Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

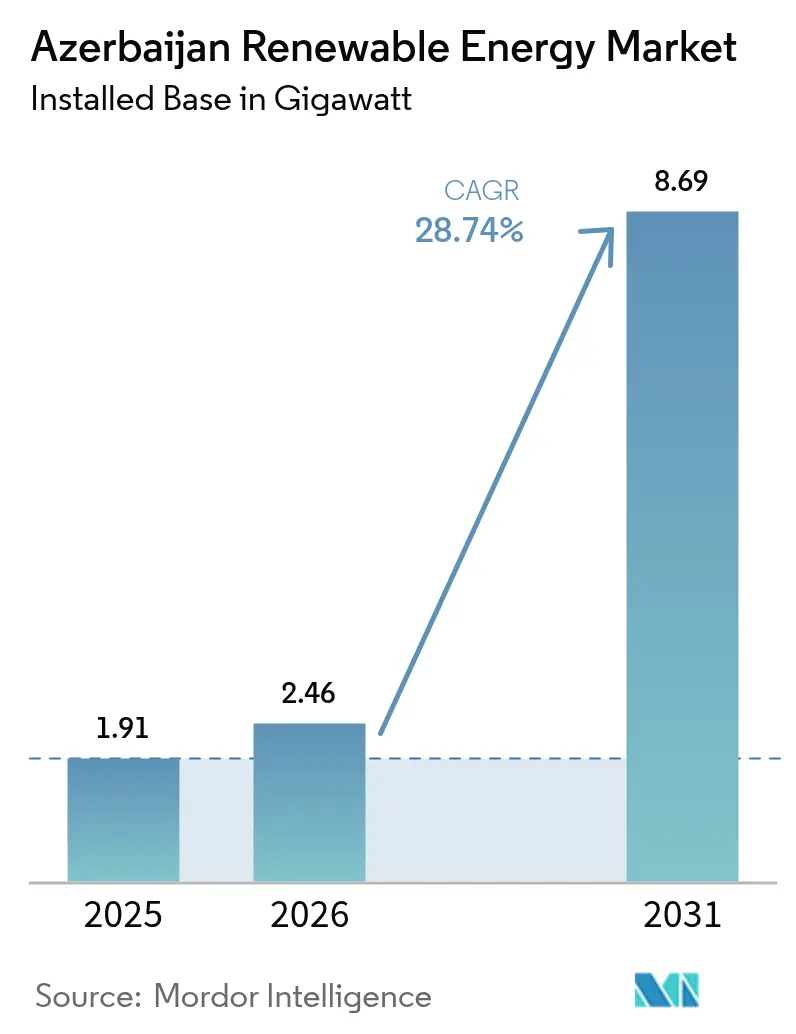

| Base Year Market Size (2025) | 1.91 gigawatt |

| Market Volume (2026) | 2.46 gigawatt |

| Market Volume (2031) | 8.69 gigawatt |

| Growth Rate (2026 - 2031) | 28.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Azerbaijan Renewable Energy Market Analysis by Mordor Intelligence

The Azerbaijan Renewable Energy Market size is expected to grow from 1.91 gigawatt in 2025 to 2.46 gigawatt in 2026 and is forecast to reach 8.69 gigawatt by 2031 at 28.74% CAGR over 2026-2031.

Abundant solar and wind resources, mounting foreign direct investment, and the government’s 30% renewable capacity target are accelerating deployment. Hosting COP29 in Baku in 2024 has also amplified global visibility and unlocked concessional finance. Major developers, including Masdar, ACWA Power, bp, and SOCAR Green, have committed more than USD 1 billion through 2025, signaling confidence in long-term power-purchase agreements (PPAs) backed by sovereign guarantees. Planned undersea high-voltage direct-current (HVDC) cables linking Caspian renewable generation to European grids promise an export avenue that mirrors the Southern Gas Corridor, supporting Azerbaijan’s dual strategy of freeing domestic gas for export and diversifying the national energy mix. However, ageing Soviet-era transmission assets, gas-price subsidies, and land-use conflicts in liberated Karabakh pose near-term execution risks.[1]COP29 Presidency, “Baku Finance Goal Outcome Document,” cop29.az

Key Report Takeaways

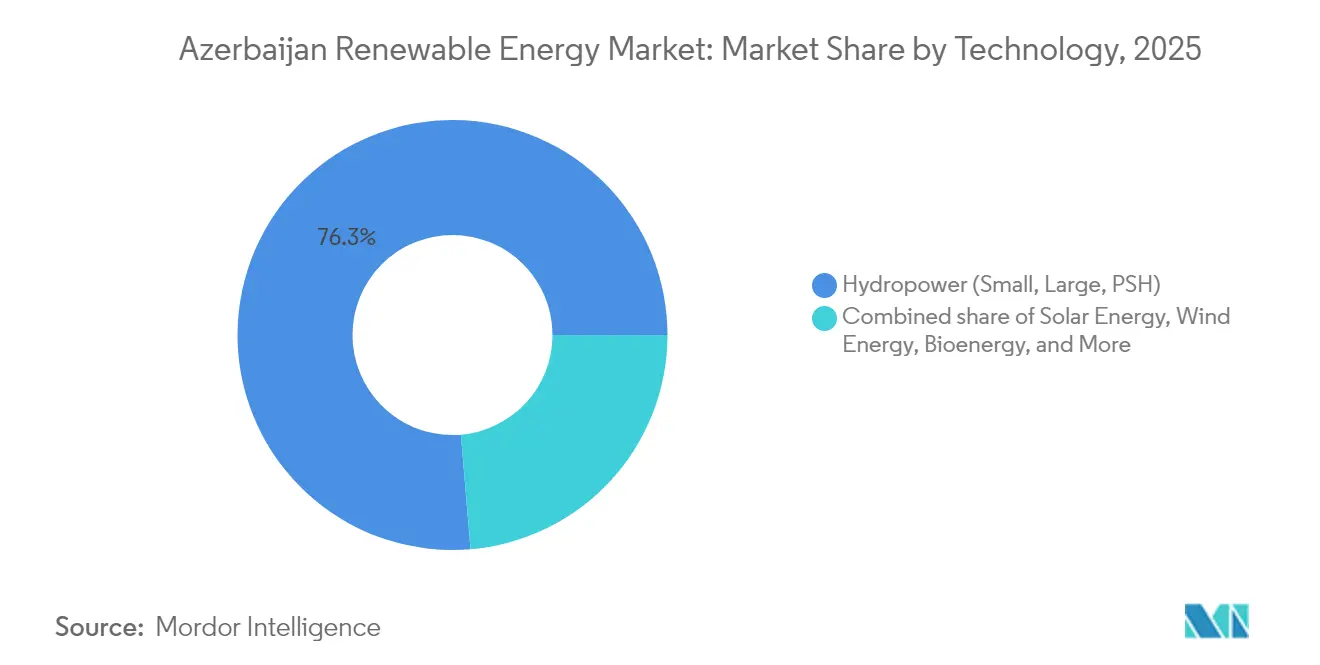

- By technology, hydropower led with a 76.34% share of the Azerbaijan renewable energy market in 2025, while solar is forecast to expand at a 62.4% CAGR through 2031.

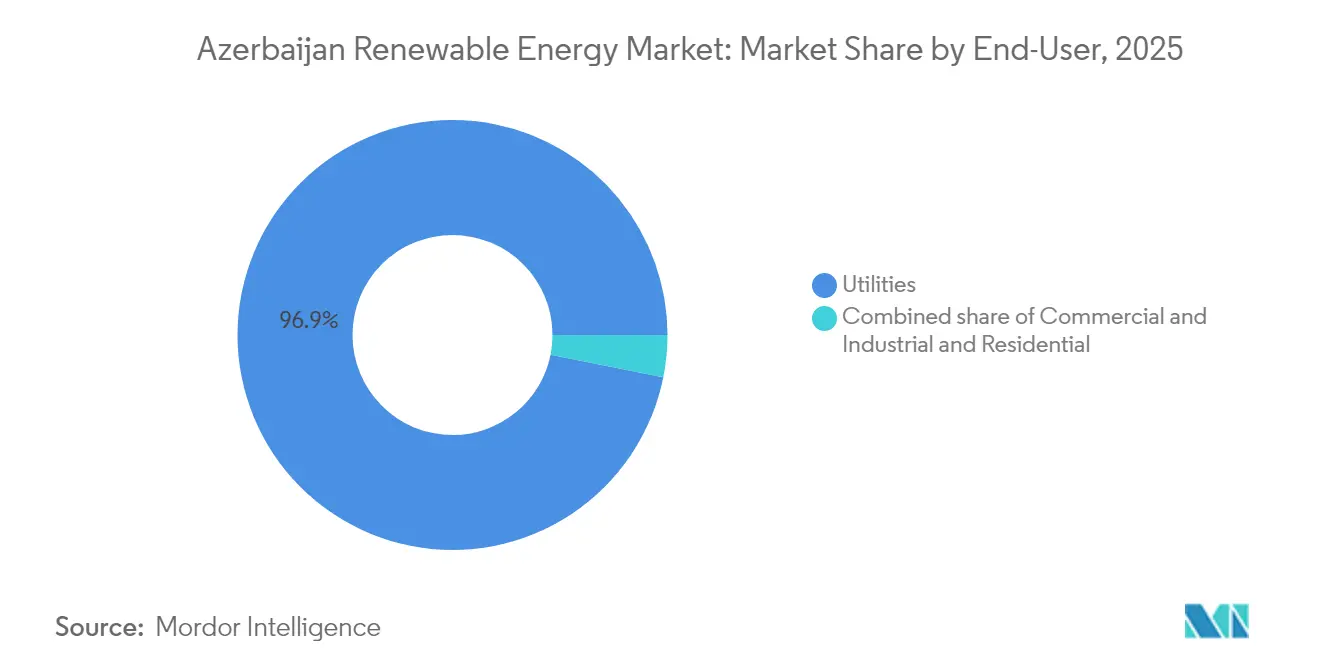

- By end-user, utilities held 96.85% of the Azerbaijan renewable energy market share in 2025, whereas residential capacity is projected to grow at a 38.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Azerbaijan Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 30% renewable-capacity target by 2030 | +8.00% | National, with priority zones in Absheron, Karabakh, Nakhchivan | Medium term (2-4 years) |

| Abundant solar & wind resources (135 GW onshore, 157 GW offshore) | +6.50% | National, offshore Caspian concentrated in shallow-water zones | Long term (≥ 4 years) |

| Foreign IPP inflows & long-term PPAs (Masdar, ACWA, bp) | +7.50% | National, early concentration in Absheron, Bilasuvar, Jabrayil | Short term (≤ 2 years) |

| EU-bound Green Energy Corridor export opportunity | +4.50% | National, with transmission infrastructure linking Caspian to Black Sea | Long term (≥ 4 years) |

| Hosting COP29 catalyzes climate finance access | +3.00% | National, with spillover to regional Caucasus initiatives | Short term (≤ 2 years) |

| Digital-oilfield know-how lowers RE O&M costs | +2.50% | National, leveraging SOCAR and bp operational expertise | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

30% Renewable-capacity Target by 2030

The target requires 1,500 MW of new builds beyond existing assets. Competitive auctions, fixed-price tariffs, and sovereign guarantees have de-risked financing, as evidenced by the 100 MW solar lot clearing at USD 0.0354 per kWh during COP29.[2]European Bank for Reconstruction and Development, “Azerbaijan Renewables Auction Results,” ebrd.com Presidential guidance states that 1,300 MW will be operating by 2027, accelerating deployment ahead of the statutory deadline. Developers value the law’s stability because it aligns with the period in which oil production enters decline. Multilateral agencies have since underwritten 1.2 GW of projects, signalling strong lender confidence. The framework, therefore, anchors predictable demand for equipment and services within the Azerbaijan renewable energy market.

Abundant Solar & Wind Resources

The country’s 292 GW total technical potential surpasses domestic demand by an order of magnitude. Insolation peaks at 1,600 to 2,000 kWh/m² annually on the Absheron Peninsula, supporting capacity factors near 20%. Offshore wind potential reaches 157 GW in shallow Caspian waters, which already host existing energy infrastructure, thereby lowering balance-of-plant costs through shared logistics. Meteorological data indicate complementary generation profiles between onshore wind and solar, enabling higher aggregate utilisation. These endowments underpin the long-range growth path of the Azerbaijan renewable energy market.

Foreign IPP Inflows & Long-term PPAs

Masdar, ACWA Power, and bp collectively pledged more than USD 5.3 billion for new plants during 2024.[3]Asian Development Bank, “Masdar Bilasuvar Solar Financing,” adb.org Tenor-matched PPAs hedge currency risk, while virtual swaps allow bp to deliver power to its Sangachal terminal without building dedicated lines. Local manufacturing clauses foster job creation as Baker Hughes establishes a centre of excellence for renewable systems. Cost reductions arising from global procurement pipelines improve auction competitiveness and keep the Azerbaijan renewable energy market on its forecast trajectory.

EU-bound Green Energy Corridor export opportunity

A 1,200 km HVDC link is under feasibility review to send 1,000 MW of clean power through Georgia to Romania and Hungary. The corridor monetises offshore wind volumes that exceed local demand, diversifies export earnings beyond gas, and strengthens Azerbaijan’s role in European energy security. Anticipated wheeling revenues uplift project internal rates of return, incentivising earlier investment decisions for large-scale wind farms. Alignment with the EU’s REPowerEU agenda increases grant eligibility and reduces credit-spread premiums for corridor-tied projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing grid & limited inter-connector capacity | -5.00% | National, acute in Absheron and Karabakh transmission corridors | Short term (≤ 2 years) |

| Gas-price subsidies distort RE competitiveness | -3.50% | National, particularly affecting industrial and residential tariffs | Medium term (2-4 years) |

| Auction & permitting delays | -2.00% | National, concentrated in AREA and Ministry of Energy approval workflows | Short term (≤ 2 years) |

| Land-use conflicts in liberated Karabakh | -1.50% | Karabakh and East Zangezur regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing grid & limited inter-connector capacity

Soviet-era equipment hinders the integration of variable renewables, with line losses still exceeding 9%. Reconstructed substations in liberated districts lag demand growth, delaying plant energisation dates. International loans are funding digital substation rollouts that follow IEC 61850 standards, yet completion is expected to stretch past 2030. Insufficient cross-border transfer capacity also limits export of surplus generation, tempering the near-term scale-up of the Azerbaijan renewable energy market.

Gas-price Subsidies Distort Competitiveness

Natural-gas subsidies equalled almost 2% of GDP in 2018 and continue to cap retail tariffs.[4]Organisation for Economic Co-operation and Development, “Fossil Fuel Support Data,” oecd.org Cheap gas electricity narrows the cost gap with renewables, complicating project bankability for distributed systems. The government aims for ga radual subsidy rollback to safeguard household budgets, but timing uncertainty still weighs on PPA negotiations. Clarity on subsidy reform is therefore essential for unlocking the full potential of the Azerbaijan renewable energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar Ascendancy Amid Hydropower Legacy

Solar capacity is projected to climb from 0.39 GW in 2025 to 3.72 GW by 2031, a 62.4% CAGR that outpaces every other segment. Masdar's Bilasuvar and Neftchala parks are expected to increase the installed photovoltaics to nearly 15% of Azerbaijan's renewable energy market size by 2027. Hydropower's 1.46 GW base secures the largest share, yet its growth flattens as prime river sites are saturated. Pumped-storage feasibility work with PowerChina signals a shift toward flexibility assets, which are essential for higher solar penetration.

The Azerbaijan renewable energy market share for wind is expected to accelerate once ACWA Power's 240 MW onshore plant enters service in 2025, followed by Masdar's phased 2 GW offshore rollout. Offshore foundations, port logistics, and grid reinforcements will keep early-stage capacity modest, but floating-platform technology can unlock deep-water potential post-2028. Bioenergy remains dormant despite 380 MW of agricultural residue feedstock, reflecting the absence of feed-in tariffs and supply-chain fragmentation.

By End-User: Utility Monopoly Meets Residential Awakening

Utilities account for nearly the entire size of the Azerbaijan renewable energy market today, anchored by Azerenerji’s single-buyer model. In the long term, residential prosumers supported by net-metering pilots in Baku and Ganja are expected to chip away at the monopoly as rooftop system costs fall below USD 600/kW.

The Azerbaijan renewable energy market share for residential users is projected to reach 3.25% by 2031 under the World Bank’s high-deployment scenario. Commercial and industrial uptake will remain limited until gas subsidies are phased out or virtual PPA frameworks emerge that allow wheeling.

Geography Analysis

The Absheron Peninsula and the Baku-Sumgayit corridor are the primary locations for new builds, as grid capacity, load density, and brownfield land converge to offer low integration costs. The Caspian offshore zones hold a technical potential of 157 GW, and early seabed surveys inform the design of floating platforms. Western districts are leveraging proximity to Georgia for the planned EU Green Energy Corridor, which will open a 1,000 MW export route, thereby enhancing project cash flows.

The Nakhchivan Autonomous Republic operates an isolated grid but eyes cross-border swaps with Türkiye and Iran that would monetise solar peaks while improving local reliability. Liberated Karabakh receives Presidential backing as a designated green energy zone, with AZN 2.36 million earmarked for integrated master plans. The Smart Village in Zangilan demonstrates how hybrid microgrids can rebuild rural economies.

Mountainous north-west districts explore small hydro and biomass, creating a diversified regional resource mix. Coastal communities are investigating floating solar energy where land is scarce. This spatial spread distributes employment and supports nationwide uptake, reinforcing resilience across the Azerbaijan renewable energy market.

Competitive Landscape

The market remains moderately fragmented, with Masdar, ACWA Power, and bp leading utility pipelines while SOCAR and Azerenerji provide state backing. International firms supply technology and finance, and joint ventures ensure local capacity building. Developers differentiate themselves through digital asset management, as evidenced by Baker Hughes' installation of electric submersible pumps adapted for renewable water-pumping duties.

Cost curves decline as global module prices fall and lenders accept Azerbaijan's sovereign guarantees. Early movers secure prime sites near existing substations, creating barriers for late entrants. Technology suppliers, such as Siemens Gamesa and Vestas, position themselves for upcoming offshore wind rounds, while local steel fabricators target balance-of-plant work.

White-space niches appear in battery storage integration, demand-response software, and community solar services. Policy clarity on subsidy withdrawal and grid codes will influence relative advantage. Strategic partnerships continue to shape the Azerbaijan renewable energy market.

Azerbaijan Renewable Energy Industry Leaders

Azerenerji JSC

Abu Dhabi Future Energy Company PJSC (Masdar)

ACWA Power

bp Azerbaijan (Shafag Solar JV)

SOCAR Renewables

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Masdar's two solar power plants in Azerbaijan, each boasting a capacity of 760 MW, had received a combined financing of USD 480 million, with the EBRD, ADB, and AIIB each contributing USD 160 million. This investment stands as the most significant renewable energy financing in Azerbaijan's history. Situated in Bilasuvar and Neftchala, these projects align with Azerbaijan's ambition to derive 30% of its electricity from renewable sources by 2030.

- November 2024: Universal International Holding clinched a 100 MW solar power project in Azerbaijan's inaugural renewable energy auction. Situated in the Garadagh region, the project was won with a competitive bid of USD 0.0354 per kWh. This significant announcement was made at the COP29 climate summit, held in Baku. The solar project is slated to commence operations in 2027.

- November 2024: At COP29, the Baku Finance Goal was unveiled, targeting the mobilization of USD 1.3 trillion each year for global climate initiatives by 2035. This ambitious target is one of several agreements forged at the conference, which also saw the Fund for Loss and Damage being put into operation. Commonly referred to as the New Collective Quantified Goal (NCQG), the Baku Finance Goal sets a primary benchmark of USD 300 billion annually, prioritizing the needs of the least developed nations and Small Island Developing States.

- June 2024: In a significant move, the President of Azerbaijan inaugurated a series of renewable energy projects in the country, boasting a combined capacity of 1 GW. These projects, a collaboration between Masdar and SOCAR, encompass the Bilasuvar Solar PV Project (445MW), the Neftchala Solar PV Project (315MW), and the Absheron-Garadagh Onshore Wind Project (240MW).

Azerbaijan Renewable Energy Market Report Scope

Renewable energy is derived from natural sources that replenish faster than they are consumed, such as sunlight, wind, water, geothermal heat, and biomass. These resources are considered inexhaustible and are used to generate electricity, heat, and fuel, typically resulting in a lower carbon footprint and reduced environmental impact compared to fossil fuels.

The Azerbaijan Renewable Energy Market is segmented by technology and end-user. By technology, the market is segmented into Solar Energy (PV and CSP), Wind Energy (Onshore and Offshore), Hydropower (Small, Large, and PSH), Bioenergy, Geothermal, and Ocean Energy (Tidal and Wave). By end user, the market is segmented into Utilities, Commercial and Industrial, and Residential. The report also covers the market size and forecasts for Azerbaijan.

For each segment, market sizing and forecasts have been conducted based on installed capacity (GW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

How large will installed renewables be in Azerbaijan by 2031?

Total capacity is forecast to reach 8.69 GW, up from 1.91 GW in 2025, underpinned by a 28.74% CAGR.

Which technology is growing fastest?

Solar is projected to expand at a 62.4% CAGR, driven by record-low module prices and bankable PPAs.

What role will offshore wind play?

Up to 2 GW is under feasibility study for shallow-water sites, with long-term potential of 157 GW across the Caspian Sea.

Why is the Green Energy Corridor important?

The corridor could export 5-10 GW of renewable electricity to Europe, diversifying revenue and supporting EU energy security.

What are the main barriers to investment?

Ageing grid infrastructure, gas-price subsidies, and permitting delays currently restrain deployment speed.

Who are the leading developers?

Masdar, ACWA Power, bp, and SOCAR Green hold the largest project pipelines and long-term PPAs.

Page last updated on: