Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

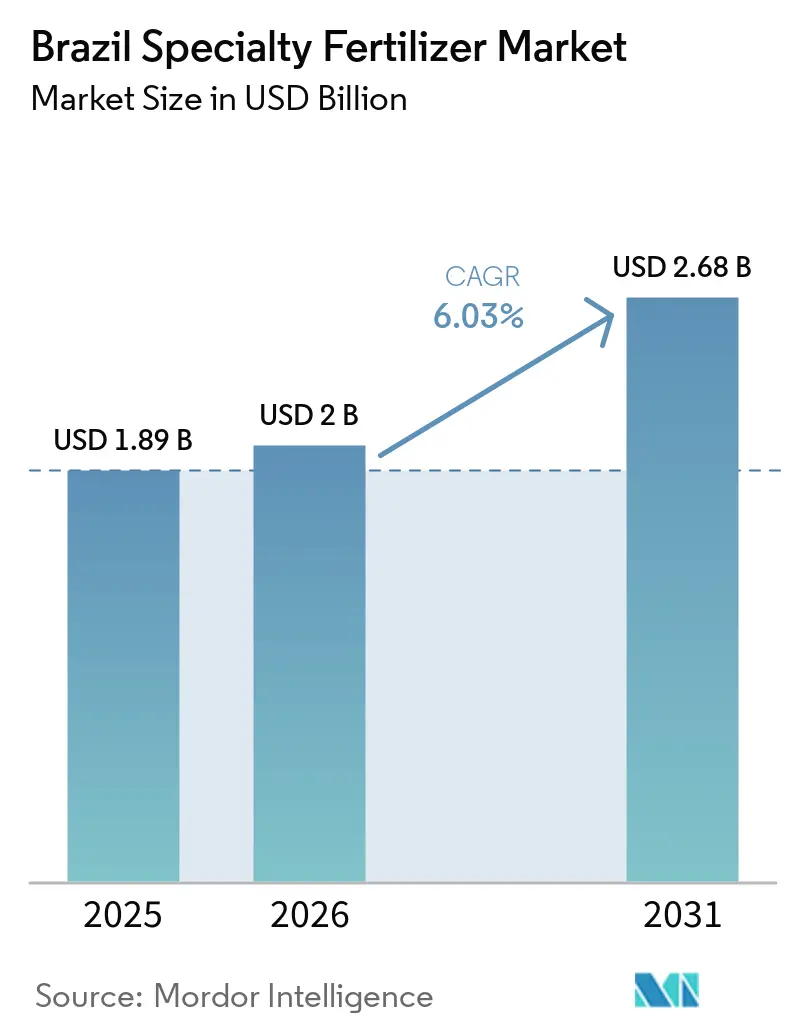

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 2 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

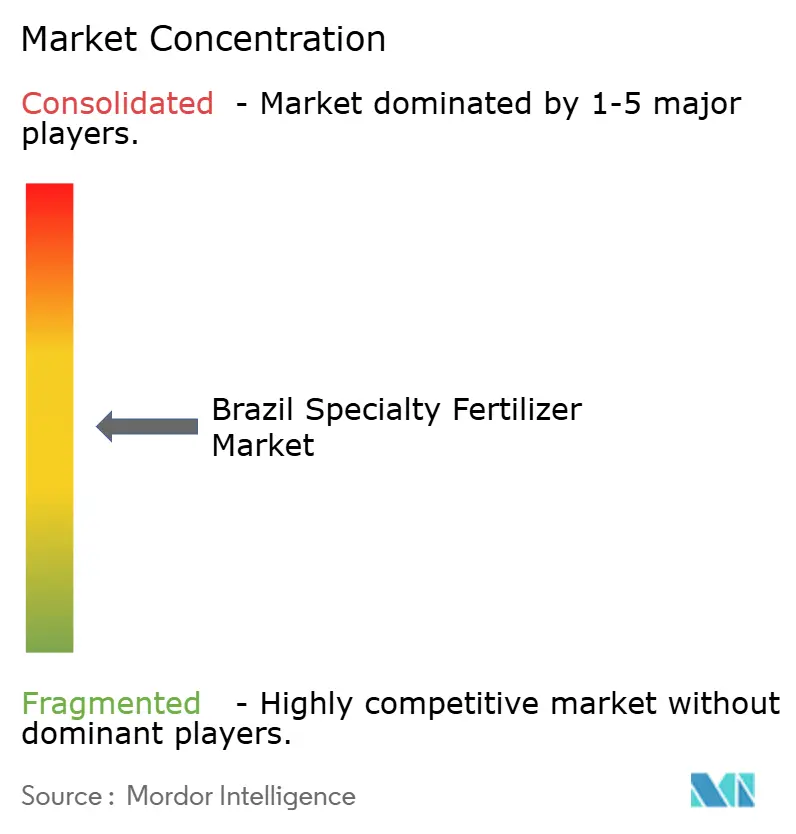

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Specialty Fertilizer Market Analysis by Mordor Intelligence

Brazil specialty fertilizer market size was valued at USD 1.89 billion in 2025 and is estimated to reach USD 2.68 billion by 2031, growing from USD 2.00 billion in 2026 at a CAGR of 6.03% during 2026–2031. This growth trajectory reflects the market's evolution from traditional commodity fertilizers toward precision-engineered solutions that address specific crop nutritional needs and environmental compliance requirements. The market's expansion coincides with Brazil's agricultural modernization drive, where farmers increasingly adopt controlled-release fertilizers and liquid formulations to optimize yield per hectare while meeting stringent environmental regulations. Investments in domestic specialty manufacturing, rural connectivity, and carbon-credit programs further amplify demand while moderating currency-related input risks.

Key Report Takeaways

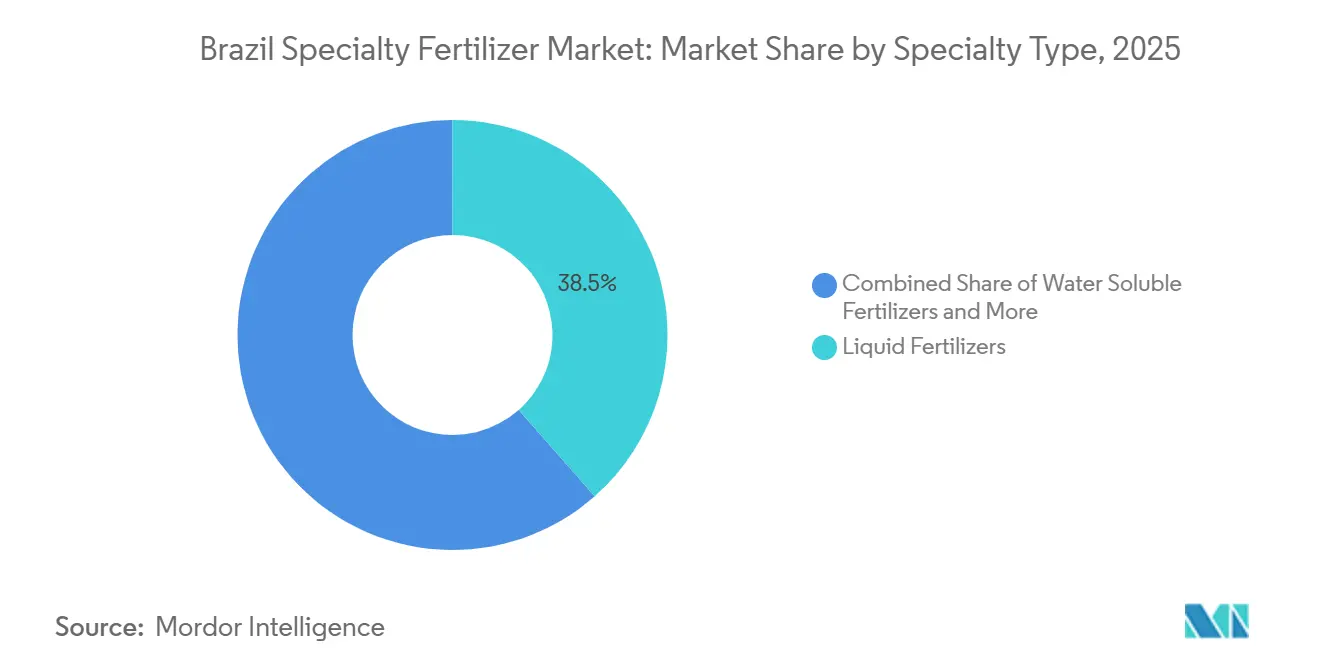

- By specialty type, liquid fertilizers led with a 38.5% revenue share in 2025, whereas controlled-release products are projected to be the fastest-growing type at a 7.4% CAGR through 2031.

- By application mode, fertigation accounted for the largest Brazil specialty fertilizer market share, 54.2%, in 2025 and is also the fastest-growing segment at a CAGR of 6.9% through 2031.

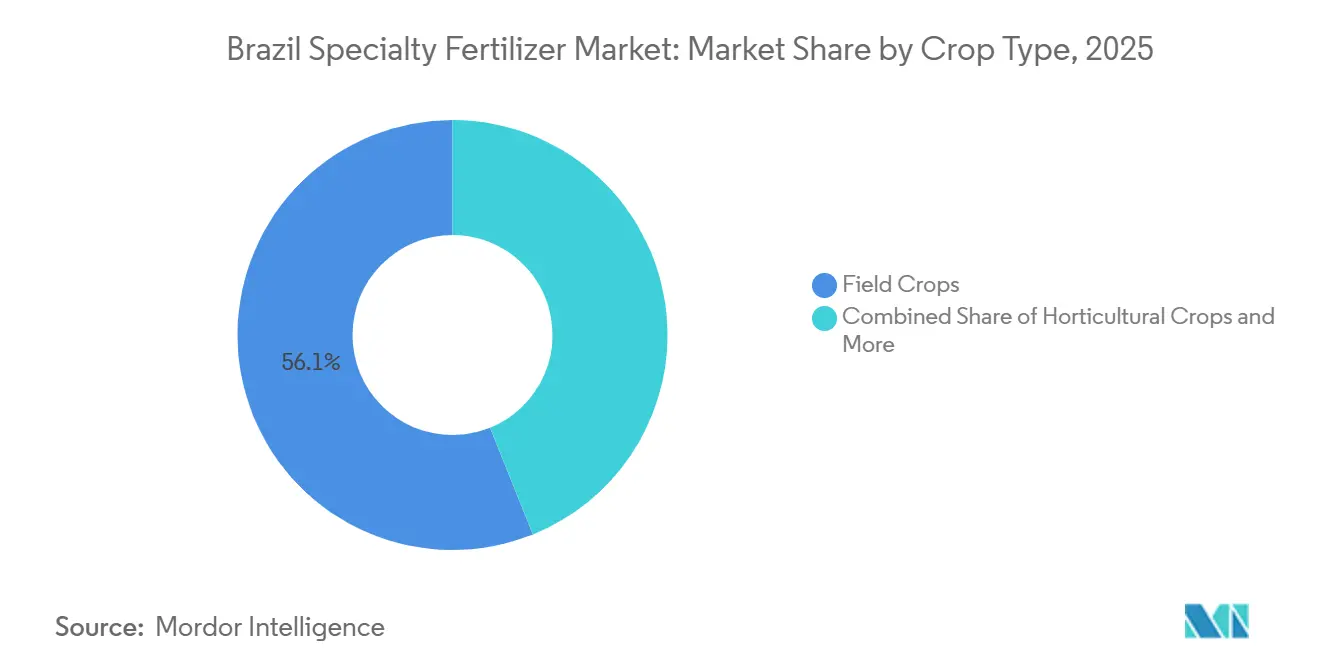

- By crop type, field crops represented the largest Brazil specialty fertilizer market size, contributing 56.1% in 2025, while horticultural crops are projected to be the fastest-growing segment, expanding at a CAGR of 7.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Specialty Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-agriculture adoption boosts demand for high-efficiency inputs | +1.2% | Cerrado, Rio Grande do Sul, Paraná core regions | Medium term (2-4 years) |

| Greenhouse and CEA acreage expansion | +0.8% | São Paulo, Minas Gerais, and Southern states | Short term (≤ 2 years) |

| Stricter nutrient-runoff regulations | +1.0% | National, with early enforcement in water-sensitive areas | Long term (≥ 4 years) |

| Surge in high-value horticulture exports | +0.7% | Export corridors: Santos, Paranaguá, and Itajaí ports | Medium term (2-4 years) |

| Nanocoated nutrient-delivery breakthroughs | +0.9% | Technology adoption centers: São Paulo, Minas Gerais | Long term (≥ 4 years) |

| Carbon-credit schemes rewarding nutrient-use efficiency | +0.6% | Cerrado expansion zones, degraded pasture restoration areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision-Agriculture Adoption Boosts Demand for High-Efficiency Inputs

Brazil's precision agriculture revolution accelerates specialty fertilizer adoption as farmers deploy variable-rate application systems that require precisely formulated inputs to maximize efficiency gains. The country's agricultural connectivity reaches only 30% of arable land currently, but partnerships between equipment manufacturers like John Deere and satellite providers like Starlink promise rapid expansion of precision farming capabilities. The precision agriculture trend particularly benefits specialty fertilizer suppliers offering digital agronomy services and product performance verification, as farmers increasingly demand data-driven proof of input efficiency gains.

Greenhouse and CEA Acreage Expansion

Controlled Environment Agriculture (CEA) expansion in Brazil drives concentrated demand for water-soluble and liquid specialty fertilizers designed for soilless production systems. The country's greenhouse sector benefits from year-round growing conditions and proximity to major urban consumption centers, creating premium market opportunities for specialty fertilizer suppliers. CEA operations require precise nutrient delivery through fertigation systems, making traditional granular fertilizers unsuitable and creating captive demand for specialty liquid formulations. Brazilian greenhouse operators increasingly adopt hydroponic and aeroponic systems that demand ultra-pure, immediately available nutrient solutions, driving specification requirements beyond conventional liquid fertilizer capabilities.

Stricter Nutrient-Runoff Regulations

Brazil's environmental regulatory framework tightens nutrient application standards through enhanced monitoring and enforcement mechanisms that favor enhanced-efficiency fertilizers over conventional products. The Ministry of Agriculture's updated Bio-inputs Law creates clearer pathways for biological and enhanced-efficiency fertilizer registration while imposing stricter environmental impact assessments on conventional products[1]Source: farmonaut, “Brazil's New Law Boosts Sustainable Agriculture with Bio-Inputs,” farmonaut.com. Remote-sensing and watershed testing provide enforcement evidence, so compliance becomes non-negotiable in sensitive basins. Specialized blends with documented release curves therefore gain share.

Surge in High-Value Horticulture Exports

Brazil's expanding horticulture export portfolio drives specialty fertilizer demand as growers optimize crop quality and shelf life to meet international market standards. Export-oriented production systems require precise nutrition management to achieve the appearance, size consistency, and post-harvest durability demanded by international buyers, creating premium market segments for specialty fertilizer suppliers. Export market access requirements, especially for European and North American destinations, necessitate traceability and sustainability documentation. This creates opportunities for specialty fertilizer suppliers that provide comprehensive agronomic support and environmental impact verification services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price premium vs. conventional fertilizers | -1.8% | National, with higher sensitivity in cost-conscious regions | Short term (≤ 2 years) |

| Supply-chain dependence on specialty polymers | -1.1% | Import-dependent regions, port-adjacent areas | Medium term (2-4 years) |

| Farmer skill gap in precision application | -0.9% | Rural areas with limited technical support infrastructure | Medium term (2-4 years) |

| Emerging biologic substitutes cannibalizing micronutrient sales | -0.7% | Technology adoption centers, research-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Premium vs. Conventional Fertilizers

Specialty fertilizers command 20-40% price premiums over conventional alternatives, creating adoption barriers particularly among cost-sensitive farmers operating on thin margins. The premium pricing structure becomes especially challenging during periods of commodity price volatility when farmers prioritize input cost reduction over efficiency gains. Economic pressures intensify during tight credit conditions or unfavorable commodity price cycles, when farmers defer specialty fertilizer adoption in favor of conventional alternatives to preserve cash flow.

Supply-Chain Dependence on Specialty Polymers

Brazil's specialty fertilizer industry relies heavily on imported polymer coating materials and specialty chemical additives, creating supply chain vulnerabilities that affect product availability and pricing stability. The concentration of polymer production in Asia and North America exposes Brazilian specialty fertilizer manufacturers to currency fluctuation risks and international trade disruptions that can significantly impact input costs. The dependency particularly affects controlled-release fertilizer production, where specialized polymer coatings represent significant portions of manufacturing costs and require consistent quality specifications that limit supplier diversification options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Specialty Type: Controlled-Release Fertilizers Lead Innovation

Liquid fertilizers maintain the largest market share at 38.5% in 2025, benefiting from their compatibility with existing fertigation infrastructure and their immediate nutrient availability, which are preferred by intensive cropping systems. Controlled-release fertilizers are the fastest-growing specialty type, with a 7.4% CAGR through 2031, driven by their superior nutrient-use efficiency and reduced application frequency requirements, which appeal to labor-constrained farming operations. Polymer-coated CRF variants dominate the controlled-release segment due to their predictable release profiles and proven field performance, while polymer-sulfur-coated alternatives are gaining traction in sulfur-deficient soils common in Brazil's Cerrado region.

Haifa Group opened the first foreign CRF plant in 2025, signaling external confidence in domestic demand. Nanocoated granules now in pilot-scale testing promise tighter nutrient-uptake alignment and lower coating mass, setting the stage for cost convergence with conventional blends. Water-soluble fertilizers, though niche, underpin intensive greenhouse operations and command premium pricing justified by yield and quality gains.

By Application Mode: Fertigation Infrastructure Drives Liquid Adoption

Fertigation accounted for 54.2% of the Brazil specialty fertilizer market share in 2025, driven by long-term investments in drip and pivot irrigation systems that deliver nutrients directly to root zones with greater precision. It is also anticipated to be the fastest-growing application method, with a projected CAGR of 6.9% through 2031, as growers increasingly combine irrigation and nutrient management to enhance efficiency and productivity.

Soil application remains a significant nutrient-delivery method for large-scale crops such as soybean, corn, and sugarcane, supported by precision spreaders and enhanced-efficiency fertilizer products. Foliar feeding continues to serve as a complementary approach for micronutrient correction and stress mitigation, particularly in citrus and coffee cultivation, further diversifying application practices within the Brazil specialty fertilizer market.

By Crop Type: Field Crops Dominate Despite Diversification

Field crops represented the largest Brazil specialty fertilizer market size, contributing 56.1% in 2025. The extensive cultivation of soybean, corn, and sugarcane in Brazil continues to drive demand for specialty fertilizers. This demand is further supported by advancements in productivity, nutrient-use efficiency, and precision farming practices. Field crops remain the primary consumption base for specialty fertilizer products in the country.

Horticultural crops are projected to be the fastest-growing segment, with a CAGR of 7.1% through 2031. This growth is attributed to the rising demand for premium-quality fruits and vegetables, increased focus on meeting export standards, and the adoption of high-value crop production systems. Although turf and ornamental applications represent a niche segment, they are benefiting from the expansion of urban landscaping and recreational infrastructure projects.

Geography Analysis

Mato Grosso, Rio Grande do Sul, and Paraná collectively consume a major share of specialty volumes thanks to consolidated farm sizes, mechanization, and early digital adoption. Mato Grosso, Brazil’s soybean heartland, shows the highest per-farm expenditure on controlled-release blends as growers seek labor savings and compliance with emerging runoff standards. The Cerrado frontier posts the fastest growth as new cropland incorporation couples precision farming with specialty inputs.

Southern states host the bulk of greenhouse acreage, driving disproportionate demand for water-soluble solutions. São Paulo’s proximity to research institutions fosters rapid nanopolymer trials that will ripple nationwide once cost parity is achieved. Meanwhile, northern arc port improvements improve supply chain access for Acre and Pará growers, positioning these regions as emerging demand nodes for the Brazil specialty fertilizer market.

Connectivity gaps still hamper precision-agriculture and specialty adoption in remote zones, yet public and private initiatives to expand rural broadband target 70% coverage by 2028. Enhanced communication will allow remote diagnostics and variable-rate prescriptions, further embedding specialty products across Brazil’s vast geography.

Competitive Landscape

Brazil's specialty fertilizer market exhibits moderate fragmentation with global players establishing local manufacturing and distribution capabilities through strategic acquisitions and partnerships. The competitive intensity increases as international companies like Indorama acquire specialty additive manufacturers such as Adfert, while established players like Nutrien expand distribution networks through multiple retailer acquisitions, including Marca Agro and Terra Nova.

Market leaders differentiate through technical service capabilities and product customization rather than price competition alone, with companies like OCP Brasil offering bespoke TerraTek formulations tailored to specific soil and crop requirements[3]Source: OCP Brasil, “TerraTek,” ocpbrasil.com.br. The competitive landscape benefits from regulatory clarity provided by MAPA's updated Bio-inputs Law, which creates defined pathways for product registration and market entry.

Ministry of Agriculture and Livestock's (MAPA) clarified bio-input regulations lower entry barriers for biological products, creating adjacent competition yet also partnership prospects for firms bundling microbials with coated nutrients. Distributors respond by enhancing trial networks, evidenced by Staphyt’s expansion, thereby accelerating product validation cycles and farmer confidence.

Brazil Specialty Fertilizer Industry Leaders

K+S Aktiengesellschaft

Sociedad Quimica y Minera de Chile SA

The Mosaic Company

Yara International ASA

ICL Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Adufértil acquired 100% of Fass Agro to strengthen its liquid fertilizer portfolio and expand distribution capabilities in Brazil's growing fertigation market. The acquisition provides Adufértil with specialized liquid formulation capabilities and established customer relationships in high-value crop segments.

- September 2025: Brazil signed a technical cooperation agreement between MAPA and ANDA targeting domestic production of 73 million metric tons of fertilizers by 2036, with specific emphasis on specialty and bioinput segments to reduce import dependency.

- April 2024: Amazone acquired MP AGRO to enhance its fertilizer application technology offerings in Brazil, focusing on precision spreader systems compatible with enhanced-efficiency granular fertilizers. The acquisition strengthens Amazone's position in the growing precision agriculture equipment market.

Brazil Specialty Fertilizer Market Report Scope

The Brazil Specialty Fertilizer Market Report is Segmented by Specialty Type (Controlled-Release Fertilizer (CRF), Slow-Release Fertilizer (SRF), Liquid Fertilizer, and Water Soluble), Application Mode (Fertigation, Foliar, and Soil), and Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Speciality Type

| CRF | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

| Speciality Type | CRF | Polymer Coated |

| Polymer-Sulfur Coated | ||

| Others | ||

| Liquid Fertilizer | ||

| SRF | ||

| Water Soluble | ||

| Application Mode | Fertigation | |

| Foliar | ||

| Soil | ||

| Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf & Ornamental |

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms