Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

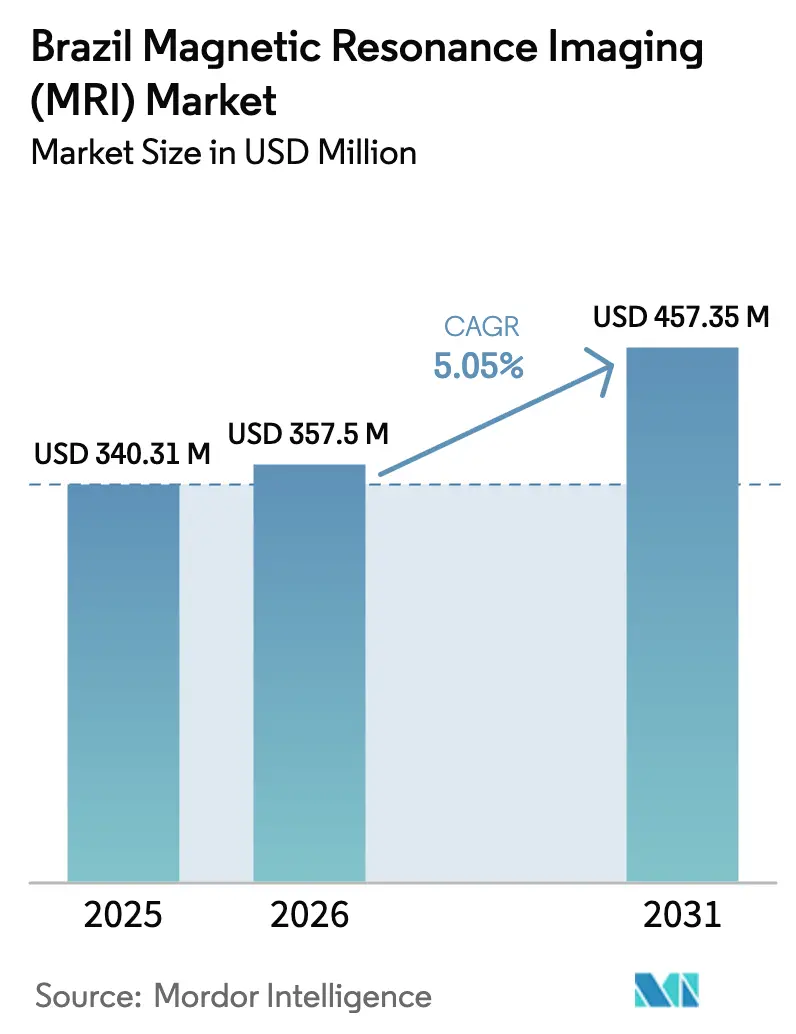

| Base Year Market Size (2025) | USD 340.31 Million |

| Market Size (2026) | USD 357.5 Million |

| Market Size (2031) | USD 457.35 Million |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Brazil Magnetic Resonance Imaging Market size was valued at USD 340.31 million in 2025 and is estimated to grow from USD 357.5 million in 2026 to reach USD 457.35 million by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

Private diagnostic chains are increasingly absorbing capital costs that public Sistema Único de Saúde (SUS) facilities often cannot justify, making private investment a critical driver of growth over technology availability. Rising demand, fueled by the prevalence of chronic diseases and academic hospitals' focus on ultra-high-field research, contrasts with limited public-sector upgrades due to low reimbursement rates. Structural challenges, including helium price volatility and an uneven distribution of radiologists, have concentrated capacity in the Southeast. However, larger providers are mitigating margin pressures through import-tax incentives and AI-driven workflow efficiencies. Competitive strategies now prioritize software bundles designed to reduce exam times and lower per-scan costs, positioning advanced 3.0 Tesla systems as a cost-effective solution for high-volume sites, despite the constraints of SUS fee structures.

Key Report Takeaways

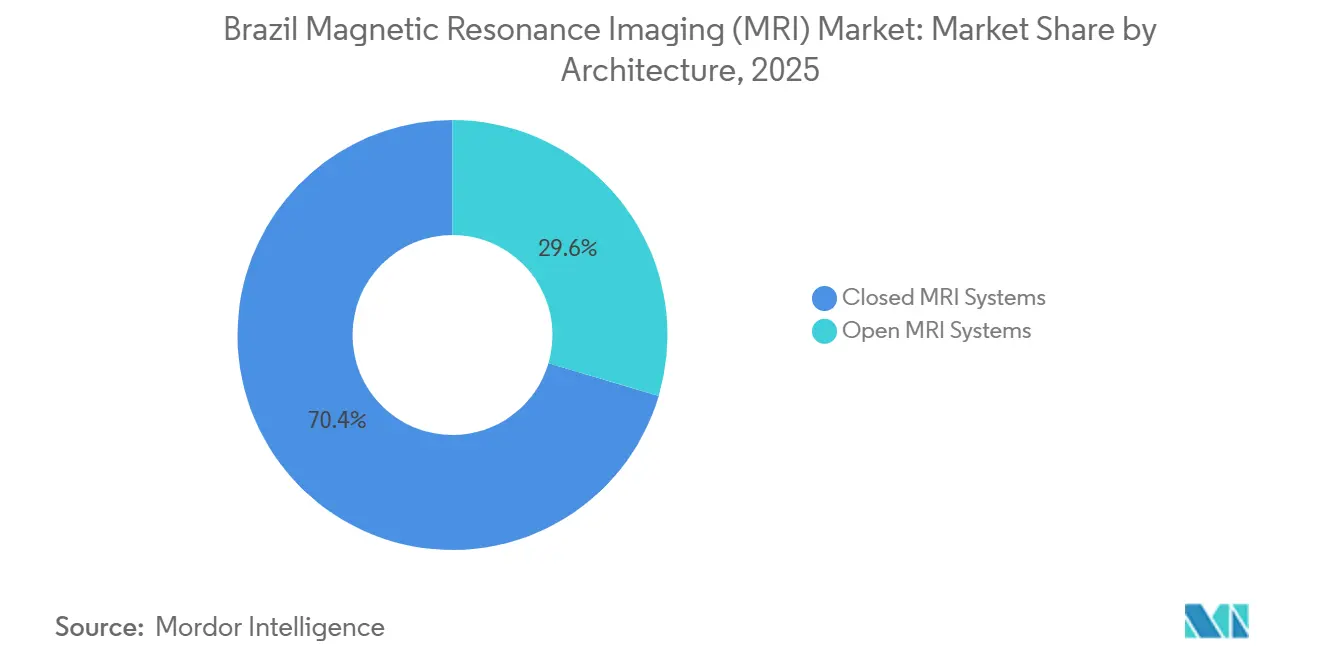

- By architecture, closed systems led with 70.43% of Brazil Magnetic Resonance Imaging (MRI) market share in 2025, while open systems record the fastest projected CAGR at 7.54% through 2031.

- By field strength, 1.0–3.0 Tesla units accounted for 57.43% share of the Brazil Magnetic Resonance Imaging (MRI) market size in 2025; platforms above 3.0 Tesla are projected to expand at a 7.12% CAGR to 2031.

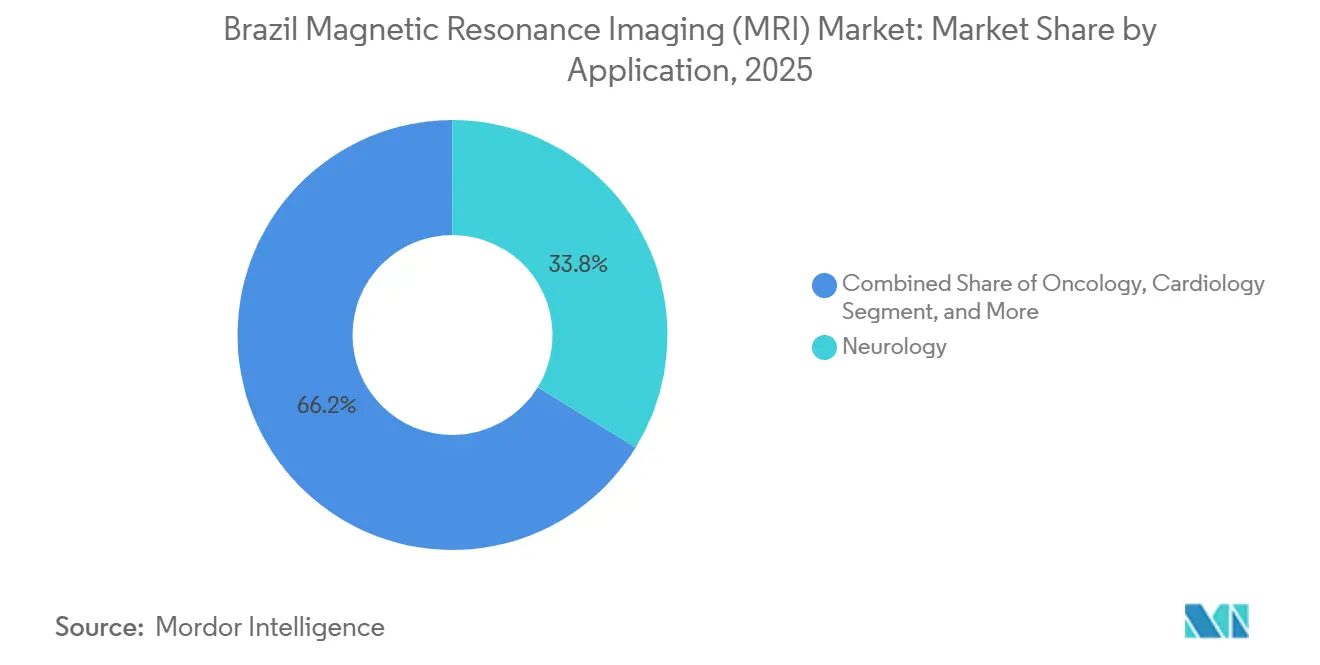

- By application, neurology commanded 33.76% of 2025 revenue, and oncology is advancing at a 7.89% CAGR through 2031.

- By end user, hospitals held 66.74% share in 2025, while diagnostic imaging centers are projected to grow the fastest at 6.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic Diseases | +1.2% | National, concentrated in Southeast and South regions | Medium term (2-4 years) |

| Expanding Private Health Insurance Coverage | +0.8% | Southeast (São Paulo, Rio de Janeiro), South (Porto Alegre, Curitiba) | Short term (≤ 2 years) |

| Technological Advancements in High-Field and Helium-Free MRI | +1.0% | National, early adoption in São Paulo, Brasília, Rio de Janeiro | Long term (≥ 4 years) |

| Government Investments in Public Hospital Infrastructure | +0.7% | North and Northeast regions, secondary cities nationwide | Long term (≥ 4 years) |

| Growing Adoption of AI-Based Imaging Workflows | +0.6% | Southeast private hospital networks, tertiary academic centers | Medium term (2-4 years) |

| Import Tax Incentives for Local Assembly | +0.4% | National, manufacturing hubs in São Paulo, Santa Catarina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases

Stroke, dementia, and cancer cases are mounting as Brazil’s population ages, so serial MRI for staging, follow-up, and treatment response is routine. Neurology already accounts for one-third of Brazil Magnetic Resonance Imaging (MRI) market demand, and oncology needs are accelerating as breast and prostate protocols expand in private centers. Cardiology imaging adds incremental volume because tertiary clinics now request functional data beyond angiography. The shift from episodic care toward chronic disease management keeps repeat-scan volumes high, reinforcing closed high-field systems for lesion detection and multiparametric exams. As chronic diseases cluster in the Southeast’s dense urban areas, diagnostic chains prioritize sites near oncology and neurology reference hospitals[1]GE HealthCare Investor Relations, “GE HealthCare and AWS to Accelerate Imaging AI,” gehealthcare.com.

Expanding Private Health Insurance Coverage

Roughly 25% of Brazilians hold private health plans, and those beneficiaries undergo 179 MRI exams per 1,000 covered lives each year, more than double OECD norms. Rede D'Or, Fleury, and DASA extend their branches into secondary cities to capture this demand, creating a two-tier model in which advanced modalities remain in private hands. ANS rules mandate baseline MRI reimbursement for specified indications, providing providers with predictable revenue streams, yet premium caps constrain insurers’ margins and may curb equipment replacement cycles if membership growth plateaus. Still, large chains leverage volume contracts to negotiate discounts, enabling faster payback on new 3.0 Tesla or AI-enabled units[2]Brazilian Ministry of Science & Technology, “Telehealth Outcomes in Primary Care: UBS+Digital,” jmir.org.

Technological Advancements in High-Field and Helium-Free MRI

High-field (1.0–3.0 Tesla) units remain the workhorse, but Philips BlueSeal and Fujifilm ECHELON Smart eliminate liquid helium, addressing price spikes that doubled global costs between 2022 and 2024. Each conventional scanner needs roughly 2,000 liters of helium, so sealed magnets shield budgets from refill risk. AI reconstruction such as GE AIR Recon DL cuts exam times by about 36% at Rede D'Or, raising daily throughput and lowering cost per study. These gains justify premium pricing in high-volume private sites while making 3.0 Tesla platforms financially feasible even with static SUS fees. Early adopters in São Paulo and Brasília showcase the productivity case to mid-tier hospitals evaluating new purchases.

Government Investments in Public Hospital Infrastructure

A November 2025 decree earmarks R$1.7 billion (USD 340 million) for smart hospital upgrades starting 2026, aiming to add AI, 5G connectivity, and robotic surgery capacity. MRI replacements could benefit underserved North and Northeast sites if allocation favors equity, yet procurement rules and CBS/IBS tax reforms create timing risk. SUS reimbursement covers only 11-16% of actual MRI costs, so public facilities still hesitate to expand unless capital grants offset operating losses. Duty-reduction programs shorten import lead times, but tariff uncertainties complicate bids. How quickly funds translate into installed scanners will influence regional access over the next five years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Maintenance Costs of MRI Systems | -0.9% | National, acute in North and Northeast public facilities | Short term (≤ 2 years) |

| Low Public Reimbursement Rates Under SUS | -1.1% | National, most severe in secondary and tertiary SUS hospitals | Long term (≥ 4 years) |

| Shortage of Skilled Radiologists and Technologists | -0.5% | North and Northeast regions, rural municipalities | Medium term (2-4 years) |

| Supply Chain Constraints for Helium and Spare Parts | -0.6% | National, exacerbated by import dependencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs of MRI Systems

A new 1.5 Tesla scanner costs USD 1.0–1.5 million, and 3.0 Tesla models reach USD 3.0 million. Annual service contracts consume up to 12% of the purchase price, while helium refills can add USD 40,000 per year. Import taxes can lift landed prices 30-50%, even after partial relief from the ex-tarifário regime. Private groups dilute costs across large patient volumes, but public hospitals with lower throughput find return-on-investment unattractive, reinforcing the urban-private concentration of equipment[3].

Low Public Reimbursement Rates Under SUS

SUS fee tables reimburse only a fraction of real imaging costs, so facilities ration access and long queues persist. Judicialization compels municipalities to buy private studies at market prices, stressing budgets. Unless reimbursement aligns with operating expense, new scanners in public sites will remain scarce, widening gaps in access. CONITEC reviews new technologies cautiously, and budget limits slow protocol updates that would otherwise stimulate volume. As a result, the Brazil Magnetic Resonance Imaging (MRI) market continues to lean on private capacity for growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Dominate, Open Platforms Gain Patient-Centric Traction

Closed units held 70.43% of 2025 revenue, underpinning the largest slice of the Brazil Magnetic Resonance Imaging (MRI) market. Image quality remains non-negotiable for neurology and oncology exams, keeping closed 1.5 Tesla and 3.0 Tesla models central to routine practice. Open designs, generally at 1.0 Tesla, expand at 7.54% annually because orthopedic, bariatric, and pediatric scans benefit from wider bores that reduce anxiety and accommodate larger body types. Diagnostic groups in São Paulo mix fleet types, pairing a 3.0 Tesla closed system with an open unit to balance throughput and comfort. Manufacturers respond by offering wide-bore hybrids such as Siemens Free.Max that merge patient access with field strength, blurring historical quality gaps.

Open units rarely match the spatial resolution of closed magnets, yet clinical protocols like musculoskeletal extremity imaging tolerate lower signal noise in exchange for positioning flexibility. Ambulatory centers exploit this trade-off to differentiate service lines while maintaining acceptable reimbursement levels. As AI accelerates reconstruction speed, the performance gulf narrows, further lifting open-system appeal for non-critical exams. Procurement choices therefore hinge on local case-mix and space constraints rather than on a simple quality hierarchy.

By Field Strength: High-Field Workhorse, Ultra-High-Field Research Frontier

High-field 1.0–3.0 Tesla equipment captured 57.43% of 2025 spending and anchors day-to-day clinical throughput, accounting for the core of the Brazil Magnetic Resonance Imaging (MRI) market size. Lower-field portable devices remain niche, serving ICU and rural outreach. Ultra-high-field scanners above 3.0 Tesla expand 7.12% each year, driven by São Paulo universities that pursue advanced neuroimaging and spectroscopy. Sealed magnets limit helium needs and make 3.0 Tesla adoption feasible even in midsize private hospitals. Hyperfine’s 0.064 Tesla Swoop targets intensive-care beds, but uptake depends on SUS reimbursement inclusion.

Academic hospitals embrace 7.0 Tesla units for research, yet budgets and infrastructure requirements cap volumes. The 1.5 Tesla band persists as the default choice for public tenders, balancing cost and coverage of approved protocols. As AI upgrades shorten scan times, 3.0 Tesla productivity rises, unlocking economic justification in centers with heavy oncology or cardiac caseloads. Equipment suppliers therefore segment offerings: workhorse 1.5 Tesla for public bids, productivity-driven 3.0 Tesla for high-volume private hubs, and 7.0 Tesla flagship systems for prestige research programs.

By Application: Neurology Leads, Oncology Accelerates

Neurology contributed 33.76% of 2025 revenue, reflecting stroke and dementia protocol growth, and anchors the largest slice of the Brazil Magnetic Resonance Imaging (MRI) market. Oncology leads growth at 7.89% through 2031 as breast, prostate, and whole-body diffusion imaging spread in private oncology networks. Cardiac MRI gains incremental ground where non-invasive viability studies replace some catheter work-ups, although training gaps slow broader uptake. Musculoskeletal and hepatobiliary imaging maintain steady but smaller contributions.

Private cancer centers deploy dedicated breast coils and, in rare cases, PET-MRI hybrids to guide biopsy and therapy monitoring. Public hospitals focus on stroke pathway mandates, sustaining neuroimaging dominance. The divergent paces leave neurology holding volume leadership but oncology adding the most incremental scanners, shaping vendor marketing and coil package bundling decisions.

By End User: Hospitals Anchor Demand, Diagnostic Centers Grow Faster

In 2025, hospitals accounted for 66.74% of expenditures, driven by their focus on emergency stroke and surgical planning services that require on-site access, thereby maintaining a dominant position in Brazil's Magnetic Resonance Imaging (MRI) market. Diagnostic imaging centers are expanding at an annual growth rate of 6.54%, supported by Rede D'Or, Fleury, and DASA's strategic penetration into secondary cities, leveraging extended operational hours and AI-driven efficiency. Ambulatory surgery centers are emerging as a niche segment by adopting open magnets for intraoperative orthopedic guidance.

High utilization of private health plans, with 179 exams per 1,000 enrollees, underpins investment strategies in diagnostic centers. However, hospitals, particularly within the SUS network, face budgetary constraints, with many scanners exceeding a decade in service. This dynamic is gradually shifting the market toward outpatient chains, which capitalize on rapid reporting capabilities and flexible scheduling, further strengthening the private sector's role in driving overall market growth.

Competitive Landscape

The competitive field is moderately consolidated. GE HealthCare, Siemens Healthineers, and Philips together control most of the installed base via long-term service contracts and AI reconstruction exclusives. Canon Medical and Fujifilm rank as challengers, bringing helium-free and cost-efficient systems that appeal to budget-sensitive buyers. Domestic supplier Imex Medical Group leverages ANVISA regulatory compliance and local assembly to undercut imports by 20-30%, targeting SUS tenders for 1.5 Tesla equipment.

Strategic focus has shifted from hardware power to lifecycle economics. Siemens Value Partnerships bundle equipment, software, and managed services into multiyear deals tied to uptime guarantees. GE’s Imaging 360 platform wraps AI, analytics, and financing around scanner fleets, securing loyalty from diagnostic chains. Portable players such as Hyperfine offer point-of-care solutions for rural outreach, but adoption depends on reimbursement inclusion. Chinese entrants United Imaging and Neusoft secure ANVISA clearances yet must prove after-sales reach. Vendors lacking AI or helium-free value propositions risk marginalization in high-volume tenders where throughput and operating expense drive decisions.

Brazil Magnetic Resonance Imaging (MRI) Industry Leaders

-

Koninklijke Philips NV

-

Fujifilm Holdings Corporation

-

Siemens Healthcare GmbH

-

Canon Inc. (Canon Medical Systems Corporation)

-

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Bracco Imaging S.p.A., a global player in diagnostic imaging, and Subtle Medical, Inc., a pioneering innovator in artificial intelligence (AI)-powered medical imaging software, announced that AiMIFY, their jointly developed AI-powered software for magnetic resonance imaging (MRI) of the brain, has received ANVISA (Agência Nacional de Vigilância Sanitária) approval in Brazil.

- May 2025: Philips partnered with NVIDIA to enhance MRI technology using the latest AI advancements, aiming to improve diagnostic accuracy and patient outcomes. This collaboration leverages AI to optimize imaging processes and streamline healthcare workflows.

- May 2024: AIRS Medical Inc., a leading provider of AI-powered healthcare solutions, announced a strategic partnership with Blue Health Group in Brazil. With this partnership, AIRS Medical’s flagship product, SwiftMR, an AI-powered MRI Enhancement solution, is set to aggressively expand into the Brazilian market.

Brazil Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of this report, magnetic resonance imaging is a medical imaging technique used in radiology to produce images of the body's anatomy and physiological processes. These pictures are also used to diagnose and detect abnormalities in the body.

The Brazil Magnetic Resonance Imaging (MRI) Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low-Field < 1.0 T, High-Field 1.0-3.0 T, and Very High/Ultra-High > 3.0 T), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, Other Applications), and End User (Hospitals, Diagnostic Imaging Centers, and Ambulatory Surgical Centers), The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (< 1.0 T) |

| High-Field (1.0 – 3.0 T) |

| Very High / Ultra-High (> 3.0 T) |

By Application

| Oncology |

| Neurology |

| Cardiology |

| Gastroenterology |

| Musculoskeletal |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (< 1.0 T) |

| High-Field (1.0 – 3.0 T) | |

| Very High / Ultra-High (> 3.0 T) | |

| By Application | Oncology |

| Neurology | |

| Cardiology | |

| Gastroenterology | |

| Musculoskeletal | |

| Other Applications | |

| By End User | Hospitals |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers |

Key Questions Answered in the Report

What is the projected value of Brazil’s MRI market by 2031?

The Brazil Magnetic Resonance Imaging (MRI) market is expected to reach USD 457.35 million by 2031, reflecting a 5.05% CAGR from 2026.

Which MRI architecture is growing the fastest in Brazil?

Open MRI systems are forecast to expand at 7.54% annually through 2031 due to demand for patient-friendly orthopedic and bariatric imaging.

How will helium-free technology impact MRI ownership costs?

Helium-free magnets such as Philips BlueSeal can remove up to USD 40,000 per year in refill expenses, significantly lowering total cost of ownership for private and public facilities.

Why are diagnostic imaging centers outpacing hospitals in new MRI installs?

Private chains leverage high utilization rates and AI-driven throughput to achieve faster payback, allowing them to invest despite stagnant SUS reimbursements.

Which applications drive MRI demand growth in Brazil?

Oncology shows the fastest growth at 7.89% CAGR through 2031, while neurology maintains the largest revenue share due to stroke and dementia protocols.

Page last updated on: