Chewing Gum Market Size and Share

Market Overview

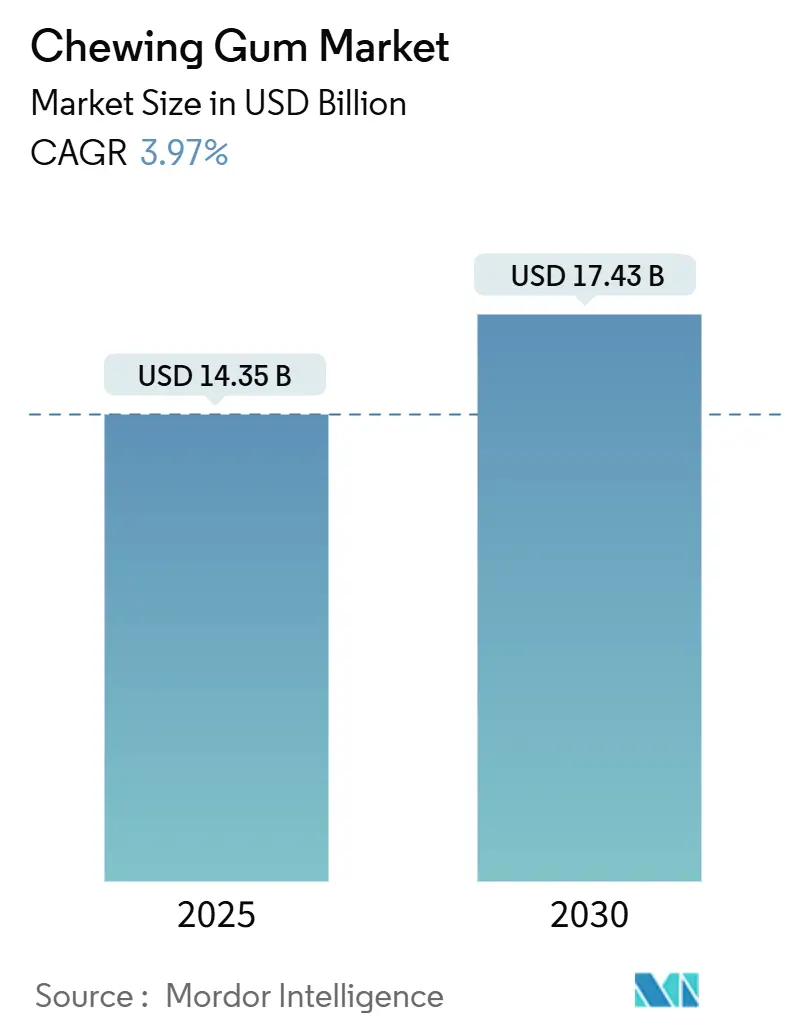

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 14.35 Billion |

| Market Size (2030) | USD 17.43 Billion |

| Growth Rate (2025 - 2030) | 3.97% CAGR |

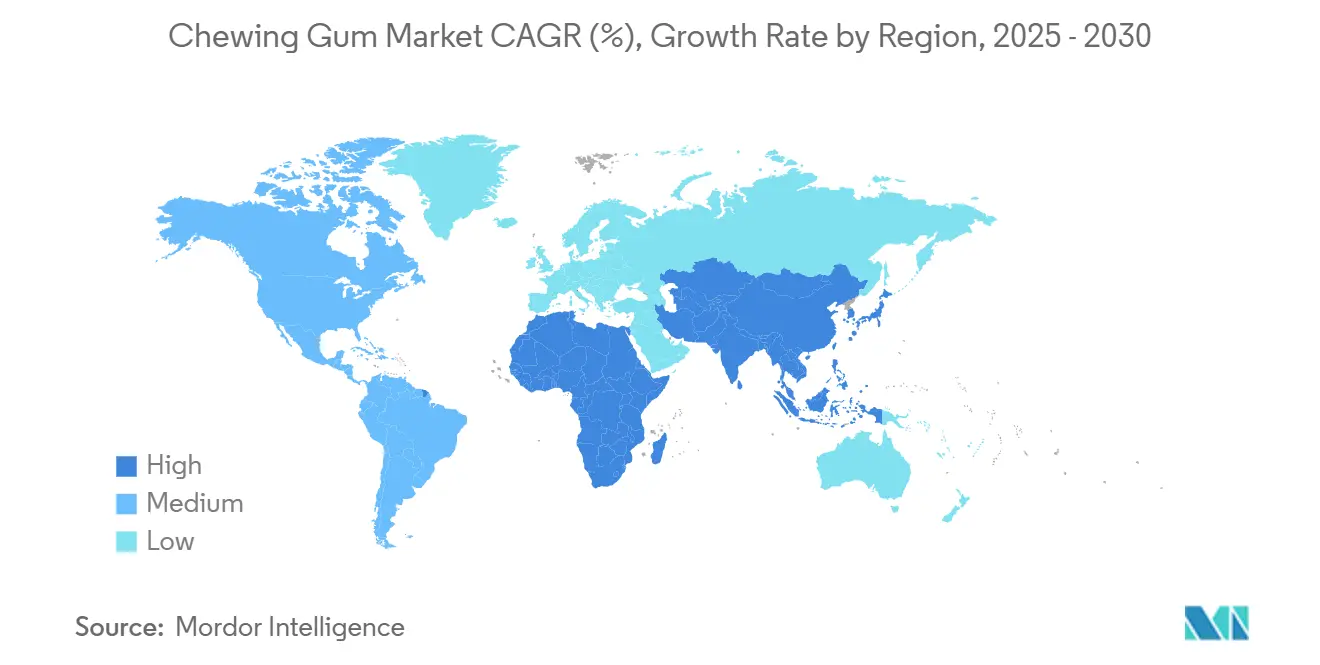

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chewing Gum Market Analysis by Mordor Intelligence

The chewing gum market, valued at USD 14.35 billion in 2025, is anticipated to reach USD 17.43 billion by 2030, registering a CAGR of 3.97% during the forecast period. This growth is driven by the rising preference for sugar-free formulations, increasing incorporation of functional ingredients, and the continued trend of impulse purchases at modern retail outlets. Manufacturers are focusing on innovations such as clean-label sweeteners, recyclable packaging, and digitally enabled convenience to maintain shelf presence and support premium pricing strategies. Additionally, growing environmental concerns are prompting producers to explore biodegradable gum bases and provide clearer disposal guidelines to address sustainability challenges. Regional dynamics reveal varied growth patterns. North America leads in per-capita consumption, reflecting a mature market with steady demand. Meanwhile, the Asia-Pacific region is emerging as a key growth driver, fueled by rapid urbanization, effective social media marketing campaigns, and rising disposable incomes, which are attracting a significant number of new consumers annually.

Key Report Takeaways

- By type, the sugar-free segment led the chewing gum market with a 60.01% market share in 2024, projected to post the fastest growth of 4.56% CAGR through 2030.

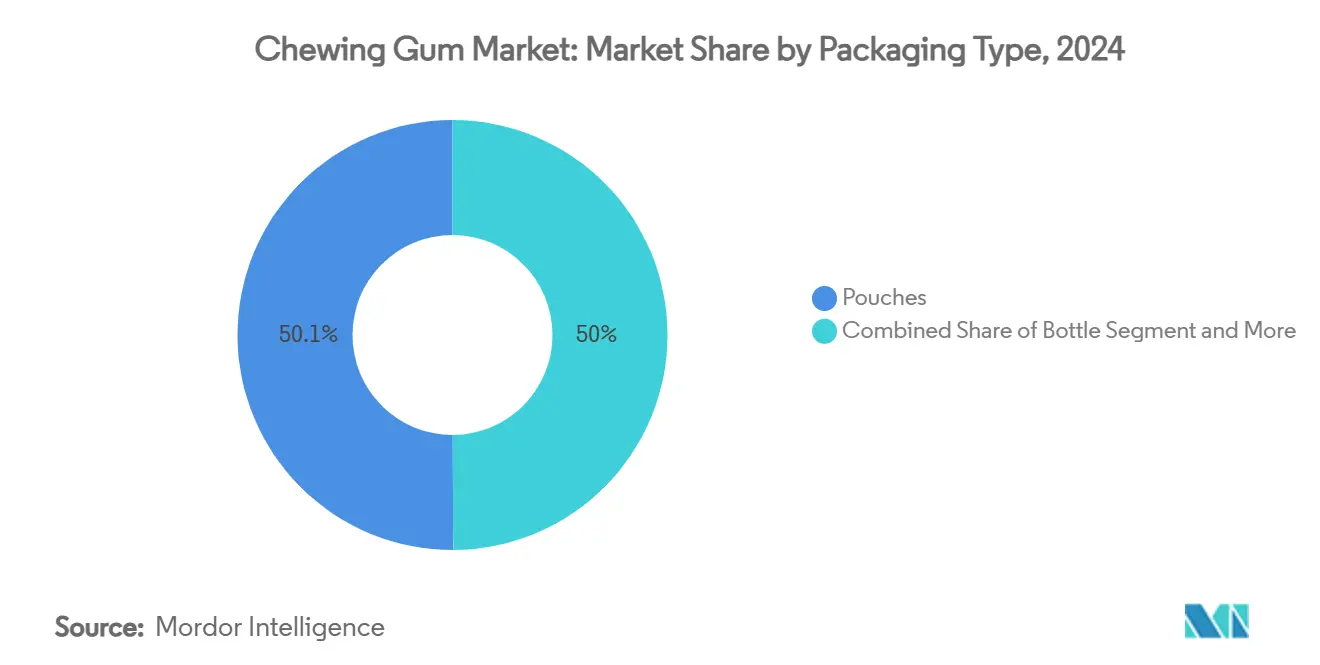

- By packaging, pouches captured 50.05% of revenue in 2024, and are forecast to expand at 6.78% CAGR to 2030.

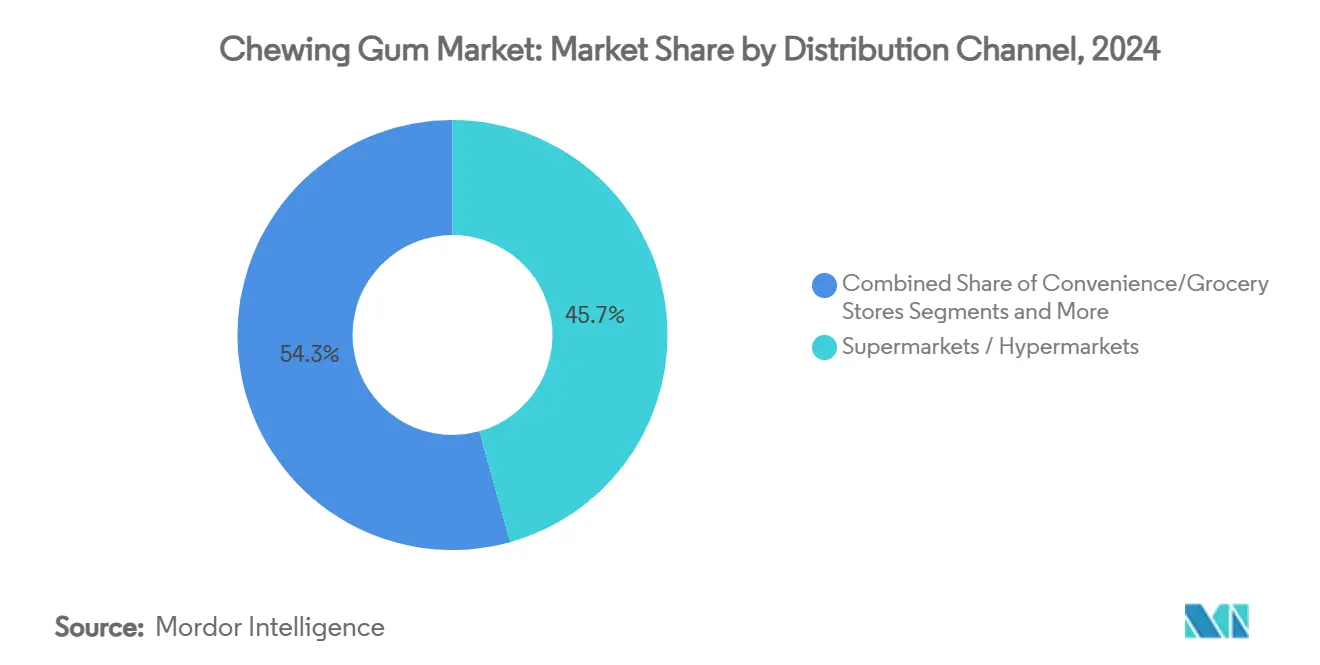

- By distribution channel, supermarkets and hypermarkets held a 45.68% share of the chewing gum market size in 2024; online retail is expected to advance at a 6.06% CAGR between 2025 and 2030.

- By geography, North America commanded 34.42% of global revenue in 2024; Asia-Pacific is on track for a 5.77% CAGR through 2030.

Global Chewing Gum Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sugar-Free Gums Supports Health-Conscious Consumption. | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Flavor Innovation Attracts Younger and Experimental Consumers. | +0.8% | Global, with emphasis on Asia Pacific | Short term (≤ 2 years) |

| Compact And Convenient Format Drives On-The-Go Snacking. | +0.6% | Global, with highest impact in urban centers | Medium term (2-4 years) |

| Marketing Focused on Oral Care Benefits Fuels Daily Usage. | +0.7% | North America, Europe, and developed Asia Pacific markets | Medium term (2-4 years) |

| Expanding Online and Convenience Store Sales Improve Accessibility. | +0.5% | Global, with strongest growth in emerging markets | Short term (≤ 2 years) |

| Impulse Buying at Checkout Counters Supports High-Volume Sales. | +0.4% | Global, with emphasis on North America & Europe | Short term (≤ 2 years) |

Source: Mordor Intelligence

Rising Demand for Sugar-Free Gums Supports Health-Conscious Consumption.

The chewing gum market is growing significantly, driven by the increasing popularity of sugar-free options. This growth reflects a broader consumer shift toward health and wellness, as people look for products that support healthier lifestyles. Functional gums, a fast-expanding segment, are gaining attention due to their additional benefits beyond traditional chewing gum. The sugar-free segment's strong performance is supported by clinical evidence, such as a 2023 study from Nutraceutical Business Review, which reported that 90% of users of functional gums designed to reduce sugar cravings experienced weight loss. To meet this rising demand, major manufacturers are reformulating existing products and launching innovative options with specific health benefits. These efforts not only align with consumer preferences but also position these products as premium offerings, enabling companies to achieve higher profit margins. Although developing natural sweeteners requires increased R&D investments, this strategy highlights the market's focus on addressing changing consumer needs and capitalizing on the growing trend of health consciousness.

Flavor Innovation Attracts Younger and Experimental Consumers.

Flavor innovation has become a pivotal factor in gaining a competitive edge, significantly contributing to the market's growth trajectory while effectively capturing the attention of younger consumers. Leading manufacturers are increasingly moving beyond traditional mint and fruit flavors, venturing into exotic, seasonal, and limited-edition offerings designed to create unique, shareable experiences that resonate strongly on social media platforms. Additionally, companies are exploring functional flavor profiles by incorporating adaptogens, nootropics, and botanical extracts, which not only enhance sensory appeal but also align with the growing consumer demand for health-oriented benefits. The strategic importance of flavor innovation is particularly evident in the Asia-Pacific markets, where consumers exhibit a higher propensity for experimenting with novel taste experiences. This region's diverse and dynamic flavor preferences present significant opportunities for market-specific product development. These locally tailored innovations often serve as a testing ground, with successful products being adapted for broader global distribution, thereby amplifying their impact on the market's overall growth.

Compact And Convenient Format Drives On-The-Go Snacking.

Chewing gum's portability makes it a perfect fit for the growing on-the-go snacking trend, which continues to gain traction among consumers. Packaging innovations have further amplified this advantage by improving convenience and addressing sustainability concerns. In 2024, the pouch segment dominates the market with a 50.05% share, driven by the adoption of recyclable materials and easy-to-open designs that enhance usability while maintaining brand identity. These advancements not only cater to environmentally conscious consumers but also improve the overall user experience. Manufacturers are strategically positioning gum as a functional snack alternative, offering benefits such as breath freshening, stress relief, and energy enhancement, all while avoiding the high caloric content of traditional snacks. This approach is particularly effective in urban markets, where time-constrained consumers prioritize portable, practical solutions that seamlessly integrate into their fast-paced lifestyles. By aligning with these evolving consumer preferences, the chewing gum market is poised for sustained growth.

Marketing Focused on Oral Care Benefits Fuels Daily Usage.

Strategic marketing efforts have successfully repositioned chewing gum from an occasional indulgence to a vital component of daily oral care routines by emphasizing its oral health benefits. Dental professionals widely support this shift, recognizing the role of sugar-free gum in stimulating saliva production, which neutralizes acids and protects tooth enamel. Manufacturers are leveraging this clinical validation by incorporating active ingredients such as xylitol, which has proven cavity-reducing properties, and forming co-branding partnerships with established oral care brands to strengthen credibility. This health-focused positioning not only creates a compelling driver for usage occasions but also encourages multiple consumption moments throughout the day. As a result, per capita consumption rates are rising in mature markets, where overall confectionery growth has stagnated, providing a significant growth opportunity for the chewing gum market.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Over Synthetic Ingredients Reduce Trust in Traditional Gums | -0.7% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Growing Preference for Natural Snacks Limits Gum Appeal | -0.5% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Regulatory Complexities Challenge Innovation and Labeling Claims | -0.4% | Global, with varying impact by region based on regulatory frameworks | Long term (≥ 4 years) |

| Environmental Concerns Over Non-Biodegradable Gum Base Hinder Sales | -0.6% | Global, with strongest impact in Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Health Concerns Over Synthetic Ingredients Reduce Trust in Traditional Gums.

Increasing consumer scrutiny of synthetic ingredients poses a significant restraint on the market. This concern extends beyond sugar content to include artificial sweeteners, flavors, and, most notably, the petroleum-based polymers used in conventional gum bases. A study conducted by the University of California, Los Angeles (UCLA) in March 2025 brought this issue into sharper focus, revealing that chewing gum can release microplastics into saliva. The research found that a single piece of gum could release up to 3,000 microplastic particles, raising alarm among consumers. This growing awareness is particularly pronounced among health-conscious demographics, who are typically the target audience for premium and functional gum products[1]American Chemical Society, "Chewing gum can shed microplastics into saliva, pilot study finds", www.acs.org. In response, manufacturers are increasingly reformulating their products to feature cleaner labels and natural alternatives. However, these efforts come with significant technical challenges and higher production costs, which exert pressure on profit margins. This financial strain limits manufacturers' ability to invest in other areas of innovation, further complicating their efforts to address evolving consumer demands.

Growing Preference for Natural Snacks Limits Gum Appeal.

The growing consumer preference for natural and minimally processed snack options is posing challenges to the growth of the chewing gum market. This shift is particularly evident among millennials and Gen Z consumers, who demand products with recognizable ingredients and transparent sourcing. Traditional gum products, often criticized for their artificial composition, are losing appeal among these demographics. This changing landscape has created opportunities for emerging players like Simply Gum and PUR Company, which emphasize plant-based ingredients in their products, like Simply sugar-free gum and sustainable sourcing to meet evolving consumer expectations. However, these natural alternatives face notable challenges. Replicating the texture, flavor longevity, and shelf stability of conventional gum remains a significant hurdle. Additionally, achieving competitive price points is difficult, limiting their ability to fully capitalize on the increasing demand for natural products. Despite these obstacles, these brands are steadily gaining traction within a niche segment. Their progress highlights the potential for further growth as they continue to address these challenges and refine their offerings to align with consumer preferences.

Segment Analysis

By Type: Sugar-Free Leads Market Transformation

In 2024, sugar-free chewing gum dominated the market, capturing a notable 60.01% share. With a projected CAGR of 4.56% from 2025 to 2030, it is poised to solidify its position as the fastest-growing segment. This surge in popularity is largely attributed to robust clinical endorsements and backing from prominent health organizations. Notably, the American Dental Association, after reviewing clinical evidence, awarded its Seal of Acceptance to several sugar-free gum brands, including Orbit and Trident. Their findings highlighted that chewing sugar-free gum for just 20 minutes post-meal can thwart cavities by boosting saliva flow, curbing plaque acids, and fortifying teeth. Since 1993, the FDA has recognized xylitol as a nutritional additive and acknowledged that sugar-free products with under 0.5 grams of sugar per serving don't contribute to dental caries. This clarity has paved the way for manufacturers to make health claims. Furthermore, clinical research underscores that sugar-free gum can notably diminish Streptococcus mutans, the chief bacteria linked to dental caries[2]American Dental Association, "Orbit Sugarfree Gum", www.ada.org. Adding to the momentum, the World Health Organization advises keeping free sugar intake below 10% of total energy consumption (around 50 grams for adults), bolstering the case for sugar-free options.

Moreover, its expanding functional benefits and robust clinical support have propelled its growth, enabling a premium position in the market. The American Academy of Pediatric Dentistry highlights xylitol's efficacy, especially in daily doses of 5-10 grams. Studies back this, showcasing caries reduction rates between 30% to 85% with regular use[3]American Academy of Pediatric Dentistry, "Policy on Use of Xylitol in Pediatric Dentistry", www.aapd.org. The Indian Health Service further emphasizes xylitol's benefits, noting its role in curbing the growth of mutans streptococci and boosting tooth remineralization. They also point out that when mothers consume xylitol gum, there's a marked decrease in the transfer of decay-causing bacteria to their children, resulting in fewer cavities. On another front, the American Diabetes Association endorses sweeteners like aspartame, saccharin, sucralose, and stevia, commonly found in sugar-free gum. They highlight these sweeteners' dual benefits: they don't elevate blood glucose levels and can assist in diabetes management, opening doors for their use beyond just confectionery items.

By Packaging: Pouches Dominate Convenience-Driven Market

Pouches, commanding a 50.05% market share in 2024, not only dominate the packaging landscape but also stand out as the fastest-growing segment, with a projected CAGR of 6.78% from 2025 to 2030. This surge underscores a clear consumer shift towards portable and convenient packaging, mirroring today's mobile lifestyles and on-the-go consumption. Pouches excel in product protection while ensuring portability, catering to time-strapped consumers seeking convenient snacking solutions. Furthermore, government-led workplace wellness initiatives and health guidelines have bolstered the rise of portion-controlled packaging, promoting mindful consumption without sacrificing convenience, solidifying pouches' market leadership.

The Federal Trade Commission mandates that environmental marketing claims, especially those related to recyclability and environmental benefits, must be backed by credible scientific evidence, ensuring marketers don't mislead consumers[4]The Federal Trade Commission, "Part 260– Guides For The Use Of Environmental Marketing Claims", www.ftc.gov. Meanwhile, the European Union's Single-Use Plastics Directive is spurring the innovation of alternative packaging materials. These materials not only preserve product freshness but also adhere to recyclability standards, giving manufacturers a competitive edge in marrying sustainability with performance. Additionally, government tax incentives for recyclable packaging, juxtaposed with penalties for non-recyclable waste, are steering the market towards pouch formats that prioritize end-of-life considerations, aligning economic growth with environmental responsibility.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Traditional Retail Maintains Leadership

In 2024, supermarkets and hypermarkets command a dominant 45.68% share of the market, skillfully using strategic product placements and understanding consumer shopping habits to lead in gum sales, capitalizing on impulse buying. Research by the Federal Trade Commission highlights the enduring power of checkout counter placements in spurring impulse buys, a trend that persists even as payment methods and shopping habits shift towards quicker transactions. Meanwhile, government agencies dedicated to consumer protection have rolled out transparent guidelines for point-of-sale marketing. These guidelines not only uphold transparency but also ensure that impulse buying strategies remain beneficial for both retailers and manufacturers. Furthermore, category management partnerships play a pivotal role, fine-tuning product assortments and placements. This collaboration bolsters the channel's effectiveness, even amidst shifting consumer behaviors and rising competition from alternative retail formats.

Online retail stores are set to be the fastest-growing distribution channel, with a projected CAGR of 6.06% from 2025 to 2030. This growth is fueled by the widespread adoption of digital commerce and supportive government initiatives that champion e-commerce development while prioritizing consumer protection. Programs by the Small Business Administration, aimed at bolstering participation in digital marketplaces, have been a boon for functional and premium gum manufacturers. These programs empower manufacturers to connect with specific consumer segments, offering detailed product insights and targeted marketing. Such strategies effectively justify premium pricing for products boasting distinct health benefits. Moreover, government regulations safeguarding online transaction consumer rights, encompassing thorough e-commerce guidelines and state-specific consumer protection laws, have fostered trust in digital shopping. This trust not only eases market entry for specialty products but also underscores the importance of consumer protection. Initiatives by the Department of Commerce, focusing on digital trade facilitation, have dismantled barriers to cross-border e-commerce. This progress enables manufacturers to tap into global markets directly via digital platforms, sidestepping traditional distribution middlemen. Concurrently, enhancements in postal services have rendered online gum purchases financially attractive for consumers, especially for specialty items not found in conventional retail outlets.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, North America dominates the global chewing gum market with a 34.42% share, driven by a strong consumer preference for sugar-free and functional gum varieties that align with the region's growing focus on health and wellness. The United States leads regional consumption, particularly excelling in the premium segment, where consumers are willing to pay a premium for innovative flavors and added functional benefits. Canada mirrors U.S. trends with a strong inclination toward health-oriented products, while Mexico exhibits a preference for traditional sugar-based gums and fruit flavors, reflecting its distinct regional taste preferences.

Asia-Pacific is emerging as the fastest-growing region in the chewing gum market, with a projected CAGR of 5.77% from 2025 to 2030. This growth is fueled by rapid urbanization, increasing disposable incomes, and rising health awareness across key markets. Japan stands out with its sophisticated consumer base, which demands innovative flavors and functional benefits, while South Korea shows a growing interest in beauty-enhancing and oral care formulations. Europe continues to hold a significant position in the chewing gum market, driven by strong demand for premium and environmentally sustainable products. Germany emphasizes functional benefits, the UK focuses on sustainability, and France prioritizes sophisticated flavor profiles. Eastern European markets are also showing potential, as rising disposable incomes drive demand for premium products, although price sensitivity remains a key consideration in these developing economies.

South America demonstrates a strong cultural connection to chewing gum, with Brazil leading regional consumption, followed by Argentina and Colombia. The region shows a marked preference for fruit flavors and social consumption occasions, prompting manufacturers to develop products tailored to local tastes and usage contexts. The Middle East and Africa represent emerging opportunities, characterized by uneven market development. South Africa leads the sub-Saharan market with growing urban consumption, while North African countries exhibit preferences influenced by Mediterranean flavor profiles. Across all regions, the trend toward sugar-free formulations is gaining momentum, although the rate of adoption varies depending on local health awareness and economic conditions.

Competitive Landscape

The global chewing gum market is moderately consolidated, with major players such as Mondelez International, Mars, Incorporated, Perfetti Van Melle Group BV, Lotte Corporation, and The Hershey Company leading the market. These companies maintain their dominance through extensive distribution networks, strong brand recognition, and continuous product innovation. However, the market also includes several regional and niche players, particularly in emerging economies, who focus on meeting local flavor preferences and offering affordable options to attract price-sensitive consumers.

Growth opportunities are emerging in the areas of sustainability and functionality. Smaller players are gaining traction by introducing natural and biodegradable chewing gum alternatives that address growing environmental concerns highlighted by government agencies and environmental organizations. These companies stand out by using clean, eco-friendly ingredients and positioning their products as environmentally responsible. This strategy aligns with government sustainability goals and the rising consumer demand for greener products, giving these players a competitive edge in the market.

Technology adoption is transforming the industry, with established companies investing in advanced formulation techniques to enhance the texture and flavor release of sugar-free gum. These innovations also help companies comply with increasingly stringent regulatory standards for ingredient safety and environmental impact. The market is shifting toward health-focused and sustainable products, driven by regulatory requirements and consumer preferences for chewing gum that offers functional benefits while reducing its environmental footprint.

Chewing Gum Industry Leaders

-

Perfetti Van Melle Group BV

-

Lotte Corporation

-

Mondelēz International Inc.

-

Mars, Incorporated

-

The Hershey Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Trident Vibes has launched its sugar-free Cotton Candy flavored gum to the national retail market, available in a 40-piece bottle, following a successful exclusive release at a major United States retailer. According to the brand, this new gum offers a sweet, nostalgic cotton candy taste with a sugar-free recipe, targeting both health-conscious consumers and younger audiences, particularly Gen Z.

- April 2025: Milliways, a British plastic-free chewing gum brand, has launched in the French market by offering plant-based, biodegradable gum as an alternative to conventional plastic-based gums. The brand introduced new flavors inspired by French tastes—Strawberry, Cherry, and Eucalyptus Mint—alongside its classic mint varieties, available in 10- and 30-piece packs across major French retailers.

- February 2025: Mars Wrigley has launched Extra Refreshers Watermelon Raspberry gum, a sugar-free product available nationwide in seven- and 30-piece packs, and backed by a GBP 4.5 million marketing campaign. According to the brand, this is the first gum of its kind, created in response to the rising popularity of fruity flavors, and it aims to attract younger shoppers and new consumers to the gum category.

- May 2024: Gandour has launched its sugar-free gum in a variety of flavors, including classics like mastic, peppermint, and spearmint, as well as fun new options, aiming to provide healthier choices for consumers. According to the brand, this launch aligns with rising demand for sugar-free products driven by health concerns such as diabetes and a focus on oral care, offering alternatives that help reduce sugar intake and support dental health.

Global Chewing Gum Market Report Scope

Gums are cohesive substances made with ingredients such as latex sap, which is combined with flavorings and sweeteners. Gums are designed to be chewed without being swallowed. The chewing gum market is segmented by type, distribution channel, and geography. By product type, the market is segmented into sugar-free and sugared chewing gums. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. The report also provides an analysis of the emerging and established trends in North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| By Type | Sugar-Based Chewing Gum | ||

| Sugar-free Chewing Gum | |||

| By Packaging | Pouches | ||

| Bottle | |||

| Box | |||

| Others | |||

| By Distribution Channel | Supermarkets / Hypermarkets | ||

| Convenience/Grocery Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Sugar-Based Chewing Gum |

| Sugar-free Chewing Gum |

| Pouches |

| Bottle |

| Box |

| Others |

| Supermarkets / Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the chewing gum market?

The chewing gum market size stands at USD 14.35 billion in 2025, reflecting sustained demand for sugar-free and functional formulations.

Which product type leads global sales?

Sugar-free chewing gum dominates with 60.01% market share in 2024, a position reinforced by dental health endorsements and clean-label sweeteners.

Which region is growing fastest?

Asia Pacific is projected to deliver a 5.77% CAGR from 2025 to 2030 due to rising disposable incomes, urban lifestyles, and appetite for novel flavors.

Why are functional gums gaining popularity?

Functional gums deliver benefits like energy, stress relief, or smoking cessation in convenient micro-dosages, with forecasts indicating a 9.7% CAGR through 2030 for this segment. . . . . . . . New Research

Page last updated on: July 3, 2025