Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

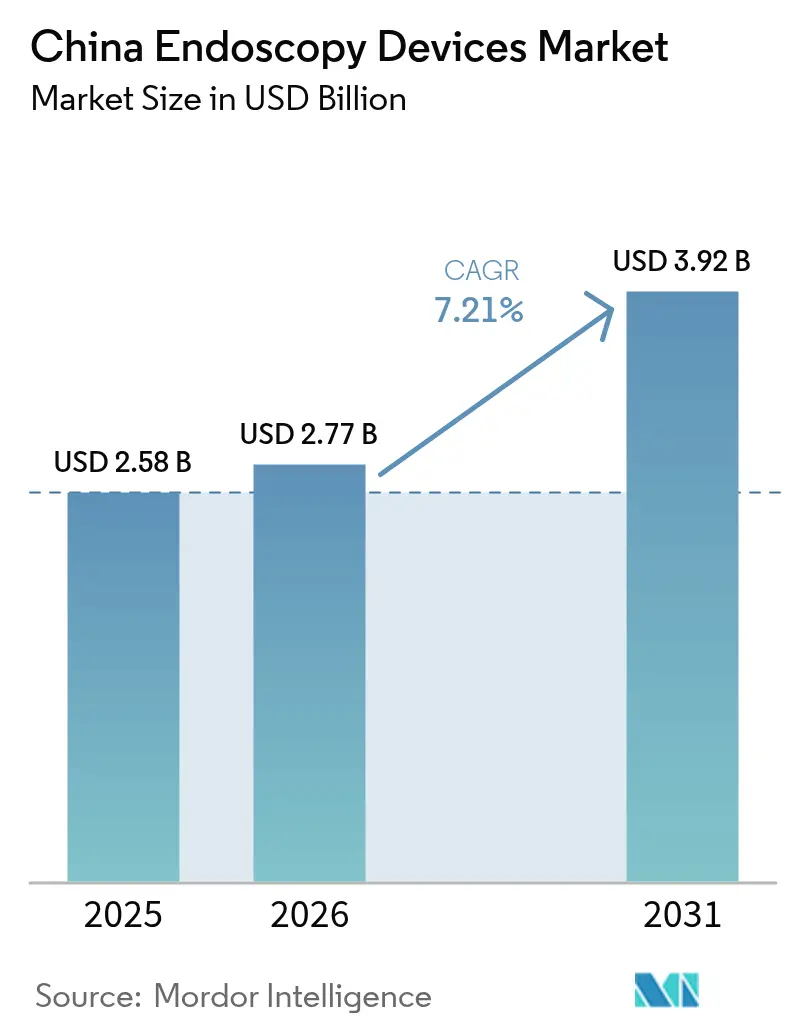

| Base Year Market Size (2025) | USD 2.58 Billion |

| Market Size (2026) | USD 2.77 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

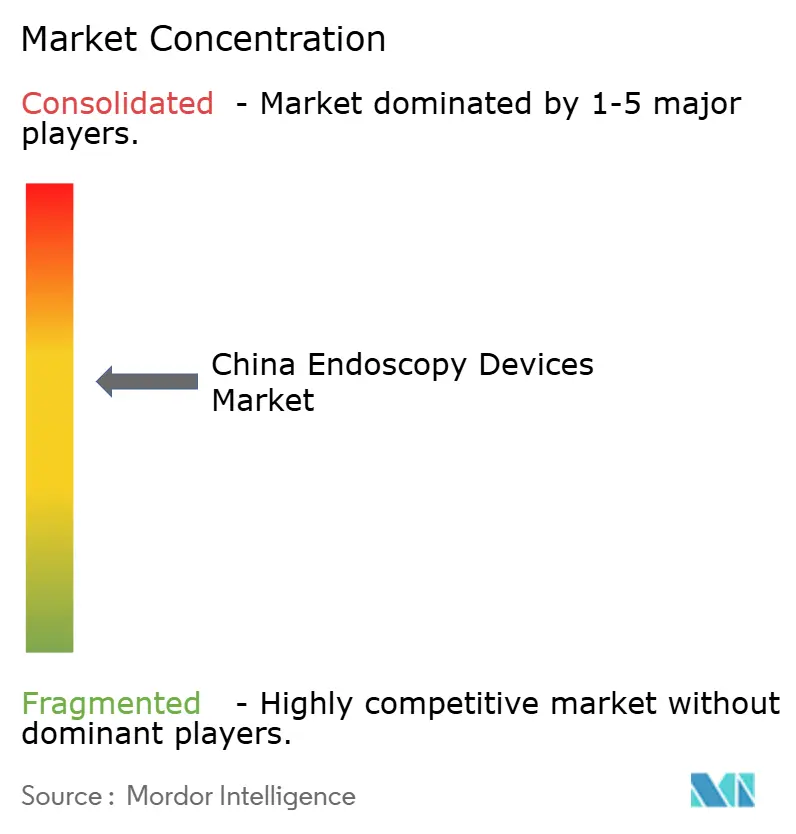

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Endoscopy Devices Market Analysis by Mordor Intelligence

The China endoscopy devices market size was valued at USD 2.58 billion in 2025 and estimated to grow from USD 2.77 billion in 2026 to reach USD 3.92 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031). Growth is underpinned by an aging population—26% of citizens will be at least 65 years old by 2050—together with national cancer-control goals that mandate earlier detection and wider procedural access. Rapid uptake of 4K/3D/AI visualization platforms, a shift toward single-use scopes, and wider insurance coverage for minimally invasive techniques are reinforcing demand. Domestic innovators are scaling output under the “Made in China 2025” localization target, eroding the longstanding dominance of imported models. Parallel investments in tertiary-hospital capacity and dedicated training hubs are easing procedural bottlenecks, while the National Medical Products Administration (NMPA) is accelerating approvals for high-technology systems. Collectively, these forces are creating multi-layered opportunities across hardware, software, and after-sales services inside the China endoscopy devices market.

Key Report Takeaways

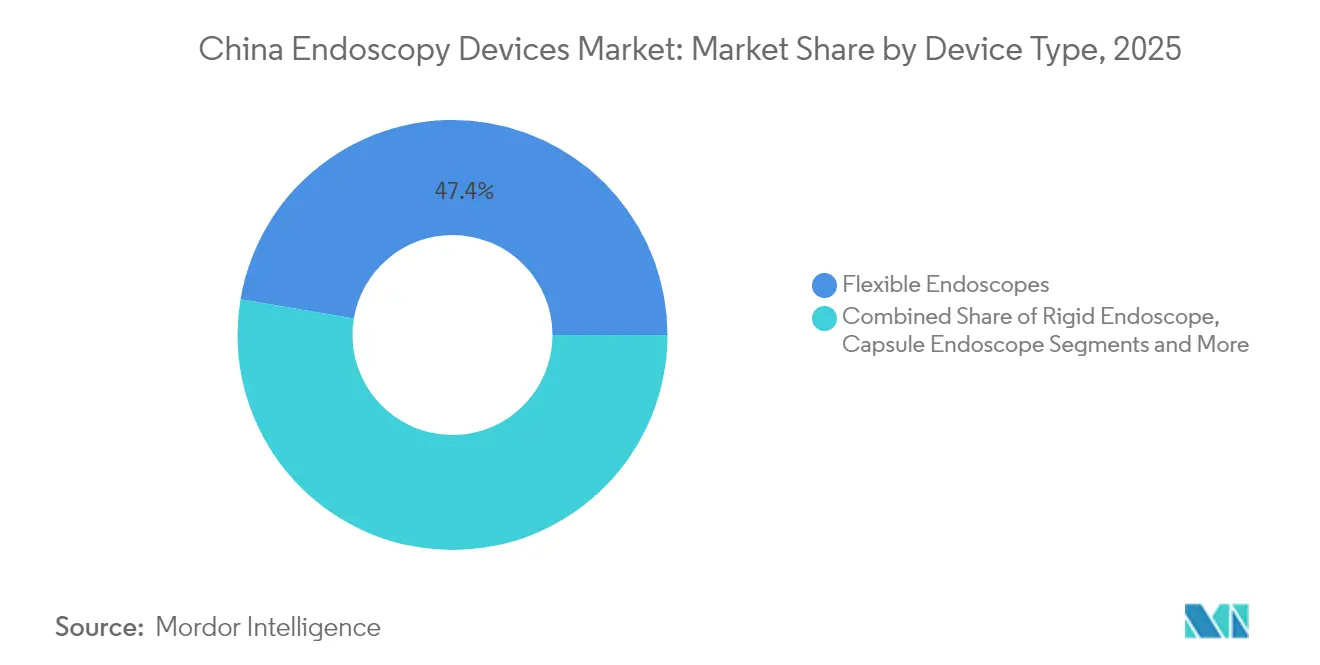

- By device type, flexible endoscopes led with 47.35% of China endoscopy devices market share in 2025; robot-assisted platforms are projected to grow at a 14.10% CAGR through 2031.

- By application, gastroenterology held 41.55% revenue share in 2025, while pulmonology is forecast to expand at a 9.85% CAGR to 2031.

- By end user, Class III hospitals accounted for 72.25% of the China endoscopy devices market size in 2025; Ambulatory Surgery Centers are advancing at a 9.10% CAGR.

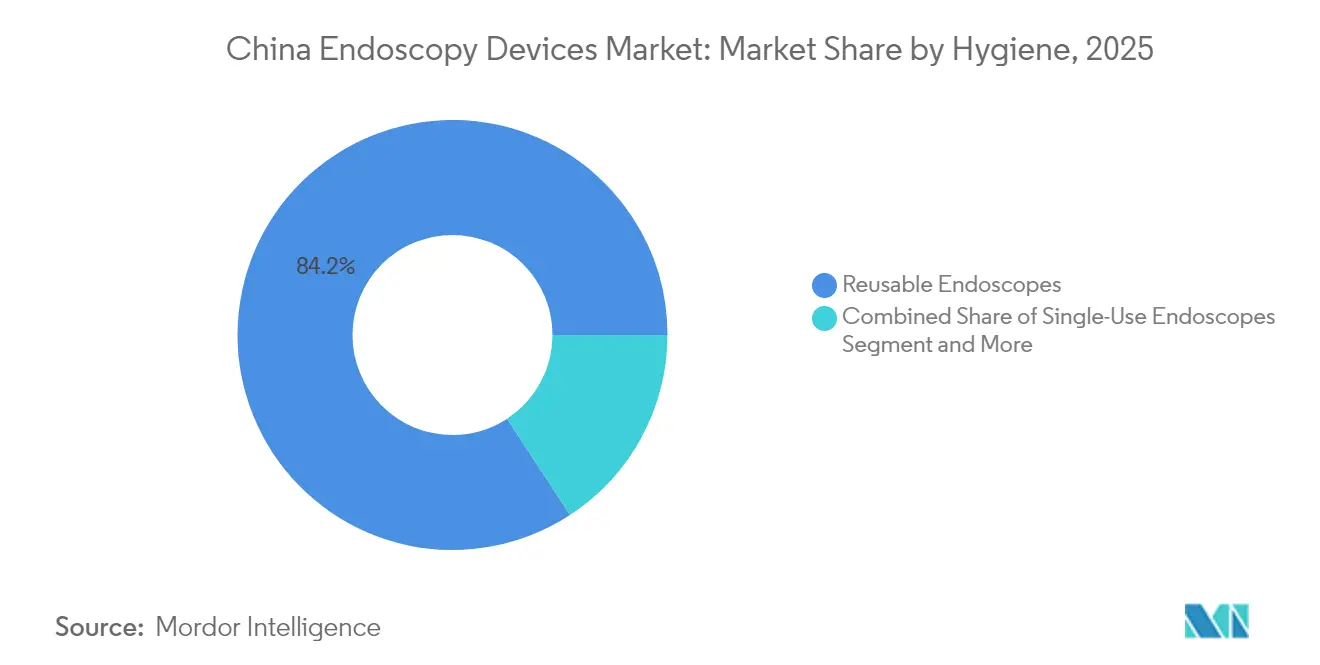

- By hygiene category, reusable systems captured 84.20% share in 2025, yet single-use models are set to rise at a 13.90% CAGR through 2031.

- By technology tier, HD platforms dominated with 62.10% share of overall value in 2025, whereas 4K/3D/AI solutions will climb at a 13.70% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Gastrointestinal Diseases Coupled with Growing Aging Population | +2.1% | National, with higher impact in urban centers and eastern provinces | Long term (≥ 4 years) |

| Technological Advancements in Endoscopy Equipment | +1.8% | National, with initial concentration in tier-1 cities | Medium term (2-4 years) |

| Expanding Healthcare Infrastructure and Medical Tourism | +1.4% | National, with emphasis on eastern coastal regions and major metropolitan areas | Medium term (2-4 years) |

| Government Initiatives and Support for Medical Devices | +1.6% | National, with stronger influence in regions prioritized in healthcare development plans | Medium term (2-4 years) |

| Growing Adoption of Minimally Invasive Procedures | +0.7% | National, with higher penetration in Class III hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gastrointestinal Diseases Coupled with Growing Aging Population

Gastrointestinal disorders are climbing in tandem with China’s demographic shift toward later-life morbidity. Among citizens aged 80 and over, multimorbidity already affects 40.2% of individuals[1]Yaoda Hu et al., “Prevalence and Patterns of Multimorbidity in China during 2002-2022,” Ageing Research Reviews, onlinelibrary.wiley.com. Government-funded screening pilots show incremental cost-effectiveness ratios as low as USD 1,343 per QALY, confirming fiscal viability for large-scale roll-outs. These economics, combined with public awareness campaigns, drive steady throughput in colonoscopy and EGD suites inside the China endoscopy devices market.

Technological Advancements in Endoscopy Equipment

Artificial-intelligence engines now cut capsule-review time by 89.3% while boosting lesion detection to 95.9% versus manual reads. Robotic bronchoscopy systems such as the MONARCH platform extend reach to peripheral nodules, broadening therapeutic indications. Integrated 3D 4K fluorescence units combine depth perception, ultra-high definition, and real-time perfusion assessment to improve oncologic margins. Experimental Raman-enabled scopes promise histology-level insight without biopsies, signalling the next frontier in precision diagnostics. These breakthroughs collectively elevate clinical expectations, accelerating capital-equipment replacement cycles throughout the China endoscopy devices market.

Expanding Healthcare Infrastructure and Medical Tourism

Tertiary centers are adding dedicated endoscopy rooms, while Olympus has opened training campuses in Shanghai, Beijing, and Guangzhou to alleviate the nationwide shortfall of qualified operators—just 2.2 endoscopists per 100,000 people versus 25 in Japan[2]“Chinese Market with High Growth Potential,” Integrated Report 2024, olympus-global.com. Parallel growth of Ambulatory Surgery Centers reflects payer and patient preference for shorter stays and lower infection risk. International seminars, often coordinated under Belt & Road academic alliances, are positioning China as a destination for advanced GI fellowships. Infrastructure expansion therefore feeds procedural volumes and skill-transfer flows, reinforcing the scale advantages of the China endoscopy devices market.

Government Initiatives and Support for Medical Devices

The draft Medical Device Administration Law of 2024 abolishes country-of-origin pre-clearance requirements, trimming months off the regulatory clock. Complementary procurement quotas aim for 70% domestic sourcing of high-end equipment. Lifecycle oversight, incentives for R&D, and targeted upgrade budgets under the “Action Plan to Promote Large-scale Equipment Renewals” all lower entry barriers for local manufacturers[3]“NMPA 2025 Regulatory Opinion,” National Medical Products Administration, english.nmpa.gov.cn. The resulting policy environment accelerates innovation, expands production scale, and reshapes competitive hierarchies inside the China endoscopy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Endoscopy Systems | -0.9% | National, with greater impact in lower-tier cities and rural areas | Medium term (2-4 years) |

| Stringent Regulatory Approvals and Certification Processes | -0.6% | National, with uniform application across regions | Short term (≤ 2 years) |

| Limited Reimbursement Policies and Low Insurance Coverage | -0.7% | National, with greater impact in less developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Endoscopy Systems

Capital prices for robotics and fluorescence units remain steep. A leading multi-port surgical robot, now discounted to spur uptake, still saw annual installations fall by nearly 30%. Annual service contracts, repair outlays, and intensive training add invisible overheads, discouraging budget-constrained hospitals. Competitive pricing by emerging local vendors is lowering the barrier, but full convergence with international cost structures is still several years away in the China endoscopy devices market.

Stringent Regulatory Approvals and Certification Processes

Class III devices must present local clinical data and audited quality systems, stretching timelines and cash needs. New provisions covering certificate transfers and local legal-entity liabilities require additional compliance bandwidth. While fast-track lanes for urgently needed technologies are expanding, smaller developers still face resource bottlenecks when navigating multi-layer dossier reviews. This complexity continues to temper near-term installation momentum across the China endoscopy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Robot-Assisted Platforms Redefine Precision

Flexible instruments commanded a 47.35% revenue share in 2025, anchoring the China endoscopy devices market through routine GI, bronchial, and ENT work. Robot-assisted systems, however, represent the fastest CAGR at 14.10% through 2031, driven by demand for sub-millimeter control and integrated AI navigation. High-definition imaging, haptic feedback, and cloud analytics are converting once-experimental prototypes into daily-use assets, particularly for peripheral lung nodules and complex urologic lesions.

Manufacturers are layering fluorescence, 3D visualization, and deep-learning pathology prediction directly into robotic arms, compressing diagnostic and therapeutic cycles. Single-use flexible robots for airway management are also under evaluation, pairing infection-control benefits with mechanical stability. As these innovations roll out, the China endoscopy devices market size for robot platforms is set to outpace legacy categories, although disposable scope ecosystems will remain indispensable in high-volume respiratory clinics.

By Application: Pulmonology Drives Diversification

Gastrointestinal indications held 41.55% of 2025 value and remain the procedural backbone of the China endoscopy devices market. Yet respiratory care shows the steepest curve, with pulmonology devices forecast to rise at 9.85% CAGR on the back of air-pollution-induced COPD and lung-cancer screening mandates. Hospitals are expanding bronchoscopy capacities and adopting microwave ablation catheters that rely on endoscopic guidance for peripheral tumors.

Orthopedic centers are scaling arthroscopic sports-medicine programs, while interventional cardiology is experimenting with micro-endoscopes for valve inspection. ENT clinics maintain consistent demand for laryngoscopes amid rising voice-disorder awareness. Gynecology and neurosurgery remain smaller but high-complexity niches where 4K 3D views are critical. This diversified pipeline reinforces the resilience of the China endoscopy devices market across clinical cycles.

By End User: Ambulatory Centers Gain Momentum

Class III referral hospitals attracted 72.25% of procedure-linked revenue in 2025 thanks to comprehensive ICUs, oncology wings, and leading surgeons. Their volumes create economies of scale for AI servers, robotic suites, and high-end optics, keeping them central to the China endoscopy devices market. Ambulatory Surgery Centers, however, are growing at 9.10% CAGR, mirroring shifts in payer policy and patient preference for same-day discharge.

Community-level Class II facilities and specialty clinics are gradually upgrading from fiber to digital platforms as financing options widen. Portable tower designs and cloud-based service models lower staffing barriers, allowing rural providers to phase in advanced imaging without full-scale infrastructure. This multi-tier end-user mix compels vendors to calibrate sales, training, and after-sales packages for each footprint.

By Hygiene: Single-Use Revolution Transforms Practice

Reusable models still make up 84.20% of units in 2025 because of embedded reprocessing workflows and high upfront cost of disposables. Yet single-use scopes are rising at 13.90% CAGR, powered by zero-contamination guarantees and elimination of repair downtime. Domestic specialists report individual disposable-scope revenue crossing CNY 100 million on specific product lines, signalling rapid clinician acceptance.

Sterilization solutions continue to serve the large installed base, but physical channel complexity in duodenoscopes and bronchoscopes makes perfect cleaning difficult. Hospital administrators increasingly factor litigation risk and staff time into total-cost equations, often tipping purchasing committees toward disposables. Venture funding—such as the USD 14 million Series B closed by MacroLux Medical—underscores confidence in single-use momentum. These dynamics are shifting revenue allocation inside the China endoscopy devices market.

By Technology: AI Integration Drives Diagnostic Revolution

HD towers retained 62.10% value share in 2025 but face rapid cannibalization as 4K/3D/AI bundles post a 13.70% CAGR. Deep-learning overlays flag polyps in real time and prompt tissue characterization scores, giving proceduralists higher confidence and shorter operating times. Fluorescence modules visualize lymphatics and perfusion, cutting conversion-to-open rates in minimally invasive oncology. As componentry prices fall, hospitals in secondary cities are leapfrogging incremental HD upgrades and moving straight to AI-ready 4K suites, reshaping demand curves across the China endoscopy devices market.

Geography Analysis

Eastern coastal provinces—Shanghai, Jiangsu, Zhejiang, Guangdong, and Beijing—accounted for roughly 59.40% of market value in 2025 on the strength of dense Class III networks, higher household incomes, and provincial equipment-upgrade grants. These centers are typically first adopters of fluorescence imaging and robotic bronchoscopic suites, reinforcing a virtuous cycle of case complexity and training opportunities.

Central and western provinces are displaying double-digit growth from a smaller base as targeted subsidies under the large-equipment renewal program funnel capital expenditure toward oncology screening equipment. Domestic manufacturers are penetrating these regions with competitively priced 4K towers and bundled service contracts, aligning with policy goals of reducing coastal-inland disparities.

Rural districts still face the thinnest device density and practitioner ratios. Tele-endoscopy pilots connect county hospitals to urban experts for live consults, while mobile units bring gastroscopy to high-incidence esophageal-cancer belts. The Healthy China 2030 target of a 15% improvement in five-year cancer survival rates is catalyzing provincial governments to equip township clinics with entry-level endoscopy carts, gradually knitting underserved populations into the China endoscopy devices market.

Regulatory Landscape

China endoscopy devices are regulated by the National Medical Products Administration (NMPA). Higher-risk endoscopic systems are typically handled under Class II or Class III pathways, which include registration, type testing, and local clinical evidence where applicable. Mandatory technical and safety compliance anchors include national standards such as GB 9706.218-2021 for basic safety and essential performance, alongside other industry standards applied during product design verification and registration testing.

Regulatory requirements are being updated through multiple NMPA actions in 2025-2026 that affect endoscopy-related dossiers and renewals. NMPA Announcement No. 63 (2025) emphasized optimized whole life-cycle regulation and special review procedures supporting high-end device innovation, while April 2026 updates included new final guidelines covering device categories such as capsule endoscope systems and electrosurgical cutting endoscopes. NMPA also published its 2026 Medical Device Guidelines Revisions Plan (April 27, 2026), covering 56 Class III and 219 Class II devices, and it progressed manufacturing compliance tightening with updated Medical Device GMP requirements scheduled to take effect on November 1, 2026.

Competitive Landscape

Legacy multinational brands—Olympus, Medtronic, and Cook Medical—historically held the majority of unit shipments, but domestic contenders increased their collective stake. Mindray has leveraged its critical-care footprint to cross-sell visualization towers, while Aohua Endoscopy scales value-priced 4K systems. Scivita Medical’s distribution alliance with Medtronic expands reach into tertiary networks, and EndoFresh won FDA clearance for its fully disposable GI system, validating export potential.

Investment in integrated platforms that merge AI, 3D vision, and fluorescence is intensifying. Bosom Medical’s X1 all-in-one 3D 4K stack gained approval in early 2024, signaling the speed at which local suppliers can match or exceed global benchmarks. Funding flows remain strong, with robotics specialists like Wiseking Surgical securing NMPA green lights for four-arm laparoscopic systems in 2025, opening adjacency channels to flexible endoscopy.

Price competition is sharper in lower-tier cities, where procurement committees weigh domestic alternatives against imported scopes that earlier enjoyed near-monopoly status. After-sales service and rapid software-update cycles have become decisive differentiators. Collectively, these shifts are recalibrating value pools throughout the China endoscopy devices market.

China Endoscopy Devices Industry Leaders

Cook Medical

Olympus Corporation

Medtronic Plc

Boston Scientific Corporation

Johnson & Johnson (Ethicon & Auris)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization is emerging as a key focus for both multinational and domestic suppliers, as procurement and registration dynamics increasingly reward China-made platforms. Olympus advanced domestic registration of locally manufactured endoscopy and surgical visualization components from its Suzhou base (including EVIS X1 processing and VISERA ELITE III components in 2025), reflecting how regulatory readiness and local manufacturing are used to maintain access to premium hospital accounts and public procurement channels. The State Council directive issued in September 2025, effective from January 2026, requiring government procurement to meet domestic product standards further reinforces demand for locally manufactured endoscopy towers, cameras, light sources, insufflators, and compatible scope fleets.

A second opportunity cluster is compliance-driven platform upgrades tied to new technical and manufacturing benchmarks being introduced by NMPA in 2026. The April 2026 Medical Device Guidelines Revisions Plan and June 2026 draft registration guidance for endoscopic imaging devices (including explicit image-quality and latency requirements) create a clearer bar for differentiation in 4K/3D/AI visualization, and they also raise the importance of software-defined performance validation. At the same time, tightening GMP inspection expectations and risk-based manufacturing controls increase the value of quality-system maturity, local test capability, and lifecycle documentation, favoring suppliers that can link hardware with validated algorithms and audit-ready manufacturing and post-market processes across Class III hospitals and expanding ambulatory settings.

Recent Industry Developments

- April 2026: NMPA published its Medical Device Guidelines Revisions Plan (April 27, 2026), spanning 56 Class III and 219 Class II devices. The update signals tighter lifecycle regulation and progresses manufacturing compliance with new GMP requirements scheduled to take effect November 1, 2026. Endoscopy-related dossiers and renewals are among the affected areas, reinforcing regulatory readiness for advanced imaging and minimally invasive platforms.

- November 2025: Olympus Suzhou Medical Device Co. received NMPA registration for the CV-1500-C video processor of the EVIS X1 endoscopy system. The approval expands local manufacturing into regulated market access for flagship imaging platforms, supporting participation in domestically oriented procurement and shortening lead times for premium installations.

- May 2024: Hisense Medical secured clearance for a 4K fluorescence endoscope that combines ultra-high-definition imaging with fluorescence visualization for tumor-margin support. The clearance broadened locally available advanced imaging options, increasing competitive pressure on imported visualization stacks in high-acuity endoscopy suites.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated in China from endoscopy devices used for diagnostic and therapeutic procedures, including endoscopes, visualization systems, and operative tools that enable endoscopic interventions across major hospital and clinic settings.

Scope exclusions: We exclude unrelated surgical tools that are not used for endoscopic visualization or endoscopic access, and general hospital capital items that are not dedicated to endoscopy.

Segmentation Overview

- By Device Type

- Endoscopes

- Flexible Endoscope

- Rigid Endoscope

- Capsule Endoscope

- Robot-Assisted Endoscope

- Single-Use/Disposable Endoscope

- Endoscopic Operative Devices

- Energy & Hemostasis Systems

- Access & Closure Devices

- Insufflation Systems

- Visualization Equipment

- Endoscopic Cameras

- HD Systems

- 4K / 3D / AI-Enabled Systems

- Accessories & Reprocessing Devices

- Endoscopes

- By Application

- Gastroenterology

- Pulmonology

- Orthopedic Surgery

- Cardiology

- ENT Surgery

- Gynecology

- Neurology

- Pediatric Endoscopy

- By End User

- Class III Hospitals

- Class II & I Hospitals

- Ambulatory Surgery Centers (ASCs)

- Specialty Clinics

- By Hygiene

- Reusable Endoscopes

- Single-Use Endoscopes

- Reprocessing & Sterilization Systems

- By Technology

- HD Imaging

- 4K / 3D Imaging

- AI-Assisted Imaging (NBI, TXI, CADx)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping how endoscopy care is delivered in China and where devices are actually used, so later assumptions can be tied to procedure flow and hospital purchasing behavior. We rely on public sources such as National Health Commission statistical releases, National Medical Products Administration guidance and registries, World Health Organization health indicators, and peer-reviewed clinical journals that discuss endoscopy adoption and outcomes.

To convert these signals into sizing inputs, we also review China customs trade statistics, hospital and provincial procurement notices, and manufacturer public materials like annual reports and investor presentations, which help clarify product mix and pricing direction. In parallel, we use paid subscriptions for company financials and patent analytics, and where needed shipment-level import and export data is checked to validate equipment inflow patterns. The above sources are not exhaustive, and many other public documents and datasets were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were completed with hospital procurement staff, endoscopy department users, distributors, and service partners across China to pressure-test what desk sources cannot show clearly, especially replacement cycles and price movement by device class. Inputs were checked across coastal and inland demand centers, so assumptions about utilization, tenders, and private versus public purchasing could be adjusted before the final model was locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | |

| Mid tier: 47% | Functional/Unit leaders: 29% | |

| Smaller Players: 21% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool where procedure volumes and installed base signals are used to reconstruct how much equipment, accessories, and supporting systems are consumed each year. We then translate that consumption into value using observed price bands. The result is checked using selective bottom-up approximations, including supplier and distributor roll-ups, sampled average selling price by device class, and tender-based channel checks, which helps us adjust when public reporting is thin.

Key inputs used in the China model include endoscopy procedure growth by specialty, hospital tier expansion and new department builds, the share shift toward high-definition systems, tender cycles and replacement timing for towers and scopes, and the reusable versus single-use mix that changes accessory consumption. For forecasting, scenario analysis is applied around procedure growth and pricing direction, then refined with expert consensus on how procurement policy and technology upgrades are likely to play out over the next five years. When any bottom-up check has missing players or incomplete coverage, the gap is handled with conservative uplift factors tied back to demand pool signals, rather than assuming full market visibility.

Data Validation & Update Cycle

Outputs are triangulated against independent signals, including trade flow direction, tender activity, and hospital installation momentum, and any variance is reviewed before sign-off. If a value looks off, we revisit the underlying driver, re-check conversion steps, and re-contact relevant respondents when the change is large enough to impact the market total.

Reports are refreshed annually, with interim updates when material events occur, such as major procurement policy shifts or sudden procedure volume disruptions. Before delivery, a final analyst pass is completed so the market size and assumptions reflect the latest available public data and interview feedback.

Mordor Intelligence's China Endoscopy Devices Market Sizing Compared With Other Published Estimates

It is common to see different market values for China endoscopy devices, even when the topic name looks the same, because the counted products and the pricing logic can vary across publishers. Differences also come from whether procedure-driven demand is used, or whether the model leans more on broad equipment spending totals that can obscure what is truly endoscopy-specific.

The biggest gap drivers here are scope and what gets counted as endoscopy value, such as whether after-sales service, software, and visualization stacks are included along with scopes and operative tools, and whether single-use items are treated as accessories or separated out. Some estimates also mix China-only demand with regional manufacturing shipments, or they apply a faster price growth curve without validating it against tender outcomes and replacement timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.58 B (2025) | |

| Industry Blog A | USD 3.10 B (2025) | This estimate appears to embed a faster upgrade cycle and a broader equipment and parts view, which can pull in service and replacement components more aggressively than a procedure-linked demand model. |

| Market Aggregator B | USD 2.40 B (2024) | This figure is anchored to an earlier year and may understate the 2025 step-up from post-pandemic elective procedure normalization and tender timing, especially if pricing is held flatter across device classes. |

The table shows the spread is mainly explained by how wide the product basket is and how quickly prices and upgrades are assumed to rise. When endoscopes, operative devices, and visualization stacks are tied back to procedure growth and validated with tender-cycle checks, the total tends to sit between aggressive upgrade-led views and older-year snapshots, which is the approach applied by Mordor Intelligence near the end of the modeling workflow.

Key Questions Answered in the Report

What is the projected value of the China endoscopy devices market by 2031?

Sales are expected to reach USD 3.92 billion by 2031, supported by a 7.21% CAGR.

Which segment is growing fastest within the China endoscopy devices market?

Robot-assisted platforms top the growth rankings with a 14.10% CAGR through 2031.

Why are single-use endoscopes gaining popularity?

Zero-contamination assurance, lower repair costs, and simplified logistics drive a 13.90% CAGR for disposable models.

How are government policies influencing local manufacturers?

The “Made in China 2025” quota targets 70% domestic sourcing, while streamlined NMPA approvals speed market entry for innovative devices.

Which regions account for the bulk of procedure volumes?

Eastern coastal provinces—Shanghai, Beijing, Guangdong, and neighboring areas—represent about 59.40% of market value due to dense tertiary-hospital networks.

Page last updated on: