Bone And Joint Health Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

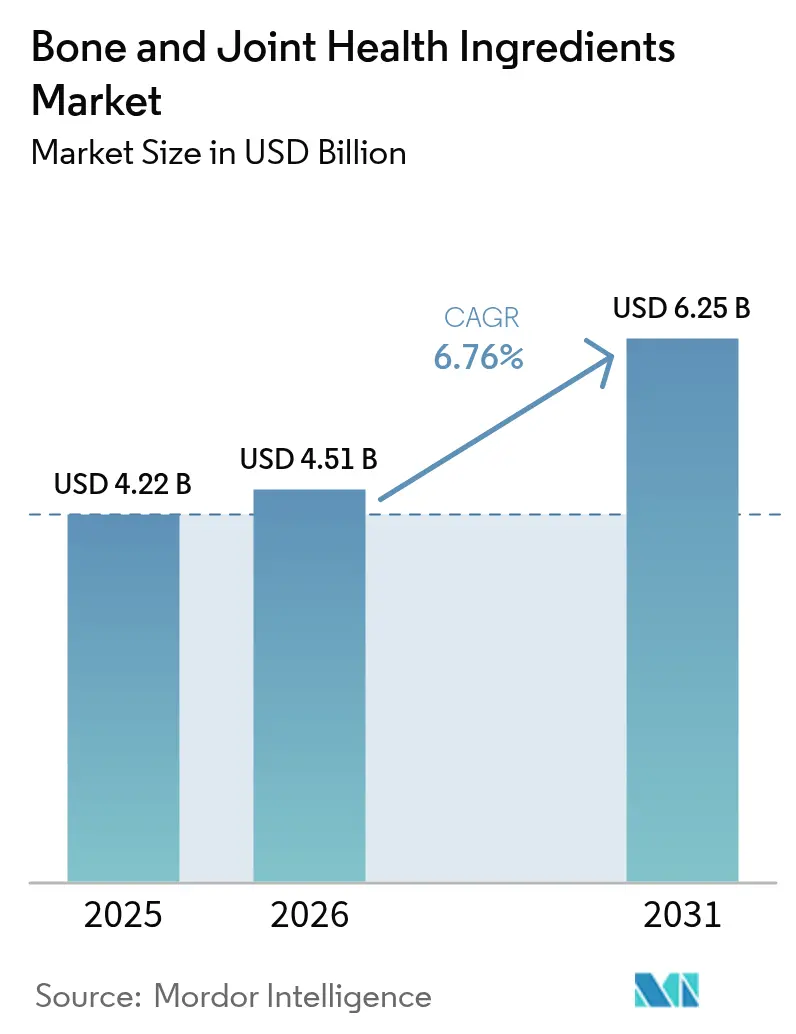

| Market Size (2026) | USD 4.51 Billion |

| Market Size (2031) | USD 6.25 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

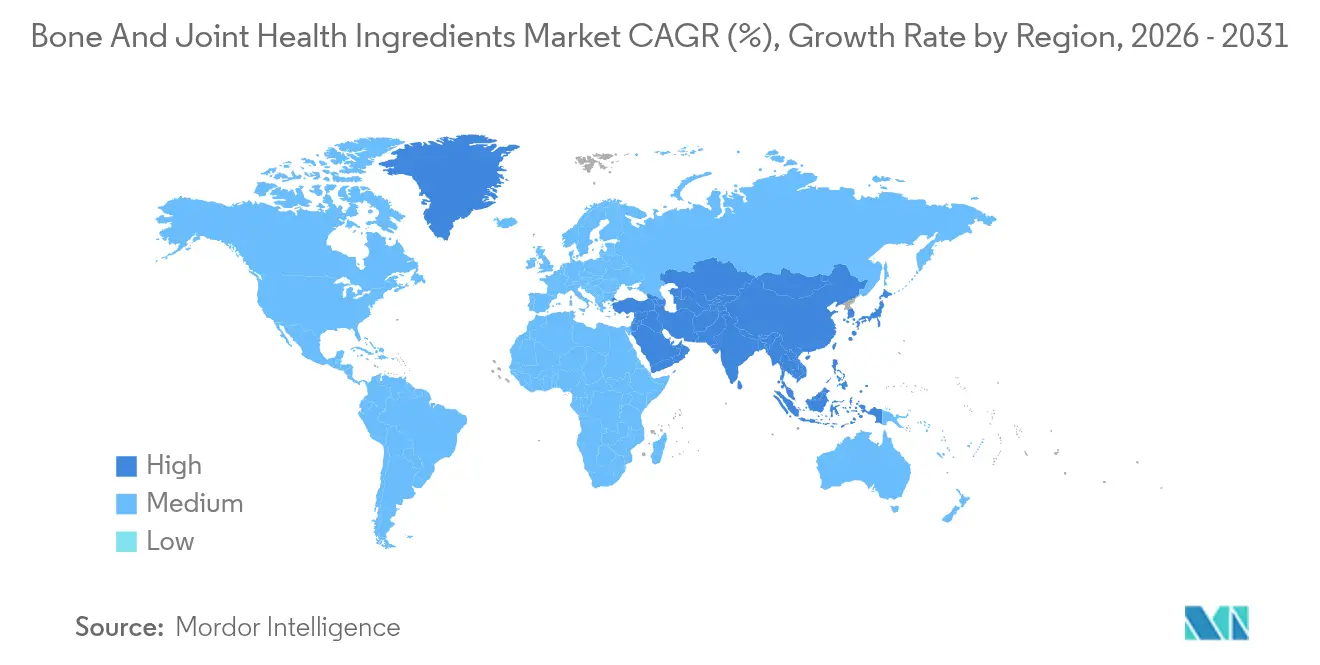

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

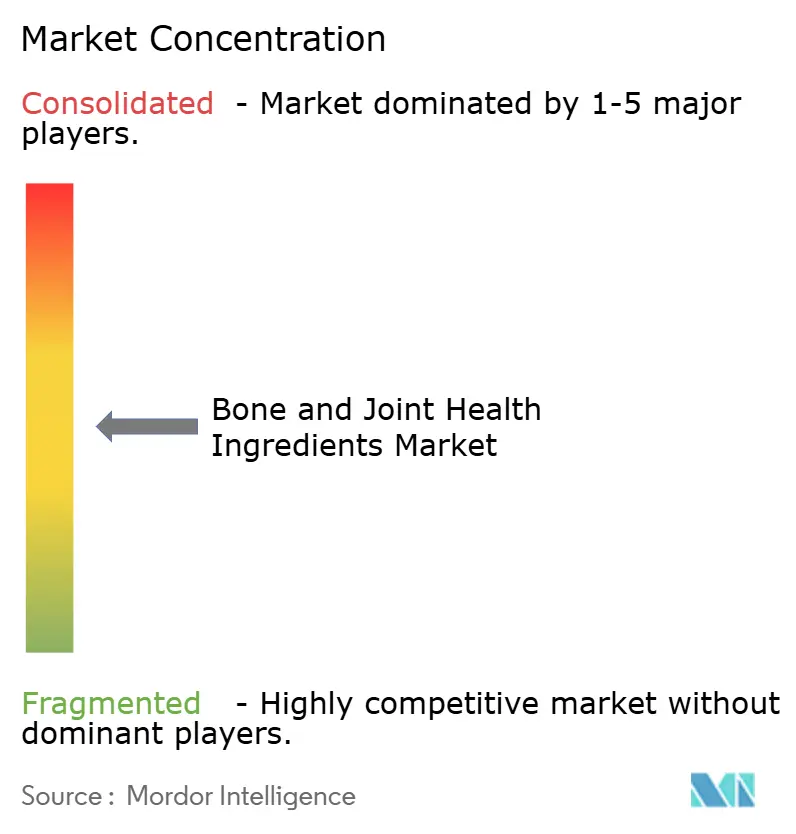

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bone And Joint Health Ingredients Market Analysis by Mordor Intelligence

Bone joint health ingredients market size in 2026 is estimated at USD 4.51 billion, growing from 2025 value of USD 4.22 billion with 2031 projections showing USD 6.25 billion, growing at 6.76% CAGR over 2026-2031. This growth trajectory reflects the convergence of demographic shifts, regulatory evolution, and technological innovation that positions joint health ingredients as critical components in preventive healthcare strategies. The market's expansion is fundamentally driven by the rising prevalence of osteoarthritis and osteoporosis, with scientific claims indicating that higher omega-3 intake reduces osteoporosis risk by ~30% among consumers. Regulatory frameworks across key markets are creating unprecedented opportunities for market expansion, particularly in Asia-Pacific, where China's State Administration of Market Regulation is drafting regulations to allow health foods to make joint health support claims, including benefits for alleviating joint pain and maintaining joint cartilage health.

Key Report Takeaways

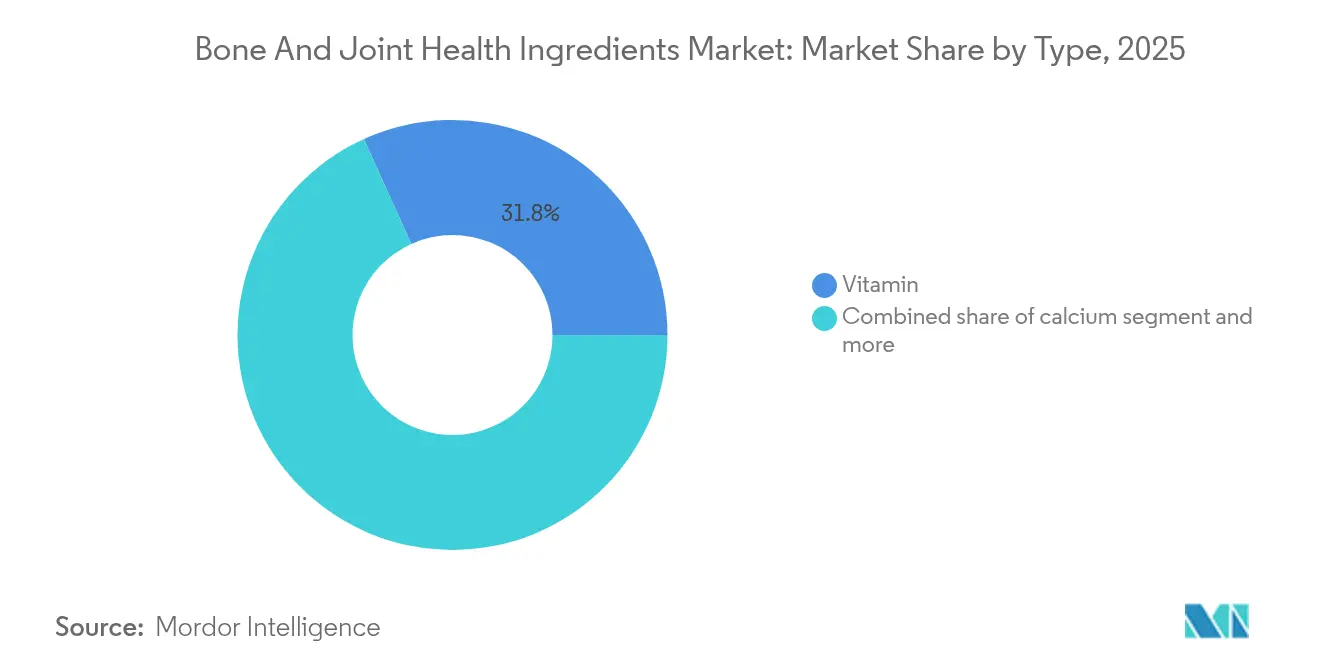

- By type, the vitamin category held 31.76% of the bone and joint health ingredients market share in 2025; calcium is forecast to expand at an 8.55% CAGR to 2031.

- By source, animal-derived ingredients captured 55.12% of the bone and joint health ingredients market share in 2025, while plant-derived alternatives are projected to grow at a 10.47% CAGR through 2031.

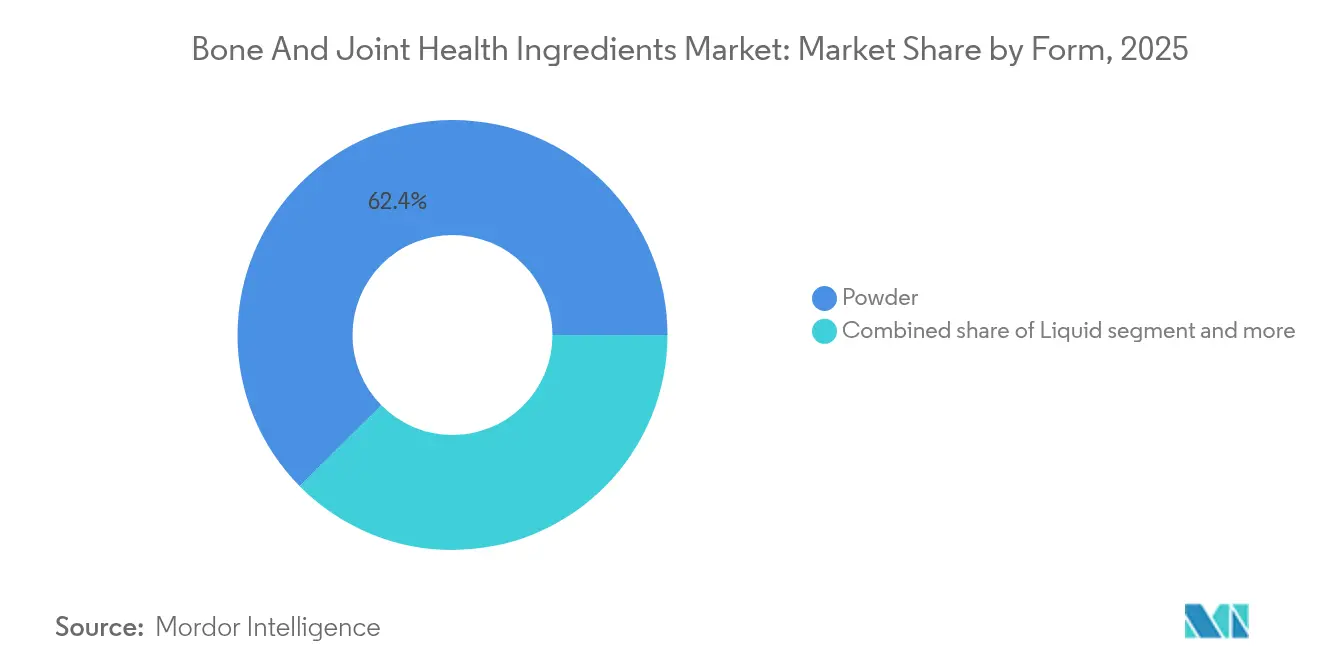

- By form, powder formulations commanded 62.42% of the bone and joint health ingredients market size in 2025 and are advancing at an 8.78% CAGR during 2026-2031.

- By application, dietary supplements accounted for 52.63% of the bone and joint health ingredients market size in 2025 and are set to record the fastest CAGR at 8.98% to 2031.

- By geography, North America led with 34.74% revenue share in 2025, whereas Asia-Pacific is the fastest expanding region at an 8.88% CAGR through the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bone And Joint Health Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoarthritis and osteoporosis | +1.8% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Growing consumer awareness of preventive joint health and self-medication | +1.2% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increasing demand from athletes and fitness professionals for joint-support | +0.9% | North America and Europe core, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Rising obesity rates increasing joint stress and osteoarthritis risk | +1.1% | Global, with pronounced impact in North America | Long term (≥ 4 years) |

| Growing demand for personalized joint health solutions | +0.7% | Asia-Pacific core, expanding to North America and Europe | Medium term (2-4 years) |

| Increasing integration of joint health ingredients in functional foods and | +0.8% | Global, with innovation leadership in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis and Osteoporosis

The rising prevalence of musculoskeletal disorders is changing healthcare priorities globally. Current projections indicate that a substantial portion of the global population will develop arthritis within the coming decades, highlighting a critical healthcare challenge. This trend affects not only the elderly but also younger populations due to lifestyle factors and work-related stress. The high molecular weight hyaluronic acid can restore trabecular bone parameters to normal levels by increasing osteoblast growth and reducing osteoclast activity through decreased RANKL expression. The treatment approach is shifting from symptom management to disease-modifying osteoarthritis drugs (DMOADs) that address cartilage deterioration and synovial inflammation. This change creates significant market opportunities for ingredients that can alter disease progression instead of providing temporary symptom relief. Market participants require comprehensive business intelligence to navigate this evolving landscape, identify emerging treatment patterns, assess competitive dynamics, and make informed investment decisions in response to changing therapeutic approaches and consumer demands.

Growing Consumer Awareness of Preventive Joint Health and Self-Medication

The COVID-19 pandemic has shifted consumer behavior toward preventive healthcare and proactive health management. The Asia-Pacific nutraceutical market expanded significantly, driven by increased consumption during the pandemic. Market growth stems from rising demand for scientifically validated formulations and clean-label products with transparent ingredient sourcing. Taiwan's Food and Drug Administration (FDA) updated its bone health functional claim regulations by eliminating animal testing requirements and establishing minimum participant requirements for bone quality studies. This regulatory change aligns with consumer demand for ethical and evidence-based products. Younger consumers, in particular, are adopting self-medication practices, emphasizing convenience and personalized health management solutions. These market dynamics present opportunities for businesses to develop targeted strategies and product innovations that meet evolving consumer preferences and regulatory requirements.

Increasing Demand from Athletes and Fitness Professionals for Joint-Support Products

The increasing focus on comprehensive athlete wellness has driven demand for specialized bone and joint health ingredients in the sports nutrition market. Companies are developing products that extend beyond muscle recovery to support sustained mobility and injury prevention. Bioiberica launched joint-supporting milk beverages in Spain containing Mobilee™, a patented combination of hyaluronic acid, polysaccharides, and collagen, targeting athletes with joint discomfort. Multiple clinical trials have claimed that daily consumption of Mobilee™ improves joint function and reduces pain, establishing its effectiveness as a functional ingredient in performance nutrition. The ingredient received European Food Safety Authority (EFSA) safety approval and Generally Recognized as Safe (GRAS) status for use in dairy products. Athletes require ingredients with high bioavailability and safety profiles, which influence product development and delivery methods. Professional sports teams prioritize joint health for competitive advantage, creating a market segment for evidence-based solutions. Market participants need comprehensive insights into consumer preferences, regulatory compliance requirements, competitive positioning strategies, and emerging technological innovations to make informed business decisions and maintain market competitiveness.

Rising Obesity Rates Increasing Joint Stress and Osteoarthritis Risk

Obesity places excessive stress on joints, creating a cycle where joint pain reduces physical activity, leading to further weight gain and joint damage. The relationship between obesity and osteoarthritis involves both mechanical stress and inflammatory processes, as fat tissue releases cytokines that damage cartilage and inflame joint tissue. Research continues into compounds that target inflammation and bone metabolism through dietary interventions, focusing on the connection between gut health and bone health. The market shows significant potential for ingredients that address weight management, inflammation, and joint health together, particularly as obesity medications gain broader acceptance in treatment protocols. Companies investing in this market segment benefit from understanding emerging treatment combinations, consumer preferences for natural solutions, and regulatory pathways for new product development. Market participants need comprehensive insights into patent landscapes, clinical trial outcomes, and competitive positioning to capitalize on opportunities in this expanding therapeutic area. The World Heart Federation estimates that 2.7 billion adults will be living with overweight or obesity by the end of 2025. The global prevalence of obesity continues to rise, making it one of the most significant public health challenges worldwide[1]Source: World Heart Federation, "Obesity is a Medical Condition," world-heart-federation.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of key raw materials | -0.8% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| High manufacturing costs impacting product pricing and accessibility | -0.6% | Global, with pronounced impact in emerging markets | Medium term (2-4 years) |

| Competition from conventional pharmaceutical products | -0.4% | North America and Europe, with regulatory preference variations | Long term (≥ 4 years) |

| Inconsistent regional regulations for health claims and product approvals | -0.5% | Global, with complexity in multi-market operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Key Raw Materials

Raw material cost fluctuations affect profit margins across the bone and joint health ingredients value chain, particularly in collagen and marine-derived compounds where supply chains face sustainability and scalability limitations. Marine collagen production continues to experience challenges in sensory characteristics and manufacturing costs, despite technological improvements in yield and quality optimization. These challenges include off-flavors, texture inconsistencies, and high processing expenses that impact final product quality and market competitiveness. The price volatility extends to plant-based alternatives, as agricultural commodity price variations directly influence ingredient costs, creating uncertain pricing conditions for manufacturers. Weather patterns, crop yields, and global demand fluctuations contribute to this market uncertainty. Supply chain disruptions have led companies to explore vertical integration and alternative sourcing strategies, though these solutions require significant capital investment and long-term planning. Integration efforts often involve establishing direct relationships with raw material suppliers, investing in processing facilities, and developing proprietary extraction technologies. In response, the market has developed synthetic alternatives and fermentation-based production methods to achieve better cost stability and supply reliability. These innovative approaches include laboratory-produced compounds and bioengineered solutions that reduce dependency on traditional raw material sources.

High Manufacturing Costs Impacting Product Pricing and Accessibility

The manufacturing of bone and joint health ingredients involves complex processes due to strict quality standards, specialized extraction methods, and regulatory compliance requirements. The Food and Drug Administration (FDA)'s Generally Recognized as Safe (GRAS) notification process for ingredients such as hydrolyzed porcine trachea cartilage (Peptan II) requires extensive safety documentation and testing [2]Source: U.S. Food & Drug Administration, “GRAS Notice GRN 1101: Hydrolyzed Porcine Trachea Cartilage,” fda.gov. While these regulatory requirements ensure product safety, they create significant entry barriers and compliance costs, particularly affecting smaller manufacturers. The implementation of advanced processing technologies, including microencapsulation and specialized delivery systems, increases production costs but enhances product bioavailability and consumer acceptance. This cost structure affects product accessibility, especially in price-sensitive developing markets where joint health needs are significant. The market dynamics necessitate comprehensive business intelligence to navigate regulatory complexities, optimize manufacturing processes, and identify cost-effective solutions for market expansion. Companies must analyze market trends, competitor strategies, and emerging technologies to maintain competitiveness and develop sustainable manufacturing approaches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Calcium Drives Innovation Despite Vitamin Dominance

The vitamin group anchored 31.76% of the bone and joint health ingredients market share in 2025, underpinned by broad clinical validation for vitamins D3, K2, and C in mineralization and collagen synthesis. Emerging formulation advances keep this portfolio relevant, yet calcium is racing ahead with an 8.55% CAGR on the back of chelation technologies and prebiotic co-administration systems that raise fractional absorption. Collagen maintains steady growth through marine-derived alternatives that offer superior bioavailability compared to mammalian sources, while glucosamine benefits from regulatory recognition in markets like China, where health products containing glucosamine have received approval for increasing bone density.

Magnesium demonstrates consistent performance through its established role in bone mineral density regulation and osteoblast/osteoclast activity modulation. Omega-3 segments are experiencing renewed interest following research demonstrating a 32% reduction in osteoporosis odds among the highest intake quartiles, driving innovation in specialized delivery systems that address oxidation challenges and improve bioavailability. Hyaluronic acid represents an emerging growth segment, supported by clinical evidence of its effectiveness in alleviating ovariectomy-induced bone loss through osteoblast proliferation promotion and osteoclast activity inhibition.

By Source: Plant-Derived Alternatives Challenge Animal Dominance

Plant-derived sources are rapidly gaining market traction at 10.47% CAGR through 2031, despite animal-derived ingredients maintaining 55.12% market share in 2025. This shift reflects consumer preferences for sustainable, allergen-free alternatives and regulatory support for plant-based innovations. Traditional Chinese medicine flavonoids are emerging as significant contributors to plant-derived growth, offering advantages including fewer side effects and cost-effectiveness for long-term use compared to conventional drugs.

Animal-derived sources maintain their dominance through established supply chains and proven efficacy profiles, particularly in collagen and chondroitin sulfate applications where molecular structure and bioactivity are well-characterized. The segment benefits from regulatory clarity, with established Generally Recognized as Safe (GRAS) notices for ingredients like hydrolyzed porcine trachea cartilage containing type II collagen and chondroitin sulfate. However, sustainability concerns and ethical considerations are driving innovation toward fermentation-based production methods that can replicate animal-derived compound structures while addressing supply chain vulnerabilities. Other sources, including synthetic and fermentation-derived alternatives, represent emerging opportunities for manufacturers seeking to balance efficacy, sustainability, and cost considerations in their product portfolios.

By Form: Powder Dominance Reflects Processing Innovation

Powders owned 62.42% of the bone and joint health ingredients market in 2025 and are still the fastest mover at an 8.78% CAGR. That paradox is made possible by process upgrades, spray-chilling, fluid-bed agglomeration, and lipid-layer microencapsulation that remove the gritty mouthfeel and fishy notes once associated with collagen or glucosamine. Commercial beverage lines now dispense shelf-stable, clear solutions that incorporate 10 g of protein per serving without cloudiness, a leap that migrates powder into ready-to-drink channels.

Liquid formulations maintain steady market presence through specialized applications in sports nutrition and clinical settings where rapid absorption and precise dosing are critical requirements. The segment benefits from innovations in emulsification technologies and stabilization systems that extend shelf life and improve palatability. Liquid forms particularly excel in pediatric and geriatric applications where swallowing difficulties make powder or solid alternatives less suitable. Other forms, including gummies, soft gels, and effervescent tablets, represent growing market segments driven by consumer convenience preferences and improved manufacturing technologies that maintain ingredient stability and bioactivity across diverse delivery mechanisms.

By Application: Dietary Supplements Retain Primacy, Functional Foods Accelerate

Dietary supplements maintain market leadership with 52.63% share in 2025 and demonstrate continued growth momentum at 8.98% CAGR through 2031, reflecting the segment's adaptability to evolving consumer preferences and regulatory frameworks. This growth is supported by increasing sophistication in formulation science, including combination products that address multiple aspects of bone and joint health through synergistic ingredient interactions. The segment benefits from established regulatory pathways and consumer acceptance, particularly in markets like the United States, where dietary supplement regulations provide clear guidelines for product development and marketing claims.

The increasing demand for functional foods and beverages that deliver specific health benefits has driven growth in bone and joint health ingredients, especially among consumers looking to maintain mobility and wellness. Innovations such as calcium-fortified drinks paired with chicory-root prebiotic fiber have demonstrated greater calcium uptake in humans. Brands are equally exploring clear-protein Ready to Drink (RTD)'s enriched with type II collagen to serve wellness-minded millennials who prefer nutrition “in the meal.” Cosmetics and topical patches form a small but strikingly innovative sub-segment that exploits transdermal channels to reach peri-articular tissues, a direction underpinned by micro-needle array technology transferring hyaluronic acid deeper than conventional creams.

Geography Analysis

North America maintains its position as the dominant regional market with a 34.74% share in 2025, driven by established healthcare infrastructure, regulatory clarity, and high consumer awareness of preventive health strategies. The region benefits from well-developed distribution channels and premium pricing acceptance for scientifically validated products. Regulatory frameworks in the United States provide clear pathways for ingredient approval, with established Generally Recognized as Safe (GRAS) notice procedures that enable market entry for novel compounds like olive leaf extract containing at least 50% polyphenols and 40% oleuropein. The region's growth is supported by increasing integration of joint health ingredients into functional foods and beverages, with manufacturers leveraging advanced processing technologies to address taste and stability challenges.

The Asia-Pacific market is expected to grow at a CAGR of 8.88% during 2026-2031, making it the fastest-growing region. This growth stems from increasing disposable incomes, urbanization, and health awareness, especially in China and India. The region's consumers are focusing more on preventive healthcare, increasing the demand for functional foods and supplements that support bone and joint health. Government programs supporting healthy aging and investments in food processing technologies enable manufacturers to develop products aligned with local preferences, supporting continued growth in the bone and joint health ingredients market.

Europe demonstrates steady market performance through stringent regulatory standards that ensure product quality and safety while creating barriers to entry for lower-quality alternatives. The European Food Safety Authority's rigorous health claim evaluation process, while challenging for manufacturers, ultimately supports premium market positioning for approved products. EFSA's scientific opinions on ingredients like collagen hydrolysate and glucosamine provide regulatory clarity that enables informed product development decisions. European manufacturers benefit from advanced processing technologies and established supply chains that enable efficient production and distribution across diverse national markets with varying regulatory requirements.

Competitive Landscape

The bone and joint health ingredients market is moderately fragmented, with the top five companies holding a significant share of the global market, while regional specialists and new companies focusing on fermentation technology maintain a competitive presence. The industry structure enables diverse market participation, ranging from established multinational nutrition companies to specialized biotechnology firms that develop innovative ingredients. This competitive landscape enables continuous product development and technological advancement in ingredient manufacturing processes, particularly in areas such as bioavailability and sustainable production methods.

Top incumbents, including DSM-Firmenich AG, BASF SE, Archer Daniels Midland Company, Glanbia plc, and Cargill Incorporated, among others, leverage ingredient breadth and regulatory infrastructure to secure multinational listings. DSM-Firmenich’s 2024 vitamin restructuring freed capital for yeast-fermented collagen trials, aiming to cut the cost of goods by 18% over traditional fish scaling. BASF applies lipid-matrix microencapsulation originally developed for carotenoids to joint-health actives, prolonging shelf life in tropical climates.

Strategically, acquisitions focus on platform technologies rather than commodity volume. Glanbia’s 2024 buyout of a micro-encapsulation specialist expanded its optionality across dairy, bar, and beverage formats. Partnerships are likewise sharpened: Lonza’s capsule division co-develops sustained-release beadlets with Kappa Bioscience’s vitamin K2, seeking a one-pill bone formulation valid across North American, EU, and ASEAN regulatory categories.

Bone And Joint Health Ingredients Industry Leaders

-

DSM-Firmenich AG

-

BASF SE

-

Archer-Daniels-Midland Company

-

Glanbia plc

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GC Rieber VivoMega introduced EPA and DHA Algae 1060 TG Premium, a concentrated algal omega-3 oil that delivers EPA and DHA in triglyceride form. The microalgae-sourced ingredient serves as a plant-based alternative to fish oil, meeting the increasing demand for vegan omega-3 options. The product supports nutraceutical applications for heart, brain, and joint health markets, featuring high purity standards, oxidative stability, and supply chain traceability.

- June 2024: Glanbia Nutritionals launched a high-potency collagen tripeptide ingredient that provides enhanced bioavailability and targeted benefits for skin, joint, and bone health. The ingredient uses advanced hydrolysis techniques to create a specific tripeptide profile, which improves absorption compared to standard collagen peptides. The company intends to incorporate the ingredient into powders, ready-to-drink beverages, and functional foods, meeting consumer demand for convenient health products.

- January 2024: DSM partnered with Azelis Pharmaceuticals and Healthcare to strengthen and expand Azelis Pharmaceuticals and Healthcare’s lateral value chain in India, with DSM’s complete range of vitamins for pharmaceutical solutions.

- October 2023: DSM-Firmenich announced the launch of Life's™ Omega 03020, a concentrated algal omega-3 ingredient that provides EPA and DHA from a single source. The product addresses increasing consumer demand for plant-based alternatives to fish oil while supporting cardiovascular, brain, eye, and joint health. The ingredient offers manufacturers a solution with traceability, proven bioavailability, and environmental sustainability benefits.

Global Bone And Joint Health Ingredients Market Report Scope

The bone and joint health ingredients market provides a range of health-oriented ingredients dedicated to dietary supplements, functional food and beverage, and other industries, such as pharmaceuticals. The product offerings of the market revolve around major ingredients, including Vitamin D, Vitamin K, Calcium, Collagen, Magnesium, Glucosamine, Omega-3, and Other Types. By Application, the market is segmented into Dietary Supplements, Functional Foods and Beverages, and Other Applications. By geography, the study covers North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasts have been done on the basis of the value (in USD million).

| Vitamin |

| Calcium |

| Collagen |

| Magnesium |

| Glucosamine |

| Omega-3 |

| Hyaluronic Acid |

| Others |

| Plant-derived |

| Animal-derived |

| Others |

| Powder |

| Liquid |

| Others |

| Dietary Supplements |

| Functional Food and Beverage |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Vitamin | |

| Calcium | ||

| Collagen | ||

| Magnesium | ||

| Glucosamine | ||

| Omega-3 | ||

| Hyaluronic Acid | ||

| Others | ||

| By Source | Plant-derived | |

| Animal-derived | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Others | ||

| By Application | Dietary Supplements | |

| Functional Food and Beverage | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current bone and joint health ingredients market size and how fast is it growing?

The market is valued at USD 4.51 billion in 2026 and is projected to reach USD 6.25 billion by 2031, expanding at a 6.76% CAGR.

Which ingredient category is growing the fastest?

Calcium-based innovations are rising at an 8.55% CAGR thanks to new bioavailability-enhancing technologies.

Why is Asia-Pacific the fastest-growing region?

Regulatory reforms in China and rising disposable incomes across emerging economies are fueling adoption, resulting in an 8.88% regional CAGR.

What form factor dominates sales today?

Powder formulations command 62.42% of 2025 revenue and still outpace other forms at an 8.78% CAGR due to processing advances that improve taste and solubility.

Page last updated on: