Blueberry Ingredient Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

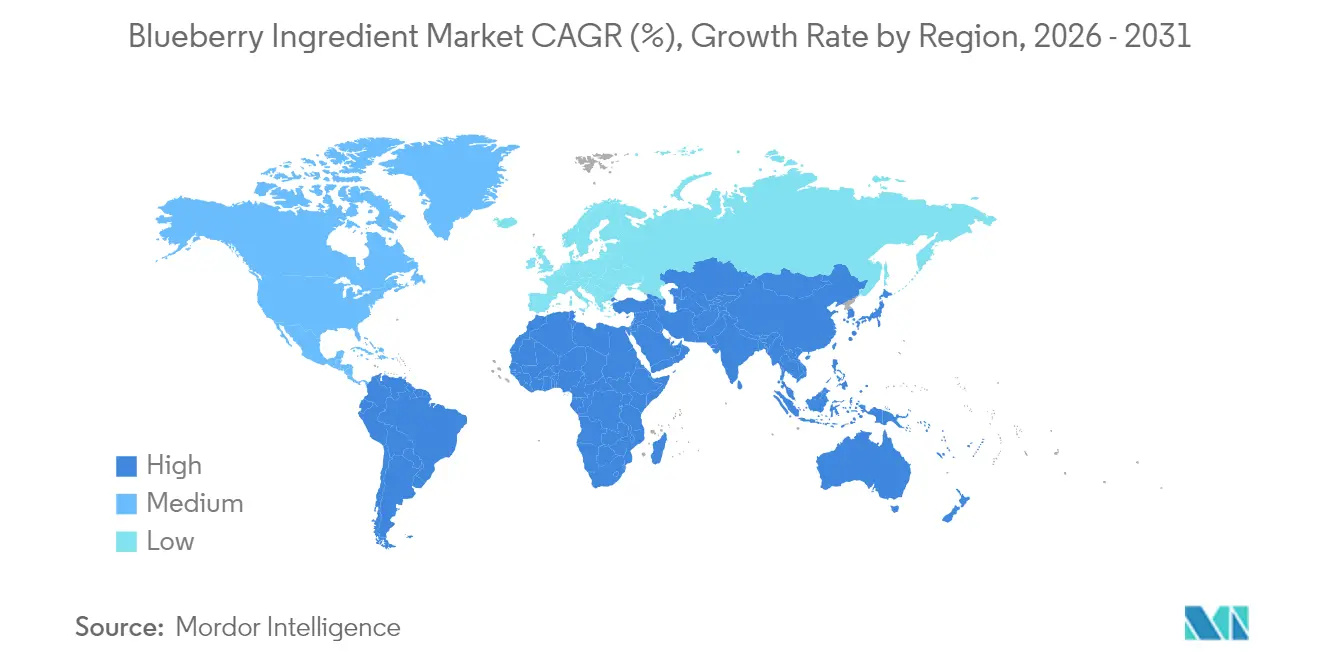

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

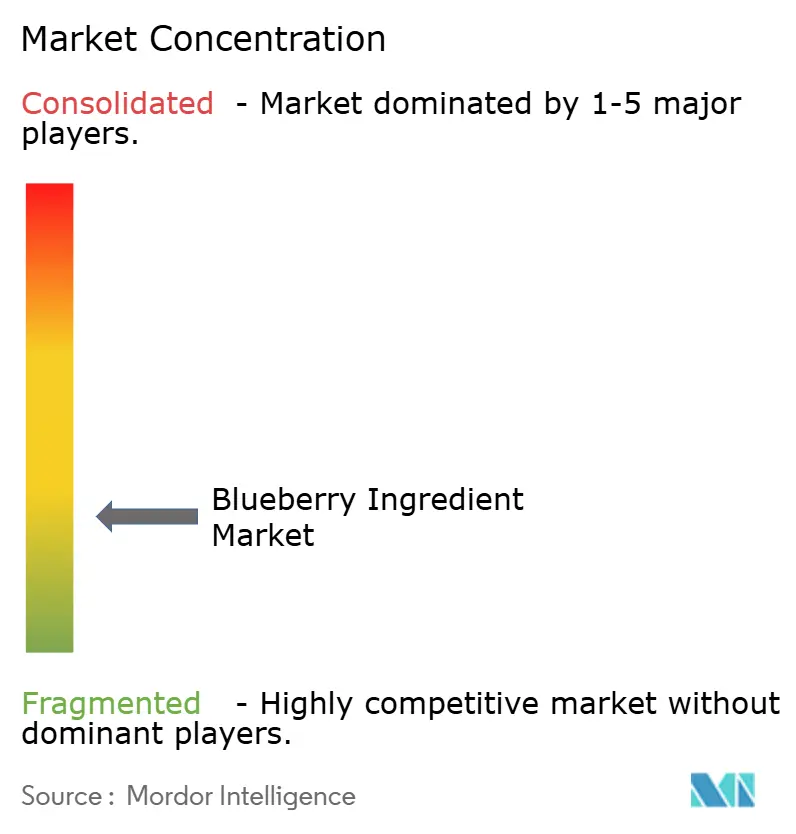

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Blueberry Ingredient Market Analysis by Mordor Intelligence

The Blueberry Ingredients market size was valued at USD 1.90 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 2.69 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031). Strong demand for standardized anthocyanin extracts, clean-label formulations, and functional products is steering the Blueberry Ingredients Market toward higher-margin formats such as powders and concentrates. Processors with spray-drying and encapsulation assets are benefiting from the shift, while frozen forms face slower growth as retail bakery channels mature. Regional supply imbalances continue to shape pricing: Peru’s export surge is compressing United States growers’ margins even as Asian demand accelerates. Competitive intensity remains low, yet the emergence of vertically integrated suppliers and investments in cold-chain infrastructure is starting to raise entry barriers.

Key Report Takeaways

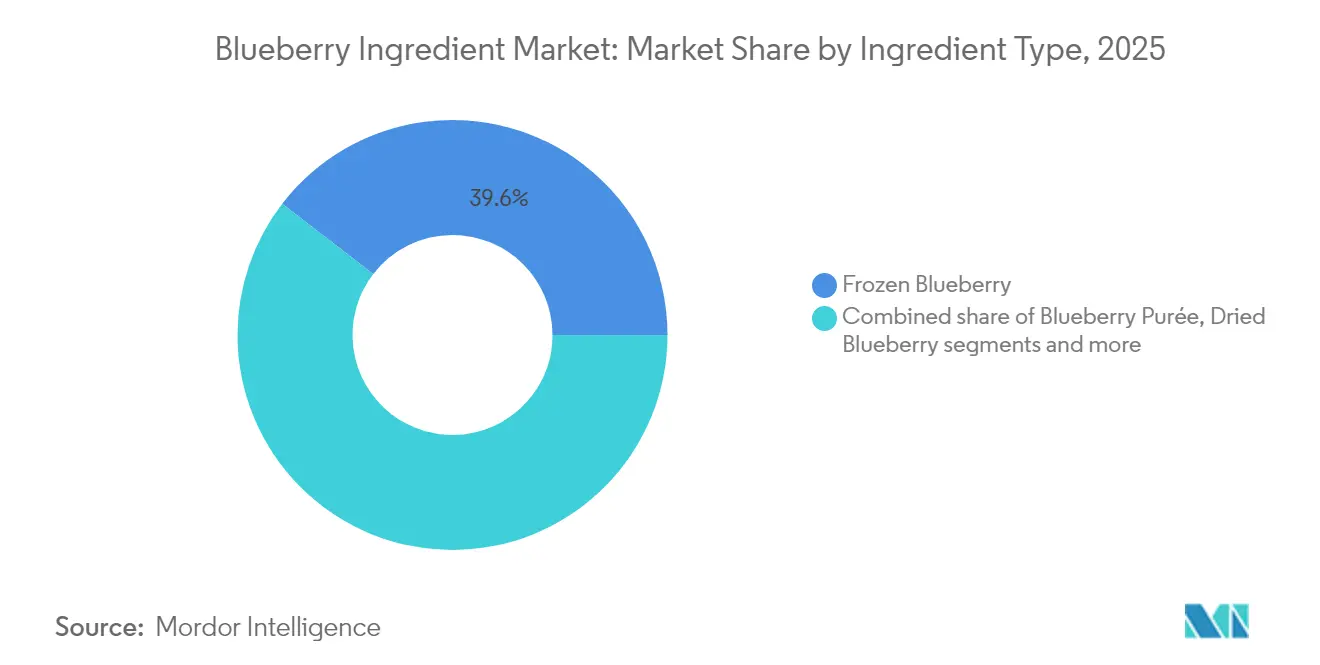

- By ingredient type, frozen blueberries led with 39.55% of the Blueberry Ingredients market share in 2025, whereas extracts and powders are advancing at a 6.82% CAGR through 2031.

- By application, food and beverage accounted for 58.10% of the Blueberry Ingredients Market in 2025; nutraceutical and dietary supplements are set to grow at 7.05% through 2031.

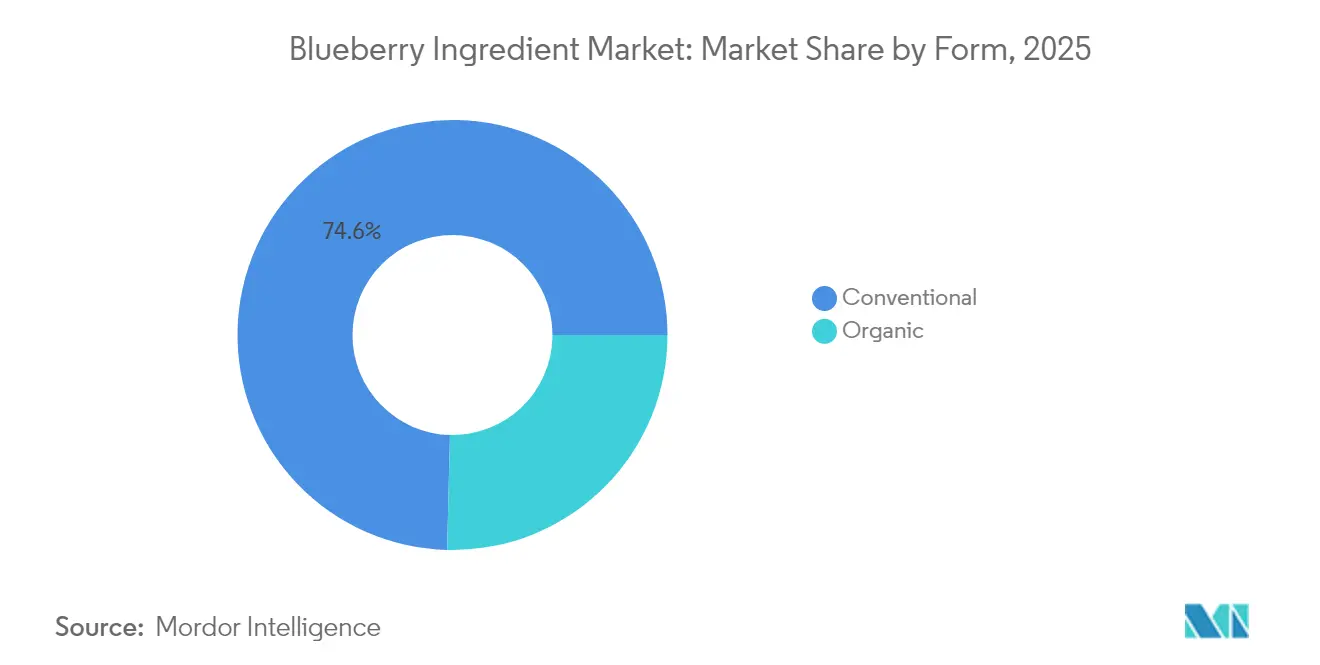

- By form, conventional products held 74.60% of 2025 revenue, while organic formats are forecast to expand at an 8.02% CAGR to 2031.

- By geography, North America generated 37.95% of 2025 revenue, yet Asia-Pacific is projected to rise at a 7.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blueberry Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of processed and convenience foods | +1.2% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising demand for functional foods and beverages | +1.5% | Global, led by North America, Europe, and Japan | Long term (≥ 4 years) |

| Consumer shift toward clean-label and natural additives amid health awareness | +1.1% | North America, Europe, with spillover to Australia and urban China | Medium term (2-4 years) |

| Increasing vegan and flexitarian diets drives plant-derived nutraceutical applications | +0.9% | Europe, North America, with emerging adoption in Southeast Asia | Long term (≥ 4 years) |

| Innovation in processing techniques enhances shelf life and versatility across forms | +0.8% | Global, with Research and Development hubs in North America and Europe | Long term (≥ 4 years) |

| Rising use in cosmetics for anti-aging properties from bioactive compounds | +0.6% | Asia-Pacific (Japan, South Korea), Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of processed and convenience foods

Rising demand for processed and convenience foods is accelerating the use of blueberry ingredients, including frozen, dried, purees, and powders, across various ready-to-eat products. These ingredients are integrated into items such as yogurt parfaits, energy bars, and smoothie packs, with frozen blueberries offering consistent freshness and nutrient retention, while dried variants cater to shelf-stable snack options. Expanding applications in bakery and confectionery further support this growth, as demonstrated by brands like Chobani, which use blueberry purees in Greek yogurts to deliver creamy textures for busy consumers, and KIND bars, which incorporate dried blueberries for convenient nutrition. The preference for natural and plant-based options is also driving demand, with blueberry juice concentrates enhancing flavor in bottled smoothies from brands like Innocent Drinks, appealing to health-conscious and vegan-friendly consumers. According to the Department for Environment, Food and Rural Affairs, average weekly per-person expenditure on food and drink in the United Kingdom reached GBP 47.19 for the financial year ending 2024, reflecting increased demand for convenient products such as Clif energy gels infused with blueberry extracts for functional benefits [1]Source: Department for Environment, Food and Rural Affairs, "Family Food FYE 2024", gov.uk . Advances in processing techniques are extending shelf life, enabling the use of blueberry extracts and powders in products like Quaker instant oatmeal, while clean-label trends promote the inclusion of organic blueberries in premium ready meals, addressing consumer demand for real-fruit convenience.

Rising demand for functional foods and beverages

Blueberry ingredients, including extracts and powders, are increasingly integrated into functional foods and beverages due to their clinically supported health benefits, such as antioxidant protection and immune support, aligning with the growing consumer preference for nutrient-dense options beyond basic nutrition. The shift toward natural, plant-based products is evident in the use of blueberry purees in smoothies from brands like Bolthouse Farms, which provide anti-inflammatory benefits while meeting clean-label demands with real-fruit formulations. Convenience snacks, such as protein bars like RXBAR featuring dried blueberries, enhance cognitive and heart health claims, reflecting the expansion of nutraceutical applications using blueberry powders for targeted wellness. In bakery products, blueberry juice concentrates are utilized in muffins to promote gut health through fiber content, catering to vegan diets with plant-based ingredients. Additionally, the rising demand for organic products has elevated the use of blueberry powders in functional beverages, aligning with clean-label trends and pharmaceutical formulations targeting specific health outcomes. A November 2023 survey by Korea Agro-Fisheries & Food Trade Corp. revealed that 84.5% of South Korean respondents consumed health functional foods, emphasizing the role of blueberries in immunity-focused ready-to-drink products [2]Source: Korea Agro-Fisheries & Food Trade Corporation, "2023 Health Functional Foods - Processed Food Segmentation Market Stats Report", atfis.or.kr . Advancements in cultivation techniques ensure consistent antioxidant potency across various forms, extending applications to cosmetics for anti-aging benefits and reinforcing their reliability in nutraceuticals, positioning blueberry ingredients as essential in meeting proactive wellness demands.

Increasing vegan and flexitarian diets drives plant-derived nutraceutical applications

The increasing adoption of vegan and flexitarian diets is driving the demand for plant-derived nutraceutical applications, with blueberry ingredients such as extracts and powders gaining prominence. Rising health consciousness is pushing consumers toward natural options, where the antioxidants in blueberries deliver clinically validated benefits in vegan supplements. This trend aligns with the growing popularity of convenience snacks, as seen in dried blueberries used in Larabar fruit bars, which provide portable, plant-based nutrition that supports immune health while meeting functional food demands. In the bakery sector, companies like LBP Bakeries are incorporating blueberry purees into Vegan Very Berry Muffin, enhancing fiber content for gut health and leveraging the organic trend for clean-label appeal. Blueberry powders are also being utilized in plant-based shakes by Orgain to address chronic disease reduction, with innovations in processing ensuring stable delivery for flexitarian diets. The rising preference for organic ingredients is boosting the use of blueberry extracts in vegan bone health formulas by Nutrabytes Advanced Vegan Collagen Supplement, which also finds applications in cosmetics for anti-aging benefits, reinforcing the reliability of nutraceuticals. A report by the Good Food Institute Europe indicates that by 2025, 51% of adults in the United Kingdom and Germany plan to increase plant-based consumption or reduce animal-based products, directly influencing the blueberry nutraceutical market [3]Source: Good Food Institute Europe (GFI Europe), "Research: Four in 10 German and UK Adults Plan to Eat More Plant-based Food", gfieurope.org . Advancements in cultivation techniques ensure bioactive consistency, supporting pharmaceutical formulations for targeted vegan wellness. These interconnected dynamics are positioning blueberry ingredients as essential components in plant-based nutraceuticals, addressing the evolving health goals of flexitarian consumers.

Rising use in cosmetics for anti-aging properties from bioactive compounds

The increasing application of blueberry ingredients in cosmetics highlights their growing importance due to their bioactive compounds, including anthocyanins, flavonoids, and vitamins, which effectively neutralize reactive oxygen species responsible for wrinkles and reduced skin elasticity. These antioxidants mitigate oxidative stress and inflammation in skin cells, supporting collagen integrity and enhancing the skin's barrier function, making blueberry extracts highly desirable in serums and creams targeting firming and wrinkle-smoothing benefits. Studies demonstrate that blueberry extracts improve skin smoothness, hydration, and elasticity, prompting formulators to use standardized extracts instead of simple fruit aromas to deliver measurable anti-aging results. Brands like Kajo Cosmetics have introduced products featuring berry-derived antioxidants, while niche players such as Natura Siberica emphasize blueberry extract in facial care to differentiate their "shielding" and "radiance" claims from conventional formulations. These developments reflect the broader functional positioning of blueberry ingredients across food, nutraceutical, and personal care sectors, leveraging the same polyphenol profile to address environmental stressors like UV exposure and pollution. Manufacturers are also adopting microencapsulation techniques to stabilize sensitive polyphenols, ensuring bioactivity over shelf life and aligning cosmetic innovation with practices in functional foods and dietary supplements. As clean-label and plant-based beauty trends gain momentum, blueberry extracts, oils, and powders offer a compelling "food-grade" narrative, fostering consumer trust in naturally derived anti-aging solutions and driving growth in high-value derma-cosmetic applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate blueberry production leads to supply shortages and sourcing challenges | -0.8% | Global, with acute pressure in North America and Europe during off-season months | Short term (≤ 2 years) |

| Perishable nature requires complex cold chain logistics, raising operational risks | -0.6% | Global, particularly impacting processors in regions with unreliable infrastructure (South America, Southeast Asia) | Medium term (2-4 years) |

| Competition from alternative berries dilutes market share in applications | -0.5% | Global, with pronounced impact in North America and Europe where açaí, aronia, and elderberry compete in functional foods | Medium term (2-4 years) |

| Stringent food safety regulations increase compliance burdens for processors | -0.4% | North America (FDA FSMA), Europe (EU Regulation 2073/2005), with spillover to export-oriented processors in South America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inadequate blueberry production leads to supply shortages and sourcing challenges

Inadequate blueberry production is causing significant supply shortages, impacting both fresh fruit availability and industrial ingredient streams such as purees, concentrates, and freeze-dried powders. Manufacturers are being forced to adjust sourcing strategies and reformulate products to address these challenges, as highlighted by the International Blueberry Organization. Reduced harvests in key producing regions are tightening raw material supplies for processors, driving up input costs and increasing the likelihood of rationing or reformulation for seasonal products like yoghurts, bakery inclusions, and functional powders, according to the Economic Research Service. With global output stabilizing at approximately 1.7–1.9 million tonnes in recent years, localized disruptions from weather, labor, or logistics issues are creating ripple effects across supply chains. In 2023, the United States experienced a production decline to around 648 million pounds, demonstrating how fluctuations in major origins can immediately reduce availability for both fresh and processed uses, as reported by the National Agricultural Statistics Service. Retailers and brands are also under pressure, with major supermarkets reporting limited shelf supplies during crop disruptions, while leading suppliers like Driscoll’s face challenges balancing contract obligations with spot-market procurement. Importers are grappling with compliance and traceability demands, navigating diverse phytosanitary regulations, freight bottlenecks, and rising cold-chain costs when shifting between hemispheres. For ingredient buyers, these pressures translate into longer lead times, fragmented supplier networks, and increased reliance on flexible formulations and multi-origin contracts, as noted by Blueberries Consulting. Rising ingredient prices are prompting manufacturers to explore blends, stabilizers, or alternative fruits to protect margins. Mitigation strategies, though costly, include long-term sourcing agreements, improved cold-chain logistics, and diversification into emerging export origins.

Competition from alternative berries dilutes market share in applications

Competition from alternative berries such as raspberries, blackberries, and cranberries is eroding the market share of blueberry ingredients across various applications, as businesses and consumers increasingly explore diverse flavor and nutritional profiles. Companies producing functional foods, beverages, and bakery products are substituting or blending blueberries with these alternatives to optimize cost, availability, and sensory appeal, as demonstrated by Driscoll’s product innovations. The growing demand for cranberry powders and raspberry purees in products like yoghurts, smoothies, and snack bars is reducing the reliance on blueberry concentrates and freeze-dried powders, as highlighted in market reports. Additionally, smaller health-focused brands are prioritizing berries with higher antioxidant claims, leading to shifts in sourcing strategies. This trend is intensifying pricing pressure on blueberry ingredients, as buyers compare the costs and nutritional benefits of multiple berry options. Seasonal and regional availability of alternative berries further enhances manufacturers’ flexibility, reducing the dominance of blueberries in formulations during supply constraints. To remain competitive, blueberry ingredient suppliers are focusing on innovation through blends, fortified powders, or exclusive sourcing agreements. The increasing presence of alternative berries is compelling global blueberry ingredient producers to differentiate their offerings strategically to sustain their market position.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Extracts and Powders Lead Innovation

Extracts and powders are driving innovation in the blueberry ingredients market, projected to grow at 6.82% annually from 2026 to 2031. Formulators are increasingly focusing on standardized bioactive content rather than bulk fruit fills. Frozen blueberries, which held a 39.55% market share in 2025, remain popular in retail bakery applications for their whole-fruit identity. However, extracts and powders offer greater flexibility, longer shelf life, and easier incorporation into functional foods, beverages, and dietary supplements. Dried blueberries, often used in snack mixes and cereals for their ambient stability, retain only 50–60% of their anthocyanin content due to heat exposure, making extracts and powders the preferred choice when nutritional potency is critical. Spray-dried powders are increasingly utilized to meet consumer demand for high-antioxidant content in clean-label applications, reinforcing the trend toward ingredient standardization and formulation precision.

Blueberry juice concentrate continues to be widely used in beverages but is constrained by its 12–15 Brix sugar content, which limits its suitability for low-calorie products. This has led to a shift toward water-soluble extracts that provide color and antioxidant benefits without adding calories. Spray-dried powders with 15–25% anthocyanin content now meet pharmaceutical-grade specifications, enabling their use in capsules and tablets. Companies such as FutureCeuticals and Martin Bauer Group are capitalizing on this trend, positioning extracts and powders as the fastest-growing ingredient type by combining nutritional efficacy, formulation versatility, and compliance with clinical validation standards.

By Application: Nutraceutical Segment Gains Clinical Traction

Food and beverage applications accounted for 58.10% of the market share in 2025. However, the nutraceutical and dietary supplement segments are expected to grow at a rate of 7.05% through 2031. This growth is supported by regulatory approvals that allow health claims on packaging, aligning with increasing consumer health awareness and the use of extracts and powders for antioxidant benefits in plant-based formulations. Pharmaceutical applications, while niche, offer high margins, with blueberry anthocyanins being studied for their potential in managing diabetic retinopathy and reducing cardiovascular risks. These developments connect with the nutraceutical segment through standardized powders that meet pharmaceutical-grade requirements. Cosmetics and personal care represent the fastest-growing application area, driven by the use of blueberry bioactives in anti-aging formulations that cater to the demand for clean-label products. Food and beverage applications continue to lead in volume, with examples such as blueberry purées in yogurt, freeze-dried pieces in granola, and juice concentrates in functional beverages. However, their slower growth reflects market maturity and rising competition from alternatives like açaí and aronia in sports nutrition, alongside the appeal of frozen products.

The nutraceutical segment benefits from the increasing demand for functional foods. Powders used in supplements provide clinical benefits beyond flavor, bridging the gap to pharmaceutical trials through consistent anthocyanin delivery, despite supply chain challenges. This trend is further supported by the shift toward plant-based diets, as plant-derived extracts in capsules enhance heart health claims. Similarly, cosmetics are incorporating these bioactives for skin protection, outpacing the growth of traditional food applications. Overall, regulatory support and bioactive standardization position nutraceuticals as a high-growth segment, expanding the use of blueberry ingredients across premium applications, even as traditional food applications face growing competition.

By Form: Organic Surges on Retailer Mandates

Organic blueberry ingredients are anticipated to grow at a compound annual growth rate of 8.02% from 2026 to 2031, outpacing conventional forms. This growth is driven by stricter pesticide-residue limits and clean-label initiatives from European retailers such as Aldi and United States brands like Whole Foods. These measures align with increasing consumer demand for natural, health-focused food and cosmetic products, where blueberries are valued for their antioxidant properties. In 2025, conventional blueberries held a 74.60% market share, supported by established supply chains and lower production costs. This dominance is evident in price-sensitive applications such as bakery products, private-label yogurt, and juice blends. However, concerns over synthetic fungicides and fertilizers are limiting growth in the conventional segment, creating opportunities for organic blueberries in premium categories like nutraceuticals and personal care.

Conventional blueberries maintain leadership in bulk fruit applications due to cost efficiencies, but the rising demand for organic products is compressing this market. Retailers are implementing stricter sourcing mandates, prompting processors to expand offerings of organic blueberry purees, powders, and extracts. Innovation trends further support this shift, with organic powders increasingly featured in functional beverages by brands such as Bai. The growing adoption of vegan and flexitarian diets, which favor certified organic products for their perceived health and environmental benefits, is also driving demand. The interplay between cost advantages of conventional supply chains and the rising preference for organic products underscores the evolving dynamics of the blueberry ingredients market.

Geography Analysis

North America accounted for 37.95% of 2025 revenue but faces moderate growth challenges due to domestic production limitations and increased reliance on imports. In Canada, blueberry production is concentrated in regions such as British Columbia and Quebec, supplying frozen ingredients to processors like Driscoll's. However, labor shortages are impacting harvest efficiency. Mexico's emerging blueberry industry primarily focuses on fresh exports to the United States, leaving limited volumes for domestic processing. This affects ingredient availability for nutraceutical and convenience food producers. The region's dependence on imports adds pressure to supply chains, particularly as demand for frozen, dried, and powdered blueberry forms continues to grow in the food and personal care industries.

Asia-Pacific is projected to grow at 7.46% from 2026 to 2031, driven by increasing domestic consumption in China and a well-established nutraceutical market in Japan, where blueberry extracts are gaining traction in functional foods and dietary supplements. India and Southeast Asia are developing markets with limited domestic production, relying on imported frozen fruit for premium yogurt and bakery products. Rising middle-class incomes and growing awareness of health trends are expected to accelerate demand for blueberry powders and purees in wellness and convenience food segments. This growth is likely to increase imports and drive supply chain developments in the region.

Europe remains a significant market, supported by production in Poland, Spain, and Germany, but continues to rely on imports from South America, particularly Peru and Chile. South America primarily serves as a raw material supplier, with Peru leading in production and exports but showing limited value-added processing capabilities. Meanwhile, the Middle East and Africa, with marginal market shares, depend on imports for premium segments. Emerging production in Morocco and South Africa could diversify supply sources post-2027, supporting growth in food, nutraceutical, and cosmetic applications.

Competitive Landscape

The blueberry ingredients market demonstrates a low concentration level, reflecting significant fragmentation among grower cooperatives, toll processors, and ingredient specialists. No single company holds a dominant global market share, enabling a diverse supply of extracts and powders. This structure supports the expanding nutraceutical segment, where companies standardize bioactive compounds to enhance clinical applications. The low concentration is also linked to the growing demand for organic products. Cooperatives supply conventional frozen blueberries for food applications, while toll processors convert limited harvests into stable dried forms to address production shortages. Fragmentation further drives innovation in cosmetics, particularly in anti-aging and vegan applications, as ingredient firms develop anthocyanin-rich powders that cooperatives often cannot customize efficiently.

Grower cooperatives dominate the supply of bulk purée and frozen blueberries for bakery applications, leveraging economies of scale to maintain their position in conventional products. However, climate variability has increased reliance on toll processors for extracts. Ingredient specialists focus on functional beverages, offering water-soluble concentrates that align with trends in convenience snacks and health-conscious products. These specialists also provide pharmaceutical-grade options, going beyond the bulk-focused offerings of cooperatives. The fragmented market structure sustains competition, as no single entity controls the entire supply chain, promoting partnerships for developing powders used in personal care products despite supply chain disruptions.

Fragmentation in the market drives adaptation in high-growth segments such as nutraceuticals. Companies produce flowable powders that address the limitations of frozen blueberries, particularly for vegan supplements. Toll processors bridge gaps in grower output, enabling flexible processing of organic blueberries to meet clean-label demands. Despite challenges such as volatile yields, this structure ensures a rapid response to surging demand for functional foods and clinical validations, positioning the market for sustained innovation and growth.

Blueberry Ingredient Industry Leaders

-

Südzucker AG

-

Döhler Group SE

-

Ingredion Incorporated

-

Symrise AG

-

R. J. Van Drunen & Sons, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Researchers from North Carolina State University, in collaboration with other institutes, reported findings on acyltransferase genes that regulated anthocyanin acylation in blueberries. The study identified two specific acyltransferase genes, VcBAHD-AT1 and VcBAHD-AT4, responsible for the acylation of anthocyanins in blueberries. These findings provided a molecular basis for enhancing the stability and health-related benefits of blueberry pigments.

- August 2025: The U.S. Highbush Blueberry Council (USHBC), in collaboration with VentureFuel, announced that four companies had been selected for the inaugural cohort of the Blueberry Boost Accelerator. The program focused on blueberry-based innovations, including extracts for gut health and snacks, aimed at advancing ingredient commercialization.

- October 2024: Fruit d'Or, a global producer specializing in the cultivation and processing of cranberries and wild blueberries, announced the launch of Blue d'Or™ Vitality at SupplySide West 2024. Attendees had the opportunity to explore this blend of wild blueberry and cranberry powders, formulated to leverage the combined antioxidant properties of these fruits. Targeted at the sports nutrition and nutraceutical industries, Blue d'Or Vitality represented a clean-label, organic option designed to support vitality and overall wellness.

Global Blueberry Ingredient Market Report Scope

| Frozen Blueberry |

| Dried Blueberry |

| Blueberry Juice Concentrate |

| Blueberry Purée |

| Extracts and Powders |

| Food and Beverage |

| Nutraceutical/Dietary Supplement |

| Pharmaceutical |

| Cosmetics and Personal Care |

| Conventional |

| Organic |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Frozen Blueberry | |

| Dried Blueberry | ||

| Blueberry Juice Concentrate | ||

| Blueberry Purée | ||

| Extracts and Powders | ||

| By Application | Food and Beverage | |

| Nutraceutical/Dietary Supplement | ||

| Pharmaceutical | ||

| Cosmetics and Personal Care | ||

| By Form | Conventional | |

| Organic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Blueberry Ingredients Market?

The Blueberry Ingredients market size is USD 2.01 billion in 2026 and is projected to climb to USD 2.69 billion by 2031.

Which ingredient type is growing fastest?

Extracts and powders are expanding at a 6.82% CAGR thanks to demand for standardized anthocyanin content.

Why are organic blueberry ingredients gaining traction?

European retailer residue limits and U.S. clean-label premiums are pushing organic formats to grow at an 8.02% CAGR.

Which region shows the highest growth potential?

Asia-Pacific leads with a 7.46% CAGR as China’s per-capita intake rises rapidly from a low base.

Page last updated on: