Chicago Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

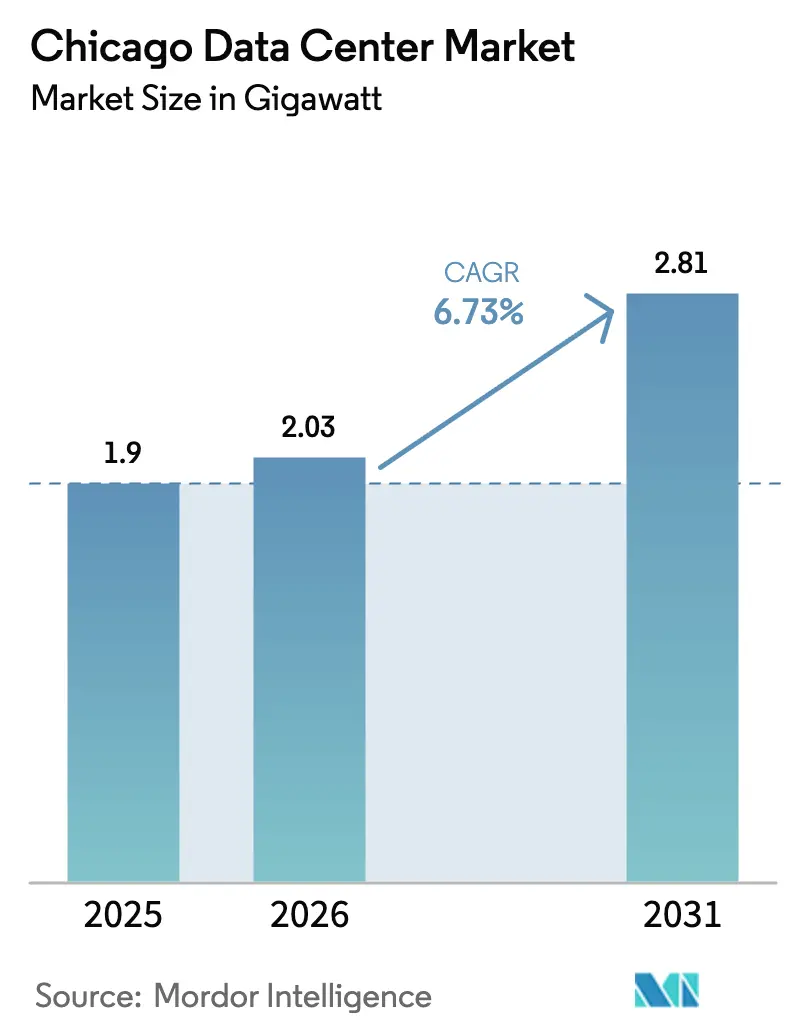

| Base Year Market Size (2025) | 1.9 gigawatt |

| Market Volume (2026) | 2.03 gigawatt |

| Market Volume (2031) | 2.81 gigawatt |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chicago Data Center Market Analysis by Mordor Intelligence

The Chicago data center market size is expected to grow from 1.9 GW in 2025 to 2.03 GW in 2026 and is forecast to reach 2.81 GW by 2031 at 6.73% CAGR over 2026-2031. Vacancy sits at a record‐low 1.9%, while average rental rates climbed 33% year-over-year, underscoring an acute supply–demand imbalance cbre.com. Illinois’ sales-tax exemption on qualified equipment and its 6.9 c/kWh industrial power tariff have drawn more than USD 11 billion in new build commitments since 2019 illinois.gov. Power planners expect data-center load on ComEd’s grid to jump from roughly 400 MW today to nearly 5 GW, equal to the output of five nuclear units. Tight power and land conditions in Northern Virginia are also steering hyperscale spill-over demand toward Chicago, lifting the city to the nation’s third-largest hub

Key Report Takeaways

- By data-center size, Massive facilities led with 44.12% of Chicago data center market share in 2025, whereas the Mega category is forecast to advance at a 7.72% CAGR through 2031.

- By tier, Tier 3 captured 58.02% of Chicago data center market share in 2025; Tier 4 is set to post the fastest CAGR at 8.21% through 2031.

- By service model, colocation accounted for 49.05% of Chicago data center market size in 2025, but cloud-service providers are projected to grow at 9.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chicago Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging cloud-service-provider demand | +1.8% | Global, focused on Chicago metro | Medium term (2-4 years) |

| Growing enterprise edge-computing needs | +1.2% | Chicago metro and suburbs | Long term (≥ 4 years) |

| Robust fiber-connectivity ecosystem | +0.9% | Chicago core, O’Hare corridor | Short term (≤ 2 years) |

| Incentive programs and Illinois tax benefits | +1.5% | Illinois statewide | Medium term (2-4 years) |

| Northern Virginia spill-over demand | +0.8% | Chicago region | Short term (≤ 2 years) |

| AI training workloads seeking Midwest power | +1.3% | Chicago and rural Illinois | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Cloud-Service-Provider Demand

Hyperscale operators are accelerating footprint expansion as premier coastal markets hit power ceilings.[1]Joel Hruska, “Hyperscalers Seek Alternatives to Ashburn,” commercialobserver.com Amazon’s USD 20 billion program for nuclear-backed campuses in the Mid-Atlantic signals a readiness to diversify locations, enabling Chicago to draw similar mega-projects. Microsoft and BlackRock’s USD 30 billion AI-infrastructure alliance has earmarked Midwest parcels, while Equinix’s USD 15 billion xScale venture identifies Chicago as an early launch point. Financial-market latency needs further amplify demand; CME Group’s private Google Cloud region in Aurora exemplifies this enterprise pull.

Growing Enterprise Edge-Computing Needs

A USD 232 billion global edge-market in 2024 is reshaping site requirements for Chicago’s manufacturers, retailers and financial firms.[2]Jonathan Vanian, “AWS Pivots to Nuclear Power for New U.S. Campuses,” cnbc.com CoreSite’s CH2 earned NVIDIA DGX-Ready status, reinforcing the metro’s suitability for AI inference clusters. Telecommunications carriers such as Comcast anchor Northlake facilities to support 5G, content-delivery networks and low-latency over-the-top workloads.

Robust Fiber-Connectivity Ecosystem

DE-CIX Chicago is the fastest-growing exchange in Illinois, interlinking with New York and Dallas to form North America’s largest peering fabric.[3]Jonathan Vanian, “AWS Pivots to Nuclear Power for New U.S. Campuses,” cnbc.com Digital Realty’s 350 E. Cermak site hosts 40+ carriers and surpasses 100 MW in load, benefiting from the metro’s dense backhaul routes. United IX offers 10 G–100 G ports and aggregates major CDN traffic, amplifying network effects that attract incremental investment.

Incentive Programs and Illinois Tax Benefits

The 2019 data-center sales-tax statute grants 10.25% exemptions on qualifying gear for projects investing ≥ USD 250 million and hiring at least 20 staff paid 120% of county averages. The policy helped double statewide private-sector capital inflows to USD 12.5 billion in 2024, with data-center projects capturing a substantial share. CyrusOne’s USD 350 million Aurora build broke ground alongside gubernatorial support, illustrating streamlined permitting gains.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising power costs (ComEd territory) | -0.7% | Chicago metro | Short term (≤ 2 years) |

| Escalating land and construction costs | -1.1% | Chicago metro and suburbs | Medium term (2-4 years) |

| Cooling constraints from Lake Michigan water rules | -0.5% | Lake Michigan watershed | Long term (≥ 4 years) |

| Lengthy grid-interconnection cycles | -0.9% | Illinois, PJM area | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Power Costs (ComEd Territory)

Projected monthly customer bills could climb USD 10.50 as data-center demand raises grid-balancing charges. PJM auction-clearing prices have risen, forcing operators to hedge higher capacity costs. Lawmakers are studying safeguards to prevent hyperscale strain on legacy infrastructure and to protect ratepayers.

Escalating Land and Construction Costs

Building out a hyperscale box now averages USD 561.33 / sq ft, an increase of 20.53% since 2019. Land near O’Hare tops USD 224,000 per acre, pushing developers toward Elk Grove, Northlake and further west cbre.com. Procuring dedicated substations and extra-high-voltage feeds adds millions to capital budgets and can extend project schedules by multiple quarters.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Mega Facilities Drive Hyperscale Expansion

Massive footprints delivered 44.12% share of Chicago data center market in 2025, reflecting a matured ecosystem supporting financial-services and legacy workloads. However, Mega campuses are set to outpace every other category at a 7.72% CAGR through 2031 as AI training clusters hunt for blocks of contiguous power above 100 MW. T5’s 480 MW suburban campus and Compass’ five-building redevelopment of the former Sears HQ evidence this pivot, each engineered for ≥ 50 kW per rack densities.

Small and medium halls remain viable for edge and enterprise hybrids but face gradual absorption into larger wholesale footprints. Hyperscale tenants favor the operating leverage and custom mechanical-electrical topologies available in Mega builds, pressuring owners of smaller suites to differentiate via latency-critical or specialty compliance offerings.

By Tier Type: Tier 4 Adoption Accelerates for Mission-Critical Applications

Tier 3 facilities held 58.02% share of Chicago data center market size in 2025 as they delivered a pragmatic uptime-cost balance sought by most enterprises. Financial and healthcare users, however, are steering fresh demand toward Tier 4 platforms that promise fault tolerance and 99.995% availability, helping the class achieve an 8.21% CAGR to 2031.

Operators are layering in concurrently maintainable electrical paths and waterless cooling to satisfy the SLA premiums commanded by regulated workloads. NTT’s CH1, Forsythe’s Elk Grove site and new speculative shells all tout Uptime Institute certifications that validate Tier 4 attributes, positioning Chicago to capture regulated-industry expansions that require deterministic availability.

By Data-Center Type: Cloud Service Providers Accelerate Market Transformation

Colocation retained 49.05% share in 2025, supported by near-zero vacancy and a 33% rent uplift, but cloud-service providers represent the fastest needle-mover, expanding at 9.07% CAGR through 2031 as hyperscalers roll out dedicated zones for AI workloads.

Wholesale shells and powered-base-build formats enjoy the tightest pricing power because they solve both capacity and speed-to-market constraints. Retail colo continues to serve SMB tenants, while modular and edge boxes target 5G, content caching and disaster-recovery niches. Equinix’s USD 2.225 billion Q1 2025 revenue and upwardly revised annual guide underline the earnings upside tied to this migration wave.

Geography Analysis

Chicago anchors the Midwest’s most mature cloud and network node, housing 154 active data centers that support 20,000 jobs and USD 3.5 billion in labor income. The Chicago data center market size leadership is reinforced by low seismic risk, abundant nuclear-derived electricity and a central location ensuring sub-20 ms round-trip latency to both coasts. Illinois hosts 126 facilities run by 68 providers and has another USD 1.7 billion in construction under way across six announced builds.

Demand displaced from Northern Virginia is landing in Chicago as Dominion Energy transmission bottlenecks defer new hook-ups until 2027. Operators pursuing concurrent capacity, therefore, favor PJM-connected Illinois, where ComEd can allocate grid import rights faster. At the same time, land and power fundamentals in suburban Columbus drive a multi-city Midwestern corridor that bolsters Chicago’s role as a core peering anchor. Within metro Chicago, Elk Grove Village, Northlake and Aurora form the most active development triangle. T5, CyrusOne and Compass collectively plan over 1 GW in these suburbs, exploiting available land parcels and 138 kV feeds. Downtown, Digital Realty’s planned 12-story tower at 330 E. Cermak shows densification via vertical builds as legacy lots reach saturation

Competitive Landscape

Digital Realty, Equinix and CoreSite maintain the largest installed bases, but aggressive greenfield programs by T5 Data Centers, Compass Datacenters and CyrusOne are diluting share, pointing to moderate concentration. Digital Realty’s 350 E. Cermak—spanning 1.1 million sq ft—hosts 70+ carriers and remains Illinois’ top-load customer at > 100 MW. Equinix is channeling USD 15 billion into U.S. xScale campuses; Chicago ranks among the first four locations, reflecting its hyperscale pull.

Hardware and power-train partnerships differentiate entrants. Siemens will supply Compass’ medium-voltage skids under a multi-year pact, shaving months off electrical deployment cycles. Meanwhile, Microsoft’s zero-water cooling pilots in neighboring Wisconsin could migrate to its Minooka, Illinois blueprint, signaling sustainability as a competitive lever.

Record MandA further shapes the field. Vantage raised USD 9.2 billion in January 2025, CBRE bought Direct Line Global for white-space services and Schneider acquired Motivair for liquid-cooling IP, stressing the strategic value of turnkey delivery and advanced thermal solutions.

Chicago Data Center Industry Leaders

Digital Realty Trust, Inc.

Equinix Inc.

CyrusOne

Quality Technology Services Holding LLC (QTS)

Stack Infrastructure, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: CyrusOne started a second Aurora campus totaling 446,000 sq ft and 40 MW initial IT load.

- February 2025: Digital Realty posted record Q4 2024 bookings and acquired land supporting up to 400 MW of expansion.

- February 2025: Equinix entered a USD 15 billion hyperscale JV with GIC and CPP to add 1.5 GW nationwide

- January 2025: Vantage Data Centers secured a USD 9.2 billion equity injection to fund a USD 30 billion global build plan

Chicago Data Center Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services and store and manage the data connected with those applications and services.

The Chicago Data Center Market is segmented by DC Size (small, medium, large, massive, mega), by tier type (tier 1&2, tier 3, tier 4), by absorption (utilized [colocation type [retail, wholesale, hyperscale], by end user [cloud & IT, telecom, media & entertainment, government, BFSI, manufacturing, e-commerce]) and non-utilized). The market sizes and forecasts are provided in terms of value (MW) for all the above segments.

| Small |

| Medium |

| Large |

| Massive |

| Mega |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | |||

| Colocation | Utilized | Colocation Type | Retail |

| Wholesale | |||

| Hyperscale | |||

| End User | Cloud and IT | ||

| Telecom | |||

| Media and Entertainment | |||

| Government | |||

| BFSI | |||

| Manufacturing | |||

| E-Commerce | |||

| Other End User | |||

| By Data Center Size | Small | |||

| Medium | ||||

| Large | ||||

| Massive | ||||

| Mega | ||||

| By Tier Type | Tier 1 and 2 | |||

| Tier 3 | ||||

| Tier 4 | ||||

| By Data Center Type | Cloud Service Providers (CSPs) | |||

| Enterprise, Modular and Edge | ||||

| Colocation | Utilized | Colocation Type | Retail | |

| Wholesale | ||||

| Hyperscale | ||||

| End User | Cloud and IT | |||

| Telecom | ||||

| Media and Entertainment | ||||

| Government | ||||

| BFSI | ||||

| Manufacturing | ||||

| E-Commerce | ||||

| Other End User | ||||

Key Questions Answered in the Report

What is the projected growth of the Chicago data center market through 2031?

The installed base is forecast to grow from 2.03 GW in 2026 to 2.81 GW by 2031, a 6.73% CAGR.

The installed base is forecast to grow from 2.03 GW in 2026 to 2.81 GW by 2031, a 6.73% CAGR.

Chicago offers available power, lower land prices and robust tax incentives at a time when Northern Virginia faces grid bottlenecks and community pushback.

How much tax relief can qualifying operators capture in Illinois?

Projects investing at least USD 250 million and hiring 20 staff can secure a 10.25% sales-and-use-tax exemption on data-center equipment.

Which data-center size segment is expanding the fastest?

Mega campuses built for AI and hyperscale workloads are projected to grow at 7.72% CAGR through 2031.

What are the main cost headwinds for new builds in Chicago?

Escalating construction materials now average USD 561.33 / sq ft, and rising grid-capacity charges are pushing ComEd customer bills up by around USD 10.50 per month.

How concentrated is market leadership today?

The top five operators hold just over 60% of installed power, giving the market a moderate concentration score of 6 while leaving room for new entrants equipped with capital and differentiated technology.

Page last updated on: