Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

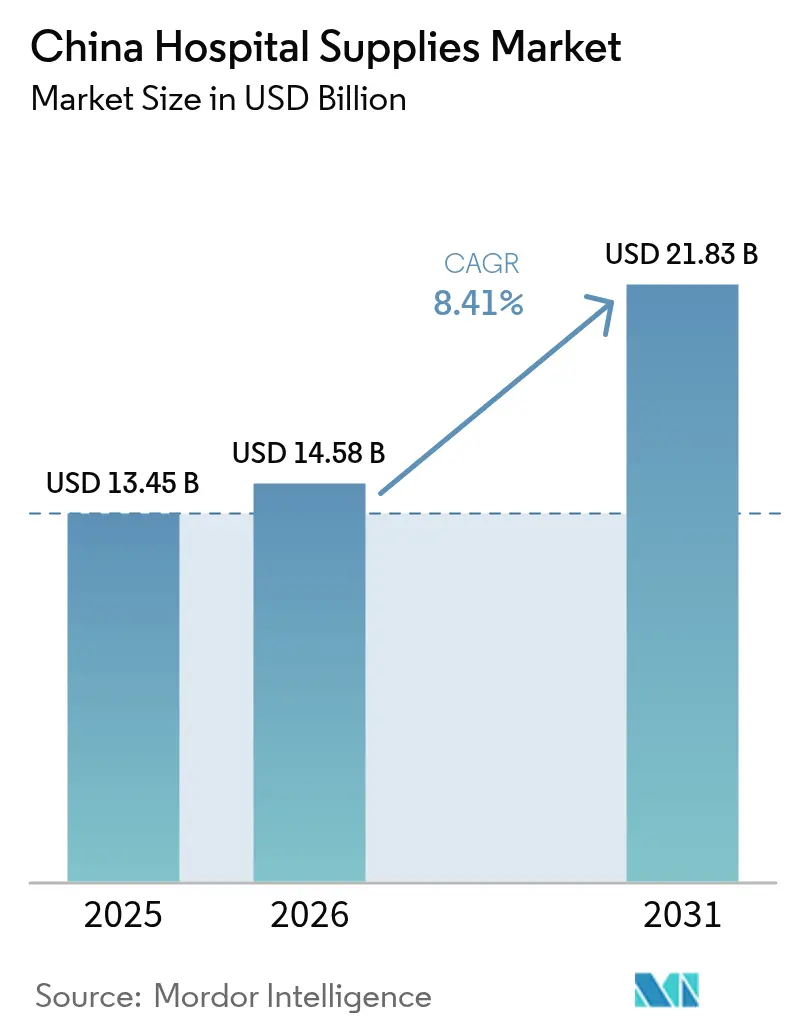

| Base Year Market Size (2025) | USD 13.45 Billion |

| Market Size (2026) | USD 14.58 Billion |

| Market Size (2031) | USD 21.83 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

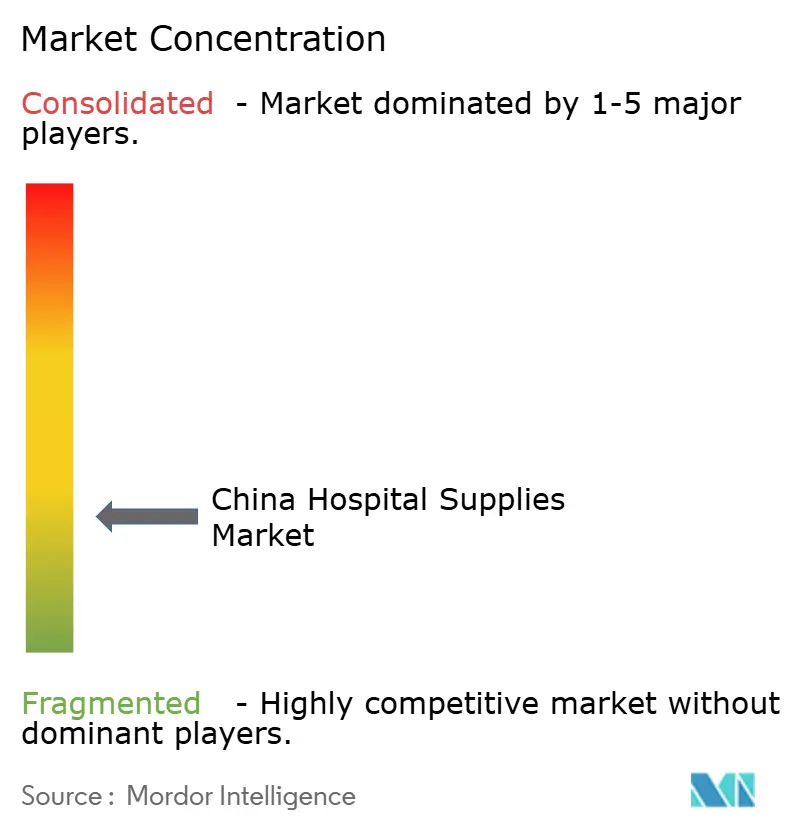

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Hospital Supplies Market Analysis by Mordor Intelligence

The China Hospital Supplies Market size was valued at USD 13.45 billion in 2025 and estimated to grow from USD 14.58 billion in 2026 to reach USD 21.83 billion by 2031, at a CAGR of 8.41% during the forecast period (2026-2031).

Expansion of hospital infrastructure, intensified infection-control protocols, and localization policies that prioritize domestic manufacturers are collectively shaping demand patterns. Disposable supplies continue to dominate procurement lists because single-use items minimize infection risk and streamline workflows, while sterilization solutions draw heightened interest as hospitals tackle hospital-acquired infection rates. Centralized purchasing mechanisms have increased volume predictability but have also intensified price competition, prompting suppliers to balance cost efficiencies with quality assurances. These factors are converging to redistribute competitive advantage toward local firms that can meet tender price caps without sacrificing regulatory compliance.

Key Report Takeaways

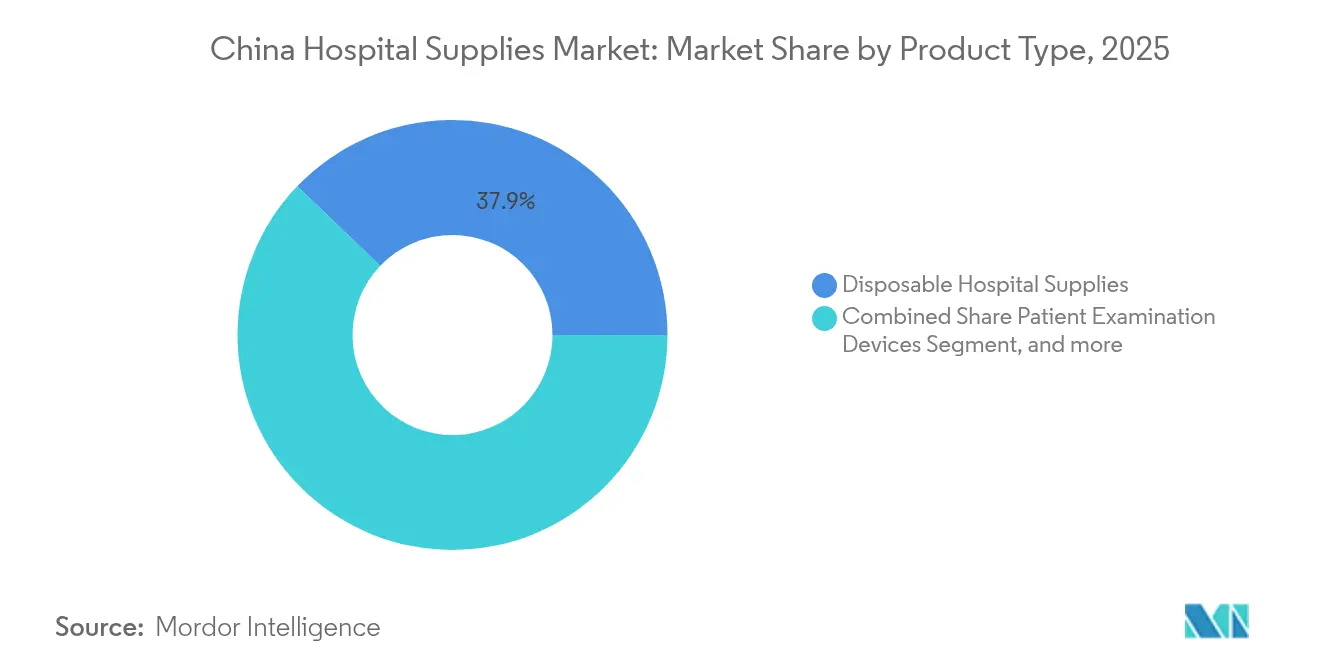

- By product type, disposable hospital supplies accounted for 37.85% of China hospital supplies market share in 2025, whereas sterilization & disinfection equipment is projected to register the fastest 9.16% CAGR through 2031.

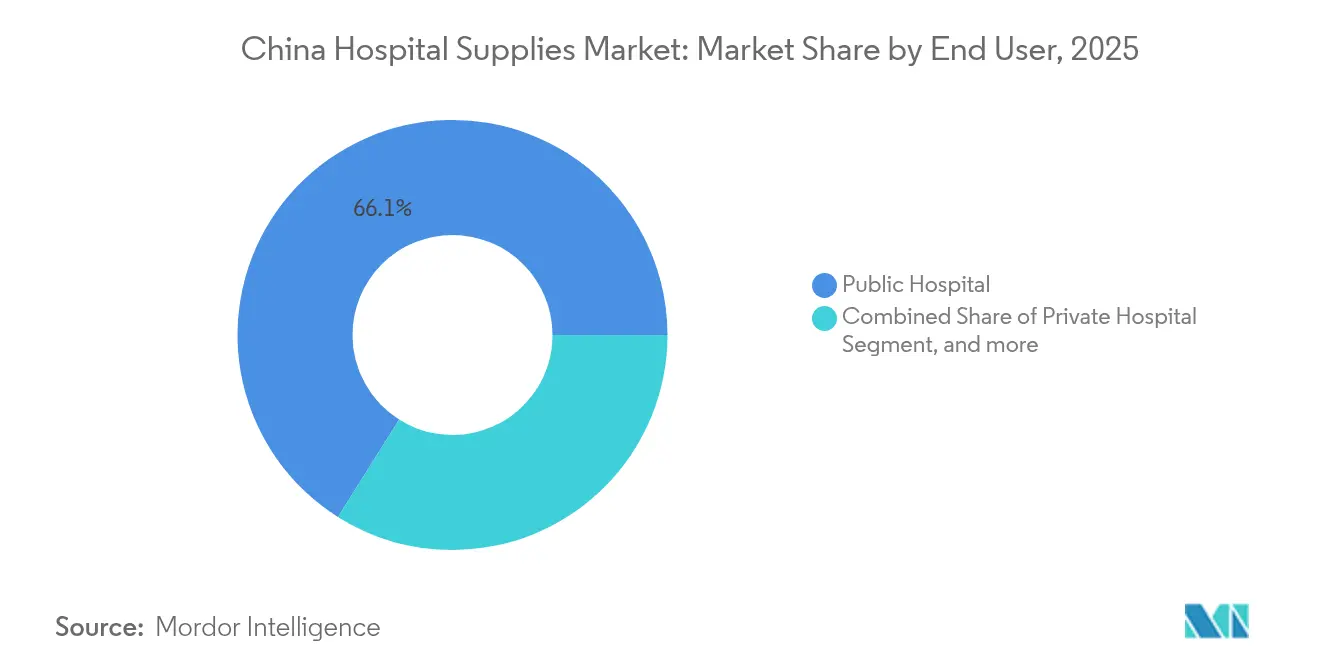

- By end user, public hospitals held 66.05% share of the China hospital supplies market size in 2025, while the private hospital segment is expected to post the highest 10.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of National Healthcare Infrastructure & Capacity Upgrades | +2.3% | Nationwide; strongest in tier-2 & tier-3 cities | Medium term (2-4 years) |

| Rising Burden of Chronic Diseases and Aging Population Boosting Procedure Volumes | +3.1% | Coastal provinces & urban centers | Long term (≥4 years) |

| Government Spending Growth through “Healthy China 2030” Initiatives | +2.5% | National; early momentum in urban hubs | Medium term (2-4 years) |

| Infection Control Awareness Post-COVID | +1.2% | Nationwide | Short term (≤2 years) |

| Growth in Public Hospital Procurement | +1.6% | Nationwide; public-hospital network | Medium term (2-4 years) |

| Digital Healthcare & Smart Hospital Adoption | +1.4% | Urban tertiary facilities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of National Healthcare Infrastructure & Capacity Upgrades

China reported 39,000 hospitals and 10.37 million hospital beds in 2024, indicating the broadest capacity expansion in the country’s history.[1]National Bureau of Statistics, “China Statistical Yearbook 2024,” stats.gov.cn New and renovated facilities in tier-2 and tier-3 cities require comprehensive clinical inventories ranging from basic disposables to advanced diagnostic systems. Government grants tied to regional medical-center programs compel hospital administrators to acquire standardized, high-quality supplies that align with national tender lists. Bed growth also stimulates stable procurement for patient-care items such as infusion sets, wound dressings, and catheters. Local manufacturers that can guarantee rapid fulfillment and competitive pricing are well positioned to capture incremental orders as construction projects reach completion.

Rising Burden of Chronic Diseases and Aging Population Boosting Procedure Volumes

Older adults already account for 66.3% of chronic-disease cases, and 33.7% experience multimorbidity, placing sustained pressure on acute-care wards.[2]Frontiers in Public Health Editorial Board, “Health Care for Older Adults in China,” frontiersin.org Procedure volumes for cardiology, oncology, and dialysis services are rising, creating downstream demand for consumables ranging from surgical drapes to implantable devices. Hospitals must also stock higher quantities of monitoring equipment to manage chronic comorbidities during inpatient stays. The financial stress associated with average out-of-pocket hospitalization costs of USD 1,199.24 has led purchasing managers to favor cost-efficient, domestically produced items over imported equivalents.

Government Spending Growth through “Healthy China 2030” Initiatives

The government’s goal to raise overall health-insurance coverage above 95% by 2025 and to shift 70% of inpatient payments to DRG models has directly increased hospital usage of standardized consumables. Centralized procurement mandates covering 80% of consumable medical devices guarantee large order volumes but enforce strict ceiling prices. Suppliers able to meet these price points without quality compromise see predictable revenue streams and lower marketing costs. In tandem, planned healthcare expenditures approaching USD 2.5 trillion by 2035 reinforce long-term consumption of sterilization equipment, personal protective supplies, and advanced monitoring systems.[3]Bayer, “Healthy China 2030: Health‐care spending trajectory,” bayer.com

Infection Control Awareness Post-COVID

Hospital-acquired infections still affect 3.64% of inpatients in specialized rehabilitation settings, sustaining a strong focus on infection-prevention protocols. Budget allocations for antimicrobial dressings, single-use surgical kits, and high-level disinfectants have been prioritized in annual tenders. Demand is also shifting toward products featuring antimicrobial coatings and automated UV-C disinfection systems. Provincial health bureaus leverage post-pandemic funding programs to install centralized sterilization departments in secondary hospitals, accelerating purchases of low-temperature plasma sterilizers and rapid biological indicators. Although total spending remains subject to tender caps, infection-control products are less price-sensitive because of their direct link to patient safety metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Tightening & Lengthy NMPA Approvals Slowing New-Product Launches | -1.8% | Nationwide; greatest on imported products | Short term (≤2 years) |

| Emergence of Home Care Services | -0.9% | Tier-1 cities | Long term (≥4 years) |

| Counterfeit Products & Quality Variability | -0.7% | Select low-tier markets | Short term (≤2 years) |

| Urban-Rural Healthcare Disparities | -1.1% | Central & western provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tightening & Lengthy NMPA Approvals Slowing New-Product Launches

The draft Medical Device Administration Law expands post-market surveillance and increases penalties for non-compliance. While domestic innovators benefit from fast-track pathways, multinational firms face longer review cycles and additional documental requirements, delaying commercial timelines. Hospitals therefore postpone the adoption of new imported devices, sustaining reliance on existing SKUs. The new legal framework also obliges manufacturers to increase investment in real-world evidence to support renewal applications, boosting compliance costs. Despite the constraints, companies that complete localized clinical evaluations may eventually secure preferential slots in provincial value-based purchasing initiatives.

Emergence of Home Care Services

In China, 90% of older adults prefer to remain at home, leading municipalities such as Shanghai to expand hospital-at-home programs. Home-based care shifts purchasing priorities toward portable monitors, compact infusion pumps, and prefilled syringes. Supply chains must accommodate smaller batch sizes and direct-to-patient logistics, challenging traditional hospital-centric distribution channels. Public reimbursement policies still favor institutional care, so growth remains gradual; however, Tier-1 cities are piloting bundled payments that include home-based follow-ups, potentially diverting certain volumes away from hospitals in the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables underpin volume leadership, sterilization accelerates

Disposable hospital supplies claimed 37.85% of China hospital supplies market share in 2025 and continue to experience steady volume growth because single-use items reduce cross-contamination risk and simplify waste-management protocols. The China hospital supplies market size for disposable syringes, gloves, and surgical drapes is projected to expand in tandem with rising procedure counts among elderly and chronic-disease cohorts. Imported brands still dominate premium catheter categories, but local firms increasingly supply commoditized disposables at price points that meet provincial tender caps. Technological upgrades such as RFID-tagged surgical packs support more precise traceability, aligning with new regulatory reporting obligations.

Sterilization & disinfection equipment is poised to register the fastest 9.16% CAGR over 2026-2031, driven by hospital-acquired infection targets and upgrades to central sterile services departments. Urban hospitals are replacing aging ethylene-oxide systems with low-temperature hydrogen-peroxide plasma units that reduce cycle times and improve occupational safety. The China hospital supplies market size for automated washer-disinfectors is expanding as tertiary hospitals move toward full ISO 13485 compliance. Domestic manufacturers have moved up the value chain with competitively priced, locally serviced sterilizers that incorporate IoT dashboards, thereby eroding the historic premium enjoyed by multinational suppliers.

By End User: Public hospitals dominate volumes, private operators outpace growth

Public hospitals accounted for 66.05% of China hospital supplies market share in 2025, reflecting their structural role in handling complex care episodes and emergencies. High bed occupancy ensures stable recurrent demand for consumables, high-usage disposables, and multichannel sterilization solutions. Centralized procurement at provincial levels aggregates this demand, compelling public institutions to accept lowest-bid pricing while maintaining NMPA quality thresholds. The China hospital supplies market size attributed to public facilities is further underwritten by multi-year capital-expenditure programs emphasizing digitalized operating rooms and high-throughput diagnostic labs.

Private hospitals, while smaller in absolute volume, are projected to realize a 10.12% CAGR to 2031, making them the fastest growing end-user group. Investors recognize opportunities to serve affluent urban populations seeking shorter waiting times and differentiated service offerings. These institutions often select higher-margin consumables and branded implants to support premium care models. The coupling coordination index between public and private hospitals improved to “partially co-developed”, enabling broader supplier engagement across both sectors. Specialty and rehabilitation centers form a nascent sub-segment, using targeted consumables such as pressure-relieving mattresses and neuro-rehabilitation electrodes to support their focused treatment pathways.

Geography Analysis

Eastern coastal provinces represent the largest purchasing centers, led by Jiangsu, Zhejiang, and Guangdong, where tertiary hospitals drive bulk orders for sophisticated surgical and diagnostic supplies. These regions often pilot national tender platforms, enabling faster adoption of value-based procurement strategies that favor competitive domestic bidders. The China hospital supplies market size in coastal cities benefits from mature logistics networks that shorten lead-times and lower inventory-holding costs.

Central and western provinces, including Sichuan and Shaanxi, are recording double-digit percentage growth as fiscal transfers under Healthy China 2030 reduce historical disparities in health-service access. Government-funded hospital expansions elevate demand for mid-range monitors, modular operating theaters, and multi-parameter patient consumables. Suppliers willing to offer tiered pricing structures and comprehensive training packages gain traction, given the relative scarcity of specialized staff in these areas.

Northern municipalities such as Beijing and Tianjin concentrate on high-technology upgrades, including AI-assisted imaging and robotic surgical systems. Although their contribution to national volume is smaller, these cities set benchmarks for advanced regulatory compliance, encouraging suppliers to position premium innovations for subsequent roll-out across provincial markets. The combined geographic dynamics illustrate how the China hospital supplies market continues to diversify, requiring nuanced go-to-market strategies that match local reimbursement levels and clinical workflows.

Regulatory Landscape

China hospital supplies are regulated primarily under the National Medical Products Administration (NMPA) framework for medical devices, covering registration, manufacturing quality, and post-market surveillance. A near-term compliance anchor is the revised Good Manufacturing Practice (GMP) for medical devices issued by the NMPA in November 2025, which takes effect on November 1, 2026. This raises expectations for manufacturers and contract producers that supply hospital tenders.

Recent regulatory activity also points to tighter standards and whole life-cycle supervision. In October 2025, NMPA Measures No. 63 advanced whole life-cycle regulation for high-end medical devices, and in March 2026 the NMPA issued 26 new and revised industry standards, including YY/T 0297-2026 on general requirements for quality of medical device clinical trials. These changes increase the importance of documentation, traceability, and clinical evidence generation for suppliers competing in centralized procurement and public-hospital demand cycles.

Competitive Landscape

Competitive intensity has risen as domestic manufacturers leverage state subsidies and public-tender preferences to penetrate mid- and high-technology segments. Mindray’s Intelli-Digital portfolio demonstrates the shift from commodity production toward interconnected, data-rich ecosystems, although the company noted slower revenue in Q3 2024 due to postponed hospital construction schedules. Jiangsu Yuyue has expanded R&D investment to accelerate smart oxygen-therapy devices, aligning with government calls for import substitution in critical-care consumables.

Multinational corporations remain influential in premium implants and sophisticated imaging consumables, but they are increasingly localizing production. Philips set up an additional sterilizer assembly line in Suzhou to satisfy volume-based purchasing thresholds, while Medtronic opened a Shanghai innovation center that co-develops minimally invasive surgical kits with local clinical partners. These localization strategies mitigate tender risks and reduce lead-times, helping foreign suppliers to retain share in the China hospital supplies market despite policy headwinds.

Mergers and strategic alliances are becoming a preferred route to broaden product portfolios and improve tender competitiveness. The acquisition of Beijing Resistomed by Shenzhen Winner in August 2024 consolidated domestic expertise in wound-closure supplies, enabling Winner to bid for larger provincial contracts. Private-equity funds are also active, targeting niche manufacturers in sterilization chemistry and specialty catheters, indicating confidence in continued market expansion and consolidation opportunities.

China Hospital Supplies Industry Leaders

3M

Johnson & Johnson

Medtronic

Cardinal Health Inc.

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Centralized procurement is expanding from consumables into equipment categories, which creates a clearer whitespace for suppliers that can compete on total cost of ownership while staying compliant and maintaining service coverage. In June 2026, the National Healthcare Security Administration (NHSA) announced the 12th batch of national centralized procurement covering medical products, and in July 2026 the National Health Commission (NHC) issued guidance on standardized centralized procurement of medical equipment by public healthcare institutions. For hospital supplies vendors, this strengthens the case for tender-ready portfolios (standardized SKUs, stable capacity, documented quality systems) and supports value-added bundling around after-sales service, training, and digital traceability in price-capped bids.

Policy support for innovation and local supply resilience also creates focused opportunities in sterilization, disinfection, and higher-value procedural kits as hospitals tighten infection-control and workflow standards. In March 2026, the State Council adopted the 15th Five-Year Plan with emphasis on high-end medical device innovation and clinical application, and in April 2026 it released a policy package to improve drug and device price-formation mechanisms and strengthen market-based competition. Alongside the broader move to DRG/DIP payment models and the expansion of provincial reimbursement medical device lists, these signals favor suppliers that can substantiate clinical value, localize manufacturing or service footprints, and provide compliant, standardized offerings for large-scale public hospital procurement.

Recent Industry Developments

- July 2026: Johnson & Johnson MedTech collaborated with Anzhen Hospital in Beijing to advance cardiovascular care, strengthening hospital-level clinical engagement tied to complex procedures. The collaboration supports adoption of specialized procedural supplies and training pathways in a major public-hospital setting, reinforcing the role of partnerships alongside product supply in tender-driven environments.

- February 2025: The National Development and Reform Commission released its 2024 report emphasizing investment in public health services, including construction of regional medical centers and county-level hospitals. Ongoing capacity buildout continues to lift baseline demand for recurring hospital consumables and essential equipment as new beds and departments come online.

- August 2024: Shenzhen Winner acquired Beijing Resistomed, consolidating domestic capabilities in wound-closure supplies. The deal broadened Winner's product portfolio for provincial bidding and increased its ability to compete for larger, bundled hospital supply contracts under centralized purchasing mechanisms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers hospital-used supplies sold and used across healthcare facilities in China, including day-to-day consumables and selected hospital equipment that directly supports patient care, infection control, and routine clinical procedures.

Scope exclusions: Medicines and pharmaceutical products are excluded, even when procured and dispensed by hospitals.

Segmentation Overview

- By Product Type

- Patient Examination Devices

- Operating Room Equipment

- Mobility Aids & Transportation Equipment

- Sterilisation & Disinfectant Equipment

- Disposable Hospital Supplies

- Other Product Types

- By End User

- Public Hospital

- Private Hospital

- Specialty & Rehabilitation Centers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and keep our assumptions consistent with what is observable in public data. We relied on official China statistics and healthcare system indicators, including National Bureau of Statistics releases, National Health Commission updates, customs trade data, and procurement and tender notices published by public agencies. Where the definition needed tightening, we also cross-checked technical and usage context using peer-reviewed clinical and infection control literature.

To connect demand signals to spending, we reviewed hospital activity indicators, reimbursement and policy notices, and publicly available standards that influence usage rates and replacement cycles, including sterilization practices and single-use rules. Company filings, investor presentations, and reputable press were used to validate category direction and pricing narratives. We also used a paid subscription for company financials and news selectively to confirm revenue splits and major product line exposure. These desk sources are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what hospitals actually buy in China, how frequently items are used, and where pricing moves first when procurement rules or policy guidance change. We spoke with a mix of manufacturers, distributors, group purchasing and tender-facing roles, and hospital procurement and department managers. The respondent input then helped close gaps left by public statistics and supported assumption checks across China.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 52% | Functional/Unit leaders: 32% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the hospital demand pool using healthcare activity and procurement-linked signals in China, then maps these to the relevant supply categories. Inputs used to shape the totals include hospital admissions and inpatient bed utilization, surgical procedure volumes, infection prevention and sterilization intensity, tender and procurement patterns, and category-level price direction drawn from public references and interview feedback.

After that, the totals are stress-tested with selective bottom-up approximations, including sampled category volumes multiplied by typical average selling prices, along with supplier and channel checks for a few high-spend baskets. When direct volume is hard to observe, we use proxy drivers, such as procedures per bed and single-use rates, and then normalize the implied spend so it aligns with what procurement teams report for mix and price bands.

For forecasting, scenario analysis is used so the model can reflect policy and tender shifts, hospital expansion pace, and mix changes between reusable and disposable items. The final forecast path is adjusted only after primary feedback confirms which demand drivers are most stable versus which are policy-sensitive.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including hospital activity trends, public procurement direction, and interview-based checks on utilization and pricing. Variance checks are run at the category and total levels, and unusual jumps are reviewed again to confirm whether they reflect real policy changes, price movements, or a modeling issue.

Before sign-off, the work is reviewed in multiple steps, and follow-up calls are triggered when a key assumption changes or when expert feedback conflicts across the value chain. Reports are refreshed annually, with interim updates when a material market event occurs, and a final pre-delivery pass is completed so clients receive the most current view.

Mordor Intelligence's China Hospital Supplies Market Size Measured Against Other Published Estimates

Published estimates for this market often differ because the scope line is drawn differently and the demand drivers selected are not the same, which then changes both the starting value and the growth path. Differences also show up when studies mix hospital-only procurement with broader healthcare spending, or when price assumptions are applied without being checked against tender reality.

Pharmaceuticals and medicines sit outside Mordor Intelligence's scope here, which is a common reason some broader China medical supplies figures appear much larger than hospital supplies-only totals. The spread also comes from how studies treat big-ticket equipment versus routine consumables, whether public tenders are used as a reality check for pricing, and how frequently currency timing and policy impacts are refreshed in the forecast.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.58 B (2026) | |

| Industry Publisher A | USD 105.00 B (2024) | Uses a broader China medical supplies definition that also includes pharmaceuticals and a wide set of medical devices across multiple care settings, which inflates the addressable spend versus hospital supplies only. |

| Industry Research House B | USD 6.50 B (2025) | Covers a narrower basket and mixes non-hospital end uses with limited clarity on what hospital equipment is included, which can understate hospital procurement that sits in routine wards and operating rooms. |

Taken together, the comparison shows that the biggest gaps come from what is included in the product basket and whether the numbers are tied back to hospital activity and procurement signals. By keeping the inputs traceable to observable hospital demand drivers and then checking the totals through interviews and pricing reality checks, the estimate stays practical to replicate and easier to interpret for planning.

Key Questions Answered in the Report

What is the current size of the China hospital supplies market?

The market is valued at USD 14.58 billion in 2026 and is forecast to reach USD 21.83 billion by 2031 at a 8.41% CAGR.

Which product segment leads the China hospital supplies market?

Disposable hospital supplies lead with 37.85% share in 2025, reflecting strong infection-control priorities.

Which end-user category is expanding the fastest?

Private hospitals are projected to post a 10.12% CAGR between 2026 and 2031, the fastest among all end users.

How are regulatory changes affecting new product launches?

Draft reforms increase documentation and penalties, slowing approvals for imported devices while accelerating domestic innovation.

What geographic regions are driving future growth?

Rapid hospital construction and investment in central and western provinces are pushing double-digit growth in those regions.

How significant is infection-control spending post-COVID?

Hospital-acquired infections remain a priority, with sterilization and disinfection equipment forecast to grow at 9.16% CAGR through 2031.

Page last updated on: