China Crustaceans Market Analysis by Mordor Intelligence

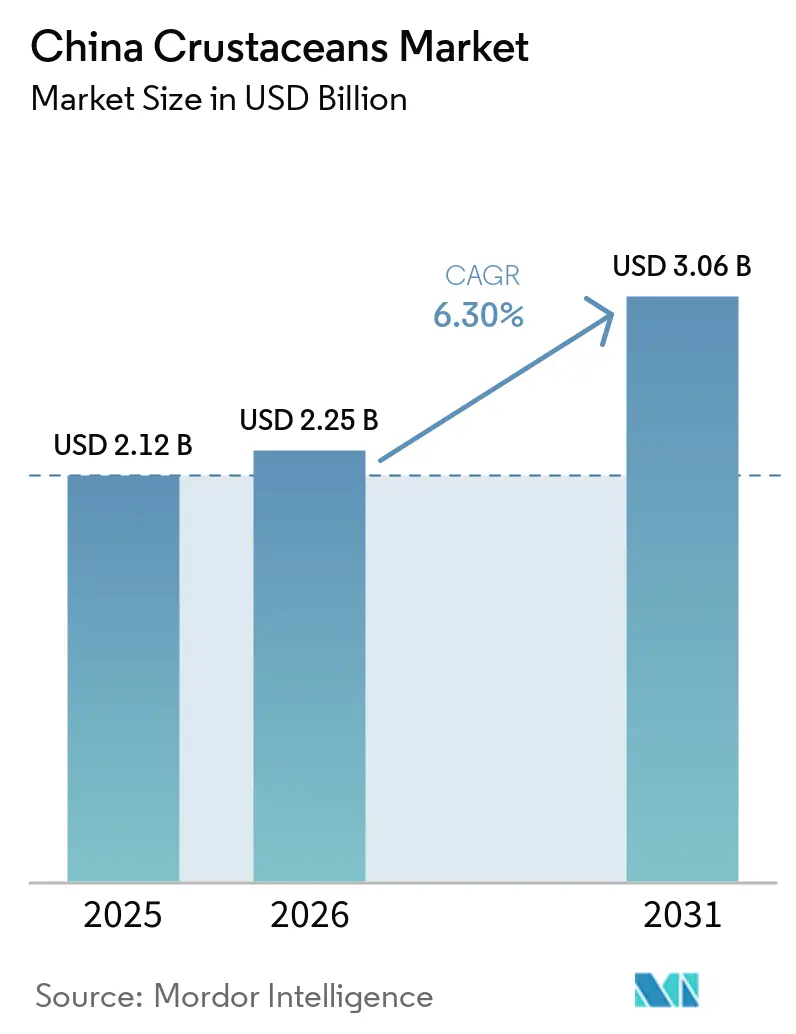

The China crustaceans market size is projected to grow from USD 2.12 billion in 2025 to USD 2.25 billion in 2026, and to USD 3.06 billion by 2031, at a CAGR of 6.3% from 2026 to 2031. This growth is driven by rising middle-class consumers shifting from low-value bulk seafood to more convenient, value-added shrimp and crayfish products. This shift is enhancing price realization per kilogram, despite farming areas facing challenges from stricter environmental regulations on groundwater use and effluent discharge implemented in recent years. Additionally, domestic production is impacted by biological challenges, particularly disease outbreaks, which have periodically disrupted supply and increased reliance on imports to stabilize the market. Companies adhering to internationally recognized certifications, such as the Aquaculture Stewardship Council (ASC) and Best Aquaculture Practices (BAP), are increasingly favored by modern retail chains, reflecting heightened consumer awareness of quality, traceability, and sustainability.

Key Report Takeaways

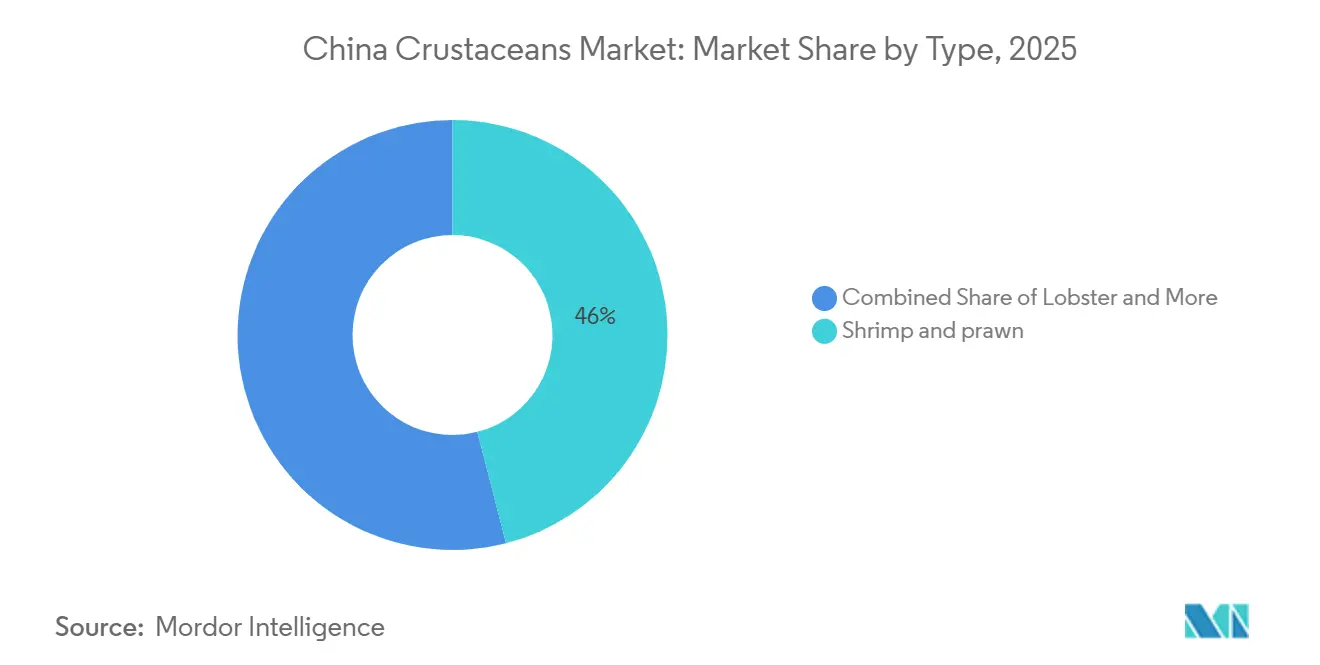

- By type, China's crustaceans market share for the shrimp and prawn segment accounted for the largest 46.0% in 2025, while China's crustaceans market size for the lobster segment is projected to grow at the fastest CAGR of 8.8% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Crustaceans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incomes boost crustacean consumption | +1.2% | National, strongest in Beijing, Shanghai, Guangzhou, and Chengdu | Medium term (2–4 years) |

| Government incentives for modern aquaculture clusters | +0.8% | Jiangsu, Zhejiang, Guangdong, Hainan, Sichuan, and Chongqing | Long term (≥ 4 years) |

| Rapid adoption of recirculating aquaculture systems (RAS) | +0.9% | Jiangsu, Fujian, and Guangdong | Medium term (2–4 years) |

| Expansion of cold-chain logistics and e-commerce seafood platforms | +1.1% | Highest density in Yangtze River and Pearl River deltas | Short term (≤ 2 years) |

| Emergence of probiotic-enriched and functional crustacean products | +0.6% | Research hubs in Qingdao, Xiamen, and Zhanjiang | Long term (≥ 4 years) |

| Rising demand for sustainably certified seafood | +0.7% | Guangdong, Fujian, Zhejiang, and Tier-1 retail | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Incomes Boost Crustacean Consumption

Increasing disposable income and changing urban consumption patterns are driving the demand for premium crustaceans, such as shrimp and crayfish. According to China's National Bureau of Statistics, per capita disposable income reached CNY 41,314 (USD 5,807) in 2024, reflecting a 5.3% increase compared to the previous year[1]Source: The State Council of the People's Republic of China, “China's Economy Expands 5% in 2024,” gov.cn. The rise in household purchasing power is encouraging consumers to allocate more of their spending to premium protein sources, including high-quality seafood products. Consequently, higher expenditure on fresh, value-added, and traceable crustacean products is contributing to stronger consumption growth and enhancing value realization in the China crustaceans market.

Government Incentives for Modern Aquaculture Clusters

Government support is driving the advancement of modern aquaculture systems in China through initiatives promoting technological upgrades and large-scale production. According to the Ministry of Agriculture and Rural Affairs of China, the country's aquatic product output reached 73.66 million metric tons in 2024, representing a 3.5% year-on-year increase[2]Source: Ministry of Agriculture and Rural Affairs of the People's Republic of China, “China's Fishery Economy Remained Stable and Improved in 2024,” moa.gov.cn.. This growth highlights ongoing investments in aquaculture modernization and production efficiency. The adoption of advanced farming systems and improved infrastructure is contributing to supply stability and enabling higher-output crustacean farming. Consequently, government-backed development programs are enhancing production capacity and fostering long-term growth in the Chinese crustaceans market.

Rapid Adoption of Recirculating Aquaculture Systems (RAS)

Technology-driven aquaculture expansion in China is advancing rapidly with the growing adoption of recirculating aquaculture systems (RAS), particularly in intensive shrimp and fish farming. According to Seafoodsource, in 2024, some RAS facilities achieve up to five production cycles per year, a significant improvement compared to traditional pond systems[3]Source: SeafoodSource, “Chinese RAS Boom Driven by Investment and Sustainability Trends,” seafoodsource.com. This productivity advantage is driving substantial investments in controlled-environment aquaculture, enhancing yield efficiency and minimizing environmental risks. Consequently, the adoption of RAS is bolstering production resilience, ensuring consistent supply, and facilitating the shift toward high-efficiency crustacean farming systems across China.

Expansion of Cold-Chain Logistics and E-Commerce Seafood Platforms

Cold-chain infrastructure and digital commerce are improving the efficiency of seafood distribution across China by enabling faster, broader delivery of perishable products. According to the International Institute of Refrigeration, China's total cold storage capacity reached 277 million cubic meters in 2025, with 3.5 million cubic meters added in the fourth quarter. This marks a 5.53% year-on-year increase, highlighting ongoing investments in temperature-controlled logistics systems. This growth enables efficient storage and transportation of fresh and frozen seafood, including crustaceans, across various regions in the country.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring disease outbreaks | -0.9% | Guangdong, Fujian, and Jiangsu | Short term (≤ 2 years) |

| Volatile feed costs tied to soybean and fishmeal prices | -0.8% | National, cost pass-through highest in exporters | Medium term (2–4 years) |

| Stricter effluent discharge and environmental compliance costs | -0.6% | Jiangsu, Zhejiang, Guangdong, and Hainan | Long term (≥ 4 years) |

| Uncertain trade policies in key export destinations | -0.5% | Guangdong, Fujian, and Shandong | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Recurring Disease Outbreaks

Disease outbreaks pose significant challenges to crustacean farming in China, disrupting production cycles and decreasing farm-level efficiency. A 2025 review published in Viruses jorunal highlights that White Spot Syndrome Virus (WSSV) can lead to cumulative mortality rates of up to 100% in infected shrimp populations within 3–10 days, making it one of the most destructive pathogens in crustacean aquaculture. These severe disease risks compel farmers to invest in biosecurity measures, health monitoring, and water treatment systems, thereby increasing operating costs. Recurring outbreaks undermine production predictability and create supply uncertainties, hindering sustainable growth in the Chinese crustaceans market.

Volatile Feed Costs Tied to Soybean and Fishmeal Prices

Feed cost volatility poses a significant challenge for China’s crustacean farming industry due to the heavy reliance of aquaculture feed formulations on fishmeal and soybean meal. According to the Food and Agriculture Organization of the United Nations, China accounted for 40% of global fishmeal imports in 2024, importing 771,000 metric tons from Peru during the first nine months of that year. This figure is more than double the 360,000 metric tons imported during the same period compared to last year. Such dependence on internationally traded feed ingredients exposes producers to supply disruptions and price fluctuations, leading to increased production costs and reduced margin stability for shrimp and other crustacean farmers. These uncertainties hinder production expansion and investment within the Chinese crustacean market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrimp Dominance Meets Lobster Premiumization

Shrimp and prawn accounted for the largest share, 46.0%, of the China crustaceans market in 2025. Shrimp remains the leading crustacean category due to its widespread consumption, well-established farming infrastructure, and strong presence across retail, foodservice, and processing channels. The species benefits from extensive aquaculture expertise, efficient feed systems, and year-round availability, making it a preferred choice for both domestic consumers and export-oriented producers. Crab, on the other hand, maintains a significant role in premium seafood consumption, driven by seasonal demand and cultural importance. Additionally, crayfish and other niche crustaceans are gaining traction through online retail platforms and diversified dining formats.

Lobster market size is forecast to grow at the fastest CAGR of 8.8% during 2026–2031. This growth is fueled by increasing consumer spending on premium seafood, rising demand from high-end restaurants, and greater acceptance of imported live lobster products in urban markets. Consumers are increasingly seeking unique seafood experiences, driving demand for higher-value crustacean species. Concurrently, advancements in aquaculture technology, cold-chain logistics, and distribution networks are enhancing product availability and quality. Emerging crustacean categories are also benefiting from the expansion of digital sales channels and modern retail formats, contributing to the diversification of the overall market landscape.

Geography Analysis

East China remains the central hub for crustacean production and consumption, supported by advanced cold-chain infrastructure, major seafood wholesale markets, and extensive aquaculture activities along the coast. According to China's 2024 National Fishery Economic Statistics Bulletin, crustacean aquaculture production reached 7,847.9 thousand metric tons in 2024, marking an approximate 6.3% increase from previous year. This growth reflects the continued expansion of shrimp, crab, and crayfish farming across the country. The region benefits from integrated farming, processing, and distribution networks, enabling efficient movement of crustacean products across domestic and export markets. Ongoing investments in aquaculture modernization and seafood processing capabilities further solidify East China's role in the national crustacean value chain.

Central and Southwest China are becoming increasingly significant to the country's crustacean industry due to the expansion of inland aquaculture and the adoption of technology-driven farming systems. Producers in provinces such as Sichuan, Chongqing, Yunnan, and Guizhou are investing in improved breeding practices, water management systems, and digital monitoring technologies to enhance productivity and operational efficiency. The region's growing aquaculture base diversifies the national crustacean supply while reducing reliance on coastal production areas. Rising seafood consumption, improved logistics infrastructure, and investments in processing facilities continue to strengthen regional crustacean value chains, supporting the long-term development of inland aquaculture.

South China plays a strategic role in the country's crustacean industry, driven by its concentration of shrimp farming, seafood processing, and export-oriented operations. According to the General Administration of Customs of the People's Republic of China, China's seafood imports reached USD 17.7 billion in 2024, reflecting strong demand for aquatic products, including crustaceans. The region benefits from established hatchery networks, favorable climatic conditions, and access to major international trade routes. Robust processing capabilities and integrated supply chains support both domestic consumption and export activities, reinforcing South China's importance within the national crustacean industry.

Competitive Landscape

The China crustaceans market is moderately consolidated, with key players including Zhanjiang Guolian Aquatic Products Co., Ltd., Shandong Haidu Ocean Product Co., Ltd., Shandong Homey Aquatic Development Co., Ltd., Fujian Yuehai Aquatic Food Co., Ltd., and Ocean Treasure World Foods Limited. Competition in the market increasingly revolves around vertical integration, product quality, and supply chain management. Leading companies operate across multiple stages of the value chain, such as hatcheries, feed production, farming, processing, and distribution. This integrated approach enhances operational efficiency, improves traceability, and allows companies to adapt more effectively to shifting consumer preferences and market demands.

Technology is emerging as a critical factor in differentiating competitors within the industry. According to China's 2024 National Fishery Economic Statistics Bulletin, aquaculture production reached 60,600.3 thousand metric tons in 2024, highlighting the growing scale and modernization of the aquaculture sector, including crustaceans. Producers are increasingly adopting digital monitoring systems, automated feeding technologies, water-quality management tools, and disease-control programs to enhance productivity and operational performance. Companies that integrate advanced farming technologies with processing and distribution capabilities are strengthening their market positions and improving their ability to meet both domestic and international demand.

Industry consolidation is gradually transforming the competitive landscape as larger companies expand their operational capabilities and geographic presence. The focus of competition is shifting from production scale to factors such as product quality, traceability, biosecurity, and supply chain integration. Companies are investing in processing facilities, cold-chain networks, certification programs, and value-added seafood products to enhance customer relationships and improve market access. Strategic partnerships with distributors, retailers, and foodservice operators are becoming more prevalent as firms aim to optimize distribution efficiency. As industry standards evolve, companies with advanced technical expertise and integrated business models are improving their competitive positioning.

Recent Industry Developments

- July 2025: Zhanjiang Guolian Aquatic Products Co., Ltd. received a USD 13 million investment for its subsidiary, Guangdong Gourmet Aquatics Co., Ltd., aimed at upgrading seafood processing facilities and improving international marketing capabilities. This investment focuses on processing higher-value shrimp and other crustacean products, enhancing export competitiveness and expanding the company's market presence.

- January 2025: Zhanjiang Guolian Aquatic Products Co., Ltd. entered into a three-year exclusive shrimp supply agreement with Ecuador-based Aquagold. This agreement ensures a stable supply of raw materials for the Chinese market, enhancing import channels and supporting crustacean processing capacity.

- January 2025: The State Council Tariff Commission of China has announced an increase in import tariffs on specific seafood products. The tariff on frozen shrimp and prawns will rise from 2% to 5%. This measure aims to enhance the competitiveness of domestic shrimp and crustacean producers while supporting the development of local aquaculture.

China Crustaceans Market Report Scope

Crustaceans, including shrimp, crabs, lobsters, and crayfish, are aquatic invertebrates distinguished by their hard exoskeletons and segmented bodies. They are commonly used as seafood for human consumption and also in animal feed, pharmaceuticals, and biotechnology applications. The China Crustaceans Market Report is Segmented by Type (Shrimp and Prawn, Crab, Lobster, and More). The report also offers Production Analysis (Volume), Consumption Analysis (Value and Volume), Trade Analysis (Value and Volume), Import Market Analysis (Import Value and Volume and Key Supplying Markets), and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Type

| Shrimp and Prawn |

| Crab |

| Lobster |

| Others |

China

| Production Analysis | Production Volume | |

| Consumption Analysis (Value and Volume) | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Type | Shrimp and Prawn | ||

| Crab | |||

| Lobster | |||

| Others | |||

| China | Production Analysis | Production Volume | |

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

What is the current value of the China crustaceans market and its forecast growth?

The market stands at USD 2.25 billion in 2026 and is projected to reach USD 3.06 billion by 2031, advancing at a 6.3% CAGR from 2026 to 2031.

Which product currently commands the biggest share of revenue?

Shrimp and prawn held the largest 46.0% market share in 2025.

Which product type is expanding the quickest?

Lobster forecast to grow at the fastest CAGR of 8.8% from 2026 to 2031 as premium dining demand rises in Tier-1 cities.

What certification trends shape export competitiveness?

Aqualture Stewardship Council and Best Aquaculture Practices approvals allow Chinese suppliers to secure premium prices in European and North American supermarkets.

Page last updated on: