Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

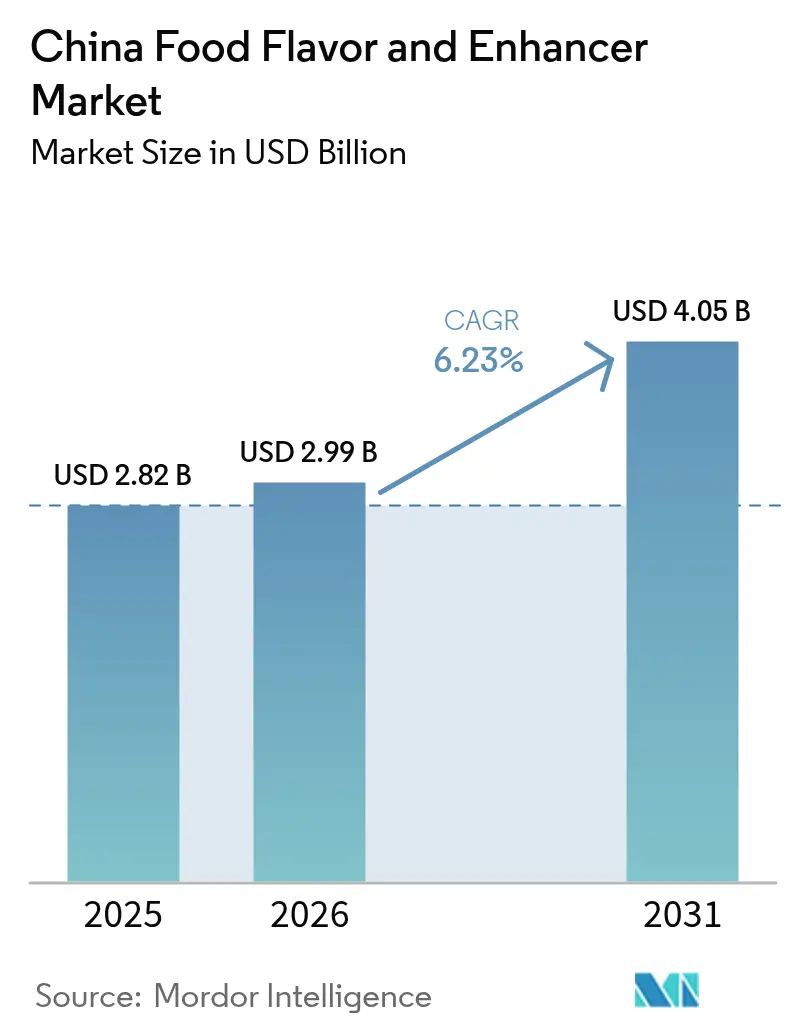

| Base Year Market Size (2025) | USD 2.82 Billion |

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 4.05 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Food Flavors and Enhancers Market Analysis by Mordor Intelligence

The China Food Flavors and Enhancers Market size is expected to grow from USD 2.82 billion in 2025 to USD 2.99 billion in 2026 and is forecast to reach USD 4.05 billion by 2031 at 6.23% CAGR over 2026-2031. This trajectory reflects structural shifts beyond simple volume growth: urbanization has compressed meal-preparation time, pushing processors to deliver consistent sensory profiles across millions of daily servings, while regulatory tightening under GB 2760-2024, effective February 8, 2025, forces reformulation toward cleaner labels [1]Source: National Medical Products Administration, "GB 2760-2024", nmpa.gov.cn. The interplay between cost-conscious synthetic dominance and accelerating natural-ingredient adoption creates a bifurcated competitive arena where scale economics clash with premiumization strategies. The food flavor market is also navigating a sharp divide: synthetic formulations remain cost leaders, but natural variants capture value growth as exporters chase clean-label acceptance in the European Union and the United States. Scaling fermentation-derived umami systems lets domestic players undercut plant-extraction costs, yet multinationals invest in AI-enabled sensory labs to defend premium niches. Short-term raw-material volatility, such as the 2024 pepper spike, tightens margins, but it simultaneously accelerates precision-biology investment that promises to decouple flavor supply from climatic swings.

Key Report Takeaways

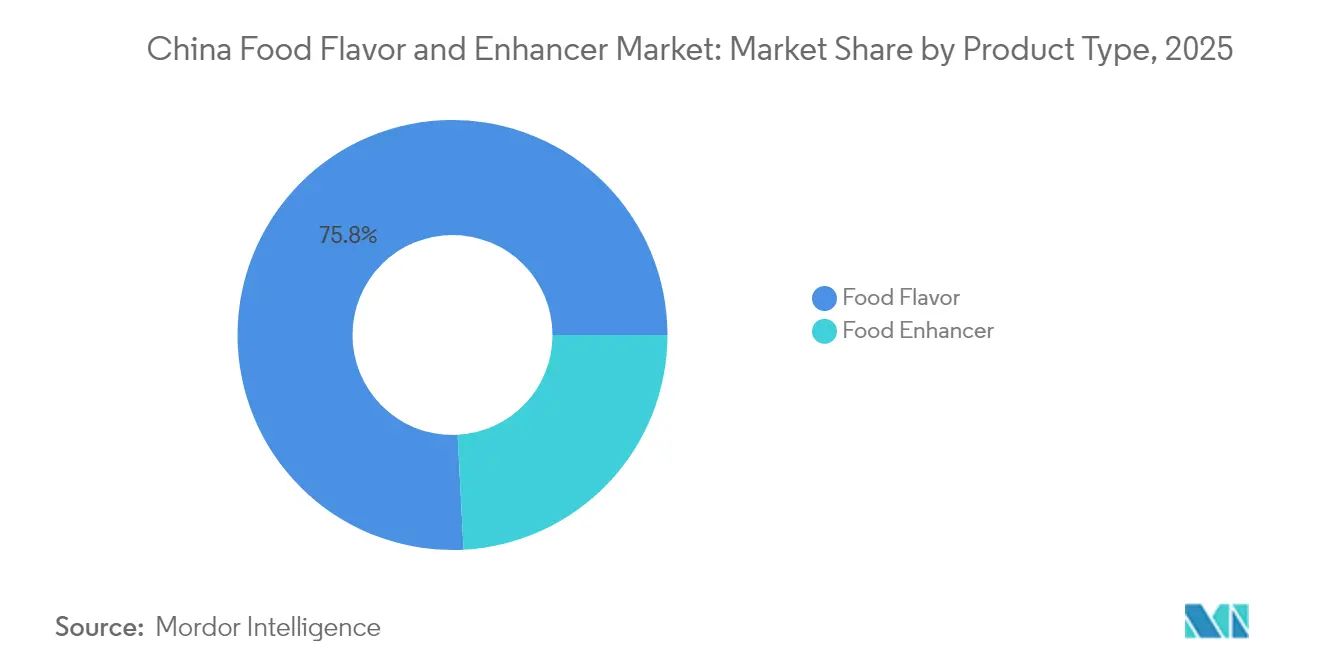

- By product type, food flavor commanded 75.82% revenue share in 2025, whereas food enhancers are expanding at a 6.61% CAGR through 2031.

- By category, synthetic variants held 71.98% of the 2025 food flavor market share, yet natural flavors are growing at a 6.79% CAGR to 2031.

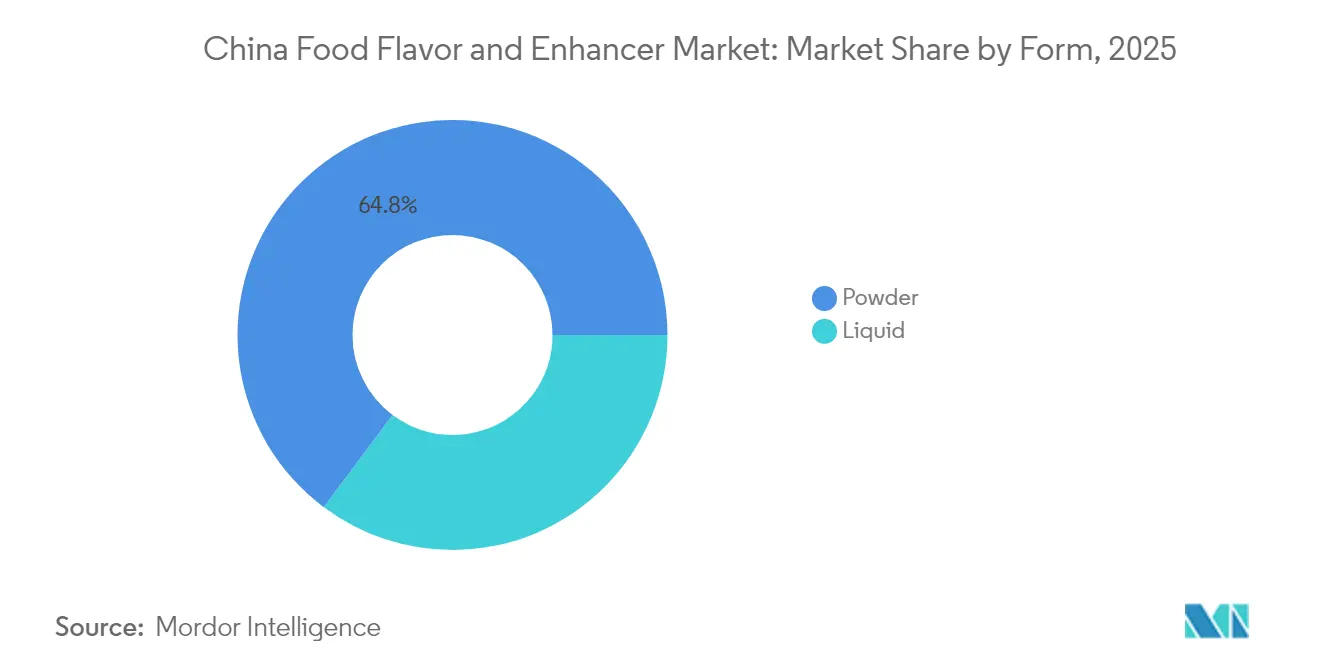

- By form, liquid flavors contributed 35.21% of 2025 sales, while powder formats are forecast to achieve a 7.12% CAGR on logistics efficiencies.

- By application, savory snacks led with 23.35% of 2025 revenue, whereas beverages hold the fastest trajectory at a 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Food Flavors and Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for processed and convenience foods | +1.2% | National, concentrated in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Consumers seeking novel, exotic and diverse flavors | +0.8% | National, with premium segments in coastal provinces | Short term (≤ 2 years) |

| Food processors needing consistent taste across products | +0.7% | National, especially large-scale manufacturers | Long term (≥ 4 years) |

| Demand for clean-label and natural/organic ingredients | +1.1% | National, export-oriented processors prioritize compliance | Medium term (2-4 years) |

| Technological advancements in flavor formulation and extraction | +0.9% | National, R&D hubs in Shanghai, Beijing, Guangzhou | Long term (≥ 4 years) |

| Culinary diversity and global cuisine influences driving innovation | +0.6% | National, urban centers with high disposable income | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Processed and Convenience Foods

Urbanization and dual-income households have compressed meal-preparation windows, pushing China's processed-food sector up 2.2% year-on-year [2]Source: U.S. Department of Agriculture Foreign Agricultural Service, "Why Do Ag Exports Matter to U.S. Farmers and the U.S. Economy?", fas.usda.gov. Flavor standardization becomes mission-critical when a single noodle brand ships 10 million packets daily across 30 provinces; even minor batch-to-batch variance triggers consumer complaints and retailer penalties. Ready-to-eat meals and frozen dumplings now account for a growing share of urban diets, requiring flavor systems that survive freeze-thaw cycles and microwave reheating without sensory degradation. This technical complexity favors encapsulated and microencapsulated flavor technologies, which protect volatile aroma compounds during thermal processing. Processors are also adopting modular flavor platforms, pre-blended bases that allow SKU proliferation without reformulation lead times, accelerating time-to-market for limited-edition launches tied to festivals or celebrity endorsements.

Food Processors Needing Consistent Taste Across Products

Scale manufacturers face a paradox: ingredient sourcing from dozens of provinces introduces natural variability, yet brand equity demands identical sensory profiles from Harbin to Shenzhen. Standardized flavor concentrates solve this by decoupling taste from raw-material fluctuations; a soy-sauce producer can maintain umami intensity even when fermentation batches vary in amino-acid composition. This consistency imperative extends to co-manufacturing arrangements, where a single brand may source from 5 regional plants, each requiring identical flavor dosing protocols. Quality-control laboratories now deploy gas chromatography-mass spectrometry (GC-MS) to fingerprint flavor profiles, flagging deviations before products reach distribution. The rise of e-commerce amplifies reputational risk; a single off-tasting batch can generate thousands of negative reviews within 48 hours, making flavor consistency a direct revenue lever rather than a background technical concern.

Demand for Clean-Label and Natural/Organic Ingredients

GB 2760-2024, effective February 8, 2025, tightened additive disclosure requirements, compelling brands to list specific E-numbers rather than generic "flavoring" categories. This transparency push coincides with consumer health anxieties: 46.37% of latiao buyers cite excessive additives as a deterrent, while 48% of surveyed consumers actively seek natural-flavor claims on packaging. Export-oriented processors face dual compliance burdens, meeting China's GB standards domestically while adhering to EU Regulation 1334/2008 or FDA GRAS protocols for overseas shipments. Natural-flavor production costs remain 3 to 5 times synthetic equivalents, but premiumization strategies are absorbing these margins; yogurt brands charging CNY 15–20 per cup can justify natural vanilla extract over vanillin. Fermentation-derived "nature-identical" compounds occupy a regulatory gray zone, chemically identical to plant extracts but biosynthesized, offering a cost-performance middle path that satisfies clean-label aesthetics without full natural-extraction economics.

Technological Advancements in Flavor Formulation and Extraction

Precision fermentation is shifting flavor production from agriculture to bioreactors; Symrise's acquisition of Wing Biotechnology in China underscores this pivot toward microbial platforms that produce vanillin, nootkatone, and other high-value compounds at costs approaching synthetic parity. IFF's October 2024 launch of its 16,000-square-meter Shanghai Creative Center integrates AI-driven sensory prediction, allowing flavorists to model consumer preference clusters before physical prototyping. Enzymatic hydrolysis technologies are unlocking umami peptides from plant proteins, critical for masking off-notes in pea- and soy-based meat alternatives. Microencapsulation extends volatile-compound shelf life and enables controlled-release profiles, citrus top notes that bloom upon chewing, or cooling sensations that persist for 30 seconds post-consumption. These capabilities are not mere technical curiosities; they enable margin expansion by reducing flavor-dosage rates (encapsulation boosts potency 2 to 3 times) and SKU differentiation in crowded categories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory scrutiny and stringent additive regulations | -0.4% | National, with heightened enforcement in tier-1 cities | Short term (≤ 2 years) |

| Consumer health concerns over synthetic additives | -0.3% | National, pronounced among millennial and Gen-Z cohorts | Medium term (2-4 years) |

| Volatile raw-material prices | -0.5% | National, import-dependent supply chains most exposed | Short term (≤ 2 years) |

| High production cost of natural/clean-label flavor enhancers | -0.4% | National, affecting small and mid-sized processors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny and Stringent Additive Regulations

GB 2760-2024's February 8, 2025, implementation mandates explicit disclosure of all flavor components, eliminating the "natural flavoring" catch-all that previously obscured formulation details. Enforcement is intensifying: China's Supreme People's Procuratorate filed 5,126 food-safety public-interest lawsuits in Q1 2024 alone, signaling zero tolerance for non-compliance. An 8-month meat-product safety crackdown launched in 2024 scrutinized additive usage across 200,000+ facilities, resulting in thousands of citations for undeclared flavor enhancers. This regulatory tightening raises compliance costs, reformulation, lab testing, and label redesign, disproportionately burdening small processors who lack in-house regulatory affairs teams. Multinational suppliers benefit from global compliance infrastructure; DSM-Firmenich's four China R&D centers can rapidly adapt formulations to meet evolving GB standards, whereas local flavor houses often lag 6 to 12 months behind regulatory updates.

Consumer Health Concerns Over Synthetic Additives

Latiao consumers' 46.37% concern rate regarding excessive additives reflects broader anxieties about synthetic ingredients, particularly among parents purchasing for children. Social-media amplification of food-safety incidents, even isolated cases, triggers nationwide brand boycotts within days, making synthetic-additive avoidance a reputational imperative. This sentiment is reshaping product portfolios: Haitian Flavouring, China's largest soy-sauce producer, reported 9.38% revenue growth in 2024, partly attributed to premium naturally brewed lines that command 20–30% price premiums over synthetic-amino-acid variants. However, the health-halo effect of "natural" claims is not uniformly distributed; tier-3 and tier-4 cities exhibit lower willingness to pay for clean-label products, creating a bifurcated market where synthetic flavors retain volume dominance even as natural variants capture value growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enhancers Gain as Umami Platforms Mature

Food Enhancer segments are forecast to grow at 6.61% through 2031, outpacing the broader market's 6.23% CAGR, as yeast extracts and fermentation-derived umami compounds displace traditional MSG in premium applications. Angel Yeast, commanding 310,000 tons of global yeast-extract capacity, reported CNY 3.81 billion in yeast-extract revenue for 2023, up 4.75%, underscoring how kokumi and umami-enhancing peptides are penetrating savory snacks, soups, and plant-based meat. Meihua Bio's November 2024 acquisition of Kyowa Hakko's food and pharmaceutical amino-acid business for approximately CNY 500 million signals consolidation in the nucleotide space, where disodium inosinate and guanylate (I+G) blends deliver 5 to 10 times MSG's potency at lower dosage rates.

Food Flavor, holding 75.82% of 2025 revenue, remains the volume workhorse, driven by bakery, confectionery, and beverage applications where sensory differentiation is paramount. However, margin pressures from raw-material volatility and clean-label reformulation costs are compressing profitability in commodity flavor segments. IFF's October 2024 inauguration of its USD 100 million Shanghai Creative Center, spanning 16,000 square meters and housing 200+ flavorists, exemplifies the capital intensity required to maintain flavor-library depth and rapid-prototyping capabilities in a market where SKU lifecycles have compressed from 18 months to 6 months. The strategic pivot is toward modular flavor platforms that allow processors to launch line extensions without full reformulation, reducing time-to-market and R&D amortization per SKU.

By Category: Natural Gains Traction Despite Synthetic's Cost Advantage

Natural flavors are expanding at 6.79% through 2031, the fastest rate across Type segments, propelled by GB 2760-2024's transparency mandates and consumer health anxieties that 46.37% of latiao buyers cite as purchase deterrents. Tate & Lyle's June 2022 acquisition of Quantum Hi-Tech for USD 238 million brought fructooligosaccharide (FOS) and galactooligosaccharide (GOS) capabilities, enabling natural sweetness and mouthfeel enhancement without synthetic additives. The company's Jiangsu stevia-agriculture program achieved 74% fertilizer reduction and 56% greenhouse-gas abatement, demonstrating that sustainability credentials can justify premium pricing in export-oriented supply chains. Fermentation-derived "nature-identical" compounds occupy a regulatory middle ground, chemically indistinguishable from botanical extracts but biosynthesized, offering cost-performance advantages that are narrowing the natural-synthetic price gap.

Synthetic formulations, commanding 71.98% of the 2025 share, retain dominance in cost-sensitive applications where sensory performance and regulatory compliance outweigh clean-label positioning. China produces 2 to 2.5 million tons of MSG annually, 70% of global supply, anchoring a mature synthetic-umami ecosystem that includes Fufeng Group's 1-million-ton capacity. However, synthetics' share erosion is structural rather than cyclical: export-market compliance (EU Regulation 1334/2008, FDA GRAS) increasingly mandates natural declarations, forcing dual-formulation strategies where domestic SKUs use synthetics while export variants employ natural alternatives. Nature-Identical compounds, though a smaller segment, are growing as precision fermentation scales; Symrise's Wing Biotechnology acquisition in China targets vanillin and citrus-terpene production via microbial platforms that achieve synthetic-level costs with natural-equivalent labelling.

By Form: Powder Logistics Edge Versus Liquid Potency

Powder formats are forecast to grow at 7.12% through 2031, the highest rate among Form segments, driven by distribution economics in tier-2 and tier-3 cities where cold-chain infrastructure remains patchy. Spray-dried and encapsulated powders eliminate refrigeration requirements, reducing logistics costs by 15–25% and extending shelf life from 6 months (liquid) to 18–24 months. This durability advantage is critical for e-commerce fulfillment, where ambient-temperature storage and multi-leg distribution favor powder over liquid. Microencapsulation technologies are enhancing powder performance; controlled-release coatings protect volatile compounds during thermal processing and enable staged flavor release, citrus top notes upon chewing, followed by umami depth, creating sensory complexity previously achievable only with liquid systems.

Liquid flavors, holding 35.21% of the 2025 share, retain dominance in beverage and dairy applications where aqueous solubility and dosing precision are non-negotiable. China's beverage market exceeded USD 170 billion in 2024, growing 6% year-on-year, with functional drinks expanding at 10.6% and sugar-free wellness waters projected to achieve growth through 2028. These categories demand liquid-flavor systems that disperse uniformly in low-pH, low-sugar matrices without precipitation or haze formation. Yili Group's 2024 innovations in enzymatic fat modification for dairy, enhancing flavor release and mouthfeel, illustrate how liquid formulations enable ingredient-technology synergies unattainable with powder. The "Others" category, encompassing pastes, gels, and emulsions, serves niche applications like bakery fillings and confectionery centers where texture and flavor must co-deliver; these formats are growing modestly but command premium pricing due to formulation complexity.

By Application: Beverages Accelerate as Savory Snacks Mature

Beverages are expanding at 7.03% through 2031, outpacing the 6.23% market CAGR, as functional-drink proliferation and sugar-reduction mandates create demand for flavor systems that mask stevia bitterness and amplify fruit-forward profiles. Functional beverages grew 26% CAGR from 2020 to 2024, with traditional Chinese medicinal ingredients (goji, ginseng, red dates) requiring flavor technologies that balance herbal astringency against consumer sweetness expectations. Sugar-free wellness waters, projected to achieve growth through 2028, rely on natural-flavor concentrates to deliver sensory satisfaction without caloric load, pushing suppliers to develop ultra-low-dosage systems (0.01–0.05% by weight) that maintain flavor intensity. Tetra Pak's 2024 dairy-processing innovations for bakery and confectionery applications demonstrate cross-category technology transfer, where beverage-flavor encapsulation techniques are adapted for solid-food matrices.

Savory snacks, commanding 23.35% of the 2025 share, remain the largest application but face maturity headwinds; latiao's CNY 83.48 billion market in 2024 is forecast to grow only 5.5% annually through 2026, below the overall market rate. Consumer fatigue with existing flavor profiles, 38.07% cite insufficient innovation, is driving demand for regional-cuisine authenticity (Sichuan mala, Hunan sour-spicy) and global-fusion variants (Korean gochugaru, Japanese yuzu). This premiumization shift favors flavor houses with localized sensory labs; Givaudan's TasteEssentials platform and IFF's Shanghai Creative Center enable rapid prototyping of region-specific profiles that can be validated with consumer panels within 4 to 6 weeks. Dairy applications leverage yeast extracts for umami depth in cheese and fermented products, while Bakery and Confectionery segments are experimenting with osmanthus, jasmine, and lychee to differentiate yogurt and pastry SKUs in saturated categories. Meat applications, though smaller, are critical for plant-based alternatives where flavor masking of pea and soy off-notes determines consumer acceptance; enzymatic hydrolysis and Maillard-reaction precursors are enabling chicken and pork analogs that pass blind taste tests against animal proteins.

Competitive Landscape

The China Food Flavors and Enhancers Market exhibits a moderate concentration score, reflecting a duopoly dynamic where multinational ingredient conglomerates (IFF, DSM-Firmenich, Givaudan, Symrise) control premium segments through IP-protected flavor libraries and global R&D networks, while domestic champions (Angel Yeast, Huabao International, Meihua Bio) dominate cost-sensitive and fermentation-derived categories via scale manufacturing and local-sourcing advantages. IFF's October 2024 launch of its USD 100 million Shanghai Creative Center, 16,000 square meters housing 200+ flavorists and AI-driven sensory prediction, exemplifies the capital intensity required to maintain competitive moats in a market where SKU lifecycles have compressed to 6 months. Symrise's July 2024 expansion of its Shanghai Jinqiao powder-blending facility and August 2024 Beijing R&D hub upgrade (EUR 1.5 million, 800 square meters) signal a localization race where proximity to brand customers and speed-to-prototype trump centralized innovation models.

Opportunities cluster around precision fermentation, microbial platforms producing vanillin, nootkatone, and umami peptides at costs approaching synthetic parity, and plant-based meat flavor masking, where off-note suppression technologies command 20–30% premiums over commodity flavor systems. Strategic bifurcation is evident: multinationals pursue premiumization through clean-label reformulation and sensory-science differentiation, while domestic players leverage vertical integration and fermentation-platform economics to defend volume share. Angel Yeast's 310,000-ton global yeast-extract capacity and CNY 3.81 billion segment revenue in 2023 illustrate how biomanufacturing scale creates cost structures unattainable via botanical extraction. Meihua Bio's November 2024 acquisition of Kyowa Hakko's amino-acid business for approximately CNY 500 million consolidates nucleotide (I+G) supply, positioning the company to capture margin expansion as MSG-alternative adoption accelerates.

Emerging disruptors include precision-biology startups partnering with established players, Symrise's Wing Biotechnology acquisition targets fermentation-derived citrus terpenes, and ingredient-technology hybrids like enzymatic fat modification (Yili Group) that blur boundaries between flavor, texture, and nutrition. Compliance with GB 2760-2024 and ISO 22000 food-safety standards is table stakes, but leaders are differentiating through sustainability certifications (Tate & Lyle's 74% fertilizer-reduction stevia program) and traceability platforms that satisfy export-market due diligence.

China Food Flavors and Enhancers Industry Leaders

-

International Flavors & Fragrances Inc.

-

DSM-Firmenich AG

-

Givaudan SA

-

Symrise AG

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2021: U.S. grain merchant Archer-Daniels-Midland Co (ADM.N), opened a new flavour production facility in China to meet the growing demand for beverages and healthy foods. The new facility - ADM Food Technology (Pinghu) Co Ltd, located in the eastern province of Zhejiang and about one hour away from Shanghai - marks a further expansion by the global grains trader in the nutrition segment.

- April 2021: Kerry Group announced its acquisition of Jining Nature Group, a Shandong, China-based producer of savory flavors, seasonings, and prepared food products. Kerry stated that acquiring Jining Nature Group would broaden its customer base in China, granting enhanced access to the nation's vast regional markets through established distribution and foodservice channels.

China Food Flavors and Enhancers Market Report Scope

The China Food Flavors and Enhancers Market is segmented by product type, category, form, and application. By product type, the market is segmented into food flavor and food enhancer. By type, the market is segmented into natural, synthetic, and nature-identical. By form, the market is segmented into powder, liquid, and others. By application, the market is segmented into dairy, bakery, confectionery, savory snack, meat, beverages, and other applications. the market forecasts are provided in terms of value (USD).

By Product Type

| Food Flavor |

| Food Enhancer |

By Category

| Natural |

| Synthetic |

| Nature-Identical |

By Form

| Powder |

| Liquid |

| Others |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverages |

| Other Applications |

| By Product Type | Food Flavor |

| Food Enhancer | |

| By Category | Natural |

| Synthetic | |

| Nature-Identical | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Application | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snack | |

| Meat | |

| Beverages | |

| Other Applications |

Key Questions Answered in the Report

What is the 2026 value of the China food flavor market?

The food flavor market size is USD 2.99 billion in 2026.

How fast will the sector grow by 2031?

It is forecast to expand at a 6.23% CAGR, reaching USD 4.05 billion.

Which segment is growing faster, flavors or enhancers?

Food enhancers lead with a 6.61% CAGR through 2031, outpacing core flavors.

Page last updated on: