Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

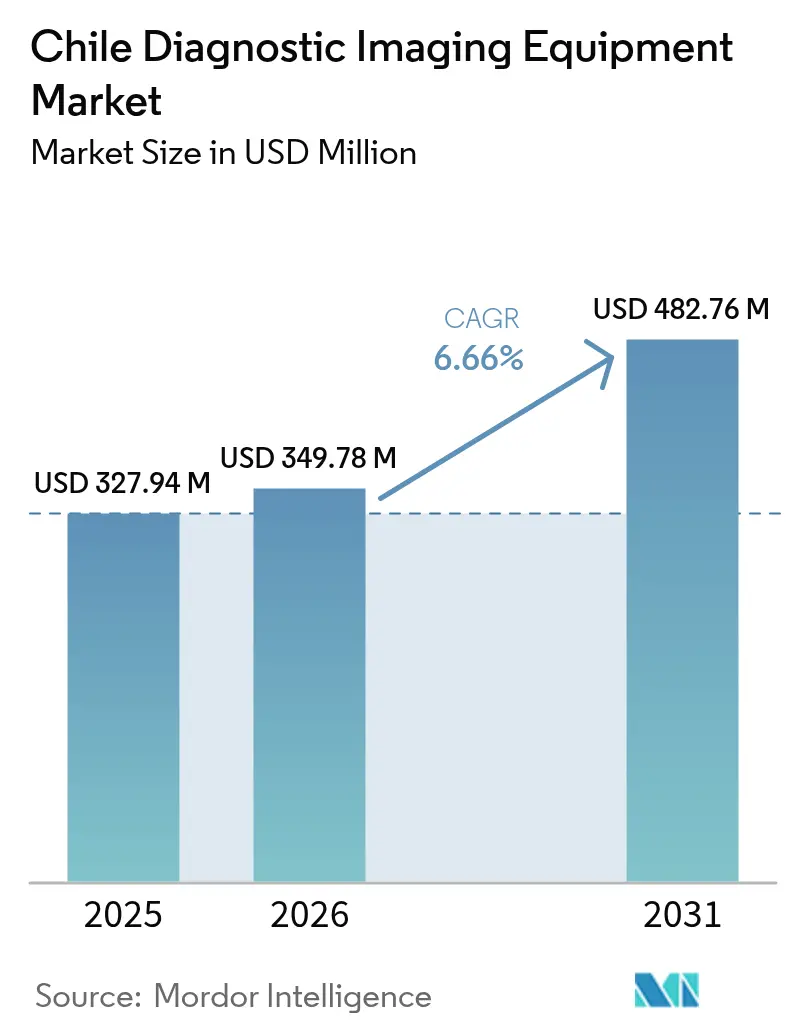

| Base Year Market Size (2025) | USD 327.94 Million |

| Market Size (2026) | USD 349.78 Million |

| Market Size (2031) | USD 482.76 Million |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Chile diagnostic imaging equipment market size was valued at USD 327.94 million in 2025 and estimated to grow from USD 349.78 million in 2026 to reach USD 482.76 million by 2031, at a CAGR of 6.66% during the forecast period (2026-2031). Steady public-sector investment, rapid private-sector digitization, and an aging population that now accounts for 16% of residents reinforce equipment demand across modalities. Oncology’s rise as Chile’s top mortality driver, together with cardiovascular prevalence affecting 27% of adults, pushes providers to upgrade to high-throughput CT, MRI, and mammography units that integrate decision-support software.

Key Report Takeaways

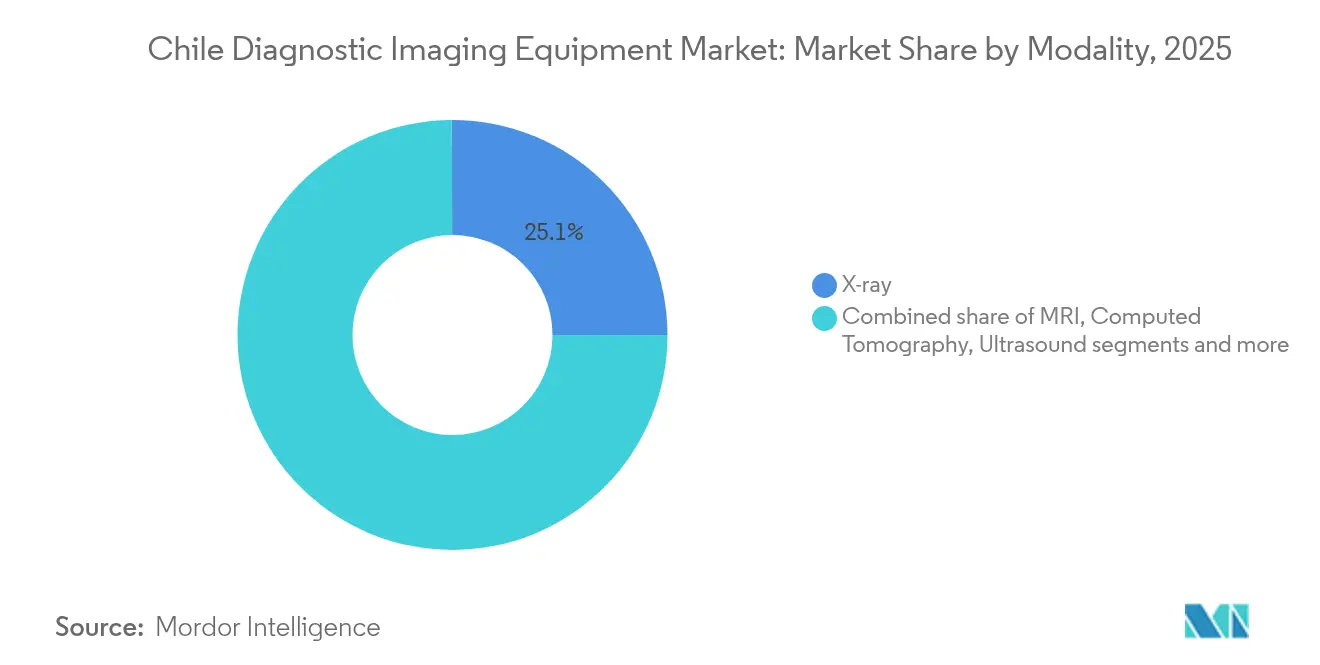

- By modality, X-ray systems led with 25.05% of the Chile diagnostic imaging equipment market share in 2025, whereas MRI is projected to expand at an 7.95% CAGR through 2031.

- By portability, fixed systems commanded 79.65% of the Chile diagnostic imaging equipment market size in 2025, while mobile and handheld systems exhibit the fastest 7.55% CAGR to 2031.

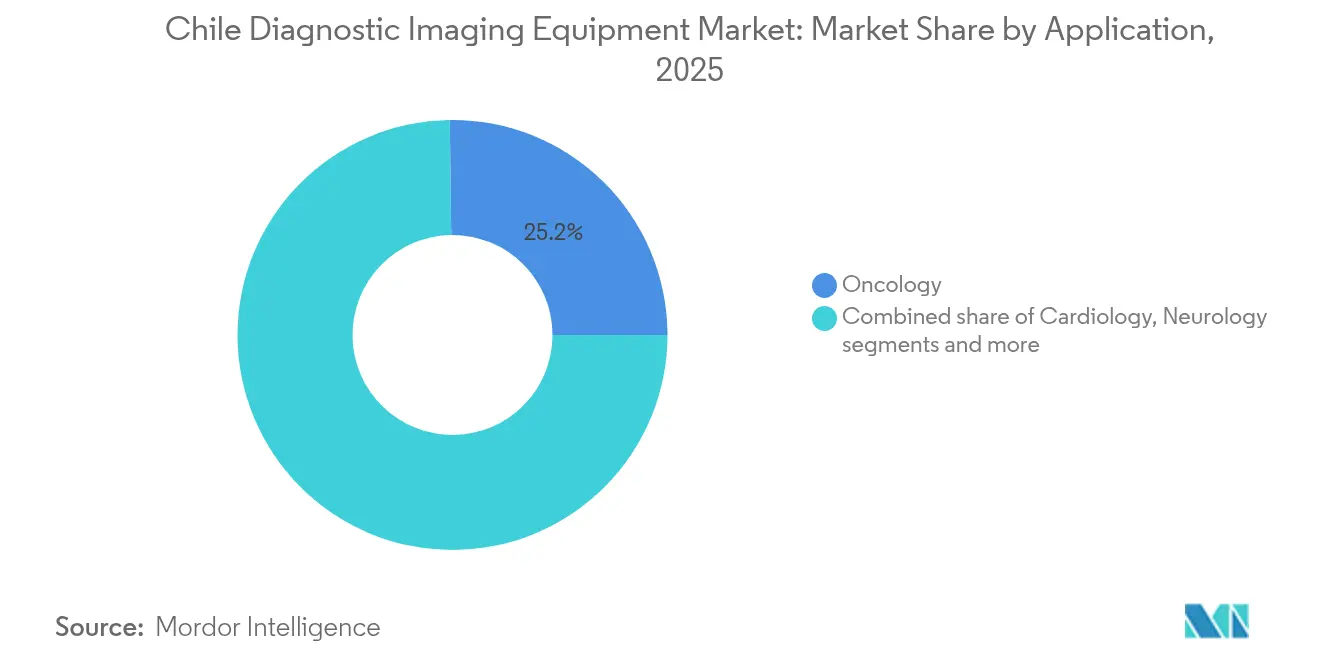

- By application, oncology accounted for 25.20% share of the Chile diagnostic imaging equipment market size in 2025; cardiology is advancing at an 8.05% CAGR through 2031.

- By end user, hospitals captured 55.62% of the Chile diagnostic imaging equipment market size in 2025, yet diagnostic imaging centers record the leading 7.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing geriatric population | +1.2% | National, concentrated in Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Rising prevalence of chronic diseases | +1.5% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Technological advancements & digitization | +1.8% | National, spill-over to regional centers | Short term (≤ 2 years) |

| Government investment in hospital network expansion | +1.1% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Expansion of national teleradiology network | +0.9% | National, particularly benefiting remote regions | Medium term (2-4 years) |

| National cancer and cardiovascular initiatives prioritizing advanced diagnostic capacity | +1.3% | National, concentrated in major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population

By 2030, people aged 65 and older will form one-fifth of Chile’s residents, and they undergo imaging 3.2 times more often than younger cohorts, especially for musculoskeletal and cardiovascular assessments. National survey results show that 74% of seniors have at least one condition needing routine scans, which pushes hospitals to replace legacy radiography with dose-reduction digital units that cut exposure up to 70%. Procurement teams therefore prioritize patient-friendly gantries and faster table times to minimize discomfort among mobility-restricted elders.

Rising Prevalence of Chronic Diseases

Cancer has overtaken cardiovascular illness as Chile’s top mortality driver,[1]Source: Cecilia Vial, “A snapshot of cancer in Chile II,” Biological Research, biolres.biomedcentral.com and the National Cancer Institute expanded its research pipeline, signaling higher requirements for CT, mammography, and PET-CT capacity. Cardiovascular disease still burdens 27% of adults, spurring adoption of cardiac CT and MRI that integrate with tele-cardiology platforms. Facilities seek scanners capable of dual oncology-cardiology use to maximize asset utilization, a key strategy in budget-constrained provincial hospitals.

Technological Advancements & Digitization

Local health-tech firm Sked24 cut average appointment delays by 70% through AI-driven scheduling that now supports more than 1 million visits annually. AGFA-RedSalud’s domestic cloud deployment enables AI triage and remote reading while satisfying data-sovereignty rules. Vendors embed algorithms inside scanners. These advances ease radiologists' workload and let smaller sites access subspecialty interpretations.

Government Investment in Hospital Network Expansion

The Ministry of Public Works committed USD 180 million to new Rengo and Pichilemu hospitals that will add 262 beds and incorporate full imaging suites by 2028. Twenty-five further hospitals are simultaneously under construction, marking Chile’s largest ever healthcare build-out. Standardized tenders on the ChileCompra platform streamline purchasing, permitting suppliers to offer volume discounts across modalities. FONASA’s PAD reimbursement scheme removes financial uncertainty for public patients, guaranteeing a baseline scan volume once the new facilities open.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of imaging equipment & procedures | -0.8% | National, particularly affecting smaller regional centers | Long term (≥ 4 years) |

| Shortage of radiologists & sonographers | -0.6% | National, with acute shortages outside Santiago | Medium term (2-4 years) |

| Inadequate reimbursement tariffs for high-end modalities limiting provider ROI | -0.5% | National, particularly affecting ISAPRE beneficiaries | Medium term (2-4 years) |

| Limited service and maintenance capabilities outside major metros reducing equipment uptime | -0.4% | Regional, affecting facilities outside Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Imaging Equipment & Procedures

A single 1.5 T MRI can cost USD 1-3 million, and annual maintenance absorbs 8-12% of purchase value. Private ISAPRE plans reimburse only 60-80% of high-end scan fees, forcing middle-income households to shoulder large co-payments.[2]Source: Andrew Anderson, “Access to medicines for the treatment of chronic diseases in Chile,” BMC Health Services Research, bmchealthservres.biomedcentral.com Peso volatility lifts import prices because virtually all scanners arrive from the United States, Europe, or Japan. To counter the strain, vendors propose leasing and pay-per-exam contracts that tie fees to utilization and outcomes.

Shortage of Radiologists & Sonographers

Chile’s radiologist-to-population ratio lags OECD norms, and 18% of posts in public hospitals remain vacant. Scan volumes expand 8-10% annually, so AI triage and tele-radiology have become essential stopgaps that allow metropolitan experts to serve southern and northern hospitals in real time. Career migration toward higher-paying private clinics further widens gaps in public facilities, prompting the Ministry of Health to co-fund residency slots and sponsor overseas fellowships starting in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-ray Dominance Faces MRI Innovation Challenge

X-ray equipment retained 25.05% of the Chile diagnostic imaging equipment market share in 2025 as every emergency department depends on radiography for trauma screening. Demand for digital detectors that slash dose and produce instant images keeps replacement cycles brisk. MRI, while representing a smaller installed base, is growing at 7.95% CAGR because neurological research and oncology follow-up require higher resolution and soft-tissue detail.

Chile’s procurement strategy now favors multi-purpose platforms. A single DR room can manage trauma, chest, and orthopedic exams with AI-based positioning that speeds throughput. MRI vendors highlight non-contrast angiography and synthetic CT capabilities that let oncologists stage disease without additional radiation. Computed tomography suppliers integrate metal-artifact reduction essential for Chile’s sizable orthopedics patient pool linked to mining accidents and sports injuries. Mammography system vendors increasingly deliver tomosynthesis as a standard feature, advancing early lesion detection rates in national screening centers.

By Portability: Fixed Systems Anchor Market Despite Mobile Growth

Fixed installations represented 79.65% of the Chile diagnostic imaging equipment market size in 2025, as tertiary hospitals require gantry-mounted MRI and multi-slice CT to handle high patient volumes. Major centers in Santiago and Valparaíso typically operate two to four CT suites each, ensuring redundancy for 24/7 trauma coverage. Mobile systems, however, post a 7.55% CAGR because mountainous geography and island communities necessitate transportable solutions. Mobile CT trailers serve Antofagasta’s mining camps, and handheld ultrasound bridges care gaps in Patagonia’s primary clinics. Vendors now market battery-powered portable X-ray units that fit in emergency vehicles, responding to Chile’s national disaster preparedness protocols linked to seismic risk. The Chile diagnostic imaging equipment market benefits as government grants fund ruggedized equipment certified for earthquake resilience.

Adoption patterns vary by region. Metropolitan public hospitals replace legacy fixed radiography with ceiling-suspended DR to clear floor space and speed patient turnover. Private orthopedics practices adopt compact extremity MRI for dedicated sports medicine workflows. Meanwhile, rural hospitals choose multi-modality vans that combine digital X-ray with ultrasound, enabling a single technologist to perform essential scans on rotational visits. Industry players expect future growth in self-shielded mobile PET-CT that can operate without purpose-built bunkers, extending oncology staging services to secondary cities.

By Application: Oncology Leadership Challenged by Cardiology Growth

Oncology controlled 25.20% of the Chile diagnostic imaging equipment market size in 2025, mirroring cancer’s primacy in national mortality. PET-CT expansion accompanies new radiopharmaceutical import channels through Santiago airport, shortening isotope delivery windows. Cardiology shows the highest 8.05% CAGR; 512-slice CT systems offer sub-second coronary scans that integrate with cloud PACS for rapid cardiologist review. Neurology leverages advanced MRI for stroke triage and dementia studies tied to the rising elder population. Orthopedics imaging revenues sustain mid-single-digit growth as Chile’s agrarian and mining sectors generate high fracture rates. Gastrointestinal and gynecological imaging maintain stable uptake through routine endoscopy and women’s health programs.

Clinical workflows increasingly overlap. Oncologists use cardiac-gated CT to monitor chemotherapy-induced cardiotoxicity, a practice driving cross-department justification for shared equipment. AI algorithms target both oncology lesion mapping and cardiology calcium scoring, allowing providers to justify premium software licenses across specialties. Portable ultrasound sees uptake in oncology wards for vascular access and in cardiology clinics for rapid ejection-fraction assessment, demonstrating convergence of use cases.

By End User: Hospitals Dominate While Imaging Centers Accelerate

Hospitals accounted for 55.62% of the Chile diagnostic imaging equipment market size in 2025, housing the bulk of fixed CT, MRI, and angiography suites. The public FONASA system remains the single largest purchaser, leveraging bulk tenders to equip new regional hospitals. Private groups such as Clínica Alemana and RedSalud differentiate through faster appointment slots and AI-assisted reporting, deepening their scanner refresh cycles every five to seven years. Imaging centers grow at 7.26% CAGR because urban patients value short wait times and specialized staff. Many centers deploy high-end 3 T MRI and dual-energy CT to attract research contracts and clinical trials, a trend underscored by the rise from 20 to 33 device trials between 2021-2023. Smaller clinics and mobile operators cover niche demands, often leasing portable ultrasound or DR systems to manage cash flow.

Competition blurs boundaries: public hospitals outsource overflow scans to private imaging centers under per-case agreements, while private chains build mini-hospitals that include day surgery and intensive care. Vendor service contracts therefore span both segments, bundling hardware, cloud PACS, cybersecurity, and radiologist training into single multi-year deals that cover entire regional ecosystems.

Geography Analysis

Metropolitan Santiago concentrates the Chile diagnostic imaging equipment market, hosting the densest cluster of radiologists, specialty hospitals, and academic research centers. The region’s tertiary hospitals routinely operate multiple MRI magnets and 256-slice CT systems to support trauma, oncology, and cardiac workloads. Valparaíso, the nation’s second urban hub, combines port logistics with provincial referrals, sustaining diversified modality demand and acting as a receiving point for imported scanners. Concepción anchors the south-central corridor, where new public-private hospitals align with forestry and manufacturing industries that require occupational health imaging.

Northern macro-zones, including Antofagasta and Tarapacá, reflect mining-driven demand for on-site digital radiography and low-dose CT to monitor silicosis and musculoskeletal injury among workers. Mobile vans operate along the Pan-American Highway, attending remote camps three to four times monthly. Rise in fixed CT installations in Antofagasta’s trauma centers meets the region’s elevated accident rate, while portable ultrasound assists emergency care at high-altitude sites. Southern regions such as Los Ríos and Los Lagos rely on handheld ultrasound and compact DR units that can be ferried to island clinics across the inland sea.

Chile’s length and mountainous terrain create logistical obstacles that shape supplier strategies. Vendors maintain parts depots in Santiago, Concepción, and Antofagasta to satisfy guaranteed 48-hour service clauses. Equipment frames must meet local seismic standards; hospitals specify reinforced floor mounts and automatic magnet-quench vents. Tele-radiology networks using cloud PACS connect rural hospitals to Santiago sub-specialists, raising justification for advanced modalities at smaller regional sites because interpretation can be outsourced without relocating staff.

Regulatory Landscape

Chile regulates diagnostic imaging equipment through a dual-control model that combines device-level sanitary oversight with site-level authorization for ionizing-radiation installations. The Instituto de Salud Publica de Chile (ISP) manages sanitary registration and lifecycle controls through its digital platforms (commonly referenced as GICONA/SAFIS), while regional SEREMI de Salud authorities authorize facilities that operate X-ray and other ionizing modalities, including review of shielding designs and radiation-safety conditions validated by accredited professionals.

A key regulatory anchor is March 2026, when the Ministry of Health (MINSAL) issued Exempt Decree No. 25, expanding mandatory sanitary control to imaging equipment such as X-ray, CT, mammography, and PET/SPECT. This shift increases the importance of having valid ISP registrations for participation in institutional purchases and ChileCompra tenders, while providers also need to maintain SEREMI permits and radiation-protection compliance for each installed system.

Competitive Landscape

The Chile diagnostic imaging equipment market is moderately consolidated, with GE Healthcare, Siemens Healthineers, and Philips supplying most MRI, CT, and premium ultrasound units. Canon Medical Systems and Fujifilm strengthen mid-tier competition through competitive pricing and AI features. AGFA HealthCare leads enterprise imaging software after sealing the RedSalud cloud deal that covers multiple hospitals and imaging centers. Local distributor Global Ultrasonido fills gaps for refurbished ultrasound and DR in community clinics, supporting lower budgets and fast turnaround service.

Strategic alliances define differentiation. Siemens Healthineers pilots value-based partnerships tying lease payment to clinical throughput in provincial hospitals. GE Healthcare’s worldwide radiopharmaceutical acquisition bolsters Chilean PET-CT growth by ensuring isotope supply chain reliability. Canon establishes an innovation hub in Cleveland that will export workflow updates to Chilean install bases, promising remote software upgrades without equipment downtime.

Price competition intensifies in mobile X-ray and portable ultrasound, where handheld entrants undercut established brands. Vendors seek differentiation through AI bundles, dose-management analytics, and cloud PACS integration. Service quality remains a decisive purchase factor because rural hospitals rely on quick part replacement to keep scanners operational in single-system environments. Manufacturers partner with local biomedical engineering schools to certify technicians, strengthening after-sales capacity and satisfying tender requirements for domestic knowledge transfer.

Chile Diagnostic Imaging Equipment Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

Koninklijke Philips N.V.

GE HealthCare

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large public hospital build-outs and equipment reception milestones create near-term whitespace for new fixed-room suites and fleet standardization across regions. Evidence of commissioning activity includes the Hospital Provincial Marga Marga beginning reception of more than 30,000 medical devices in June 2026 (habilitation and testing phase), the Hospital de Curanilahue imaging unit modernization reaching 90% completion in June 2026 with new CT, ultrasound, and X-ray equipment, and the Hospital de Ancud reporting 86% of medical equipment acquired and received by July 2026 with imaging units installed. In parallel, Hospital del Salvador and the Instituto Nacional de Geriatria reported 98.56% construction progress in May 2026 as projects move into final installation of sophisticated medical technology, supporting multi-year tender cycles for CT, MRI, radiography, and mammography rooms.

A second opportunity area involves workflow, financing, and compliance adaptations that reduce barriers for regional facilities, including fee-for-service and OPEX models for imaging access, cloud-enabled reading tied to the national teleradiology push, and upgrades that raise throughput amid staffing shortages. The March 2026 Decree No. 25 transition to risk-based sanitary control also creates service demand for registration support, documentation readiness, and standardized acceptance testing, as suppliers and providers align procurement timing with ISP registration and facility-level SEREMI authorizations for ionizing-radiation equipment.

Recent Industry Developments

- April 2026: Andes Salud incorporated a gallium generator at its Puerto Montt and Concepcion facilities to support specialized PET-CT diagnostics for oncology. Expanding local radiotracer capability helps decentralize molecular imaging beyond Santiago and supports higher utilization of PET-CT installations in the south.

- May 2025: Subtle Medical launched FDA-cleared SubtleHD AI in Chile via Hospiline, targeting MRI image quality improvements and shorter scan times. The software-first rollout supports capacity expansion without immediate magnet replacement, which is relevant for providers managing high equipment costs and radiologist constraints.

- August 2024: SonoVascular commenced first-in-human use of the SonoThrombectomy System at Hospital DIPRECA in Santiago. The clinical adoption highlights continued uptake of advanced image-guided approaches in tertiary centers, reinforcing demand for high-quality ultrasound and fluoroscopy-enabled procedural imaging environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This methodology defines the Chile diagnostic imaging equipment market as revenue from sales of new imaging systems for in-vivo visualization across Chile, covering hospitals, stand-alone imaging centers, and specialty clinics.

Scope exclusions: refurbished systems, consumables, image-management software, and service or maintenance contracts are excluded from the market value.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography

- Ultrasound

- X-ray

- Nuclear Imaging

- Fluoroscopy

- Mammography

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics

- Gastroenterology

- Gynecology

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Other End Users

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, understand the buying environment in Chile, and build starting points for volumes and pricing ranges. We referenced public sources such as Ministry of Health publications, Central Bank of Chile macro series, Chilean customs trade statistics for relevant equipment categories, OECD health indicators, and peer-reviewed radiology and health economics journals.

Alongside these, we reviewed supplier and distributor websites, product brochures, tender notices, and publicly available presentations that describe installed-base needs, replacement cycles, and modality upgrades. A paid subscription for company financials and news was used selectively to cross-check revenue exposure and major contract wins, and patent databases were used to spot technology shifts that can change average selling prices. The sources listed here are illustrative only, and additional public and paid sources were also used for validation and clarification.

Primary Interviews and Surveys

Primary work focused on confirming which modalities are actually being purchased in Chile, how procurement is split between public and private providers, and how prices vary by configuration and supplier support terms. We spoke with manufacturers and channel partners, plus imaging department leaders and biomedical teams from hospitals and imaging centers, so assumptions from desk research could be challenged and corrected.

Because purchase timing can be lumpy, questions also covered tender cadence, import lead times, and the typical timing of price resets. That information helped align the model to the correct year and the currency conversion window.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 53% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

Sizing started from a top-down rebuild of Chile equipment demand by modality. Import flow signals, the direction of healthcare capital spending, and replacement timing were used to shape an annual demand pool. We then corroborated that total with selective bottom-up checks, using sampled unit volumes by modality multiplied by observed price bands, followed by channel checks to adjust for mix shifts.

Key inputs in the model included modality mix (CT, MRI, ultrasound, X-ray, nuclear imaging, fluoroscopy, mammography), the public versus private procurement share, expected replacement cycles for major systems, installation lead times tied to tenders, and average selling price movement by configuration (for example, fixed versus mobile and base versus advanced features). Where the bottom-up view had gaps, volumes were bridged using conservative penetration assumptions anchored to facility counts and observed tender frequency.

For forecasting, we ran scenario analysis around capital budget pace, tender timing, and price progression, then smoothed the final path so one-off procurement spikes did not distort the trend. Inputs were reviewed with primary respondents to confirm what is realistic for the next few years in Chile.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as trade trends, typical procurement calendars, and observed pricing ranges from recent deals, and then inconsistencies were investigated before final sign-off. When a value looked off, we revisited assumptions behind modality mix, unit volumes, and currency conversion timing, and then re-contacted sources if the gap could not be explained.

A second analyst review was applied to ensure calculations, scope rules, and year labeling were consistent throughout. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view.

Mordor Intelligence's Chile Diagnostic Imaging Equipment Market Size Versus Other Published Estimates

Published numbers for Chile diagnostic imaging equipment can differ even when the topic sounds the same, because the scope boundary and timing choices are not consistent across sources. In practice, the biggest swings come from whether refurbished systems and service revenue are counted, how prices are converted into USD, and whether the latest tender cycle is reflected.

A refresh-led gap is also common in this market because large public purchases can move the total in a single year, and price resets often follow supplier updates and currency changes. By rechecking ASP bands and the USD conversion window close to publication, and validating those shifts with recent tender and channel feedback, Mordor Intelligence reduces timing drift that can make other estimates look unusually high or low.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 349.78 M (2026) | |

| Regional Consultancy A | USD 320.00 M (2024) | Uses an earlier base year and can understate the impact of later tender cycles, and the scope description is broader, which may blend equipment definitions across modalities and procurement channels. |

| Global Consultancy B | USD 710.00 M (2025) | Appears to use a wider category for medical imaging equipment that can pull in adjacent device groups and related revenue pools, which inflates the total versus a new-systems-only equipment scope. |

Taken together, the spread is explained mainly by scope boundaries and year timing, rather than a true disagreement on demand direction. Keeping the market tied to new-system sales, transparent price bands, and a clearly defined currency timing makes the estimate easier to reconcile and repeat when buyers revisit the model next year.

Key Questions Answered in the Report

What is the main factor accelerating demand for diagnostic imaging equipment in Chile?

The convergence of an aging population with rising cancer and cardiovascular cases is pushing hospitals to expand imaging capacity and upgrade to advanced, multi-modality systems.

How is artificial intelligence reshaping imaging workflows across Chilean facilities?

AI tools embedded in scanners and cloud platforms shorten exam times, automate triage, and let radiologists interpret studies remotely, which helps offset the country’s specialist shortage.

Why are mobile and handheld imaging devices gaining traction outside Santiago?

Chile’s mountainous geography and dispersed rural communities favor portable units that can travel to remote clinics, mining sites, and island hospitals where fixed suites are impractical.

How do government hospital projects influence equipment purchasing decisions?

Standardized public tenders tied to new hospital builds create bulk orders that reward vendors offering scalable service contracts, cybersecurity compliance, and earthquake-resistant designs.

Page last updated on: