Capacitive Ceramic Pressure Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

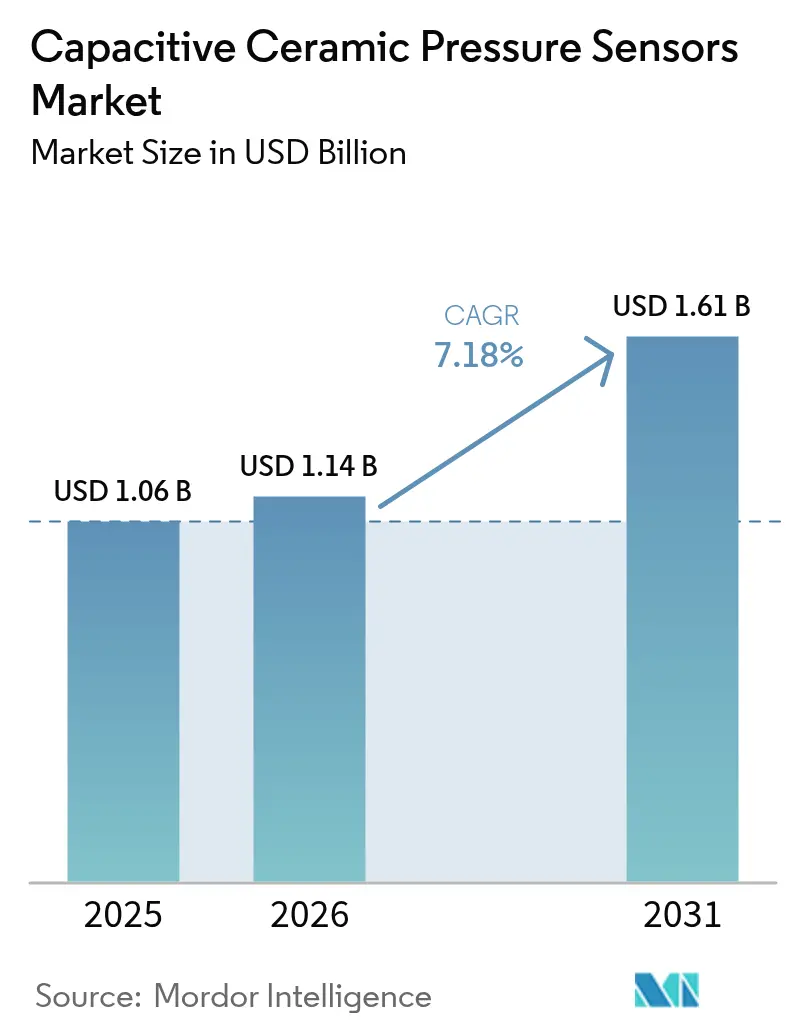

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

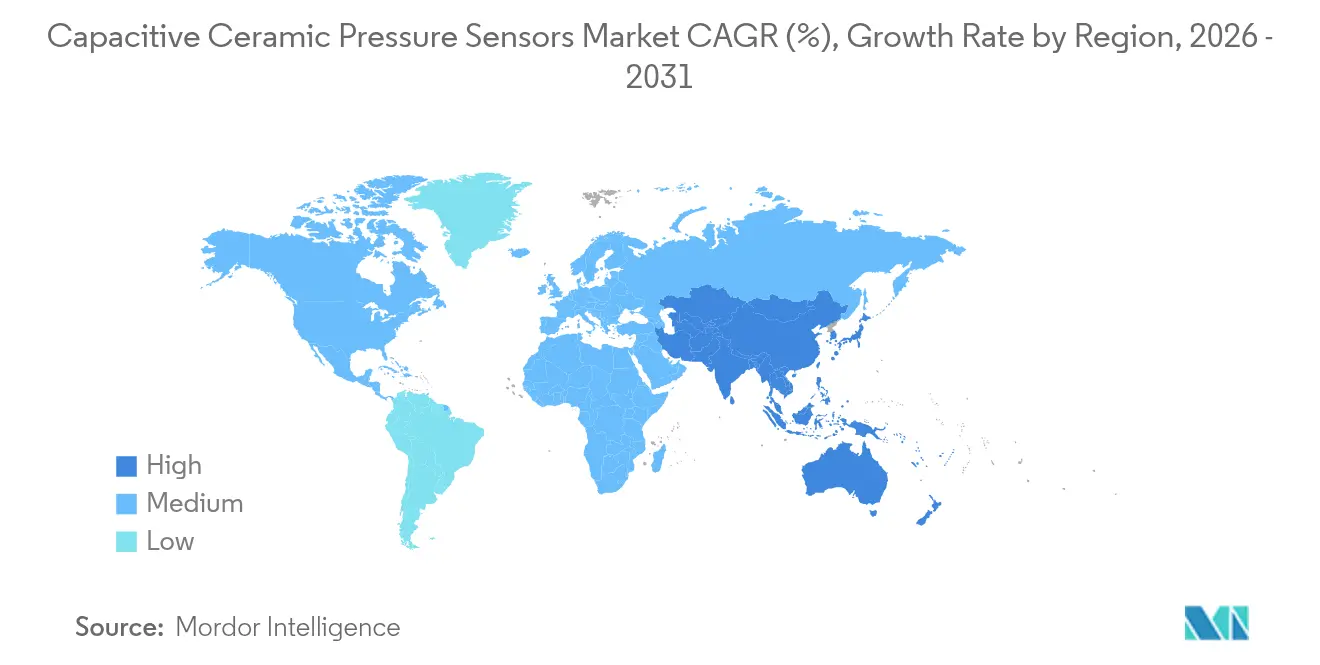

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

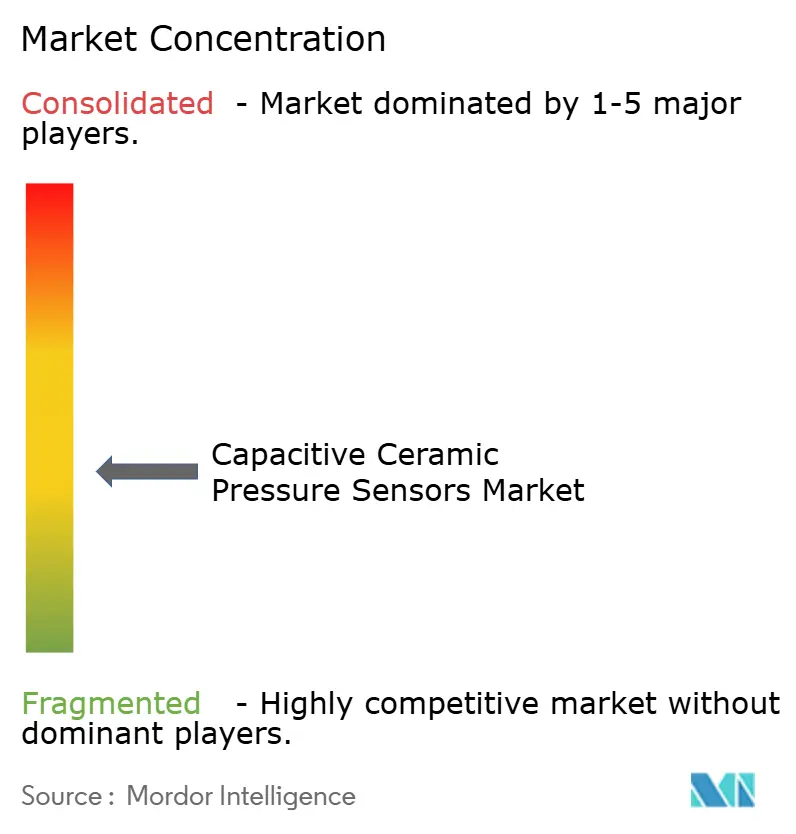

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Capacitive Ceramic Pressure Sensors Market Analysis by Mordor Intelligence

The capacitive ceramic pressure sensors market size is expected to grow from USD 1.06 billion in 2025 to USD 1.14 billion in 2026 and is forecast to reach USD 1.61 billion by 2031 at 7.18% CAGR over 2026-2031. Growth stems from regulatory mandates for tire pressure monitoring systems, post-pandemic expansion in critical medical equipment, and Industry 4.0 upgrades that favor sensors able to withstand heat, vibration, and corrosive media. Automotive electrification adds further momentum as high-voltage battery packs require pressure feedback immune to electromagnetic interference. Healthcare equipment suppliers continue shifting toward ceramic diaphragms to meet long-duration accuracy and biocompatibility standards. Process industries deploy ceramic devices in wireless networks where low drift reduces recalibration cycles, while early green-hydrogen projects specify them for electrolyzer safety.

Key Report Takeaways

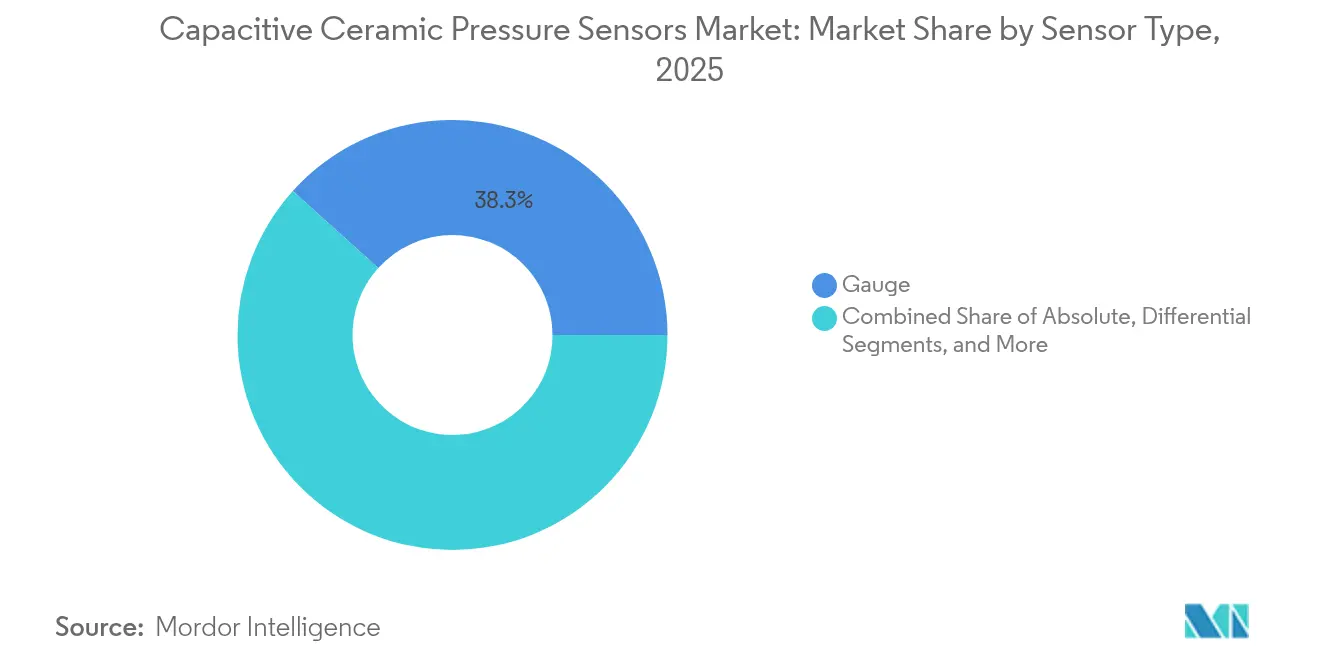

- By sensor type, gauge variants delivered 38.32% revenue share of the capacitive ceramic pressure sensors market in 2025; differential sensors record the fastest CAGR at 7.96% through 2031.

- By application, automotive and transportation held 41.25% of capacitive ceramic pressure sensors market share in 2025, whereas medical and healthcare is advancing at an 8.06% CAGR through 2031.

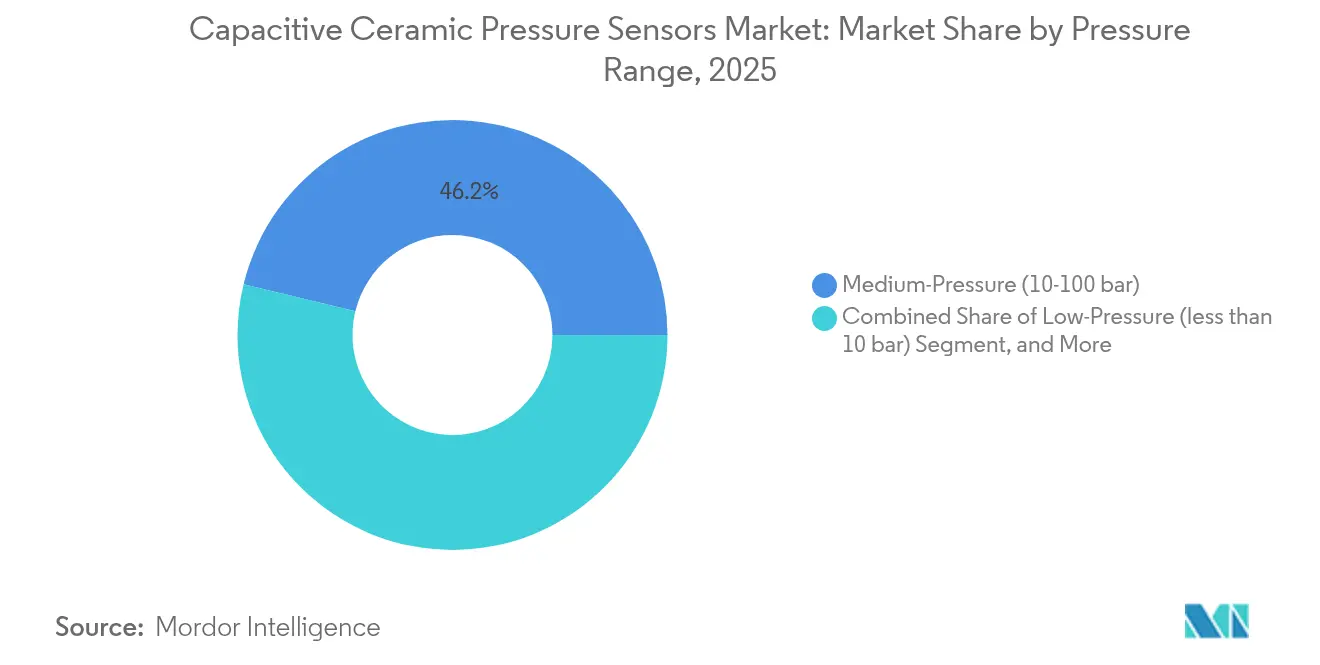

- By pressure range, medium-pressure devices accounted for 46.20% of the capacitive ceramic pressure sensors market size in 2025, while low-pressure models are projected to grow at an 8.24% CAGR between 2026-2031.

- By end-use industry, automotive OEMs accounted for 35.25% of the capacitive ceramic pressure sensors market size in 2025, while medical device manufacturers are projected to grow at an 7.71% CAGR between 2026-2031.

- By geography, North America captured 38.40% of the capacitive ceramic pressure sensors market size in 2025, whereas Asia-Pacific leads growth at an 7.97% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Capacitive Ceramic Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates for TPMS and engine management in next-gen vehicles | +1.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Industry 4.0 retrofits demanding rugged, corrosion-resistant sensors | +1.2% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Post-pandemic boom in ventilators and infusion pumps | +1.5% | Global, concentrated in established medical device hubs | Short term (≤ 2 years) |

| Ceramic sensors' high-temperature and chemical-resistance edge | +0.9% | Global, particularly in harsh industrial environments | Long term (≥ 4 years) |

| Electro-lyzer pressure monitoring for green-hydrogen plants | +0.7% | EU, APAC, with emerging presence in North America | Medium term (2-4 years) |

| Chiplet-based sensor-fusion modules for EV battery packs | +0.6% | APAC manufacturing centers, global deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates for TPMS drive automotive integration

Safety rules such as FMVSS 138 in the United States and ECE R64 in Europe require tire pressure monitoring in every new passenger vehicle, locking in stable demand for robust sensing solutions. Ceramic capacitive elements preserve calibration from -40 °C to +125 °C, whereas silicon MEMS variants drift above +85 °C. Electric-vehicle makers additionally install ceramic units in sealed battery enclosures to monitor pack pressure during rapid charging events that create thermal spikes. The move toward 800 V powertrains elevates electromagnetic interference, yet ceramic devices exhibit lower intrinsic noise than semiconductor alternatives, helping automakers protect data integrity. In 2024, automotive OEMs accounted for 35.83% of global offtake, underscoring the segment’s volume influence.

Industry 4.0 retrofits accelerate industrial sensor adoption

Factories modernizing under Industry 4.0 connect established controllers with digital feedback loops and predictive-maintenance software. Ceramic capacitive sensors ship with 4-20 mA and IO-Link outputs, enabling rapid plant-wide installation without rewiring legacy input cards. Corrosion-proof diaphragms minimize unplanned downtime caused by caustic cleaners or acidic process media. As analytics platforms rank sensor stability above lowest piece-price, ceramic units benefit from life-cycle savings that outweigh higher purchase cost. Wireless gateways exploit their low leakage current to extend battery life in remote assets. Industrial OEMs now form the second-largest buyer cohort, particularly in chemical and pulp-and-paper lines operating up to 500 °C.

Post-pandemic medical device expansion boosts precision requirements

Ventilator shipments surged in 2024-2025, cementing ceramic capacitive devices as the reference technology for airway pressure loops where sub-1 % total error band is mandatory. FDA 21 CFR 820 and ISO 13485 emphasize long-term drift below 0.25% full scale, specifications regularly met by alumina-based diaphragms. Biocompatibility and protein-fouling resistance favor ceramics in hemodialysis pumps and infusion controllers. Market growth extends into home-health respiratory aids, where portable units rely on ceramic stability to cut service calls. Medical and healthcare revenue is tracking an 8.34% CAGR to 2030, the fastest among all end-use categories.

Ceramic sensors’ high-temperature and chemical-resistance edge

Many refineries, smelters, and food-sterilization autoclaves expose instrumentation to 400 °C gas streams, acid steams, and abrasive slurries. Alumina diaphragms retain Young’s modulus and dielectric constant across this span, allowing linear output without complex compensation circuitry. Chemical inertness avoids chlorine-induced pinholes that plague metallic or polymer diaphragms. Semiconductor MEMS chips, by contrast, require exotic passivation layers that add cost and still degrade under cyclic heat. As asset managers prioritize uptime, total cost of ownership tilts toward ceramic platforms even if initial list price runs 3-4 times higher than MEMS. This resilience edge contributes roughly 0.9 percentage points to forecast CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-competition from piezoresistive MEMS alternatives | -1.4% | Global, particularly in cost-sensitive applications | Short term (≤ 2 years) |

| High tooling and calibration cost of ceramic capacitive lines | -0.8% | Manufacturing centers in APAC and Europe | Medium term (2-4 years) |

| Supply-risk of high-purity alumina feedstock | -0.6% | Global supply chain, concentrated risk in APAC | Long term (≥ 4 years) |

| EMI issues in 800-V EV platforms | -0.5% | EV manufacturing regions, primarily APAC and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost competition from silicon MEMS alternatives pressures pricing

High-volume MEMS fabs ship basic piezoresistive sensors below USD 5, whereas ceramic capacitive units often list between USD 15-50 depending on range and certification tier.[1]Keysight Technologies, “Lowering the Cost of MEMS Pressure Sensor Production,” keysight.com Consumer IoT buyers frequently accept tighter temperature deratings to hit aggressive bill-of-materials targets. While ceramics hold favor in harsh settings, downward price pressure forces makers to streamline LTCC firing cycles and automate final calibration. Some vendors now co-package thin-film signal conditioners to eliminate external electronics and trim module cost.

High ceramic manufacturing costs limit market penetration

Low-temperature co-fired ceramic stacks demand furnace dwell times above 850 °C, specialized molybdenum metallization, and precision lapping equipment. A new gauge-pressure production line can exceed USD 0.5 million in capital outlay, a hurdle that discourages new entrants. Multi-point temperature calibration also remains labor-intensive because dielectric constants vary batch-to-batch. Although scale economies help majors dilute fixed costs over millions of parts, smaller firms struggle to match the price curves set by integrated MEMS producers. Until automated optical test platforms mature, this restraint could shave 0.8 percentage points off long-term CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Gauge Sensors Anchor Automotive Demand

Gauge devices accounted for 38.32% of the capacitive ceramic pressure sensors market in 2025, reflecting wide deployment in tire pressure monitoring, brake hydraulics, and industrial compressors. The capacitive ceramic pressure sensors market size for gauge designs stood at USD 0.41 billion the same year and is projected to expand steadily as electric-vehicle makers integrate in-wheel pressure nodes. Automotive compliance cycles drive steady, high-volume bids, enabling suppliers to amortize their tooling investments. In parallel, the rollout of smart meters by water utilities is creating incremental demand for gauges, as submerged installations favor ceramic corrosion immunity.

Differential variants are projected to advance at an 7.96% CAGR through 2031, driven by HVAC filter monitoring and fuel-cell stack management. These devices exploit the inherent linearity of capacitive plates to resolve sub-20 Pa pressure drops, a key metric in medical ventilators. Absolute and sealed sensors together occupy a modest niche but gain relevance in altitude drones and deep-well pumping. Across the broader capacitive ceramic pressure sensor market, technology vendors are increasingly bundling digital ASICs inside stainless housings to simplify installation.

By Application: Automotive Holds Scale while Medical Leads Growth

Automotive and transportation dominated revenue with 41.25% share in 2025, underpinned by statutory TPMS inclusion and emerging battery-pack pressure loops. Vehicle architectures adopting 800 V inverters generate electromagnetic fields that ceramic sensors tolerate without signal distortion, protecting traction-control algorithms. Rail operators also specify ceramic diaphragms for brake-line safety in alpine routes where -40 °C ambient is routine.

Medical and healthcare spending accelerates fastest at an 8.06% CAGR to 2031, fueled by intensive-care ventilators, infusion pumps, and dialysis circuits that demand zero drift over thousands of sterilization cycles. The capacitive ceramic pressure sensors market size for medical equipment is predicted to reach USD 0.32 billion by 2031, translating into meaningful supply contracts for firms holding ISO 13485 lines. Long-term home respiratory therapy and remote monitoring further widen the revenue funnel as aging populations seek outpatient options.

Industrial automation remains a resilient third pillar. Plants handling sulfuric acid, ammonia, or hydrogen sulfide migrate to ceramic inserts because polymer MEMS coatings blister under chemical attack. Consumer wearables adopt miniature ceramic chips for barometric altitude, though volumes remain modest versus automotive.

By Pressure Range: Medium-Pressure Tier Leads, Low-Pressure Surges

Sensors rated 10-100 bar secured 46.20% of capacitive ceramic pressure sensors market share in 2025 as they align with brake systems, hydraulic jacks, and general industrial pneumatics. In this bracket, ceramics outperform metal-foil gauges at extreme ambient swings, cutting warranty claims for heavy-duty trucks.

Low-pressure devices below 10 bar are progressing at an 8.24% CAGR, amplified by smart-building diff-pressure loops and IoT weather stations. Here, ceramic capacitors achieve resolutions better than 0.01% full scale, enabling precise airflow balancing in cleanrooms. High-pressure models up to 700 bar target hydrogen storage drums for fuel-cell vehicles, green-hydrogen pipeline trials, and oilfield downhole telemetry.

By End-Use Industry: OEM Integration Sets the Pace

Original automotive manufacturers represented 35.25% of total shipments in 2025, and most seek Tier-1 suppliers able to deliver AEC-Q100 qualified sensors with functional-safety documentation. Integrated assembly at the factory line ensures optimal routing and shields against aftermarket fitment errors. The capacitive ceramic pressure sensors industry also serves industrial OEMs building chemical reactors, utility meters, and packaging machines, many of whom embed sensors into proprietary modules.

Medical OEMs constitute the fastest-growing buyer group at a 7.71% CAGR. Their purchasing patterns prioritize supplier audit trails, sterilization evidence, and biocompatibility certificates. Utilities and energy developers embracing hydrogen electrolysis also contract directly with sensor makers for high-pressure variants, while contract electronics manufacturers handle volume board-level integration for smart-home brands.

Geography Analysis

North America held 38.40% of global sales in 2025 and remains the single largest region thanks to early TPMS legislation, entrenched medical-device clusters, and substantial electric-vehicle output. U.S. sensor suppliers leverage DOE grants targeting hydrogen supply chains to pilot 700 bar ceramic assemblies. Canada’s cold-weather truck market values ceramic consistency at -30 °C, supporting domestic Tier-2 fabrication.

Asia-Pacific is the growth engine at 7.97% CAGR. China’s EV leaders such as BYD embed ceramic nodes inside blade-battery modules to monitor gas formation during fast charging. Japan’s robotics integrators specify alumina diaphragms for six-axis arms that sanitize with pressurized steam. South Korea channels public subsidies into green-hydrogen hubs where electrolyzer stacks operate near 30 bar and demand ceramic reliability. Europe sustains a solid share through German automotive giants Bosch and Continental, which co-develop ceramic chips for next-generation driver-assistance platforms. Scandinavia deploys sensors in offshore wind turbine gearboxes exposed to salt spray and oscillating load cycles. Middle East refiners adopt ceramic packages for sulfur recovery units running above 400 °C, while Africa’s mining firms experiment with ceramic telemetry in acid leach pads.

Competitive Landscape

The capacitive ceramic pressure sensors market is moderately fragmented; the five largest vendors hold roughly 50% collective share, leaving ample room for mid-tier specialists. Established multinationals differentiate through broad certification portfolios, vertically integrated LTCC lines, and global application-engineering teams. Niche players compete on custom diaphragm alloys, hermetic feedthroughs, and miniaturized form factors.

Strategic moves center on digital interface upgrades, package ruggedization, and regional production footprints that hedge geopolitical supply risks. Sensata debuted a water-meter sensor with ten-year lithium battery life, targeting utilities facing non-revenue water losses. Bosch Sensortec expanded its gel-filled barometric family for swim-proof wearables, exploiting ceramic resistance to chlorine exposure. Start-ups such as Peratech chase keyboard and haptic markets with quantum-tunneling films that offer capacitive-like performance but lower thickness profiles.

Patent filings increasingly address multilayer sealing rings, autonomous self-calibration algorithms, and EMI-hardened ASIC layouts. Supply-chain conversations focus on alumina purity above 99.7% to limit dielectric loss tangent, with some firms inking long-term offtake contracts to stabilize cost curves. Overall competition balances premium-priced performance against commoditizing volumes in IoT, ensuring sustained innovation.

Capacitive Ceramic Pressure Sensors Industry Leaders

Vega Americas Inc.

Nanjing Jiucheng Technology Co. Limited

Sensata Technologies Holding PLC(Impress Sensors and Kavlico Corporation)

Metallux SA

Angst+Pfister Sensors and Power AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Micro Sensor Co. launched MPM489W NB-IoT wireless transmitter employing oil-filled ceramic cores for petrochemical fields.

- February 2025: STMicroelectronics upgraded ILPS28QSW capacitive MEMS with Qvar channel for leak detection.

- September 2024: Peratech secured USD 31.5 million to scale quantum-tunneling composite force-sensing arrays.

- May 2024: Rechner Electronics Industries added KA1590 capacitive models featuring IO-Link communication for sanitary processes.

Global Capacitive Ceramic Pressure Sensors Market Report Scope

Capacitive pressure sensors measure pressure by detecting changes in electrical capacitance caused by the movement of a diaphragm. The scope of the study is pressure sensors with a capacitive ceramic cell. The distinct advantages of ceramic material allow sensors to offer long-term stability and reliability, with high resistance to pressure. They have vital importance in the industry, owing to their excellent inert nature to corrosion. The higher strength of ceramic sensors in testing environments has resulted in capacitive ceramic pressure sensors witnessing an increasing range of applications across various industries.

| Absolute |

| Gauge |

| Differential |

| Sealed |

| Automotive and Transportation | Marine Systems |

| Electric and Hybrid Vehicles | |

| Industrial | Food and Beverage Processing |

| HVAC and Refrigeration | |

| Energy and Chemical | |

| Industrial Robotics and Factory Automation | |

| Medical and Healthcare | Respiratory and Ventilation Equipment |

| Hemodialysis and Infusion Pumps | |

| Consumer Electronics and IoT | |

| Other Applications (Aerospace, Smart Agriculture) |

| Low-Pressure (less than 10 bar) |

| Medium-Pressure (10-100 bar) |

| High-Pressure (above 100 bar) |

| Automotive OEMs |

| Industrial OEMs |

| Medical Device Manufacturers |

| Process Industries |

| Utilities and Energy |

| ODMs / Contract Manufacturers |

| North America | United States | |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Absolute | ||

| Gauge | |||

| Differential | |||

| Sealed | |||

| By Application | Automotive and Transportation | Marine Systems | |

| Electric and Hybrid Vehicles | |||

| Industrial | Food and Beverage Processing | ||

| HVAC and Refrigeration | |||

| Energy and Chemical | |||

| Industrial Robotics and Factory Automation | |||

| Medical and Healthcare | Respiratory and Ventilation Equipment | ||

| Hemodialysis and Infusion Pumps | |||

| Consumer Electronics and IoT | |||

| Other Applications (Aerospace, Smart Agriculture) | |||

| By Pressure Range | Low-Pressure (less than 10 bar) | ||

| Medium-Pressure (10-100 bar) | |||

| High-Pressure (above 100 bar) | |||

| By End-Use Industry | Automotive OEMs | ||

| Industrial OEMs | |||

| Medical Device Manufacturers | |||

| Process Industries | |||

| Utilities and Energy | |||

| ODMs / Contract Manufacturers | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What CAGR is projected for capacitive ceramic pressure sensors between 2026-2031?

The global capacitive ceramic pressure sensors market is forecast to grow at 7.18% during 2026-2031.

Which region is expected to post the fastest revenue growth?

Asia-Pacific leads with an anticipated 7.97% CAGR through 2031 driven by electric-vehicle production and hydrogen investments.

Why are ceramic sensors preferred over silicon MEMS in TPMS?

Ceramic diaphragms retain accuracy from -40 °C to +125 °C and resist electrolyte corrosion, key for long-life tire sensors.

What application segment is growing quickest?

Medical and healthcare devices show the fastest expansion at an 8.06% CAGR due to ventilators and infusion pumps.

Which pressure range currently dominates demand?

Sensors rated 10-100 bar hold the largest share at 46.20% thanks to automotive hydraulics and industrial pneumatics.

Page last updated on: