Cardiopulmonary Stress Testing Systems Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

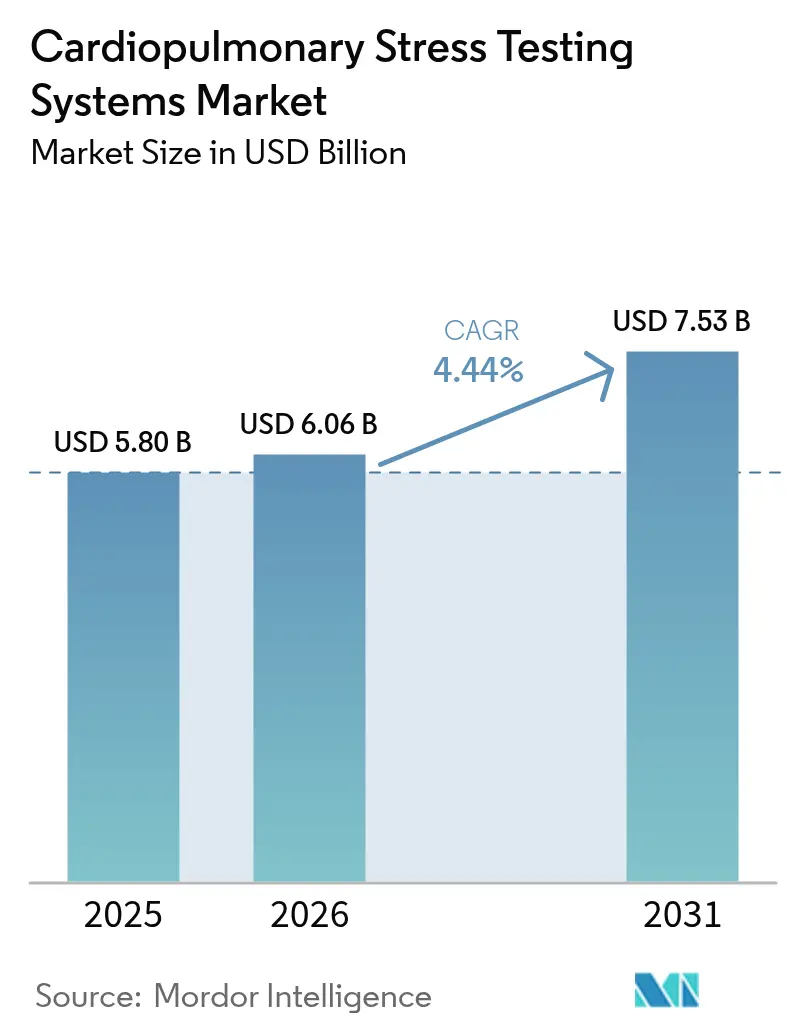

| Market Size (2026) | USD 6.06 Billion |

| Market Size (2031) | USD 7.53 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiopulmonary Stress Testing Systems Market Analysis by Mordor Intelligence

The cardiopulmonary stress testing systems market size was valued at USD 5.80 billion in 2025 and estimated to grow from USD 6.06 billion in 2026 to reach USD 7.53 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031). Growth rests in the broader shift from volume-based diagnostics to precision cardiopulmonary evaluation, helped by AI-enabled real-time VO₂ analytics that shorten interpretation time and raise diagnostic consistency. Hospitals, sports laboratories, and rehabilitation centers also view these systems as strategic assets because early physiological insights reduce downstream treatment costs. Portable CPET platforms extend testing into home-based rehabilitation, while wearable sensors feed continuous data to cloud algorithms, linking disease diagnostics with fitness monitoring. North American reimbursement clarity, rising Asia-Pacific chronic-disease burden, and steady European clinical research activity collectively underpin demand for the expanding fleet of AI-ready devices. Meanwhile, mid-tier device makers face a regulatory maze that lengthens launch cycles, keeping bargaining power with hospitals moderate, even as user expectations for seamless workflow integration rise.

Key Report Takeaways

- By product type, cardiopulmonary exercise-testing systems held 25.47% of the cardiopulmonary stress testing systems market share in 2025, and the segment is growing fastest at 10.74% CAGR to 2031.

- By end user, hospitals captured 28.02% revenue in 2025, while sports-performance and research labs post the highest projected CAGR of 9.82% through 2031.

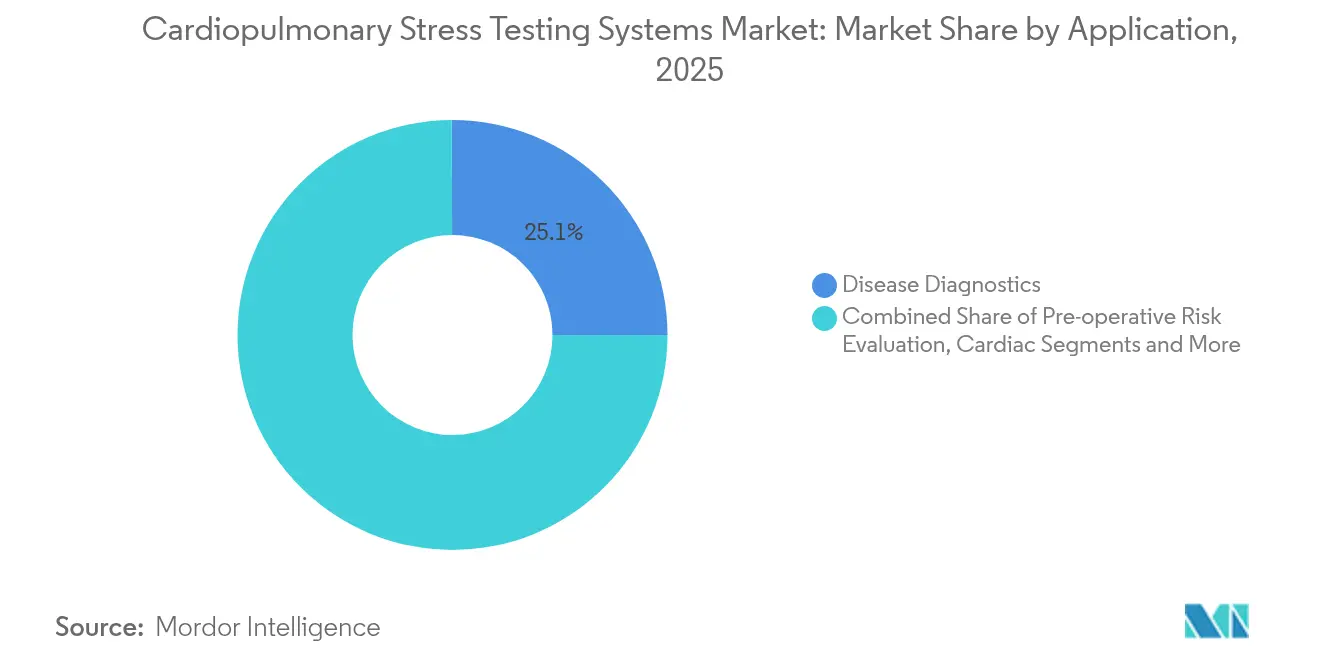

- By application, disease diagnostics commanded 25.06% of the cardiopulmonary stress testing systems market size in 2025; sports and human-performance assessment is expanding at a 9.05% CAGR to 2031.

- By technology, treadmill-based stress testing generated 27.18% of 2025 revenues, whereas wearable and patch-based CPET systems are projected to rise at 9.88% CAGR.

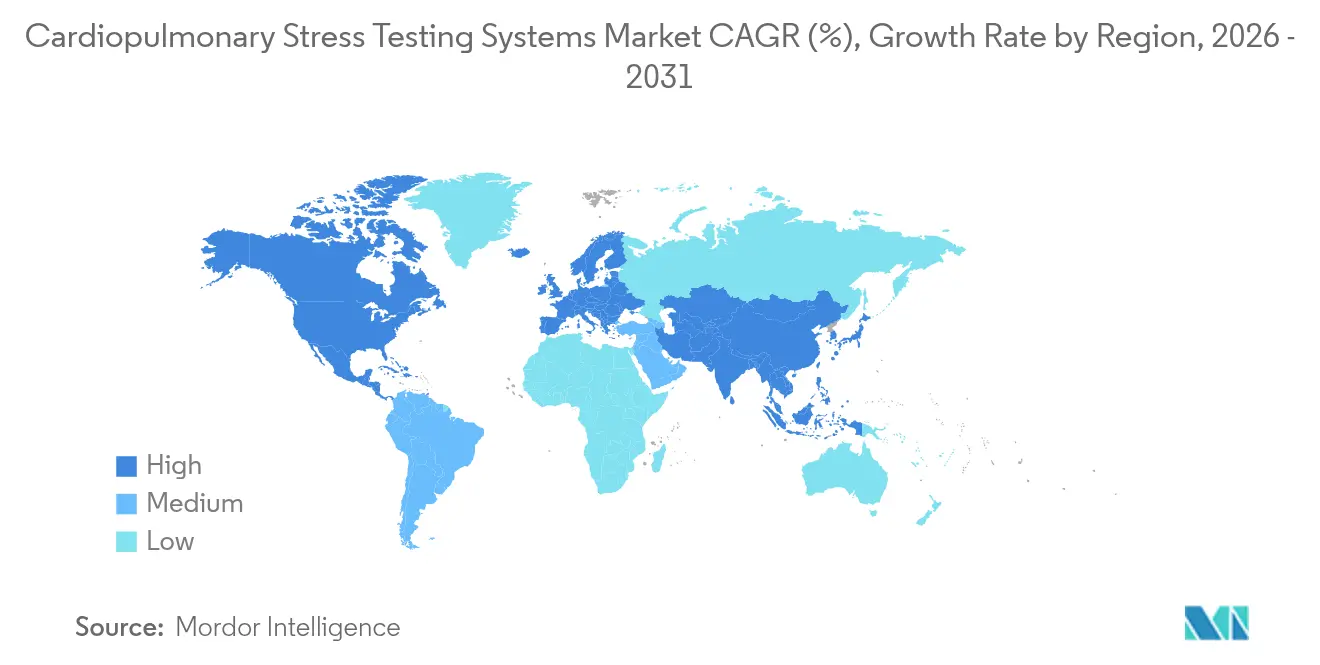

- By geography, North America led with 28.74% revenue in 2025; Asia Pacific is advancing at an 8.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiopulmonary Stress Testing Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in global healthcare expenditure | +1.20% | North America, Europe, selected emerging economies | Medium term (2-4 years) |

| Rising prevalence of cardiopulmonary disorders | +1.00% | Asia Pacific, North America | Long term (≥4 years) |

| Technological advances in stress-ECG & carts | +0.80% | North America, Europe, expanding Asia Pacific | Short term (≤2 years) |

| Favorable reimbursement for diagnostic tests | +0.70% | North America, Europe | Medium term (2-4 years) |

| AI-enabled real-time VO₂ analytics adoption | +0.60% | Global, led by North America | Short term (≤2 years) |

| Home-based rehab using portable CPET | +0.50% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Global Healthcare Expenditure

Expanding health budgets are shifting hospital decisions away from cost-containment toward value-based procurement of advanced CPET systems that package metabolic carts, stress ECG, and cloud analytics into one console.[1]World Bank, “Hospital Systems Efficiency 2024 Report,” worldbank.org Medicare’s 2024 upgrade to cardiac rehabilitation billing further raises the economic case to deploy such platforms, giving providers long-run revenue certainty. Emerging economies replicate this approach as multi-clinic groups co-finance shared CPET suites to widen access. Lower amortized unit cost plus higher throughput help facilities justify the replacement of legacy ergometers with AI-ready devices.

Rising Prevalence of Cardiopulmonary Disorders

Around 48.6% of US adults lived with cardiovascular disease, while fewer than 24.2% met activity guidelines, pushing hospitals to adopt physiologically rich testing to separate cardiac from pulmonary sources of exercise intolerance.[2]American Heart Association, “2024 Heart Disease and Stroke Statistics Update,” heart.orgIntegrating CPET with invasive hemodynamic monitoring allows earlier detection of exercise pulmonary hypertension, which in turn guides targeted therapy. Aging populations and multimorbidity reinforce the need for comprehensive load-response insight that plain stress ECG misses.

Technological Advances in Stress-ECG & Metabolic Carts

Algorithms now classify limitation patterns at pulmonology-grade accuracy using decision-tree and random-forest models fed by breath-by-breath data. MGC Diagnostics’ Ascent software, FDA-cleared in October 2024, merges pulmonary function and CPET into a single interface that automates report drafting. AI-driven quality-control alerts during testing cut rescans, lifting lab throughput and enhancing patient safety.

Favorable Reimbursement Policies for Diagnostic Testing

Updated Medicare coverage decisions define clear medical-necessity rules for CPET during dyspnea work-ups or pre-operative assessment.[3]Centers for Medicare & Medicaid Services, “Cardiac Rehabilitation Programs: Final Rule 2024,” cms.gov Parallel policy moves in commercial insurance reduce prior-authorization delays. Remote monitoring codes now pay for telerehabilitation sessions tied to validated CPET results, expanding patient pools that can be served without new brick-and-mortar capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Multi-Region Device Approval Pathways | -0.40% | Global, most restrictive in Europe & North America | Long term (≥ 4 years) |

| High Capital & Lifecycle Costs Of Integrated CPET Labs | -0.30% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Shortage Of Trained CPET Technologists | -0.50% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Wearable Multiparametric Diagnostics Diverting Demand | -0.20% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Device Approval Pathways

The European Medical Device Regulation demands extensive bench data even for incremental upgrades. At the same time, US post-market surveillance can trigger costly recalls, as seen with Vyaire’s Twin Tube incident in April 2024. Divergent cybersecurity requirements further extend timelines for AI-enabled systems, often forcing smaller firms to stage launches region by region.

High Capital & Lifecycle Costs of Integrated CPET Labs

Full CPET suites bundle high-flow analyzers, calibrated treadmills, spirometry stations and network servers, creating an upfront burden that can top USD 0.5 million for a tertiary-care lab. Continuous calibration gases, filter replacements and analyst retraining add recurring overhead, discouraging adoption in facilities that lack a cardiology volume base to amortize costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: CPET Systems Lead Innovation Wave

Cardiopulmonary exercise-testing systems generated 25.47% of 2025 revenue, and this category is pacing the field with 10.74% CAGR. The cardiopulmonary stress testing systems market size linked to these systems will expand as integrated gas analyzers and stress ECG modules converge into touchscreen carts that auto-score data. Metabolic carts now self-calibrate in 90 seconds, reducing downtime. Meanwhile, stress blood-pressure monitors and entry-level ECG ergometers retain demand in clinics where budgets cannot yet stretch to full platforms.

Algorithm-based interpretation cements this leadership: random-forest classifiers find mechanical-ventilatory bottlenecks that trainees might overlook, and automated ventilatory-threshold detection supports precise exercise prescriptions. Providers therefore prefer single-vendor bundles that cover cardiopulmonary stress testing systems market compliance and remote-monitoring extensions in one purchase.

By End User: Sports Labs Drive Market Evolution

Hospitals controlled 28.02% expenditure in 2025, yet sports-performance and research labs headline growth at 9.82% CAGR, reflecting rising elite-fitness budgets and university studies. The cardiopulmonary stress testing systems market benefits from pro-team demand for daily readiness scoring, and cycle-ergometer protocols fine-tuned to altitude camps. Rehabilitation centers follow suit, folding CPET into post-operative care plans reimbursed under newly expanded cardiac-rehab codes.

Unlike hospital procurement, sports facilities favor portability and rapid setup. Vendors are responding with backpack analyzers weighing under 400 g, Bluetooth-linked to tablets that parse breath-by-breath data through cloud AI, keeping the cardiopulmonary stress testing systems market aligned with field-based applications while still compliant with clinical standards.

By Application: Disease Diagnostics Face Performance Assessment Challenge

Disease diagnostics retained 25.06% in 2025 and remains the anchor use case, yet sports and human-performance assessment is rising at 9.05% CAGR. Cardiac surgeons rely on pre-operative CPET when frailty assessment informs risk conversations. In ICUs, weaning protocols now reference exercise capacity recorded before admission.

Conversely, collegiate athletics and corporate wellness programs adopt CPET to benchmark training efficacy, spurring vendors to add gamified dashboards. This interplay widens the cardiopulmonary stress testing systems market as single platforms serve both pathological detection and peak-performance mapping, eliminating duplicate capital outlays.

By Technology: Wearables Challenge Traditional Testing

Treadmill-based stress testing brought in 27.18% of revenue last year, but wearable and patch-based CPET devices show 9.88% CAGR, signaling decentralization. Pressure-sensing insoles, cuffless BP patches, and micro-ultrasound vests feed AI servers that compute equivalent VO₂ kinetics in real time. The cardiopulmonary stress testing systems market size for wearables will thus climb quickly as hospitals prescribe home-monitoring kits to post-MI patients who cannot attend in-person sessions.

Tilt-table robotics retains a niche for syncope evaluation, and pharmacologic stress labs serve immobile patients, yet continuous ambulatory data increasingly supplement snapshots collected in those venues. This hybrid landscape cements the cardiopulmonary stress testing systems market position as a cross-setting solution rather than a purely lab-based modality.

Geography Analysis

North America generated 28.74% of 2025 revenue. Adoption is buoyed by CMS rules that reimburse CPET for unexplained dyspnea, plus academic trials that bundle CPET endpoints into cardiovascular drug studies. GE Healthcare’s March 2025 release of Revolution Vibe CT illustrates the region’s appetite for AI-rich cardiology diagnostics that integrate seamlessly with CPET-derived risk scores. Canadian health networks invest in mobile units serving rural communities, broadening access while preserving provincial cost controls.

Asia Pacific is the fastest mover at 8.23% CAGR, propelled by chronic disease growth and hospital build-outs. China’s provincial tenders now stipulate VO₂max capability in county cardiac centers, while Japanese teaching hospitals employ CPET in oncology rehab pathways. India’s tier-two cities add dual-use CPET labs serving both clinical referrals and sports academies, further lifting cardiopulmonary stress testing systems market penetration.

Europe maintains robust demand, helped by harmonised clinical guidelines that embed CPET into surgical clearance algorithms. Germany’s DiGA fast-track process incentivises vendors to pair CPET outputs with digital-therapeutic coaching apps, giving patients integrated post-test pathways. The UK National Health Service funds CPET slots in cardiac-rehab settings, citing reductions in unplanned readmissions. Southern Europe relies on EU structural funds to refresh metabolic-cart inventories, ensuring parity with northern centers.

Regulatory Landscape

Cardiopulmonary stress testing systems and associated modules are regulated as medical devices when intended for diagnosis or clinical decision support, which anchors market entry to conformity assessment and post-market controls. In the United States, many systems and software components route through FDA Class II frameworks and the 510(k) pathway, and Prolaio, Inc. received FDA 510(k) clearance in December 2025 for the prolaio eVO2peak Module as an Adjunctive Cardiovascular Status Indicator under 21 CFR 870.2200.

Across major markets, compliance is closely tied to medical electrical equipment and software standards commonly referenced in dossiers and audits, including IEC 60601-1 (safety and essential performance), IEC 60601-1-2 (EMC), ISO 14971 (risk management), and IEC 62304 (software life cycle processes). In Europe, the Medical Device Regulation (MDR) governs CE marking for diagnostic-intent cardiopulmonary stress testing systems, while products positioned purely for sports or fitness without medical claims can fall outside MDR medical device requirements. This distinction influences how vendors label, validate, and commercialize similar hardware across clinical and performance settings.

Competitive Landscape

The cardiopulmonary stress testing systems market remains moderately fragmented. Top multinationals such as GE Healthcare, Philips and MGC Diagnostics deepen moats by embedding AI that simplifies interpretation workflows. GE’s purchase of the remaining stake in Nihon Medi-Physics in December 2024 broadened its reach in radiopharmaceutical-enabled cardiac imaging, a complement to CPET. Philips invests in ultrasound-based cardiac hemodynamics that can cross-link with VO₂ data streams to create unified cardiovascular dashboards.

Wearable-first entrants are tightening the race. Nanowear secured FDA clearance for its cuffless BP monitor that captures 85 biomarkers, offering a cheaper on-body surrogate to in-lab gas analysis for trend tracking. Start-ups leverage subscription software models, contrasting with capital-sale paradigms of incumbent cart manufacturers. Hospitals weigh these options against cybersecurity risk and integration complexity.

Strategic collaborations proliferate: GE Healthcare aligns with imaging-software houses to deliver non-invasive coronary flow ratios that dovetail with CPET stress protocols, while sports-tech brands partner with university labs for validation studies, thereby entering the clinical reimbursement chain. Patent portfolios around breath-sensor membranes and AI algorithms remain key differentiators that could trigger future consolidation.

Cardiopulmonary Stress Testing Systems Industry Leaders

MGC Diagnostics Corporation

General Electric Company

Koninklijke Philips N V

COSMED Srl

Nihon Kohden Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is clinical-grade validation and interoperability that reduces variability between lab carts and emerging wearable measurements, which supports wider use of CPET outputs across rehabilitation, dyspnea work-ups, and performance programs without duplicative testing. This direction is visible in May 2026 clinical research activity, when Calibre Biometrics initiated a study (NCT07596108) comparing agreement between its wearable sensor and the FDA-cleared COSMED Quark CPET metabolic cart, pointing to demand for quantified comparability between on-body monitoring and established carts.

Software-led differentiation is also expanding as labs and hospitals seek faster, more standardized interpretation of breath-by-breath data, especially for ventilatory and gas-exchange thresholds that have historically depended on expert manual review. AI-assisted analytics that automate threshold identification, paired with adherence to ATS/ERS-driven quality and calibration practices used with systems such as MGC Diagnostics Ultima CPX and Geratherm Respiratory BLUE CHERRY, creates an opportunity for vendors to bundle validated algorithms, quality-control tooling, and training workflows into upgrades. These upgrades fit smaller-footprint, in-office CPET setups and more specialized pathways such as invasive CPET for complex exercise intolerance.

Recent Industry Developments

- March 2026: Philips received FDA 510(k) clearance for EchoNavigator R5.0 with DeviceGuide, adding AI-enabled, real-time guidance for complex minimally invasive heart valve repair procedures. The clearance strengthens Philips positioning in AI-driven cardiology software workflows that can be integrated with broader diagnostic pathways, where stress testing and hemodynamic assessment increasingly intersect.

- July 2025: Philips launched an ECG AI marketplace to expand access to AI applications aimed at earlier cardiac diagnosis. The initiative supports a platform strategy that can accelerate third-party algorithm adoption inside hospital cardiology ecosystems, which raises expectations for stress testing vendors to offer interoperable analytics and streamlined integrations.

- October 2024: MGC Diagnostics obtained FDA 510(k) clearance for Ascent software that unifies pulmonary function testing and cardiopulmonary exercise testing into a single interface. Consolidating workflows and automating reporting reduces operational friction in CPET labs, reinforcing software upgrades as a lever for throughput and standardization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers cardiopulmonary stress testing systems used during graded exercise to measure respiratory gas exchange alongside heart and circulatory signals, and then convert these readings into clinical or performance interpretation outputs through integrated hardware and software.

Scope exclusions: Stand-alone cardiac imaging devices, home-use pulse oximeters, and single-use disposables are excluded from this sizing.

Segmentation Overview

- By Product Type

- Stress Blood-Pressure Monitors

- Stress ECG Systems

- Exercise Testing Systems

- Cardiopulmonary Exercise-Testing (CPET) Systems

- Metabolic Carts & Gas-Analysis Modules

- By End User

- Hospitals

- Specialty & Cardiology Clinics

- Ambulatory Surgical & Day-Care Centers

- Rehabilitation Centers

- Sports-Performance & Research Labs

- By Application

- Disease Diagnostics

- Pre-operative Risk Evaluation

- Cardiac & Pulmonary Rehabilitation

- Sports & Human-Performance Assessment

- Critical-Care & ICU Monitoring

- By Technology

- Treadmill-based Stress Testing

- Cycle-Ergometer-based Testing

- Robotics-Assisted Tilt-Table (RATT)

- Wearable / Patch-based CPET

- Pharmacologic Stress Testing Platforms

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for cardiopulmonary evaluation and stress testing, then mapping where cardiopulmonary testing systems are typically bought across care settings. We rely on public sources such as the World Health Organization, the US CDC, the US FDA device databases, OECD health statistics, and selected peer reviewed clinical guidelines and journals that describe CPET usage and protocols.

To translate this context into sizing inputs, we also scan manufacturer product pages, user manuals, and regulatory clearances to confirm what is included in an integrated system versus an adjacent device. Company annual reports, investor presentations, and reputable press coverage are used to understand revenue exposure, regional focus, and product launch timing. In parallel, we use paid subscriptions for company financials and intelligence, plus patent databases where it helps confirm technology shifts and replacement cycles. These examples are not exhaustive, and many other public sources were used for data collection, validation, and clarification during the analysis.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions that are hard to observe in public data, such as typical selling prices by configuration, buyer replacement timing, and the share of demand coming from hospitals versus rehabilitation and sports performance labs. We speak with a mix of device-side roles, clinical users, and channel participants across APAC, EMEA, and the Americas, so country-level reimbursement patterns and procurement practices do not skew the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 17% | Managers: 44% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down model where procedure and patient-pool signals are converted into an addressable installed base, which is then translated into annual system demand through replacement and new-site additions. The totals are corroborated with selective bottom-up approximations such as sampled average selling price ranges by system type, channel checks on typical deal bundles, and a sanity roll-up of supplier revenue exposure where disclosures allow.

Key inputs for this market include CPET and exercise stress testing adoption in cardiology and pulmonology pathways, hospital and rehab facility counts, installed base refresh cycles for carts and gas analyzers, typical treadmill or cycle integration rates, and regional reimbursement and procurement timing. When a variable is not consistently available by country, we use a transparent proxy, for example healthcare infrastructure indicators and specialist density to scale demand, then refine using interview feedback.

For forecasting, we run scenario analysis around adoption and replacement pace, supported by trend-fitting on more stable series such as healthcare spend, chronic respiratory and cardiovascular burden, and facility expansion. If input signals disagree, the model is adjusted only after re-checking the underlying definition and confirming the direction with expert feedback.

Data Validation & Update Cycle

Outputs are checked against independent signals such as expected device replacement volume implied by the installed base, regional procurement seasonality, and the pace of new cardiopulmonary lab setup. We also run variance checks across regions and end users so that one high-growth assumption does not unintentionally inflate the total market.

Before sign-off, the model goes through multi-step analyst review, and outliers trigger a re-check of inputs and, when needed, a short re-contact with interviewees to confirm whether the shift is real or a data artifact. The report is refreshed annually, with interim updates added when material events occur, such as a major regulatory change or a notable pricing shift. Right before delivery, we do a fresh pass on key assumptions so clients receive the latest updated view.

Mordor Intelligence's Cardiopulmonary Stress Testing Systems Market Size Measured Against Other Published Estimates

Published market values for cardiopulmonary exercise and stress testing often differ because the category can be defined narrowly as integrated testing systems or broadly as a basket that includes adjacent monitoring and imaging tools. Differences also come from which year is treated as the starting point, which care settings are counted, and how pricing and replacement cycles are assumed.

The table shows a clear spread mainly because some publishers fold in products like echocardiograms, SPECT, and basic monitors, which increases the total even if core CPET cart demand is unchanged. Mordor Intelligence's value is limited to integrated cardiopulmonary stress testing systems (such as CPET carts with treadmill or cycle platforms, stress ECG recorders, gas-analysis modules, and interpretation software), and it excludes stand-alone imaging, home-use oximeters, and single-use disposables, which keeps the demand pool closer to actual system purchases.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.06 B (2026) | |

| Global Consultancy A | USD 3.96 B (2025) | Uses a broader cardiopulmonary exercise testing framing where product coverage includes echocardiograms, SPECT, pulse oximeters, and stress blood pressure monitors, which shifts spend into adjacent device categories and changes the comparability with integrated system-only totals. |

| Industry Research Desk B | USD 3.82 B (2024) | Counts multiple monitoring and diagnostic tools within the same bucket and anchors the sizing to an earlier year, so the value reflects a wider diagnostic equipment pool rather than purchases tied specifically to bundled CPET system configurations. |

Looking across the three figures, scope choices drive most of the gap, and timing and pricing assumptions add a second layer of difference. By keeping inputs traceable to system purchase behavior, replacement cadence, and configuration-level pricing checks, our estimate stays practical to replicate and easier to defend in planning discussions.

Key Questions Answered in the Report

What is the current size of the cardiopulmonary stress testing systems market?

The cardiopulmonary stress testing systems market is valued at USD 6.06 billion in 2026.

How fast is the cardiopulmonary stress testing systems market expected to grow?

The market is projected to expand at a 4.44% CAGR, reaching USD 7.53 billion by 2031.

Which product segment is growing the quickest within the cardiopulmonary stress testing systems market?

Cardiopulmonary exercise-testing systems lead growth at an 10.74% CAGR through 2031.

What geographic region shows the highest growth rate for cardiopulmonary stress testing systems solutions?

Asia Pacific posts the fastest regional expansion with an 8.23% CAGR between 2026 and 2031.

Page last updated on: