Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

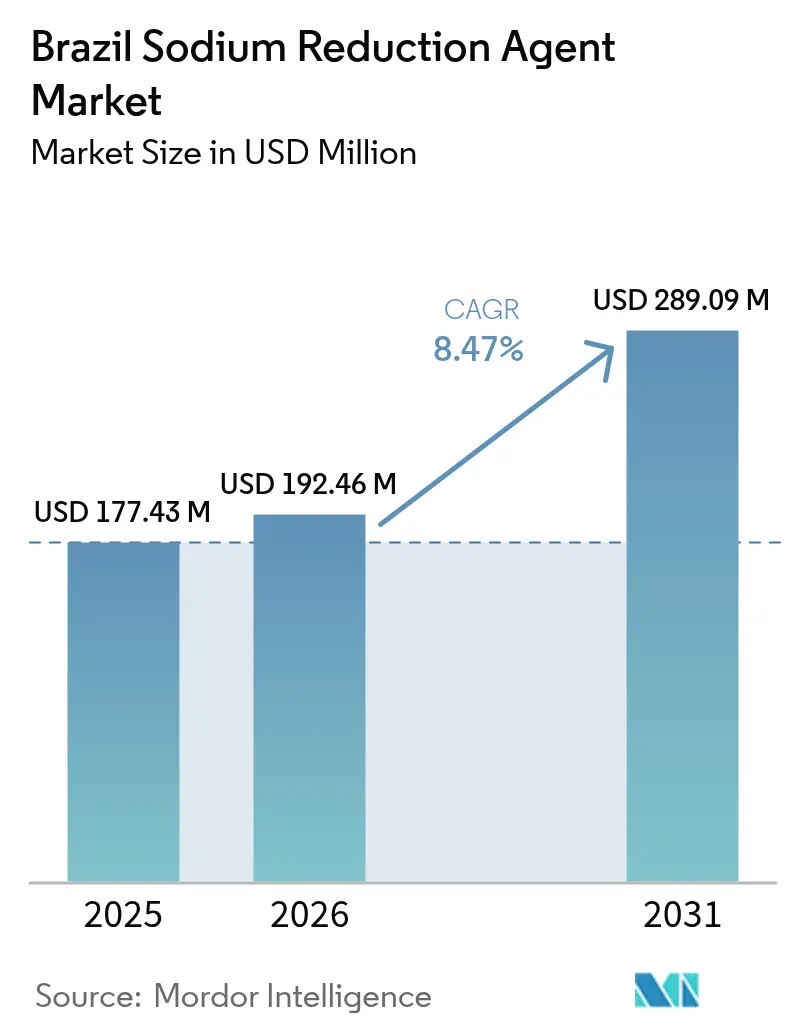

| Base Year Market Size (2025) | USD 177.43 Million |

| Market Size (2026) | USD 192.46 Million |

| Market Size (2031) | USD 289.09 Million |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Sodium Reduction Agent Market Analysis by Mordor Intelligence

The Brazil sodium reduction agents market size was valued at USD 177.43 million in 2025 and estimated to grow from USD 192.46 million in 2026 to reach USD 289.09 million by 2031, at a CAGR of 8.47% during the forecast period (2026-2031). This growth is driven by stringent regulatory measures, a significant national burden of hypertension, and ongoing reformulation efforts within Brazil's food-processing industry. The implementation of front-of-pack warning labels by the National Health Surveillance Agency (ANVISA), along with voluntary sodium-reduction targets, has accelerated reformulation timelines, particularly for high-sodium processed meats and convenience foods. Ingredient suppliers are enhancing application-laboratory support to help food processors address challenges related to sensory attributes, texture, and shelf life when replacing sodium chloride with alternatives such as mineral salts, yeast extracts, and fermentation-derived compounds. Collaborations between multinational ingredient companies and local producers are expanding access to technical expertise. Additionally, functional-food positioning allows processors to offset higher ingredient costs through premium pricing. These factors collectively support the growth of the Brazil sodium reduction agents market in the medium term.

Key Report Takeaways

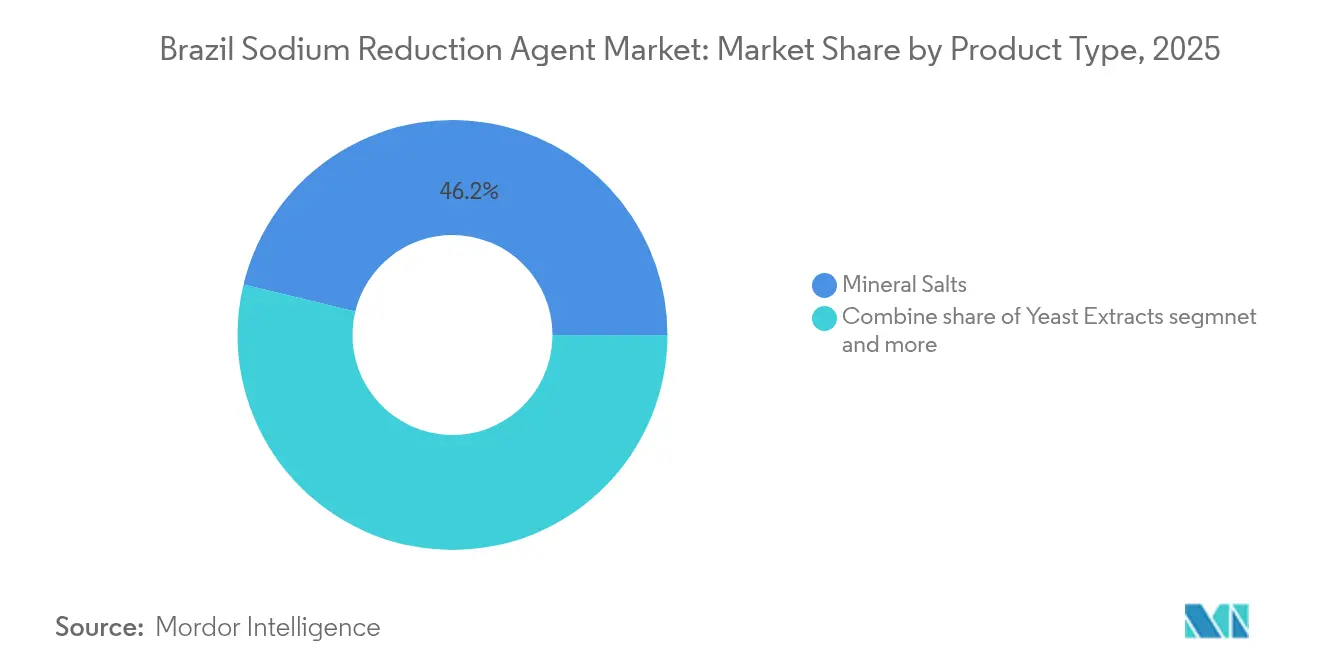

- By product type, mineral salts led with 46.22% of the Brazil sodium reduction agents market share in 2025, while yeast extracts are forecast to post the fastest 9.58% CAGR through 2031.

- By form, powders and granules accounted for 66.10% of the Brazil sodium reduction agents market size in 2025; liquid concentrates are projected to expand at a 9.62% CAGR between 2026-2031.

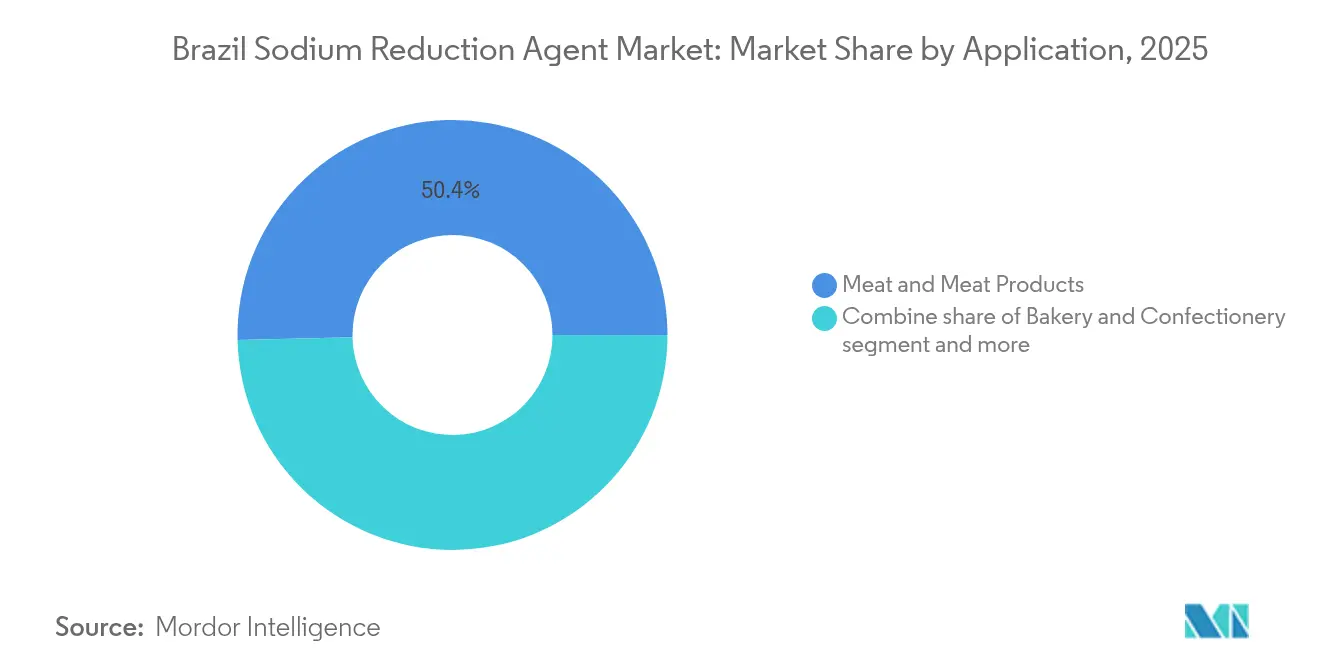

- By application, meat and meat products held 50.37% of the Brazil sodium reduction agents market share in 2025 and are advancing at a 9.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Sodium Reduction Agent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hypertension and cardiovascular diseases | +1.8% | National, with higher burden in urban centers (São Paulo, Rio de Janeiro, Belo Horizonte) | Medium term (2-4 years) |

| Growing consumer awareness about sodium-related health risks | +1.5% | National, accelerated by front-of-pack labeling in retail channels | Short term (≤ 2 years) |

| Expansion of ultra-processed food consumption | +1.3% | Urban and peri-urban areas, youth and middle-income segments | Medium term (2-4 years) |

| Natural and clean-label ingredient preferences | +1.6% | National, strongest in premium and organic retail segments | Long term (≥ 4 years) |

| Partnerships and collaborations between manufacturers and ingredient suppliers | +1.2% | National, concentrated in São Paulo industrial corridor | Medium term (2-4 years) |

| Development of functional foods and fortified products | +1.1% | National, with early adoption in sports nutrition and wellness categories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of hypertension and cardiovascular diseases

Hypertension affects nearly one-third of Brazilian adults and is the leading cause of disability-adjusted life years lost, surpassing the impact of tobacco use and elevated fasting plasma glucose levels. The average daily sodium intake in Brazil is approximately nine grams, nearly double the limit recommended by the World Health Organization (WHO). Studies reveal that about 15% of cardiovascular-related deaths in the country are linked to excessive salt consumption. Urban areas such as São Paulo, Rio de Janeiro, and Belo Horizonte report higher hypertension rates, primarily due to increased reliance on processed foods. This trend presents a significant market opportunity for sodium-reduction agents in retail and food-service channels. The Brazilian Ministry of Health introduced voluntary sodium-reduction targets in 2011, which were updated in 2024. However, compliance has been limited, leading the National Health Surveillance Agency (ANVISA) to adopt mandatory front-of-pack labeling as a more effective regulatory measure[1]Source: Brazilian Health Regulatory Agency, “Management Report Brazilian Health Regulatory Agency 2024,” gov.br. This shift is accelerating reformulation efforts, with food processors that had previously delayed investments now exploring alternatives such as potassium chloride blends and yeast extracts to avoid high-sodium warnings on packaging. The link between hypertension prevalence and ingredient demand is evident: each percentage-point reduction in sodium content necessitates substitution with mineral salts, amino acids, or flavor enhancers, transforming a public health challenge into a driver of market demand.

Growing consumer awareness about sodium-related health risks

Front-of-pack warning labels became mandatory in October 2023. A March 2024 Bain survey revealed that 56% of shoppers noticed the high-sodium magnifying-glass icon, and 46% adjusted their purchasing behavior. The strongest response was observed among women aged 25-44 and households with children. This heightened awareness is shortening the reformulation timeline for brands. Companies that fail to remove the warning risk losing shelf space to private-label and premium competitors that have already reformulated their products. For instance, Knorr's introduction of a zero-salt bouillon cube in Brazil demonstrates proactive adaptation, utilizing yeast extracts and vegetable powders to achieve umami flavor without exceeding the 600 milligrams per 100 grams sodium threshold. Social media is amplifying the impact of these labels as consumers share images of high-sodium products, creating reputational risks that extend beyond the point of sale. This increased awareness is also segmenting the market. Premium segments are adopting clean-label solutions, such as yeast extracts and fermented ingredients, while value-tier products are relying on lower-cost potassium chloride blends, often combined with masking agents to reduce metallic off-notes. This dual approach is driving volume growth in both mineral-salt and yeast-extract categories, as manufacturers align their formulations with specific price points and brand strategies.

Expansion of ultra-processed food consumption

Ultra-processed foods contribute significantly to the total energy intake in Brazil, with higher consumption levels observed among urban populations and younger age groups. These food categories, including packaged snacks, ready meals, condiments, and processed meats, contain the highest sodium levels, making reformulation efforts a key focus. A paradox arises as the growing consumption of ultra-processed foods simultaneously increases hypertension rates and the demand for sodium-reduction agents. While sodium content per serving may decrease, the overall volume of sodium requiring substitution rises due to increased consumption. Brazil's food-processing industry has witnessed substantial growth, driven by strong demand for convenience-focused products aligned with dual-income households and urbanization trends [2]Source: USDA Foreign Agricultural Service, “Food Processing Ingredients – Brazil,” USDA.gov. Food processors are prioritizing sodium reduction during the development of new products rather than reformulating existing stock-keeping units (SKUs). This strategy is shaped by front-of-pack labeling requirements at product launch, as reformulating products after launch entails costly re-registration with the National Health Surveillance Agency (ANVISA). By incorporating sodium-reduction agents into research and development processes, food processors are ensuring consistent demand. New products, such as snack bars, instant noodle variants, and frozen entrées, are designed to meet sodium thresholds from the outset.

Natural and clean-label ingredient preferences

Clean-label demand is influencing ingredient selection, with yeast extracts emerging as a preferred alternative to monosodium glutamate in premium meat, sauce, and snack formulations. Yeast extracts, containing 5% free glutamic acid, can reduce sodium content by up to 50% when used at rates of 0.5-2%. Brazilian consumers are increasingly attentive to ingredient lists, particularly avoiding synthetic additives, a trend driven by social media influencers and wellness-oriented retail chains like Mundo Verde and Hortifruti. Yeast extracts meet both sodium-reduction and clean-label requirements as they are derived from Saccharomyces cerevisiae fermentation and lack an E-number designation, enabling "natural flavor" claims on product packaging. This dual functionality is a key factor behind the projected 10.10% compound annual growth rate (CAGR) of yeast extracts through 2030, surpassing mineral salts despite a smaller base in 2024. ProVerde's planned May 2024 launch of a fermented-bean protein concentrate, which combines umami flavor with plant-based protein fortification, highlights the growing demand for multifunctional ingredients [3]Source: FAPESP, “ProVerde Develops Fermented Bean Protein Concentrate,” fapesp.br . These ingredients address multiple consumer priorities, including sodium reduction, protein enrichment, and sustainability, within a single product declaration. Additionally, processors targeting export markets, particularly in the European Union where clean-label standards are more stringent, are increasingly adopting yeast extracts and fermented peptides. This trend is creating a premium quality tier that supports margin growth for ingredient suppliers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of reformulation and research and development investment | -1.4% | National, most acute for small and mid-sized processors outside São Paulo | Short term (≤ 2 years) |

| Regulatory complexity and evolving standards across product categories | -0.9% | National, with category-specific thresholds creating compliance fragmentation | Medium term (2-4 years) |

| Supply chain constraints and ingredient availability | -0.7% | Regional, concentrated outside São Paulo and Rio de Janeiro distribution hubs | Short term (≤ 2 years) |

| Competing flavor enhancement alternatives | -0.6% | National, with premium segments adopting fermentation-derived peptides and taste modulators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of reformulation and research and development investment

Reformulation cycles for sodium reduction involve sensory panels, shelf-life testing, and pilot production runs, with costs ranging from USD 50,000 to USD 200,000 per stock-keeping unit. These costs pose a significant challenge for small and mid-sized processors, which often operate on narrow margins and have limited access to affordable capital. Potassium chloride is two to three times more expensive per kilogram than sodium chloride, while yeast extracts are priced even higher, at USD 8 to USD 12 per kilogram compared to USD 0.30 for table salt. These cost differences reduce gross margins unless processors can pass the additional expenses on to retail or food-service buyers. As a result, many smaller manufacturers are postponing reformulation efforts, waiting for competitors to initiate a market-wide shift. This creates a prisoner's dilemma, slowing the overall adoption rates. Geographical disparities further intensify the challenge. Processors in São Paulo and Rio de Janeiro benefit from proximity to ingredient suppliers' application laboratories and pilot facilities, which helps reduce logistics costs. On the other hand, processors in the Northeast and Central-West regions face higher freight expenses and longer lead times, increasing the reformulation gap between urban and regional producers. This cost imbalance is consolidating market share among larger, well-capitalized companies that can manage the upfront investment and distribute it across high-volume stock-keeping units.

Regulatory complexity and evolving standards across product categories

ANVISA's (Agência Nacional de Vigilância Sanitária) front-of-pack labeling regulation establishes varying sodium thresholds based on product categories, such as 600 mg per 100 g for solids and 300 mg per 100 ml for liquids. Additionally, processors must adhere to category-specific standards for products like meat, dairy, and bakery goods, each governed by distinct technical regulations. This fragmented approach increases compliance costs. For example, a processor with stock-keeping units (SKUs) across snacks, sauces, and frozen meals must reformulate to meet three separate targets, often requiring different sodium-reduction agents and dosing protocols for each category. The regulatory environment is also subject to change, as ANVISA periodically revises thresholds based on population sodium-intake surveys. This creates uncertainty, discouraging long-term investments in reformulation. In the first year following the October 2023 mandate, only 12.9% of products displayed compliant labels, highlighting the gap between regulatory objectives and industry readiness. Processors are advocating for harmonized thresholds and extended phase-in periods. However, until such changes are implemented, the complexity of compliance will continue to hinder adoption rates, particularly for smaller firms lacking expertise in regulatory affairs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Yeast Extracts Lead Innovation Despite Mineral Salts Dominance

Mineral salts accounted for 46.22% of the projected 2025 revenue, driven by the cost-effectiveness and established use of potassium chloride in meat processing, bakery, and dairy applications. Potassium chloride can directly substitute sodium chloride at ratios of 1:1 to 2:1, depending on formulation tolerance. Blends of potassium chloride with masking agents such as potassium lactate or calcium chloride are widely used by processors targeting 30-40% sodium reduction without causing consumer rejection due to metallic or bitter off-notes. Yeast extracts, although representing a smaller market share, are expected to grow at the fastest rate, with a compound annual growth rate (CAGR) of 9.58% through 2031. This growth is driven by their clean-label positioning, umami flavor enhancement, and the absence of E-number designations, which appeal to premium and export-oriented segments.

Yeast extracts contain approximately 5% free glutamic acid and can reduce sodium content by up to 50% when used at levels of 0.5-2%. They are particularly effective in high-umami applications such as sauces, seasonings, and meat marinades. Amino acids and glutamates occupy a niche role, primarily used in industrial seasoning blends where cost considerations favor monosodium glutamate over yeast extracts. However, regulatory scrutiny and the growing demand for clean-label products are gradually impacting this segment. The "Others" category includes emerging solutions such as fermented peptides, mushroom extracts, and seaweed-derived compounds. These alternatives offer both sodium reduction and functional benefits, but their commercial adoption remains limited due to high costs and supply chain challenges.

By Form: Liquid Concentrates Gain Ground in High-Throughput Lines

Powder and granule forms accounted for 66.10% of 2025 revenue, attributed to their ease of handling, extended shelf life, and suitability for dry-blending operations in seasoning, bakery, and snack production. Powder formats are particularly preferred by smaller processors that do not have inline liquid-dosing infrastructure, as they rely on batch mixing. Free-flowing granules simplify inventory management and minimize waste in such operations.

However, liquid concentrates are expected to grow at a faster rate, with a compound annual growth rate (CAGR) of 9.62% through 2031. This growth is driven by operational efficiencies in high-throughput meat and sauce production lines, where inline injection systems enable precise dosing and reduce labor costs. Liquid yeast extracts and mineral-salt brines can be directly metered into tumblers, mixers, or emulsifiers, eliminating the dust and dissolution steps required for powders and enhancing batch-to-batch consistency. Large meat processors, such as those in Brazil, the world's leading beef exporter, are retrofitting injection systems to incorporate liquid sodium-reduction agents. This is particularly relevant for products like embutidos, including mortadella and salsicha, which require uniform sodium distribution to comply with the National Health Surveillance Agency (ANVISA) thresholds.

By Application: Meat Products Anchor Demand Amid Bakery and Snack Reformulation

Meat and meat products accounted for 50.37% of 2025 revenue and are projected to experience the highest application growth, with a Compound Annual Growth Rate (CAGR) of 9.74% through 2031. This growth is supported by Brazil's position as the world's largest beef exporter and increasing domestic consumption of processed meats, which have historically contained sodium levels exceeding 1,200 milligrams (mg) per 100 grams (g). Embutidos, including sausages, ham, mortadella, and salsicha, are the primary focus for reformulation due to their tendency to trigger the Brazilian Health Regulatory Agency (ANVISA) front-of-pack warning for sodium levels above 600 mg per 100 g. To address this, processors are utilizing potassium chloride blends and yeast extracts to achieve sodium reductions of 30-50% while maintaining water-holding capacity and shelf life. However, this presents a significant technical challenge, as sodium chloride is essential for protein solubilization, emulsion stability, and microbial control. Direct substitution with potassium chloride often results in texture degradation and off-flavors unless masking agents are incorporated.

In bakery and confectionery applications, reformulation efforts are focused on products such as sandwich breads and crackers, where sodium functions as a dough conditioner and flavor enhancer. These categories typically have a lower sodium baseline of 400-500 mg per 100 g, resulting in fewer Stock Keeping Units (SKUs) triggering the warning label. Meanwhile, condiments, seasonings, and sauces represent a high-intensity use case. Products like soy sauce, ketchup, and bouillon cubes can contain sodium levels exceeding 3,000 mg per 100 g. Reformulation in this segment requires the use of yeast extracts or amino acids to maintain umami flavor while achieving sodium reductions of 40-60%.

Geography Analysis

Brazil's domestic market accounts for the majority of sodium-reduction agent demand, driven by factors such as mandatory front-of-pack labeling, the high prevalence of hypertension, and the significant scale of the country's food-processing sector, which is growing at an annual rate of 9.9%. São Paulo and Rio de Janeiro lead in demand due to their concentration of large food manufacturers, ingredient distributors, and application laboratories that support product reformulation. In contrast, the Northeast and Central-West regions face challenges such as higher logistics costs and limited access to specialty ingredients like yeast extracts and proprietary mineral-salt blends.

The geographic concentration of demand is also reflected in company operations. For instance, Caldic's acquisition of Bring Solutions in March 2024 expanded its distribution network across Brazil. However, the acquired firm's warehouses and technical staff remain concentrated in the Southeast, highlighting the infrastructure limitations that restrict ingredient availability in secondary markets.

Export-oriented processors, particularly those supplying the European Union where sodium-reduction regulations have been in place for over a decade, are increasingly utilizing clean-label yeast extracts and fermented ingredients. This approach allows them to meet both Brazilian and European Union standards with a single formulation, thereby reducing stock-keeping unit (SKU) complexity and inventory costs. Additionally, Brazil's meat-export sector, which serves over 150 countries, is incorporating sodium reduction into production protocols to avoid the need for market-specific reformulations. This proactive strategy is driving sustained demand for premium sodium-reduction agents, even for SKUs that do not yet require Brazil's front-of-pack warning labels.

Competitive Landscape

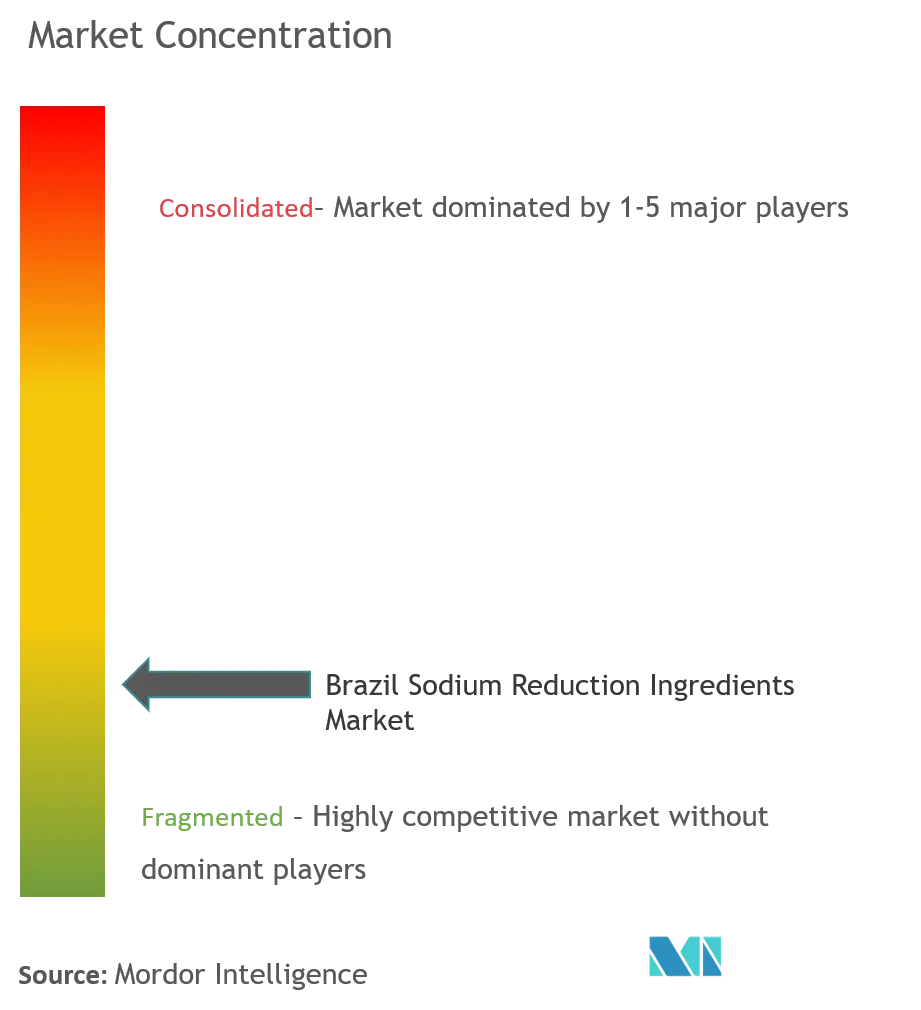

The Brazil sodium reduction agents market is moderately consolidated, featuring both multinational ingredient companies and regional specialists. Key multinational players include Ajinomoto, Cargill, Kerry Group, DSM-Firmenich, Givaudan, and International Flavors & Fragrances (IFF). These companies leverage global research and development (R&D) networks and application laboratories to deliver comprehensive reformulation solutions, integrating sodium-reduction agents with taste modulators, texture enhancers, and shelf-life extenders. Regional specialists, such as Biospringer, Lesaffre, and Saltwell, focus on yeast extracts or mineral-salt blends. These regional players primarily compete on pricing and localized technical support, often embedding staff at customer sites to accelerate trial-and-error processes.

A clear strategic divide exists between suppliers of mineral salts and yeast extracts. Mineral-salt suppliers focus on cost efficiency and logistics, as potassium chloride is a low-margin commodity. Yeast-extract suppliers, on the other hand, differentiate through flavor complexity, clean-label attributes, and multifunctional benefits such as umami enhancement and B-vitamin fortification. An example of a distribution-led growth strategy is Caldic's planned acquisition of Bring Solutions in March 2024. This move aims to expand geographic reach and improve customer engagement in a market where technical service and fast delivery are as critical as product performance.

Emerging opportunities are evident in fermentation-derived peptides and plant-based umami compounds. Startups like ProVerde are leveraging academic partnerships, such as the São Paulo Research Foundation's (FAPESP) funding of ProVerde's fermented-bean protein concentrate, to develop multifunctional ingredients that address sodium reduction, protein enhancement, and sustainability within a single product declaration.

Brazil Sodium Reduction Agent Industry Leaders

Ajinomoto Co., Inc.

Angel Yeast Co., Ltd.

Biorigin

Armor Protéines

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cargill introduced a comprehensive content series on sodium reduction, emphasizing the dual benefits of potassium chloride in lowering sodium levels and increasing potassium intake. The series provides detailed insights into the health implications of sodium and potassium balance, along with practical applications of potassium chloride in food products.

- December 2024: Brenntag Specialties has been designated by K+S Minerals & Agriculture GmbH as the global strategic distributor for three high-purity pharmaceutical salts: APISAL Sodium Chloride (GMP, pharmacopoeia quality, API), Potassium Chloride 99.9% KCl Ph. Eur., USP (API), and HD-NaCl.

- April 2024: Kerry introduced Tastesense Salt, a product developed to provide salt and savory flavors without increasing sodium content. It maintains key flavor characteristics while replicating the salty impact, body, and linger. This initiative addresses consumer demand for healthier food options by reducing sodium intake without sacrificing taste.

Brazil Sodium Reduction Agent Market Report Scope

Brazil sodium reduction ingredients market is segmented by product type and application. On the basis of product type, the market is segmented into Amino Acids & Glutamates, Mineral Salts, Yeast Extracts, and Others. On the basis of application, the market is segmented into Bakery & Confectionery, Condiments, Seasonings & Sauces, Dairy & Frozen Foods, Meat & Meat Products, Snacks, Others.

By Product Type

| Amino Acids and Glutamates |

| Mineral Salts |

| Yeast Extracts |

| Others |

By Form

| Powder/Granules |

| Liquid |

By Application

| Bakery and Confectionery |

| Condiments, Seasonings and Sauces |

| Dairy and Frozen Foods |

| Meat and Meat Products |

| Snacks |

| Others |

| By Product Type | Amino Acids and Glutamates |

| Mineral Salts | |

| Yeast Extracts | |

| Others | |

| By Form | Powder/Granules |

| Liquid | |

| By Application | Bakery and Confectionery |

| Condiments, Seasonings and Sauces | |

| Dairy and Frozen Foods | |

| Meat and Meat Products | |

| Snacks | |

| Others |

Key Questions Answered in the Report

What is the current value of the Brazil sodium reduction agents market?

The market stands at USD 192.46 million in 2026.

How fast is the market growing?

It is projected to expand at an 8.47% CAGR, reaching USD 289.09 million by 2031.

Which product type is expanding fastest?

Yeast extracts will grow at a 9.58% CAGR through 2031.

Why are meat processors key customers?

Processed meats exceed sodium thresholds, so they rely on potassium-salt blends and yeast extracts to avoid mandatory high-sodium warnings.

Page last updated on: