Calcium Carbide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

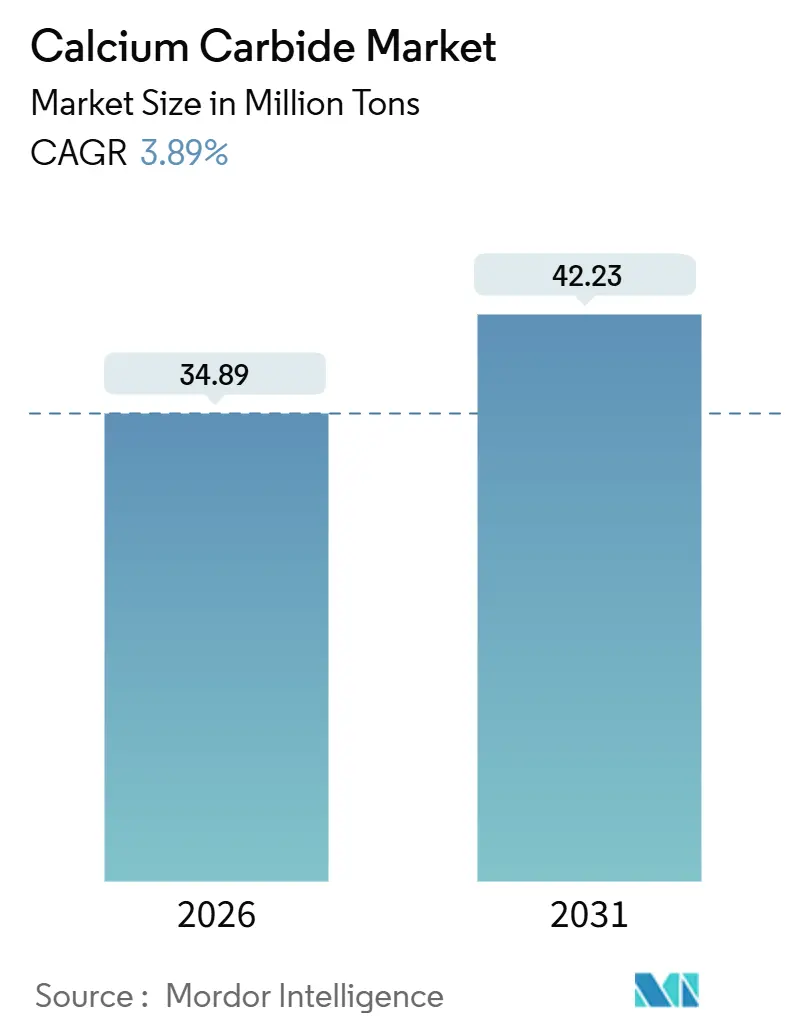

| Market Volume (2026) | 34.89 Million tons |

| Market Volume (2031) | 42.23 Million tons |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

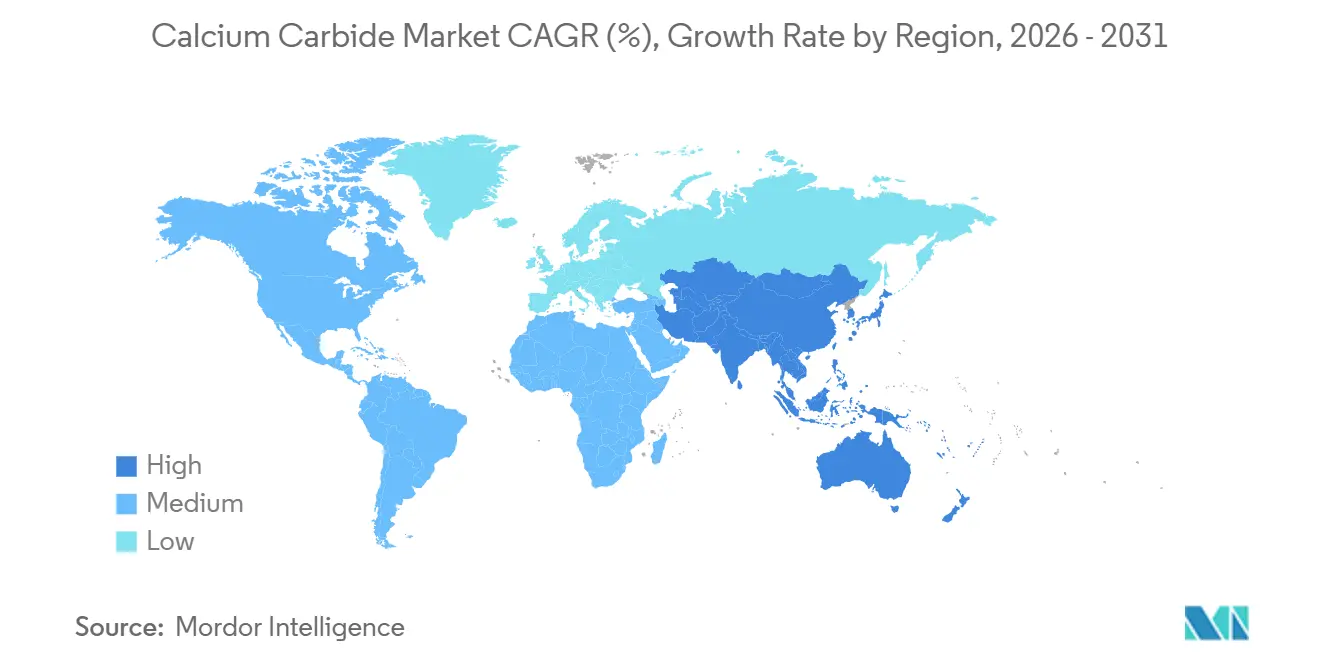

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Carbide Market Analysis by Mordor Intelligence

The Calcium Carbide Market size is estimated at 34.89 million tons in 2026, and is expected to reach 42.23 million tons by 2031, at a CAGR of 3.89% during the forecast period (2026-2031). Asia-Pacific remains the demand anchor, yet China’s 2024-2025 State Council Action Plan is forcing 30% of furnaces to meet stiff energy-efficiency benchmarks, which in turn accelerates capacity rationalization and capital spending on plant upgrades. High-purity grades are expanding faster than lower grades because the acetylene-to-VCM chain, responsible for roughly one-third of global vinyl chloride output, cannot tolerate catalyst-poisoning impurities. Green-chemistry pathways - biochar substitution for petroleum coke, waste-heat recovery, and hydro-powered furnaces in Yunnan and Sichuan - are emerging as cost-advantaged options as China’s carbon dual-control regime tightens. Outside China, India’s push to erase a USD 31 billion chemical trade deficit is positioning localized PVC, calcium cyanamide, and specialty chemicals as the next volume catalysts.

Key Report Takeaways

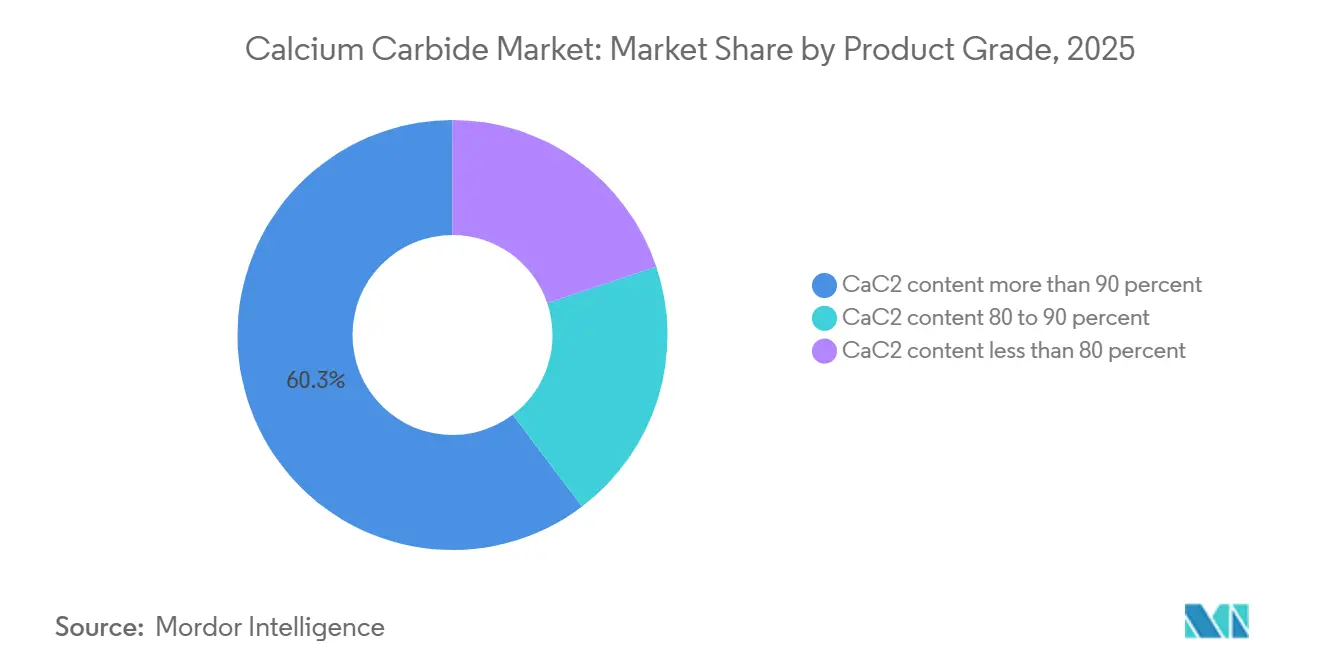

- By product grade, CaC₂ content more than 90% captured 60.29% of the calcium carbide market share in 2025 and is projected to expand at a 4.12% CAGR through 2031.

- By application, acetylene gas generation accounted for 77.15% of the calcium carbide market size in 2025 and is set to grow at a 3.93% CAGR between 2026-2031.

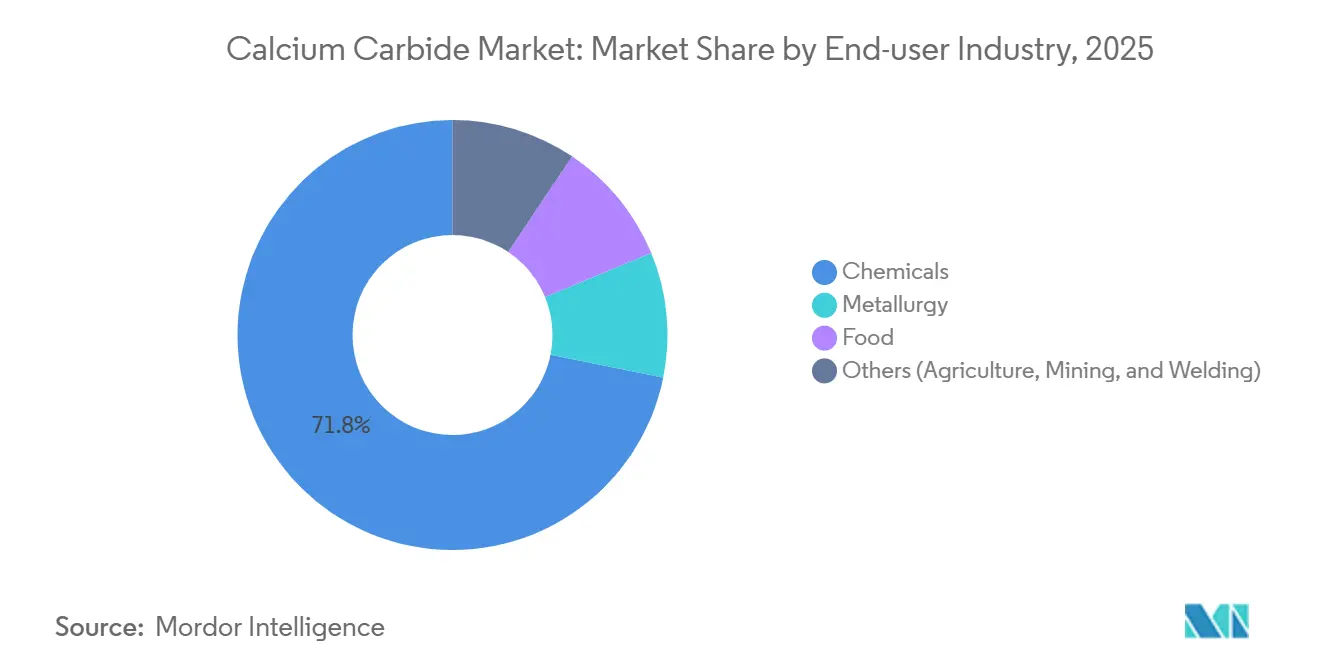

- By end-user industry, chemicals held 71.82% of the calcium carbide market size in 2025, advancing at a 4.02% CAGR to 2031.

- By geography, Asia-Pacific commanded 95.31% of the calcium carbide market share in 2025, with regional volume rising at a 3.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Carbide Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable demand from global steel industry | +0.8% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Rising on-site metal fabrication demand | +0.6% | Asia-Pacific core, North America clusters | Short term (≤ 2 years) |

| Expanding downstream chemical synthesis | +0.9% | China, India, ASEAN | Long term (≥ 4 years) |

| Growing utilization in agriculture | +0.3% | India, Brazil, ASEAN | Medium term (2-4 years) |

| Surge in green CaC₂ production via renewable power | +0.5% | Yunnan, Sichuan, Nordic Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Favorable Demand From Global Steel Industry

Global crude steel output hit 1,884.6 million tons in 2024, providing a stable baseline for desulfurization agents and oxy-acetylene cutting gases[1]World Steel Association, “World Steel in Figures 2025,” worldsteel.org. India’s finished-steel production of 139.153 million tons in 2024 created derivative demand for domestic carbide, especially as the country imported 58.12 million tons of coking coal, raising feedstock costs for coke-intensive industries. China’s shift toward emissions-intensity targets by 2025 will penalize inefficient furnaces and consolidate supply among plants able to finance energy-saving retrofits.

Rising On-Site Metal Fabrication Demand

Acetylene’s 3,100°C flame keeps it irreplaceable for pipeline repair and shipyard fabrication in regions where electric arc systems are impractical[2]OSHA, “Acetylene Standard 1910.102,” osha.gov. Safety mandates under OSHA and the US EPA raise compliance costs, encouraging large industrial users with ISO 45001 certification to lock in long-term supply contracts, while small workshops migrate to propane or HHO, fragmenting demand.

Expanding Downstream Chemical Synthesis

China still relies on coal-based acetylene for about 50% of PVC production, even though feedstock at USD 12 per kilogram represents 43% of VCM raw-material costs, exposing producers to carbon-pricing risk. India's NITI Aayog roadmap (July 2025) targets the reduction of the USD 31 billion chemical trade deficit toward net-zero by 2030, proposing chemical hubs, opex subsidies, and fast-track environmental clearances to localize PVC and specialty-chemical production. Calcium cyanamide (CaCN₂), produced by reacting CaC₂ with nitrogen at high temperature, contains 19-21% nitrogen and serves as a slow-release fertilizer, soil disinfectant, and precursor for dicyandiamide and melamine.

Growing Utilization in Agriculture

Calcium cyanamide's dual function as a nitrogen source and biocide positions it for specialty applications in high-value crops and contaminated-soil remediation, where conventional fertilizers fail to address pathogen loads. The compound's slow hydrolysis in soil releases cyanamide, which inhibits nitrification and extends nitrogen availability, reducing leaching losses by 44-51% in peer-reviewed field trials. India's Union Budget 2025-26 allocated INR 161,965 crore (USD 18.7 billion) to the Ministry of Chemicals & Fertilizers, signaling policy support for domestic specialty-fertilizer production. ASEAN's industrial energy demand is projected to rise from approximately 10 exajoules in 2023 to 16 exajoules by 2050, with coal remaining 44% of energy-intensive industries, which could support carbide-cyanamide integration if carbon capture and utilization systems (CCUS) are deployed.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and safety hazards of CaC₂ handling | -0.4% | South Asia, parts of Africa | Short term (≤ 2 years) |

| Stringent environmental regulations on carbide furnaces | -0.7% | China, EU, North America | Medium term (2-4 years) |

| Availability of alternate welding and cutting gases | -0.3% | North America, Europe, advanced ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health And Safety Hazards Of CaC₂ Handling

Calcium carbide's violent reaction with moisture, liberating flammable acetylene gas and heat, creates acute risks in storage, transport, and end-use settings, prompting the European Union's REACH framework to classify it as H260 (releases flammable gas on contact with water) and Skin Corr. 1B. The U.S. Department of Transportation classifies CaC₂ as UN 1402, Class 4.3 (dangerous when wet), requiring specialized packaging, moisture-proof containers, and hazmat-certified carriers, which raises logistics costs by an estimated 15-20% versus non-hazardous chemicals.

Stringent Environmental Regulations On Carbide Furnaces

China's State Council Action Plan for Energy Conservation and Carbon Reduction (2024-2025) explicitly lists calcium carbide among industries whose new production capacity will be strictly controlled, mandating that new or expanded CaC₂ projects meet energy-efficiency benchmark levels and environmental performance at an A level. By end-2025, over 30% of CaC₂ capacity must exceed energy-efficiency benchmarks; sub-benchmark capacity must complete technical transformation or face elimination. The European Union's Carbon Border Adjustment Mechanism (CBAM) will impose tariffs on carbon-intensive imports starting in 2026, affecting CaC₂ shipments from non-EU producers unless they demonstrate equivalent carbon pricing or adopt CCUS.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Premium Purity Drives Acetylene Economics

High-purity grades in which CaC₂ content is more than 90% secured 60.29% of the 2025 volume, and their 4.12% CAGR underpins the largest share of the calcium carbide market size because acetylene-to-VCM producers demand low-impurity feedstock to protect catalysts. Biochar substitution and process-control upgrades enable compliant plants to maintain more than 90% CaC₂ content, supporting premium pricing. Lower purity grades face shrinking outlets after India’s 2024 ripening ban and tighter food-contact rules.

Process simulations show that producing 220.7 tons of VCM needs 85.3 tons of high-purity CaC₂, so any impurity spike directly erodes plant margins. As MIIT’s February 2024 guidance pushes coal-to-chemicals toward cleaner feedstocks, integrated producers with ISO 9001 quality systems are well placed to capture long-term contracts, while legacy furnaces without retrofit capital face exit barriers.

By Application: Acetylene Rule Persists But Substitution Looms

Acetylene gas accounted for 77.15% of demand in 2025, retaining the largest share of the calcium carbide market despite environmental scrutiny. Moreover, this share is expected to grow with the fastest CAGR of 3.93% during the forecast period (2026-2031). Ethylene-based PVC routes are gaining share wherever cheap natural gas is available, meaning carbide-centric chains must cut carbon intensity or lose competitiveness.

Calcium cyanamide occupies a smaller but higher-margin niche in specialty fertilizers and dicyandiamide intermediates, sustained by agronomic proof of reduced nitrogen leaching. Metallurgical, reducing, and dehydrating uses add diversity but remain tied to steel-cycle volatility, while lamp carbide and acetylene black are exposed to rapid material-science shifts favoring graphene and CNTs.

By End-User Industry: Chemicals Lock-In Versus Metallurgy Cycles

Chemicals commanded 71.82% of 2025 volume and a 4.02% CAGR, underpinned by India’s USD 1 trillion 2040 chemical ambition and China’s massive VCM base. The calcium carbide market share concentration in chemicals binds suppliers to the regulatory trajectory of PVC and specialty intermediates, increasing sensitivity to carbon-pricing shocks.

Metallurgy offers counter-cyclical balance, but over 600 million tons of global steel overcapacity constrains upside. Food applications have shriveled post-FSSAI ban, leaving niche agricultural remediation and mining explosives as the primary other uses. Geographic co-location of carbide and cyanamide plants near hydropower sites may emerge as a strategic hedge against fossil-energy volatility.

Geography Analysis

Asia-Pacific held 95.31% of the 2025 volume and is expected to post a 3.91% CAGR through 2031 as China’s Coal Triangle pivots toward low-carbon upgrades totaling CNY 437.3 billion by 2030. India’s chemical expansion, backed by port-linked clusters and production-linked incentives, creates a second growth pole for the calcium carbide market. Japan and South Korea cater to electronics-grade acetylene black, while ASEAN’s USD 226 billion 2024 FDI inflows foreshadow rising specialty-chemical demand, albeit with feedstock cost pressure as industrial energy use climbs to 16 exajoules by 2050.

North America and Europe grow slowly because REACH and OSHA compliance add cost layers absent in the Asia-Pacific. The EU’s CBAM will further reshape trade when carbon tariffs on carbide begin in 2026. South America relies on imports for agriculture and mining, while the Middle East and Africa remain nascent due to limited lime and coke integration outside South Africa and Saudi Arabia.

Competitive Landscape

The Calcium Carbide market is moderately consolidated. A significant amount of global capacity sits with five Chinese producers located near coal and lime reserves, signaling moderate concentration for the calcium carbide market. Inner Mongolia Baiyanhu Chemical and Ningxia Jinyuyuan Chemical are shutting inefficient furnaces to meet State Council energy targets, while Xinjiang Tianye Group is investing in mercury-free acetylene hydrochlorination. Strategic themes include vertical integration, biochar feedstock adoption, and CCUS-ready furnace retrofits aimed at dodging EU CBAM tariffs.

Calcium Carbide Industry Leaders

Inner Mongolia Baiyanhu Chemical Co Ltd

Ningxia Jinyuyuan Chemical Group Co., Ltd.

Xinjiang Zhongtai Chemical Co., Ltd.

Alzchem Group AG

Ningxia Yinglite Chemical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: High electricity tariffs forced Kazakhstan's Temirtau ElectroMetallurgical Plant JSC (TEMP), the sole calcium carbide producer in the CIS (Commonwealth of Independent States), to halt its operations. The plant has remained inactive since March 2025, leading to the idling of a carbide furnace and staff layoffs, with only auxiliary workshops still in operation.

- February 2025: The Lahore High Court cleared the transfer of Ghani Chemical Industries’ calcium carbide project to subsidiary Ghani ChemWorld Limited, enabling dedicated operations at Hattar Special Economic Zone.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the calcium carbide market as the annual production and trade of technical-grade CaC₂ supplied from new electric-arc furnaces for direct sale to end-users that generate acetylene, calcium cyanamide, or employ the compound in steel desulfurization. According to Mordor Intelligence, the addressable pool amounted to 34.51 million tons in 2025, tracked in metric-ton units rather than revenue.

Scope exclusion: recycled carbide fines and downstream acetylene derivatives are kept outside the boundary to avoid double counting.

Segmentation Overview

- By Product Grade

- CaC₂ Content More Than 90%

- CaC₂ Content 80–90%

- CaC₂ Content Less Than 80%

- By Application

- Acetylene Gas

- Calcium Cyanamide

- Reducing and Dehydrating Agent

- Desulfurizing and Deoxidizing Agent

- Others (Ripening, PVC and Acetylene Black, Lamps, etc.)

- By End-user Industry

- Chemicals

- Metallurgy

- Food

- Others (Agriculture, Mining, Welding)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with operators of carbide furnaces across China, India, Norway, and Kazakhstan, distributors that supply welding gases and metallurgical agents, as well as regional regulators overseeing coal-based emissions. These discussions confirmed utilization rates, average selling prices, and emerging quality requirements, filling gaps left by desk material and guiding assumption ranges.

Desk Research

We began with national statistics such as UN Comtrade shipment codes, China National Bureau of Statistics' ferroalloy output, the World Steel Association crude-steel tables, and customs bulletins from India and Vietnam that reveal import parity prices. Trade-association papers from the European Industrial Gases Association, peer-reviewed journals on acetylene chemistry, and patent families mined via Questel added insight on technology shifts. Company 10-Ks, investor decks, and regional press briefings fleshed out capacity additions. Paid sources like D&B Hoovers supported plant-level financial sanity checks. The sources mentioned are illustrative, and many further publications helped data gathering and validation.

Market-Sizing & Forecasting

A top-down production and trade reconstruction sets the baseline: national furnace capacity, reported run rates, import-export balances, and average conversion losses yield apparent domestic supply, which is then balanced against end-use demand pools. Select bottom-up spot checks, plant roll-ups, and dealer channel volumes calibrate the totals. Key drivers include coal price parity, acetylene PVC capacity additions, regional crude-steel output, fertilizer demand for calcium cyanamide, and prevailing carbide yield coefficients. Forecasts apply multivariate regression blended with scenario analysis so that macro indicators such as steel intensity per capita and PVC buildouts anchor growth, while expert interviews provide variable-level consensus.

Data Validation & Update Cycle

Model outputs pass variance checks against independent trade statistics and price indices. Senior reviewers scrutinize anomalies before sign-off, and the report is refreshed every twelve months, with interim updates when material events, policy shifts, or plant outages arise. A final analyst pass ensures clients receive the latest view.

Why Mordor's Calcium Carbide Baseline Earns Decision-Makers' Trust

Published figures often diverge because providers choose different units, include ancillary products, or fix exchange rates differently.

We stick to physical tonnage, align scope tightly with furnace output, and revisit assumptions annually, which keeps our baseline transparent and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 34.51 million tons (2025) | Mordor Intelligence | - |

| USD 16.6 billion (2024) | Global Consultancy A | Converts revenue using fixed ASP, bundles acetylene derivatives, no reconciliation with customs tonnage |

| USD 17.6 billion (2024) | Industry Association B | Relies on reported sales from large firms, omits unorganized Asian capacity |

| USD 16.75 billion (2024) | Regional Consultancy C | Applies spot currency rates and single growth scenario, lacks trade-flow cross-checks |

The comparison shows that volume-based scoping, multi-source triangulation, and scheduled refreshes enable Mordor Intelligence to deliver a dependable, middle-path baseline that executives can trace back to clear variables and replicate with confidence.

Key Questions Answered in the Report

How big is the calcium carbide market in 2026?

The calcium carbide market size reached 34.89 million tons in 2026 and is forecast to grow to 42.23 million tons by 2031.

What is the main growth driver for calcium carbide demand?

Expansion of downstream PVC and specialty chemicals, especially in China and India, is the primary volume driver.

Why are high-purity carbide grades gaining share?

Acetylene-to-VCM producers require more than 90% CaC₂ to protect catalysts, which sustains premium-grade demand and pricing.

How will environmental policy affect carbide producers?

China’s energy-benchmark mandates and the EU’s CBAM carbon tariffs are forcing furnaces to retrofit, adopt biochar, or exit.

Which regions offer the lowest-cost carbide production?

Which regions offer the lowest-cost carbide production?

Page last updated on: