Market Overview

| Study Period | 2023 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

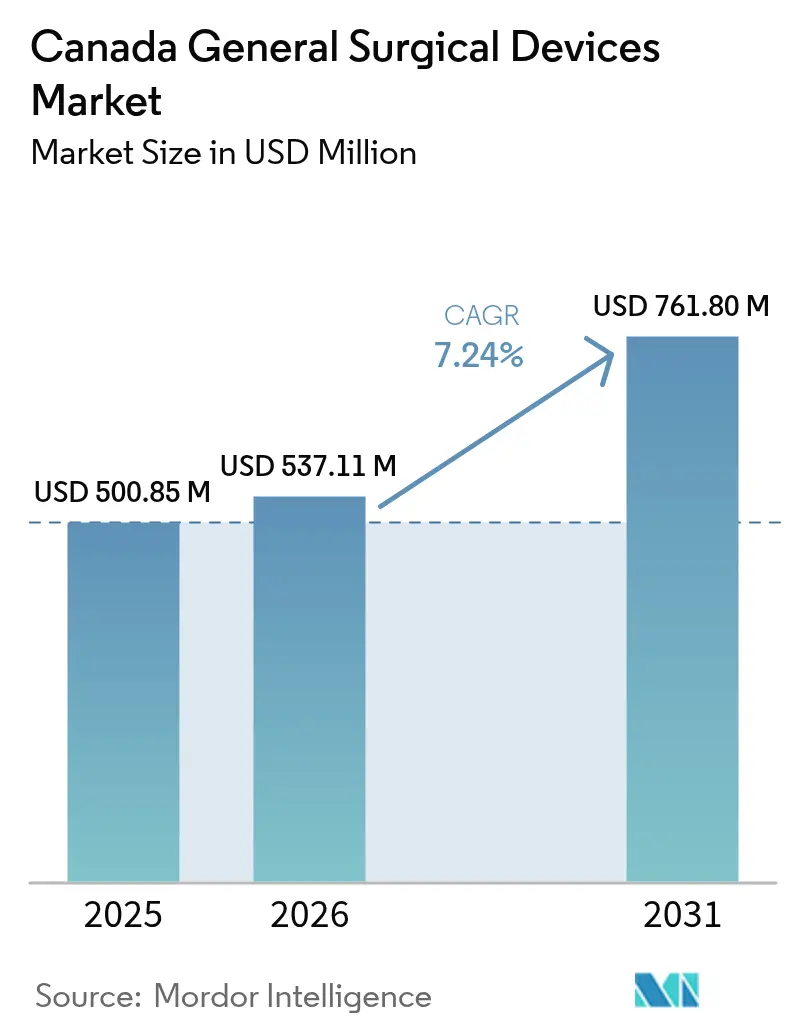

| Base Year Market Size (2025) | USD 500.85 Million |

| Market Size (2026) | USD 537.11 Million |

| Market Size (2031) | USD 761.8 Million |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

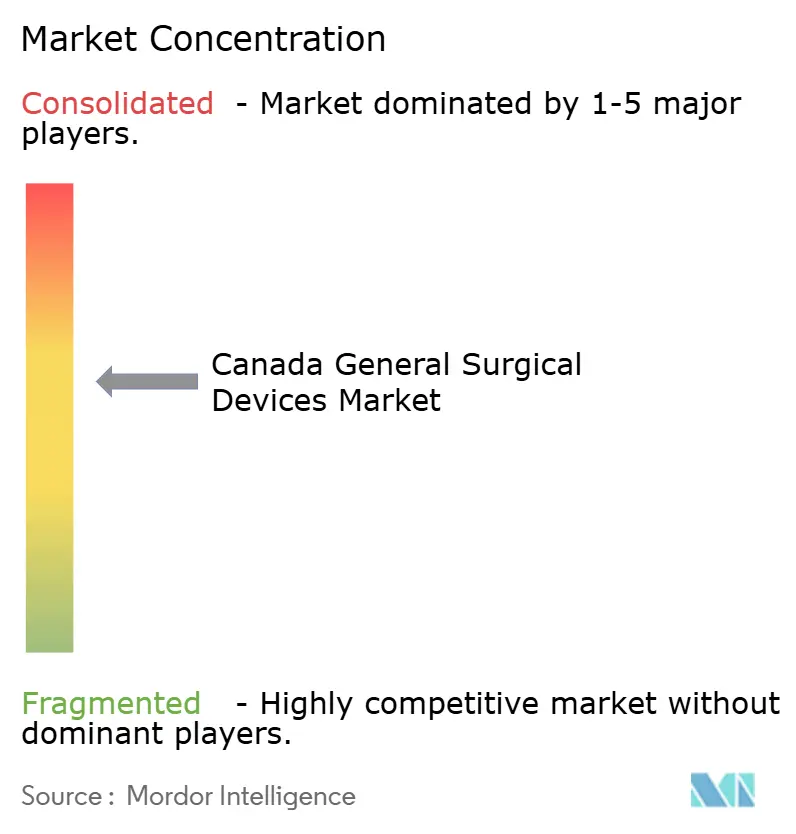

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada General Surgical Devices Market Analysis by Mordor Intelligence

The Canada General Surgical Devices Market size in 2026 is estimated at USD 537.11 million, growing from 2025 value of USD 500.85 million with 2031 projections showing USD 761.8 million, growing at 7.24% CAGR over 2026-2031. Stable public funding, a rapidly aging population, and hospital modernisation programs underpin this growth. Provincial investment cycles add momentum; for example, Alberta’s USD 800 million cancer-care program is already generating multi-year equipment orders.[1]Source: Government of Alberta, “Government of Alberta Invests $800 million CAD to Improve Cancer Care,” siemens-healthineers.com Shifting surgical preferences toward minimally invasive and robotic techniques accelerate replacement demand, while expanded private surgery capacity widens buyer diversity. At the same time, regulatory streamlining through Health Canada’s joint eSTAR pilot with the FDA shortens product-launch timelines and raises competitive intensity.

Key Report Takeaways

- By product, hand-held instruments led with 32.10% of Canada general surgical devices market share in 2025, while robotic and computer-assisted systems are projected to expand at an 8.64% CAGR through 2031.

- By procedure approach, minimally invasive surgery accounted for 72.95% of the Canada general surgical devices market size in 2025 and is advancing at an 7.95% CAGR to 2031.

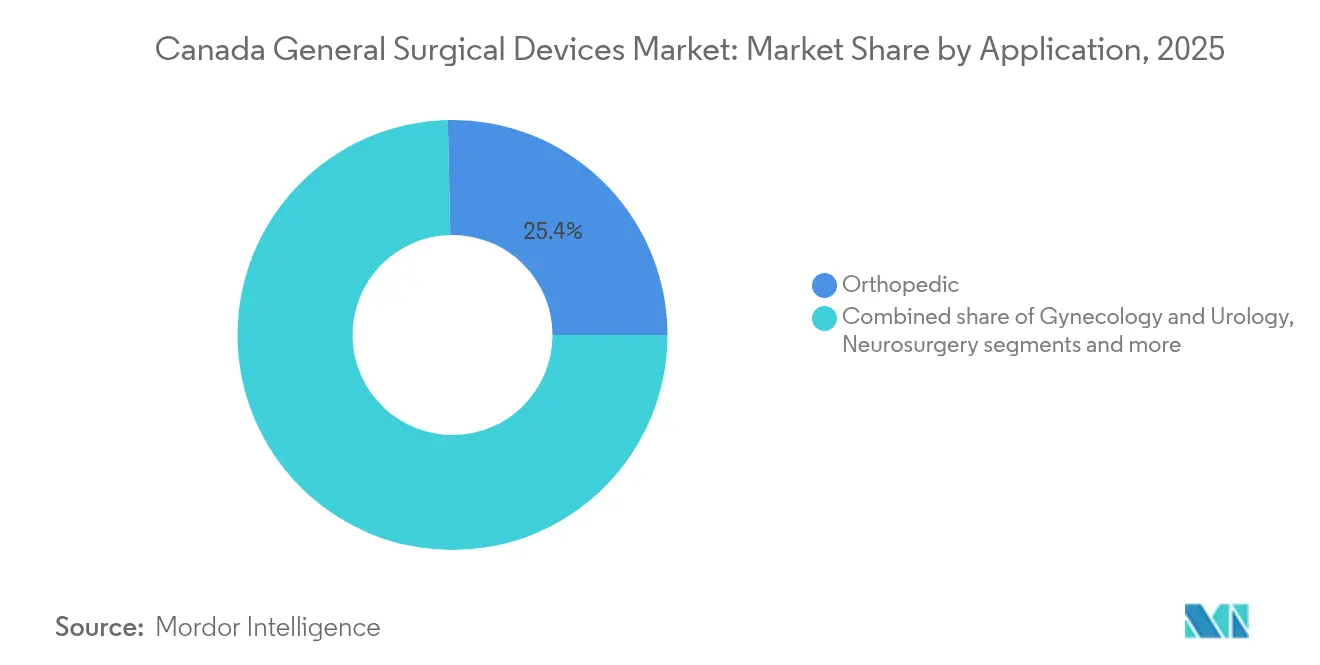

- By application, orthopedics captured 25.35% revenue share in 2025; neurosurgery is the fastest-growing application at an 8.22% CAGR to 2031.

- By end user, hospitals dominated with 68.85% share in 2025, whereas ambulatory surgical centers post the highest 8.70% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada General Surgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical procedure volume due to aging population & chronic-disease burden | +1.8% | National, with concentrated impact in Ontario, Quebec, British Columbia | Long term (≥ 4 years) |

| Rapid adoption of minimally-invasive & robotic techniques | +1.2% | Urban centers and major hospitals, strongest in Alberta, Ontario | Medium term (2-4 years) |

| Federal/Provincial funding boosts (e.g., Canada Health Transfer escalator) | +1.5% | National, with provincial variations in deployment timing | Medium term (2-4 years) |

| AI-enabled asset-light robotic platforms for ambulatory centres | +0.9% | Metropolitan areas, early adoption in British Columbia, Alberta | Long term (≥ 4 years) |

| Technological advancements and rising healthcare expenditure | +0.7% | National, with premium adoption in major urban centers | Medium term (2-4 years) |

| Expansion of private hospitals and ambulatory surgical centers | +0.6% | Alberta, Ontario, with emerging presence in other provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedure Volume Due to Aging Population & Chronic-Disease Burden

Canada’s elderly cohort is expanding quickly, with the ≥ 85-year segment projected to more than triple between 2023 and 2073.[2]Source: Statistics Canada, “Population Projections: Canada, Provinces and Territories, 2023 to 2073,” statcan.gc.ca Surgical case loads followed suit; over 2.3 million procedures were completed in fiscal 2023-24, a 5% rise versus pre-pandemic levels. Chronic conditions such as cancer and heart disease accounted for 43.7% of deaths in 2023, underscoring persistent demand for complex operations. High incidence in rural populations concentrates referrals to tertiary centres, reinforcing equipment purchases in metropolitan hospitals. Access bottlenecks remain: 15.6% of seniors report difficulty obtaining specialist care, highlighting unmet needs that bolster capital expenditure on surgical infrastructure.

Rapid Adoption of Minimally-Invasive & Robotic Techniques

Procedure mix continues its migration from open to minimally invasive approaches. Robotic surgery adoption faces capital constraints, with da Vinci systems costing between USD 1.5 million and USD 2.2 million plus USD 2,000 per procedure, yet Canadian urology residents show 77% participation rates in robotic-assisted procedures, indicating workforce readiness. Laparoscopic colectomy penetration varies widely—7.6% in Newfoundland and Labrador versus 60.2% in British Columbia—illustrating untapped regional potential. Training readiness is improving: 77% of Canadian urology residents participated in robotic-assisted cases during residency. Although capital requirements remain steep, evidence of faster recovery and lower readmission rates sustains the upgrade narrative.

Federal/Provincial Funding Boosts

Total government outlays for health reached USD 253.2 billion in 2023, equal to 23.4% of aggregate public spending. The Canada Health Transfer escalator locks in predictable 5% annual increases, allowing provinces to align multi-year equipment budgets. Health Canada’s 2024-25 departmental plan dedicates more than USD 801 million to health protection programs that include regulatory modernisation, directly supporting faster device authorisations. British Columbia’s USD 85 million renal unit illustrates how matched provincial funding brings advanced surgical devices into secondary hospitals.

AI-Enabled Asset-Light Robotic Platforms for Ambulatory Centres

Fraser Health has deployed more than 40 AI projects, including a Digital Twin that models entire regional operations from 16 terabytes of data, demonstrating scalable analytics for surgical scheduling. The MRI-compatible neuroArm, developed at the University of Calgary, validates domestic capability in advanced robotics with 35 clinical neurosurgery cases completed. Cost-efficient cloud processing lowers entry barriers for ambulatory surgical centers, aligning with provincial wait-time reduction strategies that rely on outsourced volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance cost of advanced systems | -1.4% | National, with acute impact in smaller hospitals and rural centers | Short term (≤ 2 years) |

| Shortage of MIS-trained surgeons in non-metro provinces | -0.8% | Rural and smaller urban centers, particularly Atlantic provinces | Medium term (2-4 years) |

| Health-technology-assessment backlog delaying approvals | -0.6% | National, with provincial variations in assessment capacity | Medium term (2-4 years) |

| "Made-in-Canada" preference clauses limiting foreign OEMs | -0.4% | Federal and provincial procurement, strongest in Quebec and Ontario | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Cost of Advanced Systems

Robotic platforms carry price tags between USD 1.5 million and USD 2.2 million, with disposables adding roughly USD 2,000 per case. Cost-utility analysis for prostatectomy found minimal quality-adjusted life-year gains, challenging reimbursement models. Maintenance contracts and surgeon certification expenses further strain budgets, forcing smaller hospitals to delay upgrades. Provincial budget constraints force healthcare administrators to prioritize device procurement based on utilization projections rather than clinical superiority, favoring established technologies over innovative solutions.

Shortage of MIS-Trained Surgeons in Non-Metro Provinces

A substantial portion of urology residents considered robotic surgery feasible within Canada’s public system despite near-unanimous belief in future growth, citing limited access outside teaching hospitals. Rural facilities struggle to maintain case volumes needed for skill retention, prolonging regional disparities. Continuing medical education requirements for MIS certification create additional barriers for practicing surgeons in remote locations who face travel and time constraints for training programs. Telemedicine and simulation-based training initiatives offer partial solutions, but hands-on experience requirements limit their effectiveness for complex surgical skill development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robotics Drive Innovation Despite Hand-Held Dominance

Hand-held instruments remain indispensable, holding 32.10% of Canada general surgical devices market share in 2025. Robust replacement cycles in electrosurgical pencils, forceps, and scalpels sustain volume, especially in mid-tier hospitals. Conversely, robotics delivers the highest 8.64% CAGR, supported by clinical evidence of reduced conversion rates and surgeon demand for ergonomic advantages. The neuroArm exemplifies local innovation, opening export opportunities for Canadian OEMs. Laparoscopic towers, smoke-evacuation modules, and smart staplers round out mid-growth niches addressing operating-room efficiency priorities.

The Canada general surgical devices market benefits from continuous incremental improvements, such as nebulisation-based smoke clearance that improves visibility during MIS and complies with occupational-safety guidelines. Workflow-oriented adjuncts like the C-Flex Traction system cut setup time by 50%, complementing primary device demand.

By Procedure Approach: MIS Transformation Accelerates

Minimally invasive surgery dominated the Canada general surgical devices market with 72.95% share in 2025 and continues at an 7.95% CAGR. Ambulatory centers and short-stay hospital units prefer MIS for lower infection risk and faster turnover. Open surgery persists for trauma and complex oncologic resection yet faces relative volume decline as laparoscopy and endoscopic submucosal dissection techniques mature. Robotic-assisted MIS has achieved 77% exposure among graduating urology trainees, ensuring a skilled pipeline once capital barriers recede.

Ambulatory surgical centers drive MIS adoption through operational efficiency requirements, with studies demonstrating successful advanced laparoscopic procedures achieving 4.5-hour median postoperative stays and manageable complication rates. Training infrastructure development supports MIS expansion, with residency programs increasingly incorporating advanced techniques during surgical education rather than post-graduation skill acquisition.

By Application: Neurosurgery Innovation Leads Growth

Orthopedics generated the largest slice (25.35%) of the Canada general surgical devices market size in 2025, driven by joint-replacement demand from aging cohorts. Neurosurgery, however, posts the fastest 8.22% CAGR, fuelled by intra-operative imaging breakthroughs and MRI-compatible robotics. Image-guided cannula systems, such as the NeurADe prototype, underscore future potential for precision interventions. Gynecology and urology maintain solid double-digit MIS penetration, while bariatrics and colorectal surgery expand gradually through ASC channels.

Private healthcare expansion creates parallel demand channels for elective procedures, with knee replacement costs ranging from USD 32,000 to USD 70,000 in private facilities, indicating willingness to pay for reduced wait times. Other applications including ophthalmology and plastic surgery represent niche segments with specialized device requirements and premium pricing structures.

By End User: ASC Expansion Transforms Care Delivery

Hospitals held 68.85% of 2025 revenue, but ambulatory surgical centers deliver the leading 8.70% CAGR. Alberta alone targets 310,000 chartered procedures in 2024-25 to cut wait lists, driving bulk purchases of portable towers and single-use staplers. Private-equity-backed networks such as Clearpoint Health operate 53 facilities, creating consolidated buyer blocs that value supplier training packages alongside hardware. Simulation labs and research institutes form a niche buyer group demanding cutting-edge prototypes for investigator-initiated trials.

Bariatric surgery outcomes comparison between tertiary care hospitals and ambulatory hospitals reveals equivalent safety profiles with improved operational efficiency at ambulatory sites, achieving shorter operative times and recovery periods without compromising patient outcomes. Other applications including ophthalmology and plastic surgery represent niche segments with specialized device requirements and premium pricing structures.

Geography Analysis

Ontario and Quebec anchor demand, accounting for more than half of all surgical volumes because of dense populations and broad tertiary hospital networks. Alberta exhibits the quickest growth trajectory as public-private models scale; its USD 800 million cancer initiative with Siemens Healthineers signals long-range commitment to imaging-surgical ecosystems. British Columbia prioritises diagnostic expansion, adding 18 MRIs and 9 CTs in 2024, thereby boosting downstream surgical throughput.

Atlantic provinces face the steepest aging curves, raising per-capita procedure demand yet confronting surgeon shortages. These constraints stimulate interest in tele-mentored MIS and low-maintenance laparoscopy kits. Northern territories, with sparse populations and limited OR infrastructure, show nascent uptake of battery-powered electrocautery and portable arthroscopy towers, often funded through federal programs targeting remote healthcare equity.

Provincial health-technology-assessment processes introduce staggered adoption schedules; for example, Québec’s “made-in-province” preference slows foreign OEM entry but opens space for domestic start-ups aligning with procurement criteria.

Regulatory Landscape

General surgical devices in Canada are regulated by Health Canada under the Food and Drugs Act and the Medical Devices Regulations (SOR/98-282), which establish risk-based classification (Class I to IV), licensing requirements, and post-market obligations. Class II to IV products require a Medical Device Licence (MDL), while most importers and distributors (and Class I manufacturers) require a Medical Device Establishment Licence (MDEL). For many manufacturers, ISO 13485 is demonstrated through the Medical Device Single Audit Program (MDSAP), which in turn shapes supplier eligibility for hospital tenders.

Regulatory processes are also moving toward more structured electronic and lifecycle oversight. As of April 1, 2026, Health Canada mandated use of the Common Electronic Submission Gateway (CESG) and the Regulatory Enrolment Process (REP) for Class II to IV device licence applications and amendments, increasing the focus on submission readiness for both multinational OEMs and smaller entrants. Amendments that came into force on December 14, 2024 (SOR/2024-136) strengthened expectations around recalls, establishment licensing, and finished product testing. Guidance updates in 2026, including areas such as post-market surveillance and AI/ML-enabled devices, further specify expectations for software-driven surgical platforms and connected operating-room components.

Competitive Landscape

The Canada general surgical devices market balances multinational scale with home-grown ingenuity. Medtronic, Johnson & Johnson, and Stryker combine strong cross-portfolio integration and after-sales service. These leaders bundle instrumentation, imaging, and post-operative analytics into value-based contracts, securing multi-year deals with teaching hospitals. Boston Scientific and Olympus leverage endoscopic specialisation to defend share in MIS consumables.

Canadian innovators occupy targeted niches. Titan Medical advances a single-port robotic concept but remains pre-commercial pending regulatory clearance. Baylis Medical excels in interventional devices now transitioning into surgical adjuncts following recent acquisitions. Synaptive Medical’s April 2025 bankruptcy petition highlights capital-intensity risks despite strong IP positions.[3]Source: Canadian Healthcare Technology, “Synaptive Medical enters bankruptcy protection,” canhealth.com

Strategic activity features cross-border alliances in the country. Top players increasingly embed AI decision-support modules into consoles, aligning with provincial analytics initiatives.

Canada General Surgical Devices Industry Leaders

Boston Scientific Corporation

Medtronic

B. Braun SE

Johnson & Johnson (Ethicon, DePuy)

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Robotic-assisted surgery rollout beyond traditional academic hubs creates room for capital equipment, instruments, and service contracts linked to minimally invasive programs. Hospital deployments show expansion into new sites and specialties: in January 2026, Fraser Health introduced a CAD 5.5 million da Vinci Xi system at Surrey Memorial Hospital, initially targeting thoracic and ENT procedures, and in February 2026 the QEII Foundation funded a CAD 3.8 million da Vinci Xi for the QEII Health Sciences Centre in Halifax, bringing the center to seven surgical robots. These projects support demand for complementary general surgery device categories that increase operating-room throughput, including laparoscopic towers, advanced energy devices, and workflow tools designed for short-stay pathways.

Procurement modernization and supply resilience also create opportunities for vendors that can support multi-site standardization and faster replenishment. Health Canada maintains an exceptional importation and sale framework to mitigate potential device shortages, and its 2025-2026 departmental plan references development of national bulk purchasing and appropriate-use strategies for drugs and related health products through Canada’s Drug Agency. Together, these initiatives raise the value of compliant labeling and quality documentation, interchangeable product configurations, and service models that help hospital networks and expanding ambulatory surgical centers manage utilization, training, and lifecycle costs for higher-acuity MIS and computer-assisted systems.

Recent Industry Developments

- May 2026: Boston Scientific announced a strategic investment in MiRus LLC to expand access to proprietary medical technologies. The investment adds optionality around future technology integration and pipeline adjacency relevant to minimally invasive procedural ecosystems.

- April 2026: GE HealthCare announced digital integration between its bkActiv intraoperative ultrasound system and Medtronic’s Stealth AXiS surgical navigation system for cranial procedures. The interoperability between imaging and navigation platforms supports more connected operating-room workflows and can affect hospital purchasing toward integrated vendor stacks.

- January 2024: Thornhill Medical signed a USD 356 million ventilator contract with the U.S. Army. The award highlighted Canadian medical device manufacturing credibility and export-scale production capability, supporting broader supplier confidence for hospital-grade equipment categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues from general surgical devices sold and used in Canada for open and minimally invasive procedures across care settings, including manual instruments, powered and energy-based systems, access devices, and wound closure tools.

Scope exclusions: Single-use commodity consumables such as drapes, gowns, and basic sutures are not counted in this market size.

Segmentation Overview

- By Product

- Handheld Instruments

- Laparoscopic Devices

- Electrosurgical Devices

- Wound-Closure Devices

- Trocars and Access Systems

- Robotic and Computer-Assisted Systems

- Others

- By Procedure Approach

- Open Surgery

- Minimally Invasive Surgery

- By Application

- Gynecology and Urology

- Orthopedic

- Cardiology and Thoracic

- Neurosurgery

- Gastrointestinal and General

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the Canada procedure context, and put reasonable guardrails around volumes and pricing. We mainly relied on public sources such as Health Canada device and licensing information, Statistics Canada health expenditure and demographic series, the Canadian Institute for Health Information (CIHI) for surgery activity indicators, and OECD health statistics to sanity check trends.

To make the model more practical, we also reviewed sources such as importer and exporter trade statistics where relevant, peer-reviewed clinical literature on adoption of minimally invasive approaches, and public company filings plus investor presentations to understand product mix shifts. Select paid subscriptions were used only for company financials and news screening, and for patent checks when new device categories were discussed. This list is not exhaustive, and many other public and paid sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were used to confirm what is actually purchased and used in Canada, and how product mix is changing between open, laparoscopic, electrosurgical, and access tools. We spoke with a mix of manufacturers and distributors, procurement and materials management teams, surgeons, and OR leaders, and then cross checked the inputs against typical tender behavior and replacement cycles.

Because this is a Canada-only market, coverage focused on major provinces and key care settings such as hospitals, ambulatory surgical centers, and specialty clinics, so gaps from desk research could be closed before finalizing assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 18% | |

| Mid tier: 49% | Functional/Unit leaders: 28% | |

| Smaller Players: 20% | Managers: 54% |

Market-Sizing & Forecasting

The core model was built using a top-down demand pool approach where procedure volumes and care setting activity are translated into device demand, before values are assigned through realistic average selling price ranges. The totals were then corroborated with selective bottom-up checks such as supplier revenue splits tied to Canada exposure, channel feedback on category shares, and sampled price points for high-usage device groups.

Key inputs that moved the model in visible ways included surgical procedure growth trends, the share of minimally invasive cases, adoption pace of energy based systems, utilization of trocars and access devices per case, wound closure method mix, and replacement and capital refresh cycles for powered platforms. Where bottom-up signals were incomplete, gaps were handled by using conservative share ranges and then reconciling them back to the procedure-linked ceiling.

For forecasting, we used scenario analysis supported by simple trend modeling, and the assumptions were adjusted based on what interviewees expected for OR modernization, staffing constraints, and budget cycles. The final forecast reflects the most likely path, with sensitivity ranges used internally to test how outcomes shift when procedure growth or price progression changes.

Data Validation & Update Cycle

Validation was done through several checks, and not as a single end step. We compared the modeled totals with independent signals such as health spending direction, procedure volumes, and category-level adoption commentary from public sources, and then outliers were reviewed and corrected if the logic did not hold.

Before sign-off, the output is reviewed across analysts, followed by targeted re-contacts when a major variance is seen in pricing, category share, or scope interpretation. Reports are refreshed annually, and interim updates are made when material events occur that can shift demand or pricing. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Canada General Surgical Devices Market Size Compared With Other Published Estimates

Published market sizes for general surgical devices in Canada do not always match, even when the market name looks the same. The differences usually come from what is counted as a device versus a consumable, how robotics is treated, what year is used as the base, and whether price progression is assumed aggressively or kept closer to observed purchasing behavior.

The benchmark table shows a wide spread mainly because some sources bundle large disposable supply categories and exam gloves into the same total, which lifts the value quickly, while others stick closer to core surgical instruments and systems. The benchmark table also reflects that, in Mordor Intelligence's model, the total is limited to general surgical instruments and systems used in procedures and it excludes broad single-use consumables like drapes, gowns, and basic sutures, which materially changes the 2024 to 2026 comparison.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 537.11 M (2026) | |

| Global Consultancy A | USD 928.10 M (2024) | Uses a wider basket that explicitly includes disposable surgical supplies, examination and surgical gloves, and procedural kits, and this expands the total beyond instrument and system revenues. |

| Industry Publisher B | USD 565.00 M (2024) | Anchors on a nearer-term base year and applies a narrower device grouping, but scope statements are less explicit on exclusions, so some closure and access items may be counted differently across categories. |

The table points to scope as the biggest driver, followed by base-year alignment and how mixed categories are mapped into totals. By tying value to procedure-linked demand indicators and then checking it against real purchasing and category mix feedback, the final estimate stays traceable to clear inputs and can be repeated when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the Canada general surgical devices market?

The market is valued at USD 537.11 million in 2026 and is projected to grow to USD 761.8 million by 2031.

Which product category is expanding the fastest?

Robotic and computer-assisted systems record the highest 8.64% CAGR through 2031 due to rising minimally invasive procedure volumes.

How large is the minimally invasive segment within overall revenue?

Minimally invasive surgery commands 72.95% of 2025 revenue and continues to expand as hospitals prioritise short-stay pathways.

Why are ambulatory surgical centers important to device vendors?

ASC volumes are growing at a 8.70% CAGR, offering steady demand for compact, easy-to-maintain systems and disposables.

Which provinces show the strongest purchasing momentum?

Alberta leads growth with aggressive public-private capacity boosts, while Ontario and Quebec remain the largest absolute buyers.

What limits wider adoption of high-end robotics?

Capital cost, maintenance expenses, and surgeon training availability in rural regions constrain near-term rollout despite clinical benefits.

Page last updated on: