Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.01 Billion |

| Market Size (2026) | USD 6.28 Billion |

| Market Size (2031) | USD 7.86 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Food Sweetener Market Analysis by Mordor Intelligence

The Brazil food sweetener market size was valued at USD 6.01 billion in 2025 and estimated to grow from USD 6.28 billion in 2026 to reach USD 7.86 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031). This growth is driven by Brazil's role as the world's largest sugar exporter and the increasing demand for zero-calorie and natural sweetener alternatives. Factors such as regulatory efforts to reduce added sugar consumption, growing health awareness among urban consumers, and the ethanol-sugar price arbitrage influencing sucrose pricing are contributing to the market's development. High-intensity and value-added sweeteners are gaining popularity in this environment. Global ingredient companies are expanding fermentation-based stevia production to overcome agricultural constraints, while local processors are utilizing cane juice derivatives to mitigate sugar price volatility. These trends indicate that the Brazil food sweetener market will continue to evolve toward diversified ingredient offerings, cost-effective bulk sweeteners, and premium natural solutions catering to health-conscious consumers.

Key Report Takeaways

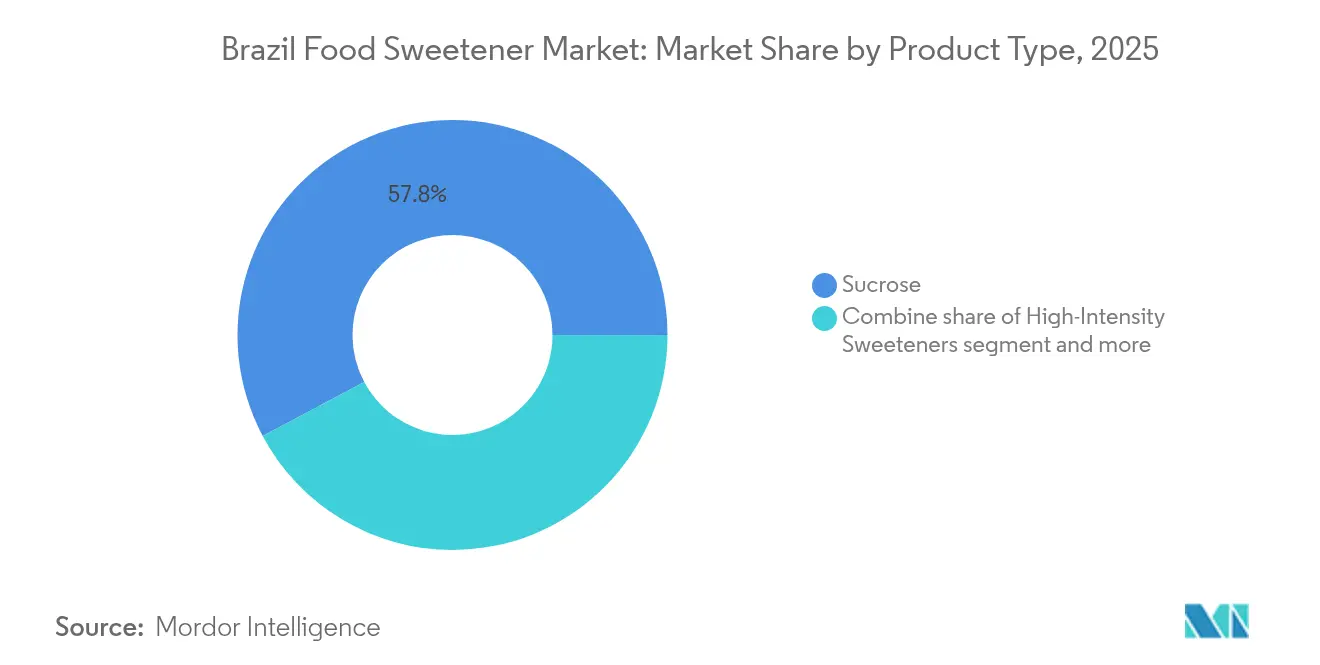

- By product type, sucrose led with 57.78% of the Brazil food sweetener market share in 2025; high-intensity sweeteners are growing at the fastest 5.66% CAGR through 2031.

- By application, beverages held 43.85% of the Brazil food sweetener market size in 2025, while dairy and desserts record the highest 5.31% CAGR to 2031.

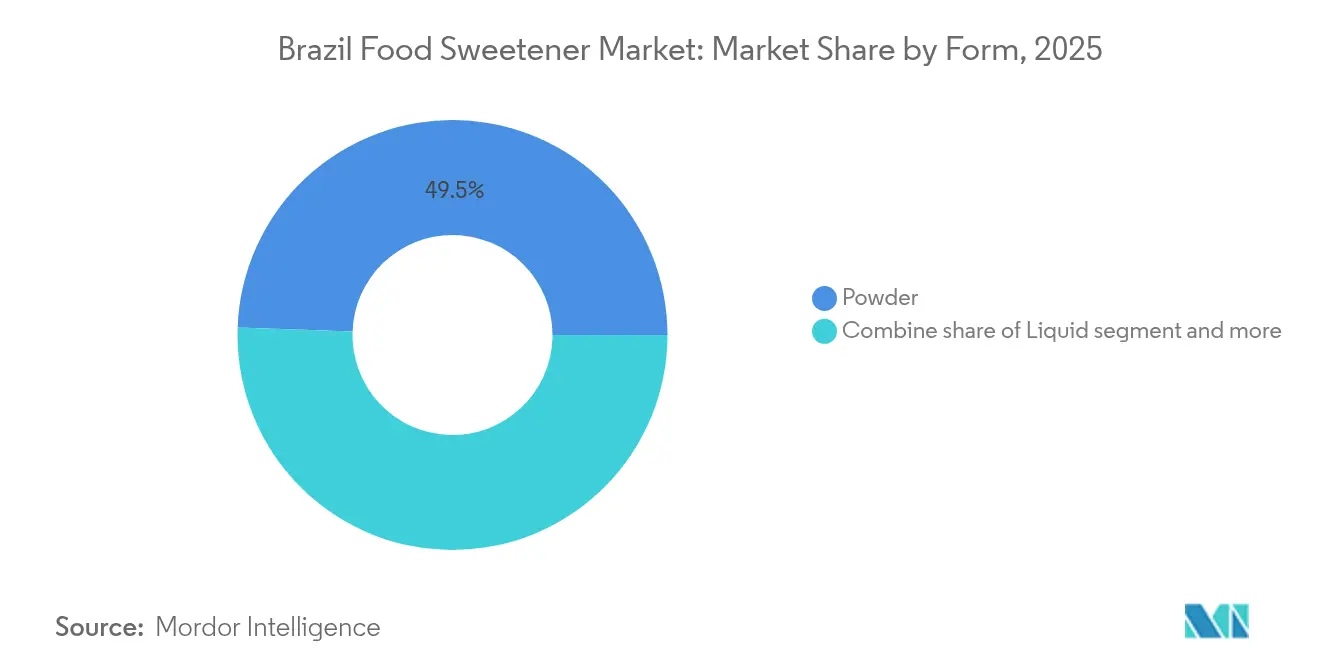

- By form, powder formats accounted for 49.45% of the Brazil food sweetener market size in 2025; liquid formats expand at a 5.75% CAGR through 2031.

- By category, conventional products dominated with 80.25% share in 2025, whereas organic variants advance at a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Food Sweetener Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumption of convenience and packaged food and beverage | +0.9% | National, concentrated in São Paulo, Rio de Janeiro, and southern states | Medium term (2-4 years) |

| Increasing demand for zero-glycemic sweeteners among low-carb consumers | +0.7% | National, with early adoption in urban centers (São Paulo, Brasília, Curitiba) | Short term (≤ 2 years) |

| Regulatory expansion of permitted natural sweeteners | +0.6% | National (ANVISA jurisdiction) | Long term (≥ 4 years) |

| Consumer preference for natural and plant-based sweeteners | +0.8% | National, strongest in Southeast and South regions | Medium term (2-4 years) |

| Sweeteners with added benefits driving demand for health-focused products | +0.5% | National, premium segments in metropolitan areas | Long term (≥ 4 years) |

| Microencapsulation and coating technologies improve stability and minimize aftertaste | +0.4% | National, adoption led by multinational ingredient suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumption of convenience and packaged food and beverage

In 2024, Brazil's processed food sector generated USD 233 billion, contributing 10.8% to the country's Gross Domestic Product (GDP). At the same time, the non-alcoholic beverage market is expected to grow significantly, rising from EUR 31.2 billion in 2024 to EUR 52.4 billion by 2034. This growth rate exceeds GDP growth and reflects changes in consumption patterns driven by urbanization [1]Source: OECD-FAO, “OECD-FAO Agricultural Outlook 2024-2033,” oecd-ilibrary.org. Since 2020, retail e-commerce penetration in food and beverage categories has doubled, leading to shorter product lifecycles and benefiting manufacturers who can quickly adapt to clean-label demands while maintaining shelf stability. The combination of convenience and health consciousness creates a dual opportunity. While traditional sugar-sweetened categories face challenges, ready-to-drink functional beverages and portion-controlled dairy desserts are gaining market share. Nestlé has announced an investment of BRL 500 million (USD 100 million) through 2028, focusing on expanding Nescafé Dolce Gusto production and coffee innovation, which demonstrates multinational confidence in Brazil's potential for premiumization. This investment follows a previous commitment of BRL 1.5 billion in 2024, highlighting sustained capital allocation to categories where sweetener choices significantly influence consumer preferences.

Increasing demand for zero-glycemic sweeteners among low-carb consumers

Survey data from the Brazilian Longitudinal Study of Adult Health (ELSA-Brasil) cohort indicates that 25.7% of adults regularly consume non-nutritive sweeteners, while the median table sugar intake remains at 14.3 grams per day. This suggests partial substitution rather than complete replacement. Coffee, consumed by 87% of Brazilians, is the primary medium for sweetener use. Among coffee drinkers, 80% add sugar (averaging 8 to 10 grams per serving), while only 8.6% choose non-caloric alternatives. This preference for sugar presents an opportunity for zero-glycemic sweeteners that replicate sucrose's mouthfeel and dissolve efficiently in hot beverages. Erythritol and tagatose demonstrate superior performance in these attributes compared to first-generation stevia extracts. The proposed selective tax on sugar-sweetened beverages, currently facing opposition from industry groups, could create a price differential that encourages substitution, particularly in cost-sensitive categories such as carbonated soft drinks and powdered drink mixes. Additionally, 89% of Brazilian consumers now view sugary drinks negatively, and 38% express an intention to reduce consumption. However, actual behavior does not yet align with these stated preferences. This gap presents an opportunity for zero-glycemic sweeteners to gain traction, provided their sensory characteristics improve to meet consumer expectations.

Regulatory expansion of permitted natural sweeteners

ANVISA's (Agência Nacional de Vigilância Sanitária) regulatory updates have advanced significantly: Resolução RDC 843 and Instrução Normativa 281, both issued in 2024, revised the list of permitted sweeteners and introduced stricter standards for purity and labeling. Additionally, Resolução RDC 839/2023 and Instrução Normativa 380/2025 aligned Brazil's regulatory framework with Codex Alimentarius standards for steviol glycosides and monk fruit extracts [2]Source: ANVISA, “Resoluções e Instruções Normativas,” gov.br. These developments differ from the European Food Safety Authority's (EFSA) ongoing reassessments of artificial sweeteners. EFSA completed evaluations of acesulfame-K in April 2025 and neotame in July 2025, resulting in tighter acceptable daily intake recommendations for specific populations. This difference creates a regulatory opportunity for natural sweetener alternatives among Brazilian food manufacturers targeting export markets. Furthermore, the approval of enzymatically produced steviol glycosides (E960c) and glucosylated variants (E960d) in various jurisdictions highlights the potential of biosynthetic production methods to overcome Brazil's agronomic challenges for stevia cultivation, such as photoperiod sensitivity and seed multiplication limitations, as documented in peer-reviewed agronomic studies.

Consumer preference for natural and plant-based sweeteners

A compliance analysis of front-of-package labeling conducted 12 months after the implementation of ANVISA's (Agência Nacional de Vigilância Sanitária) Instrução Normativa 75/2020 revealed significant reformulation efforts by manufacturers. These efforts included reducing added sugars to avoid "high in" warning labels. This trend has particularly benefited natural high-intensity sweeteners, which are often marketed as clean-label solutions. Stevia, approved in Brazil since 1988, has faced challenges in scaling production domestically. Brands such as Zero-Cal and Color Andina Foods have struggled due to agronomic limitations and competition from imported extracts. Monk fruit, which provides sweetness 250 to 300 times that of sucrose through mogrosides, encounters even greater supply constraints. Its cultivation requires specific conditions, including altitudes of 200 to 800 meters and temperatures between 18 degrees Celsius and 32 degrees Celsius, primarily found in China's Guangxi province. Additionally, biosynthetic production remains commercially unfeasible, as demonstrated by Wang et al., who achieved only 9.1 micrograms per liter of mogrol through yeast fermentation, which is far below the thresholds required by the food industry.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer skepticism toward artificial sweeteners | -0.5% | National, heightened in health-conscious urban demographics | Short term (≤ 2 years) |

| Higher costs and price sensitivity for natural sweeteners | -0.6% | National, most acute in price-sensitive Northeast and North regions | Medium term (2-4 years) |

| Taste and aftertaste issues with some sweeteners | -0.4% | National, critical in coffee and dairy applications | Short term (≤ 2 years) |

| Formulation challenges in dairy and confectionery applications | -0.3% | National, concentrated in industrial bakery and ice cream segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer skepticism toward artificial sweeteners

The World Health Organization's 2023 guideline advising against the use of non-sugar sweeteners for weight control, along with prominent cohort studies linking artificially sweetened beverages to cardiovascular events and stroke, has heightened public concern. The NutriNet-Santé cohort and several systematic reviews published in the BMJ between 2022 and 2024 have reported associations between artificial sweetener consumption and glucose intolerance, potentially mediated by gut microbiome alterations, though causality remains debated. In Brazil, where 89% of consumers view sugary drinks negatively but median sugar intake remains high, this skepticism has created a demand gap that neither artificial nor natural sweeteners fully address. Formulators face the challenge of balancing cost, taste, and health perceptions. ANVISA's intake monitoring studies, including Takehara et al.'s 2022 database on declared high-intensity sweeteners in commercial products, have revealed varied exposure patterns, complicating risk communication and contributing to consumer uncertainty regarding safe consumption levels.

Higher costs and price sensitivity for natural sweeteners

The World Health Organization's (WHO) 2023 guideline advising against the use of non-sugar sweeteners for weight control, along with prominent cohort studies linking artificially sweetened beverages to cardiovascular events and stroke, has heightened public concern [3]Source: World Health Organization, “Use of non-sugar sweeteners: WHO guideline,” who.int. The NutriNet-Santé cohort and several systematic reviews published in the British Medical Journal (BMJ) between 2022 and 2024 have reported associations between artificial sweetener consumption and glucose intolerance, potentially mediated by gut microbiome alterations, though causality remains debated. In Brazil, where 89% of consumers view sugary drinks negatively but median sugar intake remains high, this skepticism has created a demand gap that neither artificial nor natural sweeteners fully address. Formulators face the challenge of balancing cost, taste, and health perceptions. The National Health Surveillance Agency's (ANVISA) intake monitoring studies, including Takehara et al.'s database on declared high-intensity sweeteners in commercial products, have revealed varied exposure patterns, complicating risk communication and contributing to consumer uncertainty regarding safe consumption levels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sucrose Anchors, High-Intensity Sweeteners Accelerate

Brazil accounts for 23% of global sugar production and 50% of international sugar trade, supporting sucrose's projected 57.78% market share in 2025. However, the segment's reliance on ethanol co-production introduces volatility, creating opportunities for high-intensity sweeteners. High-intensity sweeteners are expected to grow at a CAGR of 5.66% through 2031, driven by regulatory support and advancements in formulation. Within this category, natural sweeteners, such as steviol glycosides and monk fruit extracts, are gaining market share from artificial alternatives. This shift is supported by ANVISA's approval of enzymatically produced and glucosylated steviol glycosides (E960c and E960d), which enhance formulation flexibility. Additionally, the Avansya joint venture between Cargill and DSM-Firmenich received approval in January 2024 from the European Union and the United Kingdom for fermentation-derived EverSweet stevia, highlighting the potential of biosynthetic production to overcome Brazil's agronomic limitations and cater to premium export-oriented food manufacturers.

Starch sweeteners and sugar alcohols, including dextrose, high-fructose corn syrup, maltodextrin, sorbitol, xylitol, and erythritol, function as bulking agents that restore mouthfeel and texture in reduced-sugar formulations. Erythritol, produced through the fermentation of corn-derived glucose, offers zero-calorie properties and freezing-point depression, which enhances the scoopability of ice cream. These attributes have driven its adoption in dairy desserts and frozen novelties.

By Application: Beverages Lead, Dairy and Desserts Surge

Beverages accounted for 43.85% of the market share in 2025. However, the segment is facing structural challenges, as 89% of Brazilian consumers have a negative perception of sugary drinks, and 38% have expressed an intention to reduce their consumption. In 2024, Brazil sold 13.4 billion liters of soft drinks, but the proposed selective tax on sugar-sweetened beverages, if implemented, could significantly impact profit margins. This potential tax is also expected to accelerate the reformulation of products toward the use of non-nutritive sweeteners, as companies adapt to changing consumer preferences and regulatory pressures.

Coffee, which is consumed by 87% of Brazilians, continues to be a critical area of focus for the market. Among coffee drinkers, 80% add sugar, typically between 8 to 10 grams per serving, while only 8.6% opt for non-caloric alternatives. This indicates a latent opportunity for substitution if non-caloric sweeteners achieve sensory equivalence with sugar. Additionally, functional beverages and ready-to-drink formats are steadily gaining market share. PepsiCo's investment of 1.2 billion Brazilian Reais (USD 240 million) in 2023, which includes the establishment of eight factories and a research and development center employing over 100 scientists, demonstrates multinational confidence in the growing trend of premiumization within the beverage industry.

By Form: Powder Dominates, Liquid Gains in Beverages

Powder forms accounted for a 49.45% market share in 2025, primarily due to their suitability for dry-mix applications such as powdered drink mixes, bakery premixes, and tabletop sweeteners. These formats are widely preferred because they offer ease of handling, an extended shelf life, and cost efficiency, making them a practical choice for various industries. Their solid format ensures convenience in storage and transportation, further enhancing their appeal in the market. The ability to maintain product stability over time has also contributed to their widespread adoption in applications where long-term usability is critical.

Liquid sweeteners are expected to grow at a compound annual growth rate (CAGR) of 5.75% through 2031, driven by the increasing preference of beverage manufacturers for solutions that simplify blending processes, ensure uniformity, and minimize dust exposure in production environments. High-fructose corn syrup and liquid stevia extracts are the leading products in this segment. Suppliers such as Tate & Lyle are focusing on improving solubility with innovations like Tasteva Sol stevia technology. This technology offers over 200 times the solubility of Rebaudioside M and D, effectively addressing challenges such as precipitation and haze in fruit preparations and syrups. These advancements are particularly beneficial in formulations aimed at achieving significant sugar reduction without compromising product quality.

By Category: Conventional Retains Dominance, Organic Carves Premium Niche

Conventional sweeteners accounted for a substantial 80.25% of the market share in 2025, driven by their cost advantages and the presence of well-established supply chains. On the other hand, organic sweeteners are witnessing significant growth, with a compound annual growth rate (CAGR) of 5.52% projected through 2031. This growth is primarily fueled by urban consumers in cities such as São Paulo, Rio de Janeiro, and the southern states of Brazil, who are increasingly seeking products with certified-organic claims. Key contributors to this trend include organic cane sugar, stevia, and agave syrup. For example, Global Organics' blue agave syrup, sourced from Mexico and marketed as a low-glycemic option, is gaining popularity in premium product categories such as yogurt, ice cream, and flavored milk.

Organic certification, which complies with both Brazilian and international standards such as the United States Department of Agriculture (USDA) and European Union (EU) regulations, involves stringent processes including traceability, third-party audits, and adherence to premium pricing structures. These requirements often restrict the availability of organic products beyond metropolitan retail channels. The future growth of the organic segment will depend on the development of more efficient supply chains and consumers' willingness to pay price premiums that can exceed 50% compared to conventional alternatives. Additionally, Lesaffre's acquisition of a 70% stake in Biorigin/Zilor in October 2024 highlights the growing interest of multinational ingredient companies in organic and natural-origin inputs. This acquisition focuses on yeast derivatives and fermentation substrates, which are increasingly valued for their role in supporting clean-label positioning in the market.

Geography Analysis

Brazil's food sweetener market reflects regional differences shaped by income levels, agricultural infrastructure, and consumption patterns. The Southeast region, led by São Paulo and Rio de Janeiro, accounts for over 50% of the national demand. This is driven by higher per-capita income, extensive retail networks, and early adoption of health-conscious consumption trends. Compliance with the Brazilian Health Regulatory Agency's (ANVISA) Instrução Normativa 75/2020 on front-of-package labeling has encouraged reformulation efforts in this region. Manufacturers are reducing added sugars to avoid "high in" warning labels and are increasingly using natural high-intensity sweeteners as clean-label alternatives.

The South region, which includes Paraná, Santa Catarina, and Rio Grande do Sul, demonstrates strong demand for organic and premium sweeteners. This demand is supported by higher education levels and the influence of European immigrant communities with established preferences for artisanal and natural products. Nestlé's investment of R$500 million (USD 100 million) through 2028 to expand Nescafé Dolce Gusto production highlights the confidence of multinational companies in the region's potential for premiumization. These factors collectively position the South as a key area for growth in the premium sweetener segment.

In comparison, the Northeast and North regions, where per-capita income is over 40% lower than in the Southeast, show limited demand for premium natural sweeteners. This income disparity sustains the dominance of sucrose in cost-sensitive applications such as powdered drink mixes and economy-tier confectionery. However, rising urbanization and retail modernization in cities like Recife, Fortaleza, and Manaus are gradually improving access to reformulated products. Regional beverage bottlers are increasingly adopting hybrid sweetener systems that combine residual sugar (5 to 7 percent) with stevia or aspartame to balance cost efficiency and sensory quality, making these products more accessible to consumers in these regions.

Competitive Landscape

The Brazil food sweetener market shows moderate concentration, with sugar-ethanol companies such as Raízen, Tereos, and Bunge managing sucrose supply, while multinational ingredient companies like Cargill, Ingredion, Archer Daniels Midland (ADM), Tate & Lyle, DuPont, and DSM-Firmenich lead in high-intensity and specialty sweeteners. Raízen's launch of the world's largest second-generation ethanol plant in May 2024, a facility costing BRL1.2 billion (USD 240 million) and producing 82 million liters annually, demonstrates how sugar-ethanol producers are diversifying into advanced biofuels to address the long-term decline in sucrose demand. This strategy positions sweetener production as a secondary product rather than a primary focus. Such diversification helps maintain pricing stability in the sucrose market, as producers can shift crushing capacity toward ethanol production when sugar margins decrease, creating a structural cost floor that natural high-intensity sweeteners find difficult to compete with in cost-sensitive applications.

Bunge's acquisition of full control of Usina Moema in January 2025 for approximately USD 896 million consolidates its crushing capacity at 15.4 million tonnes. This move enables the company to optimize sugar-ethanol spreads and supply starch-sweetener feedstocks. The market is also seeing opportunities in fermentation-derived natural sweeteners and multifunctional blends that address cost, taste, and regulatory challenges. These innovations are gaining traction as they cater to evolving consumer preferences and regulatory requirements. Companies are increasingly focusing on solutions that balance affordability with functionality, ensuring they meet the demands of both domestic and international markets.

The Avansya joint venture between Cargill and DSM-Firmenich, which received approval from the European Union and the United Kingdom for fermentation-derived EverSweet stevia in January 2024, highlights how biosynthetic production methods can overcome Brazil's limitations in stevia cultivation. This development allows manufacturers to cater to premium export-oriented markets. By leveraging biosynthetic routes, companies can bypass agronomic constraints and provide high-quality sweeteners that meet global standards. This approach not only enhances product offerings but also strengthens the competitive positioning of Brazilian manufacturers in the international market.

Brazil Food Sweetener Industry Leaders

Cargill, Incorporation

Ingredion Incorporated

Archer Daniels Midland Company

Raízen S.A.

Tereos SCA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Lesaffre acquired a 70% stake in Biorigin/Zilor, a Brazilian producer of yeast derivatives and fermentation substrates, for an undisclosed amount. This acquisition enhances Lesaffre's portfolio of natural-origin ingredients and strengthens its ability to supply organic and clean-label inputs to food manufacturers adapting to ANVISA's front-of-package labeling requirements.

- May 2024: Raízen has inaugurated an ethanol plant in São Paulo state, representing an investment of BRL 1.2 billion (USD 240 million) and producing 82 million liters annually from sugarcane bagasse and straw. This facility highlights how sugar-ethanol producers are addressing potential long-term declines in sucrose demand by diversifying into advanced biofuels, positioning sweetener production as a co-product rather than the primary business focus.

- February 2024: Amaggi acquired a stake in Milhão Ingredients, a Brazilian corn processor with an annual capacity of 280,000 tonnes, specializing in non-GMO corn derivatives. This investment aligns with Amaggi's strategy to enhance margins in value-added ingredients, such as starch sweeteners and sugar alcohols, while utilizing Brazil's well-established corn-processing infrastructure.

Brazil Food Sweetener Market Report Scope

Sweeteners are the various natural and artificial substances that impart a sweet taste to foods and beverages. Brazil's food sweetener market is segmented by type and application. Based on the type, the market is segmented into sucrose, starch sweeteners and sugar alcohols, and high-intensity sweeteners (HIS). Starch sweeteners and sugar alcohols are further sub-segmented into dextrose, high fructose corn syrup (HFCS), maltodextrin, sorbitol, and other starch sweeteners and sugar alcohols. The high-intensity sweeteners (HIS) are further sub-segmented into sucralose, aspartame, saccharin, neotame, stevia, cyclamate, acesulfame potassium (Ace-K), and other applications. Based on the application, the market is segmented into bakery and confectionery, dairy and desserts, meat and meat products, soups, sauces and dressings, and other applications. For each segment, market sizing and forecast have been done based on value (USD million).

By Product Type

| Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | |

| High Fructose Corn Syrup (HFCS) | ||

| Maltodextrin | ||

| Sorbitol | ||

| Xylitol | ||

| Other Starch Sweeteners and Sugar Alcohols | ||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose |

| Aspartame | ||

| Saccharin | ||

| Neotame | ||

| Cyclamate | ||

| Acesulfame Potassium (Ace-K) | ||

| Other Artificial HIS | ||

| Natural High-Intensity Sweeteners | Stevia Extract | |

| Monk Fruit Extract | ||

| Other Natural HIS | ||

| Other Sweeteners | ||

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Soups, Sauces, and Dressings |

| Other Applications |

By Form

| Powder |

| Liquid |

| Crystal |

By Category

| Conventional |

| Organic |

| By Product Type | Sucrose | ||

| Starch Sweeteners and Sugar Alcohols | Dextrose | ||

| High Fructose Corn Syrup (HFCS) | |||

| Maltodextrin | |||

| Sorbitol | |||

| Xylitol | |||

| Other Starch Sweeteners and Sugar Alcohols | |||

| High-Intensity Sweeteners | Artificial High-Intensity Sweeteners | Sucralose | |

| Aspartame | |||

| Saccharin | |||

| Neotame | |||

| Cyclamate | |||

| Acesulfame Potassium (Ace-K) | |||

| Other Artificial HIS | |||

| Natural High-Intensity Sweeteners | Stevia Extract | ||

| Monk Fruit Extract | |||

| Other Natural HIS | |||

| Other Sweeteners | |||

| By Application | Bakery and Confectionery | ||

| Dairy and Desserts | |||

| Beverages | |||

| Soups, Sauces, and Dressings | |||

| Other Applications | |||

| By Form | Powder | ||

| Liquid | |||

| Crystal | |||

| By Category | Conventional | ||

| Organic | |||

Key Questions Answered in the Report

What is the current value of the Brazil food sweetener market?

The market is valued at USD 6.28 billion in 2026 and is forecast to reach USD 7.86 billion by 2031.

Which segment is growing fastest within Brazilian sweeteners?

High-intensity sweeteners lead with a projected 5.66% CAGR through 2031, boosted by regulatory approvals and demand for zero-calorie products.

How will proposed beverage taxes affect sweetener demand?

A selective tax on sugar-sweetened beverages would likely accelerate reformulation toward non-nutritive sweeteners, especially in carbonated soft drinks.

Why are fermentation-derived stevia products important for Brazil?

Fermentation sidesteps agronomic limits and supplies premium Rebaudioside M and D, enabling clean-label claims and export compliance.

Page last updated on: