC’s 232-layer QLC leapfrogs global density charts, allowing Chinese CSPs to consolidate cold-data tiers without import risk. SLC and MLC retain footholds in aerospace and IIoT gear requiring extreme durability.

Further gains will hinge on controller-side LDPC refinements that mitigate QLC write fatigue. Domestic firmware vendors are experimenting with data-placement AI to extend life cycles, signalling deeper ecosystem maturity in the China solid-state drive industry. Looking forward, prototype PLC dice point to the next capacity node, though volume adoption remains outside the 2030 window.

By Application: Enterprise Growth Outpaces Client Segment

Enterprise deployments delivered 57.40% of 2025 revenue and are expanding at a 14.74% CAGR, fuelled by AI, ERP modernization, and sovereign-cloud mandates. Power-loss protection, smart telemetry, and TCG Opal encryption separate premium SKUs from retail products. Conversely, client drives ride smartphone and gaming cycles; muted handset refreshes in 2024 curbed growth, but deferred demand is set to revive shipments in late 2025.

OEM bundling strategies increasingly tie enterprise SSD orders to domestic server CPU sockets, boosting local value capture. Meanwhile, the client space benefits from PCIe 5.0 trickle-down, giving mid-range notebooks instant-on responsiveness. This dual-track dynamic secures volume resilience across the China solid-state drive market regardless of enterprise cap-ex fluctuations.

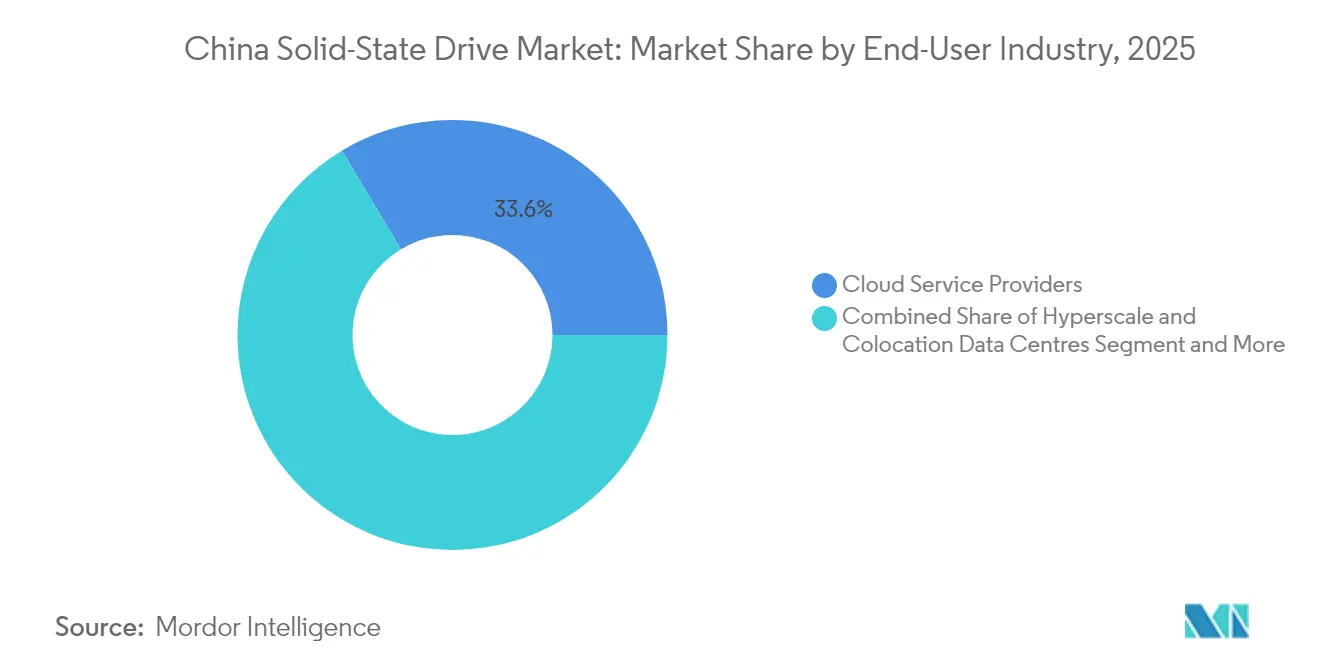

By End-User Industry: Cloud Providers Lead with Hyperscale Acceleration

Cloud service providers accounted for 33.60% of shipments in 2025, yet hyperscale and colocation operators post the fastest 16.95% CAGR on aggressive AI rollouts. Consumer electronics brands absorb large M.2 batches, but their year-over-year swings inject volatility. Industrial automation and edge gateways soak up ruggedized SKUs as factories digitize under Industry 4.0 mandates. Automotive and transport verticals show rising SSD content per vehicle, spanning infotainment caches to ADAS event recording.

Government datacentre projects, often routed through the three state telcos, guarantee anchor orders that stabilize fab loading. Such contracts intertwine with national security guidelines favouring domestic NAND, further anchoring the China solid-state drive market’s structural demand base.

Geography Analysis

Beijing-Tianjin-Hebei, the Yangtze River Delta, and the Greater Bay Area hosting the bulk of AI training clusters and semiconductor assembly plants. These corridors feature robust fiber backbones and proximity to major CSP headquarters, ensuring low latency between compute nodes and end-users. The concentration of OEM notebook lines in Suzhou and Kunshan further boosts regional pull for M.2 modules and controller ICs.

Guizhou, Inner Mongolia, and Gansu—are emerging as green-energy data-center magnets under the East-Data-West-Compute policy. Subsidized hydropower rates and expansive land parcels make these locales ideal for hyperscale campuses, translating into brisk order books for U.2 and E1.S devices. Latency targets below 20 ms necessitate high-speed SSD caching at aggregation nodes, aligning western demand directly with enterprise-grade SKUs in the China solid-state drive market.

Jiangsu, Zhejiang, and Hubei spur IIoT and automotive SSD uptake. YMTC’s Wuhan complex anchors a local ecosystem of packaging houses and firmware design studios, shortening lead times for domestic brands. Cross-provincial shipping lanes streamline supply logistics, enabling just-in-time fulfilment models that minimize channel inventory risk within the China solid-state drive industry.

Competitive Landscape

International suppliers—Samsung, SK Hynix, Western Digital, and Kioxia—retain strong brand equity, but their combined market share has slipped as domestic challengers scale production. YMTC, Kimtigo, and Biwin together surpassed 20% share in 2024, leveraging price-performance parity and quick-turn customization for local buyers. Chinese vendors benefit from policy incentives and shorter design-in cycles, allowing them to pre-load firmware tailored for Mandarin user interfaces and domestic cipher suites.

Strategic moves underscore vertical-integration ambitions. Huawei debuted a magneto-electric disk hybrid that fuses SSD throughput with tape-like capacity for cold archives, cutting energy usage by 90% in internal benchmarks. YMTC filed nearly 20 patents in early 2025 covering stacked-die EMI shielding and interconnect optimizations, signalling RandD depth. On the international front, Kioxia’s 122.88 TB LC9 NVMe SSD targets AI multitenancy scenarios, positioning the firm for ultra-high-density racks. [4]Tom’s Hardware China Desk, “Singles’ Day Sees Domestic SSD Vendors Overtake Samsung,” Tom’s Hardware, tomshardware.com

MandA plays are reshaping the landscape. Hygon and Dawning’s 2025 merger creates an end-to-end stack from x86-compatible CPUs to storage subsystems, promising tighter optimization for China-built servers. As domestic fabs scale, price overlap with imported drives narrows, intensifying competition. The moderate concentration level points to further consolidation waves as firms chase capacity synergies and controller IP portfolios to sustain differentiation within the China solid-state drive market.

China Solid-State Drive Industry Leaders

Samsung Electronics Co., Ltd.

Yangtze Memory Technologies Co., Ltd.

Kingston Technology Company, Inc.

Western Digital Corporation

SK Hynix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hygon Information Technology and Dawning Information Industry announced an all-share merger to integrate chip design and server manufacturing, targeting 53.6% domestic server CPU share.

- March 2025: KIOXIA introduced the LC9 Series 122.88 TB NVMe SSD built on BiCS FLASH Gen 8 3D NAND.

- March 2025: UNIS launched its S5 PCIe 5.0 SSD line hitting 14.9 GB/s sequential reads.

- January 2025: China’s Semiconductor Industry Association revised chip-origin rules to prioritize wafer-fab location in tariff codes.

China Solid-State Drive Market Report Scope

The SSD functions as secondary storage for the computer using integrated circuit assemblies to store data. The Chinese solid-state drive market comprises Serial Advanced Technology Attachment (SATA) and Peripheral Component Interconnect (PCI) Express used by clients from enterprise and consumer goods. The market study provides a detailed analysis of SSDs in the Chinese market and the several growth opportunities and challenges faced by the regional vendors. The market also provides a brief analysis of the impact of Covid-19 on the market studied.

The Chinese Solid-state Drive Market is segmented by Application (Enterprise and Clients) and Interface (Serial Advanced Technology Attachment (SATA) and Peripheral Component Interconnect (PCI) Express).

The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

| Serial ATA (SATA) |

| PCI Express (PCIe/NVMe) |

| Serial-Attached SCSI (SAS) |

| USB/Other Embedded |

| 2.5-inch Drives |

| M.2 Modules |

| U.2 / E1.S |

| Add-in Cards |

| SLC / MLC |

| TLC |

| QLC |

| PLC (Prototype) |

| Enterprise |

| Client |

| Cloud Service Providers |

| Hyperscale & Colocation Data Centres |

| Consumer Electronics OEMs |

| Industrial & Manufacturing |

| Automotive & Transportation |

| Aerospace & Defence |

| By Interface | Serial ATA (SATA) |

| PCI Express (PCIe/NVMe) | |

| Serial-Attached SCSI (SAS) | |

| USB/Other Embedded | |

| By Form Factor | 2.5-inch Drives |

| M.2 Modules | |

| U.2 / E1.S | |

| Add-in Cards | |

| By NAND Technology | SLC / MLC |

| TLC | |

| QLC | |

| PLC (Prototype) | |

| By Application | Enterprise |

| Client | |

| By End-User Industry | Cloud Service Providers |

| Hyperscale & Colocation Data Centres | |

| Consumer Electronics OEMs | |

| Industrial & Manufacturing | |

| Automotive & Transportation | |

| Aerospace & Defence |

Key Questions Answered in the Report

What is the current value of the China solid-state drive market?

The market stands at USD 4.56 billion in 2026.

How fast is the China solid-state drive market expected to grow?

Revenue is projected to rise at an 11.14% CAGR, reaching USD 7.72 billion by 2031.

Which interface leads the China solid-state drive market?

PCIe/NVMe drives hold 61.35% market share and grow at 14.32% CAGR through 2031.

Why is QLC NAND gaining traction in China?

QLC’s lower cost per bit suits AI data lakes and archival storage, driving an 17.92% CAGR for this technology.

How does the East-Data-West-Compute policy influence demand?

It shifts data-center construction to western provinces, boosting orders for enterprise-grade SSDs that meet latency targets.

Which end-user segment shows the fastest SSD adoption?

Hyperscale and colocation data centers exhibit the highest growth at 16.95% CAGR, fuelled by AI training workloads.

Page last updated on: