Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

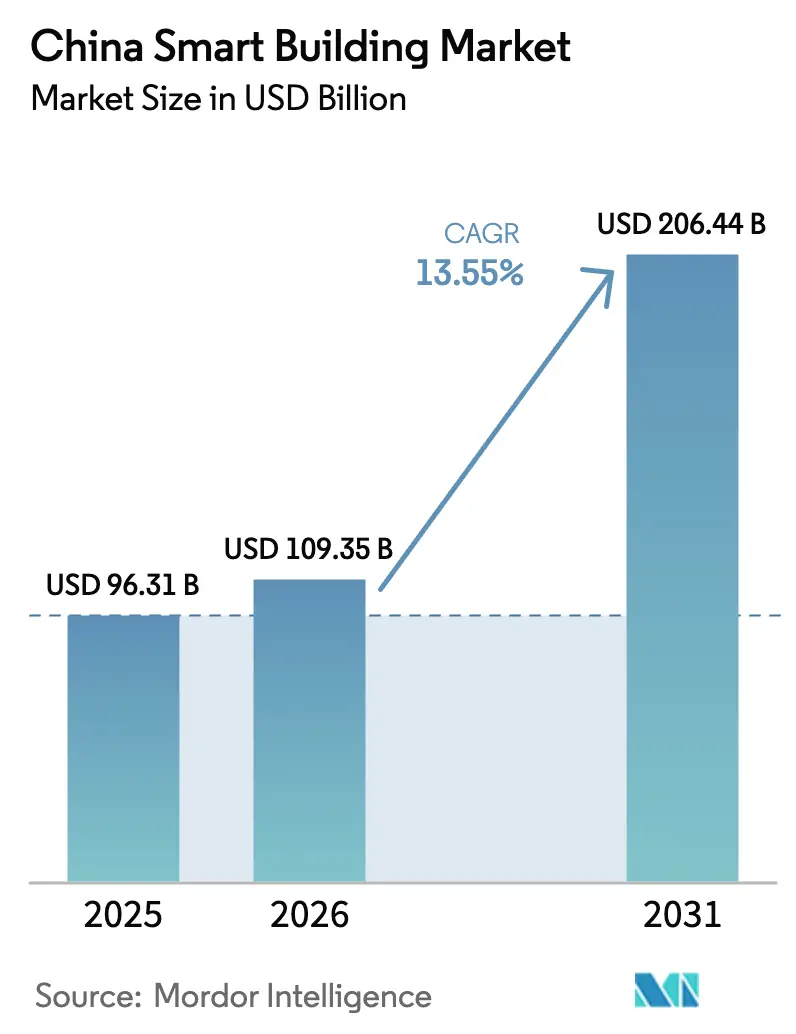

| Base Year Market Size (2025) | USD 96.31 Billion |

| Market Size (2026) | USD 109.35 Billion |

| Market Size (2031) | USD 206.44 Billion |

| Growth Rate (2026 - 2031) | 13.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Smart Building Market Analysis by Mordor Intelligence

The China smart building market size is expected to grow from USD 96.31 billion in 2025 to USD 109.35 billion in 2026 and is forecast to reach USD 206.44 billion by 2031 at 13.55% CAGR over 2026-2031. Strong policy backing, generous green-finance lines, and rapid 5G rollout are transforming intelligent buildings from optional upgrades into mandated infrastructure that supports Beijing’s digital economy agenda. Mandatory energy-performance disclosure for large commercial properties, expanded carbon-reduction lending at 1.75% interest, and city-level digital-twin platforms are converging to create a compliance-driven adoption cycle. Telecom operators and automation giants are repositioning themselves as platform players, while domestic software specialists are capturing analytics layers by embedding into municipal data exchanges. Early movers benefit from network effects that raise switching costs, while lagging small and medium-sized enterprises (SMEs) face capital and skills barriers that slow the broader diffusion.

Key Report Takeaways

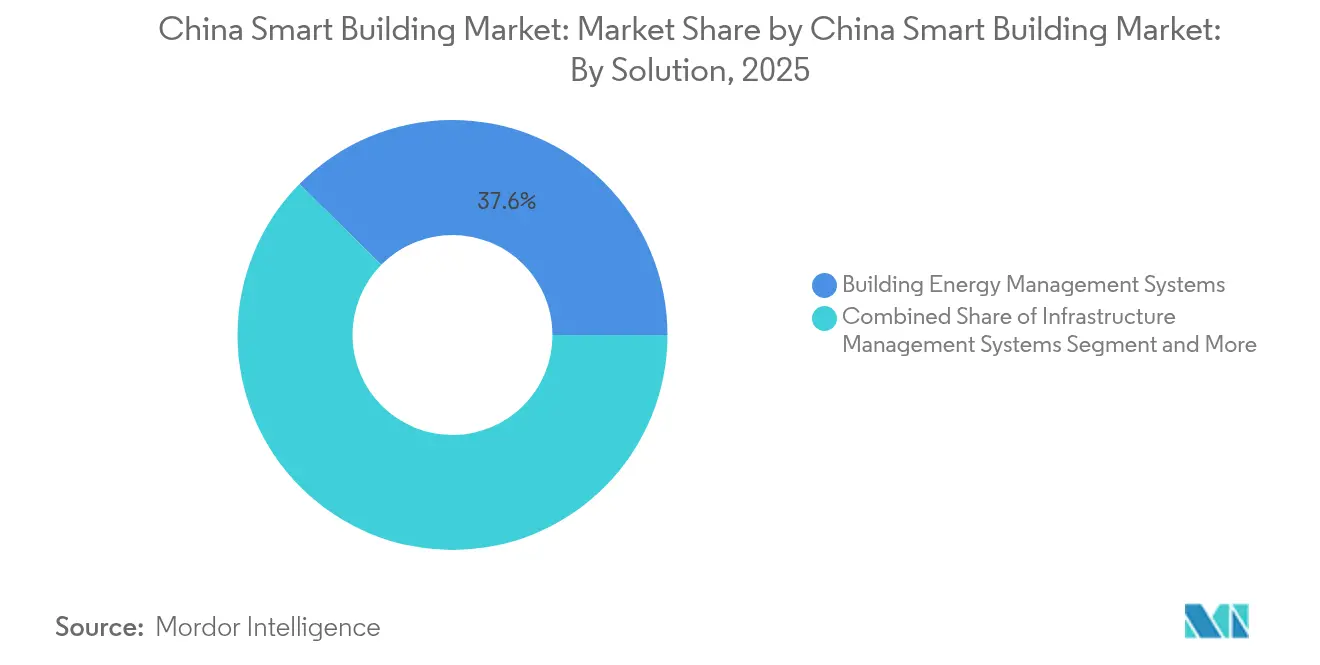

- By solution, building energy management systems led with 37.62% of the China smart building market share in 2025, while integrated workplace management platforms are forecast to expand at a 15.12% CAGR through 2031.

- By component, hardware accounted for 54.88% share of the China smart building market size in 2025 and services are advancing at a 13.95% CAGR to 2031.

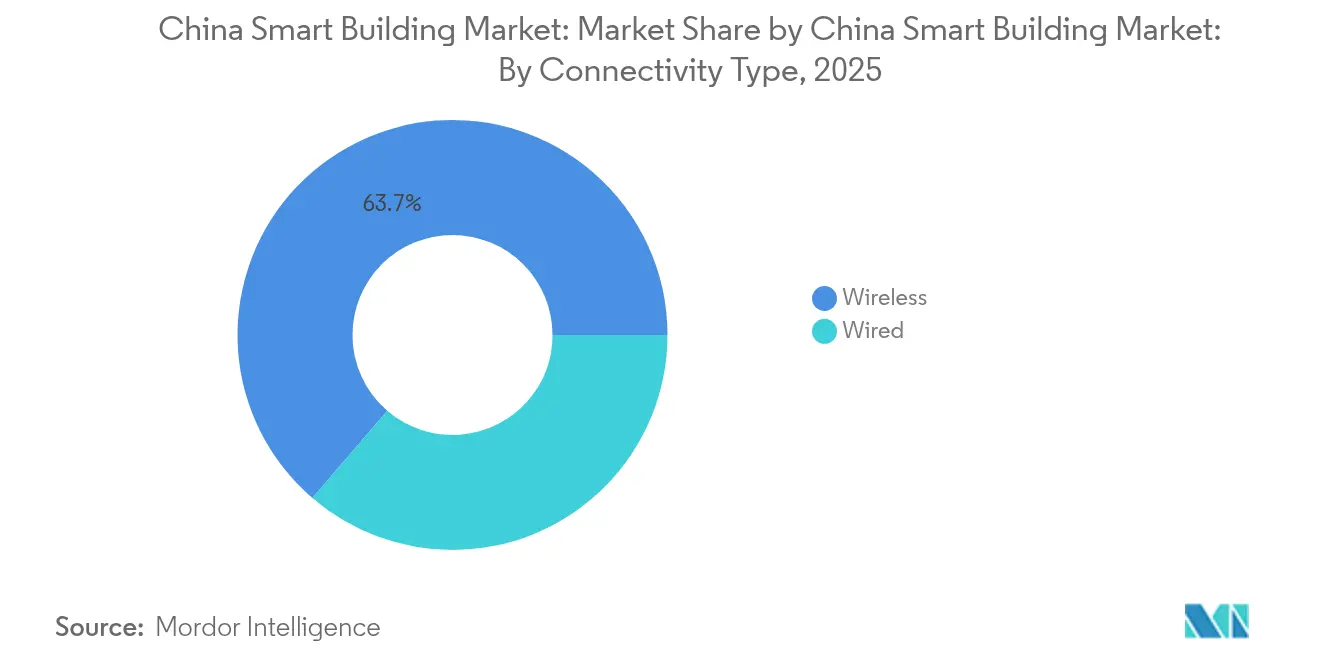

- By connectivity type, wireless technology commanded 63.70% share of the China smart building market size in 2025 and is poised to grow at a 14.42% CAGR through 2031.

- By building type, commercial facilities held 43.95% of the China smart building market share in 2025, whereas industrial buildings are projected to register the highest 15.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Smart Building Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Government Smart City Initiatives | +3.2% | National clusters such as Beijing-Tianjin-Hebei, Yangtze River Delta, Pearl River Delta, Chengdu-Chongqing | Medium term (2-4 years) |

| Rising Demand for Energy-Efficient Retrofits in Existing Buildings | +2.8% | Tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Integration of 5G and AIoT Platforms in Building Automation | +2.5% | Major urban centers with 5G-Advanced | Medium term (2-4 years) |

| Growing Corporate Net-Zero Carbon Commitments | +2.1% | Commercial real estate and industrial parks in eastern provinces | Long term (≥ 4 years) |

| Rapid Growth of Smart Property Management Services | +1.6% | Residential complexes in tier-1 and new-development zones | Short term (≤ 2 years) |

| Emergence of Digital Twin-Based Urban Planning Mandates | +1.5% | 16 smart-city demonstration zones and provincial capitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Government Smart City Initiatives

Beijing’s 2024 guideline commits CNY 1.2 trillion (USD 165 billion) through 2027 to digitalize municipal services, treating smart buildings as core infrastructure alongside 5G and data centers. The directive covers 16 demonstration zones and requires new public buildings above 10,000 m² to connect with city data platforms by 2026. Compliance timetables are driving a surge in turnkey projects, favoring vendors able to integrate automation, security, and energy modules under a single architecture. Local governments tie subsidy eligibility to adherence with the Ministry of Housing’s 2024 smart-building technical specification, effectively raising market-entry barriers.[1]Ministry of Housing and Urban-Rural Development, “Technical Specification for Smart Building Evaluation,” MOHURD.GOV.CNAs a result, the Chinese smart building market experiences policy-induced demand certainty even amid broader real-estate volatility.

Rising Demand for Energy-Efficient Retrofits in Existing Buildings

Roughly 60% of China’s building stock predates the 2010 energy codes, representing more than 20 billion square meters of retrofit potential.[2]National Development and Reform Commission, “Action Plan for Carbon Peaking in Urban and Rural Construction,” NDRC.GOV.CNThe carbon peaking plan targets a 15% reduction in operational emissions by 2030, with retrofits accounting for half of the reduction. The People’s Bank of China extended its carbon-reduction facility to cover building energy-management projects at an interest rate of 1.75%, trimming payback periods for landlords. Fourteen provinces now require energy-performance disclosure at lease renewal, creating rental premiums for smart-enabled assets, as seen in Shanghai, where automated buildings achieved 8-12% higher rents in 2024. These incentives convert energy systems from cost centers into revenue enhancers, sustaining double-digit uptake across the Chinese smart building market.

Integration of 5G and AIoT Platforms in Building Automation

5G-Advanced coverage in over 95% of prefecture-level cities by mid-2024 removes wiring cost barriers that once limited retrofit projects. Telecom operators collaborate with automation firms to deliver unified 5G cores that support security, lighting, and HVAC on a single network. Huawei’s campus solution, certified in 127 cities, combines low-latency 5G with edge analytics to cut installation times and enable real-time control of elevators and fire systems. The Ministry of Industry and Information Technology’s 2024 AIoT guideline allocates dedicated spectrum for building applications, boosting reliability, and accelerating uptake.[3]Ministry of Industry and Information Technology, “Guideline on AIoT Standardization,” MIIT.GOV.CN These developments reinforce wireless as the default connectivity model, thereby strengthening the trajectory of the Chinese smart building market.

Growing Corporate Net-Zero Carbon Commitments

Listed developers and industrial-park operators now embed net-zero goals into tenant contracts, aligning private capital with national decarbonization goals. Multinational manufacturers in the Yangtze River Delta require smart logistics and energy monitoring to meet Science Based Targets initiative benchmarks, pulling digital infrastructure deeper into supply chains. Energy-as-a-service contracts, in which vendors guarantee savings, appeal to fleet-wide portfolios seeking predictable returns. The move links enterprise sustainability strategies with city-level digital-twin models, making building data a strategic asset. As carbon reporting hardens, smart-enabled facilities become prerequisites for financing from state and commercial banks that now price loans on emissions-intensity metrics, broadening the China smart building market base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for SMEs | -1.8% | Tier-2 and tier-3 cities with SME ownership | Short term (≤ 2 years) |

| Fragmented Building Communication Protocols | -1.3% | National retrofit projects | Medium term (2-4 years) |

| Data Privacy and Cyber-Security Compliance Gaps | -0.9% | Government and financial buildings | Short term (≤ 2 years) |

| Shortage of Certified Smart-Building Facility Managers | -1.1% | Tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for SMEs

Comprehensive smart retrofits cost up to USD 200 per m², a hurdle for SMEs that hold 40% of commercial floor area but earn rental yields of only 4-6%. Commercial lending rates of 4.5-6.0% neutralize central-bank concessional lines reserved for state developers, stretching paybacks to 8-12 years. Subsidies covering 20-30% of costs in Zhejiang and Guangdong ease the burden yet remain confined to pilot budgets. As a result, the China smart building market shows bifurcation: tier-1 portfolios digitize rapidly while fragmented SME assets lag. Vendors are responding by offering modular kits, phased rollouts, and revenue-sharing energy contracts, but capital friction persists as a structural brake on nationwide penetration.

Shortage of Certified Smart-Building Facility Managers

The country is estimated to lack 150,000 certified operators capable of operating AI-driven platforms.[4]China Association of Building Energy Efficiency, “Workforce Assessment Report on Smart Building Facility Managers,” CABEE.ORGThe annual graduation of fewer than 30,000 managers under the 2024 national certification program cannot keep pace with double-digit market growth. Skill gaps lead to under-commissioned systems, as Chengdu audits revealed that 40% of automated HVAC installations were missing projected savings. Shortfalls are most acute in Tier 2 and Tier 3 cities, amplifying regional disparities within the China smart building market. Managed services and vendor-run command centers are emerging to fill the void, but scarcity continues to constrain optimal returns on installed technology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Energy Management Dominates Amid Workplace Platform Surge

Building energy management systems captured 37.62% of the Chinese smart building market share in 2025, supported by disclosure rules for properties above 20,000 m². Vendors bundle HVAC, lighting, and solar assets into algorithms that track weather and occupancy patterns, pushing the segment toward outcome-based contracts. Sliding hardware margins facilitate a shift to subscription models that ensure energy savings. Integrated workplace management, though smaller, is advancing at a 15.12% CAGR, helped by hybrid work trends and landlord demand for real-time space analytics. China Resources Land rolled out workplace dashboards across 2.8 million square meters in 2024, reducing tenant space by up to 20% and validating the segment’s value proposition.

Energy, security, and workplace modules increasingly converge on a single data layer. Infrastructure management systems offer steady if slower growth tied to new-build volume. Security remains essential amid rising compliance requirements for visitor tracking, but privacy curbs limit the use of facial recognition in residential complexes. Lighting controls fold into energy platforms, with LED retrofits serving as entry points for broader automation. Cross-domain vendors that can stitch multiple functions together are best positioned to win bundled tenders across the Chinese smart building market.

By Component: Hardware Saturation Accelerates Services Shift

Hardware generated 54.88% of 2025 revenue, yet it is losing pricing power as sensor and controller costs decline. Wireless 5G sensors further erode gateway demand, pressuring manufacturers that lack proprietary technology. Software layers, analytics, operating systems, and cyber-defense rise in strategic weight as clients seek insight rather than raw data. Subscription pricing, exemplified by Siemens Desigo CC, smooths cash flow and deepens stickiness.

Services, the smallest component in 2025, are on track for the fastest 13.95% CAGR through 2031. Integration complexity around legacy systems fuels demand for specialist integrators, while SMEs outsource operations to managed-service providers. Johnson Controls’ OpenBlue bookings in China increased by 40% in 2024 under outcome-based contracts, demonstrating the acceptance of performance guarantees. As monetization shifts from one-off hardware sales to life-cycle services, vendors with dense local support networks gain market share across the entire China smart building market spectrum.

By Connectivity Type: Wireless Dominance Driven by Retrofit Economics

Wireless connections accounted for 63.70% of revenue in 2025 and are expected to expand at a 14.42% CAGR. Retrofit projects avoid the 3-5 times extra cost of rewiring by adopting 5G-Advanced, whose ultra-reliable, low-latency performance now meets fire safety and elevator codes. Spectrum reserved for industrial IoT reduces interference risk, making wireless the default for new builds as well. Huawei’s campus deployments demonstrate how a unified 5G core can support automation, security, and energy traffic without requiring proprietary cabling.

Wired options persist only in mission-critical or cyber-sensitive sites, such as data centers and nuclear plants. Even there, hybrid topologies are emerging, with wired backbones feeding wireless edge devices. Vendors must master wireless-first designs without abandoning backward compatibility, a duality that favors incumbents familiar with decades of installed wired systems in the Chinese smart building market.

By Building Type: Industrial Segment Accelerates on Emissions Compliance

Commercial properties accounted for 43.95% of 2025 revenue, owing to concentrated ownership, strong tenant expectations, and green lease clauses. Residential adoption lags due to fragmented ownership, but grows in premium and subsidized projects tied to energy mandates. Industrial facilities, although smaller, are expected to achieve the highest 15.05% CAGR as factories install real-time energy and environmental monitoring systems to meet provincial carbon caps. Suzhou Industrial Park requires factories above 50,000 m² to install monitoring by 2026, catalyzing vendor pipelines.

Industrial projects prioritize rugged hardware, hazardous-area certifications, and integration with manufacturing execution systems. They also deliver demonstrable operational benefits, such as 20-30% reductions in downtime through the use of predictive maintenance. Vendors with an industrial-automation heritage enjoy an edge, but telecom-driven platforms are making inroads by offering unified networks that simplify site infrastructure, thereby broadening the customer base of the Chinese smart building market.

Geography Analysis

The Yangtze River Delta, Pearl River Delta, and Beijing-Tianjin-Hebei regions accounted for 61.30% of 2025 installations, supported by strong fiscal budgets, dense commercial stock, and robust telecom grids. Shanghai mandates three-star green certification for new commercial buildings above 20,000 m² by 2025, driving over 180 smart projects in 2024 alone. Shenzhen, with its technology cluster, acts as a test bed for digital twins and AI optimization, accelerating vendor learning cycles.

Chengdu-Chongqing is emerging as the inland growth pole, buoyed by central government investment and ambitions to become a smart manufacturing hub. Tier 2 and Tier 3 cities represent the next frontier, driven by ongoing urbanization and the diffusion of policy. However, fragmented ownership, high capital costs, and skills shortages delay adoption. Zhejiang and Guangdong subsidies mitigate entry costs but remain limited in scale. The October 2024 digital-twin mandate for districts exceeding 5 km² is likely to spur secondary-city projects as local governments compete for demonstration-zone status, thereby expanding the geographic footprint of the Chinese smart building market.

Domestic vendors leverage local ties and cost structures to win in secondary markets where global rivals face higher go-to-market expenses. Huawei’s certification in 127 prefecture-level cities demonstrates how telecom players leverage municipal infrastructure budgets to expand their reach. Regional integrators that blend global hardware with local software thrive under a hybrid model, tailoring solutions to local codes and budgets. Manufacturing-intensive provinces such as Jiangsu and Shandong benefit from the June 2024 AIoT spectrum allocation, which encourages industrial adoption and diversifies the Chinese smart building market landscape.

Competitive Landscape

The China smart building market is moderately fragmented, with top-10 vendors controlling a majority of the 2024 revenue, while regional integrators and niche software houses split the remainder. Global stalwarts—Honeywell, Johnson Controls, Siemens, Schneider Electric- rely on HVAC and fire-safety heritage to anchor large projects. Yet, domestic platforms capture middleware and analytics by aligning with cybersecurity and data localization mandates. Huawei’s 5G-centric architecture integrates networking, automation, and energy layers, compelling traditional control vendors to shift toward AI and cloud services or risk margin compression.

Skills shortages and SME capital gaps create opportunities for turnkey providers that bundle financing, installation, and multi-year operations. Firms that build training academies and intuitive dashboards reduce the expertise hurdle and secure recurring revenue. Patent filings in building automation reached record levels in 2024, with Chinese applicants holding 68% of global submissions, intensifying technology races. The contest now revolves around platform control rather than component differentiation, echoing earlier battles in the enterprise IT sector. Vendors able to position their software as the default operating system for buildings will capture network effects that reinforce incumbency across the China smart building market.

China Smart Building Industry Leaders

Huawei Technologies Co., Ltd.

Johnson Controls International plc

Schneider Electric SE

Siemens Aktiengesellschaft

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MECOM and Beijing CABR Building Maintenance Machinery Technology Co., Ltd signed a strategic cooperation agreement. According to the agreement, MECOM will produce a series of highly complex intelligent facade access systems tailored for skyscrapers, hotels, and various types of high-rise buildings.

- November 2024: Schneider Electric unveiled a CNY 1.2 billion collaboration with China Vanke to deploy EcoStruxure across 80 million m² by 2027.

- October 2024: Siemens partnered with China State Construction Engineering Corporation to roll out Desigo CC across 50 million m² in 20 cities by 2027.

China Smart Building Market Report Scope

The study characterizes the smart building market based on the solution and building type. Solutions that automate and optimize the building's operations and performance are studied. A smart building is a building that automates its processes to control its infrastructure, lighting, security systems, heating, ventilation, air conditioning systems, and more.

The China Smart Building Industry Report is Segmented by Solution (Building Energy Management Systems, Infrastructure Management Systems, Intelligent Security Systems, Integrated Workplace Management Platforms, Lighting Control Systems), Component (Hardware, Software, Services), Connectivity Type (Wired, Wireless), Building Type (Residential, Commercial, Industrial), and Geography (China). Market Forecasts are Provided in Terms of Value (USD).

By Solution

| Building Energy Management Systems |

| Infrastructure Management Systems |

| Intelligent Security Systems |

| Integrated Workplace Management Platforms |

| Lighting Control Systems |

By Component

| Hardware |

| Software |

| Services |

By Connectivity Type

| Wired |

| Wireless |

By Building Type

| Residential |

| Commercial |

| Industrial |

| By Solution | Building Energy Management Systems |

| Infrastructure Management Systems | |

| Intelligent Security Systems | |

| Integrated Workplace Management Platforms | |

| Lighting Control Systems | |

| By Component | Hardware |

| Software | |

| Services | |

| By Connectivity Type | Wired |

| Wireless | |

| By Building Type | Residential |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

How large is the China smart building market in 2026?

The China smart building market size stands at USD 109.35 billion in 2026.

What is the projected growth rate for China’s smart building sector to 2031?

The market is set to expand at a 13.55% CAGR, reaching USD 206.44 billion by 2031 over 2026-2031.

Which solution leads current adoption?

Building energy management systems command 37.62% of 2025 revenue, driven by carbon-intensity rules.

Why are wireless networks gaining share in building automation?

5G-Advanced coverage cuts retrofit wiring costs and offers low-latency reliability, giving wireless 63.70% share in 2025.

Page last updated on: