Brazil Biofertilizer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

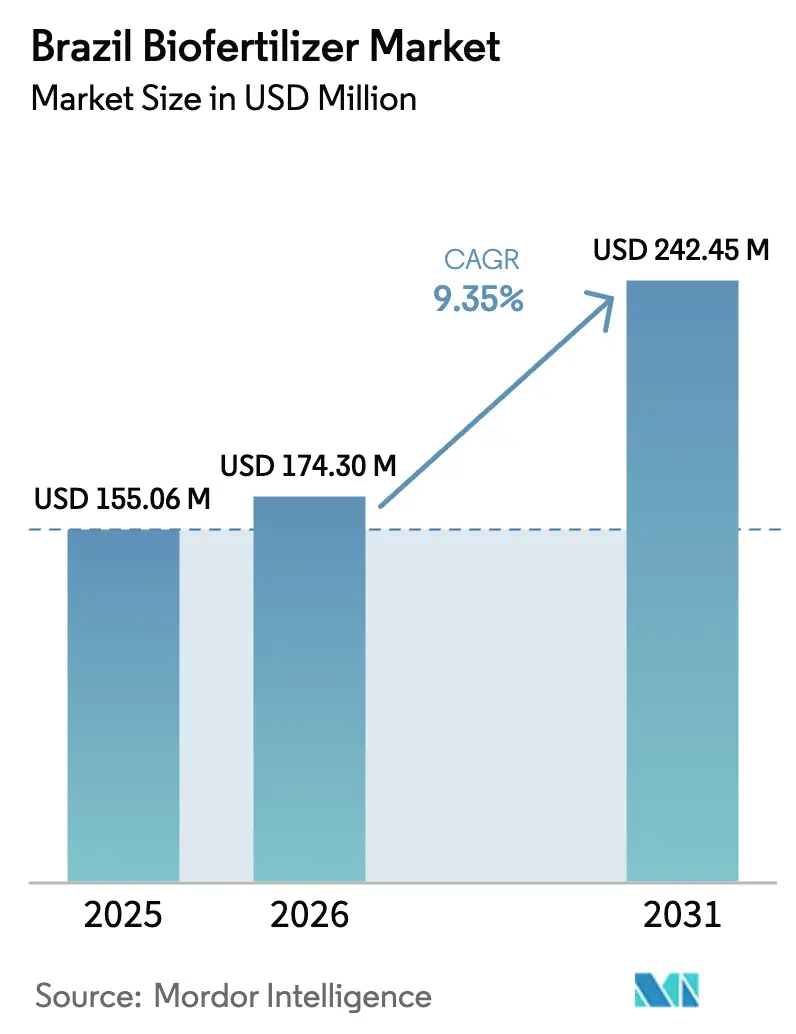

| Base Year Market Size (2025) | USD 155.06 Million |

| Market Size (2026) | USD 174.30 Million |

| Market Size (2031) | USD 242.45 Million |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Biofertilizer Market Analysis by Mordor Intelligence

The Brazil biofertilizer market size was valued at USD 155.06 million in 2025 and estimated to grow from USD 174.30 million in 2026 to reach USD 242.45 billion by 2031, at a CAGR of 9.35% during the forecast period (2026-2031). A surge in soybean acreage, volatile synthetic-nitrogen prices, and policy incentives embedded in the RenovaBio program elevate the Brazil biofertilizer market as a core pillar of crop-input strategies. Rapid microbial-formulation innovation, especially multi-strain consortia, further anchors demand, while on-farm bioreactors are reshaping cost structures for remote Cerrado producers. Carbon-credit premiums linked to verified reductions in greenhouse gas emissions now create an additional revenue stream for adopters, tightening the feedback loop between sustainability metrics and input choice. Although regulatory bottlenecks at the Ministry of Agriculture, Livestock, and Supply slow new-strain approvals, the overall momentum of the Brazil biofertilizer market remains firmly upward.

Key Report Takeaways

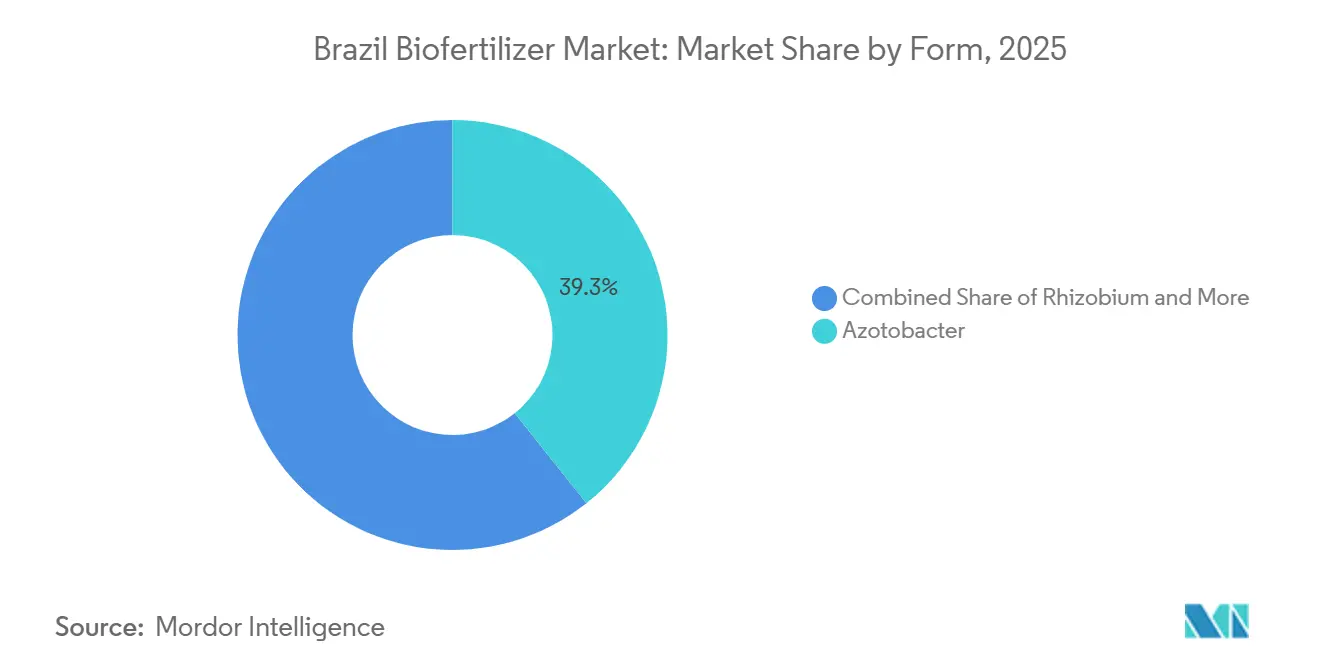

- By form, Azotobacter led with 39.3% of the Brazil biofertilizer market share in 2025, while Rhizobium is projected to advance at an 11.1% CAGR through 2031.

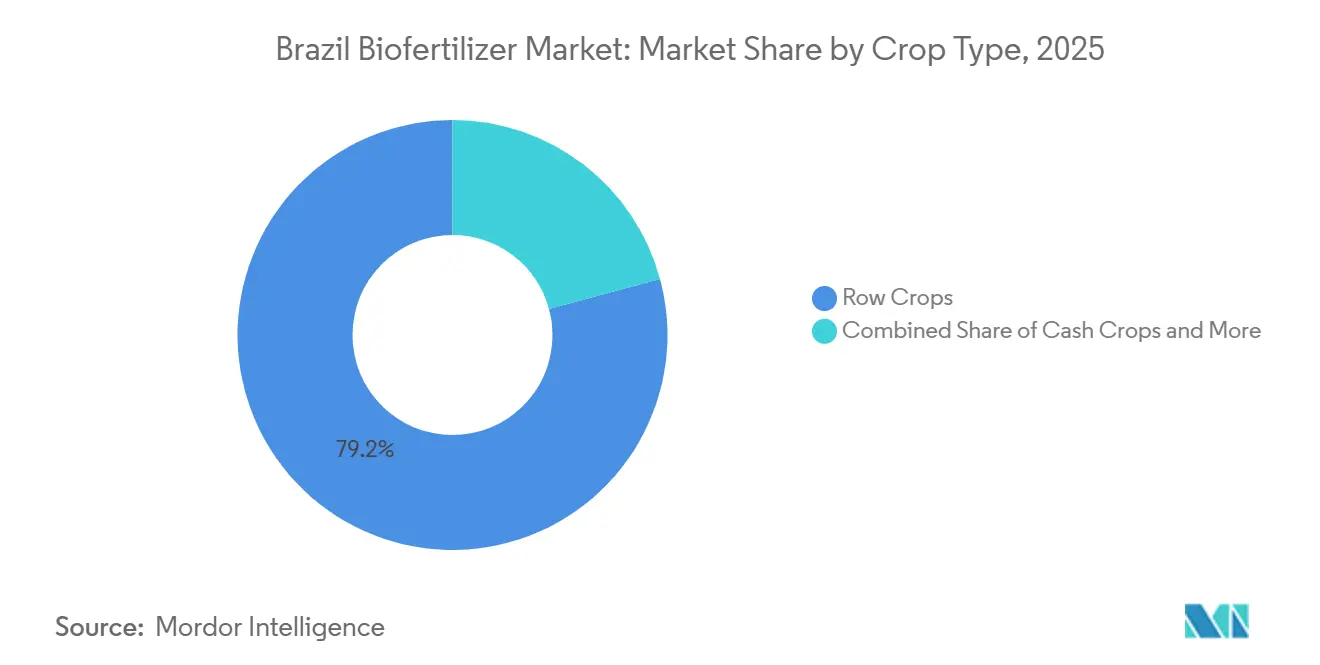

- By crop type, row crops commanded 79.2% of the Brazil biofertilizer market size in 2025, and are poised to expand at a 9.8% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Biofertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption in no-till soybean systems | +2.1% | Global, with peak intensity in South America (Brazil, Argentina, Paraguay) | Medium term (2-4 years) |

| Expansion of RenovaBio biofuel policy | +1.8% | National, with early gains in São Paulo, Goiás, Mato Grosso do Sul | Long term (≥4 years) |

| Government credit lines (PRONAF) favoring biologicals | +1.4% | National, strongest uptake in South and Southeast family-farm regions | Short term (≤2 years) |

| Carbon-credit premiums for biological inputs | +1.6% | Global, with pilot concentration in Cerrado and South Brazil | Medium term (2-4 years) |

| Microbial stacking innovations improving yield stability | +1.9% | Global, with R&D hubs in Brazil, Argentina, United States | Medium term (2-4 years) |

| On-farm bioreactor adoption lowering per-hectare cost | +1.3% | National, early adopters in remote Cerrado municipalities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption in No-Till Soybean Systems

Brazil's no-till acreage dominates soybean cultivation, enhancing inoculant efficacy by preserving soil moisture and microbial habitats[1]. Co-inoculation protocols with Bradyrhizobium japonicum and Azospirillum brasilense deliver significant yield gains and economic returns, driving high adoption rates. The shift to no-till reduces soil disturbance, minimizes oxidative stress on rhizobia, and extends nodulation windows, proving advantageous during erratic rainfall patterns. Large-scale growers in the Cerrado integrate inoculant application into precision-planting workflows, ensuring uniform distribution and reducing skip rates. This integration establishes inoculants as essential agronomic inputs, driving market growth and positioning no-till systems as a key demand driver.

Expansion of RenovaBio Biofuel Policy

Law 15,082/2024, enacted in March 2024, amended the RenovaBio framework to reward biomass producers adopting biological inputs, linking decarbonization credits (CBIOs) to verified reductions in synthetic nitrogen use. Under the revised methodology, sugarcane and soybean growers substituting a portion of nitrogen fertilizer with biological fixation can claim additional CBIOs per ton of feedstock. The National Agency of Petroleum, Natural Gas and Biofuels (ANP) projects significant growth in CBIO issuances as ethanol blending mandates increase nationwide. This policy creates a direct revenue stream that offsets the cost of inoculants and incentivizes early adoption among sugarcane growers in key regions. While the long-term impact depends on multi-year certification cycles for CBIO eligibility, the policy signals a structural shift toward carbon-credit monetization as a core business case for biological inputs.

Government Credit Lines (PRONAF) Favoring Biologicals

The National Program for Strengthening Family Agriculture (PRONAF) allocated substantial funding in the 2024/25 Plano Safra, with preferential interest rates for investments in organic and bioeconomy inputs, including biofertilizers. This subsidy structure shortens the payback period for inoculant adoption for smallholders cultivating smaller farms, a demographic that represents a significant portion of national agricultural output. Family farmers in the South region, where most properties are small-scale, have utilized PRONAF credit to transition from single-strain Rhizobium inoculants to multi-microbe consortia that include PSB and Azospirillum, achieving notable yield gains in corn and soybean rotations during the 2024/25 season. The program's short-term impact timeline stems from its annual disbursement cycle, which provides liquidity during the pre-planting window and enables immediate input procurement, contrasting with longer-term infrastructure or R&D investments.

Emergence of Carbon-Credit Premiums for Biological Inputs

Field trials conducted by Embrapa in 2024 demonstrated that co-inoculation with Bradyrhizobium and Azospirillum significantly reduces greenhouse gas emissions compared to synthetic nitrogen application. This reduction is attributed to avoided nitrous oxide volatilization and lower fossil-fuel consumption in urea production Embrapa. Early-mover farms enrolled in voluntary carbon-credit programs, such as those operated by Indigo Ag and Bayer's Carbon Initiative, captured premiums equivalent to a small percentage of gross crop revenue for soybeans Indigo Ag. The contribution from carbon-credit premiums signals a nascent but high-growth revenue stream that could accelerate as corporate Scope 3 disclosure mandates tighten under emerging ESG (Environmental, Social, and Governance) regulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of strain-specific registration fast-track | -1.2% | National, with acute bottlenecks in novel-microbe approvals | Long term (≥4 years) |

| Seasonal supply-demand mismatches for liquid inoculants | -0.9% | National, peak stress in Cerrado and South during September-November | Short term (≤2 years) |

| Limited cold-chain logistics in North and Northeast | -1.1% | Regional, concentrated in Tocantins, Pará, Maranhão, Piauí (MATOPIBA) | Medium term (2-4 years) |

| Farmer skepticism toward shelf-stable consortia | -0.7% | National, highest among smallholders and first-time adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Strain-Specific Registration Fast-Track

Normative Instruction 61 / 2020 exempts known strains from full toxicology files, but novel microbes still face lengthy approval timelines[2]Source: Ministry of Agriculture and Livestock, “Instrução Normativa 61/2020,” gov.br. However, novel strains and multi-microbe consortia still face lengthy approval timelines involving field efficacy trials, genetic stability assessments, and environmental-impact reviews. These regulatory delays disadvantage Brazilian innovators compared to competitors in other countries, where conditional registrations enable faster commercialization of advanced products. Industry stakeholders highlight that these delays hinder the market's ability to address emerging agronomic challenges, including soybean rust and nematode pressure. The entrenched nature of regulatory processes often requires legislative or ministerial intervention for reforms. There is an urgent need for a fast-track pathway for strains with proven safety records, a reform advocated by industry associations.

Seasonal Supply-Demand Mismatches for Liquid Inoculants

In Brazil, the concentrated soybean planting season creates a significant surge in demand for inoculants, straining manufacturing and distribution capacities. Liquid inoculants dominate the market due to their superior viability and ease of application, but their limited shelf life restricts inventory buildup during off-peak months. Distributors in key regions have reported stock-outs during the peak planting season, forcing growers to delay seeding or use less effective alternatives, both of which can negatively impact yields. Manufacturers are addressing these challenges by expanding production capacities, though the lead times for these expansions remain lengthy. Seasonal bottlenecks persist, but the industry is anticipated to overcome these constraints as supply-chain investments progress and on-farm bioreactor adoption increases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Azotobacter Leadership and Rhizobium Momentum

Azotobacter held 39.3% of Brazil biofertilizer market share in 2025, due to its dual role in nitrogen fixation and phosphate solubilization. The product category enjoys entrenched brand recognition, particularly in Cerrado soils where acidity intensifies phosphate fixation. Rhizobium, buoyed by rising soybean area, posts an 11.1% CAGR during 2026 to 2031, and is often blended with Azotobacter to stabilize field performance. Phosphate-solubilizing bacteria and mycorrhizal segments are trailing but gaining traction in degraded pasture restoration and specialty crop niches. As microbial stacking gains acceptance, formulators increasingly market three-strain packs, lifting average selling prices without eroding farm economics. Shelf-life breakthroughs in encapsulation also extend distribution reach, amplifying the revenue potential of the Brazil biofertilizer market at the formulation level.

Ecosystem collaboration deepens innovation. Advanced formulations now integrate Azotobacter with Rhizobium and phosphate-solubilizing bacteria to create synergistic effects that can increase crop yields by 15-25% compared to single-strain applications. Public-private research programs under Embrapa funnel local strain libraries into commercial pipelines, lowering discovery costs. Coupled with Ministry of Agriculture and Livestock (MAPA’s) new 2024 bioinputs law, which targets six-to-24-month approvals for low-risk microbes, the regulatory pulse now supports faster market entry. This environment emboldens start-ups to pursue proprietary consortia optimized for Brazil’s climatic zones, adding healthy competitive tension to the incumbent-dominated Brazil biofertilizer market.

By Crop Type: Row-Crop Dominance and Horticultural Emergence

Row crops represented 79.2% of Brazil biofertilizer market size in 2025, led by soy and corn across 26 million hectares in the Center-West, and is growing at the fastest CAGR of 9.8% through 2031. Row crops dominate the Brazil biofertilizer market, driven by extensive soybean, corn, and cotton cultivation. Soybeans account for the majority of inoculant usage due to high adoption rates on large farms, supported by years of extension outreach. Corn adoption is growing as farmers increasingly use biofertilizers to reduce nitrogen application, while cotton growers are turning to advanced blends that offer additional biocontrol benefits.

Horticultural crops hold a smaller market share but are anticipated to grow rapidly. Drip-irrigated crops like tomatoes, peppers, and citrus are adopting biofertilizers to improve fruit quality and shelf life. These crops provide higher margins for suppliers compared to row crops, helping diversify revenue streams. Government certification programs further encourage biological adoption by enforcing stricter residue limits for export-oriented produce.

Geography Analysis

The Center-West, anchored by Mato Grosso, generated sgnificant share of Brazil biofertilizer market revenue in 2025 as large, tech-savvy growers integrate biological nitrogen fixation across 13 million hectares of soybean and corn [3]Source: Companhia Nacional de Abastecimento, “Acompanhamento da Safra Brasileira de Grãos,” conab.gov.br. Acidic soils respond strongly to phosphate-solubilizing consortia, validating premium pricing models. Regional cooperatives and well-paved transport corridors bolster distribution efficiency, enabling same-week delivery even during peak seasons. The region’s MATOPIBA frontier offers additional acreage that will require microbial inoculation from day one, helping maintain long-term demand visibility.

The South market is driven by diversified cropping systems that facilitate year-round biofertilizer purchases. Temperate climates extend liquid shelf life, easing cold-chain pressure and cutting spoilage losses below 5%. Strong cooperative networks strengthen farmer education, enabling rapid field adoption of research findings. Government extension services focus on integrating biological inputs into sustainable intensification programs, reinforcing the Brazil biofertilizer market’s embeddedness in regional agronomy.

The Southeast, Northeast, and North together represent 26% of sales but log the highest CAGR during forecast period. In São Paulo, sugarcane mills blend vinasse with liquid biofertilizers, creating closed-loop nutrient recycling that lowers synthetic potassium demand. The Northeast’s semi-arid zones gain from drought-tolerant inoculants paired with drip irrigation systems financed under Pronaf. Cold-chain gaps in the North invite shelf-stable granules and local fermentation hubs, shortening lead times by up to 10 days. As logistics and credit frameworks mature, these frontier territories will add incremental volume to the Brazil biofertilizer market size every season.

Competitive Landscape

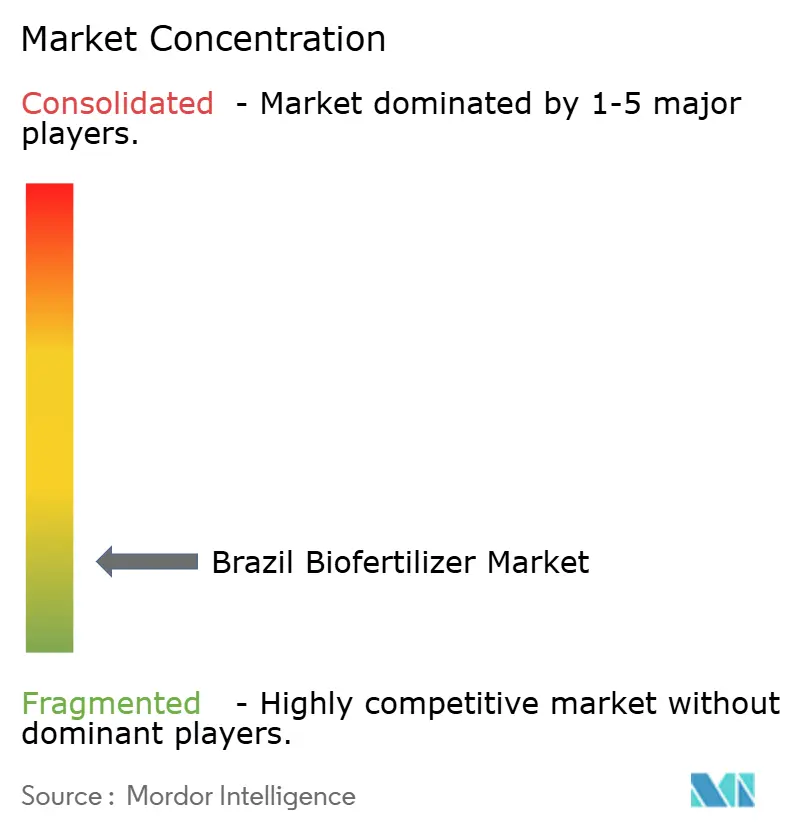

The Brazil biofertilizer market features prominent players like Vittia Group, Rizobacter, Novozymes A/S (Novonesis Group), Biolchim SpA, and Lallemand Inc., leading the industry through various strategic initiatives, accounting for significant share of 2025 sales, signaling a fragmented arena where scale and strain libraries serve as paramount competitive moats. Companies are increasingly focusing on research and development to create innovative biological fertilizer solutions, particularly in nitrogen fixation and nutrient enhancement technologies.

Strategic partnerships shape the innovation pipeline. The SPARCBio public-private hub, launched in December 2024, unites Dutch technology firms with Brazilian researchers to co-develop biological inputs for citrus and grain crops. Cooperative alliances with drone-sprayer manufacturers aim to enhance foliar-application uniformity, opening fresh revenue channels. Start-ups gain traction in on-farm bioreactor technology, offering white-label fermentation modules to large growers seeking self-sufficiency. Despite room for niche disruption, the capital and compliance burden sustains high entry barriers, preserving the concentrated structure of the Brazil biofertilizer market.

Mergers and equity stakes reinforce scale advantages. Multinational seed companies are scouting tie-ups with inoculant suppliers to bundle biological packages with proprietary genetics, locking growers into vertically integrated solutions. Competitive intensity thus pivots from price toward value-added ecosystems, a shift that supports sustained margin profiles across the Brazil biofertilizer industry.

Brazil Biofertilizer Industry Leaders

Biolchim SpA

Lallemand Inc.

Rizobacter

Vittia Group

Novonesis A/S (Novonesis Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rovensa Next, the global leader in biosolutions for agriculture, has opened a new pilot fermentation plant in Brazil, strengthening its global R&D and scale-up capabilities in microbial biosolutions. The facility creates an intermediate step between laboratory research and full industrial production, reducing development risks and accelerating the launch of new bio-inputs.

- July 2025: UPL introduced "Nuvita" in Brazil, a foliar biosolution under its Natural Plant Protection (NPP) platform designed to boost nutrient efficiency in corn and soybean. It enhances aquaporin formation, improving nitrogen uptake and water absorption, with field trials demonstrating significant nitrogen efficiency improvement.

- June 2025: Koppert Biological Systems Inc. announced it plans to invest USD 200 million to build two new manufacturing plants in Brazil by 2030, aiming to boost production of biological solutions tailored for tropical agriculture. The factories, which will focus on products derived from bacteria and fungi, are slated to begin operations in the next two to three years.

- December 2024: Brazil enacted Federal Law No. 15.070/2024, creating a unified regulatory framework for bioinputs including microorganisms, plant extracts, and inoculants. The law streamlines procedures for production, registration, and trade, accelerating innovation and investment in the biofertilizer sector.

Brazil Biofertilizer Market Report Scope

The Brazil Biofertilizer Market Report is Segmented by Form (Azospirillum, Azotobacter, Mycorrhiza, Phosphate Solubilizing Bacteria, Rhizobium, and Other Biofertilizers), and Crop Type (Cash Crops, Horticultural Crops, and Row Crops). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Azospirillum |

| Azotobacter |

| Mycorrhiza |

| Phosphate Solubilizing Bacteria |

| Rhizobium |

| Other Biofertilizers |

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Azospirillum |

| Azotobacter | |

| Mycorrhiza | |

| Phosphate Solubilizing Bacteria | |

| Rhizobium | |

| Other Biofertilizers | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biofertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Biofertilizers enhance soil quality by increasing the population of beneficial microorganisms. They help crops absorb nutrients from the environment.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.