Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.68 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

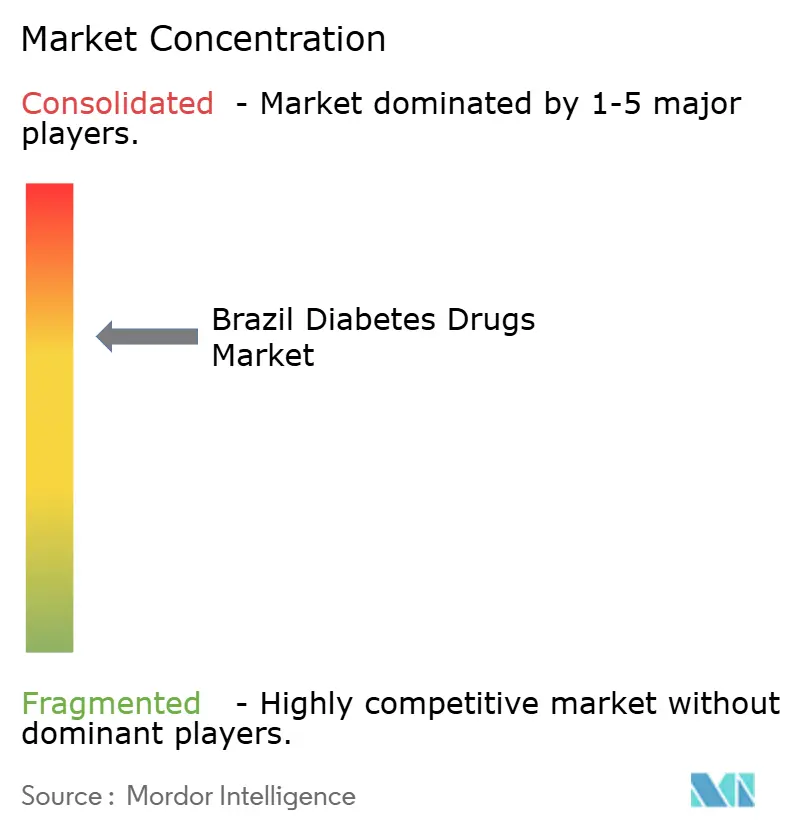

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Diabetes Drugs Market Analysis by Mordor Intelligence

The Brazil diabetes drugs market size is expected to grow from USD 1.68 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 6.72% CAGR over 2026-2031. Steady expansion is propelled by Brazil’s large and rising diabetic population, patent expirations that open space for generics, and sustained investments in local manufacturing. Increasing adoption of GLP-1 receptor agonists, weekly insulin formulations, and tele-pharmacy services signals a market shifting toward convenience-focused therapies and technology-enabled care. Intensifying competition among multinational and domestic manufacturers, coupled with government reforms such as sweetened-beverage taxes and incentives for healthy foods, provides fertile ground for both premium and cost-efficient products.

Key Report Takeaways

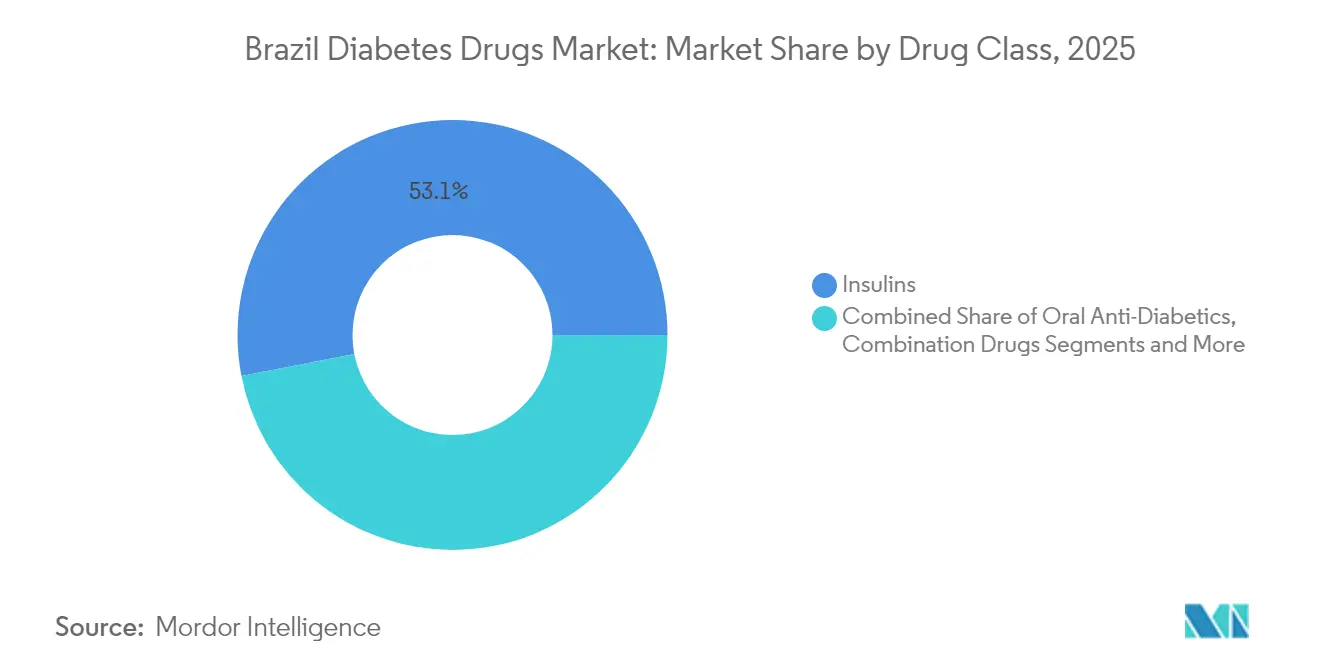

- By drug class, insulins led with 53.05% of Brazil diabetes drugs market share in 2025, while non-insulin injectables are forecast to post the fastest 10.34% CAGR through 2031.

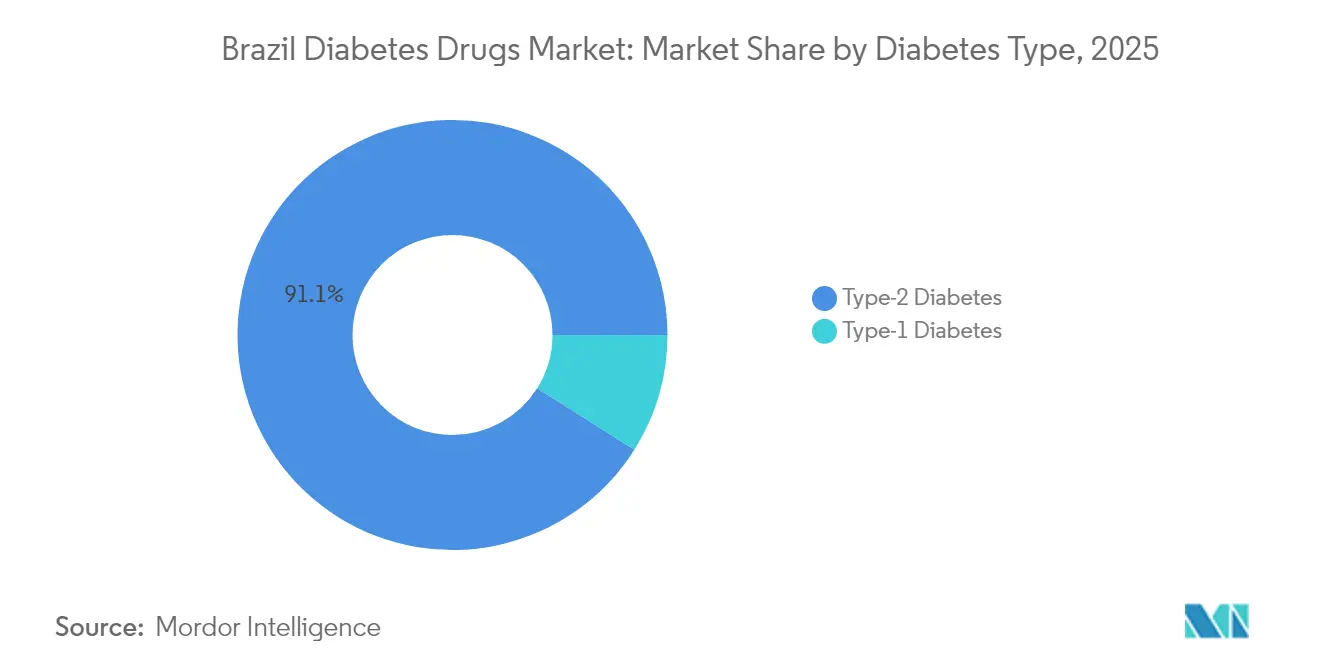

- By diabetes type, Type 2 accounted for 91.05% share of the Brazil diabetes drugs market size in 2025 and is expanding at 7.98% CAGR to 2031.

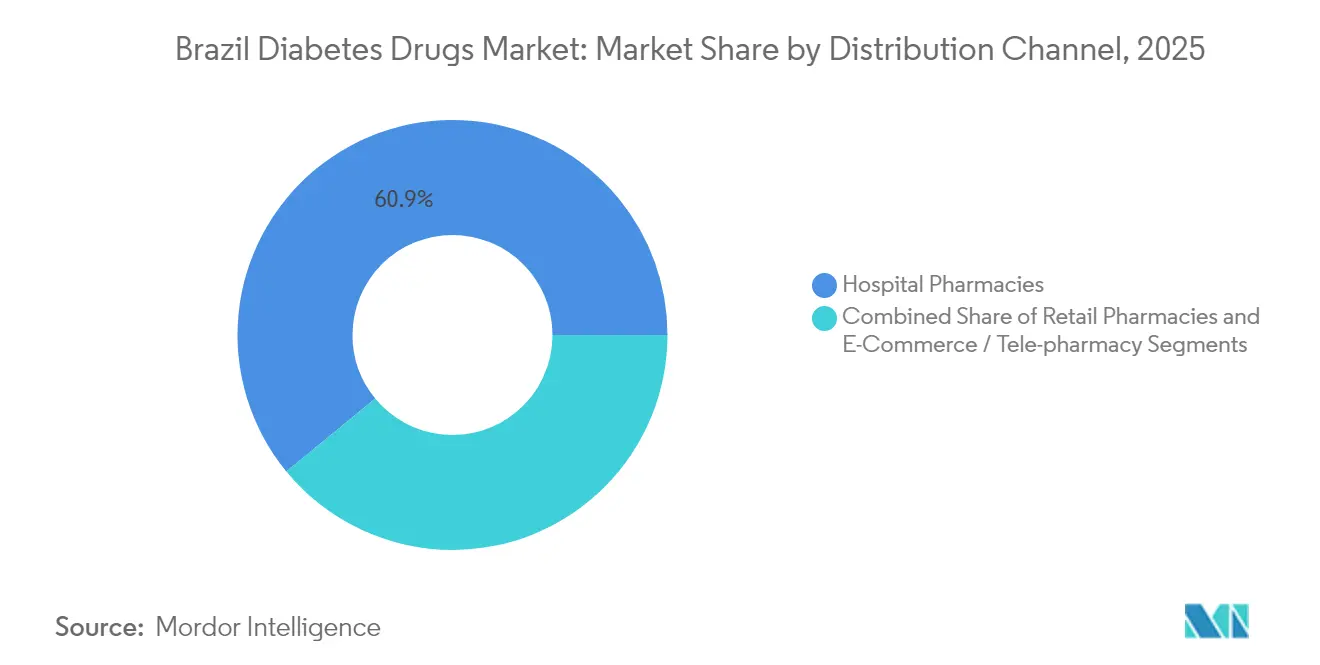

- By distribution channel, hospital pharmacies held 60.94% revenue share in 2025; e-commerce and tele-pharmacy are advancing at an 10.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Burden of Diabetes | +1.8% | National, with higher concentration in Southeast and Northeast regions | Long term (≥ 4 years) |

| Government Investment and Strategic Healthcare Program | +1.2% | National, with focus on underserved regions | Medium term (2-4 years) |

| Adoption of Novel Therapies and Delivery Systems | +1.5% | Urban centers, expanding to rural areas | Medium term (2-4 years) |

| Technological Advancement and Digital Health Adoption | +0.9% | Metropolitan areas, gradual rural penetration | Long term (≥ 4 years) |

| Local Manufacturing Investment and Partnership | +1.1% | National, with manufacturing hubs in Southeast | Long term (≥ 4 years) |

| Digital Therapeutic Reimbursement Inclusion | +0.7% | National, prioritizing SUS coverage areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Burden of Diabetes

Brazil’s persistent rise in obesity and sedentary lifestyles fuels a heavy diabetes burden that anchors long-run demand. GLP-1 receptor agonist sales reached R$4.2 billion between January 2023 and January 2024, underscoring rapid therapeutic uptake. Modeling studies foresee diabetes cases rising to 43 million by 2036, signalling a 27% prevalence if current trends continue.[1]Patrícia Vasconcelos Leitão Moreira, “Predicting the Prevalence of Type 2 Diabetes in Brazil: A Modeling Study,” Frontiers in Public Health, frontiers.org With 46% of cases undiagnosed, improved screening represents untapped volume for the Brazil diabetes drugs market.

Government Investment and Strategic Healthcare Program

The R$300 billion “Brasil Saudável” program channels R$42 billion toward health-related manufacturing, encouraging local supply, lowering import reliance, and widening drug access. Integration of diabetes indicators into the Previne Brasil pay-for-performance model signals official commitment, although 2022-2023 compliance averaged only 19.5% against a 50% target, revealing execution gaps that suppliers can help address.[2]Rodrigo Citton Padilha dos Reis, “Primary Care Performance Measurement in Brazil (Previne Brasil Program), 2022–2023,” BMC Health Services Research, biomedcentral.com

Adoption of Novel Therapies and Delivery Systems

Weekly insulins such as insulin icodec offer adherence advantages by cutting injection frequency and are poised to lift premium volumes in the Brazil diabetes drugs market. GLP-1 brands Ozempic and Rybelsus posted double-digit sales gains in 2024, while tirzepatide awaits commercial launch, highlighting persistent appetite for innovative molecules.

Technological Advancement and Digital Health Adoption

Telehealth pilots such as UBS+Digital completed 6,312 remote sessions with 85% resolution, proving virtual care’s ability to manage chronic disease at scale. [3]Celina de Almeida Lamas, “Telehealth Initiative to Enhance Primary Care Access in Brazil (UBS+Digital Project),” Journal of Medical Internet Research, jmir.orgHomegrown tools like InsulinAPP achieved clinical reliability comparable with specialist oversight, supporting broader digital rollouts within the Brazil diabetes drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Hurdles and Approval Delays | -0.8% | National, affecting all pharmaceutical companies | Short term (≤ 2 years) |

| Low Adherence and Awareness Gaps | -1.2% | National, more pronounced in rural and low-income areas | Medium term (2-4 years) |

| Healthcare Access in Rural/Low Income Regions | -0.9% | Rural areas, Northeast and North regions | Long term (≥ 4 years) |

| Shrinking SUS Budget for Chronic Drugs | -1.1% | National, affecting public healthcare system | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles and Approval Delays

ANVISA’s updated clinical-trial rules and serialization mandates lengthen product-registration cycles, requiring firms to invest in compliance and potentially slowing new-drug launches. Upcoming two-part prescription rules for GLP-1 agonists may also suppress early demand as pharmacies adjust.

Low Adherence and Awareness Gaps

Only 44.8% of primary-care patients achieve target HbA1c, indicating significant adherence challenges. Lower education levels and rural residence correlate with limited access to testing and medical consultation, curbing appropriate therapy use within the Brazil diabetes drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Insulins Dominate Despite Injectable Innovation

Insulins held 53.05% of Brazil diabetes drugs market share in 2025, reflecting entrenched dependence among Type 1 patients and late-stage Type 2 cases. Novo Nordisk’s Montes Claros site, responsible for 25% of its global insulin output, underscores Brazil’s strategic manufacturing role. The Brazil diabetes drugs market size for insulins is expected to expand steadily as weekly formulations reach pharmacies and biosimilar uptake gains speed. Non-insulin injectables, led by GLP-1 agonists, posted a 10.34% CAGR outlook through 2031, driven by strong efficacy and weight-management benefits.

Patent cliffs amplify competition: semaglutide protection ends in March 2026, prompting Hypera, Biomm, and EMS to ready generic versions. Biosimilar programs have already cut treatment outlays by 55.9% in select health-plan pilots, encouraging broader payer support. Transgenic-insulin research at Universidade de São Paulo, which engineers cows that secrete human insulin, signals a potential long-term supply breakthrough.

By Diabetes Type: Type 2 Dominance Reflects Epidemic Proportions

Type 2 accounted for 91.05% of the Brazil diabetes drugs market in 2025 and is forecast to grow at 7.98% CAGR to 2031. Sweetened-beverage excise taxes introduced in 2025 aim to blunt incidence, yet rising obesity and aging are set to keep volumes high. The Brazil diabetes drugs market size for Type 2 therapeutics is expected to climb as screening uncovers presently undiagnosed cases. Type 1 remains clinically significant; persistent HbA1c readings around 9% suggest ongoing need for advanced basal and bolus insulin combinations.

Uneven regional prevalence shapes uptake: wealthier Southeast and South house the largest absolute patient pools, while the Northeast posts the highest prevalence rates, reflecting socioeconomic and lifestyle factors. Mortality trends in the South further point to urgent control gaps among elderly populations.

By Distribution Channel: Hospital Dominance Faces Digital Disruption

Hospital pharmacies controlled 60.94% of sales in 2025 as complex regimens and inpatient initiation keep them central to therapy distribution. Yet tele-pharmacy and e-commerce platforms are set to grow 10.78% per year, reflecting consumer preference for convenience and home delivery. The Brazil diabetes drugs market size through digital channels is projected to climb sharply as remote glucose monitoring pairs with doorstep medication supply.

ANVISA’s two-part prescription rule for GLP-1s complicates in-store workflows, nudging some patients toward structured tele-pharmacy programs that manage renewals on their behalf. Telehealth pilots demonstrated 85% clinical-issue resolution, validating virtual consultation as a credible front door into the Brazil diabetes drugs market.

Geography Analysis

Regional disparities shape prescription volumes, access, and outcomes across Brazil’s vast landscape. The Southeast, anchored by São Paulo, leads the Brazil diabetes drugs market in absolute sales thanks to dense populations and a concentration of endocrinologists. Higher per-capita income and strong private-insurance penetration enhance access to novel injectables, promoting faster GLP-1 adoption in cities such as São Paulo and Rio de Janeiro. Novo Nordisk’s Montes Claros plant in Minas Gerais underpins regional job creation and reliable insulin supply, reinforcing supply-chain resilience for the entire Brazil diabetes drugs market.

The Northeast records the nation’s highest prevalence despite lower income, driving demand for cost-effective generics. Previne Brasil results show the region outperforming the Southeast on basic diabetes indicators, demonstrating effective primary-care mobilization despite limited resources. Nevertheless, mortality remains elevated due to late diagnosis and gaps in specialist care, keeping growth opportunities high for both basal insulin biosimilars and affordable oral fixed-dose combinations.

In the South, aging demographics and lifestyle patterns produce high mortality, while May 2024 floods exposed vulnerability of elderly patients when cold-chain disruptions and medication loss occurred. The North’s sparse infrastructure leaves vast rural zones dependent on telemedicine pilots and mobile clinics, offering fertile ground for tele-pharmacy expansion within the Brazil diabetes drugs market. Digital literacy programs and 4G coverage initiatives may unlock latent demand as electronic prescription and home-delivery models gain ground.

Competitive Landscape

Competition is moderate with strong multinational presence yet growing local challenges. Novo Nordisk remains the anchor, investing R$6.4 billion to enlarge Montes Claros and ensure steady supply of GLP-1 medicines such as Ozempic and Wegovy. Eli Lilly seeks share through tirzepatide and weight-loss positioning, while Sanofi capitalizes on basal-insulin heritage.

Generic makers—including Hypera, EMS, and Biomm—leverage patent expirations to carve out footholds. Hypera plans a 2026 semaglutide generic launch ahead of multiple local rivals, though pen-device supply may limit early volumes. EMS invested more than R$1 billion in liraglutide production and secured ANVISA approval that could support exports once FDA certification is obtained.

Public-private alliances play an increasing role. Fiocruz’s tie-up with Boehringer Ingelheim to produce a generic empagliflozin for SUS exemplifies state-backed strategies to boost local capacity and affordability. Digital solutions such as InsulinAPP generate competitive differentiation, allowing device-drug bundles and data-driven adherence services that reinforce brand stickiness in the Brazil diabetes drugs market.

Brazil Diabetes Drugs Industry Leaders

AstraZeneca

Novo Nordisk A/S

Sanofi

Eli Lilly

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Novo Nordisk committed R$6.4 billion to expand Montes Claros production of injectable drugs, including GLP-1 medicines Ozempic and Wegovy.

- March 2025: Hypera announced plans to launch a semaglutide generic in 2026, preparing to challenge incumbents as the patent expires.

- February 2025: EMS invested over R$1 billion in liraglutide production and received ANVISA approval for a related compound, targeting second-half-2025 launch.

- March 2024: Fiocruz partnered with Boehringer Ingelheim to co-develop a generic Jardiance for SUS distribution.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Brazil diabetes drugs market includes all prescription insulins, oral glucose-lowering agents, non-insulin injectables (for example, GLP-1 receptor agonists), and fixed-dose combinations distributed through hospital, retail, and e-pharmacy channels, valued at manufacturer selling price before taxes.

Excluded from Scope: nutraceuticals, herbal adjuvants, OTC vitamins, and any device-linked consumables.

Segmentation Overview

- By Drug Class

- Insulins

- Oral Anti-Diabetics

- Non-Insulin Injectables

- Combination Drugs

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-Commerce / Tele-pharmacy

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists, procurement heads at public hospitals, national wholesalers, and payer officials across the Southeast, South, and Northeast. These discussions clarified patient mix, reimbursement ceilings, and emerging GLP-1 uptake, enabling us to fine-tune penetration and price assumptions that secondary sources could not fully reveal.

Desk Research

Our analysts began by mapping drug utilization with open-source datasets from the Ministry of Health (DATASUS), Anvisa product registries, International Diabetes Federation prevalence tables, World Bank macro-series, and peer-reviewed medical journals that track therapy guideline shifts. Company 10-K filings and quarterly presentations supplied launch timing and pricing context. Where branded revenue detail was limited, paid databases such as D&B Hoovers and Dow Jones Factiva confirmed manufacturer sales, while Volza import records gave an external checkpoint on insulin volumes entering major ports. The sources named are illustrative; many additional references fed our data collection and verification work.

Market-Sizing & Forecasting

The top-down model starts with treated Type 1 and Type 2 patient pools, links them to monthly dose intensity, and multiplies by weighted average selling price to arrive at 2025 revenue. Supplier roll-ups and selective pharmacy sell-out checks act as a bottom-up sense check. Key variables include diagnosed prevalence, SUS reimbursement share, shift from human to analog insulins, GLP-1 adoption rate, and inflation-adjusted ASP progression. A blended multivariate regression plus ARIMA framework carries the forecast to 2030, after scenario vetting with expert respondents.

Data Validation & Update Cycle

Mordor's review stack applies variance thresholds; any outlier beyond two standard deviations triggers re-contact with data providers. Senior reviewers sign off only after cross-series alignment. We refresh every year, with interim flashes for material regulatory or pricing events and a last-minute pass before client delivery.

Why Mordor's Brazil Diabetes Drugs Baseline Earns Trust

Published estimates often diverge because firms vary in scope, patient filters, and currency timing. We show our anchors openly so users see where figures split.

Others may omit Farmacia Popular volumes or focus solely on insulins, while Mordor tracks every reimbursed molecule. Some roll forward past ASPs without checking Anvisa reference price resets, or convert reais with period averages rather than spot rates, creating drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.68 B (2025) | Mordor Intelligence | |

| USD 1.66 B (2024) | Regional Consultancy A | Excludes non-insulin injectables; fixed exchange rate |

| USD 1.63 B (2024) | Trade Journal B | Top-down only; no hospital procurement check |

| USD 1.58 B (2023) | Global Consultancy C | Older baseline; omits free-drug program volumes |

By selecting the right breadth of molecules and validating both price and volume through multiple lenses, Mordor delivers a balanced, transparent baseline that decision-makers can replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Brazil diabetes drugs market?

The market is valued at USD 1.79 billion in 2026 and is forecast to reach USD 2.48 billion by 2031.

Which drug class leads sales in Brazil?

Insulins lead with 53.05% of Brazil diabetes drugs market share, supported by a large Type 1 population and late-stage Type 2 cases.

How fast are GLP-1 receptor agonists growing?

Non-insulin injectables that include GLP-1 agonists are expected to expand at 10.34% CAGR through 2031 as patients and physicians favor weight-management benefits.

What role does local manufacturing play?

Investments such as Novo Nordisk’s R$6.4 billion plant expansion and EMS’s R$1 billion liraglutide project aim to strengthen domestic supply and cut import reliance.

How are digital health tools influencing diabetes care?

Telemedicine pilots have resolved 85% of cases remotely, while apps like InsulinAPP provide safe insulin titration, collectively driving growth in tele-pharmacy channels.

When will semaglutide generics enter the Brazilian market?

Semaglutide’s patent expires in March 2026, with Hypera and other local firms positioning to launch generics soon after regulatory clearance.

Page last updated on: