Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

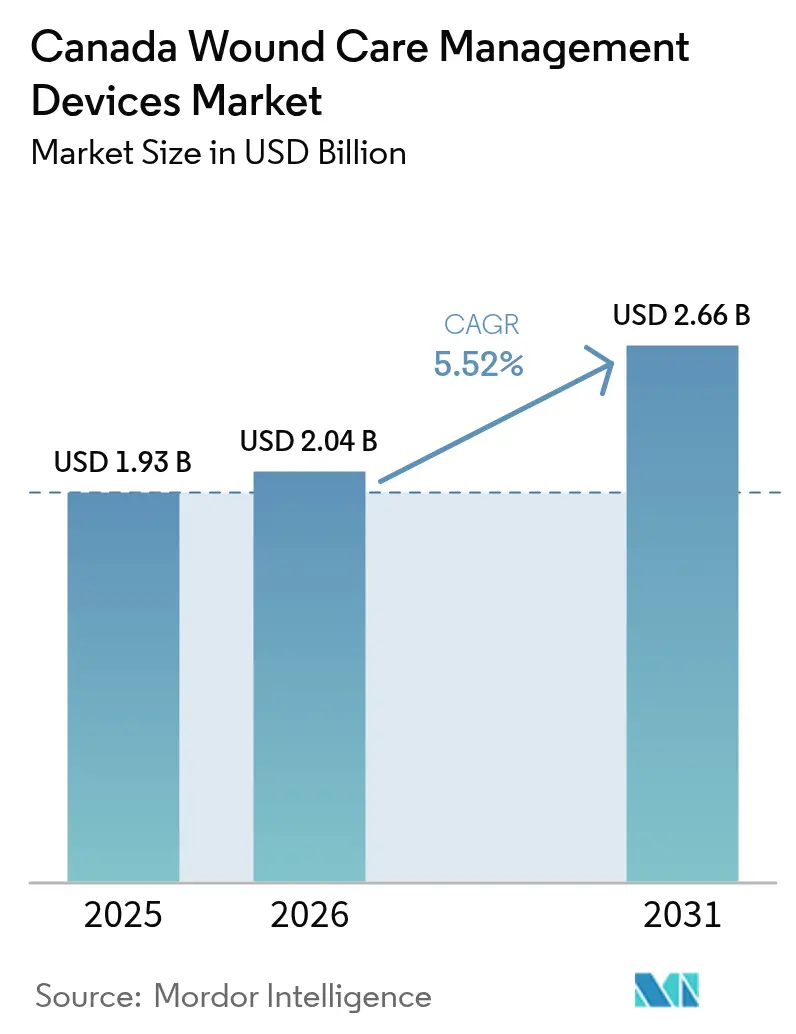

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.04 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

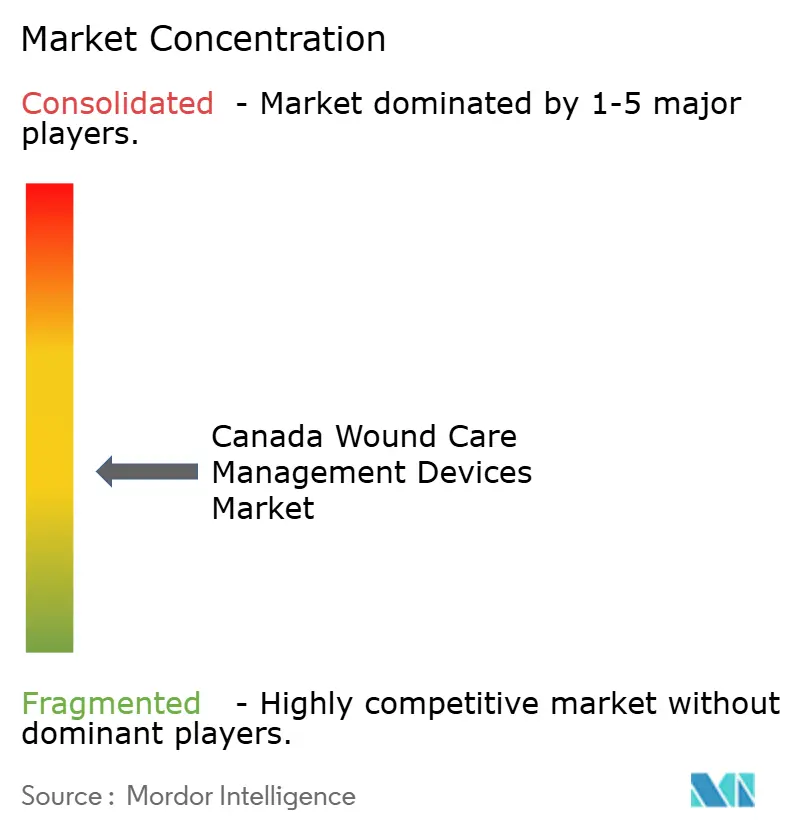

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Wound Care Management Devices Market Analysis by Mordor Intelligence

The Canada wound care management devices market size is expected to grow from USD 1.93 billion in 2025 to USD 2.04 billion in 2026 and is forecast to reach USD 2.66 billion by 2031 at 5.52% CAGR over 2026-2031. Demographic aging, expanding provincial reimbursement, and widespread digitization position the Canada wound care management devices market for steady gains throughout the forecast horizon. Procurement reforms that reward measurable outcomes, combined with strong provincial telehealth investments, are amplifying early demand for negative-pressure systems, advanced antimicrobial dressings, and connected monitoring platforms. Multinational suppliers retain scale advantages, yet product differentiation increasingly rests on ease of use, portability, and clinical-outcome evidence that satisfies diverse provincial formularies. The policy environment remains supportive after Health Canada’s modernization of device licensing, though recent toxic-substance designations for select antiseptics underscore regulatory vigilance and rising compliance costs. Overall, the market’s expansion is propelled by a convergence of reimbursement, technology, and quality-of-care metrics that align clinical efficacy with provincial budget stewardship.

Key Report Takeaways

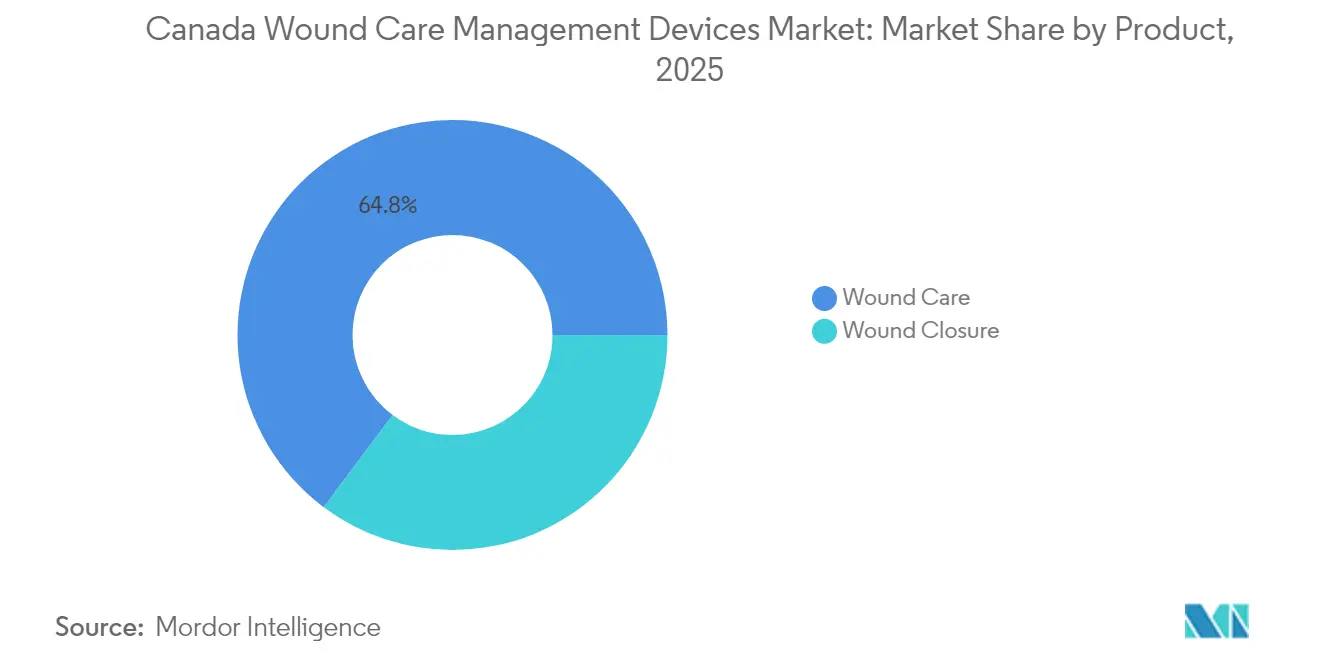

- By product category, wound care held 64.78% of Canada wound care management devices market share in 2025, while wound closure is poised for a 5.74% CAGR through 2031.

- By wound type, chronic wounds commanded 67.95% of share in 2025; acute wounds are predicted to progress at a 6.03% CAGR to 2031.

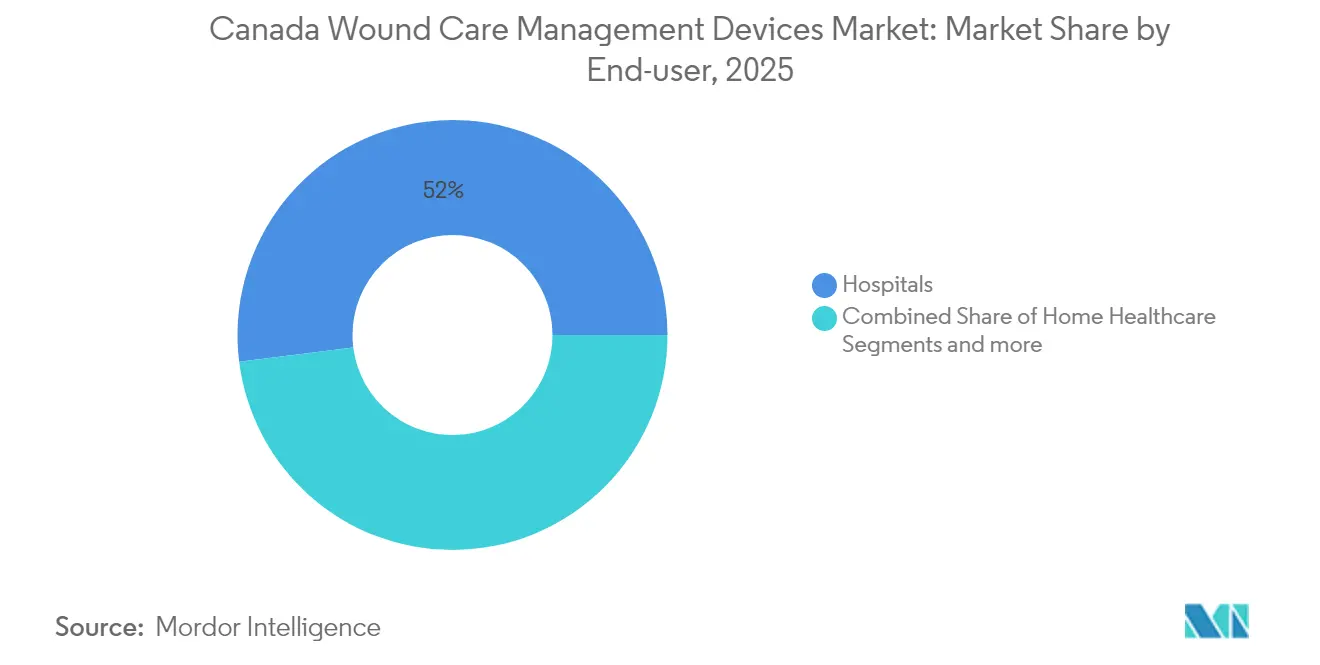

- By end-user, hospitals led with 51.98% of Canada wound care management devices market size in 2025, and home healthcare settings are set to record a 6.27% CAGR to 2031.

- By care setting, in-patient environments accounted for 56.35% of Canada wound care management devices market size in 2025, whereas community and outpatient facilities are expected to expand at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Provincial reimbursement expansion for wound care management devices | +1.2% | National, with early gains in Ontario, British Columbia | Medium term (2-4 years) |

| Availability of tele-wound solutions in the country | +0.8% | National, concentrated in rural and remote areas | Short term (≤ 2 years) |

| National quality indicators driving hospital adoption of advanced dressings | +0.7% | National, hospital-focused implementation | Medium term (2-4 years) |

| Expedited antimicrobial dressing review pathway | +0.5% | National, regulatory framework enhancement | Short term (≤ 2 years) |

| Growth of publicly funded home-care budgets supporting portable therapies | +0.9% | Provincial variations, strongest in Ontario, Quebec | Long term (≥ 4 years) |

| Growing prevalence of chronic and acute wounds | +1.1% | National, demographic-driven | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Provincial Reimbursement Expansion for Wound Care Management Devices

Provincial formulary upgrades are transforming market access by shifting payment criteria from product cost to demonstrable outcomes, and Ontario’s 2024-2025 business plan explicitly channels new funds to advanced dressings delivered through home-care programs. Value-based tenders now require suppliers to present healing-time data, readmission reductions, and health-economic models, giving firms with strong clinical dossiers a clear edge. Negative-pressure wound therapy systems, skin substitutes for diabetic foot ulcers, and silver-impregnated dressings have moved to preferred-status lists in multiple provinces, accelerating purchase cycles. Pharmaceutical cost-containment officers are also leveraging outcome-linked contracts that lower total spend for non-responding patients, a measure that heightens competition on product efficacies. Vendors able to demonstrate population-level impact, especially among Indigenous and remote communities, secure broader inclusion and longer contract terms. The reimbursement trajectory therefore not only drives immediate volume uptake but also shapes R&D priorities toward products with unambiguous clinical-benefit endpoints.

Availability of Tele-wound Solutions in the Country

Telemedicine adoption rose sharply after pandemic-related restrictions, and the TeleWound pilot in Ontario reported 89% patient-satisfaction rates alongside CAD 5,800 annual savings per patient through lower emergency-department visits. Federal grants channelled via the Canada Digital Supercluster extend these pilots to British Columbia and prairie provinces, thereby standardising remote-care protocols. Portable cameras, AI-enabled assessment software, and Health-Canada–cleared peripherals such as TytoHome permit clinicians to classify wound stages, prescribe dressings, and initiate negative-pressure therapy without in-person appointments [1]Canadian Agency for Drugs and Technologies in Health, "Connected Devices to Support Remote Examination and Diagnosis in Primary Care and Specialty Care," cda-amc.ca. These tools directly address access deficits for northern and Indigenous populations where specialist clinics are scarce. Insurers and provincial payers increasingly reimburse virtual follow-ups, accelerating the shift toward hybrid care models that blend hospital expertise with in-home service delivery. For manufacturers, device connectivity and software-integration interfaces now form essential tender requirements and open doors to subscription-based service models. Consequently, tele-wound infrastructure multiplies device utilisation rates, shortens care cycles, and elevates data-rich platforms that feed future AI-driven care pathways.

National Quality Indicators Driving Hospital Adoption of Advanced Dressings

Wounds Canada’s 2025 evidence-based protocols were incorporated into hospital quality dashboards, transforming wound-healing speed, infection rates, and length-of-stay indicators into executive compensation metrics [2]Wounds Canada, "Skin Health and Wound Management: Best Practice Recommendations 2025," woundscanada.ca. Hospitals respond by upgrading to moisture-balancing and antimicrobial dressings that score favourably in these benchmarks, and group purchasing contracts now bundle outcome guarantees. Hypochlorous-acid washes, super-oxidised solution cleansers, and silver-alginate dressings therefore enjoy accelerated adoption curves [3]Wounds Canada, "Pressure Injuries And The Use Of Hypochlorous Acid (pHA)-Based Cleanser: What Is The Science And What Are The Best Ways To Leverage This Technology With Maximal Effect?," woundscanada.ca. Parallel accreditation bodies audit adherence to these indicators, raising reputational stakes for lagging facilities. Suppliers able to deliver both product and education modules for nurses secure after-sales loyalty, as training compliance has become a line-item on quality reviews. Over time, hospital networks share benchmark data, generating a national feedback loop that encourages continuous device innovation. As a result, the quality-indicator movement cements advanced dressing demand while simultaneously filtering offerings down to those with published real-world performance.

Growing Prevalence of Chronic and Acute Wounds

Canada’s diabetic population continues its upward trajectory, and the national direct cost of diabetic foot ulcers is pegged at CAD 547 million each year, making chronic wound management a fiscal imperative. Parallel demographic aging lifts pressure-ulcer incidence in long-term care, keeping occupancy of specialty dressing products high. On the acute side, post-pandemic surgical catch-up programs raise procedure volumes, producing more surgical wounds that must heal quickly to avoid backlog relapse. Provincial trauma reforms, including 24-hour air-ambulance coverage, funnel severely injured patients to tertiary hospitals sooner, increasing the window for advanced closure devices. Meanwhile, Indigenous communities experience elevated lower-limb amputation rates due to diabetes, prompting federal grants for culturally tailored wound-prevention outreach. The dual burden of chronic and acute wounds therefore guarantees multi-year demand across hospital, outpatient, and home-care channels, firmly underpinning volume projections for the Canada wound care management devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nurse shortages in the country limiting device uptake | -0.9% | National, acute in rural areas | Medium term (2-4 years) |

| Uneven bio-skin substitute reimbursement | -0.6% | Provincial variations, inconsistent coverage | Short term (≤ 2 years) |

| High device licensing fees dampening SME innovation | -0.4% | National, regulatory framework constraint | Long term (≥ 4 years) |

| Stringent regulatory requirements | -0.5% | National, Health Canada oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nurse Shortages in the Country Limiting Device Uptake

Canada faced a vacancy rate of 10.6% for registered nurses in 2025, a figure that climbs in remote districts where wound-care specialists are scarce. Negative-pressure systems and bioengineered dressings require advanced application skills, and insufficient staffing slows protocol implementation. Existing personnel must balance higher caseloads, often defaulting to traditional gauze instead of technologically superior options to save time. Provincial immigration and fast-track credential recognition programs offer partial relief but compete with the United States for skilled nurses, limiting immediate gains. Suppliers increasingly provide simplified device formats with intuitive visual guides, reducing training load and enabling uptake by generalist staff. Nonetheless, the workforce constraint remains a material drag on near-term volume growth, especially in home-healthcare channels where nurse availability determines device deployment capacity.

Stringent Regulatory Requirements

Health Canada’s Class II and Class III pathways maintain 75- to 90-day review cycles, and the recent toxicity classification of chlorhexidine signals closer scrutiny of antimicrobial claims. Small and medium-sized enterprises carry disproportionate regulatory-affairs costs, with dossier preparation and mandatory post-market surveillance adding recurring overhead. Although the exceptional-circumstance route introduced during the pandemic expedited a handful of wound-care items, most novel dressings must still pass full pre-market evaluation. Manufacturers must also comply with bilingual labelling rules and Indigenous language considerations in certain provinces, adding complexity. The net effect is a slower innovation cadence, concentrated market shares for established companies, and risk-adjusted pricing that passes regulatory compliance costs onward to provincial payers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Faces Closure Growth

The wound care sub-category captured 64.78% of Canada wound care management devices market share in 2025, equating to USD 1.25 billion of spend against the total market that year. Advanced antimicrobial dressings—particularly silver- and polyhexanide-based variants—outpaced general category growth after multiple provinces updated formularies to reimburse outcome-verified products. Negative-pressure wound therapy systems maintained double-digit revenue growth, benefitting from smaller, battery-powered models tailored for home discharge programs. Traditional dressings still fill low-acuity use cases, yet their unit price compression counters volume stability, pulling category value down wherever public tenders award on lowest-cost criteria. Within advanced wound dressings, ConvaTec’s AQUACEL Ag Extra and Smith & Nephew’s ALLEVYN Life drove most volume, while new entrants such as Kane Biotech’s revyve gel focus on antimicrobial resistance mitigation to earn formulary slots.

The wound closure segment, while only 35.22% of revenue in 2025, is tracking a 5.74% CAGR, reflecting renewed surgical throughput and a nationwide emphasis on minimally invasive techniques that shorten recovery windows. Tissue adhesives and absorbable stapling devices attract surgeons seeking to lower post-operative infection rates and improve cosmetic outcomes. Industrial design improvements yield applicators that require fewer staff for deployment, aligning with nurse-shortage realities. Meanwhile, suture technology is evolving toward antimicrobial coatings, turning basic consumables into higher-value items with infection-control credentials. Collectively, these trends underscore how adjacent closure technologies threaten to chip away at wound-care share unless dressing suppliers broaden portfolios or integrate with closure partners, a convergence dynamic already visible in cross-licensing deals announced in late 2024.

By Wound Type: Chronic Wounds Lead Despite Acute Acceleration

Chronic wounds accounted for 67.95% of Canada wound care management devices market size in 2025, underpinned by diabetic foot ulcer prevalence and long-duration treatment protocols that consume multiple dressing cycles. Diabetic foot ulcers alone generate extended average healing windows of 20 to 26 weeks, providing steady device demand that appeals to manufacturers seeking recurring revenue. Pressure-ulcer guidelines in long-term care mandate repositioning and specialised mattress use, but adherence gaps keep advanced foam dressings in active rotation, especially products embedded with micro-climate control films. Venous leg ulcers arise in an aging, mobility-restricted population, reinforcing demand for compression-compatible dressings and off-loading devices.

Acute wounds, at 32.05% of 2025 value, are forecast to expand at a 6.03% CAGR through 2031, largely on the back of surgical backlog reduction plans that elevate elective and trauma procedures. Accelerated burn-unit admissions and elevated construction-site injuries during the post-pandemic infrastructure surge also feed the acute pipeline. Hospitals running enhanced-recovery-after-surgery pathways now pair minimally invasive closure with antimicrobial dressings to reduce site infections, a practice often stipulated in updated accreditation checklists. For device makers, the acute segment’s volume spikes require agile supply-chain capacity that can flex with surgical scheduling, a differentiator increasingly valued in provincial tender evaluations.

By End-user: Hospital Dominance Challenged by Home Healthcare Expansion

Hospitals controlled 51.98% of 2025 spend, benefiting from centralised purchasing power executed by group purchasing organisations such as Mohawk Medbuy, which managed CAD 3 billion in contracts that year. In-house wound clinics leverage multi-disciplinary teams and protocolised care pathways to deploy high-acuity devices, sustaining a stable baseline demand for premium dressings and negative-pressure systems. Teaching hospitals often pilot innovative materials under investigator-initiated studies that later inform provincial formulary decisions, putting them at the front line of technology cycle adoption.

Home-healthcare environments, representing 25.45% of 2025 value, are projected to grow at a 6.27% CAGR through 2031 as public policy pushes complex care into the community. Battery-operated negative-pressure devices, single-use portable pumps, and antimicrobial hydrogels suited for self-application are gaining traction. Provincial payment codes for wound dressings supplied via community pharmacies were expanded in Ontario and Quebec, enabling patients to access subsidised products without hospital visits. Remote monitoring systems allow visiting nurses to upload wound images, permitting specialist oversight from tertiary centres and accelerating clinical decisions. For suppliers, product design now prioritises handheld size, intuitive controls, and low-noise operation to improve patient adherence and quality-of-life measures often captured in reimbursement assessments.

By Care Setting: In-patient Prevalence Meets Community Growth

In-patient facilities retained 56.35% of 2025 revenue, driven by the complexity of burns, surgical wounds, and pressure-ulcers presenting within acute-care wards. Proprietary foam dressings with exudate-handling linings and automated negative-pressure pumps integrate with existing hospital electronic-medical-record platforms, smoothing documentation for nursing staff and satisfying audit criteria. Hospitals also hold the lion’s share of training infrastructure, allowing rapid scaling of newly licensed devices and thus sustaining market-entry momentum for innovators.

Community and outpatient facilities, which captured 43.65% of spend in 2025, are accelerating at a 6.18% CAGR to 2031 as payers exploit the cost advantage of non-hospital care. Retail clinics embedded in pharmacies now stock professional-grade dressings, while independent wound-care centers proliferate in urban corridors. Portable negative-pressure devices approved for single-patient use underpin early discharge programs, reducing hospital lengths of stay by 1.8 days on average in pilot sites. Furthermore, public-health nurses equipped with AI-enabled imaging apps perform in-home assessments, triggering automated alerts for specialist referral when healing stalls. This care-setting diversification compels suppliers to segment product lines by skill-level required, packaging complexity, and reimbursement channel.

Geography Analysis

Ontario remains the largest provincial contributor, accounting for nearly 36.72% of 2025 revenue on the strength of TeleWound adoption, high surgical throughput, and comprehensive formulary coverage that now includes bio-engineered skin substitutes for diabetic foot ulcers. The province’s outcome-linked procurement pilots extend favourable contract extensions to suppliers who prove reductions in readmissions, redirecting a share of budgeting risk toward manufacturers. British Columbia follows with an 17.84% slice, buoyed by regional procurement coalitions that leverage bulk purchasing to negotiate double-digit price concessions, albeit sometimes curbing smaller innovators’ market access. Hospitals in Vancouver Coastal Health pioneered single-pump negative-pressure rental programs that bundle consumables, an approach quickly copied by Alberta Health Services.

Quebec contributes roughly 15.92% of the Canada wound care management devices market, operating under French-language labelling statutes that favour suppliers with bilingual packaging and clinical-support staff. The province’s public insurer, RAMQ, reimburses negative-pressure therapy when prescribed by certified wound-care nurses, and the 2025 budget earmarked funds for expansion into rural Gaspé and North Shore territories. Atlantic provinces, though combining only 9.18% of market value, show above-average growth as federal equalisation payments buttress healthcare capital purchases, especially in Newfoundland’s two regional trauma centres. Prairie provinces contend with dispersed populations, prompting rapid uptake of tele-wound solutions delivered through broadband expansion grants funded by Ottawa’s CAD 200 billion, ten-year healthcare transfer. Northern Territories present small absolute numbers yet the highest per-capita device use of portable negative-pressure systems due to extreme remoteness. Indigenous Services Canada funds culturally adapted wound-prevention programs, and vendors participating in these initiatives enjoy preferential bid points for future government tenders. Collectively, geographic variation highlights that while reimbursement thresholds drive early adoption, success hinges on servicing linguistic, climatic, and access-to-care idiosyncrasies unique to each province or territory.

Competitive Landscape

The market exhibits moderate fragmentation, with the top five suppliers controlling an estimated 46% of 2025 revenue, leaving ample white space for niche innovators. Smith & Nephew strengthened its portfolio by allocating USD 1.24 billion to wound-care R&D and completing an acquisition that adds acellular dermal matrix products, enhancing its regenerative medicine leverage. Solventum (formerly 3M Health Care) retains strong hospital loyalty through integrated draping and dressing kits that fit within existing surgical workflows, while ConvaTec’s 9.5% segment growth in 2024 arose from AQUACEL Ag Extra upgrades and the ConvaFoam launch.

Domestic SMEs such as NanoTess and Biomiq focus on nano-engineered gels and super-oxidised hydrogels targeting antimicrobial resistance. Their smaller scale is offset by Canada’s Scientific Research & Experimental Development (SR&ED) tax incentives, which subsidise clinical trials and accelerate product refinements. Yet, high device-licensing fees and stringent bilingual labelling slow commercial rollouts, prompting alliances with multinational distributors for nationwide reach. Group purchasing organisations (GPOs) wield growing influence, with Mohawk Medbuy, HealthPRO, and shared-service entities like Nova Scotia Health’s SSWAP collectively dictating formulary composition for more than 300 hospitals. Suppliers must now provide multi-year outcome guarantees and training modules to secure contract renewals, favouring companies with mature health-economic datasets.

Technological convergence also reshapes competition; device makers bundle cloud-based wound-tracking dashboards with consumables, creating sticky service ecosystems. AI-driven image analytics integrated into mobile apps differentiate offerings where clinical staff shortages are acute. Meanwhile, regulatory vigilance on antimicrobials pushes R&D toward non-antibiotic materials, encouraging cross-industry collaborations with material-science firms. These dynamics collectively heighten entry thresholds but reward product depth, clinical evidence, and digital-health integration.

Canada Wound Care Management Devices Industry Leaders

-

Solventum

-

Smith & Nephew plc

-

ConvaTec Group plc

-

Coloplast A/S

-

Mölnlycke Health Care AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NanoTess announced NanoSALV, a gel formulated with nano-scale particles to accelerate healing of chronic and acute wounds, burns, and inflammatory lesions.

- March 2025: Kane Biotech Inc. signed a three-year distribution agreement with Best Buy Medical Canada to commercialise the revyve Antimicrobial Wound Gel nationwide.

- February 2025: Biomiq Inc. introduced PureGel, a super-oxidising nano-hydrogel engineered for sustained hypochlorous-acid delivery to skin injuries and burns.

- January 2025: The Ontario government invested CAD 1 million (USD 0.72 million) to train 400 long-term-care staff through NSWOCC’s SWAN program and Wounds Canada’s champion courses, bolstering workforce competency in advanced wound management.

Canada Wound Care Management Devices Market Report Scope

As per the scope of the report, wound management products are mainly used to treat complex wounds. Wounds and injuries are common afflictions that affect billions of people worldwide.

The Canada wound care management market is segmented by product, wound type, end -user, and care settings. The product type is segmented into (wound care and wound closure). The wound care is further bifurcated into (advanced wound dressings, traditional dressings, wound care devices, active/biologic therapies, topical agents, and other wound care products). The advanced wound dressings are further bifurcated into (foam dressings, hydrocolloid dressings, hydrogel dressings, alginate dressings, film dressings, collagen dressings, and antimicrobial/silver dressings). The traditional dressings are further bifurcated into (gauze & impregnated gauze, and adhesive bandages & tapes). The wound care devices are further segmented into negative pressure wound therapy (NPWT) systems, hyperbaric oxygen therapy equipment, and topical oxygen & ozone devices. The topical agents are further segmented into (antiseptics & antimicrobials, enzymatic debridement agents, and hemostatic agents). The wound closure is segmented into (sutures, surgical staplers, tissue adhesives & and sealants). The wound type is segmented into (chronic wounds (diabetic foot ulcer, venous leg ulcer, pressure ulcer, other chronic wounds) and acute wounds (surgical wounds, burns, traumatic & laceration wounds, other acute wounds)). The report offers the value (in USD million) for the above segments.

By Product

| Wound Care | Advanced Wound Dressings | Foam Dressings |

| Hydrocolloid Dressings | ||

| Hydrogel Dressings | ||

| Alginate Dressings | ||

| Film Dressings | ||

| Collagen Dressings | ||

| Antimicrobial / Silver Dressings | ||

| Traditional Dressings | Gauze & Impregnated Gauze | |

| Adhesive Bandages & Tapes | ||

| Wound Care Devices | Negative Pressure Wound Therapy (NPWT) Systems | |

| Hyperbaric Oxygen Therapy Equipment | ||

| Topical Oxygen & Ozone Devices | ||

| Other Wound Care Products | ||

| Wound Closure | Sutures | |

| Surgical Staplers | ||

| Tissue Adhesives & Sealants | ||

By Wound Type

| Chronic Wounds | Diabetic Foot Ulcer |

| Pressure Ulcer | |

| Venous Leg Ulcer | |

| Other Chronic Wounds | |

| Acute Wounds | Surgical Wounds |

| Burns | |

| Traumatic & Laceration Wounds | |

| Other Acute Wounds |

By End-user

| Hospitals |

| Specialty Wound Clinics & Out-patient Centers |

| Home Healthcare Settings |

| Others |

By Care Setting

| In-patient |

| Community / Out-patient |

| By Product | Wound Care | Advanced Wound Dressings | Foam Dressings |

| Hydrocolloid Dressings | |||

| Hydrogel Dressings | |||

| Alginate Dressings | |||

| Film Dressings | |||

| Collagen Dressings | |||

| Antimicrobial / Silver Dressings | |||

| Traditional Dressings | Gauze & Impregnated Gauze | ||

| Adhesive Bandages & Tapes | |||

| Wound Care Devices | Negative Pressure Wound Therapy (NPWT) Systems | ||

| Hyperbaric Oxygen Therapy Equipment | |||

| Topical Oxygen & Ozone Devices | |||

| Other Wound Care Products | |||

| Wound Closure | Sutures | ||

| Surgical Staplers | |||

| Tissue Adhesives & Sealants | |||

| By Wound Type | Chronic Wounds | Diabetic Foot Ulcer | |

| Pressure Ulcer | |||

| Venous Leg Ulcer | |||

| Other Chronic Wounds | |||

| Acute Wounds | Surgical Wounds | ||

| Burns | |||

| Traumatic & Laceration Wounds | |||

| Other Acute Wounds | |||

| By End-user | Hospitals | ||

| Specialty Wound Clinics & Out-patient Centers | |||

| Home Healthcare Settings | |||

| Others | |||

| By Care Setting | In-patient | ||

| Community / Out-patient | |||

Key Questions Answered in the Report

How large is the Canada wound care management devices market in 2026?

The market is valued at USD 2.04 billion in 2026 and is on track to reach USD 2.66 billion by 2031.

What is the forecast CAGR for wound-care devices sold in Canada?

The overall CAGR between 2026 and 2031 is projected at 5.52%.

Which product segment holds the largest share of current revenue?

Wound care products lead with 64.78% of 2025 revenue, well ahead of closure devices.

Which care setting is expanding fastest in device adoption?

Home healthcare is growing the quickest, advancing at a 6.27% CAGR through 2031 as provinces shift care into the community.

How impactful are nurse shortages on market growth?

Workforce gaps reduce projected CAGR by 0.9%, especially in rural regions where specialised wound-care nurses are scarce.

What role does telemedicine play in Canadian wound management?

Tele-wound platforms cut emergency visits, improve satisfaction, and expand specialist access to remote areas, accelerating overall device utilisation.

Page last updated on: