Brazil Data Center Construction Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

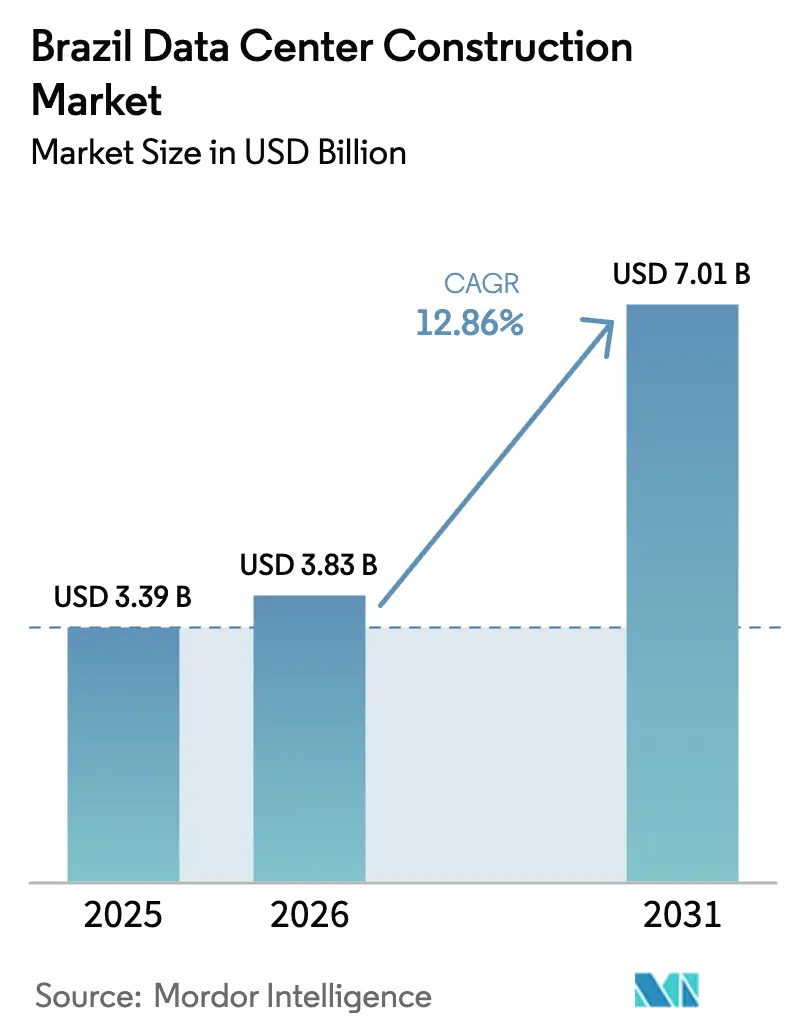

| Base Year Market Size (2025) | USD 3.39 Billion |

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 7.01 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Data Center Construction Market Analysis by Mordor Intelligence

The Brazil data center construction market size was valued at USD 3.39 billion in 2025 and estimated to grow from USD 3.83 billion in 2026 to reach USD 7.01 billion by 2031, at a CAGR of 12.86% during the forecast period (2026-2031). This rapid escalation positions Brazil as the focal point for Latin America’s AI and cloud infrastructure build-out, accounting for 75% of projected regional capital expenditures. The surge is underpinned by a mature electricity sector, in which 85% of generation comes from renewable sources, providing operators with a structural cost advantage and helping them meet their corporate decarbonization targets. Hyperscale cloud providers, such as Amazon Web Services and Microsoft, are spearheading demand by pledging multi-billion-dollar expansions, while consolidation among tier-one colocation specialists is redefining the competition. São Paulo remains the nucleus with 48 active facilities and 351 MW of installed capacity; however, new subsea-cable landings are encouraging edge deployments in Fortaleza, Rio de Janeiro, and other coastal hubs.

Key Report Takeaways

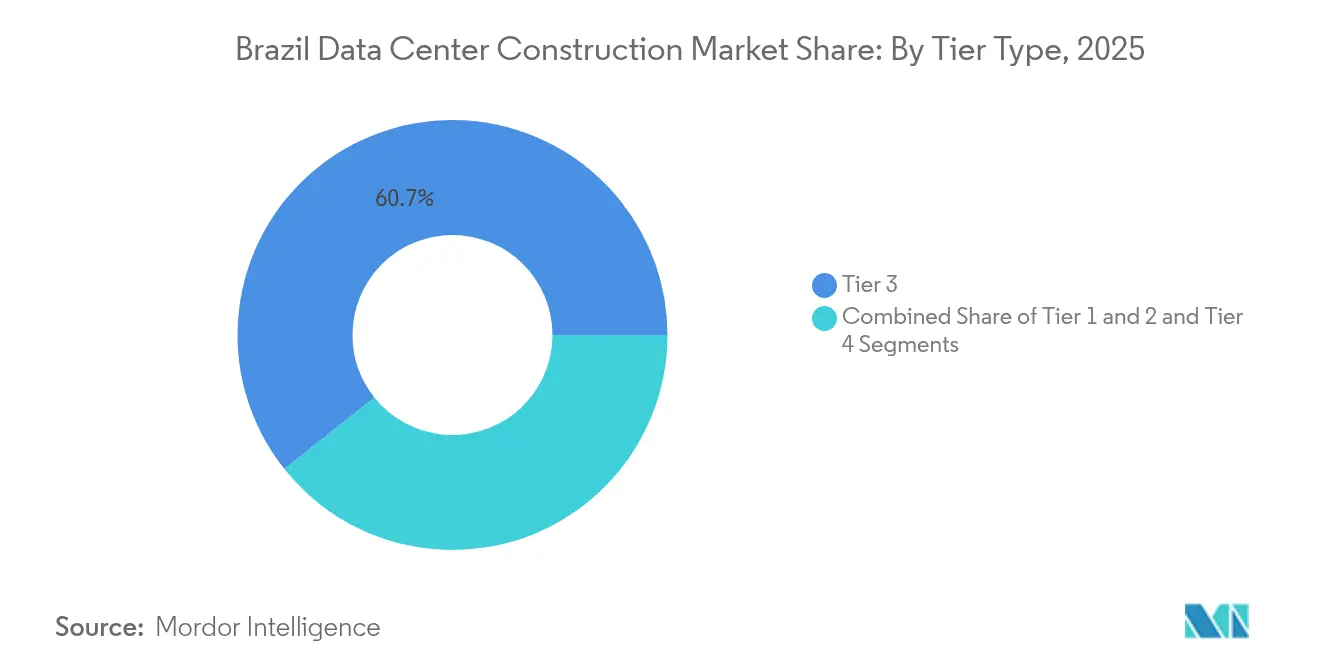

- By tier type, Tier 3 sites led with 60.72% of the Brazil data center construction market share in 2025, while Tier 4 facilities are projected to expand at a 17.15% CAGR through 2031.

- By data center type, colocation captured 65.75% revenue share in 2025; self-build hyperscale projects record the highest expected CAGR at 17.95% to 2031.

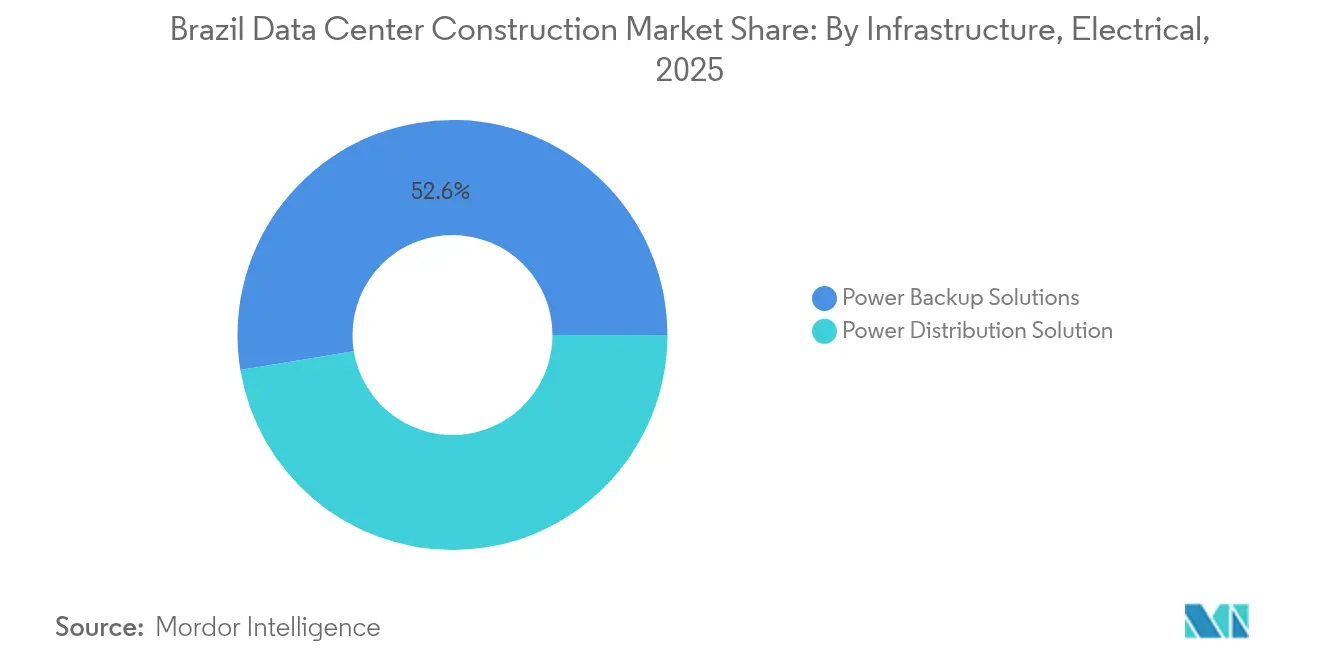

- By electrical infrastructure, power-backup systems accounted for 52.61% of spending in 2025, whereas power-distribution solutions are growing at a 17.09% CAGR to 2031.

- By mechanical infrastructure, cooling equipment commanded 47.68% of 2025 outlays, and servers plus storage are advancing at a 15.95% CAGR over the forecast horizon.

- By geography, the São Paulo metropolitan region housed 51.42% of national capacity in 2025, with Fortaleza emerging as the fastest-growing edge location on the back of new cable landings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of cloud and AI by enterprises | +3.2% | São Paulo, Rio de Janeiro, Belo Horizonte | Medium term (2-4 years) |

| Government digital-transformation programs | +2.1% | National, focus on underserved regions | Long term (≥ 4 years) |

| Abundant renewable energy | +1.8% | Hydroelectric corridors nationwide | Medium term (2-4 years) |

| 24/7 carbon-free PPAs | +1.5% | São Paulo, Minas Gerais, Rio Grande do Sul | Short term (≤ 2 years) |

| Edge build-outs near subsea cables | +1.3% | Coastal cities (Rio, Fortaleza, Santos) | Medium term (2-4 years) |

| Fast-track permits for brownfield sites | +0.9% | Industrial belts in São Paulo, Rio de Janeiro | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud and AI by Brazilian Enterprises

Enterprise migration to cloud platforms and large-scale AI workloads is reshaping facility specifications across the Brazil data center construction market. The Ministry of Mines and Energy logged a rise in projected industry power demand from 2.5 GW to 9 GW between early and late 2024,[1]Ministério de Minas e Energia — “Crescimento de Demanda de Energia para Data Centers,” mme.gov.br underscoring the speed of digital adoption. Scala Data Centers’ proposed USD 50 billion “AI City” in Rio Grande do Sul typifies the pivot toward purpose-built campuses optimized for >20 kW per rack densities. Microsoft’s R$ 14.7 billion commitment likewise targets GPU-rich infrastructure to sustain enterprise AI services. Collectively, these moves are pushing designers to integrate liquid cooling, robust power distribution and 24/7 renewable energy supply into new builds.

Government Digital-Transformation and Connectivity Programs

Federal and state initiatives ranging from nationwide 5G corridors to e-government platforms are fostering steady demand beyond Brazil’s prime metros. Draft bill PL 3018/2024 highlights infrastructure standards for AI systems and underscores the sovereign-data agenda. Public-sector modernization cascades into private investment as suppliers extend hybrid-cloud architectures into regional hubs, supporting healthcare, education and fintech workloads that require low-latency processing and strict data-residency controls.

Abundant Renewable Energy Improving PUE Economics

With 85% renewable generation on the national grid, operators can embed stringent sustainability targets into project finance models, for instance, procures 100% renewable electricity under a multi-gigawatt agreement with Serena Energia, enabling consistent sub-1.3 PUE across its campuses Scala Data Centers. The clean-power backdrop attracts foreign hyperscalers that seek carbon neutrality without relying on certificate schemes prevalent in thermal-powered markets.

24/7 Carbon-Free PPAs Enabling Green Hyperscale Builds

Round-the-clock carbon-free power purchase agreements (PPAs) are now common in Brazil, ensuring uninterrupted green energy even at peak load. Atlas Renewable Energy’s 902 MWp contract with an industrial offtaker illustrates the scale and tenor that data-center developers can replicate,[2]Atlas Renewable Energy — “902 MWp PPA Announcement,” atlasrenewableenergy.com locking in predictable electricity costs for 20-plus years . Such arrangements satisfy corporate ESG metrics and bolster investment-grade credit profiles for large campuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High power use and GHG scrutiny | -1.4% | National, strongest in dense metros | Short term (≤ 2 years) |

| Import tariffs on IT and cooling equipment | -2.3% | National | Medium term (2-4 years) |

| Grid-connection delays in North São Paulo | -1.8% | São Paulo metropolitan area | Short term (≤ 2 years) |

| Water-stress regulations | -0.7% | Drought-prone Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Power Consumption and GHG Footprint Scrutiny

Environmental watchdogs and municipal authorities are intensifying oversight as data centers already consume 0.5% of national electricity. Operators are responding with advanced cooling, on-site solar and waste-heat reuse, yet the added capex can elongate construction timelines. ODATA’s locally produced Delta Cube liquid-cooling solution exemplifies innovation aimed at curbing water draw while boosting rack densities.[3]ODATA — “Launch of Delta Cube Cooling System,” odata.com

Import Tariffs on IT and Cooling Equipment Exceeding 60%

Although Brazil’s ex-tariff lists soften duties on 1,495 ICT products, many bespoke AI-grade cooling and power components still face rates above 60%. Developers must either localize manufacturing or redesign layouts around domestically sourced parts, adding complexity and cost. Construction inflation compounds the issue, with the national SINAPI index showing 4.69% year-on-year escalation to April 2025

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Premium Uptime Requirements Accelerate Tier 4 Adoption

The Brazil data center construction market size for Tier 3 facilities stood at USD 2.06 billion in 2025, translating into a 60.72% Brazil data center construction market share for balanced-cost installations. Tier 4 builds, while smaller in absolute value, are projected to compound at 17.15% annually through 2031 as hyperscalers demand fault-tolerant architectures.

The shift reflects lower tolerance for downtime in AI training cycles and financial-services workloads. Projects such as Scala’s Tamboré campus illustrate a design philosophy that blends Tier 4-level redundancy with renewable-energy integration, setting new benchmarks for resiliency and sustainability

By Data Center Type: Self-Build Hyperscalers Reshape Supply Dynamics

Colocation retained 65.75% of the Brazil data center construction market size in 2025, delivering shared-facility efficiencies to mid-market customers. Self-build projects, however, are rising fastest at an 17.95% CAGR, driven by cloud majors customizing layouts for high-density GPU pods.

Microsoft’s three-year R$14.7 billion program underscores the momentum, signaling a future where tailored electrical backbones and proprietary cooling top the design agenda.Colocation operators are countering with build-to-suit models and joint ventures to preserve wallet share.

By Electrical Infrastructure: High-Density Power Delivery Gains Priority

Power-backup arrays led 2025 spending, yet intelligent distribution systems are forecast to expand at 17.09% CAGR as rack densities exceed 20 kW. Investments such as Scala’s planned 560 MW substation in São Paulo epitomize the pre-emptive grid modernization essential for AI workloads.

Advanced switchgear, busways and software-defined power controls afford operators the precision to toggle renewable inputs, curb harmonics and support demand-response contracts with utilities—abilities critical for both uptime and ESG compliance.

By Mechanical Infrastructure: Liquid Cooling Anchors Next-Gen Facility Design

Cooling hardware captured 47.68% of mechanical outlays, yet server and storage investments are rising at 15.95% CAGR, reflecting a pivot toward GPU-rich clusters. The industry is transitioning from air-based to immersive and direct-to-chip liquid solutions capable of extracting 100 kW per rack without penalizing PUE.

ODATA’s in-country manufacture of the Delta Cube system demonstrates how local supply chains are adapting to tariff pressures while maintaining global-class performance. Integrated rack offerings that bundle cooling manifolds with high-bandwidth fabric switches are becoming table stakes for new bids.

Geography Analysis

São Paulo concentrates 51.42% of national IT power and remains the anchor of the Brazil data center construction market. Agglomeration economics, superior fiber density and access to financial-services clients fortify its dominance, even as grid congestion nudges developers toward outlying industrial corridors.

Rio de Janeiro follows, propelled by multiterabit subsea landings on the BRUSA cable, which links Brazil to North America and Caribbean nodes. The connectivity boost shortens round-trip latency for content providers, encouraging capacity expansions such as Equinix RJ3 and Tecto’s Mega Lobster facility.

Secondary metros—Fortaleza, Belo Horizonte and Porto Alegre—are capturing edge-workload spillover and benefit from abundant renewable generation. V.tal’s R$ 550 million investment in Ceará leverages local solar resources while tapping a growing developer talent pool. Government connectivity grants and smarter grid interties suggest a progressive diffusion of capacity into Brazil’s interior, enhancing resilience and diversifying regional economic benefits.

Competitive Landscape

Sixty-seven operational data centers managed by 22 providers create a marketplace that balances scale advantages with room for specialists. Digital Realty’s USD 1.8 billion acquisition of Ascenty yields the country’s largest portfolio at 16 sites, illustrating how global operators use M&A to secure an instant footprint and bring metro-connect fabrics to local customers.

Financial investors are also scaling in. Patria’s USD 1 billion launch of a new platform and Brookfield’s ongoing partner search for Ascenty hint at a steady private-equity appetite amid robust utilization rates. Meanwhile, Vantage Data Centers’ USD 9.2 billion fundraise sets the stage for a possible Brazilian entry, which could intensify competition on energy-efficient hyperscale builds.

Brazil Data Center Construction Industry Leaders

AECOM

Jacobs Engineering Group

Turner & Townsend

Skanska

Arup

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Patria unveiled a USD 1 billion data-center platform targeting hyperscale and edge projects across Brazil

- February 2025: Tecto completed its USD 110 million Mega Lobster facility in Fortaleza, adding 20 MW of capacity.

- January 2025: V.tal’s Tecto unit acquired land for a 200 MW hyperscale campus in São Paulo

- January 2025: Vantage Data Centers raised USD 9.2 billion to support a USD 30 billion global build program, with Brazil flagged as a target.

- October 2024: V.tal launched the Tecto subsidiary with USD 1 billion earmarked for new Brazilian facilities.

- September 2024: Microsoft announced a three-year R$ 14.7 billion cloud and AI infrastructure investment across Brazil

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Brazil data center construction market as the value of capital spending on electrical, mechanical, and general-construction works required to deliver new or expanded mission-critical facilities that meet internationally recognized Tier standards. It covers colocation campuses, self-built hyperscaler sites, and enterprise or edge builds regardless of ownership model.

Scope exclusion: refurbishment budgets for live facilities are not counted.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility architects, electrical contractors, cooling-system vendors, and senior managers at colocation, hyperscale, and enterprise operators in São Paulo, Rio de Janeiro, Fortaleza, and Porto Alegre. These conversations validated cost-per-watt ranges, lead-time shifts, and utilization ramp-up patterns while resolving gaps left by secondary data.

Desk Research

We began with public macro-datasets from the Brazilian Institute of Geography and Statistics, energy regulator ANEEL, and customs shipment records, which clarify national investment cycles and imported infrastructure volumes. Trade bodies such as the Brazilian Data Center Association, Uptime Institute certification filings, and TeleGeography's colocation tracker reveal capacity adds, average rack densities, and Tier mix. Company 10-Ks, operator presentations, and local press briefings supply project-level CAPEX benchmarks and build-out timelines. Select licensed databases, including D&B Hoovers for contractor financials and Dow Jones Factiva for project news, enrich the baseline. This list is illustrative; many other open and paid sources supported data gathering.

Market-Sizing & Forecasting

A top-down model converts new IT-load additions (MW) and average cost-per-watt into annual spend, reconstructed from capacity announcements, building permits, and power-connection data, then corroborated through sampled bottom-up checks on major contractor invoices. Key variables include average equipment cost index, Tier IV penetration, hyperscaler share of new MW, currency movement, and lead-time slippage. Multivariate regression combined with scenario analysis projects these drivers through 2030, and missing bottom-up inputs are bridged by regional cost curves derived from tender data.

Data Validation & Update Cycle

Outputs run through variance checks versus historical CAPEX-to-MW ratios, exchange-rate buffers, and peer project costs; anomalies trigger re-contact of select experts before sign-off. The study refreshes annually, with interim revisions when material events, large campus announcements or policy shifts, occur, and every client copy receives a last-mile analyst review.

Why Mordor's Brazil Data Center Construction Baseline Earns Trust

Published estimates often diverge because firms choose different build-scope definitions, cost indices, and update cadences.

In comparison, two external publications place the 2024 market between USD 3.12 billion and USD 3.40 billion, reflecting narrower infrastructure baskets or older exchange assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.39 bn (2025) | Mordor Intelligence | - |

| USD 3.12 bn (2024) | Global Consultancy A | Excludes general-construction services and uses 2023 FX rates |

| USD 3.40 bn (2024) | Industry Journal B | Relies on announced projects only; limited Tier verification |

Consistently applying a full infrastructure scope, fresh currency conversions, and dual-path validation lets Mordor Intelligence deliver a balanced, transparent baseline clients can trace back to named variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Brazil data center construction market?

The Brazil data center construction market size stands at USD 3.83 billion in 2026 and is forecast to reach USD 7.01 billion by 2031.

Which city hosts the largest concentration of Brazilian data centers?

São Paulo leads with 48 facilities and 351 MW of IT load, amounting to 51.42% of national capacity.

Why are Tier 4 facilities growing faster than other tiers?

Hyperscale cloud and AI workloads require fault-tolerant architectures and 24/7 availability, resulting in a 17.15% CAGR outlook for Tier 4 builds.

How important is renewable energy to new data center projects in Brazil?

With 85% of national power generation coming from renewables, operators leverage green electricity to hit sub-1.3 PUE targets and secure carbon-free PPAs.

What are the main challenges facing developers?

High import tariffs on specialized equipment, grid-connection delays around São Paulo and rising environmental scrutiny on power and water use are key headwinds.

Are self-build hyperscale campuses overtaking colocation in Brazil?

Colocation still holds 65.75% share, but self-build campuses are expanding at an 17.95% CAGR as cloud majors seek bespoke layouts and tighter ESG control.

Page last updated on: