Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

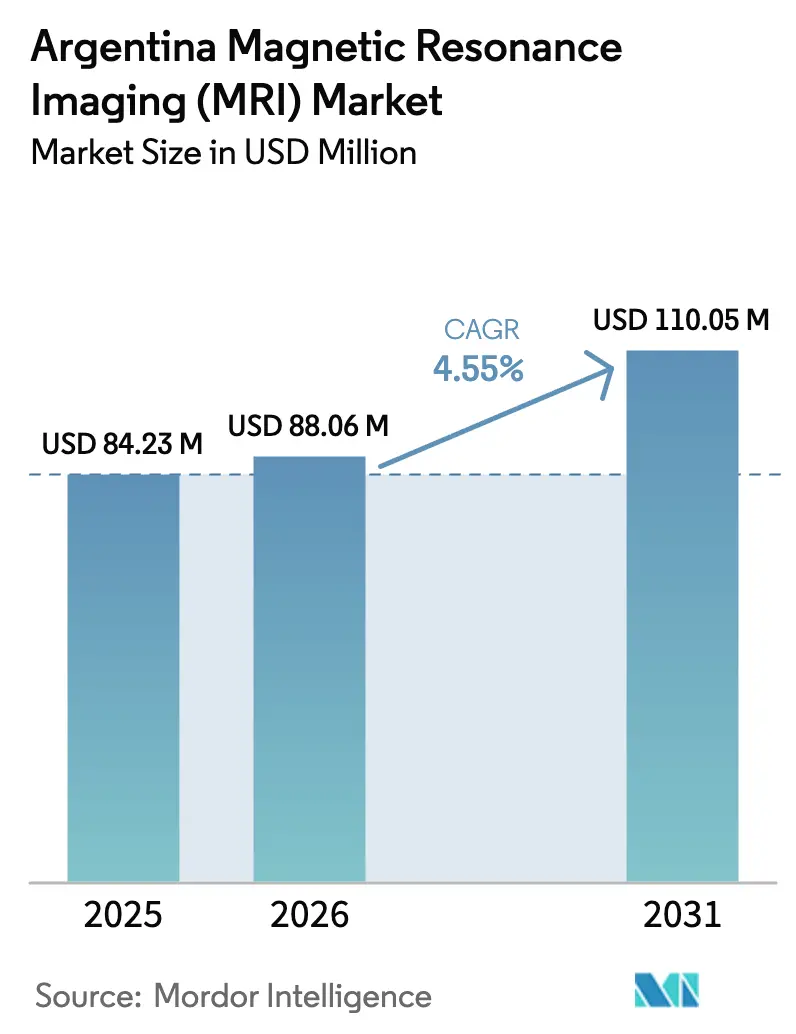

| Base Year Market Size (2025) | USD 84.23 Million |

| Market Size (2026) | USD 88.06 Million |

| Market Size (2031) | USD 110.05 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Argentina Magnetic Resonance Imaging (MRI) Market size in 2026 is estimated at USD 88.06 million, growing from 2025 value of USD 84.23 million with 2031 projections showing USD 110.05 million, growing at 4.55% CAGR over 2026-2031. Demand rises as public and private providers upgrade diagnostic infrastructure, supported by import-duty exemptions, faster foreign-currency access, and streamlined customs procedures that lower capital barriers for imaging centers. Growth persists even as health-care costs fluctuate, helped by a three-tier financing model that spreads risk across public insurance, social works, and private plans. Closed-bore installations dominate today, yet open and very-high-field systems are scaling quickly because provincial chains and research institutes seek better patient comfort and sharper neuro-oncology imaging. Ongoing investments in teleradiology and helium-free technology cut operating costs and help alleviate workforce shortages outside Buenos Aires.

Key Report Takeaways

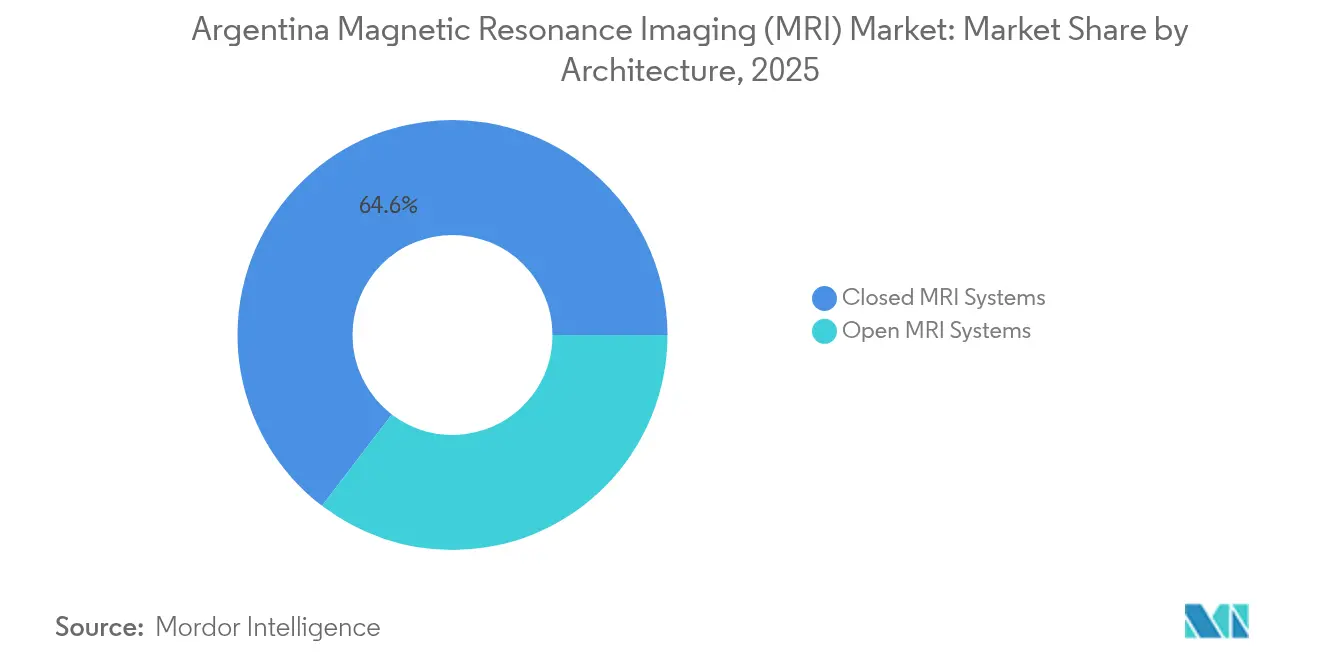

- Closed MRI systems held 64.62% of the Argentina Magnetic Resonance Imaging (MRI) market share in 2025, while open architecture is projected to expand at a 5.02% CAGR through 2031.

- High-field 1.5 T platforms accounted for 63.10% of the Argentina MRI market size in 2025; very-high/ultra-high-field units (3 T and above) show the fastest growth at 5.17% CAGR.

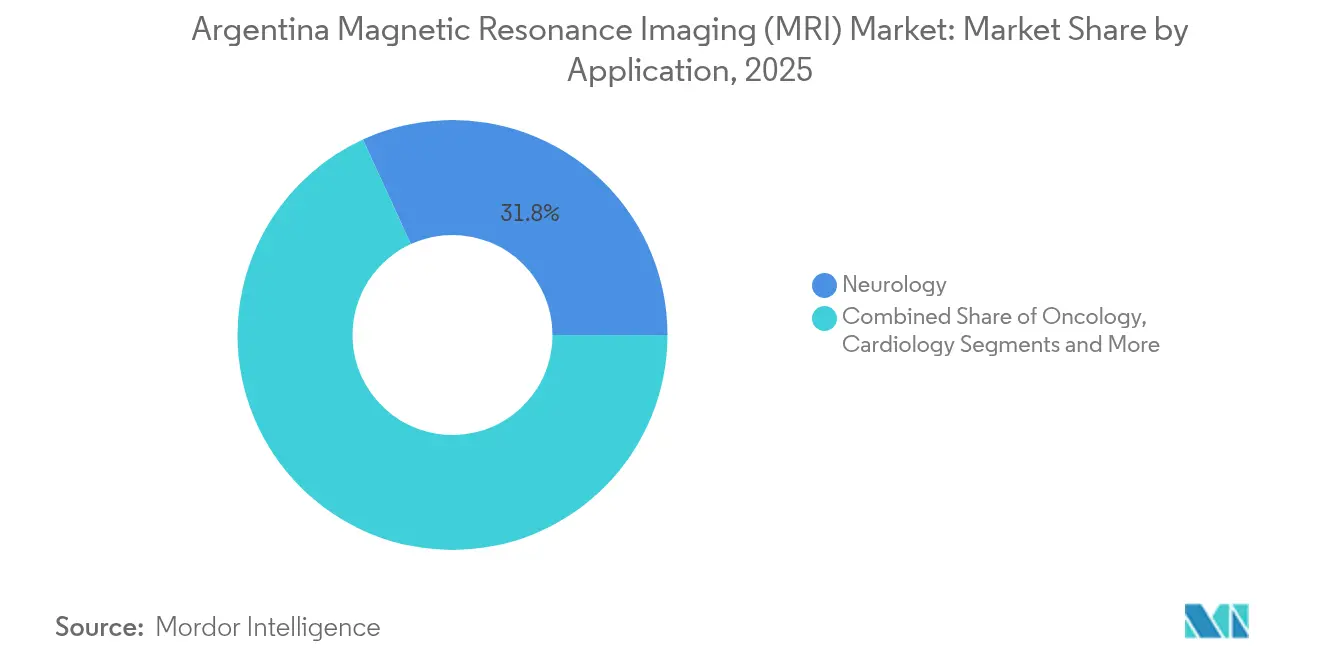

- Neurology led with 31.84% revenue share in 2025, whereas oncology imaging is set to record a 5.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of chronic diseases & rise in geriatric population | +1.2% | Buenos Aires, Córdoba, Santa Fe | Long term (≥ 4 years) |

| Growth in private diagnostic-imaging chains across provincial cities | +0.8% | Mendoza, Tucumán, Mar del Plata | Medium term (2-4 years) |

| Technological advances | +0.7% | National | Medium term (2-4 years) |

| Government import-duty exemptions for advanced medical equipment | +0.6% | National | Short term (≤ 2 years) |

| Expansion of teleradiology networks enabling remote reading | +0.4% | Provincial and rural areas | Medium term (2-4 years) |

| Oncology-focused philanthropic funding & PPP initiatives | +0.3% | Major cancer centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Diseases & Rise in Geriatric Population

Argentina’s population is aging, and chronic neurological and cardiovascular conditions are rising, which elevates MRI referrals for early detection and disease monitoring. Health-care spending climbed from 8.9% of GDP in 2003 to 10.2% in 2015 and has remained above the Latin American average, sustaining public capacity to fund advanced imaging. The physician density of 4.06 per 1,000 inhabitants supports broad referral networks, while the Sumar Program adds more than 20 million publicly insured beneficiaries who now qualify for reimbursed scans. Ninety-one new public hospitals commissioned since 2024 offer high-complexity services that routinely require cross-sectional imaging. ANMAT’s device-quality oversight further reassures clinicians that modern scanners deliver the accuracy needed for chronic-care pathways [1]AGN Business Internet BV, “Argentina Medical Device Regulations,” qservegroup.com.

Growth in Private Diagnostic-Imaging Chains Across Provincial Cities

Private operators are entering secondary cities to capture unmet demand beyond the Buenos Aires metro. Swiss Medical’s USD 80 million acquisition program, including Diagnóstico Maipú and Sanatorio Las Lomas, illustrates the momentum in midsized markets where household incomes are rising. Provincial authorities have launched 134 health-care construction projects funded with ARS 10.155 million (USD 24 million), adding 1,415 beds that raise throughput for radiology departments. A simplified import regime under Decree 70/2023 shortens delivery lead times, letting provincial buyers avoid the backlog that previously deterred equipment upgrades. Teleradiology hubs connect local scanners to subspecialty readers in the capital, allowing smaller centers to offer MRI without hiring full-time neuroradiologists.

Technological Advances

Manufacturers now market helium-free magnets, AI-assisted reconstruction, and portable consoles, which match Argentina’s need for lower operating overhead. Siemens Healthineers’ MAGNETOM Flow uses just 0.7 liters of helium and integrates deep-learning algorithms to cut scan times. GE HealthCare’s SIGNA MAGNUS 3 T head-only scanner delivers premium gradient performance for brain research while limiting system footprint. Canon Medical incorporates native neural-network reconstruction that produces higher-resolution studies at equivalent scan durations, valuable where technologist shortages limit throughput efficiency. Such advances reduce per-scan energy consumption and improve patient comfort, two parameters that provincial administrators weigh heavily when approving capital projects.

Government Import-Duty Exemptions for Advanced Medical Equipment

Since 2024 the Statistical Import System (SEDI) has removed non-automatic licensing for medical devices and lets importers pay suppliers in 30–60 days instead of six months, improving cash flow. A parallel bond scheme (BOPREAL) grants pesos-denominated access to U.S. dollars, offsetting peso volatility for distributors. Small consignments worth under USD 3,000 clear through a simplified courier window, which accelerates spare-parts availability and keeps installed scanners online longer. The policy aligns with President Milei’s broader fiscal stabilization, which returned the primary budget to surplus in 2025, reassuring foreign vendors that receivables risk is receding.

Expansion of Teleradiology Networks Enabling Remote Reading

Cloud-based picture-archiving links have expanded from urban trauma centers into provincial clinics, letting local technologists capture images and send them to off-site neuroradiologists who deliver reports within an hour. This model maximizes Argentina’s radiologist pool, of which 45% resides in Buenos Aires, by reallocating after-hours reading capacity nationwide. Diagnostic accuracy remains high because AI triage tools prioritize critical findings, and latency is mitigated by fiber upgrades under the National Connectivity Plan. Provincial governments endorse teleradiology to reduce patient transfers and associated costs, and insurers reimburse remote interpretations at the same tariffs as in-house reads, providing predictable revenue for imaging chains.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & lifecycle cost of MRI systems | -1.1% | National | Long term (≥ 4 years) |

| Peso volatility & capital-equipment financing constraints | -0.9% | National | Short term (≤ 2 years) |

| Shortage of trained MRI technologists outside Buenos Aires | -0.6% | Provincial and rural areas | Medium term (2-4 years) |

| Customs delays & regulatory bottlenecks for high-tech imports | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront & Lifecycle Cost of MRI Systems

Typical 1.5 T scanners priced above USD 1.5 million test the cash positions of provincial hospitals that have faced a 35% real-term funding drop since 2024. The suspension of VAT-exemption certificates until June 2025 forces importers to prepay taxes, raising working-capital needs by roughly 21% on average[2]Baker McKenzie, “Suspension of VAT and Income-Tax Exemption Certificates,” bakermckenzie.com. Operating expenses also stay high because helium trades near USD 35 per liter on global markets, and service contracts denominated in U.S. dollars expose buyers to exchange shocks. Although the Regime for Incentive Investments (RIGI) offers accelerated depreciation, few small facilities qualify, leaving larger private chains to absorb the benefit.

Peso Volatility & Capital-Equipment Financing Constraints

The peso depreciated 130% against the U.S. dollar between January 2024 and May 2025, complicating repayment forecasts for loans pegged to foreign currency. Domestic banks quote rates above 60%, rendering peso loans unsuitable for ten-year assets. Multilateral lenders provide cheaper lines but require sovereign guarantees that are time-consuming to arrange. The central bank’s BOPREAL bond program partly mitigates the currency gap, yet buyers still shoulder devaluation risk during the 30-day window before the first supplier payment. This uncertainty can delay purchase orders unless vendors agree to escrow-based pricing.

Shortage of Trained MRI Technologists Outside Buenos Aires

Vacancy rates for MRI technologists exceed 18%, mirroring global shortages but intensified by Argentina’s concentration of talent in the capital[3]RSNA News, “Addressing Interventional Radiology Shortage,” rsna.org . Of the 5,000 medical graduates per year, fewer than 200 pursue radiologic technology, and residency slots fill quickly. Provincial centers therefore rely on traveling technologists, which inflates staffing costs and limits scanner uptime to daytime shifts. Brain drain to North American markets further erodes the talent pool as bilingual technologists accept remote scanning roles abroad. GE HealthCare and Siemens sponsor certificate programs with local universities, yet capacity remains too small to cover projected demand through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Drive Market Dominance

Closed-bore scanners generated 64.62% of the Argentina Magnetic Resonance Imaging (MRI) Market size in 2025 as tertiary hospitals and high-volume outpatient centers continued to favor their superior signal-to-noise ratio. Patient throughput in sites such as Hospital Italiano frequently exceeds 30 scans daily, making high-duty-cycle magnets economically justifiable. The Argentina MRI market continues to shift, however, as open platforms register a 5.02% CAGR through 2031, spearheaded by provincial diagnostic chains that aim to serve claustrophobic, bariatric, and pediatric cohorts. AI-assisted reconstruction and redesigned gradient coils have narrowed the historical quality gap between open and closed geometries, letting providers deliver neurology and musculoskeletal protocols within reimbursable scan times. Government loans for accessibility upgrades further encourage adoption of wider-bore units in public hospitals.

Operational cost savings also tilt some buyers toward modern open models. Helium-light designs and air-cooling options reduce annual maintenance spending by up to 30% compared with legacy closed scanners. In smaller markets where daily volumes hover near ten scans, break-even calculations now favor open magnets that carry lower acquisition prices. Vendors bundle remote-service diagnostics that predict component failures, minimizing downtime for centers that lack on-site engineers. As patient-centric care gains policy traction, marketing campaigns emphasize comfort advantages, reinforcing adoption momentum across secondary cities.

By Field Strength: 1.5 T Systems Balance Performance and Economics

High-field 1.5 T platforms captured 63.10% of Argentina Magnetic Resonance Imaging (MRI) Market share in 2025 because they meet routine neuro and body imaging needs while staying within hospital power and cryogen limits. Most third-party payers reimburse at tariff levels calibrated to 1.5 T operating costs, sustaining their dominance. The Argentina MRI market is nonetheless transitioning toward 3 T capability, with the very-high/ultra-high segment growing 5.17% per year. Research institutes tied to CONICET adopt 3 T units for functional MRI and spectroscopy, and private cancer centers invest to differentiate services amid competitive pricing pressures.

Equipment vendors facilitate the transition by offering upgrade-friendly platforms that let sites start at 1.5 T and field-upgrade to 3 T with modular gradient amplifiers. Leasing models pegged to exam volume lower upfront exposure for private clinics exploring 3 T installations. Meanwhile, low-field portable systems under 0.5 T address rural outreach programs and sports-medicine practices, but their aggregate contribution to Argentina MRI market size remains small due to limited reimbursement and narrower use cases.

By Application: Neurology Leadership with Oncology Acceleration

Neurology held 31.84% of revenue in 2025 because stroke, epilepsy, and neuro-degeneration protocols represent core indications across Argentina’s referral network. More than 43% of MRI referrals from public hospitals relate to central-nervous-system assessment. By contrast, oncology is projected to post the quickest climb at a 5.44% CAGR, raising its share of the Argentina MRI market size as the Rays of Hope program scales radiation-therapy capacity. National cancer-registry data show incidence climbing 2.1% annually, driving demand for staging and follow-up scans.

Cardiac MRI adoption also grows, albeit from a smaller base, as cardiologists seek non-invasive methods to assess myocarditis and congenital anomalies. GE HealthCare’s manganese-based contrast agent under development could increase repeat-scan safety, benefiting oncologic and cardiac cohorts that require serial imaging. Musculoskeletal and abdominal applications diversify revenue but rise more slowly because CT and ultrasound still suffice for many orthopedic and liver indications under Argentina’s reimbursement codes.

Geography Analysis

Buenos Aires accounts for roughly 40% of installed scanners and delivers the highest exam volume because it hosts the largest concentration of neurologists, oncologists, and research centers. High patient density, comprehensive insurance coverage, and established referral pathways keep utilization above 85% of scanner capacity. Public–private partnerships allow community hospitals in the metro to outsource overflow studies to private chains during peak hours, optimizing system-wide asset use.

Secondary provinces such as Córdoba, Santa Fe, and Mendoza represent the fastest-expanding zones within the Argentina MRI market, adding open and mid-field units to meet rising middle-income demand. Provincial governments co-finance equipment through matching-fund grants tied to service obligations for low-income patients. Connectivity improvements enable these centers to leverage teleradiology for subspecialty reads, mitigating the technologist and radiologist shortages that have historically hampered advanced imaging outside the capital.

Patagonia, the Northwest, and rural Chaco remain underserved, with scanner-to-population ratios under 1 per 100,000 inhabitants. Mobile MRI trailers deployed on seasonal schedules improve access, yet logistical hurdles—long travel distances and limited power infrastructure—cap exam volumes. Public-health planners are evaluating subsidy models that couple low-field portable scanners with cloud reading hubs as a lower-cost alternative to fixed 1.5 T installations.

Competitive Landscape

Global vendors dominate the Argentina MRI market through exclusive distributor partnerships and installed-base service contracts. GE HealthCare, Siemens Healthineers, and Philips collectively control more than 65% of active units, leveraging multi-modality portfolios and financing arms to secure tenders. Canon Medical and Fujifilm are gaining share by promoting AI-ready open systems priced 10–15% below incumbents. Chinese entrant United Imaging sells high-field scanners bundled with five-year service at flat peso rates, appealing to cost-sensitive provincial buyers.

Strategic moves among provider groups also shape demand. Swiss Medical’s bid for Diagnóstico Maipú aims to create a national imaging chain capable of negotiating bulk equipment purchases and unified maintenance agreements. Grupo Olmos is modernizing its provincial clinics with helium-light systems to curb operating costs as utility tariffs rise. Academic centers partner with vendors on research protocols that test AI-based cardiac and functional MRI, accelerating clinical adoption of next-generation applications.

Price competition intensifies as government policies compress reimbursement growth. Vendors respond with productivity-boosting software—auto-positioning, deep-learning reconstruction, and cloud fleet management—that shortens exam slots by 15–20%. Service differentiation, including technician-training scholarships and in-country parts depots, emerges as a deciding factor in tender awards, especially outside Buenos Aires where uptime logistics are critical.

Argentina Magnetic Resonance Imaging (MRI) Industry Leaders

-

Fujifilm Holdings Corporation

-

Koninklijke Philips NV

-

Siemens Healthcare GmbH

-

GE HealthCare

-

Canon Inc. (Canon Medical Systems Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: AIRS Medical signed a distribution agreement with Simbioxia to deploy its SwiftMR AI-reconstruction software in Argentine scanning centers.

- April 2023: Hospital Garrahan inaugurated a 3 T pediatric-optimized MRI suite that cuts scan time and enhances image resolution for complex congenital cases.

Argentina Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique that is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. The Argentina Magnetic Resonance Imaging Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, Very High Field MRI Systems, and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (<0.5 T) |

| High-Field (1.5 T) |

| Very-High/Ultra-High (3 T and ≥7 T) |

By Application

| Oncology |

| Neurology |

| Cardiology |

| Other Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (<0.5 T) |

| High-Field (1.5 T) | |

| Very-High/Ultra-High (3 T and ≥7 T) | |

| By Application | Oncology |

| Neurology | |

| Cardiology | |

| Other Applications |

Key Questions Answered in the Report

What is the current Argentina Magnetic Resonance Imaging (MRI) Market size?

The sector is projected to generate USD 88.06 million in 2026 and USD 110.05 million in 2031 based on a 4.55% CAGR during 2026-2031.

Who are the key players in Argentina Magnetic Resonance Imaging (MRI) Market?

Fujifilm Holdings Corporation, Koninklijke Philips NV, Siemens Healthcare GmbH, GE HealthCare and Canon Inc. (Canon Medical Systems Corporation) are the major companies operating in the Argentina Magnetic Resonance Imaging (MRI) Market.

Which MRI architecture sells the most units in Argentina?

Closed-bore scanners dominate with 64.62% of 2025 installations thanks to high image quality and throughput.

What field strength is growing fastest across Argentine providers?

Very-high-field systems at 3 T and above are expanding 5.17% per year as research and oncology centers upgrade.

Page last updated on: