Aircraft Cabin Interior Composite Parts Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

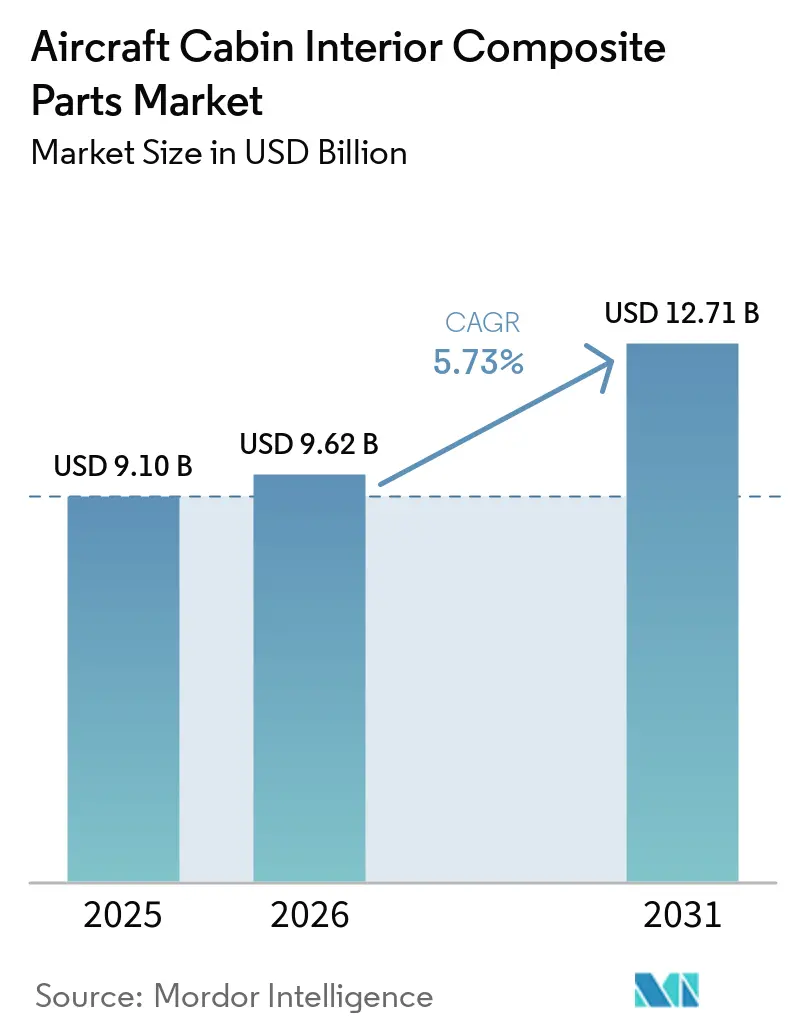

| Market Size (2026) | USD 9.62 Billion |

| Market Size (2031) | USD 12.71 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

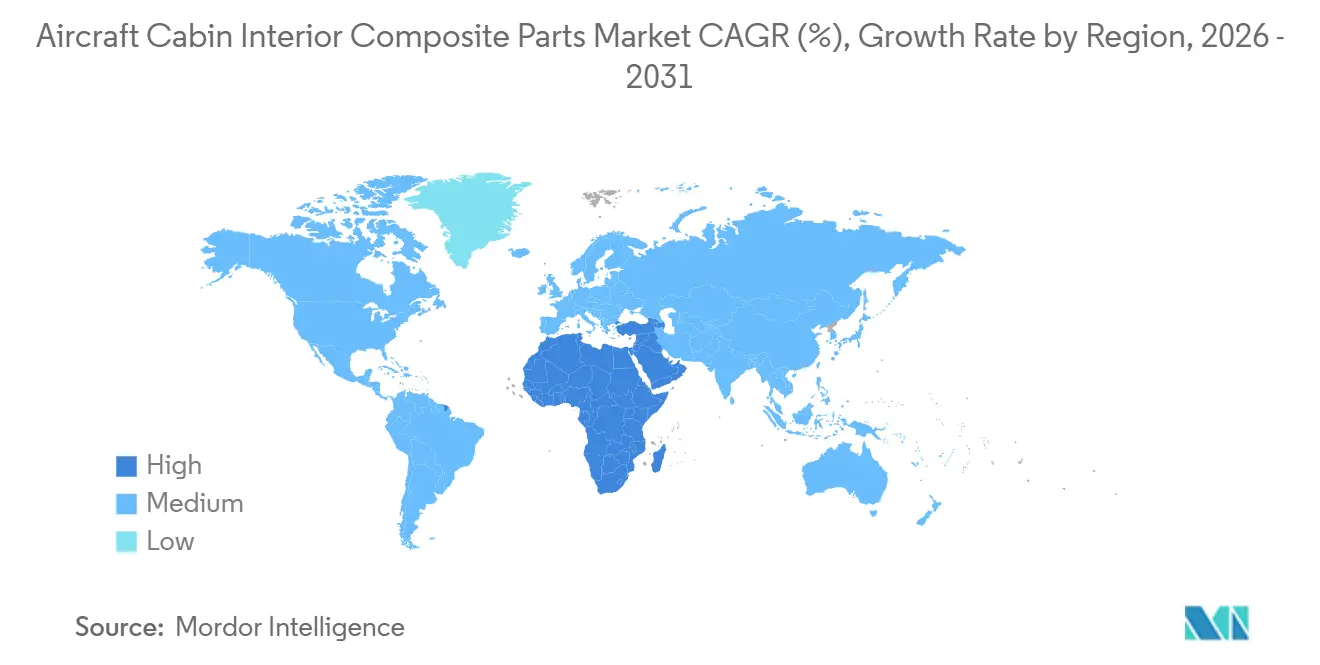

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Cabin Interior Composite Parts Market Analysis by Mordor Intelligence

The aircraft cabin interior composite parts market size is expected to grow from USD 9.10 billion in 2025 to USD 9.62 billion in 2026 and is forecasted to reach USD 12.71 billion by 2031 at a 5.73% CAGR over 2026-2031. Growth relies on increasing single-aisle output, sustaining narrowbody retrofit programs, and expanding the use of carbon-fiber-reinforced polymers and high-performance thermoplastics, which reduces cabin weight by 15-25% and results in a 3-5% lower fuel burn per flight hour. Suppliers that control both prepreg production and part fabrication are positioned to widen margins as Chinese carbon-fiber overcapacity holds raw-material prices in check. Automated fiber-placement equipment reducing panel turnaround time by up to eightfold, recycled-carbon initiatives targeting 20-30% reclaimed fiber by 2030, and stricter fire-smoke-toxicity (FST) regulations that favor phenolic and thermoplastic matrices round out the fundamental demand drivers. Amid these dynamics, supply-chain bottlenecks, particularly shortages of AFP programmers and thermoplastic welding technicians, continue to constrain capacity and lengthen lead times in North America and Europe.

Key Report Takeaways

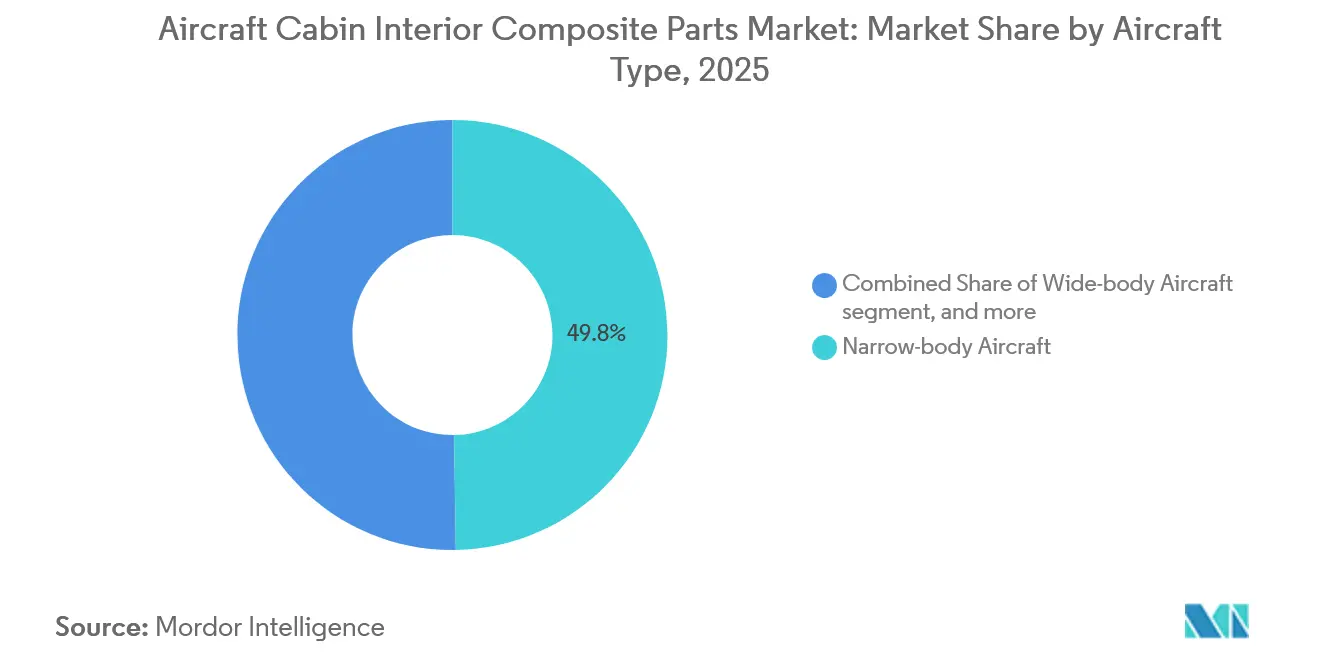

- By aircraft type, narrowbody platforms led with a 49.75% share of the aircraft cabin interior composite parts market in 2025, while business jets are forecast to post a 6.75% CAGR through 2031.

- By component, seating structures accounted for 30.20% of the revenue in 2025, whereas overhead stowage bins are projected to expand at a 7.55% CAGR through 2031.

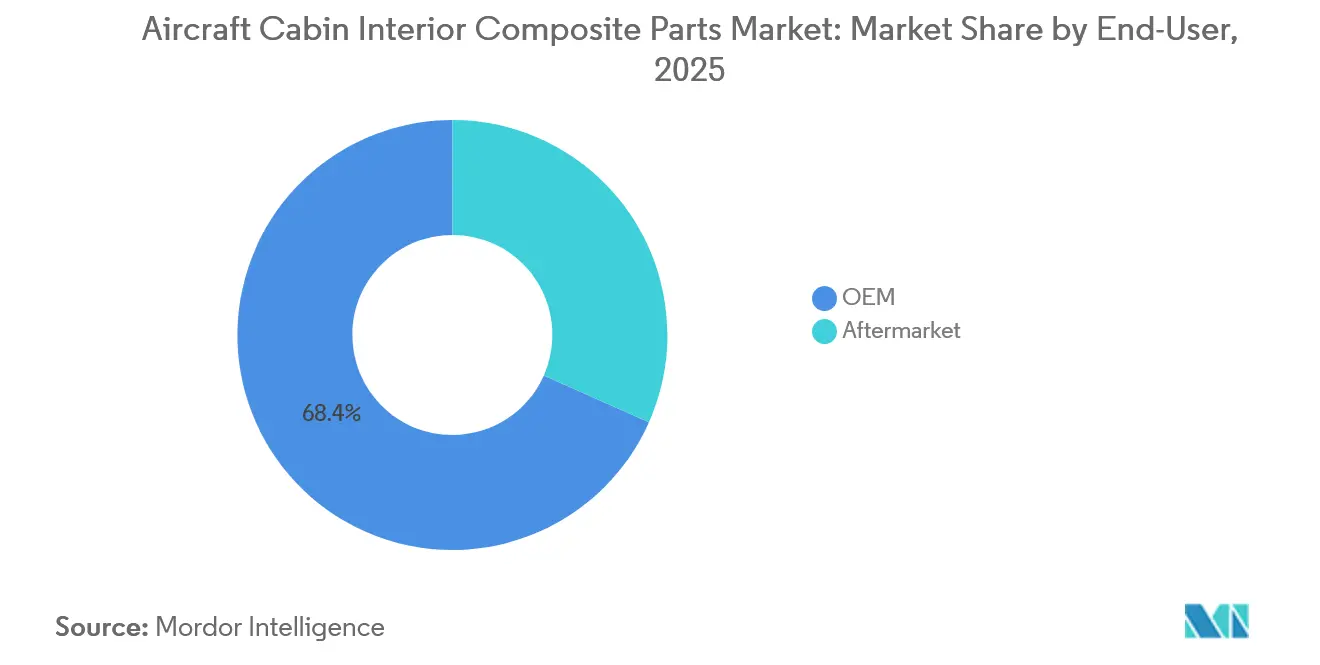

- By end-user, OEM channels accounted for 68.35% of shipments in 2025; however, the aftermarket is projected to grow at a 7.32% CAGR through 2031 as widebody fleets reach their retrofit age.

- By geography, the Asia-Pacific region accounted for 35.45% of demand in 2025; the Middle East and Africa region is forecast to grow at 7.10% from 2026 to 2031, driven by B777X deliveries and investments under Vision 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Cabin Interior Composite Parts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ramp-up of single-aisle production (A320neo/B737 MAX) | +1.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Automated fiber-placement (AFP) slashing panel TAT | +1.2% | North America, Europe, expanding Asia-Pacific | Short term (≤ 2 years) |

| Airline demand for lightweight cabins to cut fuel burn | +1.5% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Stricter FST (fire-smoke-toxicity) regulations | +0.9% | Global, led by EASA and FAA | Medium term (2-4 years) |

| Closed-loop recycled-carbon programs for sidewalls | +0.6% | Europe, North America, pilot Asia-Pacific | Long term (≥ 4 years) |

| Hydrogen-electric demonstrators requiring cryogenic-ready cabins | +0.4% | Europe with global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ramp-Up of Single-Aisle Production Drives Composite Panel Demand

Airbus aims to build 75 A320neo units each month by 2027, while Boeing is restoring B737 MAX output to pre-grounding levels, pushing ship-set demand for composite sidewalls, ceiling liners, and galley monuments higher.[1]Source: Airbus, “A320 Family,” AIRBUS.COMA narrowbody cabin consumes 120-150 square meters of composite surface, and every increase in production rate tightens the supply of aerospace-grade prepregs, forcing OEMs to qualify additional Tier 2 panel fabricators. Suppliers respond by expanding AFP capacity; Spirit AeroSystems raised throughput 30% at its Belfast plant in 2025 to keep pace with A220 fuselage deliveries.[2]Source: Spirit AeroSystems, “Composite Manufacturing Capabilities,” SPIRITAERO.COM Higher volumes amplify cost-reduction pressure, compelling fabricators to automate layup and explore recycled fibers to sustain margins.

Automated Fiber Placement Slashes Turnaround Time and Unlocks Complexity

Electroimpact’s AFP 4.0 platform reached 50.8 meters per minute layup rates in 2025, shrinking sidewall cycle times from 8 hours to under 90 minutes and enabling same-shift curing.[3]Source: Electroimpact, “Automated Fiber Placement Systems,” ELECTROIMPACT.COM The resulting four- to eight-fold productivity gain supports profitable bids on complex parts, such as contoured lavatory shells, that were previously hand-laid. FACC’s Airspace XL overhead-bin contract leverages AFP to hold dimensional tolerances within ±0.5 mm over two-meter spans, precision that manual methods cannot match. Although adoption began in North America and Europe, where labor costs exceed USD 40 per hour, award-winning thermoplastic-AFP projects in Japan show that the Asia-Pacific region is closing the automation gap.

Airline Demand for Lightweight Cabins Intensifies Amid Rising SAF Costs

A composite-rich A350 structure saves 20 tons compared to metal alternatives and reduces fuel burn by 20-25% per flight hour. With sustainable aviation fuel costing two to three times that of conventional Jet A-1, carriers prioritize cabin weight reduction to defend their margins. Emirates’ planned August 2026 retrofit of 60 A380s and 51 B777s will reduce weight by 300 kg per aircraft by installing composite premium economy seats and galley modules. Each kilogram trimmed avoids roughly 3,000 kg of CO2 over a 12-year life, aligning with EU ETS compliance goals. Composite structure aircraft seating, already 30.20% of the component mix in 2025, benefits from Safran’s 2-3 kg lighter carbon-fiber seat frames and the supplier’s new Dubai factory, scheduled to start operating in 2027.

Closed-Loop Recycled-Carbon Programs Gain Momentum in Sidewall Applications

Boeing, Airbus, and MCAM committed in 2025 to reclaim production scrap and end-of-life panels via pyrolysis and mechanical routes, targeting 20-30% recycled content by 2030. Pyrolyzed fiber retains up to 95% of its tensile strength, making it suitable for galley carts and lavatory partitions. In contrast, mechanically recycled fiber serves as a material for compression-molded Class D parts. FACC demonstrated that 25% recycled-carbon panels meet FAA flammability requirements and cost 15-20% less than virgin-fiber alternatives, drawing aftermarket interest. European circular-economy legislation incentivizes adoption, despite pending FAA guidance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of aerospace-grade composites | −0.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Lengthy certification and qualification cycles | −0.7% | North America and Europe | Long term (≥ 4 years) |

| EU chemical-policy volatility disrupting epoxy/phenolic supply | −0.5% | Europe with global ripple effects | Short term (≤ 2 years) |

| Skilled-labor shortages in AFP and thermoplastic welding | −0.6% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Aerospace-Grade Composites Constrains Price-Sensitive Segments

Hexcel’s phenolic prepregs list at USD 80-120 per kg, compared with USD 25-35 per kg for standard epoxy towpregs, a gap that deters regional carriers operating ATR 72-600s or Embraer E2s from adopting composites, despite a 10-15% weight penalty. Overcapacity in China drove T700-grade fiber prices to USD 28 per kg in 2025, but Western airframers are hesitant to qualify low-cost mills due to concerns over traceability. The resulting cost headwind limits penetration in lower-tier aircraft, trimming forecast CAGR by 0.9 percentage points.

Lengthy Certification and Qualification Cycles Delay Time-to-Market

Qualifying a new composite panel requires 18-36 months of fire, smoke, toxicity, and mechanical testing, and each material tweak triggers full retesting under the updated 2025 IATA retrofit guidance. FACC’s A320 luggage-space STC, approved in 2024, still required 14 months despite the use of pre-qualified materials, illustrating the time and cost burden. Smaller fabricators often outsource testing, adding USD 50,000-150,000 per variant, which discourages incremental innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbodies Drive Volume, Business Jets Lead Growth

The aircraft cabin interior composite parts market share for narrowbody programs is 49.75% in 2025 and is poised to expand steadily as Airbus targets 75 A320neo units per month. Each single-aisle cabin consumes up to 150 square meters of composite sidewalls, ceiling panels, and bins, so incremental production adds thousands of square meters of annual demand. Widebodies deploy more composites per frame but progress at slower build rates. A350 deliveries totaled 90 units in 2025, while the B777X entry was pushed back to 2026, resulting in limited near-term volume.

Business jets are forecast to grow at a 6.75% CAGR through 2031, outpacing all other categories as ultra-long-range models like the Global 8000 and G700 rely on composite materials to reach 7,500-plus nautical miles. High cabin customization budgets of USD 5,000-8,000 per square meter enable suppliers such as Bucher and EnCore to recoup investments in AFP and thermoplastic welding, despite lower unit counts. Fractional-ownership programs, which place large multi-year orders, further underpin demand, lifting the segment’s contribution to overall growth.

By Component Type: Seating Dominates Value, Overhead Bins Grow Fastest

Seating structures represented 30.20% of 2025 revenue, led by Safran’s carbon-fiber frames, which save 2-3 kg per unit, and RECARO’s composite pans, which pass 16g testing. Airlines favor lighter seats to offset higher SAF costs and to increase seat counts without breaching weight limits, so seating remains the largest value pool.

Overhead bins are projected to rise at a 7.55% CAGR, the fastest-growing component line, as carriers retrofit pivot-bin designs that increase baggage capacity by 40-67% without adding structural weight. Emirates’ 2026 decision to install composite bins on 60 A380s underscores its appetite for retrofitting, with paybacks tied to faster turnarounds and lower gate-check rates. Floor and ceiling panels, galleys, lavatories, and sidewalls share the remaining value and track aircraft production rather than retrofit cycles.

By End-User: OEMs Retain Majority, Aftermarket Accelerates

OEM channels captured 68.35% of 2025 shipments as Airbus, Boeing, and COMAC integrated composite panels into just-in-sequence final assembly flows, minimizing disruption risk. Suppliers meet annual cost-down targets while gaining predictable volumes and long-term contracts.

Aftermarket demand will climb at a 7.32% CAGR through 2031, supported by nearly 390 A350s reaching the eight-year retrofit trigger by 2028 and wide-scale premium-economy installations across Emirates, Lufthansa, and Delta fleets. Higher margins of 15-20% relative to OEM supply lure new entrants, and STCs for composite pivot bins that can be installed in under nine hours highlight the segment’s rapid payback and lower certification hurdles.

Geography Analysis

Asia-Pacific accounted for 35.45% of 2025 demand as COMAC’s C919 ramped to 50 units, Air India and IndiGo placed record narrowbody orders, and regional labor costs supported cost-competitive composite fabrication. JAMCO’s acquisition of Iacobucci in December 2025 expanded its galley footprint and underlined Japanese suppliers’ push into the European aftermarket. Safran’s evaluation of a Hyderabad panel facility signals broader localization as Indian retrofit work rises.

The Middle East and Africa is expected to be the fastest-growing region, at a 7.10% CAGR through 2031, as Emirates inducts B777X aircraft, Qatar Airways receives A350s, and Saudi Arabia invests in Vision 2030 aviation projects. Safran’s forthcoming 25,000 square-meter Dubai seat plant, due in 2027, exemplifies moves to shorten supply lines and cut 8-12-week logistics legs. Denel Aerostructures’ 2025 contract to build A350 sidewalls illustrates diversification away from defense toward civil composite interiors.

North America and Europe jointly held just over half of global demand in 2025, anchored by Boeing’s Seattle hub, Airbus’s Hamburg and Toulouse lines, and a dense network of Tier 1 suppliers, including Spirit AeroSystems, Diehl, and Triumph. Rising labor costs and REACH chemical rules are pushing fabricators toward AFP automation and thermoplastic matrices, yet proximity to airframers and deep engineering expertise sustain a competitive advantage for complex, high-margin monuments and business-jet interiors.

Competitive Landscape

The market is moderately concentrated. Key market players combine customer-specific design processes with expertise in composite structures, value engineering, and design automation to develop cost-effective, next-generation composite-based aircraft cabin components. JAMCO’s acquisition of Iacobucci in December 2025 expanded its presence in Europe’s retrofit galley-systems market.

Technological innovation plays a critical role in differentiating market leaders. Electroimpact’s AFP 4.0 technology achieves a layup rate of 50.8 m/min, enabling fabricators to competitively bid on high-volume contracts for A320 and B737 aircraft. FACC’s EUR 500 million (USD 589.11 million) Airspace XL bin contract highlights the complexity achievable with AFP technology, which supports premium pricing. JAMCO’s thermoplastic-CFRP welding technology, which reduces part count by up to 30%, is particularly appealing for widebody aircraft monuments and helps address cost concerns amid delays in the B777X program.

Future growth opportunities lie in the ability to certify recycled-carbon sidewalls, thermoplastic lavatories that can be welded in under 10 minutes, and cryogenic-ready liners for hydrogen-powered aircraft. Chinese fiber producers Zhongfu Shenying and Hengshen are pursuing aerospace qualification by offering price discounts of 20-30%. However, concerns about traceability have led Western OEMs to adopt a cautious approach, slowing the penetration of these suppliers into the market.

Aircraft Cabin Interior Composite Parts Industry Leaders

RTX Corporation

FACC AG

Diehl Stiftung & Co. KG

AVIC Cabin Systems (UK) Limited

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Vietjet and AVIC Cabin Systems have inked a detailed cooperation pact focused on aircraft interiors and aviation support. This collaboration signifies a pivotal strategic move for both entities, coinciding with the deepening industrial and technological ties between Vietnam and China.

- September 2025: Axiscades Technologies Limited announced its entry into the aircraft cabin interiors market with two contracts worth USD 1.20 million. This strategic expansion into cabin design, retrofit, and technical solutions highlights the growing demand for advanced interior systems. The move is poised to enhance the cabin composite parts market, driven by increasing modernization needs and the aerospace industry's focus on lightweight, durable materials to improve operational efficiency and passenger experience.

- May 2024: Collins Aerospace (RTX Corporation) introduced its Helix main cabin seat at the Aircraft Interiors Expo in Hamburg, Germany. The seat's lightweight construction, achieved with advanced composite materials, supports fuel efficiency and sustainability goals while enhancing passenger comfort. This development is expected to significantly boost demand for cabin composite parts, as airlines increasingly adopt innovative solutions to optimize operational efficiency and align with environmental and regulatory requirements.

Global Aircraft Cabin Interior Composite Parts Market Report Scope

The aircraft cabin interior composites parts market comprises various players that offer one or more of the following aircraft cabin components: floor, sidewall, and ceiling panels; lavatory panels; overhead stowage bins; seatback panels; ducts; and others.

The scope of the study does not include military aircraft or general aviation aircraft, except for business jets. The market estimates encompass both the linefit and retrofit aspects of the aircraft cabin interior composites parts market. The dominant market players have been selected based on their association with prominent active production commercial aircraft programs.

The aircraft cabin interior composites parts market is segmented by aircraft type, component type, end-user, and geography. By aircraft type, the market is segmented into narrowbody aircraft, widebody aircraft, regional jets, and business jets. By component type, the market is segmented into floor and ceiling panels, sidewall and inners, seating structures, galleys and lavatories, overhead stowage bins, and other interior components. By end-user, the market is segmented into OEM and aftermarket. The report also covers the market sizes and forecasts for the aircraft cabin interior composites parts market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Business Jets |

| Floor and Ceiling Panels |

| Sidewall and Liners |

| Seating Structures |

| Galleys and Lavatories |

| Overhead Stowage Bins |

| Other Interior Component |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Jets | |||

| Business Jets | |||

| By Component Type | Floor and Ceiling Panels | ||

| Sidewall and Liners | |||

| Seating Structures | |||

| Galleys and Lavatories | |||

| Overhead Stowage Bins | |||

| Other Interior Component | |||

| By End-User | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft cabin interior composite parts market in 2026?

The aircraft cabin interior composite parts market stands at USD 9.62 billion in 2026 and is set to grow at a 5.73% CAGR to 2031.

Which aircraft type generates the most composite-interior demand?

Narrowbody programs such as the A320neo and B737 MAX account for 49.75% of 2025 revenue and remain the primary volume driver.

Why are overhead bins the fastest-growing component?

Pivot-bin retrofits raise baggage capacity by up to 67% while holding weight constant, driving a 7.55% CAGR through 2031.

What is driving aftermarket growth?

Nearly 390 A350s will cross the eight-year retrofit mark by 2028, and widebody premium-economy installations deliver high margins for MRO providers.

Which region will see the quickest demand growth?

The Middle East and Africa lead with a projected 7.10% CAGR, thanks to B777X deliveries, A350 orders, and Vision 2030 investments.

Page last updated on: