Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

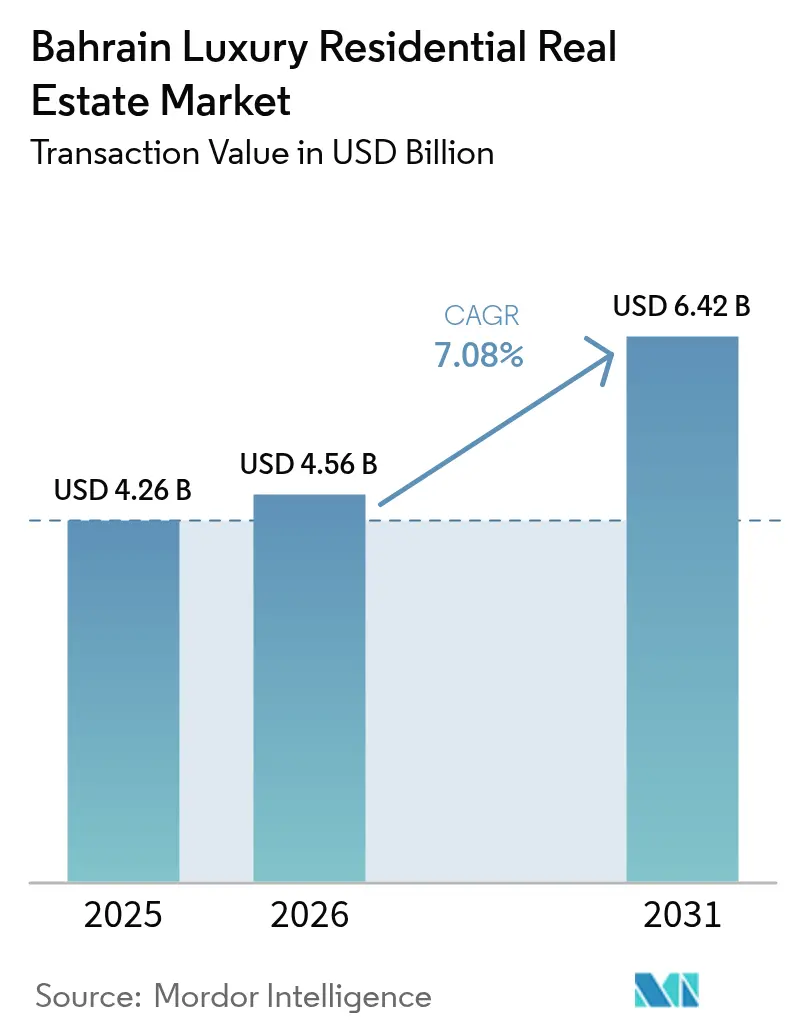

| Base Year Market Size (2025) | USD 4.26 Billion |

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

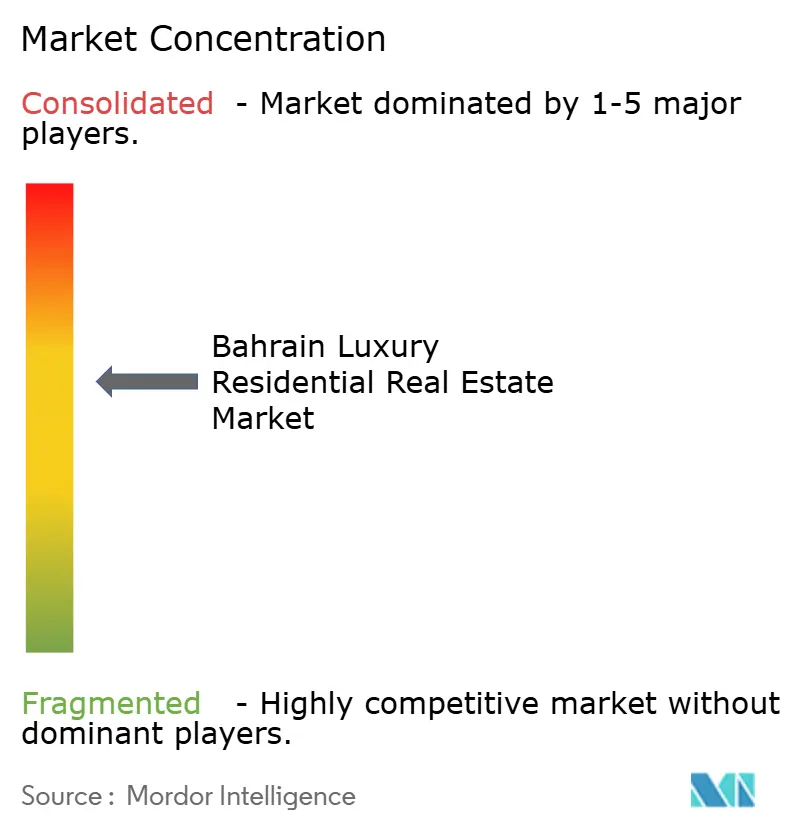

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Bahrain luxury residential real estate market size was valued at USD 4.26 billion in 2025 and estimated to grow from USD 4.56 billion in 2026 to reach USD 6.42 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). Rising cross-border wealth inflows, 100% foreign-ownership reforms, and a USD 30 billion national infrastructure pipeline are expanding the addressable premium-property pool and helping the Bahrain luxury residential real estate market capture investors who previously focused on neighboring hubs. Development activity now concentrates on large waterfront master plans, while banking-sector credit growth and falling borrowing costs underpin a steady pipeline of new projects. At the same time, tighter AML/KYC rules and climate-related insurance costs inject short-term friction, prompting buyers to favor reputable developers with strong compliance records. Overall, the market’s maturation is reshaping pricing power, supply strategies, and competitive positioning across districts.

Key Report Takeaways

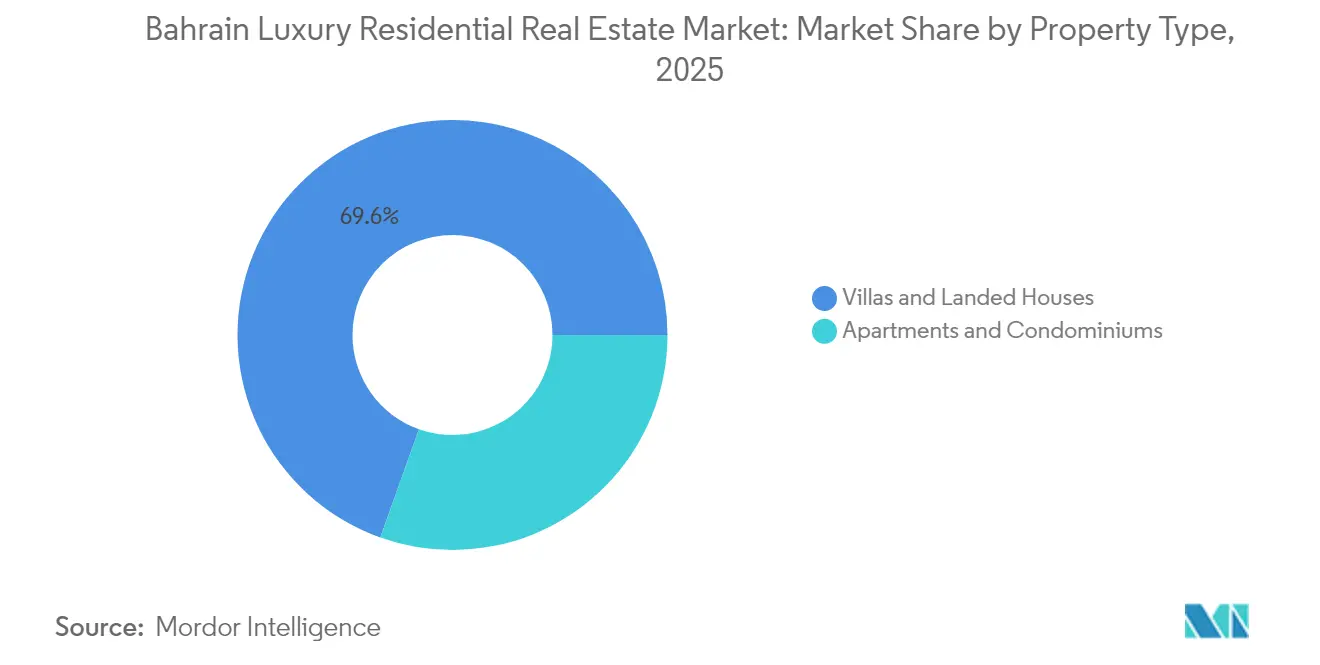

- By property type, villas and landed houses led with 69.55% of the Bahrain luxury residential real estate market share in 2025. The Bahrain luxury residential real estate market for apartments and condominiums is projected to post a 7.65% CAGR between 2026-2031.

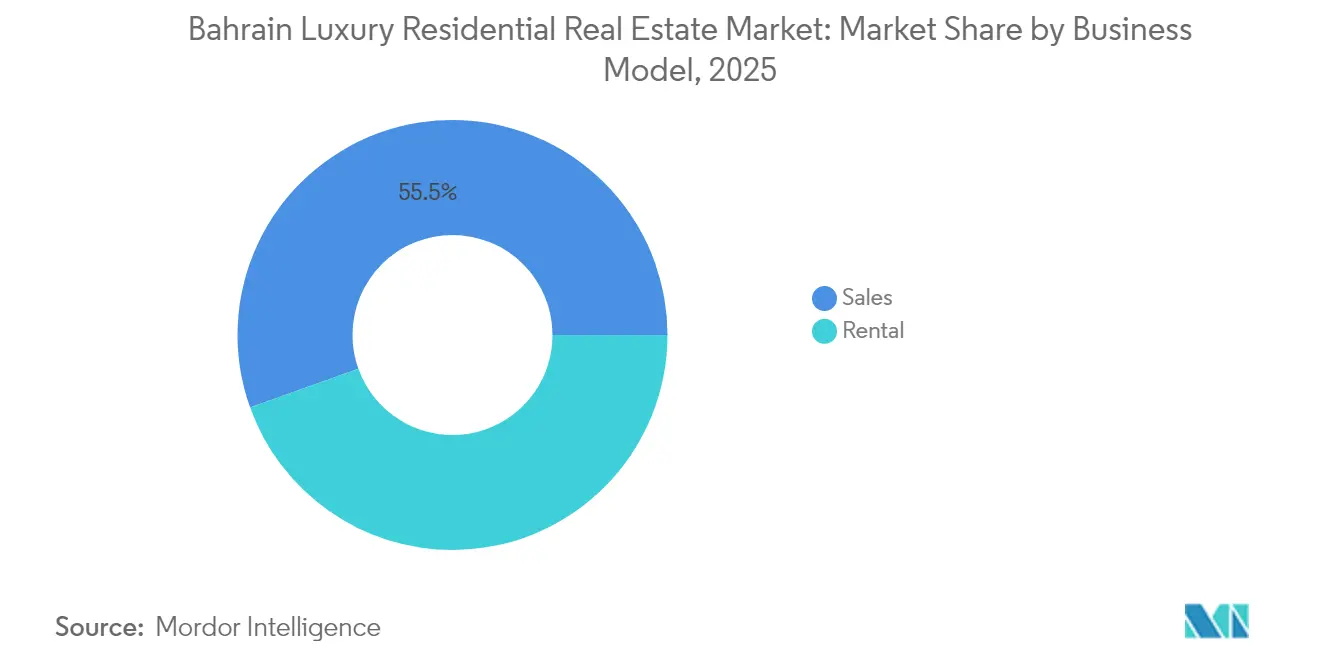

- By business model, the sales segment commanded 55.48% of the Bahrain luxury residential real estate market size in 2025. The Bahrain luxury residential real estate market for rentals is set to expand at 8.21% CAGR between 2026-2031.

- By mode of sale, secondary resale transactions captured 62.45% share of the Bahrain luxury residential real estate market size in 2025. The Bahrain luxury residential real estate market for primary new-build sales is growing at an 7.78% CAGR between 2026-2031.

- By geography, Manama accounted for 31.10% of the Bahrain luxury residential real estate market share in 2025. The Bahrain luxury residential real estate market for the Northern Governorate is projected to register the fastest 8.43% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising GCC & local HNWI population and wealth creation | +1.8% | GCC-wide, concentrated in Manama and Muharraq | Medium term (2-4 years) |

| 100% foreign-ownership reforms & Golden-Visa initiatives | +1.5% | National, strongest in waterfront districts | Short term (≤ 2 years) |

| Mega waterfront master-plans unlocking premium inventory | +1.2% | Manama, Muharraq, Northern Governorate | Long term (≥ 4 years) |

| Bahrain Metro & King Hamad Causeway boosting connectivity | +0.9% | Manama to Northern Governorate corridor | Medium term (2-4 years) |

| Emergence of branded-residence projects raises price ceiling | +0.7% | Premium districts, Bahrain Bay, Juffair | Medium term (2-4 years) |

| Blockchain-enabled real-estate tokenization is widening investor pool | +0.4% | National, early adoption in luxury segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising GCC & Local HNWI Population Driving Premium Demand

The Middle East added 2.7% more high-net-worth individuals in 2024, and nearly 10% of them now control wealth above USD 100 million, expanding the regional buyer pool for trophy homes in Bahrain. Record inward migration of 6,700 millionaires to the UAE during 2024 triggered a spill-over effect, pushing fresh capital into nearby markets that offer geographic and regulatory diversification. Capgemini’s 2024 World Wealth Report shows 65% of HNWIs intend to raise allocations to private equity and alternative assets, a trend that directs new money toward yield-bearing luxury residences. Buyers with multigenerational wealth focus on location, privacy, and long-term value rather than price, helping waterfront villas in Bahrain Bay achieve pre-sales exceeding 80% before ground-breaking. This steady inflow of affluent households keeps premium asking prices firm, even when mid-tier segments feel rate pressure, and supports a positive outlook for the Bahrain luxury residential real estate market.

100% Foreign-Ownership Reforms Eliminating Investment Barriers

Legislation that allows 100% foreign ownership of real estate, coupled with a Golden Visa available for property investments of USD 530,000 or more, removes historic shareholding restrictions and opens Bahrain to truly global capital. The Economic Development Board calculates that operating costs are 27% lower than in rival GCC financial hubs, adding an extra incentive for overseas buyers seeking both a home and a regional business base[1]Bahrain Economic Development Board, “Cost of Doing Business in Bahrain,” edb.gov.bh. Timed alongside tighter wealth taxes in older offshore centers, the reform positions Bahrain as a safe, cost-efficient domicile for family offices looking to relocate. Early evidence shows rising enquiries from European and Asian investors who previously overlooked the Kingdom due to joint-venture requirements. As confidence builds around the new rule set, developers report faster absorption of premium waterfront launches, reinforcing near-term price resilience in the Bahrain luxury residential real estate market.

Mega Waterfront Master-Plans Creating Premium Inventory

Projects such as Bahrain Bay and Diyar Al Muharraq integrate residential towers, retail promenades, and five-star hotels, enabling developers to charge 20-30% premiums versus comparable inland sites. These master plans answer modern buyer preferences for gated security, walkable amenities, and mixed-use convenience that single-plot villas rarely provide. Waterfront scarcity further underpins pricing, since only a limited coastline meets zoning and environmental standards for high-density luxury builds[2]Middle East Institute, “Climate Risk and Coastal Development in the GCC,” mei.edu . Climate-adapted design, including elevated podiums and flood-resistant utilities, is now a selling point that attracts ESG-focused investors. Together, these large-scale schemes broaden Bahrain’s luxury supply while sustaining high values for the best-located plots.

Infrastructure Connectivity Expanding Accessible Premium Locations

Phase 1 of the USD 2 billion Bahrain Metro will add 29 kilometers of track and 20 stations, slashing travel times between the Northern Governorate and Manama’s financial center. In parallel, the USD 3.5 billion King Hamad Causeway will improve road access to Saudi Arabia, enlarging Bahrain’s commuter and investor catchment area. Better connectivity lets developers market larger waterfront homes at price points below core-district levels, stimulating an 8.85% CAGR forecast for Northern Governorate luxury sales. Walkability and reduced car dependence also resonate with younger expatriates who value sustainable mobility. These transit upgrades, therefore, extend the prime map and lift long-term demand across multiple districts.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sticky high mortgage rates & tighter bank lending | -0.8% | National, affecting mid-tier luxury segments | Short term (≤ 2 years) |

| Demand–supply mismatch in secondary districts | -0.6% | Secondary districts outside Manama core | Medium term (2-4 years) |

| Rising coastal-risk insurance premia on waterfront assets | -0.4% | Waterfront developments, Northern coastline | Long term (≥ 4 years) |

| Enhanced AML/KYC scrutiny limiting anonymous offshore capital | -0.3% | National, concentrated in ultra-luxury segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mortgage Rate Volatility Constraining Financing-Dependent Buyers

Although headline borrowing costs are easing, lenders still price risk conservatively, leaving many mid-tier luxury buyers exposed to rate swings that complicate budgeting for USD 1-3 million homes. Stricter underwriting standards lengthen approval cycles, which frustrate time-sensitive purchases and occasionally lead to deal cancellations. Consolidation in GCC banking reduces the number of competitors willing to negotiate bespoke mortgage terms. Cash-rich investors remain active, but financing headwinds temporarily dampen momentum in segments where leverage often covers 60-70% of the ticket size. Developers respond with staged payment plans to bridge the gap, yet overall absorption in rate-sensitive brackets stays uneven.

Enhanced AML/KYC Compliance Extending Transaction Timelines

Regional regulators have tightened anti-money-laundering checks, pushing closing periods for cross-border deals from roughly 45 days to as much as 90 days, especially when offshore entities or crypto funds are involved. Mandatory disclosure of beneficial ownership deters buyers who value anonymity, diverting some ultra-luxury demand to other jurisdictions. Developers equipped with robust compliance teams can still process high-value deals efficiently, whereas smaller firms struggle with document backlogs. Bahrain’s OneID digital identity program will streamline future verification steps, yet temporary friction persists. Over time, stricter rules should enhance market credibility, but in the short run, they act as a speed bump for the uppermost price tiers of the Bahrain luxury residential real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Villas Retain Primacy but Apartments Accelerate

Villas and landed houses captured 69.55% of the Bahrain luxury residential real estate market share in 2025, reflecting entrenched cultural preferences for privacy, multigenerational layouts, and outdoor space. Traditional buyers, especially GCC family offices, continue to view villa plots as a safe-haven asset that can appreciate alongside land scarcity in Manama’s core districts. Several waterfront villa clusters inside Diyar Al Muharraq recorded pre-sales above 80% in 2024, underscoring the depth of demand for large detached residences.Apartments and condominiums post the fastest 7.65% CAGR forecast through 2031, mirroring demographic shifts toward younger HNWIs, expatriate executives, and international professionals who prioritize turnkey convenience. Projects such as the 186-unit Kempinski Residences at Bahrain Harbor weave hotel-style services with branded privacy, drawing investors willing to pay premium rates for managed yields. Developers now add townhouse-style duplexes, private elevators, and rooftop terraces to high-rise offerings, thus narrowing perceived lifestyle gaps between villas and vertical living. This evolution positions the apartment segment as a viable upmarket alternative, especially where villa land is scarce or prohibitively.

By Business Model: Ownership Dominates but Rentals Gain Traction

A 55.48% share of the Bahrain luxury residential real estate market size still lies in outright sales, as legacy investors regard freehold title as both a status symbol and a hedge against regional currency fluctuations. Large family offices prefer completing block purchases in early construction phases, locking in custom specifications and transferring units across generations. The longevity of freehold demand should sustain primary revenues for integrated developers such as Eagle Hills, which often bundle marina berths or club memberships to reinforce premium positioning.Rental-oriented strategies, however, show an 8.21% CAGR through 2031, reflecting an emerging yield play by global HNWIs who aim to balance portfolio risk. Corporate tenancy demand rises as Bahrain strengthens its role as a financial-services bridge between Saudi Arabia and the wider MENA region, pushing expatriate executives toward fully serviced residences. The dual-hotel agreement signed by Indian Hotels Company to open Taj properties in Hamala and Seef will add branded inventory that can be flexibly leased, illustrating how hotel brands import hospitality skill sets into the Bahrain luxury residential real estate market. Forward-looking landlords now structure medium-term serviced-apartment leases that track corporate assignment cycles, producing steady cash flows that rival global real-estate investment trusts.

By Mode of Sale: Secondary Resale Prevails but Primary Sales Accelerate

Secondary transactions represented 62.45% of market turnover in 2025, buoyed by ready-for-occupancy inventory around Seef, Juffair, and older Manama precincts. Cash buyers favor properties with proven rental histories, especially those aligned with diplomatic enclaves and Grade-A offices that ensure constant expatriate occupancy. Resellers also capitalize on the liquidity premium afforded by transparent title records and mature community infrastructure.Primary new-build deals, projected to expand at 7.78% CAGR through 2031, reflect developer-led land-bank consolidation and disciplined phased releases. Onyx SkyView’s recent sell-out of two penthouse floors ahead of ground-breaking signals revived confidence in off-plan purchasing for technologically advanced green buildings. Many new schemes integrate smart-home systems, LEED or BREEAM certifications, and blockchain-enabled fractional ownership, which collectively widen the Bahrain luxury residential real estate market investor pool. Government net-zero goals and buyer awareness of operating-cost differentials are nudging demand toward these contemporary green developments.

Geography Analysis

Manama maintained a 31.10% share of premium transactions in 2025 because its Seef, Diplomatic Area, and Bahrain Bay sub-markets bundle financial-district access with high-end retail, dining, and marina infrastructure. Occupancy levels in flagship towers such as Harbor Heights remain above 90%, reflecting sustained demand from bankers, consultants, and multinational executives. The sales cycle is typically shorter in Manama than in outlying districts because buyers can benchmark pricing across multiple mature comparable markets.

Northern Governorate is the fastest-growing luxury corridor, clocking an 8.43% CAGR forecast through 2031. Master-planned waterfront projects such as Water Garden City appeal to cross-border Saudi professionals who commute via the King Hamad Causeway, scheduled for phased opening before 2030. Developers exploit lower land-acquisition costs to offer larger footprints and private beachfronts at price points 15-20% below central Manama, while the upcoming metro stations anchor future resale values.

Muharraq and Juffair continue to attract distinct buyer profiles. The culturally rich Muharraq Island positions luxury villas alongside UNESCO-listed heritage zones, combining lifestyle authenticity with yacht access via the expanded marinas. Juffair, located adjacent to the US Naval Support Activity base and major embassies, draws high-income expatriates who prioritize short commutes to international schools and retail malls. Both districts enjoy resilient rental streams that encourage investors seeking predictable yields within the Bahrain luxury residential real estate market.

Competitive Landscape

Competition remains moderate but intensifying as top developers assemble land banks and integrate construction, sales, and property-management functions. Diyar Al Muharraq recently consolidated two adjacent plots to create a contiguous 12 million sq ft waterfront canvas, enhancing economies of scale in utilities, landscaping, and security provisioning. Eagle Hills, for its part, partnered with local contractors to de-risk supply-chain bottlenecks and accelerate handover timelines in its Marassi Al Bahrain precinct.

Strategic alliances between real-estate firms and hospitality brands now serve as a quality signal. Kempinski’s management agreement for Bahrain Harbour residences introduces European concierge standards, compelling local developers to uplift service packages that include valet, housekeeping, and membership privileges. Similarly, Taj’s entry validates Bahrain’s ability to command ADR-linked residential premiums, nudging competing schemes to differentiate via wellness centers, private beach clubs, or Michelin-aligned dining.

Technology adoption marks another competitive divider. Several mid-size developers launched blockchain tokenization portals in 2025 that enable fractional unit purchases starting at USD 50,000 equivalents, thereby democratizing participation in the Bahrain luxury residential real estate market. Early movers leverage smart contracts for automated dividend distribution and secondary trading, while laggards still rely on manual escrow frameworks that slow settlement. Rising compliance costs further tilt the field toward capital-rich incumbents capable of absorbing AML/KYC system investments.

Bahrain Luxury Residential Real Estate Industry Leaders

Diyar Al Muharraq

Bin Faqeeh

Eagle Hills / Marassi Al Bahrain

Naseej B.S.C

Durrat Khaleej Al Bahrain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The Ministry of Industry and Commerce introduced a one-stop commercial bank account service at Bahrain Financial Harbor and through the Sijilat portal, shortening developer onboarding and deal settlement timeframes.

- January 2025: A Domestic Minimum Top-up Tax on multinational enterprises with global revenues exceeding EUR 750 million (USD 877.64 million) came into force, aligning Bahrain with OECD pillars while preserving tax advantages for individual property buyers.

- September 2024: Mumtalakat and M42 announced the expansion of Amana Healthcare Bahrain, with operations commencing in 2025, bolstering premium healthcare access and reinforcing residential demand from affluent medical tourists.

- August 2024: Indian Hotels Company signed a dual-hotel agreement to develop 251-room and 200-room Taj properties in Hamala and Downtown Seef, respectively, marking its first foray into Bahrain’s luxury hospitality-residential hybrid space.

Bahrain Luxury Residential Real Estate Market Report Scope

Luxury residential real estate refers to properties that are exclusively designed for human occupation and that provide charm and resort life with high-end amenities. A complete background analysis of the Bahrain luxury residential real estate market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Bahrain luxury residential real estate market is segmented by type (apartments and condominiums, villas, and landed houses) and by key cities (Manama, Muharraq, Juffair, and the rest of Bahrain).

The report offers market size and forecast values (in USD) for all the above segments.

By Property Type

| Apartments and Condominiums |

| Villas and Landed Houses |

By Business Model

| Sales |

| Rental |

By Mode of Sale

| Primary (New-build) |

| Secondary (Resale) |

By Key District

| Manama |

| Muharraq |

| Juffair |

| Northern Governorate |

| Rest of Bahrain |

| By Property Type | Apartments and Condominiums |

| Villas and Landed Houses | |

| By Business Model | Sales |

| Rental | |

| By Mode of Sale | Primary (New-build) |

| Secondary (Resale) | |

| By Key District | Manama |

| Muharraq | |

| Juffair | |

| Northern Governorate | |

| Rest of Bahrain |

Key Questions Answered in the Report

What is the current value of the Bahrain luxury residential real estate market?

The market is valued at USD 4.56 billion in 2026 and is expected to reach USD 6.42 billion by 2031.

Which property type holds the largest share?

Villas and landed houses dominate with 69.55% market share as of 2025.

Which segment is growing the fastest?

Apartments and condominiums show the highest forecast growth at a 7.65% CAGR through 2031.

Why is Northern Governorate considered an emerging hotspot?

Large waterfront master plans and improved connectivity via the upcoming metro and King Hamad Causeway underpin an 8.43% CAGR forecast in the district.

How are AML/KYC regulations affecting high-value transactions?

Stricter compliance now extends closing timelines to as much as 90 days, particularly for ultra-luxury deals involving complex offshore structures.

What role do branded residences play in the market?

Branded residences introduce hotel-level services and professional management, lifting achievable price points and attracting yield-driven global investors.

Page last updated on: