Black Start Generator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

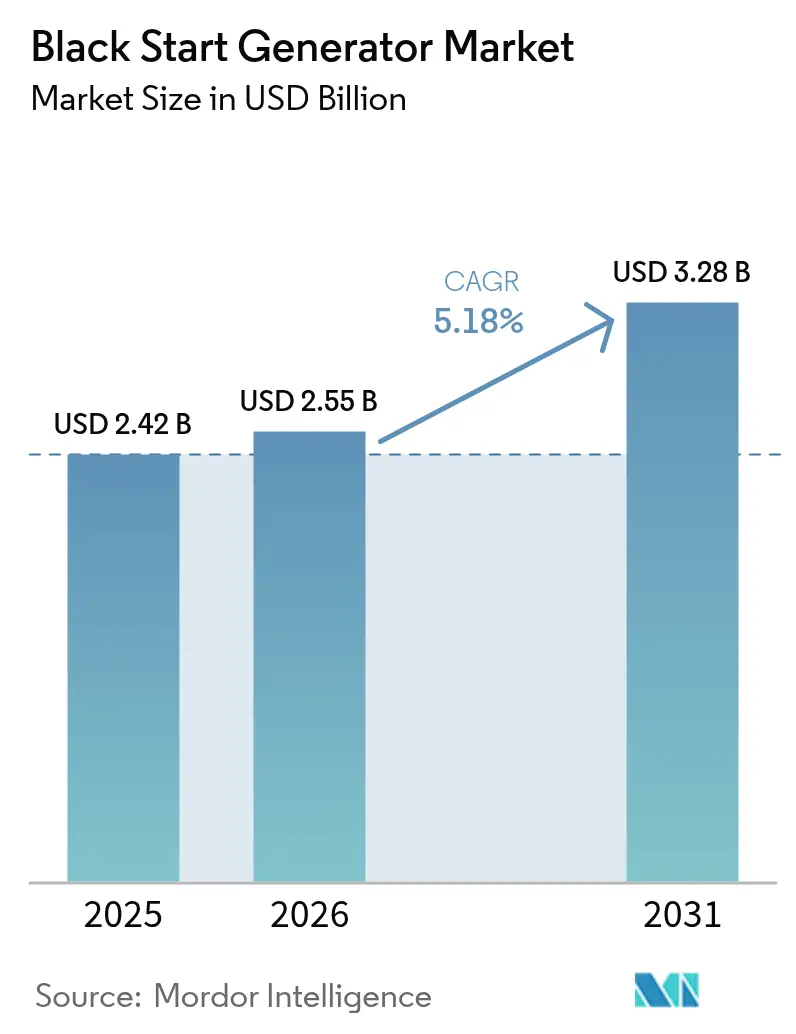

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.28 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

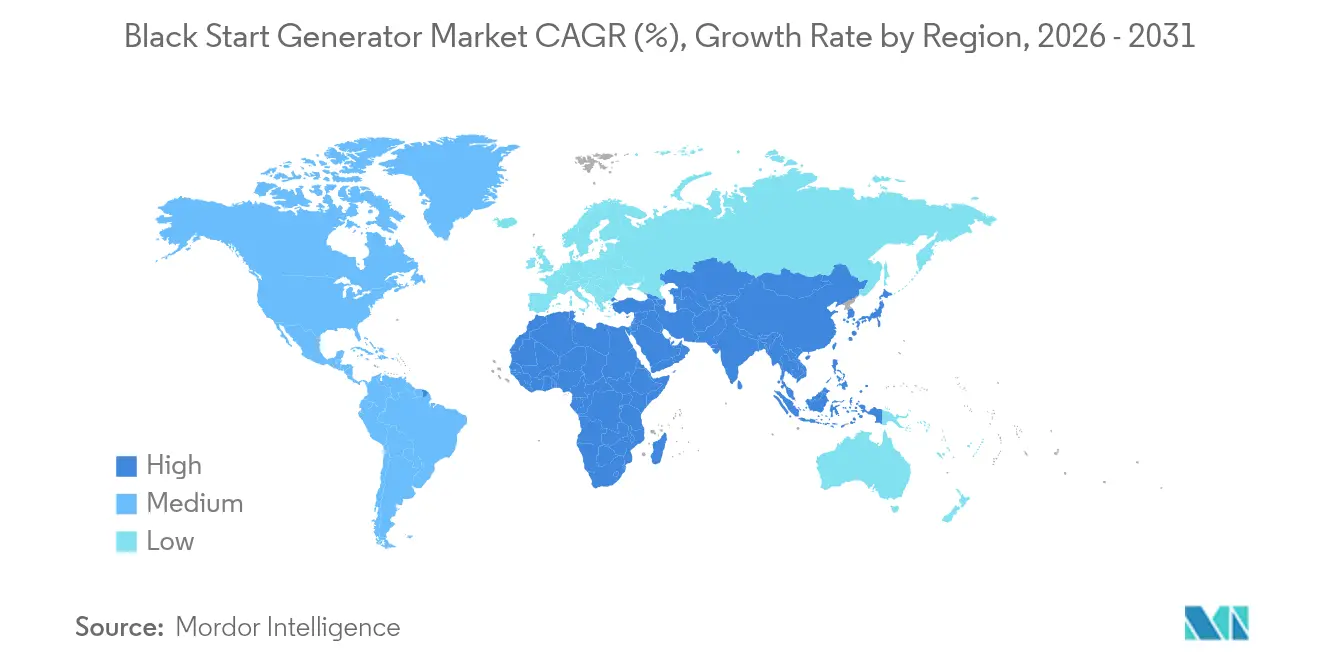

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Black Start Generator Market Analysis by Mordor Intelligence

Black Start Generator market size in 2026 is estimated at USD 2.55 billion, growing from 2025 value of USD 2.42 billion with 2031 projections showing USD 3.28 billion, growing at 5.18% CAGR over 2026-2031.

Grid-resilience mandates, the growing share of inverter-based renewables, and an increase in extreme weather events are driving demand for robust restoration assets across utilities, data centers, and industrial facilities. North America remains the largest regional cluster because NERC and FERC require operators to demonstrate reliable restart capability. In contrast, the Asia-Pacific region is expanding fastest as China and India modernize their grids and add renewable capacity. Hybrid battery-diesel systems are gaining traction as emission regulations tighten in major cities, yet diesel retains its leadership due to the simplicity of fuel handling and proven field performance. Meanwhile, the supply chain faces pressure from rare-earth metal bottlenecks that affect alternator production, although new designs employing ferrite magnets and silicon-carbide electronics are easing exposure. Competition is moderate, with Caterpillar, Cummins, GE Vernova, and Generac investing in digital controls and lower-carbon starter technologies to defend share against emerging storage-led solutions.

Key Report Takeaways

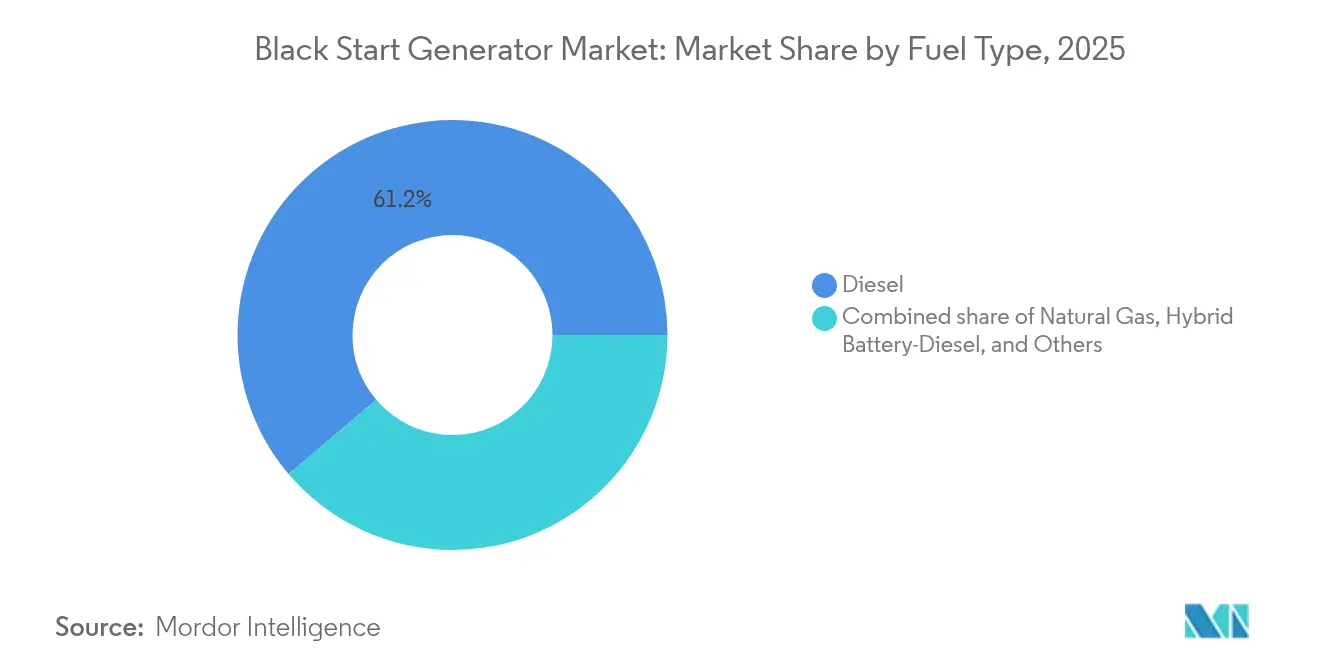

- By fuel type, diesel held 61.20% of the black start generator market share in 2025. Hybrid battery-diesel systems are projected to grow at a 8.95% CAGR through 2031.

- By power rating, units with a capacity of up to 1 MW commanded a 52.80% share of the black start generator market size in 2025. Sets rated 1-5 MW are expected to expand at an 8.12% CAGR between 2026 and 2031.

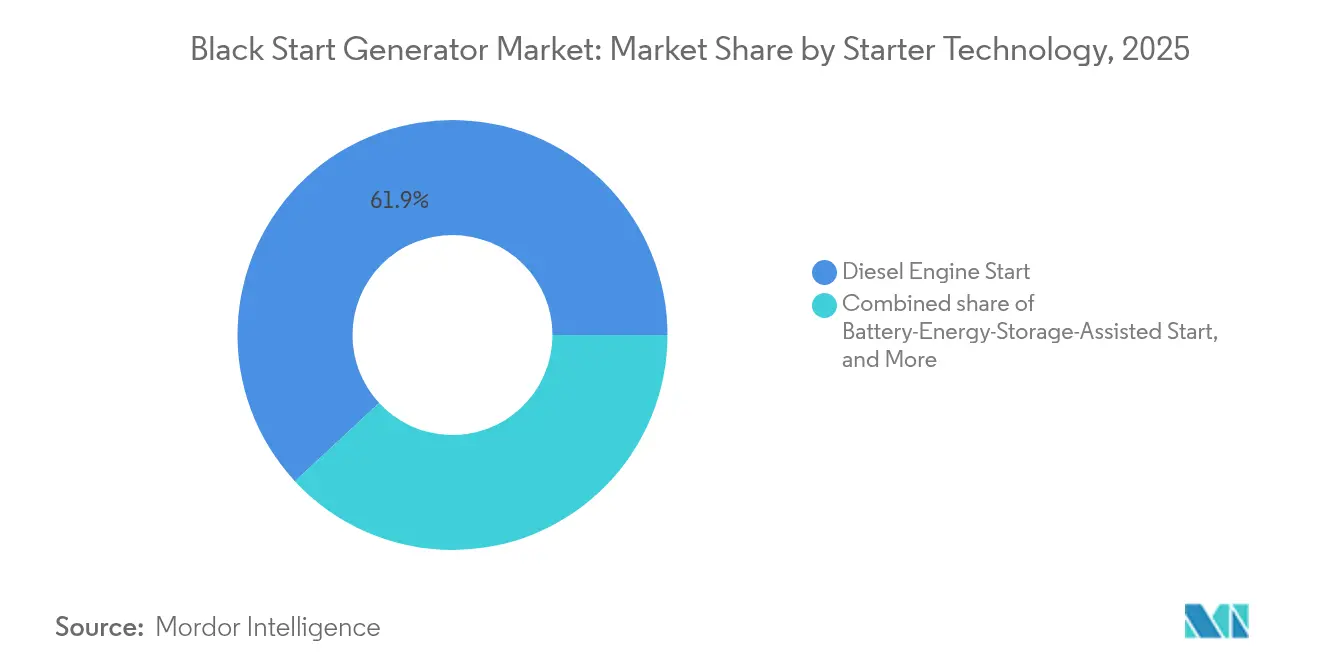

- By starter technology, diesel-engine start units accounted for a 61.90% share in 2025, while battery-assisted start systems led growth at a 12.05% CAGR.

- By end-user, utilities and transmission operators captured a 47.10% share in 2025; data centers are advancing at a 10.02% CAGR.

- By geography, North America led with a 37.70% share in 2025, while the Asia-Pacific region is expected to show the fastest growth at 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Black Start Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-disturbance frequency & blackout mandates | +1.20% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Grid-code compliance for renewables | +0.90% | Asia-Pacific, Europe, global | Long term (≥ 4 years) |

| Aging-infrastructure modernization | +0.80% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of mission-critical data centers | +1.10% | North America, Asia-Pacific, global | Short term (≤ 2 years) |

| Offshore-wind HVDC platforms | +0.40% | Europe, Asia-Pacific coastal regions | Long term (≥ 4 years) |

| Hybrid battery-diesel adoption | +0.70% | North America, Europe urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Disturbance Frequency & Blackout Resilience Mandates

Unplanned outages totalled 1.5 billion customer-hours in the United States during 2024, prompting federal rules that oblige transmission operators to restore service within three hours and sustain operation for at least 16 hours without external support.(1)Federal Energy Regulatory Commission, “Winter Storm Elliott Recommendations,” ferc.govUtilities are therefore investing in dual-fuel and hybrid systems that guarantee fuel availability during prolonged events, a trend mirrored across Europe, where TSOs built new restoration zones after recent gas-price shocks. Suppliers that demonstrate rapid-start verification and extended run-time certification are winning multi-year framework contracts. Insurance carriers now require proof of black start capability at large industrial sites before underwriting business-interruption policies, accelerating private-sector procurement. As a result, the black start generator market is witnessing a steady replacement of legacy fleets with Tier 4-compliant or hybrid units.

Grid-Code Compliance for Renewable Integration

FERC Order 901 establishes performance-based ride-through and monitoring standards for inverter-based resources by 2030, shifting restoration procedures toward grid-forming controls.(2)North American Electric Reliability Corporation, “Standards for Inverter-Based Resources,” nerc.com Demonstrations in the North Sea proved that offshore wind farms can deliver independent voltage and frequency support during restart sequences using advanced converters.(3)DNV, “Offshore Wind Grid-Forming Controls,” dnv.com European projects such as Carbon Trust’s BLADE aim to commercialize these findings by 2027, potentially reducing diesel run-time during coastal blackouts. However, intermittency still necessitates hybrid arrangements that combine storage with synchronous inertia to stabilize frequency fluctuations. Generator OEMs now bundle digital coordinators that manage dispatch between diesel sets, batteries, and renewable feeders during restoration, improving restart certainty and emission performance.

Expansion of Mission-Critical Data-Centre Footprint

Global data-centre power demand is predicted to exceed 50 GW of additional capacity by 2030, with Tier IV facilities increasingly adopting “bring-your-own-power” strategies that include full black start capability. NFPA 110 Type 10 rules stipulate a 10-second start and long-duration autonomy, driving orders for fast-cranking diesel sets teamed with lithium-iron-phosphate batteries for ride-through. Major hyperscalers are sourcing dedicated gas turbines adjacent to their server farms, while oil-and-gas majors, such as ExxonMobil, are building on-site plants that operate off-grid. Generator vendors now integrate cellular remote diagnostics, enabling operators to continuously validate restart readiness. This segment outpaces traditional utility spending because downtime equates to significant data loss penalties, reinforcing the need for premium-priced service contracts.

Aging Infrastructure Modernization Programs

The State Grid Corporation of China budgeted USD 83 billion for transmission upgrades in 2024, earmarking a share for black-start-ready substation converters that can draw power from adjacent healthy zones.(4)State Grid Corporation of China, “2024 Transmission Investment Plan,” sgcc.com.cn In the United States, the Infrastructure Investment and Jobs Act allocates funds for synchronous condensers and fast-start engines that support microgrids and rural feeders. Projects such as Hitachi’s Higashi-Shimizu VSC installation, due in 2027, illustrate the deployment of frequency converters capable of sections’ autonomous restart. Modernization programs also replace vintage diesel day tanks with double-containment systems and introduce cyber-secure PLCs that withstand remote-command attacks, increasing project scope and average order value. These upgrades extend equipment life while meeting stricter reliability metrics set by regulators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter diesel-emission legislation | -0.80% | North America, Europe | Short term (≤ 2 years) |

| Inverter-based black-start alternatives | -0.60% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Rare-earth alternator bottlenecks | -0.40% | Global | Short term (≤ 2 years) |

| Cyber-security compliance costs | -0.30% | Global critical facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Diesel-Emission Legislation

California’s Air Resources Board is preparing Tier 5 off-road standards that phase in between 2029 and 2034, requiring further reductions in NOx and particulate matter from standby engines. The EPA Tier 4 Final framework already requires a 94% reduction in particulates compared to Tier 1, adding after-treatment complexity and cost. While emergency-only units still qualify for limited exemptions, many utilities operate beyond the 50-hour maintenance ceiling, triggering non-attainment penalties. Similar Stage V rules in the European Union require diesel particulate filters across mobile generator fleets, which raises capital expenditures and prompts a shift toward gas or hybrid systems in urban deployments. Consequently, project sponsors increasingly favor battery-assisted starts or gas microturbines for downtown installations.

Emerging Inverter-Based Black-Start Alternatives

GE Vernova demonstrated a 7.4 MW battery that successfully restarted a combined-cycle plant at Entergy’s Perryville station, eliminating the need for diesel fuel during the sequence. Grid-forming battery containers now supply full active and reactive power for up to four hours, matching the time needed for main blocks to synchronize. In addition, advanced nuclear small-modular reactors advertise inherent black start capability through passive cooling systems, which allow for cold restarts without external electricity. Although these technologies remain niche, their success prompts generator OEMs to bundle storage as a standard feature. Over time, displacement risk could erode diesel volumes, particularly in regions with stringent carbon reduction targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Dominance Faces Hybrid Challenge

The diesel category accounted for 61.20% of the black start generator market share in 2025, as utilities value energy density and established supply chains for emergency stockpiling. Hybrid battery-diesel technology, however, is forecast to grow at 8.95% CAGR, supported by urban low-emission zones that reward reduced idling. This transition maintains the overall health of the black start generator market by introducing premium hybrid skids while retaining diesel anchors for long-duration coverage.

Natural gas occupies the second slot, benefiting from pipeline access at large plants yet exposed to supply cuts during cold snaps. Alternatives, such as hydrotreated vegetable oil and biodiesel, receive pilot funding in Europe, but their volumes remain small. The fuel-type split underscores operators’ preference for redundancy; many new packages are engineered with dual-fuel injectors that switch between gas and diesel within seconds and synchronize seamlessly with battery modules.

By Power Rating: Small Units Lead, Mid-Range Accelerates

Units up to 1 MW contributed 52.80% of the black start generator market size in 2025 because commercial buildings, hospitals, and distributed renewables require localized restart assets. Demand in the 1-5 MW range is rising fastest, at an 8.12% CAGR, as data-center clusters and industrial parks consolidate multiple feeders into campus-wide microgrids.

Customers prefer mid-range sets that strike a balance between footprint, cost, and step-load performance. Above 5 MW machines remain specialized for petrochemical complexes and large utility substations; although fewer in number, they command high margins because of bespoke engineering. The shift toward modular packages enables integrators to parallel smaller units to reach a 10 MW class without the installation complexity of a single-frame engine.

By Starter Technology: Battery-Assisted Systems Disrupt Tradition

Diesel-engine cranking technology held a 61.90% share of the black start generator market in 2025, reflecting decades of reliability. Battery-energy-storage-assisted start systems are expected to register a 12.05% CAGR, fueled by successful commercial deployments that trim startup emissions and accelerate breaker closure times.

OEMs are embedding super-capacitors and lithium-ion racks within generator enclosures, allowing engines to reach nominal speed faster and smoothing voltage dips during synchronization. Gas-turbine start remains relevant for large combined-cycle blocks, while compressed-air systems offer mechanical independence when electrical auxiliaries fail. The technological mix is widening, yet control architectures are converging on digital PLCs that autonomously select the optimal starter path based on ambient conditions and fuel availability.

By End-User Industry: Utilities Lead, Data Centers Surge

Utilities and transmission operators represented 47.10% of the black start generator market share in 2025 because NERC rules obligate grid owners to maintain restart assets across every interconnection. Data centers are set to post a 10.02% CAGR through 2031 as hyperscalers scale AI workloads that cannot tolerate power loss.

Oil-and-gas facilities rely on black start capability to prevent flaring and maintain pipeline integrity during grid trips, while manufacturing plants seek protection for high-value process lines. Commercial and institutional sites, from airports to government campuses, are increasingly specifying hybrid packages to meet Scope 3 carbon pledges without sacrificing security of supply.

Geography Analysis

North America led the black start generator market with 37.70% share in 2025, buoyed by the United States’ resilience investments after Winter Storm Uri and federal funding that rewards grid-hardening projects. Utilities in Texas alone tapped USD 1.8 billion in grants to finance microgrids and fast-start engines for retail chains and critical services. Canada enforces provincial restart plans for hydro-dominated grids, while Mexico’s manufacturing corridor adds capacity to secure export supply chains.

Europe ranked second, shaped by Stage V emission rules that accelerate hybrid adoption and by offshore wind pilots that test turbine-based black start scenarios. Germany maintains 174 designated restart plants, yet contracts only 26 of them commercially, indicating scope for market reshaping through auctions. The Nordic region is advancing synchronous condensers linked to hydropower, whereas Central and Eastern member states leverage EU funds to retrofit diesel fleets with SCR kits.

The Asia-Pacific is the fastest-growing hub, with an 8.55% CAGR, spearheaded by China’s USD 83 billion grid-upgrade plan and India’s pumped-storage ramp-up, which enhances restart coverage. Japan upgrades aging thermal plants with dual-fuel engines, and South Korea invests in LNG-to-power terminals equipped with auxiliary generators. Emerging ASEAN economies are deploying containerized 1 MW sets at industrial parks to support rapid electrification and prevent productivity losses during monsoon-induced power outages.

Regulatory Landscape

In North America, black start readiness is governed by mandatory reliability requirements under the North American Electric Reliability Corporation (NERC), including EOP-005-3. These requirements drive formal restoration plans, documented procedures, and periodic capability validation for designated blackstart resources. Federal Energy Regulatory Commission (FERC) oversight and ISO/RTO rules translate these requirements into procurement and testing programs, with system operators such as CAISO, ERCOT, and ISO New England using technical specifications and operating procedures to qualify resources, define cranking paths and performance criteria, and enforce testing intervals (including unannounced demonstrations in some programs).

In Europe, the ENTSO-E Network Code on Requirements for Generators (RfG) provides a common framework that Transmission System Operators implement locally, with black start obligations and verification embedded into national grid codes and ancillary service arrangements. In Australia, the Australian Energy Market Commission (AEMC) issued an updated System Restart Standard in December 2025, effective 1 July 2027, adding specificity around restart services and strengthening the compliance perimeter for providers participating through AEMO procurement. Together, these frameworks push suppliers toward documented testability, cyber-secure controls for remote start, and packages that can demonstrate voltage and frequency regulation under islanded conditions.

Competitive Landscape

The black start generator market is moderately fragmented. Caterpillar, Cummins, GE Vernova, and Generac collectively account for less than half of global value, leaving room for regional specialists and storage entrants. Generac commands 80.38% share within its fabricated-products subsegment but only 2.01% overall, reflecting heavy concentration in residential backup. Cummins posted 24% year-on-year revenue growth in power solutions in Q3 2024, buoyed by data-centre demand, yet its total market share remains near 4.4%

Strategic acquisitions underscore consolidation. DEUTZ purchased U.S. set assembler Blue Star Power Systems in June 2024 to enhance its turnkey capabilities. Blackstone took control of Trystar in August 2024, signalling private-equity appetite for backup infrastructure. Meanwhile, Mainspring Energy secured USD 258 million to accelerate the roll-out of linear generators, which promise fuel flexibility and ultra-low NOx emissions.

Technology partnerships multiply. GE Vernova and Duke Energy agreed to deploy up to 11 domestically manufactured gas turbines in April 2025, thereby expanding the Greenville factory's capacity by 1,500 jobs. OEMs also integrate digital twins that predict starter battery health and forecast fuel aging, reducing unplanned failures. As storage costs fall, incumbent engine builders bundle lithium packs, blurring competitive lines with pure-play battery suppliers.

Black Start Generator Industry Leaders

Aggreko plc

Caterpillar Inc.

Cummins Inc.

Mitsubishi Heavy Industries Ltd

Man Diesel & Turbo Se

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The opportunity is shifting toward hybrid and inverter-integrated black start architectures as grid operators formalize pathways for inverter-based resources (IBR) and storage to contribute alongside conventional generator sets. Australia provides a clear example, where AEMO completed contract negotiations in June 2026 for transitional blackstart services to trial IBR black start capability, reflecting procurement interest in grid-forming controls and fast restoration without sole dependence on large synchronous machines. At the same time, ERCOT and other operators continue to publish and refine black start procurement and operational criteria, keeping qualification, periodic testing, and locational diversity central to service-agreement awards.

Investment programs that upgrade transmission and generation assets are also expanding the addressable scope for suppliers that can bundle restoration-ready packages with controls, commissioning, and compliance documentation. In the United States, the Department of Energy announced a USD 1.9 billion SPARK funding opportunity in March 2026, which aligns with modernization work that often includes black start capable auxiliaries, microgrid-ready fast-start engines, and islanding controls. For OEMs and integrators, the near-term opportunity clusters around (i) battery-assisted start and grid-forming add-ons that support stringent start-time and stability requirements, (ii) retrofit kits that bring legacy black start fleets into tighter testing and cyber-compliance regimes, and (iii) distributed portfolios of smaller black start resources that meet operator preference for diversity and reduced single-point failure risk.

Recent Industry Developments

- July 2026: BRNG LLC announced a USD 900 million investment in a dual-fuel energy facility in Kershaw County, South Carolina, designed with black start capability. The project highlights continued build-out of resilient, fuel-flexible generation that can provide restoration services and support large-load growth in addition to traditional utility needs.

- June 2026: Eku Energy announced its entry into Germany through the acquisition of the 400 MW/1,600 MWh Dion battery energy storage system project in Lamspringe, which includes black start capability. The shift underscores the expanding role of grid-forming BESS assets as alternatives or complements to rotating black start units in ancillary service procurement.

- June 2025: ERCOT published an updated Grid Insights document focused on black start procurement and operational criteria. By clarifying how resources are evaluated, located, and maintained for restoration plans, the update reinforces the importance of compliance-ready designs, routine testing, and demonstrated performance for contract retention.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market covers revenue generated from black start generators and related starter configurations that can restart power assets after a total or partial outage, including packaged systems sold to utilities and other critical facilities.

Scope exclusions: We exclude routine standby gensets that are not specified or engineered for black start duty and grid restoration sequences.

Segmentation Overview

- By Fuel Type

- Diesel

- Natural Gas

- Hybrid Battery-Diesel

- Others (Bio-diesel, HVO, etc.)

- By Power Rating

- Up to 1 MW

- 1 to 5 MW

- Above 5 MW

- By Starter Technology

- Diesel Engine Start

- Gas Turbine Start

- Battery-Energy-Storage-Assisted Start

- Compressed-air/Pneumatic Start

- By End-User Industry

- Power Utilities and T&D Operators

- Oil and Gas Upstream and Midstream

- Manufacturing and Process Industries

- Data Centres and ICT Hubs

- Commercial/Institutional and Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, map demand centers, and anchor the model to real world power system activity. We referred to public sources such as the U.S. Energy Information Administration for generation and outage context, the International Energy Agency for power capacity trends, and the World Bank for infrastructure and electricity access indicators.

We also reviewed grid and reliability publications from sources such as NERC and ISO or TSO websites, along with public procurement notices, company annual reports, and investor presentations that describe projects and installed base priorities. Where available, we cross-checked trade flows for large engine and turbine equipment using an import-export shipment-level database and checked innovation activity through a patent database to understand starter technology direction. The sources listed above are illustrative, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the sizing logic and confirm what gets counted as true black start scope across different buyer types. We spoke with a mix of OEM-facing experts, EPC and service participants, utility and T and D stakeholders, and large end users such as data center operators, with inputs balanced across APAC, EMEA, and the Americas so regional procurement patterns were not over-assumed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 41% |

| Mid tier: 47% | Functional/Unit leaders: 35% | EMEA: 32% |

| Smaller Players: 17% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where power capacity additions, grid restoration needs, and critical-load expansion are translated into an addressable demand pool for black start capable systems. From there, we validate the totals using selective bottom-up checks, such as sampled project values, typical package pricing by MW band, and supplier and channel discussions, which then help adjust for overcounting and double booking.

Inputs used in the model include utility black start procurement cycles, MW-based power rating mix (up to 1 MW, 1 to 5 MW, and above 5 MW), starter technology adoption (diesel engine, gas turbine, battery-energy-storage-assisted, and pneumatic), and fuel preference shifts between diesel, natural gas, and hybrid configurations. To forecast, scenario analysis was applied around outage and resilience spending intensity, backed by expert views on lead times and budget timing, and then smoothed with trend-based checks so year-to-year jumps stayed realistic. When specific country or end-user data points were missing, gaps were handled through proxy indicators like installed capacity, grid expansion activity, and comparable project density before being validated again through interviews.

Data Validation & Update Cycle

Outputs are checked against independent signals such as grid reliability programs, major black start tenders, and stated utility resilience investments, and then reviewed for outliers at the region and technology level. If a segment shows an unusual swing, we revisit the assumptions, re-check calculations, and re-contact select experts to confirm whether the change is real or a modeling artifact.

A multi-step review is followed before sign-off, where another analyst re-tests the logic and verifies that the final totals reconcile with the demand pool and pricing assumptions. Reports are refreshed annually, and interim updates are made when material events occur, such as large grid incidents, policy shifts, or a visible change in procurement activity. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Black Start Generator Market Size Measured Against Other Published Estimates

Published market sizes for black start generators often do not match because the scope line is drawn differently, and then the pricing and timing assumptions are applied with different levels of checking. Differences also come from whether the estimate is anchored to utility restoration programs, or expanded to include broader standby generator demand.

The spread is usually explained by what is counted as black start eligible equipment, how hybrid battery-diesel packages are treated, and whether starter technology and MW ratings are modeled with separate price curves. In this study, routine standby gensets are kept out unless they are specified for restoration sequences and validated through buyer and project signals, a scoping choice used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.42 B (2025) | |

| Trade Publisher A | USD 1.71 B (2024) | Uses an earlier base year and appears to center the value on a narrower utility-only interpretation, which can undercount industrial and data center deployments and does not clearly separate starter technology pricing. |

| Industry Research Portal B | USD 1.71 B (2025) | Likely applies broader averaged pricing and a conservative growth path, and the scope description is not explicit on inclusion of hybrid packages and MW-based price steps, which can compress the total market value. |

The table shows that most of the gap comes from scope tightness and how pricing is stepped by power rating and starter configuration. When the counted systems are tied back to identifiable restoration use cases and cross-checked with tender and interview feedback, the resulting market value becomes easier to trace and repeat in future updates.

Key Questions Answered in the Report

How large is the black start generator market in 2026?

The black start generator market size stands at USD 2.55 billion in 2026 with a 5.18% CAGR outlook through 2031.

Which fuel dominates restart applications?

Diesel sets lead with 61.20% share in 2025 because of rapid start capability and robust supply logistics.

What segment is growing fastest by end-user?

Data centers and ICT hubs are expanding at 10.02% CAGR as AI workloads demand uninterrupted power.

Which region shows the highest growth?

Asia-Pacific posts the fastest 8.55% CAGR thanks to extensive grid modernization across China and India.

How are emission rules influencing technology choice?

Tier 4 / Stage V legislation accelerates adoption of hybrid battery-diesel and natural-gas packages in urban zones.

What innovations may disrupt diesel reliance?

Grid-forming batteries and hydrogen-ready turbines demonstrated successful black start capability, signaling future alternatives to conventional engines.

Page last updated on: