China Feed Enzymes Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

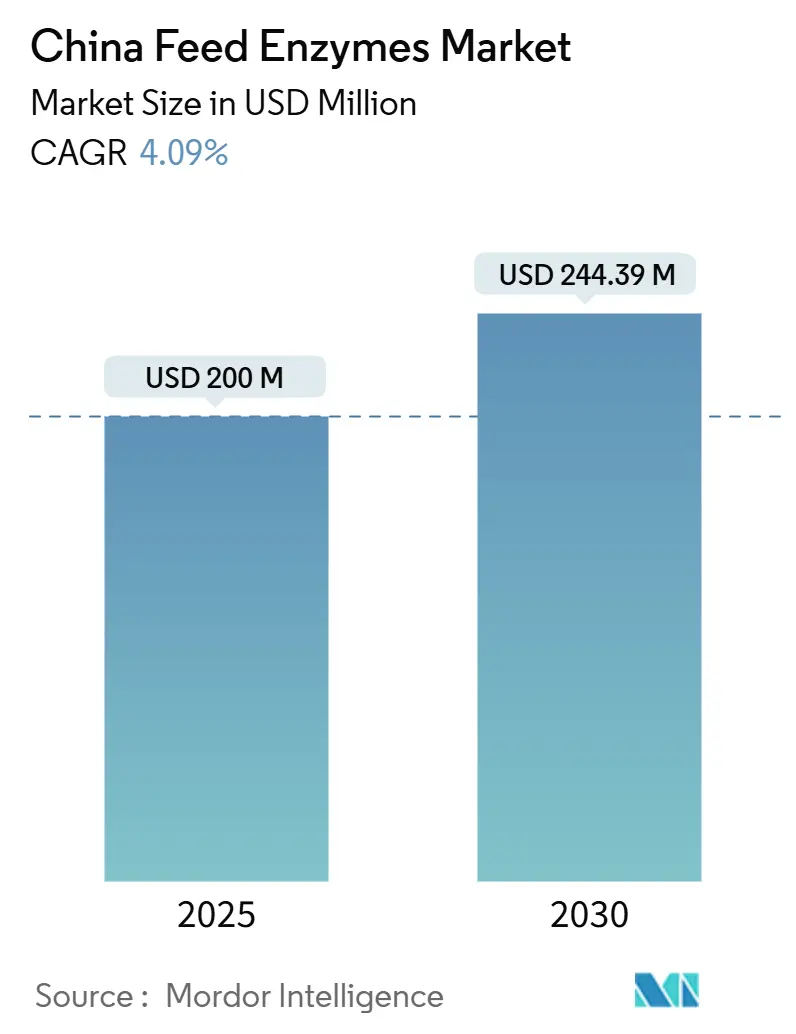

| Market Size (2025) | USD 200 Million |

| Market Size (2030) | USD 244.39 Million |

| Growth Rate (2025 - 2030) | 4.09% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Feed Enzymes Market Analysis by Mordor Intelligence

The China feed enzymes market size stands at USD 200.00 million in 2025 and is forecast to reach USD 244.39 million by 2030, advancing at a 4.09% CAGR over the period. Demand grows as the livestock sector adapts to the Ministry of Agriculture and Rural Affairs (MARA) feed-protein reduction mandates, antibiotic-free production rules, precision-feeding systems, and aquaculture decarbonization subsidies. Carbohydrase adoption remains widespread because it improves corn–soybean diet energy, while phytase gains momentum under phosphorus discharge limits. Large integrators are installing real-time dosing platforms that raise enzyme utilization efficiency, and domestic biotech scale-ups are narrowing price gaps with imported brands. Meanwhile, mycotoxin co-contamination and tariff-induced cost pressures shape buying cycles, pushing suppliers to offer stabilized, heat-resistant products and responsive technical support.

Key Report Takeaways

- By sub-additive, carbohydrases led with 46.0% of the China feed enzymes market share in 2024; phytases are projected to expand at a 4.13% CAGR to 2030.

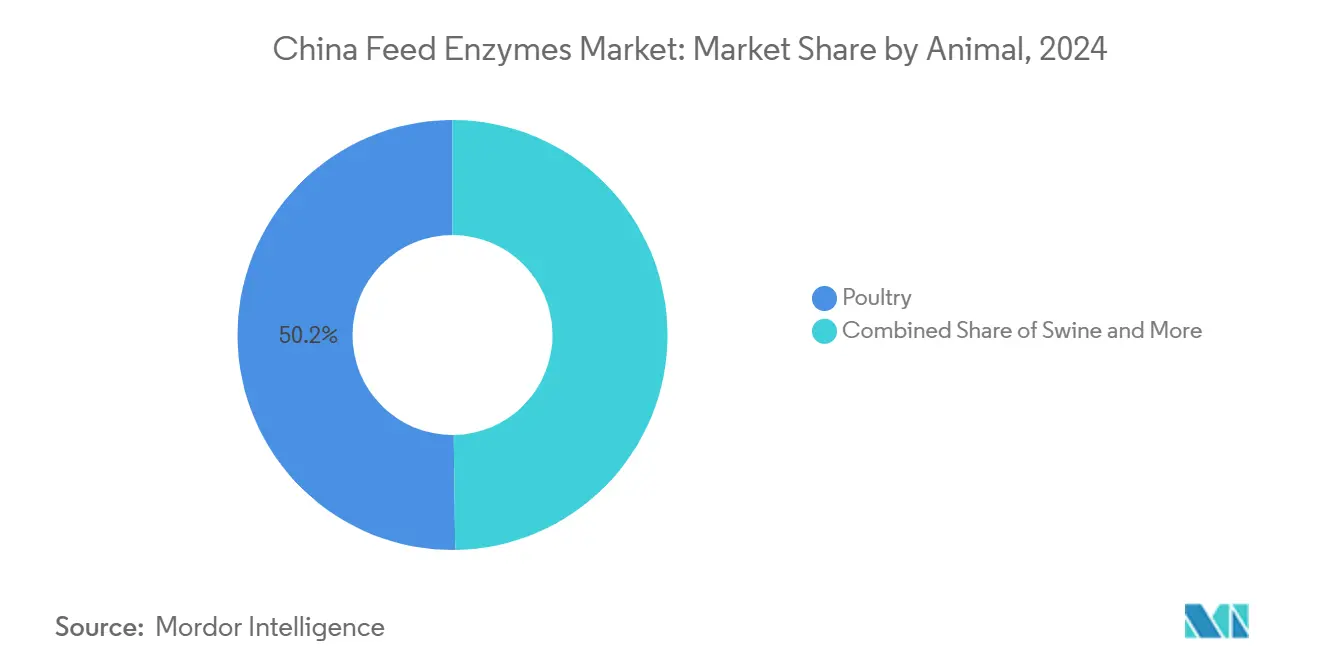

- By animal, poultry held 50.2% of the China feed enzymes market size in 2024, while the “other animals” category is forecast to rise fastest at a 4.95% CAGR through 2030.

China Feed Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed-protein reduction mandates from MARA spur phytase uptake | +0.8% | National, concentrated in major pig and poultry regions | Medium term (2-4 years) |

| Antibiotic-free livestock policies elevate multi-enzyme blends | +0.7% | National, early adoption in integrated operations | Medium term (2-4 years) |

| Large-scale pig and poultry integrator upgrades to precision-feeding tech | +0.6% | Shandong, Henan, Guangdong production clusters | Short term (≤ 2 years) |

| High mycotoxin co-contamination drives demand for detox-enzyme combos | +0.5% | Southern China humid regions, seasonal peaks | Short term (≤ 2 years) |

| Subsidies for low-carbon aquaculture favor carbohydrase use in plant-rich diets | +0.4% | Coastal provinces, freshwater aquaculture zones | Long term (≥ 4 years) |

| Domestic biotech scale-up lowers price barriers | +0.3% | National, concentrated in biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Feed-Protein Reduction Mandates from MARA Spur Phytase Uptake

MARA’s campaign to push soybean-meal inclusion below 13% of compound feed by 2025 compels mills to unlock bound phosphorus, making phytase indispensable in reformulated diets. Shandong’s Linyi cluster alone logs 4.78 million pigs and 17 billion poultry annually[1]Source: Guochu Report, “Shandong Linyi Meat Industry Hub: 4.78 Million Pigs and 17 Billion Poultry,” mp.weixin.qq.com. The policy eases soybean import dependence, curbs phosphorus runoff, and aligns with carbon-reduction goals. Domestic suppliers that navigate MARA dossiers quickly profit from first-mover status, while global brands leverage high-purity strains to protect premium positions. Adoption will intensify in medium-term budgets as mills retrofit pelleting lines for heat-stable phytases.

Antibiotic-Free Livestock Policies Elevate Multi-Enzyme Blends

China’s 2025 prohibition of antibiotic growth promoters shifts nutritional strategies toward digestive support solutions. Multi-enzyme cocktails combining protease, xylanase, and amylase deliver feed conversion improvements, matching the performance once attributed to in-feed antibiotics. Integrated producers in Shandong and Henan embed these blends into precision diets and rely on supplier field teams for in-barn calibration. Regulatory scrutiny raises documentation demands, giving established firms an edge. As consumer labeling for “antibiotic-free” meats spreads across tier-one cities, enzyme inclusion is becoming a branding necessity as well as a productivity tool.

Large-Scale Pig and Poultry Integrator Upgrades to Precision-Feeding Tech

Major livestock integrators across China's primary production regions implement precision feeding systems that optimize enzyme dosing based on real-time feed composition and animal performance metrics. Muyuan Group's deployment of AI-driven feeding systems achieved cost reductions through precise nutrient delivery, while similar technologies adopted by regional integrators in Shandong's Linyi cluster support. The technology adoption creates demand for enzyme products with consistent activity profiles and precise dosing capabilities, favoring suppliers who can provide technical support and formulation expertise. Integration with feed mill automation systems requires enzyme products that maintain stability during mixing, pelleting, and storage processes, driving innovation in enzyme coating and stabilization technologies.

High Mycotoxin Co-Contamination Drives Demand for Detox-Enzyme Combos

Southern provinces report 60–80% mycotoxin positivity in feed samples, with 70% showing multiple toxins during summer harvests. Enzymatic detoxifiers that convert aflatoxin B1 or deoxynivalenol into non-toxic metabolites outperform conventional binders in warm, humid storage environments. The seasonal nature of mycotoxin contamination, peaking during humid summer months and harvest periods, creates cyclical demand patterns that favor enzyme suppliers with flexible production capacity and rapid response capabilities. Feed manufacturers in Guangdong, Fujian, and Jiangxi provinces increasingly adopt enzyme-based mycotoxin management as part of comprehensive feed safety programs, supported by MARA's recognition of enzyme-based detoxification methods in feed safety regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MARA's new-enzyme approval timeline slows launches | -0.4% | National regulatory bottleneck | Medium term (2-4 years) |

| Volatile feedstock prices compress feedmill margins and delay additive spend | -0.3% | National, acute in corn-deficient regions | Short term (≤ 2 years) |

| Import tariff on enzyme fermentation media raises costs | -0.2% | National, affecting international suppliers | Short term (≤ 2 years) |

| Enzyme-activity loss during high-temp pelleting in small regional mills | -0.2% | Regional mills in secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MARA New-Enzyme Approval Timeline Slows Launches

Novel strains must pass toxicology, efficacy, genomics, and manufacturing audits that extend registration cycles to 12–18 months, delaying commercialization and dampening innovation rhythms. The approval bottleneck particularly affects innovative enzyme combinations and novel microbial strains that could address emerging nutritional challenges in alternative protein sources. International suppliers face additional complexity navigating China's regulatory system, while domestic companies leverage local regulatory knowledge to accelerate approval processes for incremental product improvements.

Volatile Feedstock Prices Compress Feedmill Margins and Delay Additive Spend

Corn prices swing seasonally, squeezing feedmill margins that hover at 3–5%. During spikes, mills defer premium additive purchases or down-spec formulations, temporarily denting enzyme demand. The price volatility particularly affects smaller regional mills that lack purchasing power and storage capacity to buffer against commodity price swings. Soybean meal price fluctuations, driven by import dependency and trade dynamics, create additional margin pressure that limits feed manufacturers' willingness to invest in premium enzyme solutions. The cyclical nature of feedstock price volatility creates unpredictable demand patterns for enzyme suppliers, requiring flexible pricing strategies and inventory management to maintain market share during high-cost periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Carbohydrases Lead Through Corn-Diet Optimization

Carbohydrases captured 46% of the China feed enzymes market share in 2024 as mills rely on xylanase, beta-glucanase, and cellulase to unlock 3–5% extra metabolisable energy from corn-soybean rations. The China feed enzymes market size attributable to carbohydrases is projected to reach a good place by 2030, advancing alongside continuous corn price volatility and stricter energy-use audits. The segment benefits from research showing coated xylanase retains 85% activity after 90 °C pelleting, supporting uptake in small and mid-size mills. Suppliers differentiate through multi-substrate specificity, granular particle uniformity for low dust, and data-backed dose matrices that tie enzyme cost to kilocalorie savings.

Phytase, though smaller in value, posts the fastest 4.13% CAGR as MARA’s phosphorus discharge caps necessitate inclusion in high-density broiler and layer complexes. The China feed enzymes market size for phytase is projected to climb by 2030. Domestic fermentation scale-ups anchor price points under USD 7/kg, narrowing gaps with mineral phosphorus, while next-gen 6-phytase variants cut inclusion rates by 20%. “Other enzymes,” mainly protease and lipase, remain niche but gain in antibiotic-free production and alternative protein diets.

By Animal: Poultry Dominance Reflects Production Scale

Poultry’s 50.2% grip on the China feed enzymes market in 2024 mirrors the sector’s 10 billion-bird annual slaughter, concentrated in Shandong, Henan, and Guangdong integrators that operate closed-loop feed-to-food models. Phytase and carbohydrase bundles drive feed conversion ratio (FCR) improvements of 5–7%, making enzymes a line-item in every phase feed. The China feed enzymes market size tied to poultry is forecast to reach a high by 2030, with layer operations embracing phytase to curb phosphorus excretion under tightened manure regulations.

“Other animals”, aquaculture, rabbits, and emerging specialty livestock show a 4.95% CAGR, the fastest within the matrix. Carbohydrase demand escalates in aquafeed, where plant-based protein inclusion can exceed 60% and where enzyme-aided digestion offsets fishmeal cuts mandated under low-carbon subsidy schemes. Swine, recovering from African swine fever, sustains steady enzyme use as large producers target a 2.5:1 feed-to-gain ratio ceiling. Ruminants currently lag due to forage-heavy diets, but precision feeding in confined dairy units is opening windows for fibrolytic enzymes tailored to silage variability.

Geography Analysis

Shandong, Henan, and Guangdong collectively consume a major share of national enzyme tonnage owing to dense livestock inventories, integrated feed mills, and early adoption of precision-feeding technologies. Shandong’s Linyi cluster logs a good population of pigs and poultry, underpinning continuous demand for high-activity carbohydrases and thermostable phytases. Feed mills here often exceed 300,000 metric tons capacity and deploy liquid-enzyme spraying systems, positioning the region as a test bed for next-generation blends.

Southern provinces, Guangdong, Fujian, and Jiangxi, experience seasonal spikes in enzyme orders aligned with humidity-driven mycotoxin outbreaks. Detox-enzyme combos displace clay binders during wet months, and coastal aquaculture farms tap carbohydrase solutions to utilize rapeseed and peanut meals incentivized under low-carbon grants.

Western provinces such as Inner Mongolia and Xinjiang exhibit lower penetration, yet rising investments in large dairy and beef feedlots are boosting trials of fibrolytic enzymes suited to silage-heavy rations. Lower corn costs allow room in ration budgets for digestibility enhancers, and local governments partner with state banks to finance pelleting and post-pellet liquid application equipment, priming long-term growth even in historically extensive systems.

Competitive Landscape

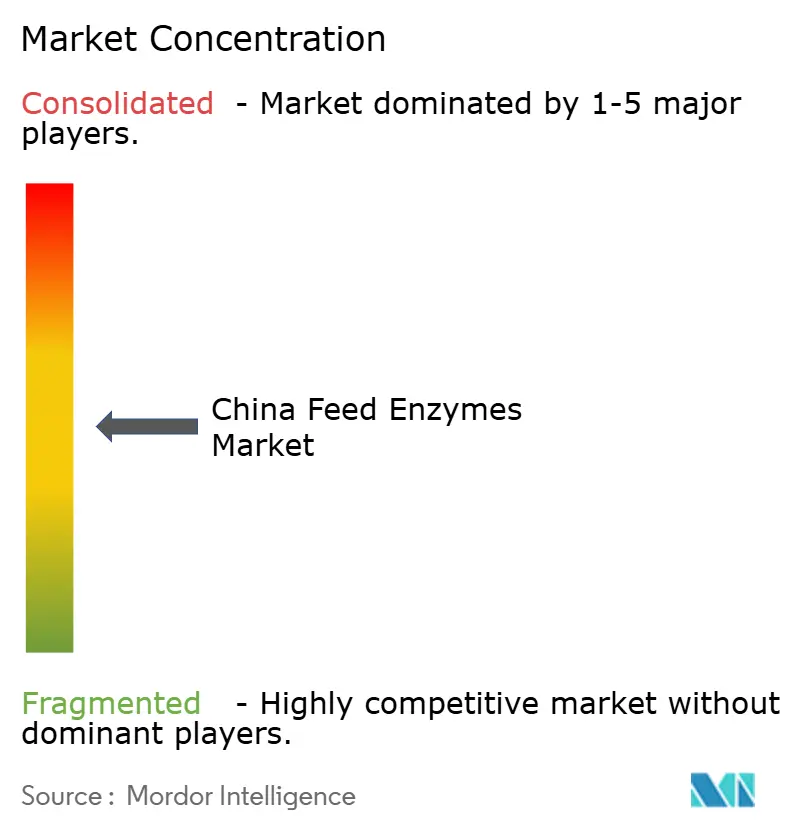

The China feed enzymes market is moderately concentrated; the top five players hold a combined good share. Domestic challengers Angel Yeast, Sunson, and Pangbo leverage local regulatory fluency and cost advantages rooted in homegrown fermentation substrates. Angel Yeast’s approval for yeast protein in 2024 burnished its image as a biotech innovator and opened cross-selling scenarios for protease and carbohydrase packages in microbial-protein feeds[2]Source: Plant-Based Net, “Yeast Protein to Lead Future Protein Market,” plantbasednet.cn .

Global incumbents like Novonesis, Alltech, and others anchor the premium tier with broad portfolios, validated efficacy dossiers, and embedded technical field teams. Novonesis’ 2024 merger fortified its fermentation depth and pipeline, broadening coated phytase offerings that meet MARA’s safety norms faster than standalone innovations[3]Source: Novonesis, "investors-annual-report", novonesis.com. Sunson’s 2024 capacity expansion, incorporating submerged fermentation control tech, trimmed batch cycle times by 18%, enabling prompt deliveries during peak mycotoxin seasons.

Strategic moves increasingly revolve around precision-feeding integration. Global firms hedge tariff impacts by co-fermenting with Vland and Meihua, whereas domestic suppliers court export markets in Southeast Asia to scale further. Patent landscapes focus on thermostable coatings and broad-substrate specificity, with 14 enzyme-coating patents filed in China during 2024 alone.

China Feed Enzymes Industry Leaders

-

Adisseo

-

Elanco Animal Health Inc.

-

IFF(Danisco Animal Nutrition)

-

Kerry Group PLC

-

Novonesis A/S (DSM-Firmenich)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Meihua Bio bought Kirin’s amino-acid assets for CNY 500 million (USD 70 million), bolstering its fermentation raw-material chain.

- March 2024: Evonik and Vland set up a joint venture for amino-acid production, integrating fermentation know-how with local logistics.

- January 2024: Novonesis finalized its merger with Chr. Hansen, creating a larger enzyme portfolio targeting heat-stable phytase and coated carbohydrase solutions.

China Feed Enzymes Market Report Scope

Carbohydrases, Phytases are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal.| Carbohydrases |

| Phytases |

| Other Enzymes |

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

| Sub Additive | Carbohydrases | |

| Phytases | ||

| Other Enzymes | ||

| Animal | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms