China Biocontrol Agents Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

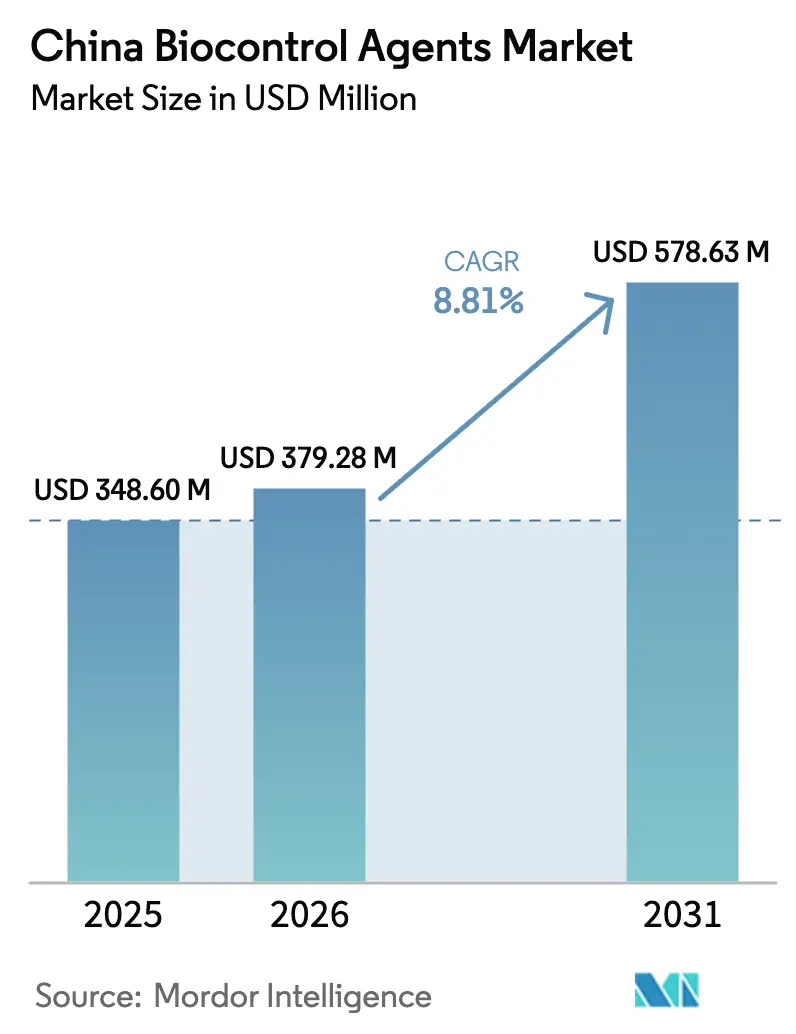

| Base Year Market Size (2025) | USD 348.6 Million |

| Market Size (2026) | USD 379.28 Million |

| Market Size (2031) | USD 578.63 Million |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

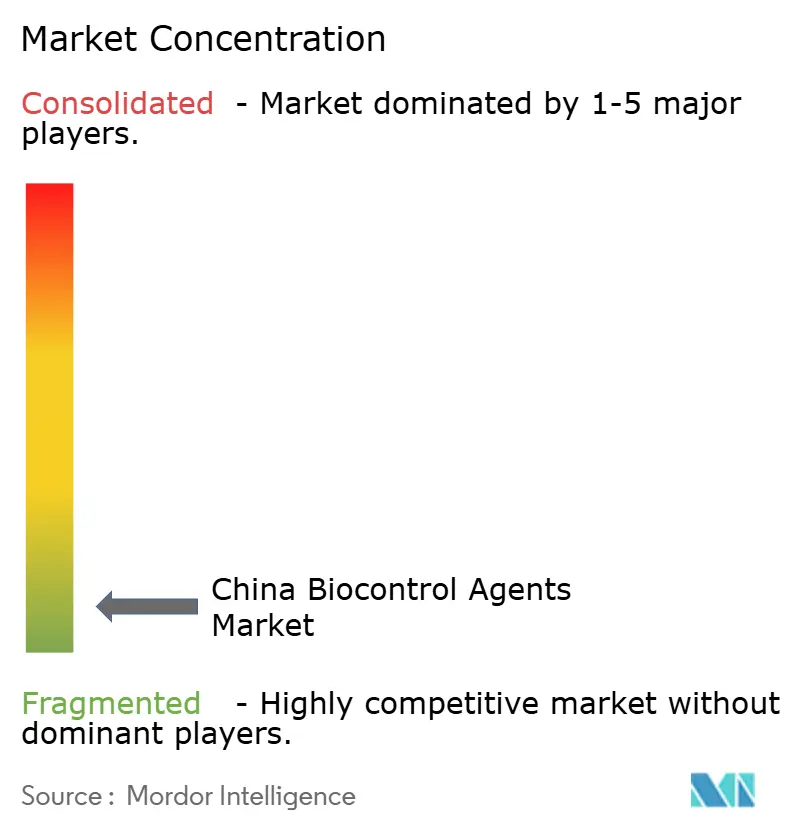

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Biocontrol Agents Market Analysis by Mordor Intelligence

The China biocontrol agents market size is expected to grow from USD 348.6 million in 2025 to USD 379.28 million in 2026 and is forecast to reach USD 578.63 million by 2031 at 8.81% CAGR over 2026-2031. Strong government enforcement of the “zero-growth” pesticide policy, rapid expansion of certified organic acreage, and tighter export residue rules are the principal engines propelling this pace. Producers of macrobials largely dominate due to streamlined registration pathways, while drone-enabled application services are expanding access to smallholders. Investment in cold-chain networks and RNA-based technologies signals a structural shift toward higher-margin biological inputs, and rising pest resistance to chemical actives further solidifies the trend. Intensifying provincial pilot projects, along with mounting consumer demand for residue-free produce, keeps the adoption momentum steady, especially in the more technologically advanced coastal provinces.

Key Report Takeaways

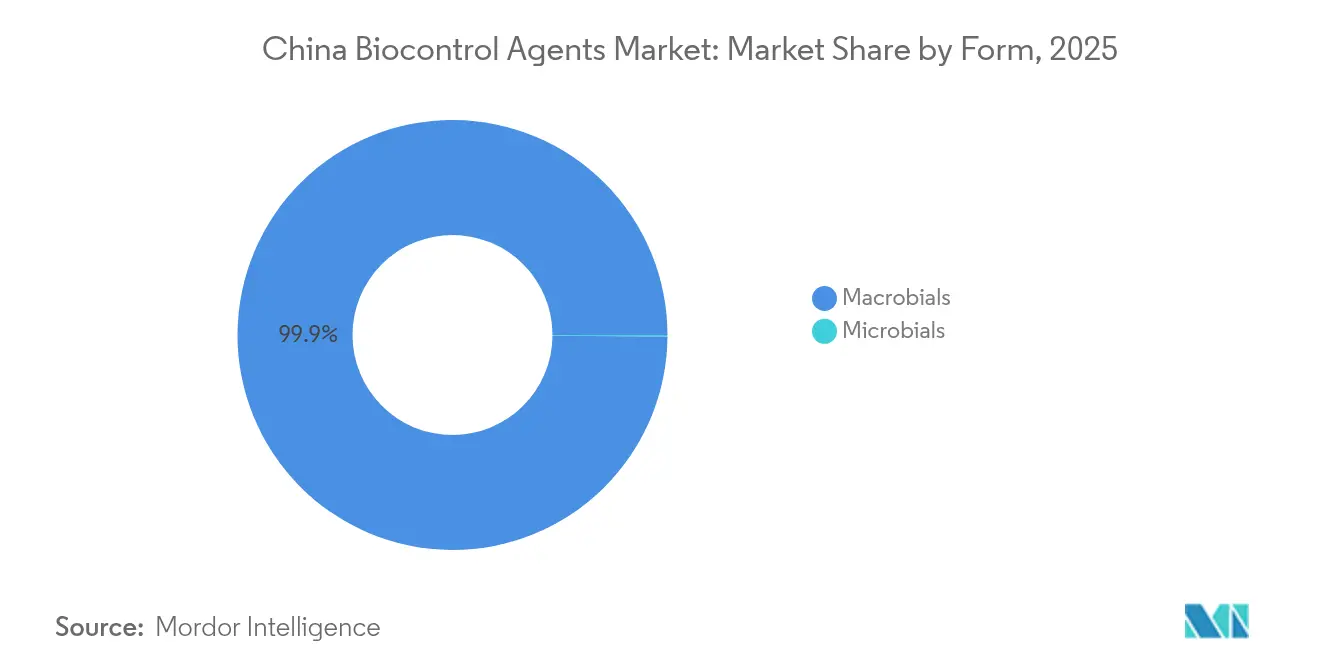

- By form, macrobials held 99.88% of the China biocontrol agents market share in 2025, and are forecast to expand at an 8.86% CAGR through 2031.

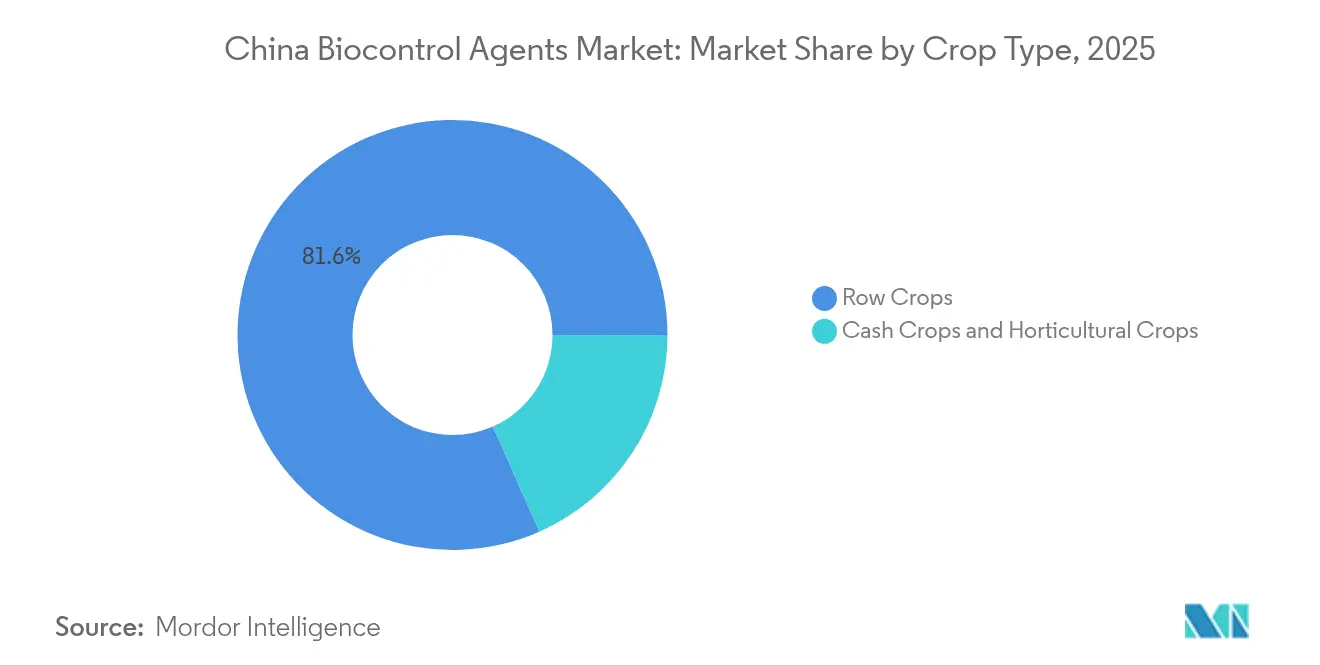

- By crop type, row crops accounted for 81.62% share of the China biocontrol agents market size in 2025, while cash crops are anticipated to advance at a 9.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Biocontrol Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government “zero-growth” pesticide policy pushes green inputs | +2.1% | National; strongest in Shandong, Hebei, Yunnan | Medium term (2-4 years) |

| Organic acreage expansion in key provinces | +1.8% | Shandong, Hebei, Yunnan | Long term (≥ 4 years) |

| European Union MRL stringency for export crops | +1.4% | Export-oriented coastal regions | Short term (≤ 2 years) |

| Chemical-resistant pest outbreaks accelerate adoption | +1.2% | National; acute in rice and corn zones | Short term (≤ 2 years) |

| Provincial RNA-biopesticide pilot programs | +0.9% | Zhejiang, Shanghai | Long term (≥ 4 years) |

| Drone-as-a-Service bundles with biocontrol apps | +0.7% | Developed agricultural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government “zero-growth” pesticide policy pushes green inputs

Since 2020, the Ministry of Agriculture and Rural Affairs has capped national chemical pesticide consumption. Enforcement is tied to provincial performance metrics, prompting growers to seek non-chemical options. This framework removes the price-performance comparison with unrestricted synthetics, carving out a protected space for biological solutions. Streamlined approval procedures under the 2024 Biosafety Law amendments further accelerate the roll-out of domestic microbial products.[2]Source: Ministry of Commerce of the People's Republic of China, “Biosecurity Law of the People's Republic of China (2024 Amendment),” policy.mofcom.gov.cn

Organic acreage expansion in key provinces

China's organic farmland area was approximately 2.9 million hectares in 2023, ranking it as the country with the fourth-largest certified organic agricultural land area globally according to the 2024 FiBL (Research Institute of Organic Agriculture) report [1]Source: Research Institute of Organic Agriculture, “The World of Organic Agriculture, STATISTICS & EMERGING TRENDS 2025,” fibl.org. Organic standards prohibit synthetic chemistries, forcing growers to rely exclusively on biological inputs. With subsidies covering up to 40% of certification costs, the economics of adoption improve, attracting premium-priced international formulations and stimulating local research and development. Rising urban incomes and expanding e-commerce channels sustain double-digit growth in domestic organic food sales.

European Union MRL stringency for export crops

Brussels reduced allowable residues for several actives by 50-90%, making compliance with conventional pesticides alone impossible. Exporters of tea, vegetables, and fruit in China have adopted biocontrol programs to preserve access to the European market. In 2024, 15% of Chinese agricultural shipments rejected at EU borders were cited for residue violations, prompting upstream contractual obligations that mandate registered biocontrol protocols, aiding the growth of the biocontrol agents market.

Chemical-resistant pest outbreaks accelerate adoption

China has traditionally been one of the largest global producers and consumers of chemical pesticides, often utilizing them at high frequencies and doses. Chemical-resistant pest outbreaks have become a significant factor driving market growth and the increasing adoption of biocontrol agents in the country. Resistance to pyrethroids and neonicotinoids in pests such as the brown planthopper and fall armyworm exceeds 80% in key rice-growing regions. Additionally, whiteflies, which affect crops like cotton, vegetables, and ornamentals while transmitting plant viruses, exhibit high resistance to neonicotinoids and other systemic insecticides across various regions in China. Biological products, including biocontrol agents with unique modes of action, address this efficacy gap and align with integrated resistance management strategies recommended by provincial plant protection stations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher per-hectare cost and variable field efficacy | -1.8% | National, acute in price-sensitive regions | Short term (≤ 2 years) |

| Lengthy, complex registration and residue-data requirements | -1.2% | National regulatory bottleneck | Medium term (2-4 years) |

| Fragmented extension services are causing misapplication losses | -0.9% | Rural inland provinces | Medium term (2-4 years) |

| Cold-chain gaps for live macrobials in inland provinces | -0.7% | Inland agricultural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher per-hectare cost and variable field efficacy

The higher costs and inconsistent efficacy of biocontrol agents present a significant challenge for farmers, who must balance short-term economic considerations with long-term sustainability benefits. Producing living organisms, such as macrobials (e.g., predatory insects) or microbials (e.g., fungi and bacteria), is more complex and resource-intensive compared to the mass production of synthetic chemicals. Per-hectare costs for biocontrol agents are 15-30% higher than those of chemical alternatives, and their performance is highly dependent on climate conditions and the timing of application. The economic strain of higher upfront costs is particularly challenging for smallholder farmers, who constitute a large portion of China's agricultural sector and often prioritize immediate cost savings over long-term investments in sustainable pest management practices.

Lengthy, complex registration and residue-data requirements

The complexity and length of China's biocontrol agent registration process create significant delays in market entry, hindering market growth. Many test data points required for testing must be generated within China at laboratories accredited by the Ministry of Agriculture and Rural Affairs (MARA). Completing full dossiers, including toxicology, environmental fate, and efficacy studies, typically takes 36-48 months for approval. The 2024 amendments to the Biosafety Law introduced additional requirements for genetically engineered organisms, further extending the timelines. Smaller innovators often rely on partnerships with state institutes to access the necessary expertise and funding. New products must undergo multi-location field trials to establish efficacy and safety, adding substantial time and cost to the registration process, which continues to constrain market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Macrobials sustain dominance over microbials

Macrobials command 99.88% of the Chinese biocontrol agents market share in 2025. Macrobial biocontrol agents (predatory insects, mites, and parasitic wasps) have sustained dominance over microbials (bacteria, fungi, viruses) in the Chinese biocontrol market primarily due to their superior perceived efficacy, reliability, and ease of use in specific high-value crops. They are projected to post the fastest 8.86% CAGR as improvements in packaging enhance survivability. Entomopathogenic nematodes gain traction in tobacco and root vegetable systems where soil pest pressure is high. Successful cold-chain pilot runs in Jiangsu showcase distribution models that inland provinces may replicate.

Farmer willingness to pay for precision-released parasitoids grows in greenhouses where high margins justify premium inputs. Regional cooperatives invest in insectaries to localize production, cutting transport times and viability risks. Provincial subsidies covering up to 20% of macrobial purchase costs further stimulate uptake. These developments send a clear signal that live biologicals will form a meaningful slice of the China biocontrol agents market within the next decade.

By Crop Type: Cash crops set the growth tempo

Row crops safeguard food security and account for 81.62% of 2025 revenue, yet their price sensitivity hinders growth potential. The China biocontrol agents market size for row crops is projected to grow modestly through 2031. Government procurement programs for rice and wheat continue to favor low-cost inputs, though resistance crises may open space for biologicals. Cash crops such as tea, tobacco, and specialty vegetables clock the highest 9.05% CAGR, buoyed by export premiums and domestic organic demand. Farmers can pass input costs upstream, enabling faster technology turnover.

Horticultural crops, notably fruit and vegetables for urban supermarkets, bridge the two extremes. Adoption here hinges on retailer residue requirements and the value of branding. Green Food certification channels encourage repeat purchases, embedding biologicals more deeply into integrated pest management routines. Subsidy programs targeting cash and horticulture clusters package product rebates with training vouchers, smoothing the learning curve for complex application protocols.

Geography Analysis

Coastal provinces set the adoption benchmark. Shandong leverages its dense cluster of vegetable export firms and ready port access to top the provincial leaderboard in terms of revenue. Hebei follows, riding on robust organic programs and generous provincial funds that cover up to half of biocontrol costs for certified growers. Zhejiang and Shanghai, though smaller in cropped area, wield outsized influence through RNAi pilots and technology incubators that shape national standards.

Yunnan registers the highest provincial growth, anchored by premium tea and cut-flower operations that demand residue-free protection. A favorable climate and higher margins justify the early adoption of costly macrolides. Inland strongholds such as Henan and Hubei lag but show steady progress as extension pilots and cold-chain corridors come online. Western regions remain nascent; scattered demonstration plots illustrate potential, yet cost-to-serve ratios stay unfavorable without significant logistics upgrades.

Regional policy alignment with the National Development and Reform Commission’s rural revitalization agenda is becoming increasingly tight. Provinces that embed biocontrol targets into five-year plans unlock earmarked funds for research centers, demonstration farms, and public–private partnerships. Over time, such frameworks are anticipated to even out geographic disparities and expand the China biocontrol agent market's nationwide footprint.

Competitive Landscape

High Fragmentation defines the competitive map: the top five firms capture a minor share of 2024 revenue, a hallmark of early-stage industries. Koppert leads, trailing a long tail of local microbial specialists. International incumbents leverage technology leadership to secure premium segments, often via joint ventures that navigate regulatory intricacies and local sourcing preferences. Domestic firms focus on cost leadership, using fermentation scale and shorter supply chains to undercut imports.

Service orientation is growing. Technology companies bundle biocontrol products with drone spraying, field diagnostics, and data analytics, moving value capture from product sales to integrated solutions. Patent filings in formulation and delivery have surged, reflecting rising domestic R&D capacity. Consolidation looms as financing flows into acquisition war chests targeting niche innovators with compelling IP or regional distribution strength. The market trajectory suggests that the Chinese biocontrol agents industry will see an increase in strategic alliances, particularly around next-generation RNAi and AI-enabled application platforms.

Success in the Chinese biological control agents market increasingly depends on companies' ability to innovate and develop effective distribution networks. Market leaders are focusing on developing specialized products for different crop types and pest varieties, while also investing in research to improve product efficacy and shelf life. Companies are establishing strong technical support teams to provide customized solutions and building relationships with agricultural institutions and farmers to enhance product adoption.

China Biocontrol Agents Industry Leaders

Henan Jiyuan Baiyun Industry Co. Ltd

Andermatt Biocontrol AG (Andermatt Holding AG)

Biobest Group NV (Floridienne SA)

Isagro S.p.A. (Gowan Company LLC)

Koppert B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: Keyun Biocontrol's Spodoptera frugiperda multiple nucleopolyhedrovirus (SfMNPV) has been officially approved by the Institute for the Control of Agrochemicals, Ministry of Agriculture and Rural Affairs (ICAMA) in China. This approval complies with the provisions of the Administrative Approval Law and the Regulations on the Control of Agrochemicals. Following its registration, the product will be introduced to both domestic and international markets for the control of Spodoptera frugiperda (fall armyworm).

- November 2023: Keyun Biocontrol deployed Trichogramma chilonis, a parasitic wasp, via drone over 5,000 mu (equivalent to 333 hectares) of paddy fields in Xinyang, Henan Province, China. This initiative aims to control Chilo suppressalis (Rice Stem Borer).

China Biocontrol Agents Market Report Scope

Macrobials, Microbials are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type.| Macrobials | By Organism | Entamopathogenic Nematodes |

| Parasitoids | ||

| Predators | ||

| Microbials | By Organism | Bacterial Biocontrol Agents |

| Fungal Biocontrol Agents | ||

| Other Microbials |

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Macrobials | By Organism | Entamopathogenic Nematodes |

| Parasitoids | |||

| Predators | |||

| Microbials | By Organism | Bacterial Biocontrol Agents | |

| Fungal Biocontrol Agents | |||

| Other Microbials | |||

| Crop Type | Cash Crops | ||

| Horticultural Crops | |||

| Row Crops | |||

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biocontrol agents applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biocontrol agents are the natural predators and parasitoids used to control various pests. Biocontrol agents include both microbials (Microorganisms) and macrobials (Insects).

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.