Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

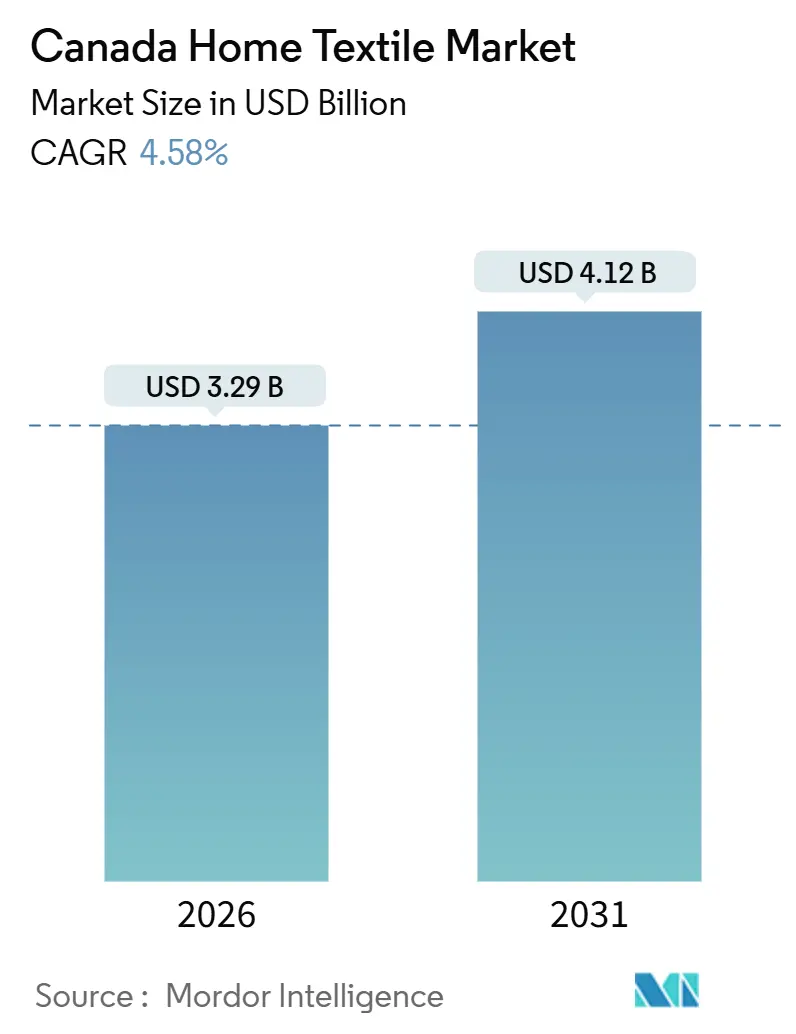

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 4.12 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Home Textile Market Analysis by Mordor Intelligence

The Canada home textile market size is USD 3.29 billion in 2026 and is projected to reach USD 4.12 billion by 2031 at a 4.58% CAGR. Procurement reforms such as the Buy Canadian Policy are shifting federal demand toward domestic suppliers while moderating import reliance in public projects. Residential building activity is stable at a national level, although monthly data show volatility that influences near-term order flows for bed, bath, and window textiles. E-commerce scale advantages improve selection and speed, yet offline stores remain the dominant channel for tactile discovery and assisted selling in the Canada home textile market. Hospitality performance is mixed across months, and commodity costs for cotton and synthetics add margin pressure that favors wrinkle-resistant, antimicrobial, and quick-dry fabrics in institutional settings[1]Source: Public Services and Procurement Canada, “Government of Canada implements Buy Canadian Policy to strengthen Canada’s economy and support homegrown industries,” Government of Canada, canada.ca.

Key Report Takeaways

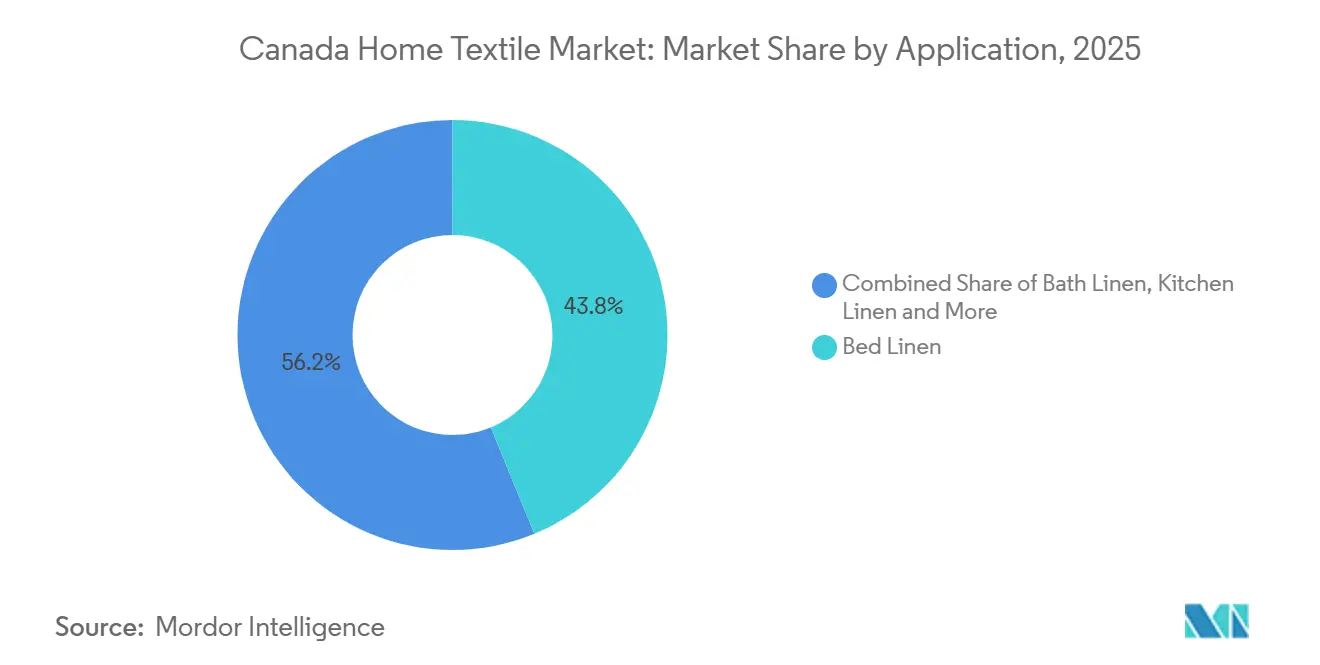

- By application, bed linen led with 43.77% share in 2025 in the Canada home textile market, while upholstery is forecast to grow at 5.61% CAGR through 2031.

- By material, cotton held a 56.25% share in 2025 in the Canada home textile market, while synthetic fibres are projected to rise at a 4.93% CAGR through 2031.

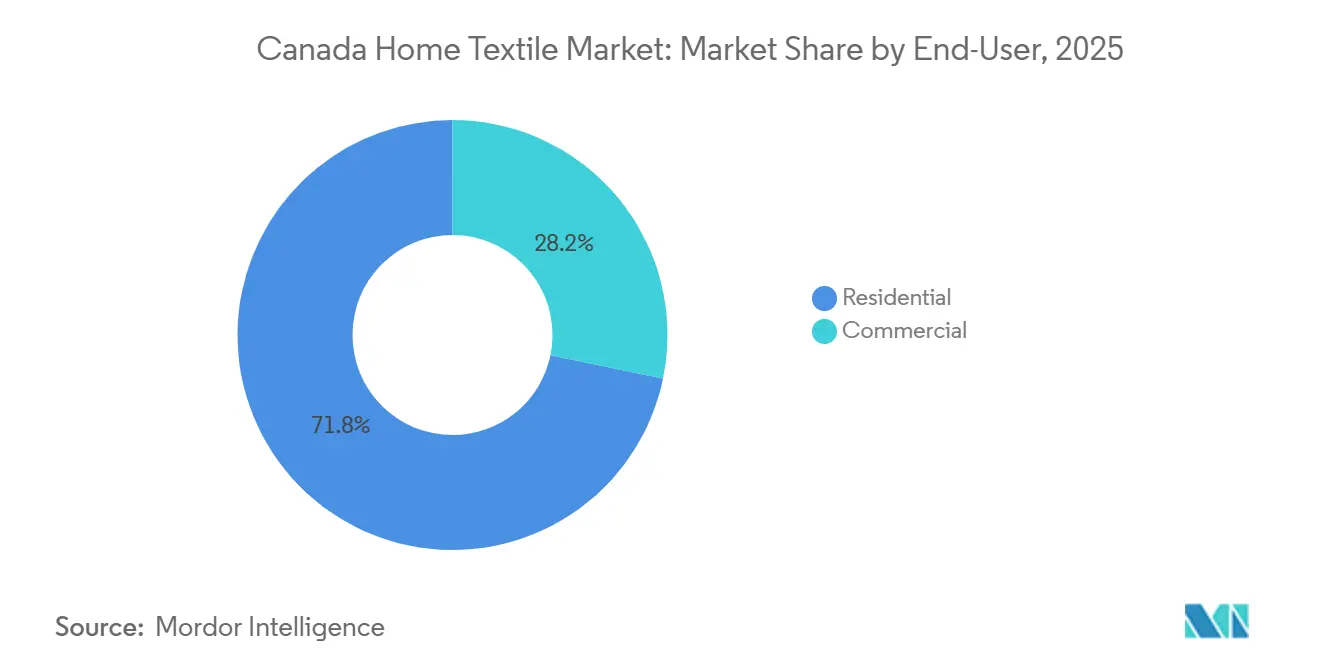

- By end-user, residential accounted for a 71.75% share in 2025 in the Canada home textile market, while commercial is set to expand at a 4.62% CAGR through 2031.

- By distribution channel, offline captured 76.13% share in 2025 in the Canada home textile market, while online is expected to grow at 6.15% CAGR through 2031.

- By geography, Ontario held a 35.31% share in 2025 in the Canada home textile market, while British Columbia is projected to grow fastest at a 6.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Home Textile Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Home Textiles | + 0.8% | Global, with early gains in Ontario, British Columbia, and Quebec | Medium term (2-4 years) |

| Growth in Residential Construction & Renovations | +1.2% | National, strongest in Quebec, Atlantic, and Prairie provinces | Short term (≤ 2 years) |

| Expansion of E-commerce Home Décor Platforms | +0.9% | National, urban concentration in Toronto, Montreal, and Vancouver | Medium term (2-4 years) |

| Hospitality Sector Recovery Post-COVID-19 | +0.6% | National, strongest in Newfoundland/Labrador, Nova Scotia | Short term (≤ 2 years) |

| Government Incentives for Domestic Textile Manufacturing | +0.5% | National, regulatory compliance through ISO, CSA, and federal procurement | Long term (≥ 4 years) |

| Indigenous Design Collaborations Driving Local Appeal | +0.4% | Regional, highest in Quebec, British Columbia, Prairie provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Home Textiles

Environment and Climate Change Canada funded Fashion Takes Action in March 2025 to advance the Canadian Circular Textiles Consortium, which mobilizes stakeholders to pilot fabric-scrap collection and align circularity standards in the Greater Toronto Area[2]Source: Environment and Climate Change Canada, “Government of Canada invests in Canadian innovators to reduce textile and plastic waste and promote circular economy,” Government of Canada, canada.ca. Quebec’s regional planning targets a higher textile recovery rate by 2031, supported by municipal drop-off coordination and écocentre acceptance that together set a clearer policy path for diversion from landfills. Retailers and brands are responding with greener materials and verified claims, including Naia-based blends and certified down or rug-pad components promoted at retail, which cater to buyers willing to pay a premium for validated sustainability attributes. Grassroots supply-chain initiatives such as Fibreshed Québec’s research and events seek to formalize standards for local wool and facilitate farm-to-finished product linkages that cut transport emissions. Export capacity and scale remain uneven, which constrains domestic labels that still source greige textiles offshore when local mills lack throughput, as reflected in provincial trade profiles.

Growth in Residential Construction & Renovations

Total housing starts reached 245,367 units in 2024 at a national level, while multi-unit activity sustained completions that underpin recurring demand for bed and bath basics in the Canada home textile market[3]Source: Statistics Canada, “Canada Mortgage and Housing Corporation, housing starts, under construction and completions, all areas, annual,” Statistics Canada, statcan.gc.ca. Through November 2025, year-to-date starts were higher than the prior year, although the monthly trend softened, which underlines the near-term variability in purchase planning for retailers and suppliers. Quebec outperformed on several housing indicators in late 2025, and that momentum supports broader assortment planning for bed linen, window coverings, and rugs. In this environment, modern smaller-format concepts such as IKEA’s Plan and Order Points deepen category engagement in bedrooms and living rooms, supported by a network expansion and an investment program to reduce prices across key SKUs. These shifts combine structural and channel effects that sustain the Canada home textile market as households plan staged upgrades for bedrooms, bathrooms, and living spaces.

Expansion of E-commerce Home Décor Platforms

E-commerce reach has scaled with large platforms that add SKUs and accelerate fulfillment, which widens the consideration set for textiles and décor purchases in the Canada home textile market. Wayfair’s investor communication highlights the breadth of its North American addressable home category and the influence of its fulfillment assets for two-day delivery on best sellers, which underpins its bedding and related textile lines. Offline retail still commands the majority of transactions for home textiles, yet omni services and digital merchandising increase conversion in urban cores where high-intent shoppers seek in-stock options. Duty assessments and compliance checks add cost and complexity to cross-border e-commerce models, as reflected in Wayfair’s reported CBSA-related charges, which vendors must factor into pricing and inventory turnover. The channel landscape, therefore, blends in-store curation with digital convenience in the Canada home textile market, especially in bedding, terry, and window categories.

Hospitality Sector Recovery Post-COVID-19

Hotel performance strengthened in October 2025 with occupancy and RevPAR growth that supports higher linen turnover at full-service properties, followed by a softer November that showed the sector’s sensitivity to event-driven comparisons across key cities. Tourism’s macro contribution rose in 2024, with increased arrivals and trips reflected in employment levels, which reinforces room-night demand and replacement cycles for bed and bath textiles[4]Source: Statistics Canada, “Tourism among the fastest growing sectors in 2024, setting the stage for 2025,” Statistics Canada, statcan.gc.ca. Hospitality procurement trends favor durable blends and antimicrobial options, as shown in buyer guides and supplier programs linked to recognized environmental and building standards relevant for institutional buyers. These specifications support consistent performance in high-laundry environments while helping operators manage energy, water, and compliance requirements. The result is a steady institutional baseline for the Canada home textile market that ebbs and flows with occupancy patterns.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Cotton & Poly-fiber Prices | -0.7% | Global commodity markets, import costs amplified by CAD weakness | Short term (≤ 2 years) |

| Import Competition from Low-Cost Asian Producers | -0.9% | National, acute in value retail channels and online marketplaces | Long term (≥ 4 years) |

| Retail Footprint Contraction of Big-Box Stores | -0.5% | Ontario, Manitoba, Alberta—former HBC strongholds | Short term (≤ 2 years) |

| Skilled Labor Shortage in Canadian Textile Mills | -0.3% | Quebec, Ontario—legacy manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton & Poly-fiber Prices

Cotton price and availability dynamics influence sourcing costs for mills and retailers, with industry updates in early 2025 signaling tighter ending stocks and shifting price floors that affect budget planning and replenishment decisions. Hospitality procurement guidance emphasizes fiber blends and durability to extend wash cycles and manage per-unit costs, which shapes specifications for sheets and terry lines used in hotels and institutions. Retailers respond with price guarantees, targeted promotions, and multi-SKU price investments to defend value perception across core bedding and bath assortments. These moves help offset commodity headwinds in the Canada home textile market and limit inventory risk tied to long ocean lead times. The outcome favors blends that deliver consistent performance across laundering and daily use.

Import Competition from Low-Cost Asian Producers

The majority of home textile imports originate from established supply hubs in Asia, and tariff treatment and trade controls shape how goods enter Canada under relevant customs and trade frameworks. Compliance and duty reviews can add cost to cross-border e-commerce participants, as shown in Wayfair’s reported liabilities related to CBSA assessment for 2021–2023 imports. Domestic players respond by emphasizing curation, inventory visibility, and omnichannel service as differentiators when unit-price competition is intense. Premium brick-and-mortar expansions support this approach by offering tactile discovery and integrated pickup and delivery options. These adjustments moderate but do not eliminate the price gap that motivates imports in the Canada home textile market.

Segment Analysis

By Application: Upholstery Gains as Remote Work Fuels Home-Office Retrofits

Bed linen commanded 43.77% of the Canada home textile market share in 2025, while upholstery is projected to expand at a 5.61% CAGR through 2031. Households continue to refresh bedrooms and living rooms at a steady pace as new builds deliver occupancy and as existing units undergo staged updates. The Canada home textile market benefits from displays and consultative selling in stores that simplify material selection for bed, sofa, and window categories. IKEA’s growing Plan and Order Point network complements large-store coverage by putting bedroom and living-room planning services closer to customers in metro and growth corridors. Bedding and drapery innovation aligns with practical needs such as blackout, thermal insulation, and hypoallergenic attributes, which support premium trading in the Canada home textile market.

Canada's home textile market size for upholstery is projected to expand at a 5.61% CAGR through 2031, alongside rising at-home work and entertainment needs. Hospitality procurement trends also reinforce performance fabrics in the wider ecosystem, with durable blends designed for frequent washing cycles. Specialty assortments and curated online experiences help shoppers navigate thread counts, finishes, and weave types without overpaying for features that do not align with usage. Retailers balance core bed-linen price points with seasonal color and texture updates in throws and accent pillows. These dynamics lift the category mix and keep the Canada home textile market responsive to evolving room configurations.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Synthetic Fibres Close the Gap on Cotton Dominance

Cotton held a 56.25% share in 2025, while synthetic fibres are projected to rise at a 4.93% CAGR through 2031. Product development emphasizes performance aspects such as wrinkle resistance and quick-drying properties that reduce energy use and turnaround time for laundering. In institutional settings, blended constructions support longevity and colorfastness across hundreds of wash cycles, which sustains predictable replacement calendars. Consumer-facing assortments integrate new cellulosic blends and sustainably sourced inputs to enrich hand feel without sacrificing durability. The Canada home textile market shifts toward verified materials and traceability that reinforce quality claims.

Canada's home textile market size for synthetic fibres is projected to expand at a 4.93% CAGR through 2031 as procurement and consumer preferences converge on easy-care benefits. Industry updates indicate tighter cotton supply conditions in 2025 that influence pricing floors and mix decisions, which support blended-fiber growth trajectories. Premium linen and wool retain a distinct niche in bedding, throws, and décor where natural aesthetics and thermoregulation matter, supported by regional fiber initiatives and artisan communities. The overall material mix remains diversified and responsive to use-case requirements across residential and commercial end markets in the Canada home textile market.

By End-User: Commercial Segment Lags Despite Hospitality Recovery

Residential accounted for a 71.75% share in 2025, and steady household formation underpins baseline demand for bedding, towels, drapery, and accent textiles. Hotel performance in 2025 contributed to higher textile turnover in strong months, though comparisons later in the year showed variability across provinces. Procurement guidelines continue to specify durable blends for industrial laundering, which shifts the commercial mix toward performance constructions. The Canada home textile market sees incremental institutional gains, although residential still drives the majority of sales through the forecast window.

Canada home textile market size for the commercial segment is expected to grow at 4.62% CAGR through 2031 based on updated budgets, facility refresh cycles, and compliance-driven product specifications. Supplier networks for institutional categories integrate sustainability standards in towels and sheets, which adds value beyond basic cost per unit. Residential channels emphasize seasonal themes and comfort features that support both aesthetics and wellness. The result is a balanced but residential-led demand profile in the Canada home textile market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: E-Commerce Gains Share Despite Offline Dominance

Offline channels captured 76.13% of sales in 2025 and continue to anchor tactile discovery, bundled room planning, and same-day pickup in most urban centers. Flagship expansions and localized formats extend reach in growth corridors, which stabilizes foot traffic in bedding and bath categories where material touch and drape are important. Branded collaborations and licensed collections add distinctiveness to shelf sets and online storefronts in the Canada home textile market.

Online channels are expected to grow at a 6.15% CAGR through 2031 as merchandising depth, reviews, and delivery improve conversion in bed linen, towels, and window coverings. Wayfair’s category strategy and logistics capabilities position it to capture repeat purchases in bedding and décor, with two-day fulfillment on best sellers that align with customer expectations. Cross-border duty assessments add friction for some platforms, as reported in statutory filings, which vendors must anticipate in pricing models. The channel mix remains omnichannel in the Canada home textile market, and it benefits from integrated rewards and localized fulfillment.

Geography Analysis

Ontario retained leadership with a 35.31% share in 2025, supported by the province’s large installed base and deep retail coverage. The province experienced housing-start variability in late 2025, which influenced short-term traffic and replenishment patterns for home textile categories. Canada home textile market size in British Columbia is projected to rise at 6.41% CAGR through 2031, and the region’s hotel and multi-family dynamics continue to support linen and décor demand in 2026. Quebec’s performance in 2025 housing metrics and its textile mill employment gains add depth to the provincial ecosystem as mills align with public procurement and trade provisions under CUSMA.

The rest of Canada consolidates a diversified base across Alberta, Saskatchewan, Manitoba, and the Atlantic provinces. Markets with strong resource and tourism exposure sustain hotel demand and linen turnover when events and travel patterns stabilize. National housing activity in 2024 and 2025 supports core bedroom and bath categories, with multi-unit completions underpinning move-in bundles in the Canada home textile market. Retail expansions tailored to local catchments, including small-format planning studios, help maintain access and service levels in smaller metros.

Policy frameworks now include domestic-content prioritization for eligible procurements, which aligns with mills that document traceability and meet ISO and CSA standards for public projects. Quebec’s municipal valorization targets for textiles further encourage post-consumer collection and reuse initiatives, which can influence local assortment and sourcing practices over time. Ontario’s scale, British Columbia’s growth trajectory, and Quebec’s industrial base together frame the demand and supply context for the Canada home textile market into 2031.

Competitive Landscape

The Canada home textile market is moderately fragmented, with mass merchants, specialty retailers, and large e-commerce platforms competing on price, curation, and convenience. Companies use licensing and exclusive collections to differentiate and capture displaced demand from legacy banners. Canadian Tire’s licensed Hudson’s Bay Stripes Collection extends brand equity across a national footprint and leverages a large loyalty base for bedding and bath sell-through. IKEA continues to expand planning studios for bedrooms and living rooms to grow ticket and conversion with consultative selling. Specialty banners invest in urban markets to enhance in-person experiences and fast fulfillment in the Canada home textile market.

Platform players scale selection and speed while navigating compliance and duty considerations. Wayfair’s investor materials outline scale, traffic, and logistics infrastructure, while statutory filings detail CBSA-related charges that inform pricing and inventory planning for imported goods. Procurement partners in hospitality align product lines with environmental and building standards that matter to institutional buyers, which influences blend ratios and finishing chemistries in terry and sheets. These strategic moves support agility across price tiers and end markets in the Canada home textile market.

Distinctive design sources remain a lever for premium positioning. Indigenous collaborations add unique prints and storytelling value across décor and bedding collections, supported by wholesalers and artisan brands that have built national awareness since 2024. Sustainability-oriented material innovations, including Naia-based blends, present another path to differentiation that third-party certifications at retail can validate. Together, these approaches strengthen brand equity and reinforce the value proposition in the Canada home textile market across both residential and commercial demand.

Canada Home Textile Industry Leaders

IKEA Group

Hudson’s Bay Company

Canadian Tire Corporation

Sleep Country Canada Holdings Inc.

Simons

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: IKEA Canada opened its Plan and Order Point in Abbotsford, British Columbia, featuring kitchen, bedroom, bathroom, and living room inspirations with on-site consultations.

- November 2025: Canadian Tire Corporation launched the first-ever Hudson’s Bay Stripes Collection under a licensing agreement, introducing blankets, pillows, and towels featuring the iconic stripes exclusively at Canadian Tire stores and CanadianTire.ca.

- November 2025: IKEA announced a Plan and Order Point in Gatineau, Quebec, scheduled for 2026, with one-on-one planning services for home-furnishing solutions.

- November 2025: La Maison Simons opened its 18th store at Yorkdale Shopping Centre in Toronto as part of a multi-location Toronto expansion.

Canada Home Textile Market Report Scope

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Geography

| Ontario |

| Quebec |

| British Columbia |

| Rest of Canada |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Others | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Geography | Ontario | |

| Quebec | ||

| British Columbia | ||

| Rest of Canada | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the Canada home textile market?

The Canada home textile market size is USD 3.29 billion in 2026 and is projected to reach USD 4.12 billion by 2031 at a 4.58% CAGR.

Which application category leads demand in Canada?

Bed linen leads with 43.77% share in 2024, while upholstery is the fastest growing segment at a 5.61% CAGR to 2030.

How are materials shifting in the Canada home textile market?

Cotton remains the largest material at 56.25% share, while synthetic fibres are the fastest growing with a 4.93% CAGR through 2030, driven by durability and easy-care benefits.

Which channels will see the most growth through 2030?

Offline remains dominant at 76.13% share, while online is expected to grow at a 6.15% CAGR supported by scale logistics and expanding assortments.

Which province is the largest buyer of home textiles?

Ontario holds a 35.31% share, while British Columbia is projected to post the fastest growth at a 6.41% CAGR through 2030.

What policy changes are most relevant to domestic suppliers?

The Buy Canadian Policy prioritizes domestic content in eligible federal procurements, aligning with CSA and ISO standards and supporting qualified mills and converters.