Bio-based 1,4-Butanediol Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 42.46 kilotons |

| Market Volume (2031) | 66.54 kilotons |

| Growth Rate (2026 - 2031) | 9.40% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

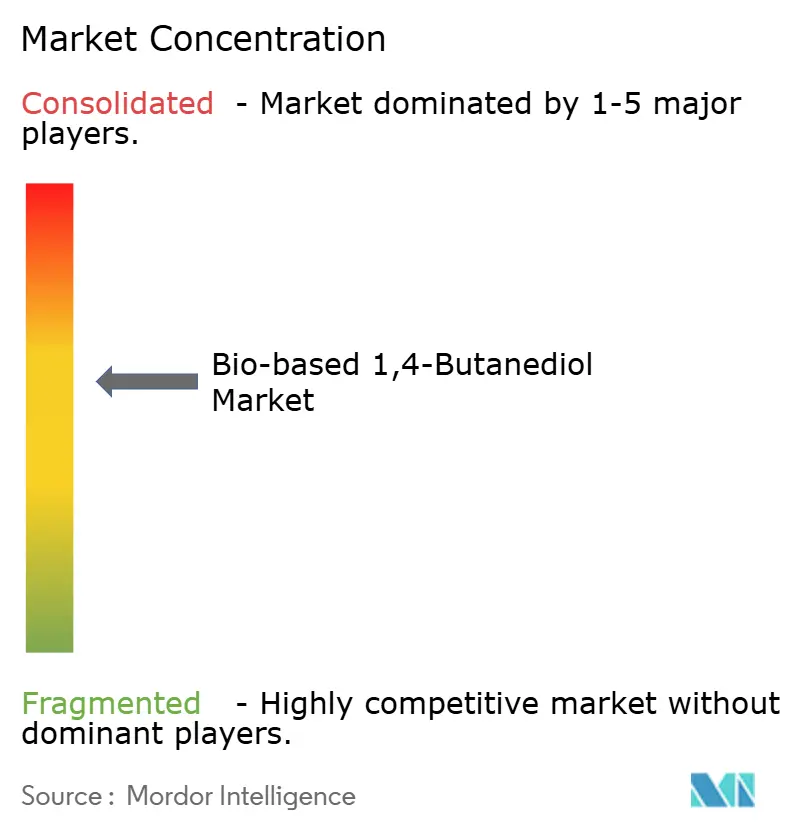

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-based 1,4-Butanediol Market Analysis by Mordor Intelligence

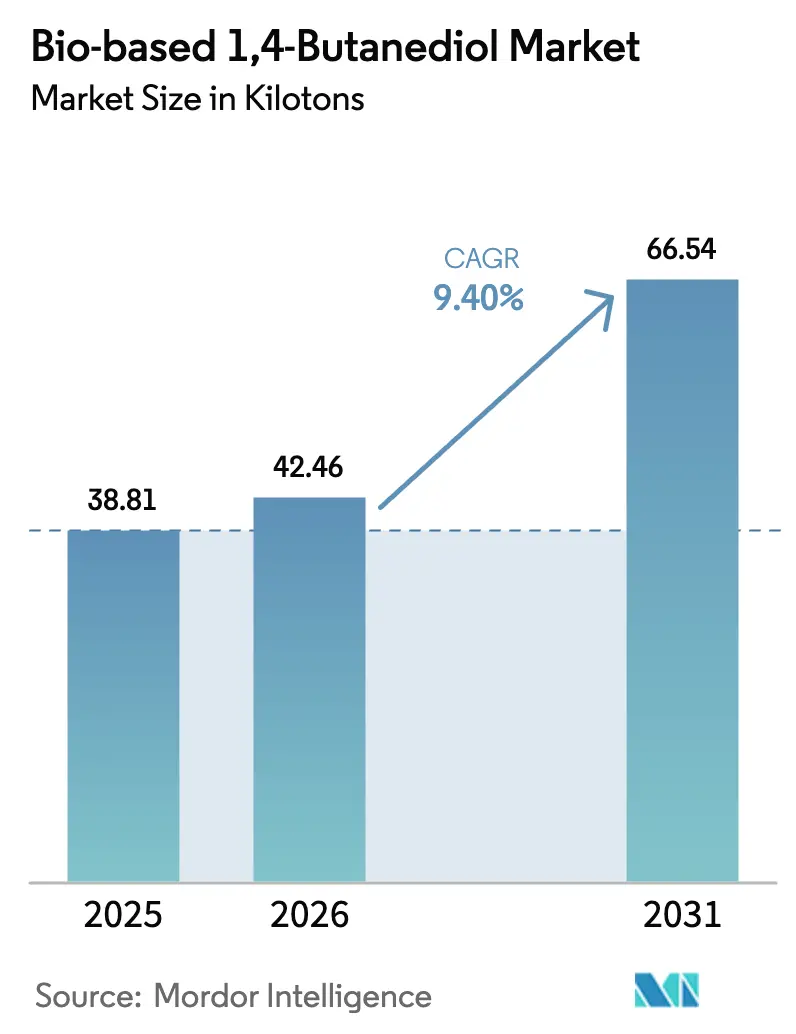

The Bio-based 1,4-Butanediol Market size is projected to be 38.81 kilotons in 2025, 42.46 kilotons in 2026, and reach 66.54 kilotons by 2031, growing at a CAGR of 9.40% from 2026 to 2031. Growth rests on brand-owner mandates for lower Scope 3 emissions, multi-year offtake agreements with chemical converters, and tightening policy frameworks that penalize fossil intermediates. Tetrahydrofuran’s (THF) large pull from performance-apparel spandex, the electrification-driven push toward polybutylene terephthalate (PBT) connectors, and steep cost declines in continuous fermentation are collectively steering demand toward low-carbon diols. Technology licensors supply high-productivity strains, while vertically integrated textile players establish captive demand that buffers price swings. Policy catalysts such as the EU Carbon Border Adjustment Mechanism and U.S. Inflation Reduction Act tax credits further level the field against naphtha- and coal-based BDO routes, cementing the momentum of the bio-based 1,4-butanediol market[1]U.S. Department of Energy, “Inflation Reduction Act Guidance for Bio-based Chemicals,” energy.gov .

Key Report Takeaways

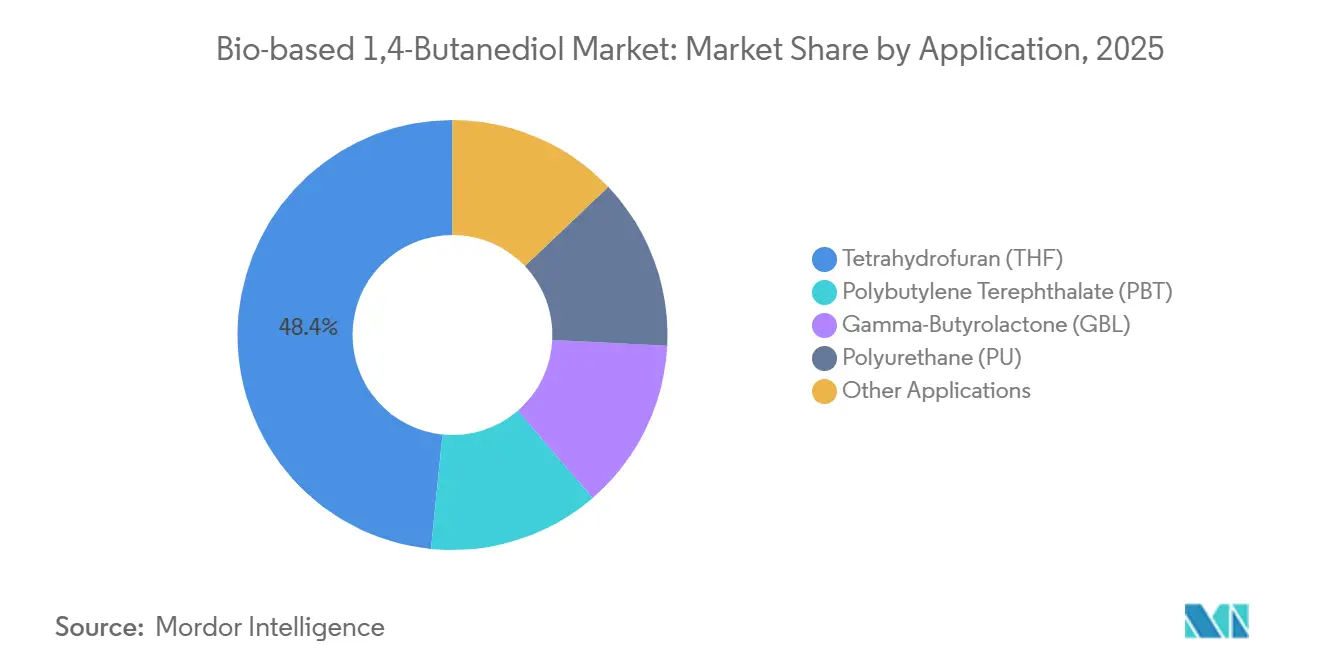

- By application, THF led with 48.40% of the bio-based 1,4-butanediol market share in 2025; PBT is projected to grow at a 9.62% CAGR through 2031.

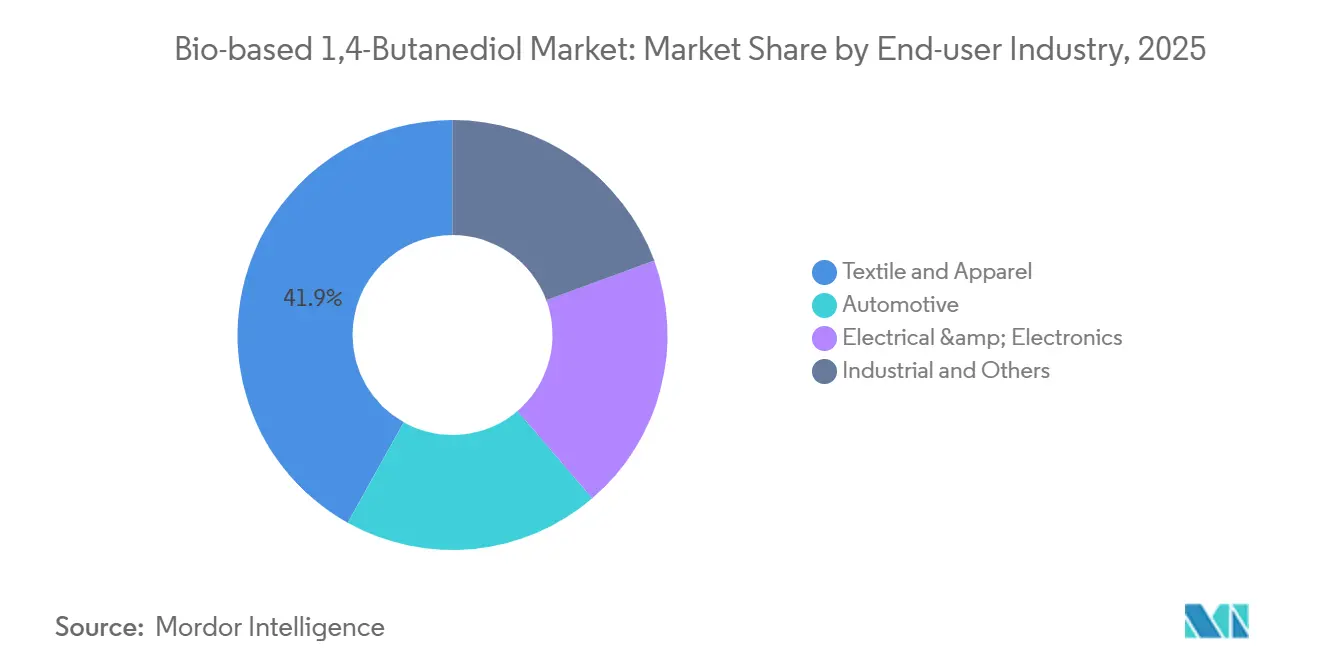

- By end-user industry, textiles accounted for a 41.90% slice of the bio-based 1,4-butanediol market size in 2025 and is advancing at a 10.02% CAGR to 2031.

- By geography, Europe commanded 75.01% volume in 2025, while North America records the highest forecast CAGR at 9.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bio-based 1,4-Butanediol Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for polybutylene terephthalate | +2.1% | Europe and Asia-Pacific automotive hubs | Medium term (2–4 years) |

| Stringent global and regional carbon mandates | +2.5% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Brand-owner net-zero commitments | +1.8% | North America and Europe head-office clusters | Medium term (2–4 years) |

| Rapid cost declines in bio-fermentation | +1.9% | North America, Europe, Asia-Pacific research and development centers | Short term (≤ 2 years) |

| Lignocellulosic feedstock commercialization | +1.3% | Asia-Pacific, North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Polybutylene Terephthalate (PBT)

Electric-vehicle architectures require PBT connectors, battery housings, and charging components able to endure temperatures above 150 °C. The material’s thin-wall moldability drops part weight by up to 20%, a benefit amplified in range-sensitive battery platforms. Bio-based BDO acts as a drop-in precursor, letting converters certify renewable content without requalifying critical parts. BASF’s REDcert2-approved biomass-balance BDO, commercial since 2024, enables identical mechanical performance while trimming embedded carbon[2]BASF, “REDcert2 Biomass Balance Certification for BDO,” basf.com. The electronics sector adds upside as 5G rollouts and data-center buildouts fuel 8% annual PBT demand growth to 2030.

Stringent Global and Regional Carbon-Reduction Mandates

The EU Carbon Border Adjustment Mechanism levies carbon fees on high-emission imports, raising the landed cost of coal-derived BDO by EUR 150–200 per ton once organic chemicals join the scope in 2026. California’s Low Carbon Fuel Standard and U.S. Inflation Reduction Act award tradable credits and production tax relief that shave USD 0.20–0.30 per kilogram from qualifying bio-BDO output. China’s dual-carbon pathway, aiming for neutrality by 2060, curtails approvals for new coal-based BDO units while prioritizing bio-routes, and RED II lifts demand for THF as a renewable fuel additive in Europe.

Brand-Owner Net-Zero Commitments Across CPG and Automotive

LYCRA Company’s 2025 launch of spandex with 70% renewable PTMEG underscores how procurement clauses now require minimum bio-content thresholds. Major apparel groups target 30–50% Scope 3 cuts by 2030, making spandex a material carbon hotspot. Automotive OEMs embed 25% renewable carbon into interior resin contracts for post-2028 models. Certification bodies such as ISCC PLUS audit mass-balance claims, raising compliance costs for suppliers unable to prove traceability.

Rapid Cost Declines in Bio-Fermentation Technologies

Continuous reactors lift productivity by 40–50% compared with batch, while high-titer Genomatica strains exceed 100 g/L, slicing separation costs. Membrane recovery lowers thermal energy by 30%. LanzaTech’s gas-fermentation pathway valorizes off-gases, producing BDO under USD 1.50 per kilogram in integrated steel sites. Unit costs narrowed to a 10–15% premium over fossil BDO in 2026, versus 25% in 2024.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price gap versus fossil BDO amid crude swings | -1.5% | Global, acute in price-sensitive Asia-Pacific | Short term (≤ 2 years) |

| Limited fermentation capacity outside Asia-Pac | -0.9% | North America and Europe | Medium term (2–4 years) |

| Strain IP litigation | -0.6% | U.S., EU, Japan patent jurisdictions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price Gap Versus Fossil BDO Amid Crude Volatility

Bio-BDO tracks glucose and sucrose costs, which surge during poor harvests, while fossil peers ride naphtha and natural-gas cycles. When crude slipped below USD 70 per barrel in late 2024, bio premiums widened to 25%. Chinese coal-based BDO sold at USD 1.60–1.80 per kilogram, undercutting bio alternatives by up to 30%, pressuring converters lacking sustainability clauses.

Limited Large-Scale Fermentation Capacity Outside Asia-Pacific

Europe and North America host just two commercial plants over 30 kilotons—Novamont in Italy and Qore in Iowa—amounting to less than 15% of global nameplate. Licensing Genomatica’s strain takes 18–24 months, and greenfield fermentation demands USD 150–200 million, deterring mid-tier entrants. Import reliance raises freight costs by USD 200–300 per ton and lengthens lead times to 4–6 weeks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: THF Dominance Reflects Spandex Fiber Surge

Tetrahydrofuran (THF) secured 48.40% of 2025 volume and is on track for a 9.62% CAGR through 2031, buoyed by brisk spandex demand in athleisure and intimate apparel. The spandex launch using Qore’s bio-BDO cut carbon footprints by 44%, turning THF into the flagship application within the bio-based 1,4-butanediol market. PBT applications follow, driven by electric-vehicle connector needs and a predicted 8% rise in automotive PBT demand to 2030. Gamma-butyrolactone supports specialty solvents, while polyurethane elastomers tap into green-building and low-VOC trends. Vertical integration projects such as Hyosung TNC’s Vietnam complex secure captive PTMEG demand, insulating THF supply chains from feedstock volatility and locking in offtake for 50,000 tons of spandex capacity by mid-2026.

Second-tier applications remain niche yet profitable. GBL feeds agrochemical intermediates where regulatory approvals favor validated bio routes. PU’s move into rigid insulation broadens market scope. These diverse outlets collectively reinforce the bio-based 1,4-butanediol market’s resilience against single-industry downturns and help suppliers balance production portfolios over multi-year contracts.

By End-User Industry: Textile Sector Leads Growth Trajectory

The textile segment consumed 41.90% of bio-BDO in 2025 and leads volume expansion at 10.02% CAGR to 2031. Athleisure’s 7% annual growth, coupled with four-way stretch innovations, boosts spandex penetration per garment and keeps THF pull robust. Automotive ranks second, buoyed by OEM carbon dashboards that now mandate renewable resin inputs for under-the-hood parts. Electrical and electronics adopt bio-based PBT for high-frequency connectors in 5G modules and server racks, driven by dielectric strength and light-weighting benefits.

Fast-fashion retailers pivot toward science-based carbon targets under EU Ecodesign rules, cascading bio-content demands through the fabric supply chain. Automotive lightweighting initiatives target 100-kilogram per-vehicle reductions by 2030, with PBT replacing metal and glass-filled nylon in structural roles. Electronic brands pursuing eco labels specify renewable PBT, capturing sustainability-minded consumers in North America and Europe. Industrial coatings and adhesives leverage bio-BDO polyols to qualify for LEED and BREEAM credits, rounding out the varied outlets that anchor long-range growth for the bio-based 1,4-butanediol market.

Geography Analysis

Europe held 75.01% of global volume in 2025, underpinned by BASF’s REDcert2-approved biomass-balance BDO and Novamont’s dedicated 30-kiloton plant. The Carbon Border Adjustment Mechanism lifts imported fossil BDO costs by EUR 150–200 per ton from 2026, effectively subsidizing regional bio output. Germany, the United Kingdom, France, and Italy contribute more than 60% of European demand, driven by automotive PBT consumption and a large textile converting base. Nordic initiatives exploit forestry residues as feedstock, while Turkey’s export-oriented textile sector draws bio-PTMEG to meet EU brand specifications.

North America posts the fastest 2026–2031 trajectory at 9.87% CAGR. Qore’s 65-kiloton Iowa facility ships commercial volumes from 2026, feeding LYCRA’s U.S. spandex lines. Inflation Reduction Act incentives drop bio-BDO cash costs and attract new fermentation proposals. California’s LCFS credits and Canada’s Clean Fuel Regulations spur THF molecules for fuel additives. Mexico’s vehicle production hub pulls bio-PBT, integrating cross-border supply chains and undergirding regional growth.

Asia-Pacific commands the bulk of global capacity, with Chinese producers leveraging corn and cassava streams at competitive cost. Hyosung TNC’s USD 1 billion Vietnam build secures captive demand and lowers supply risk. Japanese majors Toray and Mitsubishi advance cellulosic sugar routes that integrate into wider polyester and nylon programs. South Korea’s LG Chem positions bio-BDO for automotive and electronics accounts, and Southeast Asian textile clusters source renewable PTMEG to satisfy Western brands. The rest of the world leans on imports, yet growth pockets appear in Middle Eastern and South American textile expansions that require low-carbon feedstocks to preserve export competitiveness.

Value Chain Analysis

The upstream chain starts with renewable carbon feedstocks, mainly plant sugars sourced from crops such as dent corn (United States) and sugarcane (Southeast Asia), plus utilities and nutrients that shape fermentation economics. Technology licensing and strain/IP are a key enabling layer: Geno (formerly Genomatica) licenses biocatalysts and process know-how that support single-step fermentation routes, and the licensing and tech transfer timelines remain a gating item for new entrants.

Midstream production centers on industrial fermentation, purification, and logistics into merchant bio-based BDO. Scale-up bottlenecks tend to concentrate around feedstock and energy cost exposure, yield optimization, and separation energy, which affect the premium versus fossil BDO. Downstream conversion routes place bio-BDO into THF and PTMEG for spandex, and into PBT and other derivatives, where mass-balance and renewable-content certification supports adoption. The chain is increasingly shaped by vertical integration into fibers and polymers, including Qore LLC (Cargill and HELM JV) operating a 66,000 metric ton per year bio-based BDO facility in Eddyville, Iowa, and Hyosung TNC building an integrated bio-based BDO and bio-spandex platform in Vietnam using Geno technology.

Competitive Landscape

The bio-based 1,4-butanediol market remains moderately concentrated. Key industry players are heavily investing in research and development to optimize fermentation processes and enhance production efficiency. Strategic partnerships with technology providers, such as Genomatica, are playing a critical role in facilitating market entry and expansion. These collaborations are particularly significant for aligning with major chemical companies. Additionally, vertical integration is a strategic priority, encompassing renewable feedstock procurement and end-product manufacturing. Capacity expansion initiatives, including greenfield projects and joint ventures, are gaining momentum, especially in regions with stringent sustainability mandates. Companies are also improving operational flexibility by diversifying feedstock sources and adopting advanced biotechnology solutions.

Bio-based 1,4-Butanediol Industry Leaders

BASF SE

Genomatica Inc.

Cargill, Incorporated

DSM

Novamont S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regional supply diversification outside Asia-Pacific is a clear whitespace, since limited large-scale fermentation capacity continues to lengthen lead times and raise import costs for converters serving textile, automotive, and electronics customers. Capacity additions create concrete entry points for long-term offtake and derivative integration. Qore began operating its large-scale bio-based BDO facility in Eddyville, Iowa (66,000 metric tons per year), while Hyosung TNC moved its Vietnam bio-based BDO project from trial production (March 2026) to announced operation and supply (May 2026). Together, these shifts support faster qualification cycles for bio-THF/PTMEG and bio-PBT into North America and Southeast Asia, where procurement programs rely on traceable renewable content.

Process and feedstock innovation is a second opportunity pocket, focused on lowering conversion energy and widening the set of qualified feedstocks while maintaining certification. Work in microbial metabolic engineering and higher-productivity fermentation supports improved yields and steadier unit economics, which is most visible in high-volume THF demand for spandex and in PBT use for automotive and electrical connectors. Vertical integration also creates room for differentiated offerings, where suppliers connect bio-based BDO molecules to certified downstream polymers and fibers (for example, regen BIO spandex programs) to reduce switching friction and protect margins against commodity fossil BDO alternatives.

Recent Industry Developments

- May 2026: Hyosung TNC announced formal operation of its USD 1 billion bio-based BDO project in Vietnam, targeting an initial 50,000 tons per year capacity with an expansion plan to 200,000 tons per year. The announcement signals a shift toward vertically integrated supply from certified sugarcane to downstream polymer intermediates and fibers. It also adds a new Southeast Asian supply node that can serve textile value chains closer to spandex manufacturing footprints.

- July 2025: Qore (a joint venture of Cargill and HELM) commenced operations at its large-scale bio-based 1,4-butanediol facility in Eddyville, Iowa, with 66,000 metric tons per year capacity and a reported USD 300 million investment. Bringing this plant online materially increases merchant bio-BDO availability in North America and supports multi-year offtake structures with downstream THF, PBT, and polyurethane value chains. The start-up also reinforces the role of Geno-licensed fermentation technology in scaling supply.

- May 2024: BASF added REDcert2-verified BDO to its biomass-balance portfolio, providing converters a drop-in option with certified renewable content. This expanded the availability of certified BDO for customers seeking traceability without changing existing production assets. The move also strengthened Europe-led demand pull where certification is commonly embedded in procurement specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers bio-based 1,4-butanediol (1,4-BDO) produced from renewable feedstocks and supplied as an intermediate chemical, with volumes counted where it is produced and consumed across major regions.

Scope exclusions: We exclude fossil-based 1,4-BDO routes and do not count the value or volume of downstream finished products that use 1,4-BDO as an input.

Segmentation Overview

- By Application

- Tetrahydrofuran (THF)

- Polybutylene Terephthalate (PBT)

- Gamma-Butyrolactone (GBL)

- Polyurethane (PU)

- Other Applications

- By End-user Industry

- Automotive

- Electrical & Electronics

- Textile and Apparel

- Industrial and Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Turkey

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Rest of Asia-Pacific

- Rest of the World

- Middle-East and Africa

- South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the supply and demand context for bio-based intermediates, so the volume model is grounded in publicly observable information. We relied on sources such as the US EPA, European Commission publications, US International Trade Commission data tools, and UN Comtrade, plus technical papers in peer-reviewed chemistry and polymer journals.

We also reviewed company filings, investor presentations, press releases, and association websites to track commercial capacity additions, commissioning timelines, and application pull for THF, PBT, GBL, and polyurethane. Paid subscriptions were used for company financials and intelligence, and for patent databases to track process improvements and licensing momentum that can shift effective supply. These desk sources are not exhaustive, and we used additional public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what portion of 1,4-BDO output is genuinely bio-based, and how much is routed into THF, PBT, and GBL derivative chains in each region. We spoke with a mix of producers, downstream derivative participants, distributors, and large end users to test assumptions on operating rates, regional trade flows, and adoption constraints, then revisited gaps where desk signals did not align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 47% |

| Mid tier: 54% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 19% | Managers: 53% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where production capacity, operating rates, and announced ramp-ups are converted into annual bio-based 1,4-BDO volumes by region, then reconciled against derivative demand signals. Because the market is still relatively small and project-led in some countries, we corroborate totals with selective bottom-up checks such as sampled plant-level nameplate capacity, distributor channel checks, and volume splits implied by THF, PBT, and GBL output indicators.

Key inputs shaping the model include regional bio-based capacity additions, utilization ranges during ramp-up, the share of output directed to THF and PBT chains, trade movement patterns for relevant chemical intermediates, and end-use momentum in textiles, automotive, and electronics that influences derivative pull. Where bottom-up references were incomplete, we handled gaps by applying conservative utilization and allocation bands that were confirmed in calls, and then adjusted only when multiple signals pointed in the same direction.

For forecasting, scenario analysis was used so the model can reflect different ramp-up speeds and adoption rates. Here, assumptions on utilization and application split were carried forward only after primary respondents confirmed the likely ranges by region and end-use.

Data Validation & Update Cycle

Validation is done by comparing final totals against independent checks such as announced capacity timelines, observed derivative demand direction, and trade-related signals, then explaining any large variances prior to sign-off. When an input looks off, the team re-checks the source trail, pressure-tests the assumption, and re-contacts industry participants if the discrepancy persists.

Each report is refreshed annually, and interim updates are triggered when material events occur, including new plant starts, major shutdowns, or meaningful regulation changes that affect bio-based adoption. Before delivery, a final analyst pass is completed so the numbers reflect the latest available developments and any late-breaking capacity or utilization news.

Mordor Intelligence's Bio Based 1 4 Butanediol Market Estimate Compared With Other Published Estimates

Published market sizes for bio-based 1,4-BDO often diverge because unit treatment is not consistent across sources, and because the boundary between bio-based and conventional volumes is handled differently. Some sources publish value estimates, while others publish only volume, and that alone can move the headline number even when the underlying demand picture is similar.

Key gaps usually come from how conversion is handled from tons to dollars, what is assumed for average selling price by region and grade, and whether downstream derivatives are mistakenly blended into the counted market. By tracking capacity start-up timing, utilization bands, and application allocation, Mordor Intelligence keeps the calculation tied to bio-based 1,4-BDO volumes only, before any value conversion choices are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.21 B (2026) | |

| Global Consultancy A | USD 0.29 B (2027) | This estimate is value-based for a later year, and it likely uses a single blended ASP and faster ramp-up assumptions, which can lift the total when utilization is still stabilizing. |

| Regional Consultancy B | USD 0.18 B (2025) | This estimate appears to rely on a narrower demand view and may undercount trade flows and derivative pull-through, which can compress the implied volume and the converted value. |

The spread is mainly explained by timing, the volume-to-value conversion, and whether ramp-up utilization is treated conservatively in early years. Our approach stays traceable because it starts from capacity and allocation logic, then it is cross-checked with real demand signals from the main derivative chains.

Key Questions Answered in the Report

How fast is the bio-based 1,4-butanediol market projected to grow between 2026 and 2031?

The market is forecast to expand from 42.46 kilotons in 2026 to 66.54 kilotons by 2031, equating to a 9.40% CAGR.

Which application accounts for the largest share of renewable BDO demand?

THF used in spandex production led with 48.40% of volume in 2025 and is projected to sustain a 9.62% CAGR through 2031.

Why are textiles the fastest-growing end-user segment?

Athleisure and intimate-apparel brands embed bio-content clauses in supplier contracts, pushing textile demand to a 10.02% CAGR through 2031.

What makes Europe the dominant region today?

REDcert2 certification, the Carbon Border Adjustment Mechanism, and installed capacity at BASF and Novamont plants gave Europe 75.01% of 2025 volume.

Which region is expected to record the quickest growth?

North America should grow the fastest at 9.87% CAGR thanks to Qore’s Iowa plant startup and Inflation Reduction Act incentives.

Page last updated on: