Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

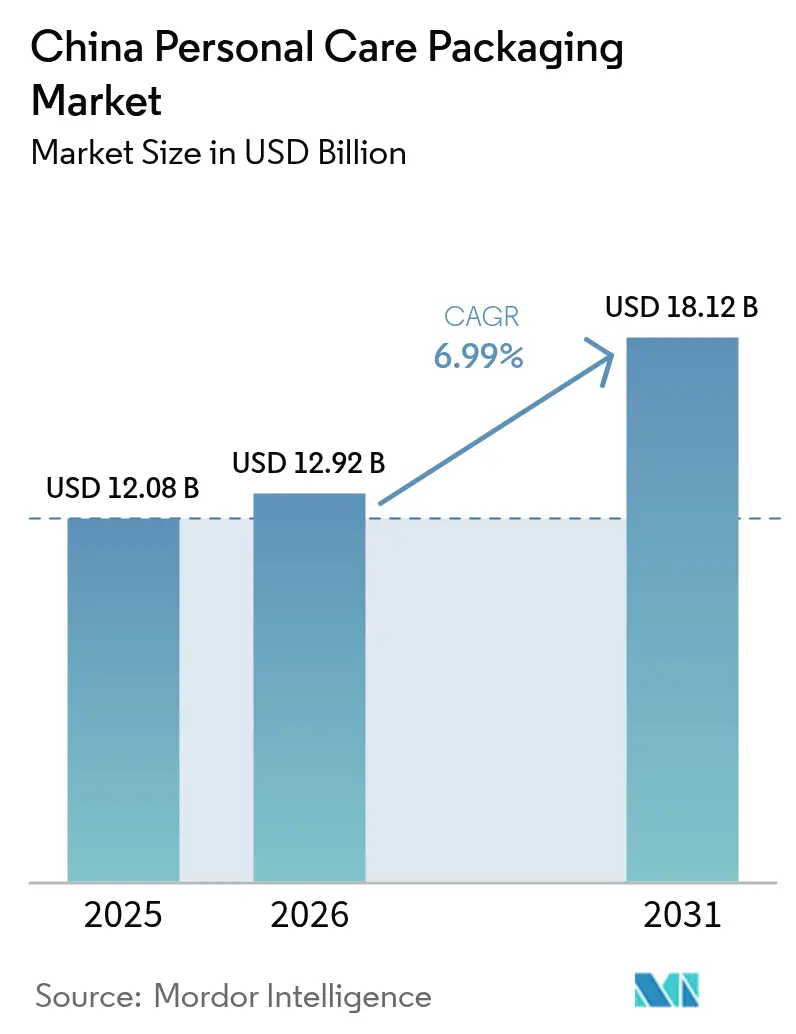

| Base Year Market Size (2025) | USD 12.08 Billion |

| Market Size (2026) | USD 12.92 Billion |

| Market Size (2031) | USD 18.12 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Personal Care Packaging Market Analysis by Mordor Intelligence

The China personal care packaging market size was valued at USD 12.08 billion in 2025 and estimated to grow from USD 12.92 billion in 2026 to reach USD 18.12 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). This trajectory is propelled by regulatory measures that curb excessive packaging, the rapid migration of beauty shopping to social-commerce channels, and brand commitments to carbon-neutral operations. Sustainable material innovation, e-commerce–ready structural designs, and premium-tier product launches are converging to redefine competitive positioning across the value chain. Brands are investing in AI-assisted prototyping to trim development cycles, while packaging converters balance lightweighting with durability demands for nationwide last-mile delivery. Heightened enforcement of the GB 23350-2021 standard, the roll-out of China’s national carbon trading scheme, and real-time social media feedback loops will continue to shape material choices and design parameters for the China personal care packaging market.

Key Report Takeaways

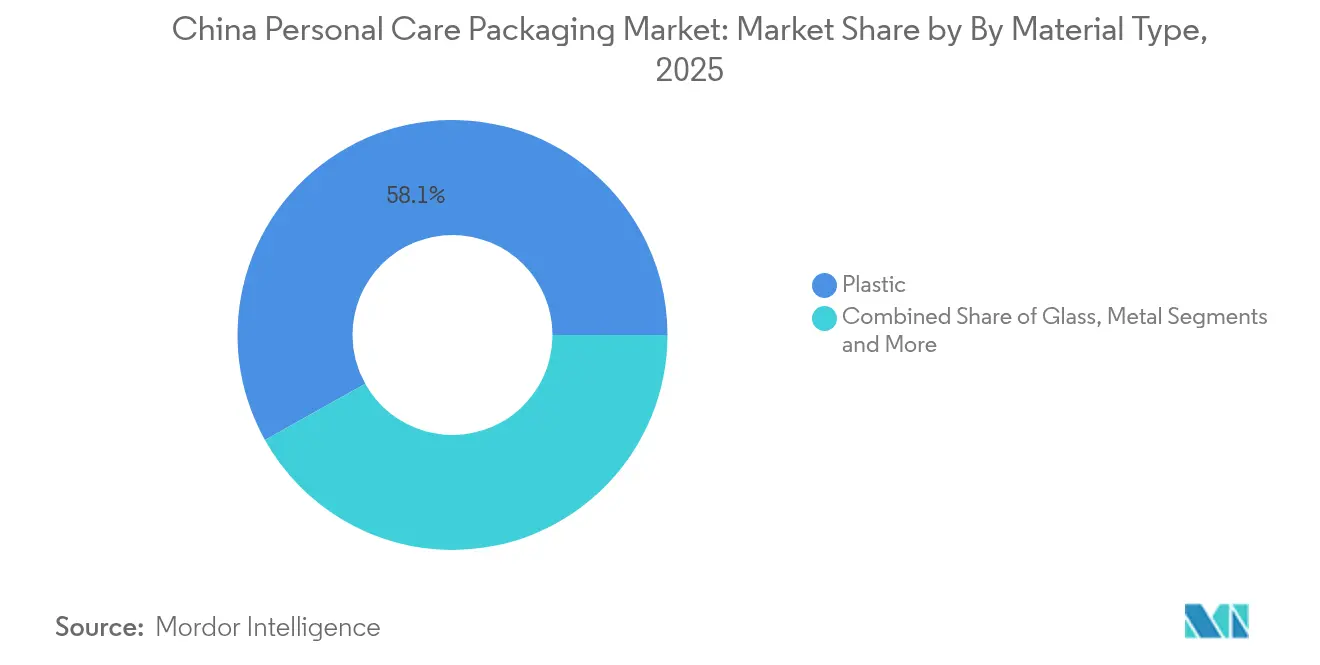

- By material type, plastic dominated with 58.12% of the China personal care packaging market share in 2025, while paper and paperboard is projected to post the fastest 8.11% CAGR through 2031.

- By packaging type, plastic bottles and jars led with 41.12% revenue share in 2025; flexible plastic formats are forecast to expand at an 7.95% CAGR to 2031.

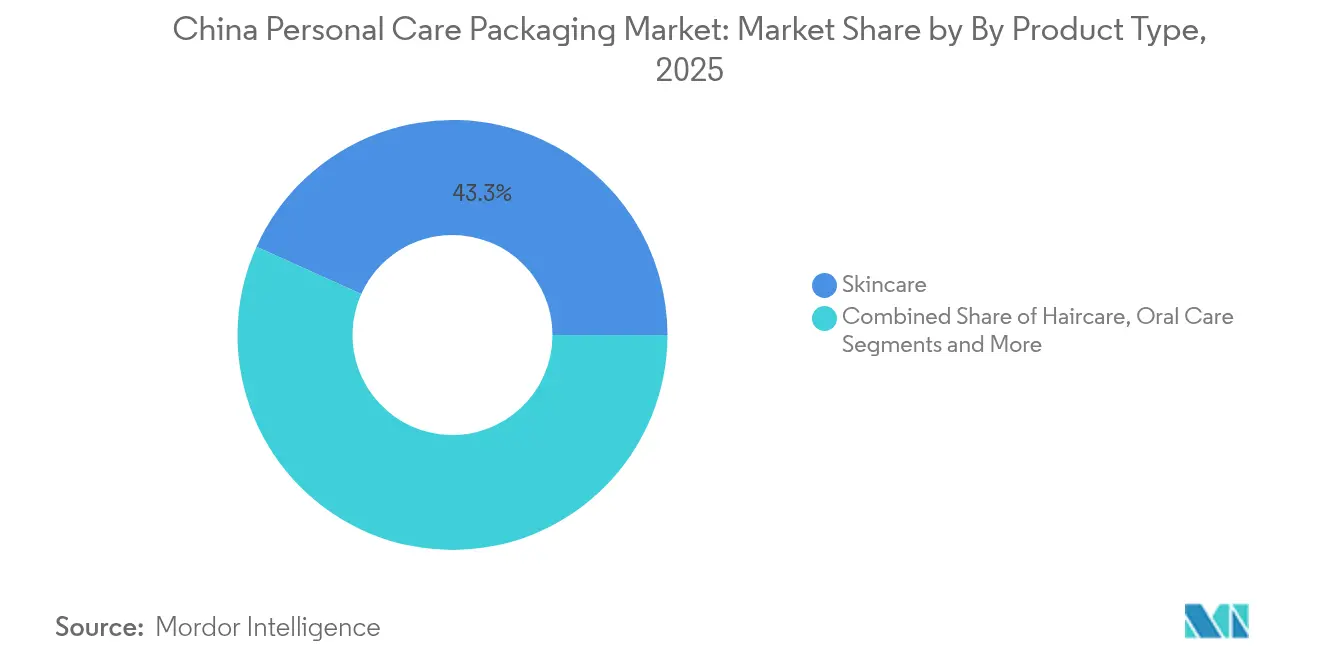

- By product type, skincare captured 43.26% of the China personal care packaging market size in 2025, whereas men’s grooming is advancing at a 9.48% CAGR to 2031.

- By sustainability attribute, recyclable mono-material solutions held 51.68% of the China personal care packaging market size in 2025; biodegradable and compostable formats are set to register a 10.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Personal Care Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom for beauty and personal care | +1.8% | National, tier-1 and tier-2 cities | Medium term (2-4 years) |

| Rise of refill-ready retail formats | +1.2% | National, early adoption in Shanghai, Beijing, Shenzhen | Long term (≥ 4 years) |

| Premiumisation of skincare and cosmetic SKUs | +1.5% | National, expanding into tier-3 cities | Medium term (2-4 years) |

| Male grooming uptake in lower-tier cities | +0.9% | Tier-3 and tier-4 cities | Long term (≥ 4 years) |

| AI-enabled design and rapid prototyping | +0.7% | Manufacturing hubs | Short term (≤ 2 years) |

| Mandatory “excessive-packaging” compliance | +0.8% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce boom for beauty and personal care

Explosive social-commerce growth is forcing brands to engineer packs capable of surviving wide-radius fulfilment while staging a photogenic unboxing moment. Douyin’s beauty GMV more than doubled between 2021 and 2023, turning platform algorithm trends into near-instant packaging briefs for converters. Brands now weigh impact resistance, dimensional weight, and camera-ready aesthetics in equal measure. As fulfillment centers proliferate outside coastal provinces, flexible pouches and lightweight corrugates gain favor for their cushioning and freight-saving attributes, reinforcing the momentum of the China personal care packaging market.

Rise of refill-ready retail formats

Circularity targets from premium beauty houses accelerated trials of refill pods, concentrate sachets, and in-store bulk dispensers. Shiseido aims for 100% sustainable packaging by 2025 and has extended refill options to hero SKUs, prompting local ODMs to retool injection-molding lines for plug-in cartridges. Early pilots in Shanghai malls show consumers accepting reusable cores when refill stations are adjacent to point-of-sale, unlocking repeat-purchase stickiness and trimming material footprints.

Premiumization of skincare and cosmetic SKUs

Luxury consumption rebounds have lifted demand for glass flacons with metallized collars, anodized aluminum droppers, and multi-layer folding cartons laminated with low-migration inks. High-tier counters, although fewer in number after store-network rationalization, report ticket sizes swelling as shoppers equate heft and finish with efficacy. Glass remains the centerpiece for fragrance and ampoule serums, supporting price-elasticity strategies and margin protection for the China personal care packaging market.

Male grooming uptake in lower-tier cities

Rising beauty literacy among 18- to 30-year-old men is translating into surging demand for minimalist tubes, airless pumps, and stick applicators that deliver discreet, on-the-go usage. Social-commerce influencers emphasize clean lines and monochrome colorways, nudging converters to develop matte-finish PP barrels and low-gloss films compatible with hot-foil stamping. Penetration in tier-3 hubs is delivering fresh volume pools that offset softer growth in saturated coastal metros.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile resin and aluminum prices | −1.3% | Guangdong, Zhejiang manufacturing clusters | Short term (≤ 2 years) |

| Recycling capacity bottlenecks for multi-layer laminates | −0.8% | Tier-2 and tier-3 cities | Medium term (2-4 years) |

| Stricter carbon-intensity quotas for plastics | −0.6% | National industrial zones | Long term (≥ 4 years) |

| Counterfeiting risk in secondary packaging | −0.4% | E-commerce channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile resin and aluminum prices

Feedstock swings, driven by oil price gyrations and geopolitical uncertainty, are compressing converter margins. PET chip producers such as Wankai trimmed operating rates to 76% in late 2024, tightening supply and pushing converters to hedge through multi-month contracts or diversify into HDPE and PP blends. Smaller firms struggling to absorb surcharges may become acquisition targets, spurring gradual consolidation within the China personal care packaging market.

Recycling capacity bottlenecks for multi-layer laminates

Although PET beverage bottles reach near-closed-loop recovery at 96.48%, cosmetic laminates containing EVOH or metallized layers remain largely unrecoverable. Municipal MRFs in Chongqing and Wuhan still lack delamination lines, forcing brands to pivot toward mono-material PE or PP pouches to sidestep downstream compliance penalties. Infrastructure gaps place additional onus on producers under China’s evolving extended-producer-responsibility rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Regulation pushes diversification beyond plastics

Plastic retained 58.12% of the China personal care packaging market share in 2025 owing to cost efficiency and process agility. Yet the GB 23350-2021 interspace ratio cap is prompting brands to trim wall thickness and explore paperboard sleeves for secondary packs. Paper and paperboard’s 8.11% CAGR positions it as the standout growth engine, propelled by consumers equating fiber-based packs with environmental stewardship. Glass volumes are stabilizing in prestige skincare where weight signals luxury, while metal aerosols gain favor in premium deodorants as they align with infinitely recyclable narratives. Volatile resin prices further amplify the case for blended substrate strategies across the China personal care packaging market.

A steady pipeline of bio-based polymers has emerged, but many blends require industrial composting conditions that remain scarce. Consequently, producers are investing in mono-material PP tubes and PCR-rich PET bottles that meet recyclability thresholds without compromising barrier performance. State-owned banks’ green finance instruments are expected to lower capital costs for retrofitting lines capable of handling recycled content, keeping material decisions tightly linked to both sustainability scorecards and input-cost hedging.

By Packaging Type: Flexible formats accelerate under e-commerce logistics demands

Plastic bottles and jars controlled 41.12% of 2025 revenues, backed by entrenched blow-molding assets and consumer familiarity. Flexible plastic pouches, however, are clocking an 7.95% CAGR as brands exploit weight savings that translate into lower courier tariffs. Tamper-evident zippers and gusseted bases are now standard to survive multi-node delivery routes while presenting flat fronts for influencer video close-ups. Tubes and sticks gain incremental traction alongside the male grooming boom, while refill cartridges enable footprint reduction in top-shelf skincare. Pumps, droppers, and actuators face cost pressure from metal spring components but benefit from premiumization that values dosage accuracy within the China personal care packaging market.

Corrugated shippers are evolving from plain kraft cubes into co-branded, print-on-demand canvases for social-media storytelling. Yet they must still comply with the GB 43352-2023 express-pack regulation limiting heavy-metal content, nudging converters toward water-based inks and starch adhesives. Aerosol cans and specialty glass remain niche by volume but over-index in value due to fragrance and spa-grade treatments that command higher averaged selling prices.

By Product Type: Skincare supremacy faces rising men’s grooming volumes

Skincare accounted for 43.26% of the 2025 China personal care packaging market size, reflecting broad consumer adoption of multi-step regimens and willingness to trade up for efficacy cues such as airless jars. The segment thrives on formula-pack synergy, with hydration creams migrating into RE-PET jars that reinforce clean-beauty positioning. Men’s grooming, advancing at 9.48% CAGR, is closing the historical gap by leveraging minimalist stick and sachet formats priced for first-time users in lower-tier cities. Haircare innovation centers on squeeze-pouch concentrates that pair with reusable silicone sleeves, while oral-care brands introduce recycled-paper blister boards for whitening strips.

Color cosmetics battles price deflation as DTC entrants launch slimline compacts made from PCR ABS to manage cost of goods. Fragrance players, emboldened by local sensorial codes, are specifying heavy-base flacons decorated with ceramic frit finishes, thereby maintaining a premium halo that supports higher packaging spend per milliliter. In baby-care, QS-code traceability labels are becoming ubiquitous to reassure parents, further integrating smart-pack technology into the China personal care packaging market.

By Sustainability Attribute: Biodegradable formats grow fastest amid mixed real-world performance

Recyclable mono-material solutions held 51.68% market share in 2025, benefitting from advances in single-polymer barrier films that match incumbent performance. Biodegradable and compostable substrates will expand 10.27% per year through 2031, yet real-world degradation often lags lab certificates when the packs end up in open landfills.

Brands therefore supplement biopolymer adoption with consumer-facing take-back schemes and clearly printed disposal instructions. Post-consumer-recycled (PCR) content integration is constrained by feedstock availability; nevertheless, the National Carbon Trading market incentivizes PCR uptake by assigning lower emission factors to recycled resin grades. Refillable systems, while capital-intensive, create annuitized revenue from cartridge replenishment and strengthen shopper loyalty across the China personal care packaging market.

Geography Analysis

The market exhibits pronounced regional divergence tied to income gradients, infrastructure readiness, and regulatory enforcement vigor. Tier-1 cities—Shanghai, Beijing, Shenzhen—set the tone for premium aesthetics and early adoption of low-carbon substrates, attracting pilot programs for AI-driven package personalization. Retail rents and labor costs in these hubs encourage prestige brands to pivot more business online, elevating the importance of ship-safe, camera-friendly packs that withstand dense urban delivery networks. Regulatory spot checks on excessive packaging are most frequent in these municipalities, driving strict conformance to interspace and layer thresholds.

Tier-2 and tier-3 conurbations such as Chengdu, Qingdao, and Xiamen deliver faster unit growth on the back of expanding middle-class wallets. Here, manufacturers tweak unit sizes and bundle designs to match regional price points, often blending PCR and virgin resin to maintain margins. Recycling infrastructure, however, lags coastal benchmarks, complicating the closed-loop economics of laminate pouches and prompting partnerships with waste-management start-ups installing smart-bin arrays. For the China personal care packaging market, these cities represent fertile ground for scalable refill pilots, provided refill stations are mapped to high-footfall malls and transportation hubs.

Manufacturing bases are still concentrated in Guangdong and Zhejiang, giving converters proximity to polymer suppliers and port logistics. Government subsidies for energy-efficient extrusion lines in inland provinces are beginning to redistribute capacity westward, easing congestion along the Pearl River Delta. National carbon trading compliance applies uniformly, but enforcement intensity remains higher in industrial parks designated as green-manufacturing pilots. Collectively, the regionally nuanced operating climate compels packaging stakeholders to orchestrate multi-tier supply chains that harmonize cost, sustainability, and consumer-experience objectives across the China personal care packaging market.

Regulatory Landscape

China's personal care packaging decisions are increasingly shaped by cosmetics and packaging compliance regimes led by the National Medical Products Administration (NMPA), alongside broader green-manufacturing and packaging policies. NMPA initiated a three-year pilot for electronic cosmetic labeling starting February 1, 2026, across Beijing, Shanghai, Zhejiang, Shandong, Guangdong, and Chongqing. The move points to digital label governance that can reduce print runs and support faster label updates across SKUs and channels.

On standards, NMPA has been advancing updates that affect primary pack labeling content and on-pack information architecture. These include a draft mandatory national standard intended to replace GB 5296.3-2008 for cosmetic labeling (in consultation) and May 2026 announcements (Announcement No. 48 and No. 51) that incorporate additional safety standards and test methods into the Safety and Technical Standards for Cosmetics. For packaging manufacturers, sector policy also emphasizes greener and smarter production, with MIIT's Light Industry Stable Growth Work Plan (2025-2026) prioritizing digital transformation and green transition in light industries including packaging. Industry-facing documents such as T/BDCA 0004-2025 (effective September 2025) also provide a framework for quality and safety control systems in cosmetics packaging.

Value Chain Analysis

The China personal care packaging value chain runs from upstream resin, glass, metal, paper, inks, and additives suppliers to converters producing bottles and jars, tubes and sticks, pumps and sprayers, folding cartons and corrugated shippers, and flexible pouches. It then feeds fillers and brand owners, with multi-channel distribution increasingly dominated by e-commerce and social commerce. Manufacturing and converting capacity remains concentrated in Guangdong and Zhejiang, supported by proximity to polymer supply, tooling ecosystems, and port-linked logistics for both domestic distribution and export-oriented runs.

Converters operate through OEM/ODM and project-based design services. Faster iteration cycles are increasingly tied to digital design, prototyping, and qualification workflows demanded by brand owners and platform-driven product refreshes. Bottlenecks concentrate around input-cost volatility (resins and aluminum components), availability of consistent recycled content feedstock, and downstream recycling limitations for multi-layer structures. These constraints are pushing value around mono-material redesign, solvent-free lamination capability, and quality-control systems aligned to packaging and cosmetics standards, including industry guidance such as T/BDCA 0004-2025. Policy direction under the China Packaging Industry Development Plan (2021-2025) also supports investments in greener production and express/e-commerce packaging compliance, which encourages converters to upgrade inks, adhesives, and process controls to meet evolving green requirements.

Competitive Landscape

Competition is moderate-to-high, with global multinationals and agile domestic specialists jostling for shelf-share and e-commerce mindshare. Amcor and Berry Global completed an all-stock merger in mid-2025, unlocking USD 650 million in anticipated synergies and elevating the combined RandD war chest to USD 180 million annually. The enlarged footprint intensifies pricing pressure on mid-sized converters, spurring them to differentiate via design consultancy and rapid proto-typing services. Chinese firms such as HCP Packaging Shanghai and Zhejiang Jinsheng leverage shorter lead times and localized service to win briefs from indie beauty labels looking for MOQ-friendly runs.

Technology adoption forms a clear battleground. AI-assisted generative design platforms, exemplified by Seymourpowell’s Identité service, accelerate iteration cycles, reduce resin mass through topology optimization, and deliver hyper-personalized aesthetics that resonate on social feeds. Anti-counterfeit inks and NFC tags are gaining traction as luxury brands combat grey-market leakage, adding complexity to print-finish specifications. Meanwhile, resin market volatility is prompting vertical integration moves, with some converters investing in upstream PCR reprocessing assets to assure material supply and ESG compliance, fortifying their positions within the China personal care packaging market.

Domestic beauty majors, emboldened by cultural fluency and community-commerce influence, are capturing share, compelling international giants to localize fragrance accords, color palettes, and pack ergonomics. Strategic partnerships between brand owners and packaging suppliers now routinely include joint carbon footprint reduction milestones and shared line-trial facilities. As domestic e-commerce champions intensify pressure for cost-effective yet brand-elevating solutions, suppliers able to blend functional robustness with sustainable storytelling stand to consolidate gains.

China Personal Care Packaging Industry Leaders

Silgan Holdings Inc.

Amcor PLC

Rieke Packaging Systems Ltd

DS Smith PLC

Bemis Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One key whitespace in China personal care packaging is compliant, e-commerce-ready sustainable design that meets tightening green and labeling requirements while still protecting product integrity through nationwide delivery. The rollout of SB/T 11266-2026 for e-commerce green packaging (released January 12, 2026, implemented July 1, 2026) provides a clearer target for platform and logistics-facing packs. It supports demand for lightweight and durable structures, including mono-material flexible formats, optimized corrugated shippers, and packaging engineered for automated fulfillment and sorting.

Cross-border and export-linked opportunities are also expanding for converters that can meet recognized green requirements and reusable express packaging standards. Effective June 1, 2026, the RCEP Green Packaging Mutual Recognition Arrangement recognizes compliant reusable express packaging under GB/T 37572-2025 for exports to Australia, New Zealand, Japan, and South Korea without redundant re-testing. This favors suppliers that can document compliance and produce standardized reusable systems at scale. On the supply side, investments in automation and intelligent manufacturing offer a direct route to capture this demand: Amcor's July 2026 start of expansion at its Dongguan flexible packaging facility, adding a 7,000-square-meter manufacturing plant and an automated warehouse, illustrates how global converters are adding China-based capacity and process capability to serve personal care along with other end markets.

Recent Industry Developments

- July 2026: Amcor began expanding its flexible packaging facility in Dongguan, China, adding a 7,000-square-meter manufacturing plant and an automated warehouse, with completion targeted for July 2027. The added footprint and automation are intended to raise throughput and consistency for recycle-ready flexible formats used in personal care, alongside food and home care applications.

- February 2026: Silgan Holdings outlined approximately USD 310 million of planned 2026 capital expenditures to support growth, including in dispensing and specialty closures that serve personal care end markets. The investment focus supports Silgan's ability to scale pump, sprayer, and closure capacity, and to fund tooling and process upgrades tied to higher-specification packaging demands.

- October 2024: Silgan Holdings completed its acquisition of Weener Packaging, expanding its dispensing solutions portfolio for personal care and health care packaging. The deal broadened Silgan's manufacturing technologies and innovation base in dispensing systems, supporting more integrated offerings for brand owners seeking performance-focused and differentiated primary packs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers packaging used to pack and deliver personal care products sold in China, including primary packs (such as bottles, tubes, jars, and dispensers) and secondary packs (such as cartons) that reach retail or e-commerce consumers.

Scope exclusions: It excludes packaging used mainly for pharmaceuticals, food and beverage, and household or industrial chemicals, even if similar materials are used.

Segmentation Overview

- By Material Type

- Plastic

- Glass

- Metal

- Paper and Paperboard

- Bio-based and Compostable Plastics

- By Packaging Type

- Plastic Bottles and Jars

- Tubes and Sticks

- Pumps, Sprayers and Droppers

- Aerosol Cans and Metal Containers

- Folding Cartons

- Corrugated Boxes

- Flexible Plastic (Pouches, Sachets, Wraps)

- Caps and Closures

- Refillable / Reuse Systems

- By Product Type

- Skincare

- Haircare

- Oral Care

- Color Cosmetics

- Men's Grooming

- Deodorants and Fragrances

- Baby Care

- By Sustainability Attribute

- Recyclable (Mono-material)

- Post-Consumer Recycled (PCR) Content

- Biodegradable / Compostable

- Refillable / Returnable

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of demand and supply signals that can be checked in public data. For China personal care packaging, we leaned on sources such as China customs trade statistics for packaging materials and components, the National Bureau of Statistics of China for industrial output and price indices, and UN Comtrade for cross-checking import and export patterns.

We also reviewed China packaging and personal care association publications, standards and regulatory notices that affect materials and recyclability claims, and peer-reviewed papers on packaging formats and recycling readiness. To connect packaging demand with the end market, company annual reports, investor decks, and credible press were used to track category growth and pack format shifts. Where needed, analyst access to paid subscriptions for company financials and news intelligence, patent databases, and shipment-level trade datasets helped fill gaps on supplier footprint, innovation direction, and component flows. Examples are not exhaustive, and additional public sources were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating pack mix and pricing logic in China across skincare, haircare, oral care, and color cosmetics. We spoke with packaging converters, material suppliers, brand procurement teams, and channel experts, then used their inputs to pressure-test desk assumptions on PCR adoption, lightweighting, and refill formats across major consuming regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 53% | Functional/Unit leaders: 28% | |

| Smaller Players: 21% | Managers: 60% |

Market-Sizing & Forecasting

Sizing was developed using a top-down build that reconstructs packaging demand from China personal care product output and consumption signals, which are then translated into packaging needs by typical pack format intensity. Results were corroborated with selective bottom-up approximations, mainly by sampling supplier revenues, checking channel mix, and validating average selling prices against observed resin, aluminum, and paperboard movements.

Inputs that shaped the model included category growth for skincare and cosmetics, pack format shares (bottles, tubes, jars, pumps and sprayers, and flexible packs), material mix shifts toward mono-material designs, PCR content penetration, and unit pricing by format and material. Where data points were thin (for example, refill and reuse volumes), ranges were taken from interviews and then narrowed using plausibility checks against retail launch activity and material availability.

For forecasting, scenario analysis was used, because packaging demand in China moves with consumer trading up, regulation-driven material substitutions, and e-commerce packaging requirements that can change quickly. Base, conservative, and upside cases were aligned to primary expert expectations on category growth, resin and aluminum price pass-through, and speed of adoption for recyclable and refillable formats.

Data Validation & Update Cycle

Model outputs were checked against independent signals like packaging material trade flows, industrial production indices, and known price bands by format, and then any large variances were reviewed and explained before sign-off. When a gap could not be explained cleanly, follow-up calls were triggered to re-check pack mix, conversion ratios, or pricing assumptions.

Reviews are done in steps, starting with analyst self-checks, followed by peer review of calculations, and then a final logic pass to confirm the story matches the numbers. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory shifts or sharp input cost changes. Before delivery, a fresh update pass is completed so clients receive the latest view available at that time.

Mordor Intelligence's China Personal Care Packaging Market Size Versus Other Published Estimates

Published market sizes for China personal care packaging can look far apart because the scope line is drawn differently and the same packaging can be counted in more than one place. Differences also come from how each publisher treats pricing, currency timing, and how quickly assumptions are refreshed when materials and pack formats change.

Green or sustainable-only packaging sits outside Mordor Intelligence's scope here, so the total reflects all personal care packaging formats and materials rather than only recycled, reusable, or degradable packs. Some sources also use higher price escalation for pumps, dispensers, and specialty packs, and others mix in adjacent uses like home care or gift sets, which can lift the headline value even when unit volumes are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.08 B (2025) | |

| Industry Research Portal A | USD 3.16 B (2023) | Uses a green-packaging-only lens for China personal care, which narrows the counted materials to recycled content, reusable, and degradable packs and leaves out conventional plastic, glass, metal, and paper packs. |

| Syndicated Publisher B | USD 610.00 B (2025) | Shows figures that are likely illustrative or not normalized to packaging-only revenue, and the disclosed table format suggests the value may be mixing broader beauty and personal care spend with packaging, which inflates the market total. |

Taken together, the spread mainly comes from scope, not just math, because one estimate focuses only on green packaging and another appears to blend packaging with a wider spend pool. By keeping the definition tied to packaging revenue in China and then checking pricing and mix with field feedback, the final number stays traceable to clear inputs and can be repeated when assumptions are updated.

Key Questions Answered in the Report

What is the projected value of the China personal care packaging market by 2031?

It is expected to reach USD 18.12 billion, expanding at a 6.99% CAGR from 2026.

Which material segment is growing the fastest?

Paper and paperboard is forecast to post the quickest 8.11% CAGR due to regulatory support and consumer preference for fiber-based packs.

Why are flexible pouches gaining popularity in beauty e-commerce?

They reduce freight weight, provide adequate drop protection, and offer printable surfaces ideal for social-media branding.

How are refill systems influencing packaging design?

Brands introduce cartridge-based or bulk-dispense formats that lower plastic usage and foster repeat purchases through dedicated refill stations.

Page last updated on: