Canada Data Center Cooling Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

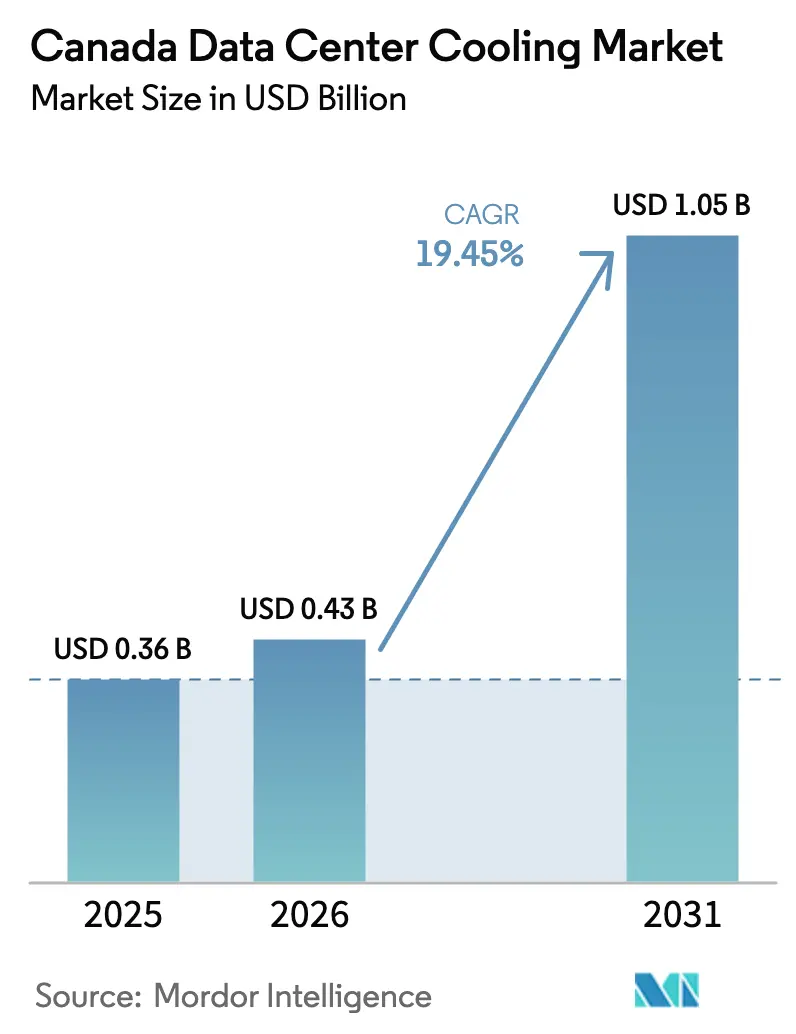

| Base Year Market Size (2025) | USD 0.36 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 1.05 Billion |

| Growth Rate (2026 - 2031) | 19.45% CAGR |

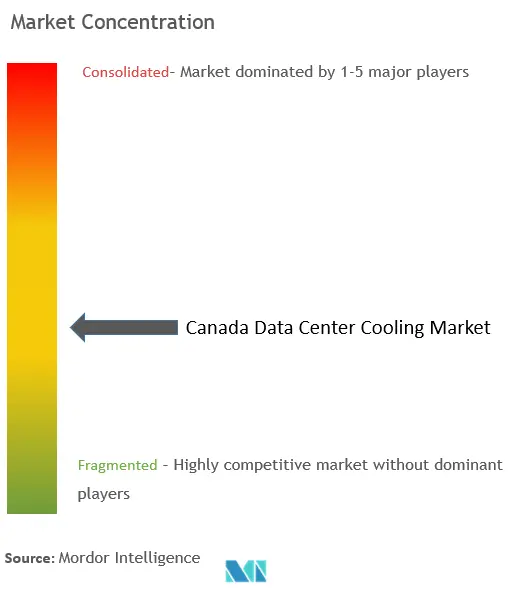

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Cooling Market Analysis by Mordor Intelligence

The Canada data center cooling market size was valued at USD 0.36 billion in 2025 and estimated to grow from USD 0.43 billion in 2026 to reach USD 1.05 billion by 2031, at a CAGR of 19.45% during the forecast period (2026-2031). Sustained expansion is tied to large-scale AI workloads, abundant hydroelectric power, and a national carbon-pricing scheme that rewards highly efficient cooling designs. Hyperscalers are accelerating fresh capacity in Quebec, British Columbia, Alberta, and Ontario as rack power densities hit 300 kW, pushing operators to adopt hybrid air-liquid systems while recovering waste heat for secondary uses. Growing investment from domestic manufacturers in coolant distribution units (CDUs) and low-GWP refrigerants is easing supply pressure, while federal rebates shorten payback periods for liquid technology upgrades. M&A activity from Schneider Electric’s USD 850 million Motivair buy-out to Vertiv’s centrifugal chiller acquisition—confirms that global suppliers are positioning aggressively for dense AI compute roll-outs

Key Report Takeaways

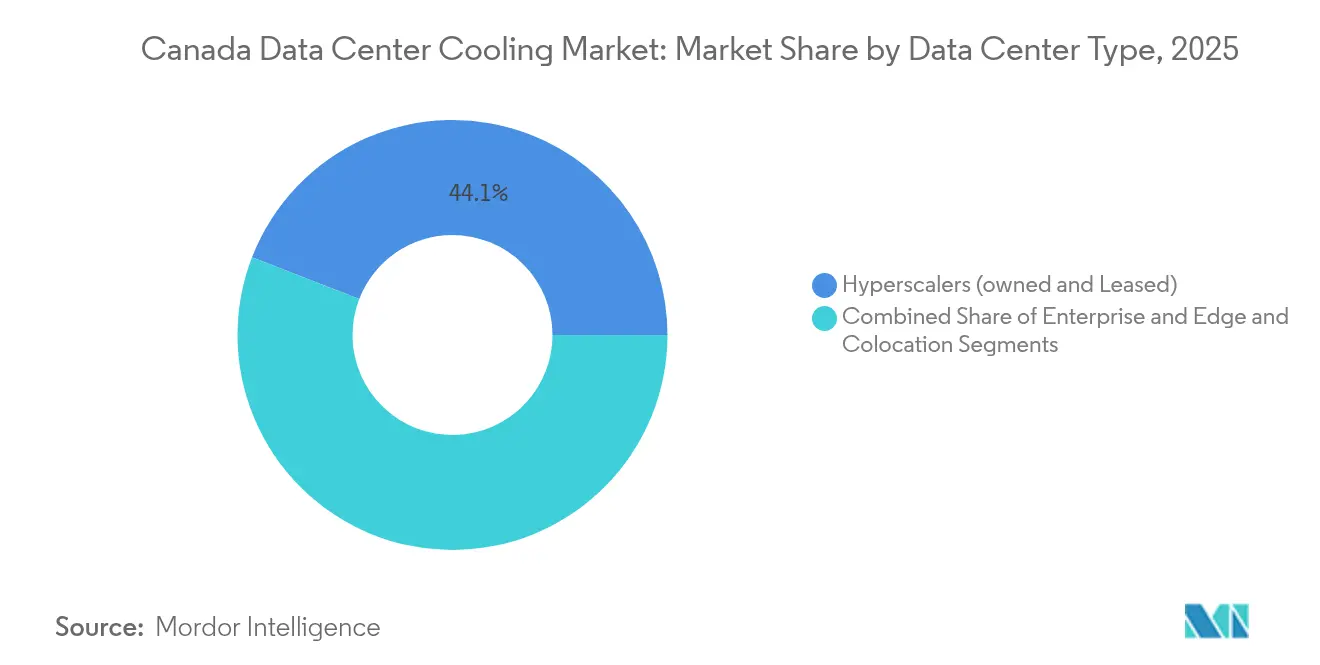

- By data center type, hyperscalers led with 44.12% of the Canada data center cooling market share in 2025; their segment is advancing at a 23.4% CAGR through 2031.

- By tier, Tier 3 facilities retained 61.45% share of the Canada data center cooling market size in 2025, while Tier 4 is expanding fastest at 22.65% CAGR to 2031.

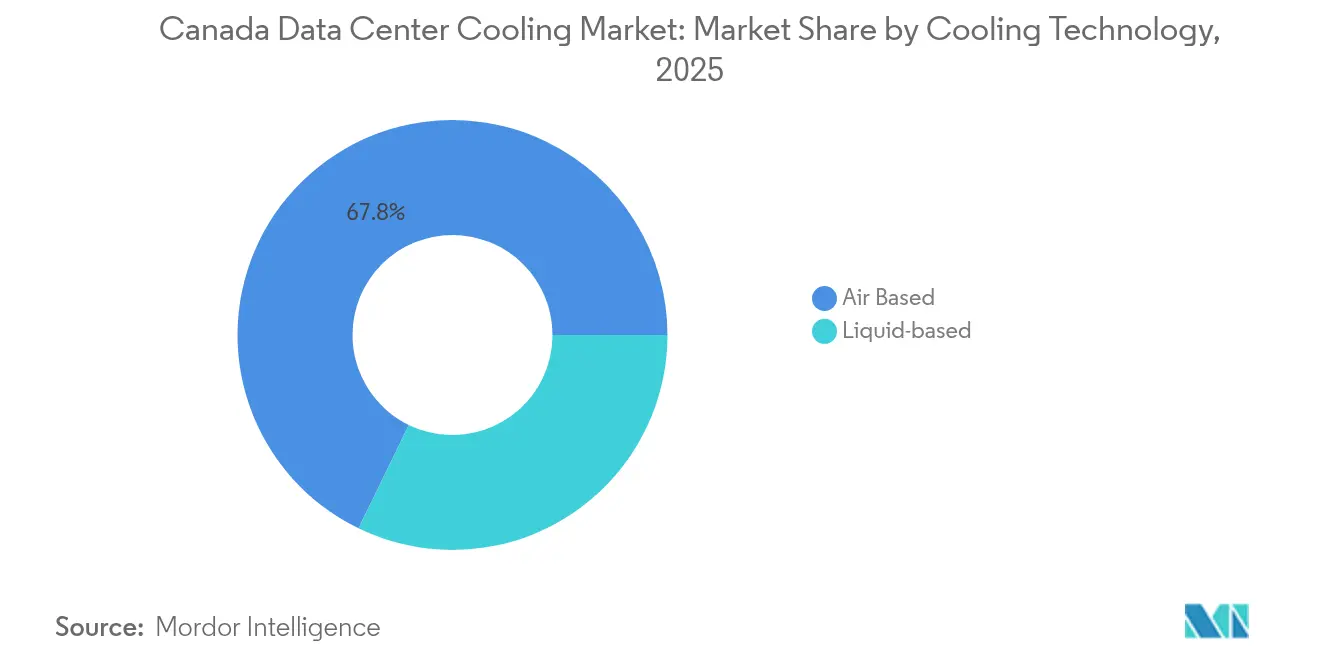

- By cooling technology, air-based systems accounted for 67.80% of the Canada data center cooling market size in 2025; liquid-based solutions are growing at 23.9% CAGR.

- By component, equipment captured 80.55% Canada data center cooling market share in 2025, whereas services show the highest growth at 22.9% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale and AI rack density surge | +6.2% | National; strongest in Quebec, BC, Alberta | Medium term (2-4 years) |

| Federal carbon-pricing and efficiency credits | +4.1% | National; enhanced in Quebec | Long term (≥ 4 years) |

| Abundant renewable power and cool climate | +3.8% | Quebec, BC, northern regions | Long term (≥ 4 years) |

| Accelerating hyperscale & colocation build-outs | +5.5% | Toronto, Montreal, Vancouver, Calgary | Short term (≤ 2 years) |

| Québec utility heat-reuse rebates | +1.4% | Quebec province | Medium term (2-4 years) |

| Early access to low-GWP refrigerants | +0.9% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale and AI Rack Density Surge

Racks exceeding 300 kW are now common, raising thermal loads nearly 20-fold versus legacy 15 kW deployments. Bell Canada’s deployment of 44 AQUILON units cut cooling energy by 80% in twenty sites,[1]Carnot Refrigeration — “AQUILON Case Study,” Carnotrefrigeration.com protecting operating margins while meeting ESG targets. Vertiv cited 24% net sales growth in Q1 2025, attributing the uplift largely to liquid cooling for GPU clusters. The Canada Energy Regulator projects data-center power demand to double by 2026 and AI workloads to lift consumption 160% by 2030, making advanced cooling an immediate necessity. SuperMicro forecasts 2,900% expansion in liquid cooling shipments within two years, a signal that the Canada data center cooling market will pivot rapidly toward fluid-based architectures

Federal Carbon-Pricing and Efficiency Incentives

Canada’s carbon price, now CAD 80 per tonne, directly rewards facilities that migrate to low-GWP refrigerants and heat-recovery designs, creating a structural ROI advantage for liquid systems. GHG offset credits under the federal Refrigeration Systems Protocol enhance payback periods, while Natural Resources Canada added CRAC units to its Energy Efficiency Regulations from May 2024.[2]Natural Resources Canada — “Amendments to Energy Efficiency Regulations,” Natural-resources.canada.ca The Green Buildings Strategy earmarks USD 800 million for efficiency retrofits, further nudging operators to implement high-efficiency CDUs, immersion tanks, and heat pumps

Abundant Renewable Power and Cool Climate

Hydro-Québec’s 100% renewable grid supports free cooling up to 80% of the year,[3]Paul Albright — “Q01 Campus Targets Net-Zero Compute,” QScale.com letting QScale’s Q01 campus run at PUE 1.2 without chillers for much of winter. British Columbia offers similar hydro capacity, encouraging Bell’s AI Fabric supercluster to concentrate 500 MW of compute in Kamloops. Cold ambient conditions shave cooling energy by 30-40% compared with most United States markets, delivering a built-in cost advantage to the Canada data center cooling market.

Accelerating Hyperscale and Colocation Build-outs

eStruxture’s CAD 1.8 billion raise will fund the 90 MW CAL-3 complex in Calgary, embedding modular liquid systems that scale with multi-tenant AI demand. Cologix is onboarding GPU-as-a-Service clients in Montreal and Toronto, leaning on hybrid cooling to accommodate mixed tenant loads. ROOT Data Center’s KyotoCooling rollout cuts power consumption 50% against local peers, highlighting cost pressure on operators still tied to legacy air designs

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of liquid-based systems | -2.8% | National; hits smaller operators hardest | Short term (≤ 2 years) |

| Facilities-engineer skills gap | -1.9% | Toronto, Montreal, Vancouver | Medium term (2-4 years) |

| Supply-chain bottlenecks for CDUs & fluids | -1.5% | National; import-dependent provinces | Short term (≤ 2 years) |

| BC municipal water-discharge limits | -0.7% | British Columbia municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Liquid-Based Systems

Direct-to-chip and immersion racks cost 3-5 times more than comparable air-cooled footprints. Capital outlays between USD 50,000 and USD 150,000 per rack deter smaller enterprises even though operational power usage can fall 90% and PUE drops below 1.03 on SMC HyperCube installations. In Quebec, cheap electricity extends payback windows to as long as 36 months, pushing some edge operators toward financing mechanisms such as equipment-as-a-service.

Facilities-Engineer Skills Gap

Uptime Institute shows 58% of global operators struggle to hire qualified talent; the shortage is acute in Canadian metros where hyperscalers compete head-to-head. Liquid cooling requires competencies in fluid dynamics and leak-prevention that traditional HVAC curricula seldom teach. IEEE Spectrum notes electrical-engineering openings in data centers will grow 9% through 2033, yet universities have not adapted course work for immersion or CDU design

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscalers Propel Liquid Uptake

Hyperscalers controlled 44.12% of the Canada data center cooling market in 2025 and are expanding at a 23.4% CAGR as their AI clusters demand efficient thermal removal at 300 kW racks. The Canada data center cooling market size for hyperscalers is expected to cross USD 0.57 billion by 2031, reflecting deep investment by cloud majors. Economies of scale justify early adoption of immersion and direct-chip cooling, demonstrated by Bell’s AI Fabric sites in British Columbia where high-density pods rely on closed-loop dielectric fluids.

Enterprise and edge operators, typically confined to budgets dictated by corporate IT, continue to retrofit air frameworks, integrating rear-door heat exchangers only at hotspots. Colocation vendors strike a balance, bundling liquid cooling as an optional premium for AI tenants while standard racks remain on CRAH units. This hybrid model lets eStruxture and Cologix convert whitespace quickly without stranding capital—a practice gaining favor with investors wary of single-tenant exposure

By Tier Type: Reliability Standards Re-shape Redundancy

Tier 3 facilities held 61.45% of the Canada data center cooling market size in 2025, mirroring customer comfort with N+1 redundancy. Tier 4 is the clear growth engine at 22.65% CAGR because sovereign AI, fintech, and federal cloud contracts now specify zero unplanned downtime. The Canada data center cooling market share for Tier 4 projects is forecast to double by 2031 as Montreal AI labs migrate to fully fault-tolerant designs.

Achieving continuous cooling under maintenance windows forces operators to deploy dual liquid circuits or modular immersion tanks backed by standby CRAHs. Vertiv’s CoolPhase Flex, capable of toggling between air and liquid pathways, addresses Tier 4 service-level agreements by preserving uptime during component swap-outs. Tier 1 and Tier 2 sites remain cost-focused, but even here, rising AI inference at the edge is nudging them toward compact CDUs to prevent thermal throttling.

By Cooling Technology: Liquid Systems Accelerate

Air solutions still represent 67.80% of the Canada data center cooling market, led by CRAHs, chilled-water loops, and dry coolers that take advantage of ambient low temperatures. Yet liquid approaches are growing 23.9% annually, signalling a transitional decade. Within liquids, immersion is outpacing direct-chip on a percentage basis, especially for GPU training farms where uniform heat capture is critical. CoolIT’s suite of 50 issued patents underpins local R&D leadership, giving Canadian manufacturing an edge in the global liquid supply chain.

Hybrid plants mixing adiabatic air coolers with rear-door heat exchangers remain prevalent because they defer wholesale retrofits while unlocking partial PUE gains. Operators in Toronto exploit Enwave’s deep-lake cooling to pre-chill CRAH coils, combining inexpensive cold water with localized CDUs for critical zones. Over the forecast horizon, the Canada data center cooling market will witness widespread adoption of secondary-loop refrigerants like propylene glycol to merge air and fluid loops seamlessly.

By Component: Services Climb as Complexity Rises

Equipment still accounts for 80.55% of the Canada data center cooling market, reflecting the heavy capital requirement for chillers, CDUs, and immersion enclosures. Services, however, are rising 22.9% annually, as facility owners outsource integration, training, and predictive maintenance. The Canada data center cooling market share for maintenance and support specifically is set to widen because liquid loops mandate continuous diagnostics to avoid micro-leaks.

OEMs are embedding AI-driven analytics—Vertiv’s Next Predict, Carrier’s QuantumLeap, Schneider’s EcoStruxure—to flag thermal anomalies before failures, feeding an annuity stream in software subscriptions. Consultants skilled in heat-recovery economics are equally busy, advising Quebec campuses on monetizing waste heat for greenhouse agriculture, a practice that shortens payback periods and aligns with provincial mandates.

Geography Analysis

Quebec commands the largest regional share of the Canada data center cooling market owing to 100% renewable hydroelectricity and winter temperatures that allow up to 80% free cooling, translating into PUE below 1.2 at QScale’s Q01 campus QScale.com. Provincial incentives, including utility heat-reuse rebates, underpin 54 active data centers consuming 0.7 TWh in 2021, a figure Hydro-Québec expects to reach 4.2 TWh by 2029. Mandatory heat-recovery clauses for new projects further stimulate demand for plate-and-frame exchangers and low-lift heat pumps.

British Columbia mirrors this renewable profile yet faces stringent municipal water discharge constraints. The Capital Regional District will ban once-through cooling from July 2028, pushing operators toward closed-loop liquids and air economizers. Bell’s Kamloops AI Fabric campus demonstrates compliance by using hydro power plus evaporative adiabatic systems that recirculate grey water. The province’s environmental rigor is spawning innovation in waterless dielectric immersion tanks, a trend expected to uplift the western share of the Canada data center cooling market.

Alberta’s grid draws on natural gas, but the AESO’s phased 1,200 MW connection program has opened room for 90 MW campuses like eStruxture’s CAL-3, making Calgary a new hotspot for GPU colocation. Cooler nights and competitive electricity tariffs help balance higher carbon intensity, while on-site gas turbines paired with absorption chillers appear in design studies. Ontario, centered on Toronto, retains the nation’s highest absolute IT capacity yet faces elevated power prices; Enwave’s deep-lake system mitigates costs by delivering chilled water for CRAH coils, keeping the regional slice of the Canada data center cooling market competitive

Competitive Landscape

The Canada data center cooling market remains moderately fragmented, with global HVAC majors, niche liquid pioneers, and regional integrators vying for share. Vertiv, Schneider Electric, and Johnson Controls supply integrated CRAH-to-CDU portfolios, while CoolIT Systems leverages its Canadian base to iterate fast on immersion and direct-chip modules. Schneider’s USD 850 million Motivair acquisition enlarges its liquid toolkit, and Vertiv’s purchase of BiXin centrifugal chillers strengthens chilled-water offerings for AI racks above 300 kW.

Emerging alliances accelerate innovation. Munters teamed with ZutaCore on dielectric direct-chip loops, and Carrier’s venture arm injected capital into Strategic Thermal Labs, anticipating 30% liquid adoption by 2028. Domestic innovators such as Carnot Refrigeration exploit natural CO₂ refrigerants for free-cooling hybrids, carving a green niche. Software-defined control is an expanding battleground, with Phaidra’s closed-loop optimization engine raising USD 12 million to automate cooling set-points in real time.

Suppliers also race to secure local manufacturing to counter supply-chain risk. Daikin Applied’s USD 121 million plant in Mexico, calibrated for North American data-center chillers, reduces lead times for CRAHs and CDUs. Meanwhile, shortages in dielectric fluids and precision valves drive opportunities for Canadian SMEs, which can step in with localized production. The skill shortage in liquid commissioning grants service specialists premium margins, further fragmenting market share yet underpinning double-digit topline growth for consultants.

Canada Data Center Cooling Industry Leaders

Vertiv Holdings Co.

Schneider Electric SE

Johnson Controls International plc

CoolIT Systems Inc.

Nortek Air Solutions LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bell Canada unveiled six AI data centers in British Columbia totaling 500 MW of hydro-electric compute, launching the first site in Kamloops in June 2025

- April 2025: Vertiv posted Q1 2025 net sales of USD 2,036 million, a 24% rise driven by liquid-cooling AI infrastructure.

- March 2025: Vertiv released a high-density hybrid heat-rejection system tailored for AI loads above 100 kW per rack

- March 2025: Telus began converting its Rimouski facility into Canada’s largest sovereign AI hub, promising 75% lower water use than average AI centers.

- February 2025: Carrier launched QuantumLeap, an integrated cooling and predictive maintenance suite, forecasting a USD 20 billion thermal market by 2029

- December 2024: Vertiv acquired BiXin Energy’s centrifugal chiller technology for AI applications up to 5.5 MW per unit.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Canada's data center cooling market as the yearly value of purpose-built mechanical and liquid systems, chillers, CRAH/CRAC units, dry coolers, immersion or direct-to-chip solutions, installed in server halls to keep inlet temperatures within ASHRAE-recommended ranges.

Scope exclusion: Building-wide HVAC that is not dedicated to IT rooms is excluded.

Segmentation Overview

- By Data Center Type

- Hyperscalers (owned and Leased)

- Enterprise and Edge

- Colocation

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Cooling Technology

- Air-based Cooling

- Chiller and Economizer (DX Systems)

- CRAH

- Cooling Tower (covers direct, indirect and two-stage cooling)

- Others

- Liquid-based Cooling

- Immersion Cooling

- Direct-to-Chip Cooling

- Rear-Door Heat Exchanger

- Air-based Cooling

- By Component

- By Service

- Consulting and Training

- Installation and Deployment

- Maintenance and Support

- By Equipment

- By Service

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility engineers in Toronto, Montreal, and Calgary, plus global cooling equipment product managers and hyperscale procurement leads. These conversations validated average rack loads, winter free-cooling hours, and aspirational PUE targets before we finalized assumptions.

Desk Research

We started with Statistics Canada energy price indices, Environment and Climate Change Canada hourly temperature records, and Natural Resources Canada renewable generation data, which illuminate electricity cost trends and free-cooling potential. Trade associations such as the Uptime Institute and the Canadian Data Centre Association offered rack density benchmarks and planned facility counts. Company 10-Ks, SEDAR filings, and provincial tender portals complemented these figures with project pipeline values. Select paid libraries, D&B Hoovers for supplier revenues and Dow Jones Factiva for deal news, filled historical gaps. This list is illustrative; many additional open and paid references fed our evidence base.

Market-Sizing & Forecasting

A top-down construct began by reconstructing national installed IT floor space from published megawatt capacities, then applying observed average rack density (kW/rack) and equipment ASPs. Supplier roll-ups and channel checks provided a bottom-up sense check, letting us adjust totals where hyperscale self-builds skewed public data. Key variables like hyperscale capex pipeline, winter free-cooling hours, average electricity tariff, and adoption rate of liquid cooling feed a multivariate regression that extends the base to 2030. Data voids, for example in private colocation spend, were bridged with region-weighted proxies drawn from primary interviews.

Data Validation & Update Cycle

Results pass variance checks against independent metrics such as PUE trends and import codes; anomalies trigger analyst rework before sign-off. Reports refresh every twelve months, with interim tweaks when major facility announcements surface.

Why Mordor's Canada Data Center Cooling Baseline Commands Reliability

Published estimates often diverge because firms weigh hyperscale projects differently, apply varied ASP progressions, or roll North American averages into Canada totals.

Key gap drivers include: some studies widen scope to cover facility power gear, others lock forecasts to constant ASPs, while a few update on a three-year cadence. Mordor's page reflects 2024 currency, quarterly project tracking, and clear equipment-only boundaries.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.36 B (2025) | Mordor Intelligence | - |

| USD 2.48 B (2024) | Global Consultancy A | Bundles power infrastructure and uses blended NA ASPs |

| USD 0.33 B (2024) | Regional Consultancy B | Excludes liquid cooling gear, assumes flat ASP decline |

| USD 0.40 B (2023) | Trade Journal C | Updates biennially; pipeline data not cross-checked with operators |

The comparison shows that when scope, refresh cadence, and price curves are normalized, Mordor's disciplined, variable-rich model offers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Canada data center cooling market?

It is valued at USD 0.43 billion in 2026 and is forecast to reach USD 1.05 billion by 2031.

Which segment is growing fastest in the Canada data center cooling market?

Liquid-based cooling technologies are expanding at a 23.9% CAGR thanks to AI rack densities reaching 300 kW.

Why are hyperscalers important to Canada’s cooling landscape?

Hyperscalers hold 44.12% market share and invest heavily in immersion and direct-chip systems, driving overall market growth at 23.4% CAGR.

Hyperscalers hold 44.12% market share and invest heavily in immersion and direct-chip systems, driving overall market growth at 23.4% CAGR.

Carbon pricing and GHG offset credits shorten payback periods for high-efficiency cooling, accelerating adoption of low-GWP refrigerants and heat-recovery systems.

Which provinces offer the strongest advantages for data center cooling?

Quebec and British Columbia lead due to hydroelectric grids and cold climates that allow extensive free cooling and lower PUE values.

What is the biggest restraint facing liquid cooling adoption in Canada?

High upfront CAPEX, often 3–5 times higher than air systems, remains the primary barrier for smaller operators despite energy-savings potential.

Page last updated on: