Chemical Peel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

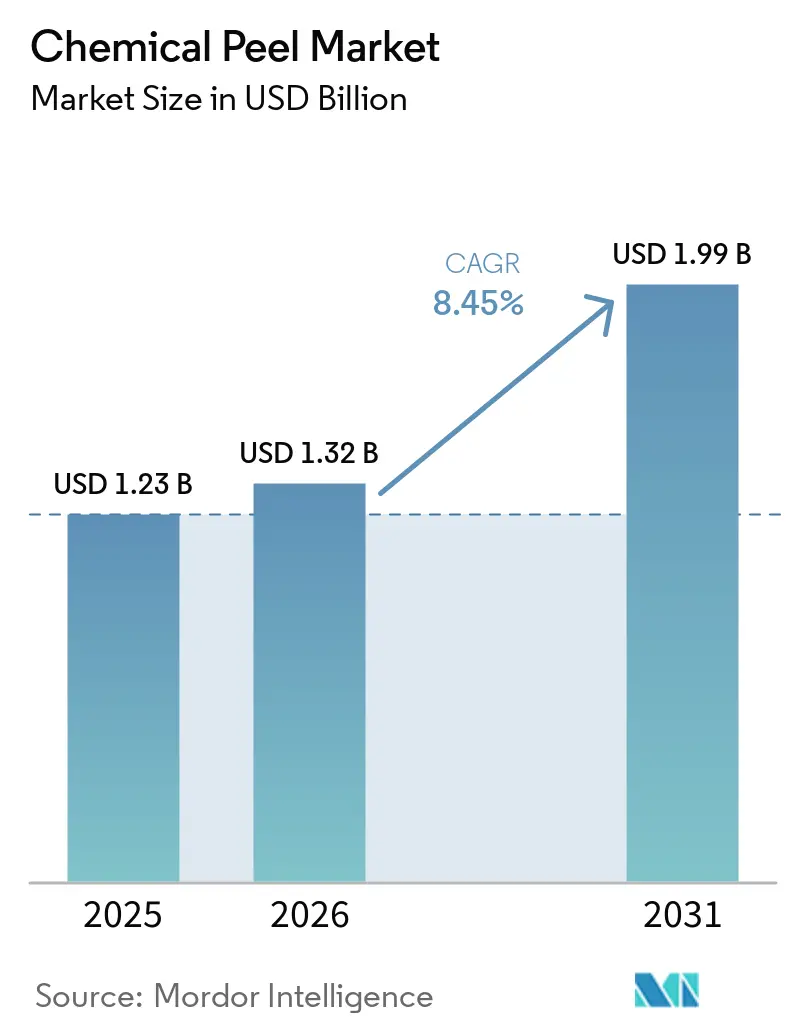

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.99 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemical Peel Market Analysis by Mordor Intelligence

The Chemical Peel Market size was valued at USD 1.23 billion in 2025 and is estimated to grow from USD 1.32 billion in 2026 to reach USD 1.99 billion by 2031, at a CAGR of 8.45% during the forecast period (2026-2031).

Growth is being supported by a broader move toward low-downtime skin resurfacing, and the AAFPRS 2025 Annual Survey published in February 2026 stated that noninvasive treatments now account for 80% of facial procedures, while facial procedure volume is set to increase 19%. The patient base is also entering treatment earlier, with people under 30 increasingly using preventive peel protocols instead of waiting for corrective care, which extends repeat treatment demand for clinics over a longer period. The chemical peel market also benefits from melanin-safe treatment protocols, stronger medical-cosmetic integration across Asia-Pacific, and reimbursement support in parts of North America for selected acne-related peel use. Competition is centered on buffered systems, combination acids, and education-led channel expansion rather than on acid strength alone, which keeps differentiation high across dermatology clinics, med spas, and aesthetic chains. At the same time, the chemical peel market remains shaped by safety limits around medium and deep peels and by tighter scrutiny of unsupervised high-strength home products, which continues to favor supervised professional settings and supports demand for AI-assisted treatment selection tools.

Key Report Takeaways

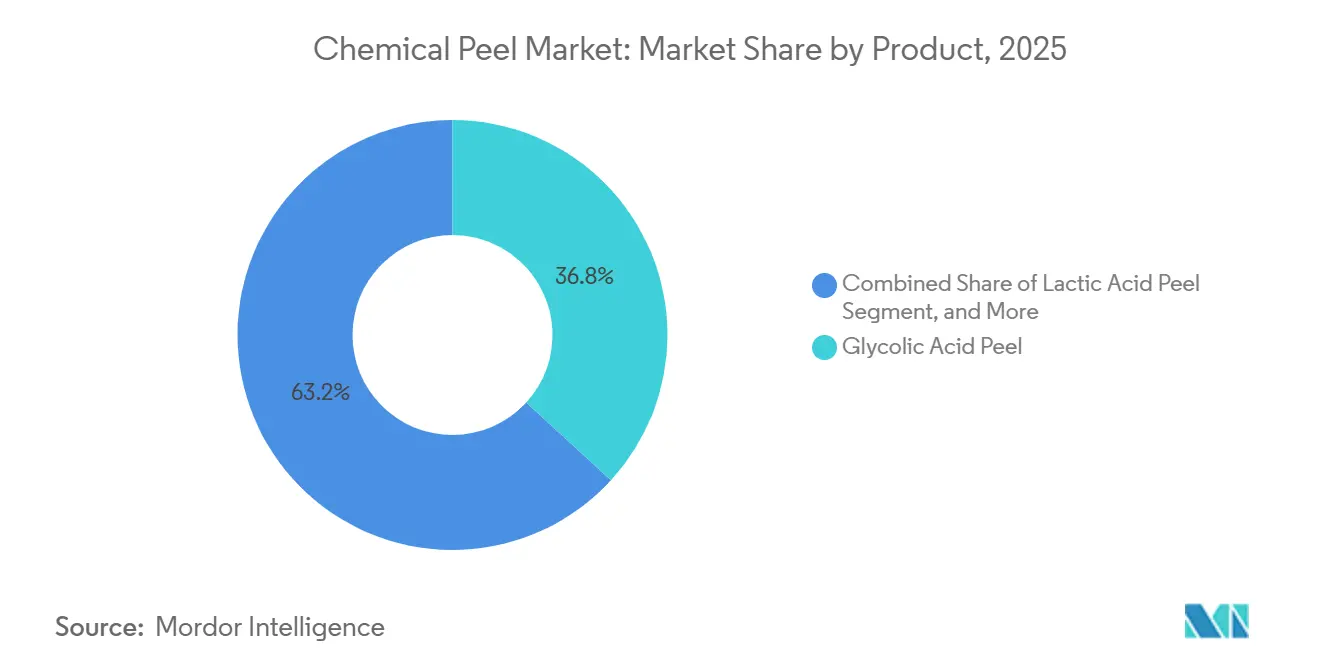

- By product, Glycolic Acid Peel led with 36.78% revenue share in 2025, while Lactic Acid Peel is projected to grow at a 9.16% CAGR through 2031.

- By peel depth, Superficial or Light Peels accounted for 42.16% share in 2025, while Medium Peels are set to advance at an 8.83% CAGR through 2031.

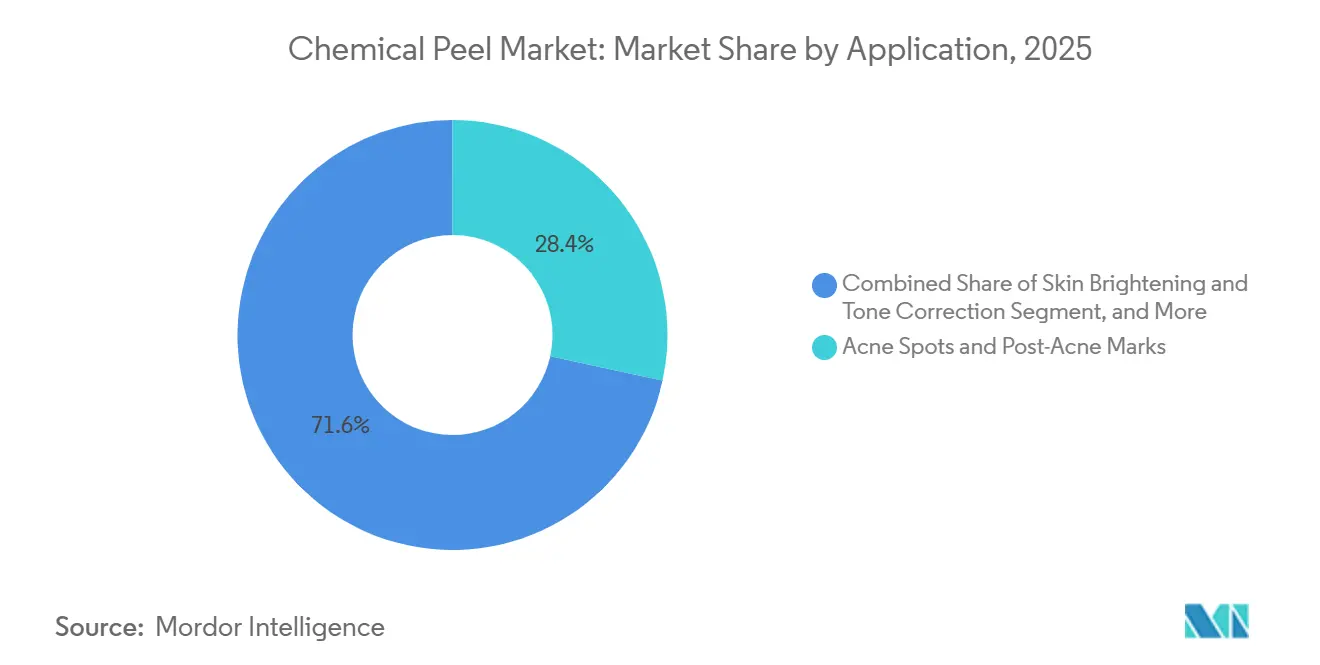

- By application, Acne Spots and Post-Acne Marks captured 28.43% share in 2025, while Skin Brightening and Tone Correction are expected to rise at a 9.85% CAGR through 2031.

- By end use, Dermatology Clinics held 52.71% share in 2025, while Beauty and Aesthetic Clinics are projected to expand at an 11.15% CAGR through 2031.

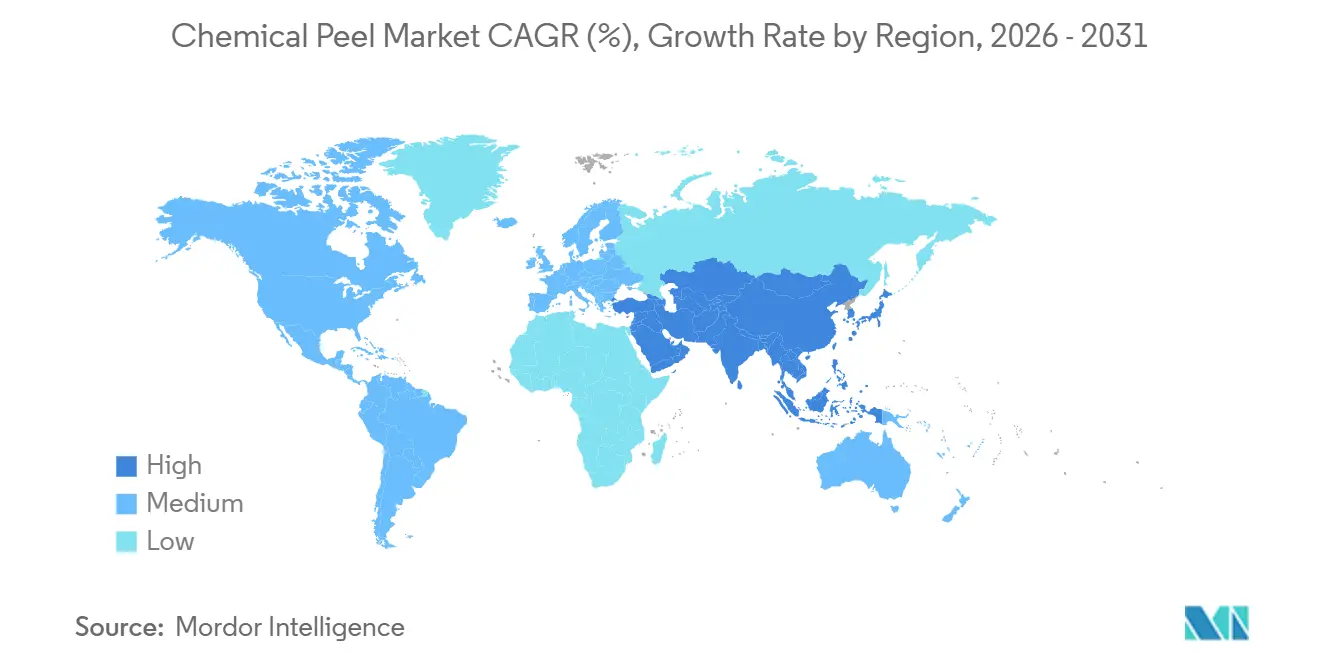

- By geography, North America held 44.21% of the chemical peel market share in 2025, while Asia-Pacific is forecast to expand at a 10.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Chemical Peel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally Invasive Resurfacing | +1.8% | Global, peak in North America and Europe | Medium term (2-4 years) |

| Acne, Pigment, and Photoaging Case-Load Expansion | +2.0% | Global, APAC and MEA disproportionate | Long term (≥ 4 years) |

| Med Spa and Dermatology Network Expansion | +0.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Buffered and Combination-Acid Product Innovation | +1.0% | Global, formulation hubs in Europe and APAC | Short term (≤ 2 years) |

| AI-Assisted Skin Analysis and Protocol Personalization | +0.7% | North America, APAC core including South Korea and China, spill-over to MEA | Medium term (2-4 years) |

| Melanin-Safe Formulations Broaden Eligible Patients | +0.6% | APAC, MEA, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Resurfacing

The sustained preference for low-downtime treatment is moving more patients toward superficial and medium-depth peels instead of more invasive resurfacing options. The AAFPRS 2025 Annual Survey, published in February 2026, stated that noninvasive procedures represent 80% of all facial procedures and also pointed to a 19% increase in facial procedure volume, which supports higher procedure flow across the chemical peel market.[1]American Academy of Facial Plastic and Reconstructive Surgery, “AAFPRS 2025 Annual Survey,” Plastic Surgery Practice, plasticsurgerypractice.com This shift matters because the procedure is easier to repeat, easier to fit into daily schedules, and easier for clinics to integrate into routine treatment menus. Demand is also getting younger, with patients under 30 choosing preventive care earlier, which extends the potential treatment cycle over more years. That pattern is pushing operators to build more repeat-visit protocols around light and medium treatments rather than relying on low-volume deep resurfacing alone.

Acne, Pigment, and Photoaging Case-Load Expansion

The chemical peel market continues to draw steady demand from acne, pigmentation, and photoaging case loads that remain large across both medical and aesthetic settings. Blue Shield of California stated in its February 2026 policy that acne vulgaris affects 80% of teenagers between 13 and 18 globally and that actinic keratosis affects 11% to 26% of the adult population in the United States, which supports durable baseline need for glycolic, salicylic, and TCA peels.[2]Blue Shield of California, “Medical Policy 8.01.16, Chemical Peels,” Blue Shield of California, blueshieldca.com The Federal Employee Program Medical Policy Manual from April 2025 also classified superficial 40% to 70% AHA peels as medically necessary for active acne unresponsive to systemic antibiotics and recognized dermal peels as medically necessary when more than 10 actinic keratoses are documented. That type of payer recognition reduces the usual price sensitivity seen in elective aesthetics and gives dermatology clinics a more predictable floor of demand. It also keeps chemical peels clinically relevant against newer topical options because the treatment can still deliver competitive outcomes at a lower procedural cost in many patient pathways.

AI-Assisted Skin Analysis and Protocol Personalization

AI-based skin assessment is becoming a practical support layer for treatment planning across the chemical peel market. Haut.AI released Face Analysis 3.0 in November 2025, and the platform evaluates more than 40 skin parameters from standard photographs while improving measurement stability by 30% against earlier versions. Clarins also deployed its AI Skin Observer across 20 stores globally in January 2026 and said the tool assesses 22 biophysical skin parameters during each consultation session. These systems help narrow the gap between high-end dermatology centers and independent aesthetic clinics because they make screening, protocol selection, and contraindication review more consistent. They also support safer use of medium-depth procedures by helping practitioners screen for skin type, barrier weakness, rosacea, and other factors that can raise the risk of post-procedure complications.

Melanin-Safe Formulations Broaden Eligible Patients

The addressable patient pool in the chemical peel market is widening as suppliers build more protocols for Fitzpatrick IV to VI skin types. VI Aesthetics launched VI Peel Precision + Peptides in September 2025 with a Fitzpatrick I to VI validated protocol that is deployed across more than 7,000 provider sites, including Mayo Clinic and Cedars Sinai. This matters because many of the fastest-expanding patient pools in Asia-Pacific, the Middle East, Africa, and Latin America need better tolerance and lower post-inflammatory hyperpigmentation risk before they enter regular treatment cycles. Melanin-safe positioning is therefore not a niche product claim, because it directly broadens who can be treated with confidence and how often those patients return. It also reinforces the shift toward brightening, tone correction, and pigment-focused uses that are expanding faster than older wrinkle-only treatment pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-Event Risk in Medium and Deep Peels | -1.6% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Competition from Laser, Microneedling, and IPL | -1.4% | North America, Europe, APAC core | Medium term (2-4 years) |

| FDA Scrutiny of Unsupervised High-Strength Home Peels | -1.3% | United States, with spill-over to English-speaking markets | Short term (≤ 2 years) |

| Training Variability and Imported-Input Margin Pressure | -0.9% | APAC, MEA, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Risk in Medium and Deep Peels

Medium and deep peels still face a real adoption ceiling because adverse-event risk rises quickly when protocols are not handled by trained medical practitioners. Data presented at the AIME Congress in January 2026 stated that phenol-croton oil deep peels can deliver an average 8.2-year visual age reduction, but the face must be divided into aesthetic units and each application needs at least 15 minutes between sections to avoid cardiac arrhythmia risk. Those limits reduce throughput and keep the treatment concentrated in specialist dermatology and plastic surgery settings. They also make insurance, training, and legal exposure more difficult for mid-tier aesthetic clinics that want higher-margin treatments but lack the same depth of medical supervision. As a result, the chemical peel market continues to favor broad volume in superficial protocols while medium and deep peels remain narrower and more concentrated.

FDA Scrutiny of Unsupervised High-Strength Home Peels

Regulatory pressure on unsupervised high-strength home peels is limiting one part of the chemical peel market even as it redirects some demand to clinics. In July 2024, the FDA sent warning letters to 6 online retailers, including Amazon and Walmart storefronts, for selling chemical peel products with strengths as high as 100% TCA, 70% glycolic acid, and 90% lactic acid, classifying them as unapproved new drugs under the FD&C Act. The agency then issued a consumer safety communication on July 30, 2024 and stated that no chemical peel products carry FDA approval. This action is pushing consumer products toward lower strengths that fit cosmetic status more clearly, while professional-strength outcomes remain concentrated in supervised settings. The result is a clearer split between clinic-grade resurfacing and consumer exfoliation, which supports professional channels but constrains the direct-to-consumer high-strength segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Glycolic Acid Holds Command, Lactic Acid Charts a Different Course

Glycolic acid peel held 36.78% of the chemical peel market in 2025, which made it the largest product segment in the report. Its lead came from long clinical use across acne, photoaging, and hyperpigmentation, and from a penetration profile that practitioners understand well in daily treatment planning. That familiarity keeps glycolic acid in a strong first-line position across dermatology clinics and med spas because operators value protocol consistency as much as visible results. Salicylic acid maintains durable demand in acne care because of its lipophilic and comedolytic action, while TCA and phenol remain tied to specialist resurfacing use where deeper correction is needed. The chemical peel market still treats glycolic acid as the reference product because it sits at the center of both medical and aesthetic workflows, which gives it a reach that narrower specialty acids do not match.

Lactic acid peel is projected to grow at a 9.16% CAGR from 2026 to 2031, making it the fastest-growing product segment in the chemical peel market. Its appeal comes from a dual role in resurfacing and moisture support, which fits the growing preference for gentler protocols among patients with sensitivity concerns. That profile also aligns well with rising treatment demand from higher Fitzpatrick skin types, where tolerability matters more in first-time or maintenance care. Combination and fruit acid peels are the part of the chemical peel industry seeing the most active redesign, as brands use buffered systems and skin-mimetic carriers to improve tolerance and widen use across different skin types. As those systems improve recovery and comfort, they may pull some future demand away from single-acid formats before 2028.

By Peel Depth / Type: Superficial Volume Holds, Medium Peel Upgrades the Category

Superficial or light peels retained 42.16% share of the chemical peel market size in 2025, supported by minimal downtime and broad compatibility across settings and skin types. They remain the default offer in beauty clinics and home-oriented routines because they are easier to repeat and carry a wider safety margin. Deep Peels stay concentrated in advanced dermatology and plastic surgery environments where cardiac monitoring, careful interval timing, and specialist training can be maintained. This creates a clear barbell structure in the chemical peel market, with high-volume superficial procedures at one end and low-volume high-revenue deep procedures at the other end. Medium Peels are filling the space between those two poles and are becoming the main value-growth layer through 2031.

Medium peels are projected to expand at an 8.83% CAGR from 2026 to 2031, making them the fastest-growing depth category in the chemical peel market. That pace reflects rising practitioner confidence in buffered TCA protocols and stronger comfort with medium-depth treatment for acne scarring and moderate photoaging. AIME Congress material presented in January 2026 also reinforced the clinical value of deeper resurfacing, which helps clinics justify selective upselling where training and patient screening are strong. AI-supported screening adds to this shift because it helps practitioners review contraindications more consistently before selecting a deeper procedure. The result is a broader middle tier in the chemical peel market where operators can move beyond basic resurfacing without taking on the full risk profile of deep phenol treatment.

By Application: Brightening Reshapes the Growth Narrative

Acne spots and post-acne marks accounted for 28.43% of the chemical peel market in 2025, which made acne-related treatment the largest application category. That lead reflects the scale of acne burden in younger populations and the continued role of peels in managing active acne, residual marks, and textural irregularity in a repeat-care format. The segment also benefits from reimbursement support in defined clinical cases, which gives dermatology channels steadier demand than purely discretionary cosmetic care. Hyperpigmentation and melasma remain large adjacent uses because they often respond well to combination protocols that pair peels with topical maintenance. This keeps the chemical peel market closely tied to conditions that sit between therapy and appearance, which broadens the base of paying patients.

Skin brightening and tone correction is forecast to grow at a 9.85% CAGR from 2026 to 2031, the fastest application pace in the chemical peel market. VI Aesthetics supported this direction in September 2025 by launching VI Peel Precision + Peptides with a Fitzpatrick I to VI validated protocol across more than 7,000 provider sites. The category is gaining momentum because demand is moving from purely corrective care toward visible tone refinement and more even complexion outcomes, especially in regions with larger darker-skin populations. Fine lines and wrinkles remain important, but they face more substitution from laser and microneedling options in part of the anti-aging pathway. Scars and dark circles stay smaller in volume, yet they remain commercially relevant because combination peels provide a lower-cost entry point than several energy-based alternatives.

By End Use: Clinical Anchor Holds, Aesthetic Channels Define Future Margin

Dermatology clinics held 52.71% of the chemical peel market size in 2025, which kept the clinical channel in the lead by a clear margin. This position is supported by medical necessity pathways for selected indications and by the supervision requirements that still shape medium and deep peel use. Dermatologists also benefit from stronger patient trust in cases involving acne, actinic damage, melasma, or higher-risk skin types, which helps protect procedure volume even when consumer spending is uneven. Hospitals contribute a more limited volume, but they remain relevant for medically indicated treatments that sit within broader dermatology care. This gives the chemical peel industry a stable clinical base even as more growth shifts into non-hospital environments.

Beauty and aesthetic clinics are projected to grow at an 11.15% CAGR from 2026 to 2031, making them the fastest-growing end-use segment in the chemical peel market. Marini SkinSolutions expanded directly into this channel in January 2025 through its partnership with Restore Hyper Wellness, introducing 4 zero-downtime chemical peels and 4 facials across more than 220 studios in 40 U.S. states. That move shows how standardized protocols can be scaled through lower-cost, higher-frequency consumer touchpoints outside the traditional physician office. Med spas sit in the middle of the channel mix because they combine some clinical signaling with strong aesthetic positioning, which makes them highly responsive to both regulation and brand training. Home Care Settings remain the most constrained end use after the FDA action against high-strength direct-to-consumer peel products, which has limited unsupervised formats to lower-strength exfoliation rather than true resurfacing.

Geography Analysis

North America accounted for 44.21% of the chemical peel market share in 2025, which made it the largest regional segment in the report. Demand remains high because the region has a dense network of dermatology clinics, med spas, and professional skincare brands that can support repeat treatment use. The AAFPRS 2025 Annual Survey published in February 2026 stated that noninvasive treatments represented 80% of all facial procedures and pointed to a 19% increase in facial procedure volume, which supports recurring peel demand across U.S. clinical and aesthetic settings. Canada and Mexico add support to regional volume, and Mexico is especially relevant in medium and deep procedures because its medical tourism offer provides lower treatment costs than many U.S. clinics.

Europe remained the second-largest regional block in the chemical peel market, and product design in the region is strongly shaped by EU Cosmetics Regulation (EC) No 1223/2009. The regulation limits glycolic acid to 10% in rinse-off products and 8% in leave-on products with a minimum pH of 3.5, while salicylic acid is capped at 2% in leave-on formats . These limits favor buffered and combination systems that rely on protocol design rather than one high-strength acid alone. Germany, France, the United Kingdom, Italy, and Spain account for most regional volume, and Germany's import dependence leaves part of the market more exposed to exchange-rate movement and supply disruption.

Asia-Pacific is forecast to expand at a 10.21% CAGR from 2026 to 2031, the fastest regional pace in the chemical peel market. The region benefits from South Korea's role as a formulation hub, China's closer links between cosmetic and medical service models, and India's expanding urban dermatology network. Melanin-safe protocol development matters strongly here because a large share of the addressable patient base falls within Fitzpatrick IV to VI skin types, which raises demand for pigment-safe brightening and resurfacing options, and VI Peel Precision + Peptides is one example of this direction. The Middle East and Africa add growth through affluent GCC demand and medical tourism flows into specialist aesthetic centers. South America also remains relevant because Brazil combines a large eligible patient pool with a mature aesthetic medicine ecosystem, which makes it the strongest structural market in the region for professional peel brands.

Competitive Landscape

The chemical peel market is moderately concentrated, with pharmaceutical-backed aesthetics groups and professional skincare brands competing across many of the same clinic and med-spa channels. Companies such as Allergan Aesthetics, Merz Aesthetics, mesoestetic Pharma Group, and Obagi Medical bring broader medical portfolios and deeper clinical relationships, while PCA SKIN, IMAGE Skincare, ZO Skin Health, and VI Aesthetics compete heavily through education and protocol support. In practical terms, buyers are no longer choosing mainly by acid type, because buffered systems, melanin-safe protocols, skin-mimetic carriers, and ease of use now shape the decision more directly. The chemical peel market also favors suppliers that can give practitioners repeatable training, since clinics tend to remain with systems they can deliver safely and consistently over time.

Channel expansion was one of the clearest competitive patterns in 2025 and 2026. Marini SkinSolutions used its January 2025 partnership with Restore Hyper Wellness to place 4 zero-downtime chemical peels and 4 facials across more than 220 studios in 40 U.S. states. Obagi Medical leaned into clinician education and presented 6-year apparent age-reversal data from its ALOHA Program across more than 300 sites at the May 2026 Music City SCALE meeting. Galderma expanded the treatment ecosystem in May 2026 by launching Alastin Regenerating Skin Nectar with TriHex+™ as a pre- and post-peel recovery adjunct in the United States. These moves show that the chemical peel market is being contested through access, education, and treatment system depth rather than through price alone.

White space remains visible in mid-tier aesthetic clinics across Asia-Pacific and the Middle East, in regulated home-use exfoliation, and in products tailored for Fitzpatrick IV to VI patients. VI Aesthetics moved directly at the last of these gaps in September 2025 by launching VI Peel Precision + Peptides for Fitzpatrick I to VI use across more than 7,000 provider sites, including Mayo Clinic and Cedars Sinai. IMAGE Skincare also signaled a clinical refocus in January 2026 when co-founder Dr. Marc Ronert returned as CEO after a more distribution-led phase. Because several suppliers are credible in both medical and aesthetic channels, no single company appears to control the chemical peel market across all acids, depths, and end uses. That balance keeps rivalry active, yet it also leaves room for education-led specialists and regional partnerships to gain traction without needing mass consumer scale.

Chemical Peel Industry Leaders

Dermalogica

Allergan Aesthetics

L'Oréal

Merz Aesthetics

Pierre Fabre / Glytone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Galderma launched Alastin Regenerating Skin Nectar with TriHex+™ in the United States, incorporating Octapeptide-45 and positioning the product as a pre- and post-chemical peel recovery adjunct. International expansion is confirmed, indicating Galderma's intent to build a peri-peel product ecosystem beyond its injectable franchise.

- January 2026: IMAGE Skincare co-founder Dr. Marc Ronert returned as CEO, signaling a strategic refocus toward clinical differentiation and innovation leadership following a distribution-oriented management period.

- September 2025: VI Aesthetics launched VI Peel Precision + Peptides, combining MelanoCalm Peptide, SkinBoost Peptide, and bioavailable retinoids in a Fitzpatrick I-VI-validated protocol deployed across more than 7,000 provider sites including Mayo Clinic and Cedars Sinai.

- September 2025: ZO Skin Health launched its Peptide Facial Refining Concentrate, supported by a 12-week clinical study showing 92% of subjects experienced reduced fine lines and 84% reported visibly younger facial geometry.

Global Chemical Peel Market Report Scope

The Chemical Peel Market refers to the global commercial sector focused on the manufacturing, distribution, and sale of chemical solutions used in dermatology and cosmetic procedures. These solutions are applied to the skin to cause controlled exfoliation and peeling, promoting cellular turnover, collagen production, and skin rejuvenation.

The Chemical Peel Market Report is segmented by Product, including Glycolic, Lactic, Salicylic, TCA, Phenol, and Combination Acid Peel, by Peel Depth, including Superficial, Medium, and Deep, by Application, including Acne, Hyperpigmentation, Fine Lines, Scars, Dark Circles, and Skin Brightening, by End Use, including Dermatology Clinics, Med Spas, Hospitals, Aesthetic Clinics, and Home Care, and by Geography, including North America, Europe, Asia-Pacific, MEA, and South America. The market forecasts are provided in terms of value in USD.

| Glycolic Acid Peel |

| Lactic Acid Peel |

| Salicylic Acid Peel |

| Trichloroacetic Acid Peel |

| Phenol Peel |

| Combination and Fruit Acid Peel |

| Superficial / Light Peel |

| Medium Peel |

| Deep Peel |

| Acne Spots and Post-Acne Marks |

| Hyperpigmentation and Melasma |

| Fine Lines and Wrinkles |

| Scars |

| Dark Circles |

| Skin Brightening and Tone Correction |

| Dermatology Clinics |

| Med Spas |

| Hospitals |

| Beauty and Aesthetic Clinics |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Glycolic Acid Peel | |

| Lactic Acid Peel | ||

| Salicylic Acid Peel | ||

| Trichloroacetic Acid Peel | ||

| Phenol Peel | ||

| Combination and Fruit Acid Peel | ||

| By Peel Depth / Type | Superficial / Light Peel | |

| Medium Peel | ||

| Deep Peel | ||

| By Application | Acne Spots and Post-Acne Marks | |

| Hyperpigmentation and Melasma | ||

| Fine Lines and Wrinkles | ||

| Scars | ||

| Dark Circles | ||

| Skin Brightening and Tone Correction | ||

| By End Use | Dermatology Clinics | |

| Med Spas | ||

| Hospitals | ||

| Beauty and Aesthetic Clinics | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of chemical peels through 2031?

The chemical peel market stands at USD 1.32 billion in 2026 and is projected to reach USD 1.99 billion by 2031, growing at an 8.5% CAGR over 2026 to 2031.

Which product category leads sales and which one is growing the fastest?

Glycolic acid peel led with 36.8% share in 2025, while Lactic acid peel is projected to grow the fastest at a 9.2% CAGR through 2031.

Why are more clinics adding these treatments to their menus?

Demand is rising because patients want low-downtime resurfacing, acne and pigmentation cases remain large, and some clinical uses benefit from reimbursement support in North America.

Which region leads demand and which region is expanding the fastest?

North America led with 44.21% share in 2025, while Asia-Pacific is forecast to post the fastest growth at a 10.21% CAGR through 2031.

Page last updated on: