Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

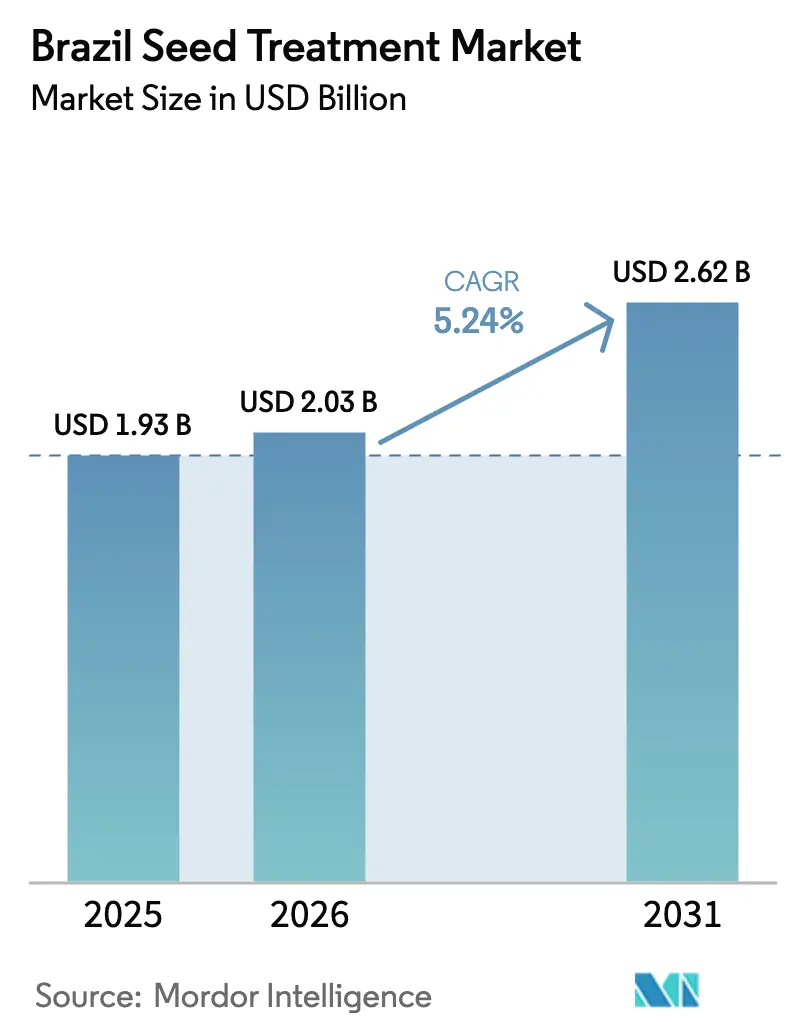

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.03 Billion |

| Market Size (2031) | USD 2.62 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Seed Treatment Market Analysis by Mordor Intelligence

The Brazil seed treatment market is valued at USD 1.93 billion in 2025 and is estimated to grow from USD 2.03 billion in 2026 to reach USD 2.62 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). Synthetic chemicals still account for a high share of spending, yet growers are shifting toward biological formulations as China tightens residue limits and Brazil scales up its National Bioinputs Program. Fungicidal coatings continue to play a crucial role in disease control, but rising losses from soybean cyst nematodes are redirecting investment toward higher-value nematicide offerings. Seed coating remains the prevalent application method, although polymer-based pelleting systems are gaining favor because they protect microbial actives and minimize dust during high-speed planting. Grain and cereal plantings dominate demand, yet expanding peanut and common bean acreage is broadening the market for crop-specific treatment blends tailored to legume and secondary oilseed pest complexes.

Key Report Takeaways

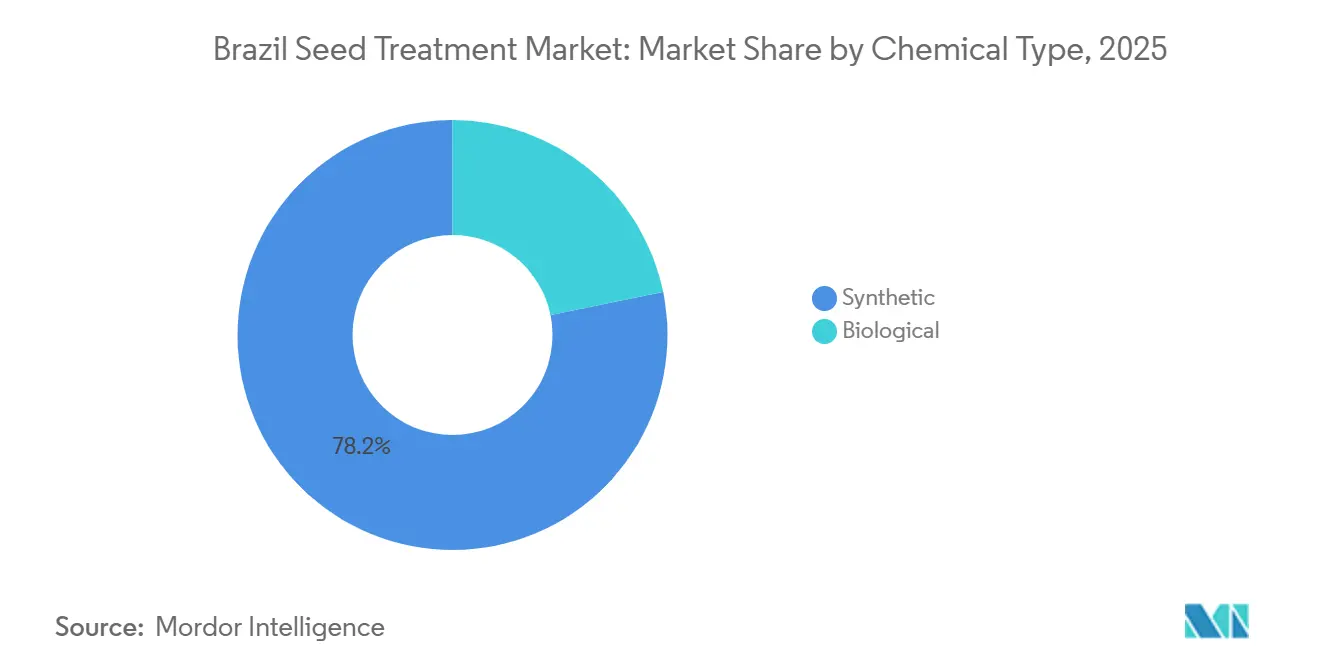

- By chemical type, synthetic formulations held 78.2% of the Brazil seed treatment market share in 2025, while biologicals deliver the highest forecast growth at 7.5% CAGR through 2031.

- By product type, fungicides accounted for the largest revenue share of 45.3% in 2025. Nematicides are advancing at an 8.1% CAGR to 2031.

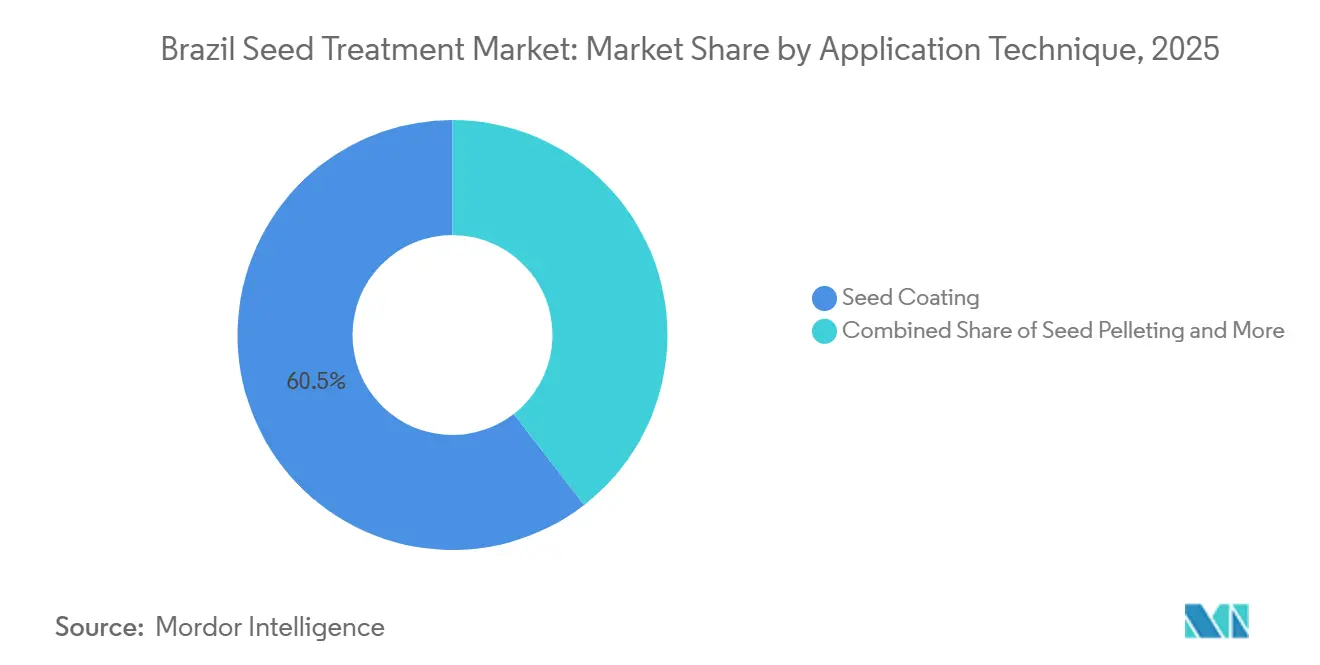

- By application technique, seed coating accounted for 60.5% of the Brazil seed treatment market size in 2025, while pelleting is projected to expand at a 7.2% CAGR through 2031.

- By crop type, grains and cereals accounted for 38.1% of the Brazil seed treatment market size in 2025. Pulses and oilseeds posted the fastest 8.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming soybean exports driving seed-quality investments | +1.2% | Mato Grosso, Paraná, Rio Grande do Sul | Medium term (2-4 years) |

| Rise in biological formulations complying with Brazil's zero-residue targets | +0.9% | Export-oriented farms nationwide | Long term (≥ 4 years) |

| Intensifying seed-borne disease pressure from climate change | +0.8% | Center-West and South | Short term (≤ 2 years) |

| Adoption of on-farm mobile seed-treatment units | +0.6% | Mato Grosso, Goiás, Bahia | Medium term (2-4 years) |

| Digital advisory platforms bundling seed treatment recommendations | +0.5% | Tech-led cooperatives | Long term (≥ 4 years) |

| Government subsidies on low-toxicity agro-inputs | +0.7% | Family farms nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Soybean Exports Driving Seed-Quality Investments

Brazil shipped 104 million metric tons of soybeans in 2024, and domestic output is forecast to hit 169 million metric tons in 2025/26, cementing soybean export premiums that reward residue-free production [1]Source: Oilseeds and Products Annual, United States Department of Agriculture Foreign Agricultural Service, apps.fas.usda.gov. Chinese buyers enforce near-zero pesticide limits, so growers view premium biological coatings as the first defense that preserves export contracts. Estate managers integrate certificates of analysis into shipping documents, reducing dockside rejections. The federal B20 biodiesel mandate lifts domestic soy-oil demand and tightens supply, reinforcing willingness to pay for high-quality seed. As a result, the Brazil seed treatment market records penetration rates that outpace overall crop-protection spending.

Rise in Biological Formulations Complying with Brazil's Zero-Residue Targets

Law 15,070 of 2024 established a USD 183 million (BRL 1 billion) credit line for biological inputs and reduced the Agência Nacional de Vigilância Sanitária (ANVISA) approval period for qualified microbial products from 36 to under 12 months [2]Source: National Bioinputs Program, Ministry of Agriculture and Livestock, gov.br. Approvals for 612 biopesticides between 2020 and 2024, with 28% intended for seed treatment, validate regulatory momentum. Trichoderma, Bacillus, and Bradyrhizobium inoculants are now co-applied with synthetics, reducing the active load by 30 to 40% while maintaining vigor. UPL’s Bioplanta facility produces 50 million liters of biological coatings annually, underscoring scale. FMC Corporation and Ballagro embed nitrogen fixation and phosphate solubilization in one pass, attractive in Cerrado soils where phosphorus lock-up harms yields. Together, these developments reinforce the 7.50% CAGR posted by biologicals within the Brazil seed treatment market.

Intensifying Seed-Borne Disease Pressure from Climate Change

A 1.2°C temperature rise and a 15% increase in extreme rainfall since 2000 create conditions for Fusarium and Rhizoctonia outbreaks [3]Source: Climate Change Impacts on Brazilian Agriculture, MDPI, mdpi.com. Wheat blast and soybean rust now start earlier and last longer, squeezing the window for foliar rescues. Nematode populations, notably Pratylenchus brachyurus, migrate northward as warmer soils accelerate the cycle, and 76% of sampled soybean plots in Mato Grosso exceed economic thresholds. Consequently, nematicidal seed treatments are standard, propelling the highest 8.1% product-category CAGR. Climate models predict an additional 1.5 to 2 °C warming by 2040, underscoring disease pressure as a key structural driver for the Brazil seed treatment market.

Adoption of On-Farm Mobile Seed-Treatment Units

Estates exceeding 10,000 hectares deploy Solubio and Grazmec equipment to bypass toll bottlenecks and tailor biological blends at planting. Through one-pass polymer coating, liquid biologicals and chemicals can be turned around from weeks to hours, safeguarding microbial viability. Solubio’s OnFarm Biofactories reduce the inoculant cost by 40% while ensuring cell counts above 10^9 CFU per seed. Grazmec systems adjust polymer thickness using near-infrared sensors, enhancing uniformity and reducing waste. Leasing spreads extend reach to mid-sized farms, supporting additional growth in the Brazil seed treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of Genetically Modified Organism seed traits with in-built resistance | -0.8% | Nationwide soybeans and corn | Short term (≤ 2 years) |

| Limited smallholder access to application equipment | -0.5% | Northeast and North interior | Medium term (2-4 years) |

| Stringent ANVISA re-registration process delaying product launches | -0.4% | National | Long term (≥ 4 years) |

| Price sensitivity amid fertilizer-price shocks | -0.6% | Growers under margin stress | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Genetically Modified Organism Seed Traits With In-Built Resistance

Transgenic soybeans cover 99% of 47.6 million hectares in 2024/25, providing in-plant protection against lepidopteran pests and soybean cyst nematode, cutting insecticide and nematicide coating needs by 15 to 20%. Corn hybrids post similar penetration at 96%. While fungicidal seed treatments remain essential, Genetically Modified Organism (GMO) traits do not address seed-borne pathogens. The overall restraint on market growth is material, particularly in the insecticide and nematicide product categories. Trait licensing fees, which add USD 15 to USD 25 per hectare, are being absorbed by growers as a substitute for seed treatment costs, reinforcing the substitution dynamic.

Limited Smallholder Access to Application Equipment

Farms smaller than 50 hectares constitute 77% of agricultural holdings but contribute only 23% of total output, primarily due to limited access to capital for treatment systems costing between USD 5,000 and USD 300,000. Toll services, which charge USD 3-8 per hectare, are often avoided by smallholders. Additionally, biological products requiring refrigeration face significant distribution challenges in remote areas. Without credit lines that include equipment financing, adoption in this segment will remain limited, restricting the market's reach. This access gap hampers market penetration among smallholders, who represent 40% of Brazil's total crop area, thereby reducing the addressable base for the seed treatment market and slowing volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Chemical Type: Biologicals Scale Despite Synthetic Dominance

Synthetic formulations retained 78.2% of the Brazil seed treatment market share in 2025 due to their validated efficacy and lower upfront costs. Biologicals, however, are recording a 7.5% CAGR, as zero-residue certification and faster approvals from the Agência Nacional de Vigilância Sanitária (ANVISA) are boosting confidence. Trichoderma fungicides and Bradyrhizobium inoculants are mainstream in soybeans, while hybrid products, such as BASF SE Poncho Votivo, combine chemical and microbial actives for complementary control. Rovensa's acquisition of Cosmocel for USD 76 million (EUR 70 million) in May 2022 contributed USD 33 million (BRL 180 million) in biological revenue, highlighting strong investor interest.

Margin-oriented domestic growers still rely on lower-priced synthetics, yet export estates in Mato Grosso and Paraná favor biological stacks that avoid residue rejections. Field trials have shown that Trichoderma coatings reduce Fusarium incidence by 40% and increase yield by 3-5%, resulting in a return that offsets the premium pricing. As cold-chain logistics expand and formulation shelf life improves, biological penetration could reach 30% by 2031, recalibrating competitive positioning in the Brazil seed treatment market.

By Product Type: Nematicides Outpace Fungicides

Fungicides dominated 45.3% of 2025 revenue, reflecting non-substitutable protection against seed-borne fungi, yet nematicides enjoy an 8.1% CAGR because soybean cyst nematode drives USD 1.5 billion in losses annually. Abamectin and fluopyram coatings are routine in high-pressure fields. Although a nematode-resistant trait aims for high adoption by 2028, seed treatments remain essential for non-trait crops such as cotton and sugarcane.

Other product types, including growth regulators and micronutrient coatings, account for the residual share and are expanding modestly as precision agriculture platforms enable tailored seed treatment prescriptions. Syngenta's Vibrance Integral, which combines fungicide, insecticide, and nematicide actives in a single formulation, exemplifies the industry's move toward multi-functional products that simplify application and reduce labor costs.

By Application Technique: Pelleting Picks Up Speed

Seed coating accounted for 60.5% of 2025 sales, primarily due to the use of legacy equipment and improved throughput efficiency. Pelleting posts a 7.2% CAGR because polymer shells meter active release, improve singulation, and boost microbial survival. Trials in Paraná showed that pelleted seeds maintained 90% germination under drought conditions, compared with 78% for conventional coatings. Grazmec machines adjust layer thickness via near-infrared feedback, enhancing consistency.

Seed dressing remains prevalent among smallholders because entry costs are minimal, yet growth levels off as cooperatives upgrade to coating lines. Film coating and priming are gaining popularity in high-value vegetables and turf, where seed value per unit justifies extra cost. As on-farm seed treatment units proliferate, pelleting is becoming the preferred technique for large estates that prioritize customization and just-in-time application, while coating remains dominant in toll treatment and cooperative facilities where throughput and cost control are paramount.

By Crop Type: Pulses and Oilseeds Diversify Demand

Grains and cereals contributed 38.1% of the 2025 value, led by soybeans and corn. Pulses and oilseeds posted the fastest 8.8% CAGR through 2031. Peanut cultivation, concentrated in São Paulo and Mato Grosso, is benefiting from rotation programs that break soybean disease cycles and improve soil health. Peanut seed treatments targeting Aspergillus flavus and aflatoxin contamination are mandatory for export markets, driving demand for specialized fungicide formulations. According to the United States Department of Agriculture's Foreign Agricultural Service, sunflower, cultivated on 150,000 hectares in Mato Grosso and Goiás, is emerging as a rotation crop for soybeans and cotton, with seed treatments targeting Sclerotinia and downy mildew gaining traction in 2024.

Commercial crops, such as cotton, employ seed treatments against the boll weevil, where GMOs fall short, and sugarcane uses coatings for smut in seedling propagation. High-value fruit and vegetable acreage remains small but favors advanced pelleting for transplant success. Turf and ornamentals meet the urban landscaping demand around the São Paulo stadium construction, although the volume remains minor in the broader Brazil seed treatment market.

Geography Analysis

The Center-West and South regions account for a significant portion of soybean and corn acreage, thereby driving the Brazil seed treatment market size at the regional level. Mato Grosso alone plants 12.3 million hectares of soybeans and leads the adoption of on-farm coating and pelleting units, which enable estates to tailor biological blends. Paraná and Rio Grande do Sul contribute significantly to the national soybean and wheat production in 2024. Growers in these regions prioritize fungicidal coatings to address wheat blast and soybean sudden-death syndrome, particularly in humid climates. In Paraná, state grants for cooperative equipment costs are driving the adoption of biological solutions among mid-sized farms.

Goiás and Bahia, key states within the MATOPIBA frontier, are expanding soybean and cotton cultivation on reclaimed Cerrado soils, driving the fastest-growing demand for nematicidal coatings to combat root-lesion nematodes. Mobile pelleting systems from Grazmec optimize polymer thickness in real-time, enhancing uniformity across large seed lots and contributing to advancements in the Brazil seed treatment market. Producers in these frontier states also incorporate micronutrient primers to address phosphorus lock-up, a common issue in acidic soils.

The Northeast and North regions account for a significant number of agricultural establishments but only 15% of the cropped area, indicating the prevalence of small plots that seldom utilize treatment equipment. Toll services are priced between USD 3-8 per hectare, a cost that many family growers avoid, resulting in a penetration rate approximately 25% below the national average. The National Bioinputs Program offers subsidized credit to these regions, aiming to increase biological adoption to over 30% of hectares by 2028. In areas such as São Paulo and Rio de Janeiro, landscape contractors invest in high-value turf and ornamental coatings for stadium and park projects. However, this segment remains a niche within the overall seed treatment market in Brazil.

Regulatory Landscape

Seed treatment in Brazil sits under the National System of Seeds and Seedlings (SNSM) framework established by Law 10.711/2003 and regulated by Decree 10.586/2020, with the Ministerio da Agricultura e Pecuaria (MAPA) overseeing seed production, certification, treatment, and trade. Companies performing production, beneficiation, or treatment activities must hold registration in the National Registry of Seeds and Seedlings (RENASEM), which ties commercial seed-treatment operations to facility-level compliance and traceability requirements.

For crop-protection actives used in seed treatment, Brazil runs an inter-agency process involving MAPA alongside ANVISA and IBAMA. A procedural change took effect in September 2025: pesticide registration requests must be submitted exclusively to MAPA, which then coordinates the competent bodies (Ato CGAA no. 40 dated September 1, 2025), applied as of September 15, 2025. Treated seed lots also face mandatory visual differentiation and labeling obligations, including disclosure of active ingredient, dosage, treatment date, and withdrawal period. Export seed treatment can require MAPA authorization when importing-country phytosanitary standards demand pesticides not approved for the target crop in Brazil.

Competitive Landscape

The Brazil seed treatment market is highly concentrated, with five multinational companies, namely Syngenta Group, BASF SE, Corteva Agriscience, FMC Corporation, and Bayer AG, dominating the market in 2025. Syngenta Group’s Vibrance Integral mixes three actives in one coating, while Bayer AG locks growers into its Intacta 5+ trait that ships with prescribed treatments. Corteva Agriscience aims to capture a significant market share by integrating treatment recommendations into its digital platform, which supports planting decisions across more than 5 million hectares of land.

Regional specialists are scaling fast in biologicals. Rovensa added USD 33 million in microbial revenue through its USD 76 million Cosmocel acquisition in May 2022, extending its reach into Mato Grosso and Goiás. Sumitomo bought Nufarm’s South American assets for USD 1.2 billion, gaining a strong distributor network for hybrid coatings. Solubio and Grazmec partner with input makers to sell turnkey on-farm units that integrate hardware, biologicals, and data analytics, capturing estates that want full control over seed quality.

Agência Nacional de Vigilância Sanitária (ANVISA)'s fast-track Reference Specification pathway favors microbial products, shortening the time-to-market to one year, while synthetic re-registrations can take four years and cost up to USD 5 million. Suppliers with deep microbial R&D pipelines, such as UPL Limited and Rizobacter Argentina SA (Bioceres Crop Solutions Corp.), therefore gain speed and margin advantages. Equipment innovators also blur traditional boundaries as they secure recurring revenue from biological refill contracts. Competition is projected to intensify as digital platforms funnel purchasing data to preferred partners, raising switching costs and reinforcing current leadership positions in the Brazil seed treatment market.

Brazil Seed Treatment Industry Leaders

BASF SE

Corteva Agriscience

FMC Corporation

Syngenta Group

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Bioinputs and low-residue seed treatment stacks create openings in export-linked soy and corn systems and in Cerrado production where microbial nutrition and biological protection are increasingly combined into single-pass applications. The Bioinputs regulatory framework (Law No. 15,070/2024) entered into force on December 24, 2024, improving the operating environment for biological inputs through clearer rules on production, registration, and use, and supporting faster biological registration timelines (commonly cited at 6-12 months) through coordinated review involving MAPA, ANVISA, and IBAMA. Industry momentum is also reflected in the scale of bio-input commercialization activity cited for 2025 (BRL 6.2 billion revenue and 162 new bio-input products registered), which broadens the range of microbial and bio-based actives available for seed-applied use in Brazil.

A further opportunity is building industrial treatment platforms and agronomic advisory models around advanced formulations, including polymers and pelleting that protect microbial viability and reduce dust, to improve performance consistency across large soybean and corn seed volumes and to extend adoption beyond top-tier estates. In June 2026, Bayer marked 15 years of its SeedGrowth Center in Paulinia (SP), reinforcing ongoing investment in seed-treatment-focused capability and integrated crop-protection positioning. Equipment-linked service models, whether on-farm or through cooperatives, also address a practical bottleneck in the market context: access to treatment quality and timing, while enabling suppliers to attach recurring biological refills and stewardship programs to installed treatment capacity.

Recent Industry Developments

- July 2026: Corteva Agriscience partnered with Arevo to add arginine-based seed treatment nutrition technology for soybeans, with stated plans to expand the technology into Brazil by 2027. The update extends the seed-treatment value proposition beyond protection into nutrition and vigor, creating differentiation in a highly concentrated supplier landscape.

- August 2025: BASF SE, Corteva Agriscience, and M.S. Technologies signed an agreement to bring a new soybean trait stack to the Brazilian market. Trait-led pest and nematode protection increases substitution pressure on certain chemical seed treatment segments, pushing suppliers to compete more through integrated packages that combine genetics, treatment systems, and complementary biologicals.

- September 2024: Corteva Agriscience launched Lumitreo, a soybean seed-treatment fungicide in Brazil formulated with oxathiapiprolin, picoxystrobin, and ipconazole for early-stage disease control. The launch reinforced multi-active fungicide positioning in a market where fungicides hold the largest product-type share and where growers prioritize stand establishment and uniformity under disease pressure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this methodology, the Brazil seed treatment market means the value of products applied to seeds before sowing to protect early crop growth and improve seed performance through common treatment techniques.

Scope exclusions: We exclude general crop protection sprayed after planting and non-treatment seed processing steps such as cleaning and simple grading.

Segmentation Overview

- By Chemical Type

- Synthetic

- Biological

- By Product Type

- Insecticides

- Fungicides

- Nematicides

- Other Types

- By Application Technique

- Seed Coating

- Seed Pelleting

- Seed Dressing

- Other Techniques

- By Crop Type

- Commercial Crops

- Fruits and Vegetables

- Grains and Cereals

- Pulses and Oilseeds

- Turf and Ornamentals

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context for treated seed in Brazil, and then matching it with seed treatment use practices by crop. We mainly use public series such as Brazilian agricultural statistics and crop area data, trade and tariff lines for crop inputs, and official pesticide registration and label information where available.

To structure assumptions, we also use sources such as FAOSTAT for crop production signals, Brazilian government agriculture agencies for planting area and yield direction, customs statistics for import and export indicators, peer-reviewed agronomy studies on seed-borne disease pressure and treatment efficacy, and association publications that discuss seed quality and treatment practices. Company annual reports, investor presentations, and reputable press are used to sanity-check pricing direction, product mix shifts, and channel changes. A paid subscription for company financials and a patent database are used selectively to validate innovation and portfolio changes. These desk sources are not exhaustive, and many other public references were also used for data collection, validation, and clarifying questions during the study.

Primary Interviews and Surveys

Primary work is used to convert general crop and seed facts into Brazil-specific treatment rates, dosage norms, and price ranges that are actually used in the field. We spoke with seed processors, input distributors, agronomists, and large farm operators to confirm what is applied by crop and how adoption changes by region and season.

Since this is a country study, inputs were validated across major producing states and customer types so that desk assumptions could be corrected, and the final numbers could be triangulated against on-ground purchasing and application behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 61% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where planted area and seed usage by key crops are translated into a treated-seed demand pool using crop-level treatment rates, typical active-ingredient loading, and average selling prices for the applied solutions. After that, the totals are cross-checked using selective bottom-up approximations, such as rolling up a sample of supplier and distributor revenues, and validating implied volume by comparing it with seed processing throughput and channel checks.

A few practical inputs shape the model, including soybean and corn acreage shifts, the share of certified versus farm-saved seed, regional disease and pest pressure that drives preventive treatment, the split between chemical and biological solutions, and observed price movement by formulation and pack size. Where direct data is thin for smaller crops, we fill gaps using analog crops with similar agronomy, and then adjust using interview feedback so we do not overstate adoption.

For forecasting, scenario analysis is used and then narrowed using consensus views from primary experts on seed quality demand, regulation-driven product changes, and expected cropping mix. This keeps the forecast explainable and it stays tied to variables that can be refreshed each year with new planting and pricing signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including implied spend per hectare, adoption versus seed sales direction, and consistency checks against known pricing bands shared by channel participants. When results look off, the assumptions are revisited, outliers are questioned, and follow-up calls are triggered to confirm whether the shift is real or just a data artifact.

Before sign-off, the model goes through a multi-step internal review so calculation logic, units, and conversion factors are consistently applied. The report is refreshed annually, with interim updates if a material event changes planting intent, regulation, or pricing, and a final freshness check is completed right before delivery so clients receive the latest view.

Mordor Intelligence's Brazil Seed Treatment Market Size Compared Against Other Published Estimates

Published market values for Brazil seed treatment can differ a lot, even when they use the same currency and similar years. The spread usually comes from what gets counted as seed treatment, which crops and regions are emphasized, and how pricing and adoption are projected forward.

Some external estimates roll in on-farm treatment services and broader seed-applied biological inputs, which can move the total up or down depending on what is bundled. In Mordor Intelligence's sizing, only the value of seed-applied treatment products within Brazil is counted, and the model is kept tied to treated-area adoption, typical dose rates, and checked price ranges rather than bundled service revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.03 B (2026) | |

| Industry Publisher A | USD 0.21 B (2025) | Uses a narrower value pool that can focus on selected crops and labeled application categories, and it can also treat biological inoculants and service elements differently, which reduces the counted spend versus a full treated-seed product view. |

| Industry Publisher B | USD 0.85 B (2023) | Often mixes study years and applies higher growth assumptions from an earlier base, and may not reconcile implied spend per hectare with crop-level treatment rates, leading to a mid-range figure that is not fully anchored to treated-area math. |

Across the three figures, the main drivers are scope choices and how adoption and pricing are translated into dollars by crop and technique. By keeping the calculation steps traceable to planted area, treatment penetration, and realistic price bands, the estimate stays balanced and easier to replicate when new crop and input signals come in.

Key Questions Answered in the Report

How large is the Brazil seed treatment market in 2026?

The Brazil seed treatment market size is USD 2.03 billion in 2026 and is forecast to reach USD 2.62 billion by 2031.

Which product category is expanding fastest?

Nematicides post the quickest 8.1% CAGR through 2031, because soybean cyst nematode infestations keep rising across key growing regions.

Why are biological seed treatments gaining share?

Strict residue limits from foreign buyers and the National Bio inputs Program's credit lines push biological formulations, which grow at 7.5% CAGR through 2031..

What regions adopt on-farm treatment systems most rapidly?

Estates in Mato Grosso, Goiás and Bahia lead on-farm adoption to tailor biological blends and avoid toll-plant bottlenecks.

Page last updated on: