Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

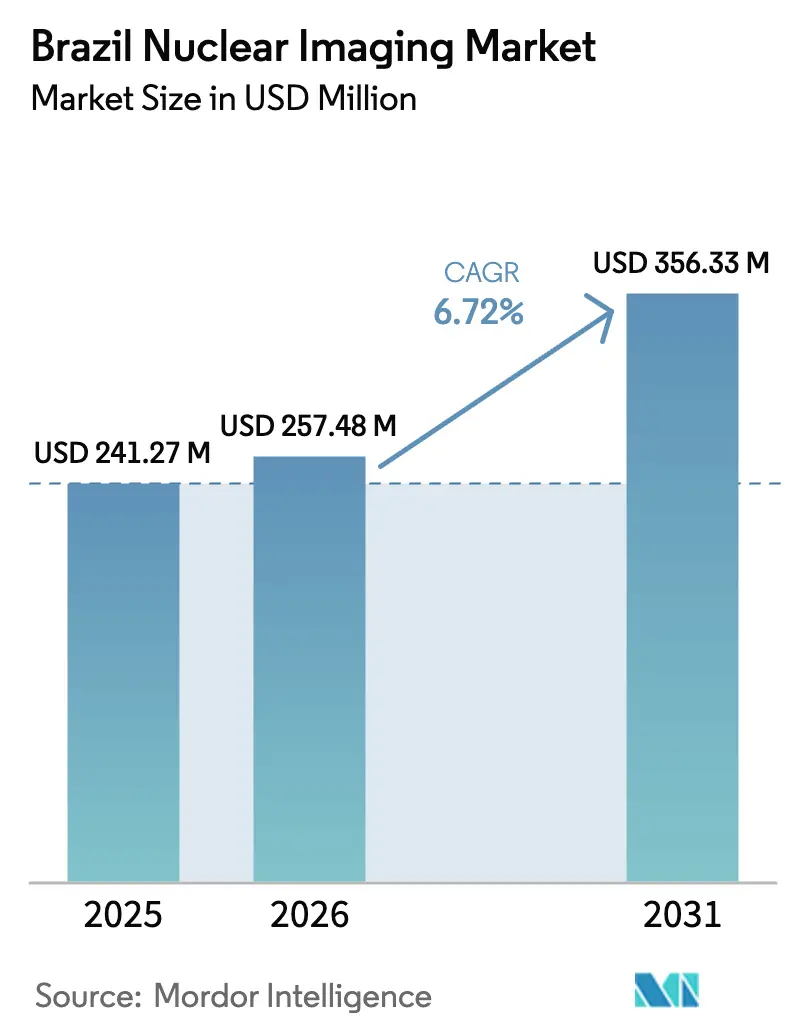

| Base Year Market Size (2025) | USD 241.27 Million |

| Market Size (2026) | USD 257.48 Million |

| Market Size (2031) | USD 356.33 Million |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

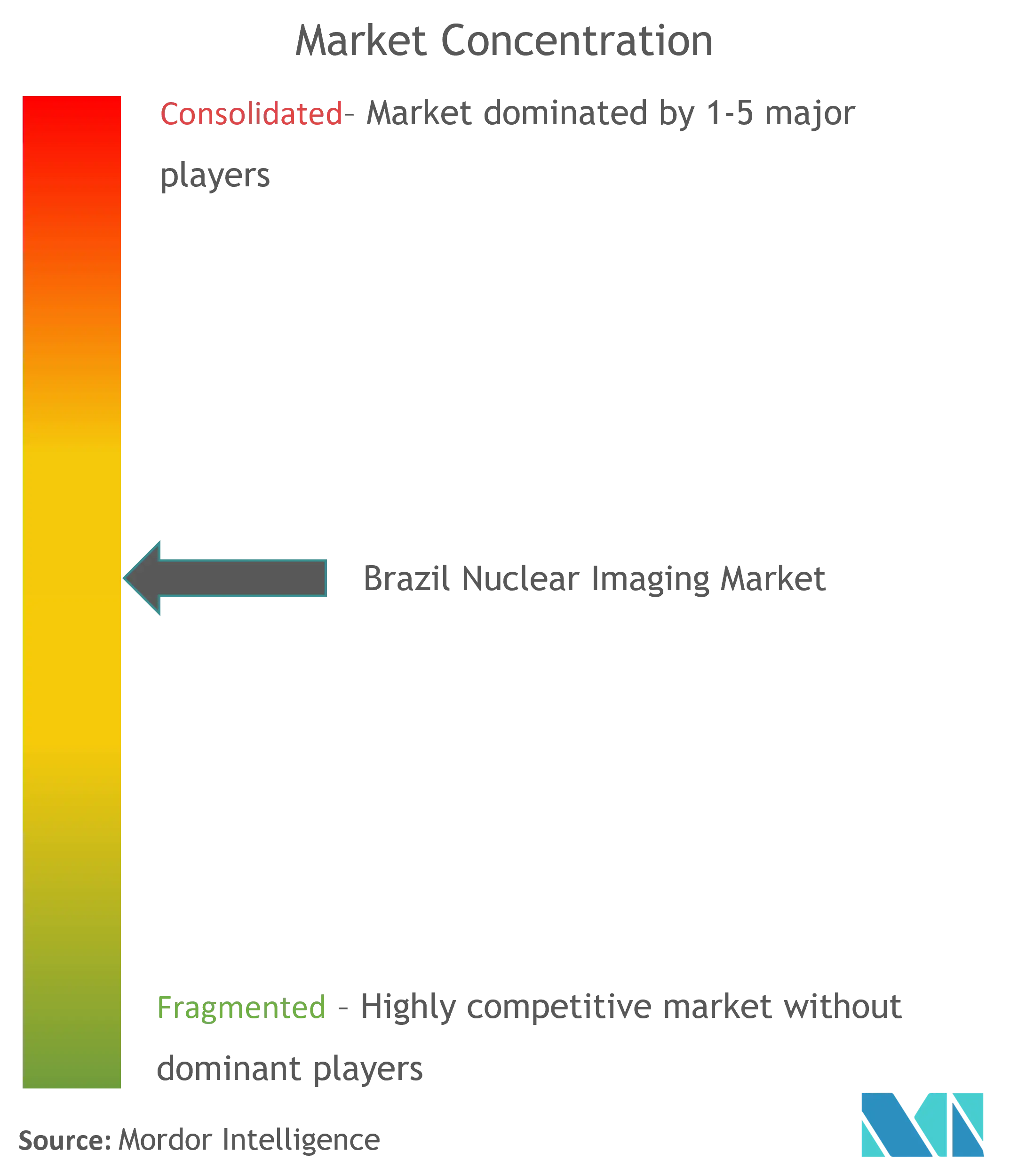

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Nuclear Imaging Market Analysis by Mordor Intelligence

Brazil nuclear imaging market size in 2026 is estimated at USD 257.48 billion, growing from 2025 value of USD 241.27 billion with 2031 projections showing USD 356.33 billion, growing at 6.72% CAGR over 2026-2031. Accelerated demand for precision diagnostics in oncology and cardiology, rapid uptake of digital PET/CT and full-ring CZT SPECT platforms, and federal investment in domestic molybdenum-99 production collectively underpin this trajectory. Private insurers continue to broaden coverage for high-complexity tests, while the Brazilian Multipurpose Reactor (RMB) in Iperó promises a resilient isotope supply chain. Competitive rivalry intensifies as hospital networks consolidate and outpatient imaging centers gain share, yet a shortage of nuclear-medicine specialists and high acquisition costs temper near-term growth momentum. Infrastructure modernization programs, public-private cyclotron partnerships, and e-labeling reforms by ANVISA are opening streamlined pathways for technology deployment.

Key Report Takeaways

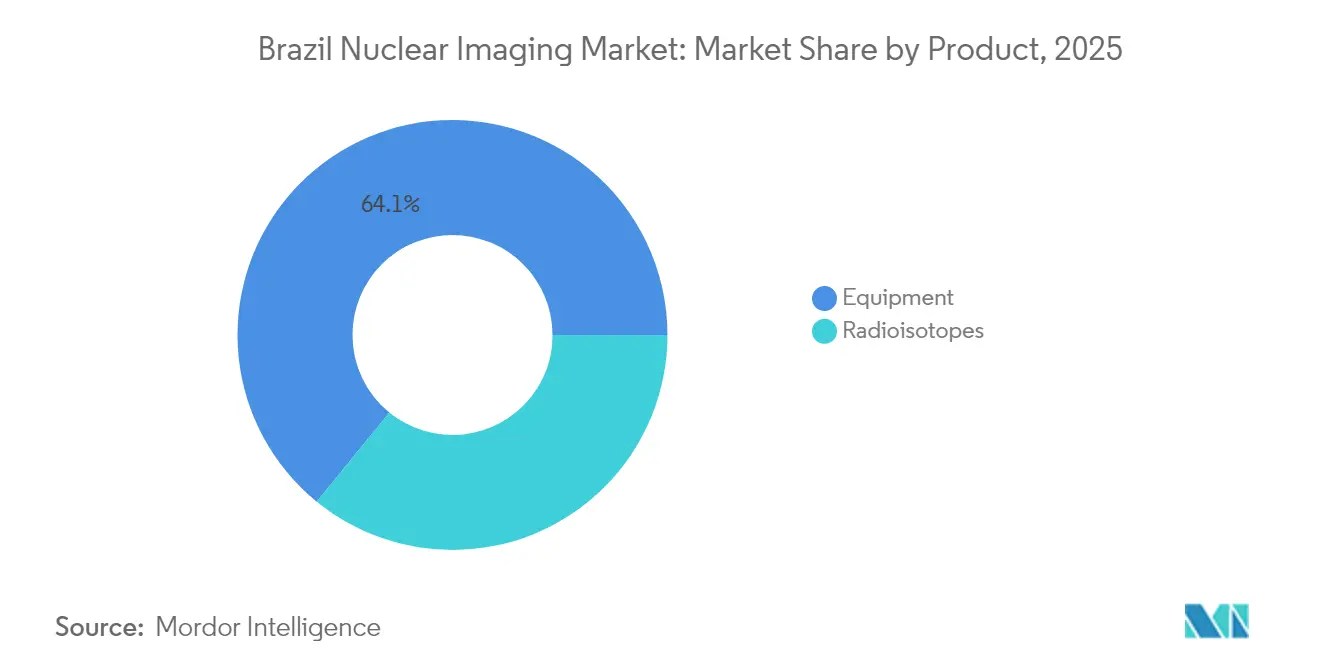

- By product, equipment led with 64.12% revenue share of the Brazil nuclear imaging market in 2025, Radioisotopes are projected to post the fastest 6.91% CAGR through 2031.

- By application, cardiology accounted for 63.21% of the Brazil nuclear imaging market share in 2025, Neurology imaging is forecast to grow at a 7.04% CAGR to 2031.

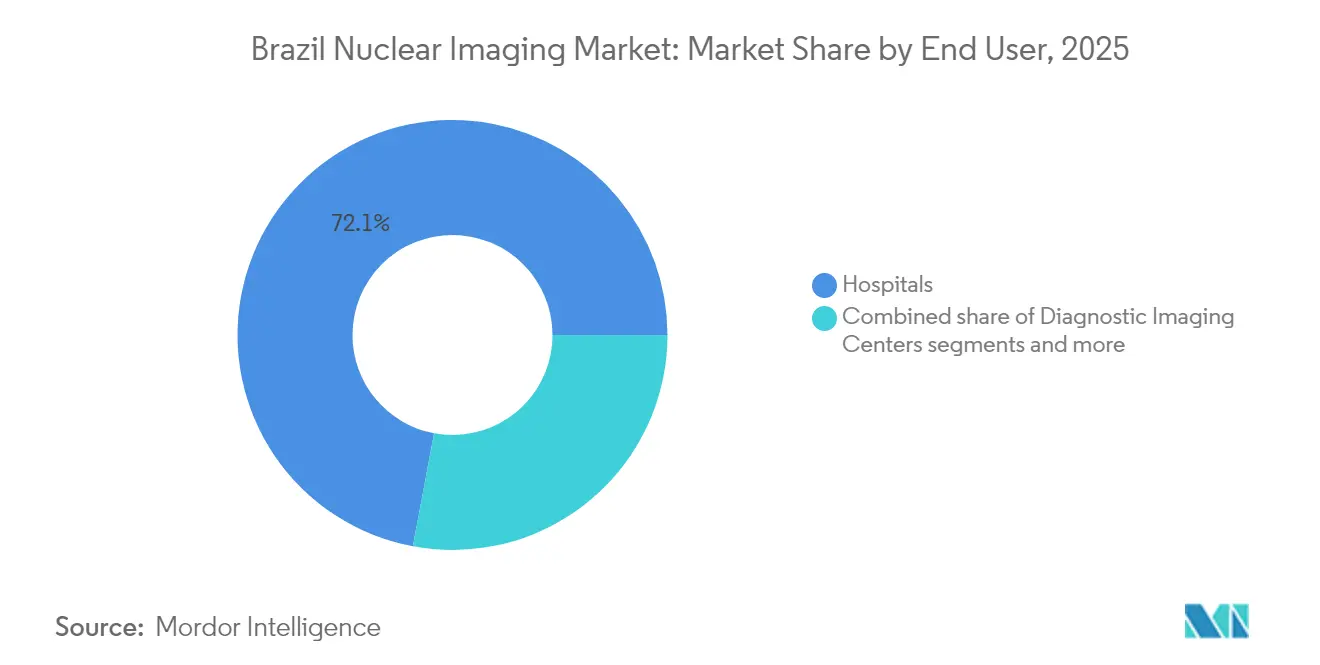

- By end user, hospitals held 72.05% of the Brazil nuclear imaging market size in 2025, Diagnostic imaging centers are expected to advance at a 6.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cancer & CVD incidence | +1.8% | National, concentrated in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Expansion of private health-insurance coverage | +1.2% | National, with early gains in São Paulo, Rio de Janeiro, Brasília | Short term (≤ 2 years) |

| Federal investments in domestically produced Mo-99 | +0.9% | National, centered on Iperó production facility | Long term (≥ 4 years) |

| Rapid adoption of digital & hybrid PET/CT platforms | +1.1% | National, led by major urban centers | Medium term (2-4 years) |

| New multipurpose research reactor (RMB) enabling isotope security | +0.7% | National, with distribution from Iperó hub | Long term (≥ 4 years) |

| Public-private cyclotron partnerships in underserved regions | +0.5% | Regional, targeting North and Northeast regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cancer & CVD Incidence

Cardiovascular diseases remain Brazil’s primary mortality cause, driving sustained uptake of technetium-99m myocardial perfusion imaging and accelerating deployment of cadmium-zinc-telluride cardiac-dedicated gamma cameras that cut scan times to 7 minutes. Rising prostate, breast, and thyroid cancer prevalence also fuels demand for PSMA-targeted and 18F-fluorodeoxyglucose PET/CT studies. PET/CT-guided biopsies are delivering higher diagnostic yields than CT-guided protocols, while Brazilian investigators present outcome data on neuroendocrine tumor therapies at international congresses, underscoring domestic clinical expertise.

Expansion of Private Health-Insurance Coverage

Private providers conduct 82% of nuclear procedures, reflecting insurer willingness to reimburse high-complexity exams. Sector revenue of BRL 1 trillion (USD 190.1 billion) in 2025, with private spending at 55%, supports fresh capital deployment into imaging suites. Fleury’s BRL 69.8 million acquisition of São Lucas Centro de Diagnósticos typifies regional roll-outs, and a BRL 250 million health-finance fund now advances up to 75% of procedure costs immediately after service delivery, easing facility cash-flow constraints.

Federal Investments in Domestically Produced Mo-99

The RMB reactor targets full national radioisotope self-sufficiency and will generate up to 3,500 antineutrinos daily alongside isotope output, ending reliance on imported molybdenum-99. IPEN’s IEA-R1 upgrade from 2 MW to 5 MW, combined with 84.4%-yield fission 99Mo purification routes, underlines technical capacity . CNEN’s designation of IPEN as an IAEA Collaborating Centre enhances quality assurance for isotope processing and nuclear security.

Rapid Adoption of Digital & Hybrid PET/CT Platforms

Studies comparing full-ring solid-state SPECT detectors to conventional Anger cameras show normal perfusion classification rising to 64.3% from 28.6%, validating technology leapfrogging. GE HealthCare’s MINItrace Magni and Omni Legend 21 cm PET/CT packages bring on-site tracer production to mid-sized hospitals, cutting radiopharmaceutical transit time and broadening theranostic access. PET/MRI adoption gains traction for neuro-oncology and cardiology indications, offering superior soft-tissue contrast with lower radiation doses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & upkeep cost of imaging systems | -1.4% | National, most pronounced in smaller municipalities | Short term (≤ 2 years) |

| Complex CNEN / ANVISA licensing procedures | -0.8% | National, affecting all nuclear medicine facilities | Medium term (2-4 years) |

| Workforce shortage of certified nuclear-medicine specialists | -1.1% | National, severe in North and Northeast regions | Long term (≥ 4 years) |

| Periodic supply disruptions of I-131 & Tc-99m isotopes | -0.6% | National, with regional distribution challenges | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Upkeep Cost of Imaging Systems

A PET/CT procedure currently costs USD 1,612.23 under academic wage scales and USD 1,023.47 at full 10-scan daily throughput, limiting small-facility economics. Fleury’s pivot toward joint ventures over outright purchases echoes industrywide capital-cost sensitivity. Maintenance of detectors and generator systems demands scarce technical expertise outside major cities, magnifying ownership burdens for interior clinics.

Workforce Shortage of Certified Nuclear-Medicine Specialists

Only 499 specialists serve a population of 203 million, with density ranging from 10.26 doctors per 1,000 residents in the South to 0.75 in the North. While 225 new medical courses opened in the past decade, specialty-training uptake is 8%, leaving the pipeline thin. IPEN’s continuing-education programs and tele-mentoring initiatives offer partial relief but do not offset steep geographic imbalances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment Dominance Drives Infrastructure Expansion

Brazil nuclear imaging market size for equipment reached USD 154.7 billion in 2025, representing 64.12% of total value. Hybrid PET/CT and SPECT/CT platforms account for the bulk of purchases as hospitals retire aging Anger cameras. Full-ring CZT SPECT systems improve coronary artery visualization and trim scan times, supporting higher patient throughput. The Brazil nuclear imaging market size for radioisotopes is forecast to rise at a 6.91% CAGR, propelled by RMB-enabled molybdenum-99 output and cyclotron expansion in underserved states. SPECT isotopes such as technetium-99m still represent 80% of procedure volume, yet PET tracers like 18F and 68Ga gain momentum in oncology and cardiology.

Financial hurdles persist. Capital cost per digital PET/CT exceeds USD 2 million, and rural clinics rely on leasing or volume-based vendor arrangements. GE HealthCare’s MINItrace Magni lowers tracer logistics costs, positioning mid-tier hospitals to upgrade. RMB production is slated to reduce 99Mo import costs by 40% once fully operational, enhancing isotope affordability. Long-term demand for PET/MRI remains niche due to USD 7 million price tags and high service requirements, yet early adopters cite diagnostic differentiation in neuro-oncology and congenital heart disease imaging.

By Application: Cardiology Leadership Faces Neurological Growth

Cardiology commanded a 63.21% share of the Brazil nuclear imaging market in 2025. Myocardial perfusion scintigraphy remains the clinical workhorse, supported by Brazilian Society of Cardiology guidelines affirming cost-effectiveness relative to invasive angiography . CZT detectors have cut scan times by 70%, allowing urban centers to clear backlogs and boost throughput. Neurology contributes the smallest revenue today but posts the highest 7.04% CAGR, lifted by Alzheimer’s and Parkinson’s disease prevalence and expanded access to amyloid-PET probes.

Oncology also accelerates on regulatory clearances of PSMA agents and alpha-emitter therapeutics. Thyroid applications remain stable, with 93.3% cure rates for Graves’ disease using radioiodine confirming therapeutic utility. The Brazil nuclear imaging market share for neurology is projected to double by 2031 as PET/MRI capacity broadens. Cardiac centers in São Paulo now integrate reserve-flow quantification, while regional hospitals in the Northeast focus on essential gated-SPECT protocols due to budget constraints.

By End User: Hospital Dominance Shifts Toward Specialized Centers

Hospitals represented 72.05% of Brazil nuclear imaging market size in 2025, reflecting their infrastructure advantage and critical-care alignment. Private hospital groups such as DASA and Rede D’Or are enlarging bed counts and investing in hybrid scanners to support cardiology and oncology service lines. Diagnostic imaging centers, however, register the quickest 6.86% CAGR as outpatient demand for shorter wait times rises. These stand-alone facilities increasingly sign reagent-supply contracts with isotope producers and adopt point-of-care PET radiopharmacy units.

Academic institutes and research hospitals collaborate with IPEN to trial theranostic protocols and train fellows, supplying a modest but strategic demand segment. Hospital-network consolidation continues: DASA’s proposed merger with Amil would create a 4,500-bed platform capable of bulk-buying scanners and negotiating favorable service contracts. Outpatient chains counter by emphasizing flexible scheduling, AI-assisted workflow, and Same-Day results, all of which strengthen their value proposition.

Geography Analysis

The Brazil nuclear imaging market shows strong regional concentration. São Paulo and Rio de Janeiro account for more than 55% of installed scanners and host the RMB and IPEN complexes, anchoring isotope logistics. Physician density in the South reaches 10.26 per 1,000 inhabitants, enabling higher per-capita procedure rates. Conversely, the North and parts of the Northeast face scant infrastructure and specialist shortages, limiting exam availability. The IAEA-donated SPECT camera in Niterói illustrates targeted interventions to bridge capability gaps.

New cyclotron ventures aim to supply short-lived PET tracers locally, cutting transport losses and stimulating regional demand. Government initiatives such as Programa Mais Médicos bolster general physician presence but stop short of nuclear specialization. State fiscal capacity shapes purchasing cycles: wealthier states upgrade to digital PET/CT on five-year timelines, while interior clinics depend on refurbished systems. Tele-nuclear medicine pilots link remote sites to metropolitan readers, partially offsetting specialist scarcity.

Urban networks leverage AI and cloud-PACS to centralize image interpretation, widening service radius without duplicating staff. Yet isotope supply remains vulnerable to logistics disruptions in Amazonian regions, where river transport causes delivery delays. RMB’s ramp-up, complemented by INB’s uranium exports, is expected to stabilize nationwide isotope availability by 2028. The Ministry of Health’s 800-bed digital hospital in São Paulo underscores public-sector commitment to smart healthcare infrastructure and may serve as a blueprint for other state capitals.

Competitive Landscape

The Brazil nuclear imaging market is moderately consolidated. Top equipment vendors—GE HealthCare, Siemens Healthineers, Philips, Canon Medical, and United Imaging—compete on detector innovation and workflow automation, while national service giants DASA and Fleury scale through acquisitions and joint ventures. DASA recorded record EBITDA in 2025 and seeks platform growth via merger with Amil, potentially expanding bargaining power over scanner procurement. Fleury favors partnerships to mitigate capital costs and taps regional niches.

Cyclotron operators such as Cyclobrás and RPH pursue vertical integration from isotope production to tracer distribution. The RMB project introduces state-controlled isotope capacity, shifting buyer leverage from importers to domestic suppliers. Regulatory reforms on e-labeling and software oversight require robust compliance, giving larger operators an administrative edge. Niche entrants target outpatient cardiac PET and neurological PET/MRI, differentiating on subspecialty reporting and quicker turnaround. Market entry barriers persist in rural zones due to physician scarcity and licensing complexity, yet public-private collaborations could unlock white-space opportunities in the North and Northeast.

Brazil Nuclear Imaging Industry Leaders

GE Healthcare

Grupo RPH

Siemens Healthineers AG

Canon Inc. (Canon Medical Systems Corporation)

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Telix Pharmaceuticals received Brazilian approval for a PSMA imaging agent, expanding precision oncology diagnostics

- March 2025: INB secured a contract to export 275,000 kg of uranium concentrate, underscoring Brazil’s upstream nuclear capability

Brazil Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer, cardiac and neurological disorders. Brazil Nuclear Imaging Market is segmented by Product (Equipment, and Diagnostic Radioisotope (SPECT Radioisotopes, and PET Radioisotopes), Application (SPECT Application (Cardiology, Neurology, Thyroid, and Other SPECT Applications), and PET Application (Oncology, Cardiology, Neurology, and Other PET Applications). The report offers the value (in USD million) for the above segments.

By Product (Value)

| Equipment | PET/CT Scanners | |

| SPECT/CT Scanners | ||

| PET/MRI Scanners | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

By Application (Value)

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other PET Applications |

By End User (Value)

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product (Value) | Equipment | PET/CT Scanners | |

| SPECT/CT Scanners | |||

| PET/MRI Scanners | |||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application (Value) | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other PET Applications | |||

| By End User (Value) | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

How large is the Brazil nuclear imaging market in 2026?

The Brazil nuclear imaging market size is USD 257.48 billion in 2026 and is projected to climb to USD 356.33 billion by 2031.

Which product category leads sales?

Equipment including PET/CT, SPECT/CT, and the first PET/MRI units accounts for 64.12% of 2025 revenue.

What application generates most demand?

Cardiology holds 63.21% of 2025 value because myocardial perfusion imaging is widely adopted for coronary artery disease assessment.

Where are most scanners located?

São Paulo and Rio de Janeiro concentrate over half of the nation's PET and SPECT installations, reflecting higher physician density and private investment.

Who are the key service providers?

DASA, Fleury, and Rede D'Or top the list, with DASA planning a 4,500-bed network that will deepen its imaging footprint.

What limits faster growth?

High equipment costs and a shortage of just 499 certified nuclear-medicine specialists nationwide constrain service expansion, especially in the North and Northeast.

Page last updated on: