Bangladesh Mustard Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

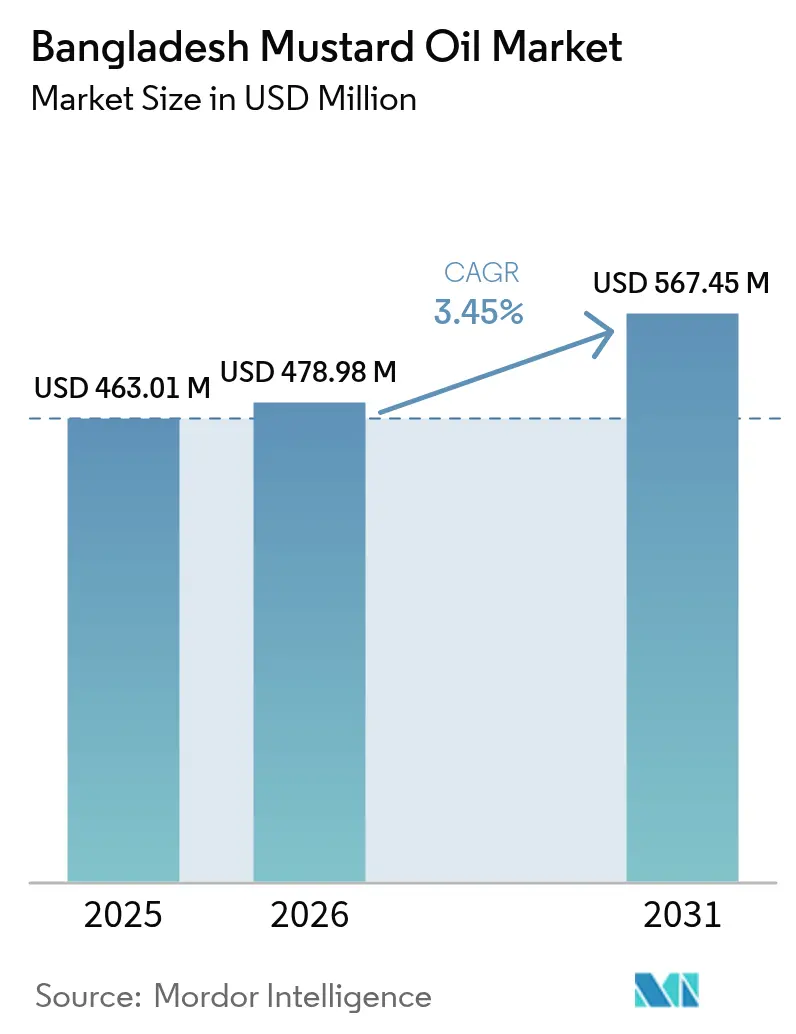

| Base Year Market Size (2025) | USD 463.01 Million |

| Market Size (2026) | USD 478.98 Million |

| Market Size (2031) | USD 567.45 Million |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

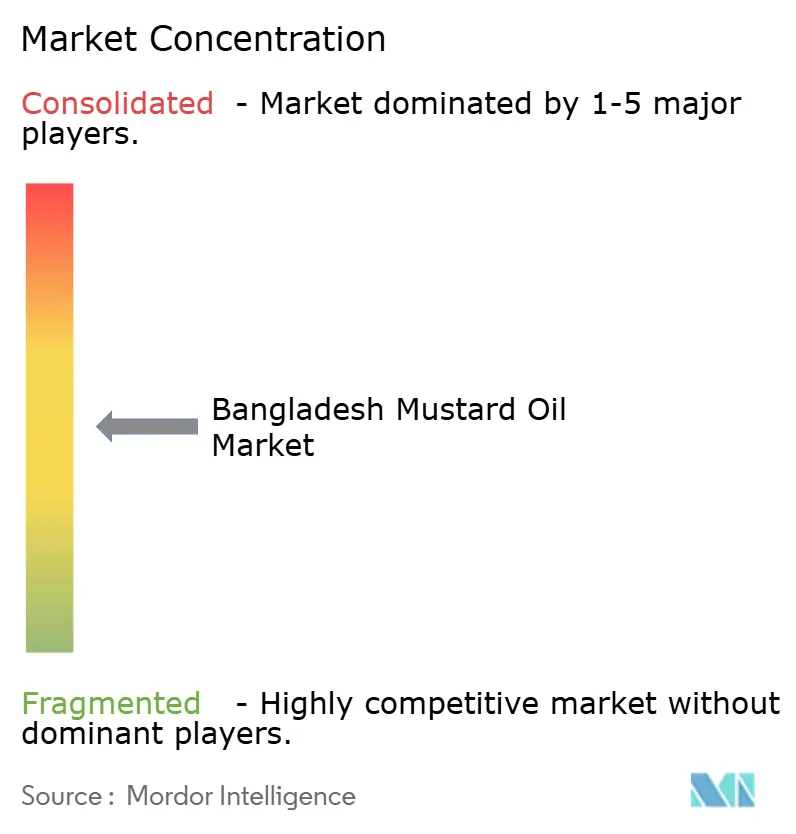

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bangladesh Mustard Oil Market Analysis by Mordor Intelligence

Bangladesh Mustard Oil Market size market size in 2026 is estimated at USD 478.98 million, growing from 2025 value of USD 463.01 million with 2031 projections showing USD 567.45 million, growing at 3.45% CAGR over 2026-2031. Rising government pressure to achieve 40% edible-oil self-sufficiency, higher domestic mustard seed output, and export momentum to Gulf countries underpin steady volume growth, while retail price parity with soybean oil sustains consumer loyalty despite import price volatility. Deep cultural attachment to unrefined Kachi Ghani oil, expanding health claims around omega-3 and natural antioxidants, and widening organized retail footprints in Dhaka and Chattogram are encouraging premiumization, whereas energy-efficient multi-oilseed crushing projects by leading processors temper cost pressures. Moderate competitive intensity, top five brands operate integrated farming, crushing, and distribution chains, but thousands of small cold-press mills still process over half of all seed, creating room for consolidation and technology-led efficiency gains. Exchange-rate constraints and tariff tweaks that favor home-grown oils over palm and soybean imports further improve pricing power for branded suppliers.

Key Report Takeaways

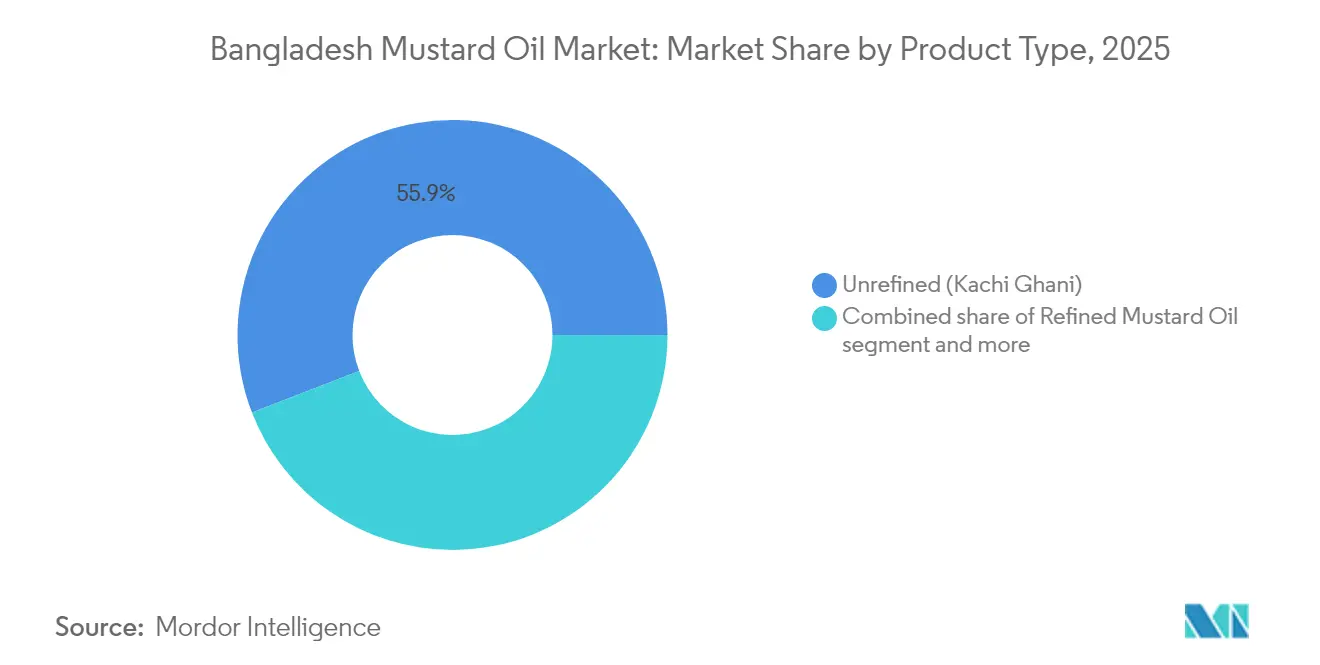

- By product type, unrefined Kachi Ghani held 55.87% of 2025 revenue, while refined mustard oil is projected to advance at a 4.61% CAGR through 2031.

- By packaging, bottles accounted for 57.64% of 2025 sales, whereas pouches are expected to expand at a 4.39% CAGR to 2031.

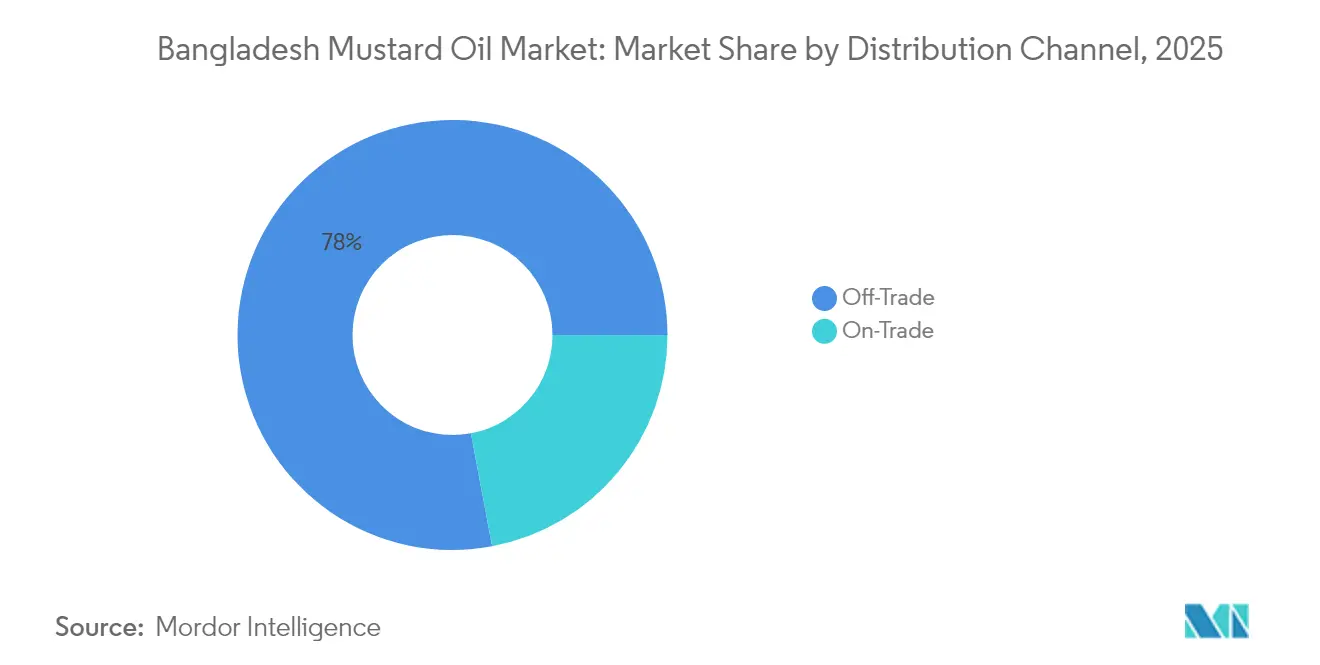

- By distribution channel, off-trade dominated with a 77.95% share in 2025, while on-trade/HoReCa is forecast to grow at a 4.73% CAGR through 2031.

- By region, Dhaka Division captured 39.88% of 2025 consumption, and Khulna Division is poised to rise at a 5.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Mustard Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deep cultural integration and culinary relevance | +0.9% | National, strongest in Dhaka, Chattogram, Rajshahi, Khulna Divisions | Long term (≥ 4 years) |

| Emergence of mobile mini-mills and on-site cold-pressing boosting rural demand | +0.6% | Rajshahi, Rangpur, Mymensingh Divisions; rural upazilas with dispersed mustard acreage | Medium term (2-4 years) |

| Strengthening health perceptions and naturalness appeal | +0.7% | Urban centers (Dhaka, Chattogram); middle/high-income segments nationally | Medium term (2-4 years) |

| Shift to mustard oil as soybean prices stay volatile | +0.5% | National, spill-over to price-sensitive rural households | Short term (≤ 2 years) |

| Government drive to cut edible-oil import bill via 40% self-sufficiency plan | +0.8% | National policy; production gains in Rajshahi, Khulna, Sirajganj, Jessore | Medium term (2-4 years) |

| Transition from loose to packaged mustard oil | +0.5% | Urban Dhaka, Chattogram; expanding to tier-2 cities and peri-urban zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Deep cultural integration and culinary relevance

Mustard oil holds a significant position in Bangladesh due to its deep cultural integration and culinary relevance. It serves multiple purposes, including use as a cooking medium, a carrier for traditional remedies like mustard paste for joint pain, a religious input for lamps in Hindu rituals, and a base for condiments such as kashundi. This cultural importance is being modernized rather than replaced, as seen in the Bangladesh Council of Scientific and Industrial Research’s July 2024 launch of sesame–mustard blended oil (SO80:MO20), which achieved a WHO/FAO-aligned fatty acid profile (SFA:MUFA: PUFA = 1:1.3:1), reduced erucic acid to 4.22%, below the 5% limit, and maintained low TOTOX values over 180 days without synthetic antioxidants [1]Source: Journal of King Saud University – Science (JKSUS), "Unique Formulation of Edible Blended Oil from Sesame and Mustard Seeds Grown in Bangladesh", jksus.org . These developments address regulatory, health, and oxidative-stability concerns while preserving the traditional characteristics of mustard oil. Public research and development initiatives support brand reformulation and premium new product development, enabling manufacturers to highlight both health benefits and traditional flavors. Recent media coverage has emphasized locally blended and cold-pressed oils as safer and more authentic alternatives to heavily refined imports. Price dynamics also favor mustard oil, with loose mustard oil retailing at BDT 160–180 per liter in March 2025, narrowing the cost gap with soybean oil and allowing middle-income households to maintain or increase their usage. Brands like Meghna Group’s Fresh Mustard Oil leverage domestic seed sourcing and automated purification to appeal to urban consumers seeking heritage and quality assurance. Government nutrition campaigns further promote indigenous oils, reinforcing mustard oil’s position due to its established role in Bengali recipes, family routines, and festivals. This convergence of cultural significance, scientific advancements, price competitiveness, and strategic branding strengthens mustard oil’s resilience against imported alternatives, positioning it as a core component in household oil consumption.

Emergence of mobile mini-mills and on-site cold-pressing boosting rural demand

The decentralization of crushing infrastructure through mobile mini-mills and on-site cold-pressing is reshaping mustard oil production in Bangladesh. This approach minimizes post-harvest losses for mustard seeds and retains value within production areas, reducing reliance on urban processors. Traditional cold-press units (Kachi Ghani), operated predominantly by small-to-medium mills, remain central to the market, processing domestically produced mustard seeds with lean inventories of 1–2 months to align with seasonal harvests. These mills sell fresh oil directly to rural retailers or urban wholesalers, bypassing intermediary layers that inflate costs. The on-site model enhances rural demand by offering fresher, pungency-retaining Kachi Ghani oil at competitive prices, while farmers benefit from dual revenue streams, oil sales and nutrient-rich mustard meal byproducts for livestock feed. This integrated approach incentivizes mustard cultivation over alternative crops. Reports highlight how localized crushing sustains the country's position as a major producer amid rising edible oil demand. Small mills have adopted mobile vending units to deliver bottled Kachi Ghani oil directly to village markets, avoiding wholesale markups. Brands like Janata Oil Mills, under Mika Group, exemplify this trend by marketing Tekka and Ghani pure mustard oils from on-site presses, emphasizing minimal processing and rural traceability. These mini-mills reduce dependency on imported rapeseed blends, stabilize supply during volatile harvests, and enable small crushers to compete with large FMCG companies. Government programs in 2024–2025 further supported this shift by subsidizing portable presses in regions like Bogra and Jamalpur, transforming rural processing into a cohesive growth engine and strengthening the mustard oil supply chain.

Shift to mustard oil as soybean prices stay volatile

Consumers in Bangladesh are increasingly shifting to mustard oil as a cost-effective alternative amid the persistent volatility in soybean oil prices. In December 2025, soybean oil prices surged, with one-litre bottles reaching BDT 198, a 5% increase from the previous week, and five-litre bottles climbing to BDT 965, up from BDT 910, as reported by the Trading Corporation of Bangladesh [2]Source: The Daily Star, "Refiners Hike Oil Price Without Govt Approval", thedailystar.net . Loose palm oil prices also rose due to global import cost pressures, fluctuations in letters of credit (LC), and a strong dollar. This price instability has driven demand for mustard oil, which benefits from local seed crushing, shielding it from international price fluctuations. Brands such as Square Food & Beverage's Radhuni Pure Mustard Oil have leveraged this trend by promoting consistent rural-sourced pricing and Kachi Ghani authenticity in urban markets, positioning mustard oil as a reliable and stable household staple. The direct link between soybean oil's price spikes and mustard oil's growing appeal has created a substitution effect, particularly in price-sensitive regions like Barishal, where families are reallocating budgets without compromising on cultural flavor profiles. Grocers have reported faster turnover of mustard oil during these periods, as consumers strategically blend it to manage costs. This shift has bolstered demand for both unrefined and branded refined mustard oil variants, solidifying its market position as a dependable alternative amid ongoing price volatility in competing oils.

Government drive to cut edible-oil import bill via 40% self-sufficiency plan

The government of Bangladesh is implementing a strategic initiative to reduce the edible oil import bill by achieving 40% self-sufficiency in domestic oilseed production by 2025 [3]Source: United States Department of Agriculture (USDA), "Oilseeds and Products Annual - March 18, 2025", apps.fas.usda.gov. This plan, led by the Department of Agricultural Extension (DAE), focuses on expanding mustard cultivation in coastal and haor areas and promoting intercropping between T. Aman and T. Boro rice seasons to enhance seed availability for crushers and stabilize supply chains. The policy aligns with recommendations from the October 2025 Prothom Alo-Solidaridad roundtable, which emphasized utilizing fallow and char lands for mustard, soybean, and sunflower cultivation, supported by high-yield, climate-resilient seeds, low-interest loans, crop insurance, and fair pricing mechanisms. These measures aim to address inefficiencies in processing and market volatility while fostering public-private partnerships for regenerative farming practices. Companies like Orion Group are leveraging this initiative by aligning their production with government-backed mustard cultivation zones, marketing products as "self-reliant Bengali oil" to align with policy goals and consumer sentiment. Mustard, as the leading domestic oilseed, plays a pivotal role in reducing reliance on volatile soybean and palm oil imports, while its byproducts contribute to livestock feed and rural income growth. This initiative integrates government extension services, research from institutions like BARI and Sher-e-Bangla University, and industry-scale operations, positioning mustard oil as a cornerstone of economic resilience and food security.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from cheaper imported palm oil | -0.7% | National; strongest in urban low-income segments and bulk institutional buyers | Short term (≤ 2 years) |

| Climatic and agronomic volatility in mustard seed supply | -0.5% | Coastal divisions (Khulna, Barishal); flood-prone Sylhet, Mymensingh; drought-prone Rajshahi | Medium term (2-4 years) |

| Quality, adulteration and standardization concerns | -0.4% | National, concentrated in unbranded/bulk segments; urban enforcement in Dhaka, Chattogram | Short term (≤ 2 years) |

| Fragmented mill structure and operational inefficiencies | -0.3% | Rural production zones (Rajshahi, Rangpur, Mymensingh); small-scale crushers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from cheaper imported palm oil

Competition from cheaper imported palm oil continues to create significant challenges for local mustard oil producers in Bangladesh by undercutting prices and reshaping purchasing behavior among low- to middle-income households. Imported palm oil, primarily sourced through large-scale refiners, is sold at substantially lower prices, making it an attractive option for cost-conscious consumers who traditionally relied on mustard oil for daily cooking. This price disparity reduces the perceived value of mustard oil, despite its cultural importance, stronger aroma, and suitability for traditional dishes like bhorta or fish fry, forcing consumers to choose between affordability and tradition. The growing adoption of palm oil in the hotel, restaurant, and catering sector, where cost efficiency is prioritized, further intensifies competition, leaving established mustard oil brands such as Pran and Teer struggling to maintain market share. The rise of blended edible oils, including palm-soy or palm-sunflower blends, adds complexity, as retailers promote these as economical alternatives, pushing mustard oil into a smaller, premium segment. Smaller artisanal ghani producers face additional pressure due to higher production costs, limiting their ability to compete with aggressively priced refined palm oil. Furthermore, the availability of palm oil in value-packs and refill pouches has expanded its reach in rural and peri-urban markets, weakening demand momentum for mustard oil and forcing producers to rely on heritage positioning, purity claims, and seasonal demand spikes.

Climatic and agronomic volatility in mustard seed supply

Climatic and agronomic volatility in mustard seed supply poses a significant challenge to market stability. Erratic weather conditions, including untimely heavy rains, hailstorms, and rising temperatures beyond the crop's optimal range of 10-25°C, disrupt cultivation in key regions such as Bogra, Jamalpur, and the haor areas, leading to inconsistent yields and reduced crushing throughput for both small mills and large processors. Climate change intensifies these issues, with events like flash floods (e.g., the Michaung cyclone in Jashore in December 2023) causing root rot and threatening harvests, while prolonged dry spells hinder germination. Crushers often ration production or blend with imports during lean seasons, driving up unrefined Kachi Ghani mustard oil prices and reducing competitiveness against stable palm oil imports. Pests, fungal diseases, and parasites further exacerbate risks in ecologically fragile zones like Hakaluki haor, where studies (BSMRAU 2023) highlight the need for stress-tolerant seed varieties as shifting rainfall and humidity impact pod development and oil content. Supply shortages force brands like TK Group's Pusti Mustard Oil to stockpile or enter forward contracts, squeezing margins, while rural mini-mills with limited inventory face post-harvest losses from cyclone damage. Farmers increasingly shift to safer crops like potatoes or rice, shrinking seed availability and compelling wholesalers to source adulterated alternatives. Government efforts to promote high-yield hybrids face adoption challenges due to competition with winter cash crops. Trials by BARI underscore additional threats, including salinity, evapotranspiration, and declining groundwater levels, which limit irrigation. Without resilient seeds and improved irrigation, supply volatility will persist, constraining market growth despite strong cultural demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unrefined Kachi Ghani Anchors Heritage, Refined Segment Rides Urban Shift

The unrefined (Kachi Ghani) mustard oil segment accounts for a significant market share of 55.87% in 2025, driven by strong consumer preference for cold-pressed oils. These oils are valued for their traditional pungent aroma and bioactive compounds such as lignans and tocopherols, which align with local culinary traditions. This segment benefits from its association with small-scale, handcrafted crushing methods that preserve intense flavor profiles, making it a preferred choice for homemade fish curries, pickles, and festive cooking. Brands like Square Food & Beverage’s Radhuni Pure Mustard Oil emphasize the "authentic cold-pressed" identity, appealing to rural households and urban consumers who view Kachi Ghani as a natural, minimally processed product reflecting health and cultural heritage. Despite the rise of premium and clean-label trends, the artisanal nature of this segment ensures its continued prominence, resisting competition from refined or blended oils by emphasizing superior flavor and local authenticity.

The refined mustard oil segment is expected to grow at a CAGR of 4.61% through 2031, supported by urbanization and evolving consumer preferences. Refined oils are favored for their lighter flavors, longer shelf life, and compliance with regulatory fortification mandates. This growth is driven by the expanding middle-class urban population seeking convenient, health-focused products with consistent quality for daily cooking and HoReCa applications. Innovations such as BCSIR’s sesame-mustard blended oil (SO80:MO20), with reduced erucic acid levels and balanced fatty acids, highlight the potential for blended and fortified variants. These products are gaining traction in export markets like Singapore, Bahrain, and Qatar, catering to the Bangladeshi diaspora's demand for premium, health-conscious oils. Meghna Group’s Fresh Mustard Oil brand exemplifies the blending of refined processing with "natural Bengali taste," targeting urban consumers who seek modern safety assurances alongside cultural connections. Together, refined and blended oils are emerging as a growing complement to the unrefined segment, reflecting a market shaped by heritage, health, and modernization.

By Packaging: Bottles Lead, Pouches Gain on Convenience and Cost

The bottled packaging segment held a significant 57.64% share in 2025, driven by the widespread adoption of PET bottles in sizes ranging from 80 ml sachets to 5-liter formats. These formats effectively address modern retail and household requirements. Leading brands such as PRAN Mustard Oil (under Natore Agro Ltd.), Meghna Group's Fresh Mustard Oil, ACI Pure Mustard Oil, and Wilmar's Rupchanda leverage features like tamper-evident seals, UV protection, and stackability to enhance product safety, extend shelf life, and ensure convenient storage. Bottled packaging aligns with consumer expectations for quality assurance and brand reliability, particularly in urban areas and organized retail chains. This format remains the preferred choice for both unrefined and refined mustard oil variants, driven by heightened attention to authenticity and hygiene.

Flexible pouches are rapidly gaining traction due to their cost efficiency and convenience, supported by a projected 4.39% CAGR through 2031, the highest among packaging types. The reduced resin content in pouch packaging lowers material costs, making smaller units (such as 200 ml, 250 ml, and 500 ml) more accessible to lower-income rural households. These households benefit from affordability and portability, particularly in regions with limited cold-chain infrastructure and constrained shelf space. Bulk tins and drums continue to serve institutional buyers, including HoReCa and commercial kitchens, where 15-liter jars and 15-kg tins remain cost-effective. However, increasing enforcement of vitamin A fortification regulations is driving a gradual shift toward fortified packaged oils, reflecting evolving regulatory and quality assurance requirements in the bulk edible oil segment.

By Distribution Channel: Off-Trade Dominates, On-Trade Recovers Post-Pandemic

In 2025, the off-trade distribution channel accounted for 77.95% of the total market share, reflecting the prominence of traditional retail formats in Bangladesh. This channel includes supermarkets, hypermarkets, convenience and grocery stores, specialty outlets, as well as wet markets and roadside vendors. Wet markets and roadside vendors are particularly significant in rural and semi-urban areas, where most food purchases occur. Although supermarkets and modern trade channels remain relatively small, they are steadily expanding in urban centers such as Dhaka, Chattogram, and tier-2 cities, driven by urbanization and changing consumer preferences. Online retail is also gaining traction, with platforms like Othoba, Chaldal, and Daraz incorporating mustard oil into their assortments. However, rural areas face challenges related to connectivity and logistics, limiting the reach of e-commerce. Brands such as PRAN and ACI leverage both traditional and digital off-trade channels to ensure accessibility and maintain brand visibility across diverse consumer segments.

The on-trade/HoReCa distribution channel is experiencing robust growth, with a projected compound annual growth rate (CAGR) of 4.73% through 2031, making it the fastest-growing segment. This growth is driven by increased demand from restaurants, hotels, and catering services returning to pre-pandemic levels, as well as institutional buyers such as schools, hospitals, and corporate canteens. These buyers prioritize packaged and fortified mustard oil products to meet food safety regulations and social safety standards. Brands like Meghna Group’s Fresh Mustard Oil cater to this segment with larger pack sizes and fortified options, aligning with institutional requirements and diversifying revenue streams in the evolving edible oil market.

Geography Analysis

Dhaka Division accounts for 39.88% of the 2025 mustard oil market, driven by its dense population, higher purchasing power, and advanced retail infrastructure, including supermarkets, specialty stores, and growing online platforms. These factors enhance access to packaged mustard oil products, fueling demand for premium and branded options. Consumers in this urban hub prioritize convenience, brand assurance, and variety, supporting the growth of refined and fortified mustard oils alongside traditional unrefined types. Brands such as ACI Pure Mustard Oil and Meghna Group’s Fresh Mustard Oil have strategically positioned themselves in Dhaka’s retail and e-commerce channels, catering to health-conscious and convenience-seeking segments. This approach sustains value growth despite challenges like market saturation and competition from imported oils, including palm oil.

Khulna Division is expected to achieve the fastest growth in the mustard oil market, with a projected CAGR of 5.36% through 2031. This growth is supported by agronomic advancements and government-backed initiatives to expand cultivation in coastal and haor areas, unlocking production potential in districts such as Jessore and Khulna. Efforts by the Department of Agricultural Extension to promote high-yield varieties and adaptive cropping practices further enhance seed production and supply stability, enabling local farmers to meet increasing demand.

Rajshahi Division, a historically significant mustard cultivation area, faces challenges such as yield fluctuations due to drought and groundwater depletion. However, industrial investments, including Meghna Group’s seed sourcing in Sirajganj and Bogra and PRAN-RFL’s Natore Park expansion, bolster processing capacity and mitigate production challenges. Together, these regional dynamics reflect a balance between urban demand in Dhaka and rural production growth in Khulna and Rajshahi, supported by government policies aimed at ensuring supply stability and fostering rural economic development.

Regulatory Landscape

Mustard oil sold in Bangladesh is subject to mandatory standardization and food-safety enforcement. The Bangladesh Standards and Testing Institution (BSTI) lists mustard oil under mandatory certification, anchored by the national standard for mustard oil (BDS 25:2015, Amendment-1:2020), which makes certification and compliant labeling central requirements for formal brands and packaged players.

Food safety and compositional integrity are also governed by Bangladesh’s Food Safety Act 2013, enforced by the Bangladesh Food Safety Authority (BFSA), alongside legacy provisions under the Pure Food Ordinance 1959 that require mustard oil to be derived exclusively from mustard or rape seed. On the trade side, the National Board of Revenue (NBR) issues annual tariff schedules, including the FY 2026-2027 tariff released on June 11, 2026, which shapes the cost position of imported edible oils and related inputs relative to domestically crushed mustard oil.

Value Chain Analysis

The Bangladesh mustard oil value chain typically moves from farmers to village aggregators and traders, onward to wholesale markets and oil mills (traditional Kachi Ghani and larger industrial crushers), then into packaged-oil distribution and retail. Upstream, the Department of Agricultural Extension (DAE) coordinates programs that expand mustard acreage and improve yields, while public research and seed systems involving BARI, BINA, and BADC support higher-yielding varieties (for example, Tori-7 and BARI/BINA mustard lines) that stabilize seed availability for crushers.

Midstream processing remains bifurcated, with a large informal base of local crushing mills processing a substantial share of domestic oilseeds. Leading branded players, including PRAN-RFL, City Group, ACI, Orion Group, and Partex, operate integrated sourcing, processing, packaging, and distribution for modern trade, e-commerce, and institutional channels. Recent field evidence from DAE-linked targets and production-zone reporting shows an expansion drive at farm level, including Dinajpur exceeding its mustard cultivation target in December 2025, which supports higher throughput for both mini-mills and larger plants. Bottlenecks persist around uneven access to quality seed and fertilizer, variable farmgate pricing, and logistics costs from rural production belts into Dhaka and Chattogram consumption centers.

Competitive Landscape

The mustard oil market in Bangladesh is moderately fragmented, with a market concentration score of 5 out of 10. Key players, including PRAN-RFL Group, Wilmar International (Rupchanda brand), City Group (TEER brand), ACI Limited (ACI Pure), and Meghna Group (Fresh Mustard Oil), dominate the formal sector through integrated value chains covering contract farming, crushing, refining, branding, and distribution. These companies focus on urban retail and export markets by offering branded, packaged mustard oils that emphasize quality, fortification, and traceability. In contrast, over 50% of domestic mustard seed is processed by small-to-medium mills and traditional cold-press (Kachi Ghani) units, which supply unbranded oils to rural and bulk markets. This creates a bifurcated structure where branded players target premium consumers, while fragmented mills cater to local demand.

Leading companies are prioritizing vertical integration and energy efficiency to enhance operations. For example, City Group secured a USD 10 million loan from the Asian Development Bank in May 2024 to establish a 3,000 MT/day multi-oilseed crushing facility in Narayanganj, capable of processing soybean, canola, mustard, and sunflower seeds. Additionally, a USD 10 million loan from FMO in January 2025 is being utilized to construct a bottling plant aimed at transitioning bulk oils into packaged, fortified formats. These initiatives have reduced electricity consumption by 37% and cut CO₂ emissions by 1,723 tons annually, aligning with sustainability goals while improving margins across processing and packaging stages.

Opportunities remain significant in fortification compliance and traceability. An April 2025 GAIN report highlighted that smaller brands and bulk oils often fail to meet vitamin A fortification standards. Mid-tier players can address this gap by adopting premix blending, accredited laboratory testing, and digital traceability methods such as QR codes and batch tracking. These measures can help secure institutional contracts and export certifications, enabling integrated branded players to strengthen their market position while the informal sector continues to serve traditional rural and cost-sensitive segments.

Bangladesh Mustard Oil Industry Leaders

-

PRAN-RFL Group

-

Square Food & Beverage Ltd

-

Wilmar International Ltd.

-

ACI Limited

-

City Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-linked upstream integration and compliance-led formalization are the most visible whitespace areas for branded mustard oil in Bangladesh. The government’s multi-year push to raise local edible-oil self-sufficiency to 40% by FY 2024-25 has been executed through DAE support and programs such as the Oilseed Crop Production Enhancement Project, expanding the pool of locally sourced mustard seed that processors can contract and trace. R&D also points to product opportunity beyond traditional profiles, as shown by BCSIR’s July 2024 sesame-mustard blended oil formulation, which reduced erucic acid to 4.22% (below a 5% limit) while maintaining oxidative stability.

Investment incentives and market governance changes further widen the commercial case for building domestic oilseed-based capacity and shifting bulk into packaged formats. In June 2026, the government proposed tax incentives for edible-oil producers using locally sourced oilseeds, and in July 2026 it initiated steps to bring the edible oil market under a systemic oversight framework, both of which favor compliant processors with auditable procurement and packaging lines. City Group’s financing-backed buildout, including multi-oilseed crushing and a bottling plant funded through 2024-2025 loans, and PRAN-RFL’s industrial park plans in Natore provide evidence that capacity, energy efficiency, and packaging conversion are working competitive levers. The remaining opportunity sits with mid-tier and regional players to pair contract farming and lab-verified fortification with wider off-trade distribution, including e-commerce platforms already stocking mustard oil, to capture consumers moving from loose oil to packaged SKUs.

Recent Industry Developments

- July 2026: Bangladesh initiated steps to bring the edible oil market under a systemic oversight framework. Tighter monitoring increases the advantage of brands that already run traceable procurement, lab testing, and compliant packaging versus loose and informal supply.

- March 2026: PRAN-RFL Group announced plans to establish a second industrial park in Natore, including new mustard oil production capacity. The move expands domestic processing depth in a key agro-sourcing belt and supports the company’s scale-up in branded edible oils alongside its broader agro-processing footprint.

- May 2024: The Asian Development Bank signed a USD 10 million loan agreement with Rupshi Seed Crushing Limited (City Group) to establish an energy-efficient, 3,000 MT/day multi-oilseed crushing plant in Narayanganj. The project strengthens large-scale crushing economics across mustard and other oilseeds while improving resource efficiency, supporting competitive packaged-oil supply.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of mustard oil sold for use in Bangladesh across household cooking and food-related uses, counted at the point where the product is sold into the domestic market within the study period.

Scope exclusions: It excludes mustard seeds as an agricultural commodity and any export sales that are not consumed within Bangladesh.

Segmentation Overview

-

By Product Type

- Refined Mustard Oil

- Unrefined (Kachi Ghani)

- Others (Blended/Fortified and Organic and Cold-Pressed)

-

By Packaging

- Bottles

- Pouches

- Bulk Tins/Drums

-

By Distribution Channel

- On-Trade/HoReCa

-

Off-Trade

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- Dhaka Division

- Chattogram Division

- Rajshahi Division

- Khulna Division

- Sylhet Division

- Barishal Division

- Rangpur Division

- Mymensingh Division

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the fact base around edible-oil demand, mustard seed availability, and trade exposure that can change local prices and volumes. We used public sources such as Bangladesh Bureau of Statistics releases, FAOSTAT oilseed series, UN Comtrade trade lines for related oils, and Bangladesh Bank or IMF exchange-rate histories to keep currency conversions consistent.

To convert these signals into market-ready inputs, we also reviewed company disclosures, investor materials, and association and regulator websites where edible oil and packaged food discussions are publicly available. In a few cases, paid subscriptions for company financials and an import-export shipment-level database were used to sanity-check large-volume movements and map the active supply chain. The examples listed here are illustrative only, and many other public and paid sources were also referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how mustard oil is priced and sold in Bangladesh across branded packs and loose sales, and how seasonality around mustard seed harvest affects availability. We spoke with processors, distributors, retailers, and foodservice-linked buyers in parallel to check and adjust assumptions from desk research before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 45% |

| Mid tier: 55% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 14% | Managers: 57% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using top-down logic where national edible-oil consumption signals, mustard seed availability, and domestic processing output are used to reconstruct a realistic mustard oil demand pool in value terms. The totals were then corroborated with selective bottom-up approximations, mainly through sampled retail prices by pack size, channel mix splits, and a supplier roll-up check on the larger processors that are visible in public records.

Key inputs used in the model included mustard seed production and crushing availability, the share of mustard oil in edible-oil usage, observed retail price bands across pack sizes, the split between loose and packaged sales, and currency and inflation movements that affect nominal value reporting. Where direct observations were thin, gaps were handled by using ranges validated in interviews, and then selecting a midpoint that matched at least two independent signals (for example, trade exposure and consumer price trend direction).

For forecasting, we relied on scenario analysis supported by short time series smoothing for prices, because the market is sensitive to crop-driven supply and general food inflation. Assumptions on volume growth and price progression were stress-tested with primary feedback, and the final outlook was kept consistent with macro indicators that are tracked regularly.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent indicators, and then checked for year-to-year jumps that did not align with known crop, trade, or price events. When a variance looked unusual, the underlying driver was re-opened, and respondents were re-contacted when needed to confirm whether a change was real or a data artifact.

Before sign-off, the model went through multi-step analyst review so key assumptions, conversions, and arithmetic checks were repeated by a second set of eyes. Reports are refreshed annually, and interim updates are done when a material event changes supply, pricing, or policy conditions. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Bangladesh Mustard Oil Market Size Versus Other Published Estimates

Published numbers for Bangladesh mustard oil can look far apart because the counted product scope and the pricing basis are not always the same, and because some studies mix value for loose oil with branded packaged sales without explaining the bridge. Differences also show up when one source uses a producer-level price and another uses retail pricing, which changes the final value even if volumes are similar.

The main gap comes from whether the estimate treats mustard oil as a narrow cooking oil market or as a broader mustard-related category that can pick up adjacent oils, personal care uses, or wider edible-oil value pools. Some sources also apply aggressive price growth year after year, even when the local crop cycle and import-linked edible-oil prices move in a more uneven pattern. In Mordor Intelligence's model, the market is counted as mustard oil sold into Bangladesh with a clear separation of domestic consumption from non-domestic flows, and pricing is cross-checked by pack-size retail bands so value does not get overstated by single-point assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 463.01 M (2025) | |

| Industry Research House A | USD 168.00 M (2025) | This estimate appears to apply a narrower counted basket or a different pricing point (closer to producer or factory gate), which can undercount retail value and miss loose-market turnover. |

| Analytics Publisher B | USD 1.35 B (2024) | The value is much higher, which often happens when mustard oil is grouped with adjacent edible oils or when high retail pricing is applied broadly without matching it to the realistic mustard oil volume base in-country. |

The table shows that the spread is mostly explained by what is included in the counted pool and how prices are applied to volumes, rather than by a true disagreement on demand direction. By keeping assumptions traceable to crop-linked supply signals, observed price bands, and channel realities, the final market value stays easier to reproduce and update each year.

Key Questions Answered in the Report

How big is the Bangladesh Mustard Oil Market in 2026?

The market stands at USD 478.98 million in 2026 and is forecast to grow to USD 567.45 million by 2031.

Which product style sells the most?

Unrefined Kachi Ghani leads with 55.87% 2025 share due to its strong culinary heritage.

What packaging type is gaining fastest?

Lightweight pouches are projected to grow at a 4.39% CAGR to 2031 on convenience and lower cost.

Which region shows the highest growth through 2031?

Khulna Division is expected to rise at a 5.36% CAGR, helped by coastal land repurposing and high-yield varieties.

Page last updated on: