Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

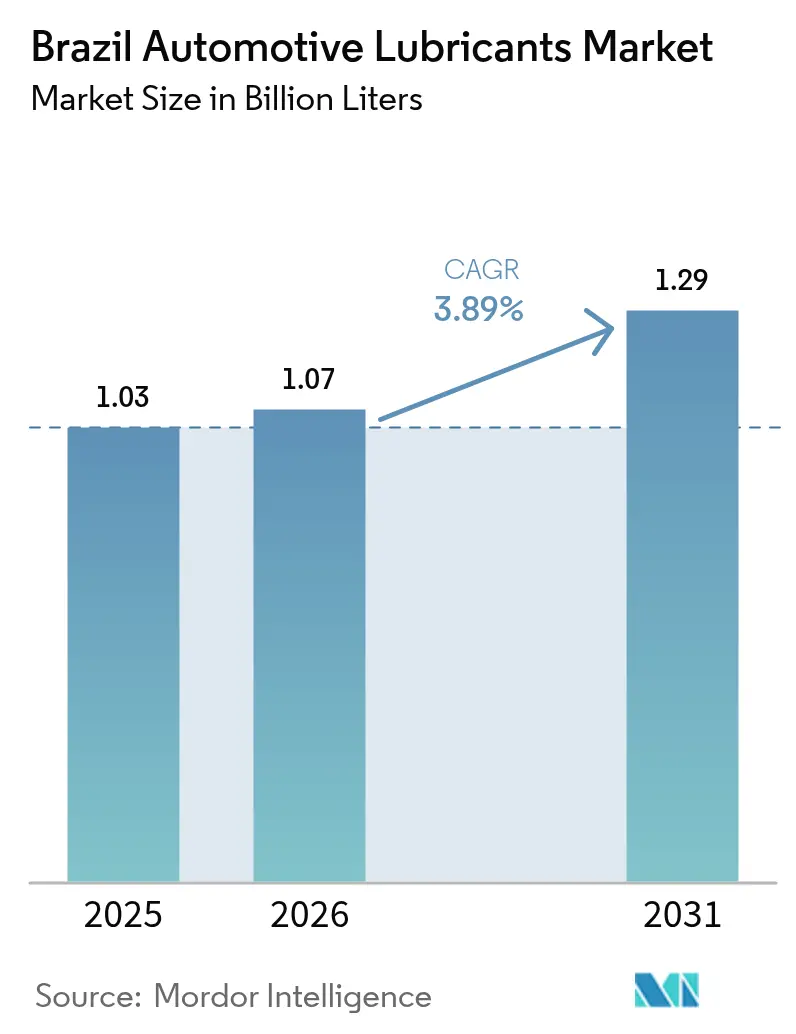

| Base Year Market Size (2025) | 1.03 Billion Liters |

| Market Volume (2026) | 1.07 Billion Liters |

| Market Volume (2031) | 1.29 Billion Liters |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

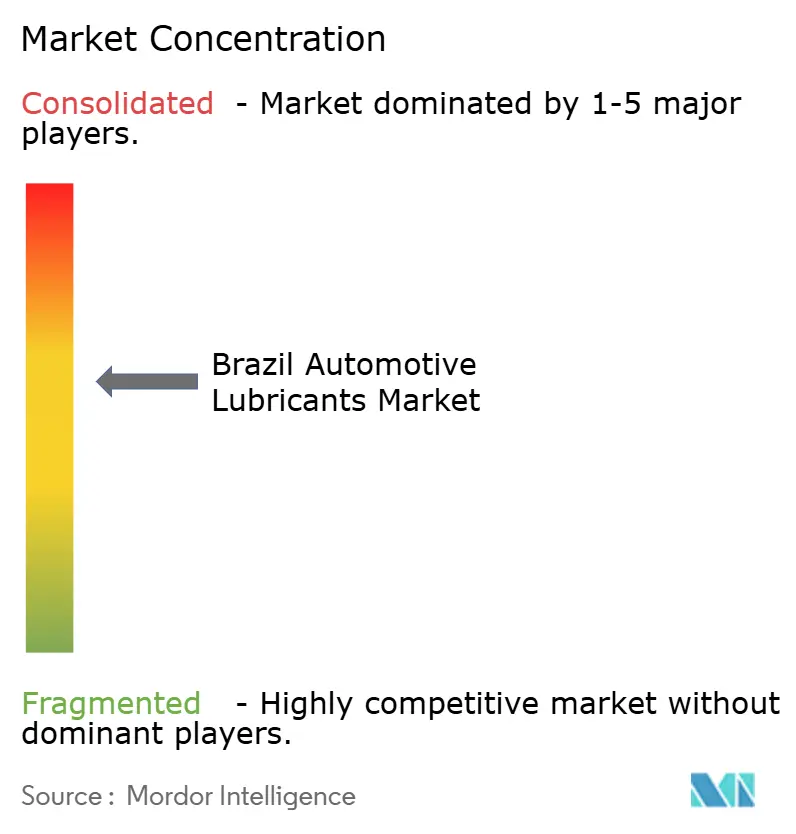

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Automotive Lubricants Market Analysis by Mordor Intelligence

The Brazil Automotive Lubricants Market size is expected to grow from 1.03 Billion Liters in 2025 to 1.07 Billion Liters in 2026 and is forecast to reach 1.29 Billion Liters by 2031 at 3.89% CAGR over 2026-2031. Brazil’s position as the largest finished-lubricant consumer in South America is anchored by resilient vehicle-parc expansion, rising synthetic-grade penetration, and tightening emissions rules that reward higher-performance formulations. Upgrades mandated by PROCONVE L7/L8, combined with mandatory biodiesel blend escalation, are accelerating demand for low-viscosity, oxidation-stable products that protect particulate filters and after-treatment systems. Robust infrastructure spending, sustained agricultural mechanization, and a rebound in light-vehicle sales support lubricant consumption across both passenger and commercial fleets. Competitive intensity remains moderate, yet rising investment in domestic Group II base-oil capacity and counterfeit-mitigation packaging is reshaping distributor strategies as suppliers chase premium margins.

Key Report Takeaways

- By product type, engine oils held 62.68% of the Brazil automotive lubricants market share in 2025, while automatic transmission fluids are projected to expand at a 3.45% CAGR through 2031.

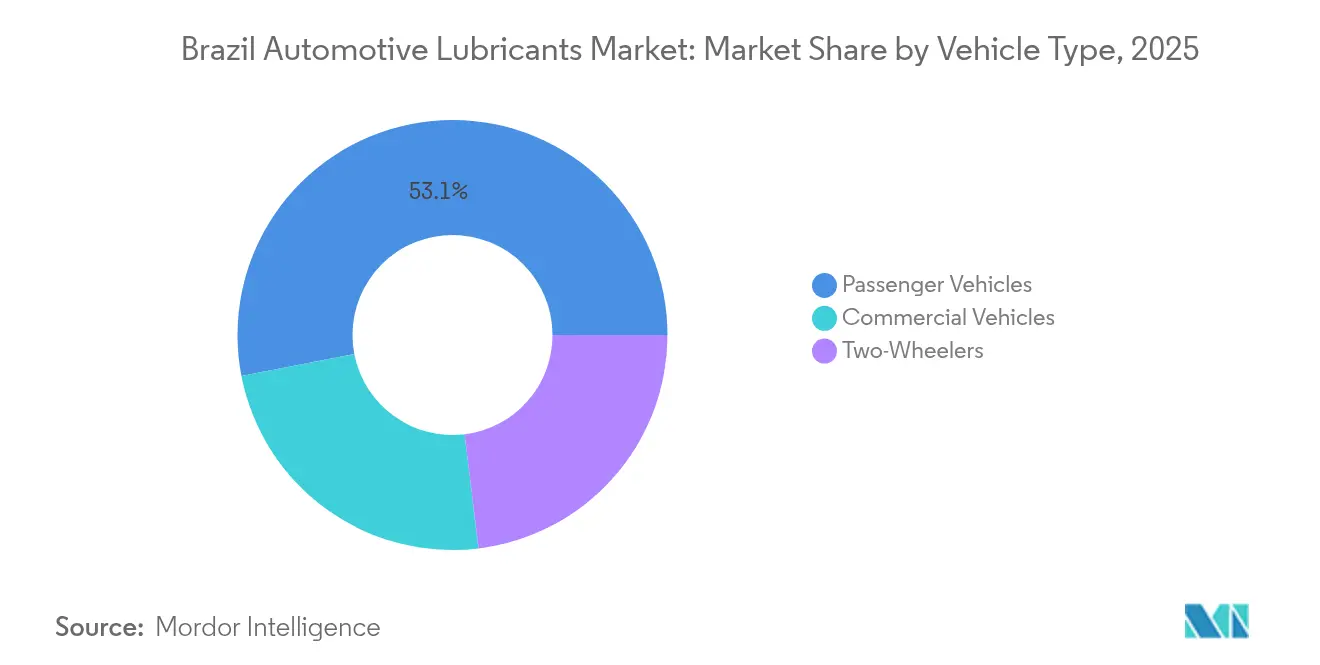

- By vehicle type, passenger cars accounted for a 53.05% share of the Brazilian automotive lubricants market size in 2025, and commercial vehicles are projected to advance at a 3.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vehicle parc and post-pandemic sales rebound | +1.2% | National, with concentration in São Paulo, Rio de Janeiro, Minas Gerais | Medium term (2-4 years) |

| Enforcement of PROCONVE L7/L8 emissions & fuel-efficiency norms | +0.8% | National, with early adoption in metropolitan areas | Long term (≥ 4 years) |

| Rapid shift toward synthetic & semi-synthetic lubricants | +0.7% | National, led by premium segments in urban centers | Medium term (2-4 years) |

| Mandatory biodiesel blend escalation (B12-B15) driving heavy-duty oil upgrades | +0.5% | National, concentrated in agricultural and logistics corridors | Short term (≤ 2 years) |

| Corn-ethanol boom boosting flex-fuel-compatible lubricant demand | +0.4% | Midwest states (Mato Grosso, Goiás), expanding nationally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing vehicle parc and post-pandemic sales rebound

Vehicle production rebounded strongly after the pandemic, pushing fleet growth across both passenger and commercial segments. The Energy Research Office projects that Brazil’s total fleet will reach 50.4 million units by 2033, providing a reliable base for lubricant demand despite the gradual electrification of vehicles. The record 2023 Otto-cycle fuel consumption of 59.1 billion litres signals healthy mileage that directly translates into lubricant drain intervals. Commercial vehicles benefit most from infrastructure and agribusiness investment, requiring higher sump volumes and extended-drain formulations. A younger fleet age also favors low-viscosity synthetic grades that align with OEM warranty requirements and PROCONVE standards[1]Energy Research Office, “Brazilian Vehicle Fleet Outlook 2025-2033,” epe.gov.br.

Enforcement of PROCONVE L7/L8 emissions and fuel-efficiency norms

PROCONVE L7/L8 introduces Euro 6-equivalent limits on particulate matter and NOx, compelling OEMs to specify low-ash, low-sulfur lubricants that protect diesel particulate filters and SCR systems. The Brazilian Vehicle Labeling Program amplifies this push by rewarding low-friction fluids that cut fuel use. A dual market is emerging: legacy vehicles continue using conventional oils, whereas new registrations demand premium synthetic or semi-synthetic products. Commercial operators face higher compliance costs because extended-drain heavy-duty lubricants must balance soot control, biodiesel stability, and hardware durability. Suppliers that secure OEM approvals and API CK-4/FA-4 certifications capture the fastest-growing share of the Brazil automotive lubricants market.

Rapid shift toward synthetic and semi-synthetic lubricants

Consumers are gravitating toward synthetic lubricants that handle Brazil’s stop-and-go traffic, ethanol blends, and high ambient temperatures with fewer top-ups. Petrobras has earmarked BRL 33 billion for a 12,000 barrels-per-day Group II upgrade at the Boaventura complex, a move that will reduce reliance on imports and stabilize feedstock pricing. Distributors promote synthetics aggressively because price premiums can lift margins tenfold compared to fuels. Premiumization also helps combat illicit trade, since counterfeiters struggle to replicate tamper-proof packaging and OEM hologram seals. Automatic transmission fluids benefit disproportionally as synthetic base stocks enable smoother gear shifts and longer service intervals in Brazil’s rising automatic-gearbox parc.

Mandatory biodiesel blend escalation driving heavy-duty oil upgrades

Brazil raised the biodiesel mandate from B12 to B15 in 2025 and has signaled a path to B20 by 2030. Biodiesel’s higher oxygen content accelerates oil oxidation, increases acidity and elevates soot loading, prompting fleets to shorten drain intervals unless they switch to higher-detergent, oxidation-stable lubricants. Soy-based feedstock, now 69% of national biodiesel output, imposes additional compatibility demands. Heavy-duty operators, therefore, tend to migrate toward synthetic or semi-synthetic diesel engine oils that are balanced for TBN retention and viscosity stability. The predictable blend-increase timeline provides additive suppliers and blenders with clear visibility to scale production of B20-ready products, thereby reinforcing growth in the Brazilian automotive lubricants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import cost spikes from BRL volatility & base-oil supply disruptions | -0.9% | National, with greater impact on import-dependent regions | Short term (≤ 2 years) |

| Accelerating light-vehicle electrification and hybrid penetration | -0.6% | Urban centers (São Paulo, Rio de Janeiro, Brasília) expanding nationally | Long term (≥ 4 years) |

| Proliferation of counterfeit & sub-standard lubricants in informal channels | -0.4% | National, concentrated in price-sensitive rural and suburban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import cost spikes from BRL volatility and base-oil supply disruptions

Brazil imports approximately 880,970 metric tons of base oils annually, so exchange-rate fluctuations directly increase the cost of goods. A shift from BRL 4.17 to BRL 5.66 per USD over recent cycles forced distributors to reprice finished lubricants and compress gross margins. Domestic capacity from three refineries (821,000 tonnes per year) still lags behind demand, exposing blenders to freight bottlenecks and spot-pricing volatility. Companies stockpile or diversify sourcing to cushion shocks, but higher working capital erodes profitability and slows channel restocking. Short-term import-cost volatility, therefore, subtracts 0.9 percentage points from the Brazil automotive lubricants market CAGR outlook.

Accelerating light-vehicle electrification and hybrid penetration

Electric and hybrid vehicles carry little or no engine oil, so their rise trims the service-fill pool. Government incentives and the expansion of charging infrastructure in São Paulo, Rio de Janeiro, and Brasília spur early adoption. OEM announcements suggest that BEV and hybrid sales could reach low-double-digit shares in key metropolitan areas by 2030, potentially dampening long-term lubricant demand. Lubricant suppliers counter with thermal-management fluids and e-gearbox oils, but volumes remain modest compared to ICE requirements. The shift undercuts growth by 0.6 percentage points but remains urban-centric through the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine oils dominate amid ATF acceleration

Engine oils retained a 62.68% share of the Brazilian automotive lubricants market in 2025, driven by a 50 million-plus vehicle fleet and frequent drain intervals in tropical stop-and-go conditions. Synthetic 5W-XX and 0W-XX grades are replacing 15W-XX mineral oils because OEMs specify low-viscosity formulations to meet fuel economy targets. Automatic transmission fluids, although only a mid-single-digit share today, post the fastest 3.45% CAGR to 2031 as car buyers gravitate toward automatic and CVT gearboxes.

The wider product mix shows manual transmission fluids slipping as dual-clutch systems gain popularity, while brake fluids trend in line with vehicle output and periodicity of safety inspections. Greases benefit from demand for commercial-vehicle chassis and agricultural equipment maintenance. Other specialist fluids evolve unevenly; electric power steering reduces hydraulic fluid consumption, but hybrid cooling fluids open a new niche. Product-level substitution, therefore, shapes revenue more than absolute volume growth, reinforcing synthetic expansion within the Brazil automotive lubricants market.

By Vehicle Type: Commercial vehicles propel incremental demand

Passenger cars held a 53.05% share in 2025; however, growth is tilting toward commercial fleets that clock higher mileages and adopt heavier biodiesel blends. Heavy-duty trucks, buses, and off-road machinery are collectively advancing at a 3.19% CAGR, driven by road-building, commodity exports, and e-commerce logistics. High sump capacities and longer drain intervals mean each truck consumes many times the oil of a passenger car, amplifying volume gains.

Two-wheelers remain important in peri-urban transport and last-mile delivery, but the expansion of electric two-wheeler pilots in major cities is tempered. Agricultural machinery in the Midwest and North requires a discrete lubricant stream, especially for engine oils and UTTO fluids, which are compatible with high-dust, high-heat operations. Commercial-vehicle ascendancy thus steers premium formulation demand and underpins overall momentum in the Brazil automotive lubricants market share.

Geography Analysis

The Southeast dominates the Brazil automotive lubricants market, with São Paulo and Rio de Janeiro accounting for roughly 39.60% of vehicle registrations and supporting the densest network of distributors, service shops, and OEM plants. Petrobras’ Duque de Caxias refinery and the planned Boaventura Group II project anchor regional base-oil supply, allowing blenders to reduce logistical costs and provide fluids promptly. Superior disposable income also boosts synthetic uptake among passenger-car owners, reinforcing premium-grade sales.

The Midwest emerges as the fastest-growing territory, powered by agricultural mechanization and a corn-ethanol boom in Mato Grosso and Goiás. Commercial trucks, flex-fuel light vehicles, and farm equipment require lubricants that can withstand biodiesel, ethanol, and abrasive field environments. Corn-ethanol output surged to 5.8 billion litres in 2023, underpinning lubricant consumption for harvesting equipment and fuel-blend-compatible engines.

The Northeast shows consistent, if slower, progress. Industrial projects around the Suape and Pecém ports increase freight traffic, while urbanization in Fortaleza and Recife drives personal vehicle ownership. Supply chains here face longer hauls from southeastern blending hubs, necessitating regional warehouses to mitigate stock-out risks. Despite infrastructural constraints, rising economic activity supports steady lubricant sales, ensuring nationwide coverage for suppliers active in the Brazil automotive lubricants market.

Regulatory Landscape

Brazil regulates automotive lubricants through the Agencia Nacional do Petroleo, Gas Natural e Biocombustiveis (ANP), with mandatory product registration and quality compliance for finished lubricants under Resolucao ANP No. 804/2019. The framework ties performance claims to recognized classifications and test regimes (for example, API, ACEA, JASO, and NMMA), which in practice shapes formulation decisions for low-ash, after-treatment compatible oils aligned with newer emissions requirements such as PROCONVE L7/L8.

ANP also enforces market conduct through tools such as the Monitoring Program for Lubricants (PML), which requires regulated agents to allow sample collection for quality surveillance. On the policy front, ANP's 2025-2026 Regulatory Agenda (56 actions) highlights continued focus on supply oversight, inspection, and product quality, and it includes workstreams to revise rules tied to biodiesel use under Law No. 14.993/2024 (Combustivel do Futuro), reinforcing how fuel policy feeds into lubricant performance requirements.

Value Chain Analysis

The value chain begins with base oils (domestic refinery output plus imports) and additives, then moves into blending and packaging by producers that register finished products with ANP under Resolucao ANP No. 804/2019. Operational participation is gated by authorizations, and ANP also structures activity registration through its electronic processes; in parallel, sector bodies such as SINDICOM, SIMEPETRO, ABRAPOL, and Sindilub influence standards adoption, market practices, and channel development across producers, distributors, and resellers.

Downstream, distribution runs through fuel-station networks, lubricant distributors, workshops, and OEM service channels, where brand assurance and anti-counterfeit practices function as commercial differentiators. A reverse-logistics loop connects the in-use phase to collectors and re-refiners, guided by CONAMA Resolution 362/2005 and reinforced by Interministerial Ordinance MME/MMA No. 4/2023, which sets used-oil collection targets for 2024-2027; ANP also supports transparency through the Painel Dinamico do Mercado Brasileiro de Lubrificantes using SIMP declarations, which firms use to benchmark volumes and plan supply continuity.

Competitive Landscape

The Brazil Automotive Lubricants Market is moderately concentrated. Localization strategies intensify as import-cost swings encourage domestic blending. Counterfeit mitigation and channel digitization shape near-term competition. QR-coded tamper-evident labels and blockchain track-and-trace pilots aim to recover the BRL 30 billion lost annually to illicit product sales. Mid-tier blenders, nimble in agricultural or EV-fluid niches, exploit white space that majors overlook, thereby sustaining dynamism in the Brazilian automotive lubricants market.

Brazil Automotive Lubricants Industry Leaders

ICONIC

Shell Plc

TotalEnergies

Exxon Mobil Corporation

Petrobras

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization is a clear whitespace, backed by the shift to synthetic and semi-synthetic grades required for newer engines, after-treatment systems, and renewable-fuel operation (ethanol and higher biodiesel blends). ICONIC's reported positioning and gains highlight the opportunity, with the company stating a 27.9% market share as of October 2025 and an 8% volume gain in 2024, alongside expansion plans. Vibra has also introduced new Lubrax Top Auto formulations aligned with the latest API SQ/ILSAC GF-7 specification for hybrid applications. Together, these moves point to a structure where OEM-aligned approvals, high-performance claims, and trusted packaging widen the gap versus informal-channel products.

Supply-side substitution and circularity also open investable pockets. Brazil still relies on imports for a large share of base-oil needs (around 60%), and Petrobras has highlighted a pathway to higher-value Group II supply through its Boaventura complex upgrade program, which is intended to support local availability of modern base stocks for low-viscosity, extended-drain lubricants. On the circularity side, re-refined used-lubricant oil (OLUC) already has a measurable footprint (about 14% of the base-oil market), making re-refining capacity, collection partnerships, and ANP-compliant traceability practical levers for blenders and distributors aiming for cost stability alongside sustainability-aligned portfolios.

Recent Industry Developments

- June 2026: ICONIC announced a distribution partnership with DuPont to supply the MOLYKOTE line of specialty lubricants in Brazil. The arrangement expands ICONIC beyond mainstream automotive lubricants into higher-margin specialty applications. It also strengthens its service proposition for industrial and fleet customers that overlap with commercial-vehicle maintenance ecosystems.

- July 2025: Petrobras confirmed, within its 2025-2029 business plan, an investment to increase Group II lubricating base-oil production capacity by 12,000 barrels per day at the Boaventura Energy Complex. This supports a structural shift from legacy Group I supply toward higher-performance base stocks used in low-viscosity engine oils and modern ATF formulations. It improves domestic sourcing optionality for blenders.

- April 2024: Petrobras initiated the tender process for constructing a new lubricants plant at the Gaslub hub in Itaborai, Rio de Janeiro, targeting a move from Group I to Group II base-oil production. The project development step signaled a longer-term reconfiguration of Brazil's base-oil slate. It has implications for local formulation capability, import exposure, and product availability for OEM-specified grades.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers finished lubricants consumed in Brazil for on-road vehicles, where demand comes from factory fill and the aftermarket, and volumes are tracked across common automotive lubricant applications.

Scope exclusions: Industrial lubricants, marine lubricants, and aviation lubricants are excluded from this market sizing.

Segmentation Overview

- By Product Type

- Automotive Engine Oil

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- Monogrades

- Other Grades

- Manual Transmission Fluids (MTF)

- Automatic Transmission Fluids (ATF)

- Brake Fluids

- Automotive Greases

- Other Product Types (Power Steering Fluid etc.)

- Automotive Engine Oil

- By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping Brazil demand context to the in-use vehicle population, new registrations, and maintenance patterns that translate into lubricant consumption. For this, we referenced public sources such as Brazil traffic and vehicle registration statistics (to track fleet trends), national fuel and biofuel data from official energy statistics (to understand operating conditions), and emissions and engine-rule updates under PROCONVE publications.

We also used customs trade statistics, association and standards body publications (for example, SAE and API documentation for viscosity and service categories), and technical papers from peer-reviewed journals to understand drain intervals and how lubricant grades shift over time. Company filings, investor presentations, and reputable news were reviewed to cross-check channel shifts and product mix. A paid subscription for company financials and intelligence was used selectively to sanity-check scale for key suppliers active in the country. This desk source list is illustrative, and other public references were also used to collect data, validate assumptions, and clarify open questions during research.

Primary Interviews and Surveys

Primary work focused on confirming how lubricant demand splits between factory fill and the aftermarket, and how purchasing differs by passenger vehicles, commercial fleets, and two-wheelers. We spoke with a mix of lubricant producers, distributors, workshops, fleet maintenance teams, and industry specialists across Brazil. The interviews helped tighten assumptions on drain intervals, packaging mix, and the price spread between mineral, semi-synthetic, and synthetic products.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 55% |

Market-Sizing & Forecasting

Sizing was built from a top-down demand reconstruction where the vehicle parc, annual mileage, typical sump sizes, and average drain intervals are converted into lubricant consumption, and then adjusted for the factory-fill share versus the aftermarket share. To keep the totals realistic, we corroborated the output with selective bottom-up checks, such as sampled price per liter by product type and a reasonableness roll-up using a limited set of supplier and channel signals.

A few inputs that mattered most were the on-road fleet by vehicle type, the pace of new vehicle sales and scrappage, the shift toward lower-viscosity grades driven by newer engine requirements, and the penetration of synthetic and semi-synthetic products, which changes both volume and the implied value per liter. We also tracked indicators like the share of commercial vehicles in use (service frequency differs), workshop activity patterns in major corridors, and the extent of counterfeit-risk controls that can shift volume between formal and informal channels.

Forecasting used scenario analysis supported by simple time-series smoothing on key drivers. Base-case assumptions were checked and refined using expert views on fleet growth, maintenance behavior, and product mix. Where bottom-up price points were thin in certain sub-categories, gaps were handled by using conservative ranges from interviews, then testing the impact on the total before finalizing the model.

Data Validation & Update Cycle

Outputs were checked against independent signals, including whether implied liters per vehicle looked sensible by vehicle type and whether year-to-year movement matched observable shifts in the parc and service behavior. When large variances showed up, the assumptions were revisited, outliers were investigated, and follow-up calls were triggered to confirm what changed and why.

Before sign-off, the model goes through multi-step analyst review so calculation logic, units, and conversions are consistent across all tables. Reports are refreshed annually, and interim updates are done when material events occur, such as regulation changes, major supply disruptions, or sudden swings in demand indicators. Right before delivery, a final pass is done so clients receive the latest updated view available at that time.

Mordor Intelligence's Brazil Automotive Lubricants Market Estimate Compared With Other Published Estimates

Published market sizes for Brazil automotive lubricants can look far apart because not everyone uses the same unit of measure, scope boundary, or timing for prices and currency conversion. Differences also show up when studies mix automotive and non-automotive lubricants, or when they use broad revenue assumptions without tying them back to the vehicle parc and service behavior.

The table points to the biggest gap driver. The gap is that this study is anchored in volume for automotive applications, and then the value translation is kept separate to avoid overstating the market. In Mordor Intelligence's model, only finished automotive lubricants consumed in Brazil (across key product types used in passenger vehicles, commercial vehicles, and two-wheelers) are counted, while some published figures roll up wider finished lubricants or apply aggressive price uplift that is not verified through channel checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.00 B (2025) | |

| Trade Journal A | USD 3.90 B (2025) | Uses a broader lubricants definition with mixed end-use coverage, and reports revenue without clearly separating automotive demand from industrial consumption and re-exports. |

| Industry Brief B | USD 1.55 B (2025) | Back-solves value from a single average price per liter, and it does not show clear checks against vehicle parc, drain intervals, or factory-fill versus aftermarket split. |

Overall, the spread is mostly explained by scope choices and how price is applied to volume. By keeping the demand pool tied to vehicle parc, usage intensity, and service intervals, the final number stays traceable to inputs that can be reviewed and repeated during updates.

Key Questions Answered in the Report

How large will lubricant consumption be in Brazil by 2031?

The Brazil automotive lubricants market is projected to reach 1.29 Billion litres by 2031, reflecting a 3.89% CAGR from 2026.

Which lubricant category is growing the fastest?

Automatic transmission fluids will expand at a 3.45% CAGR between 2026 and 2031 on the back of rising automatic-gearbox adoption.

How will biodiesel mandates influence heavy-duty oils?

The shift from B15 to B20 biodiesel will require higher detergent levels and oxidation stability, encouraging fleets to adopt synthetic diesel engine oils.

Which region consumes the most lubricants?

The Southeast, led by São Paulo and Rio de Janeiro, accounts for about 39.60% of national lubricant demand thanks to dense vehicle fleets and manufacturing plants.

Page last updated on: