Axial And Mixed Flow Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

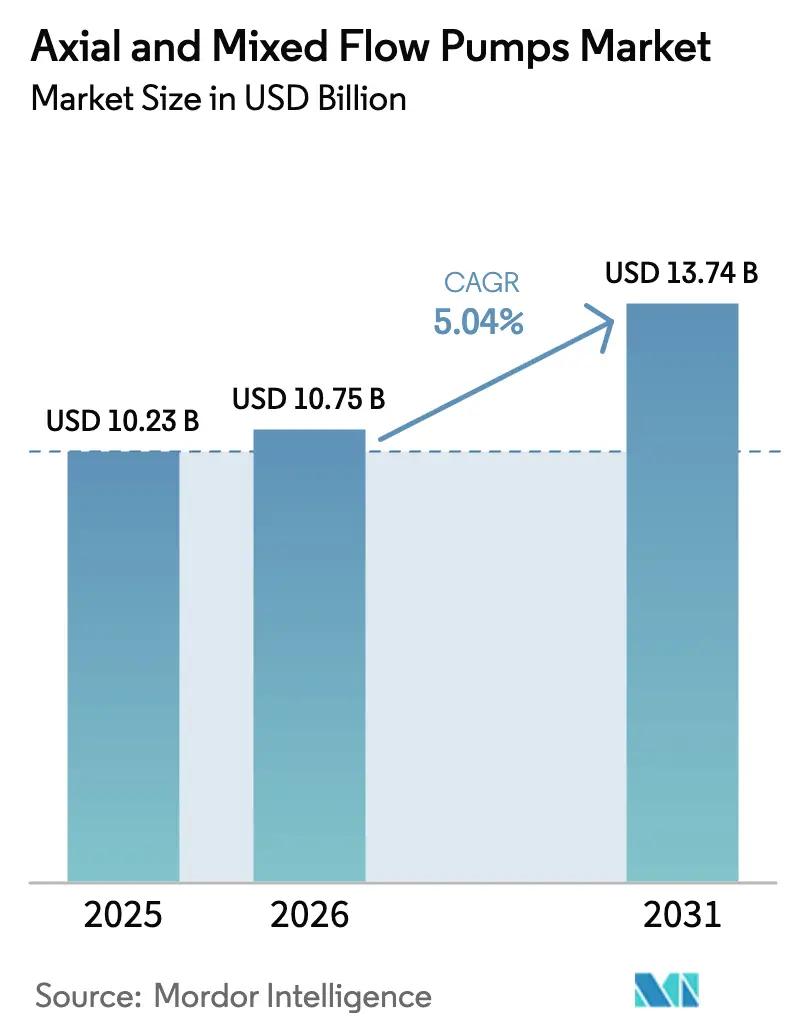

| Market Size (2026) | USD 10.75 Billion |

| Market Size (2031) | USD 13.74 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Axial And Mixed Flow Pumps Market Analysis by Mordor Intelligence

The axial and mixed flow pumps market size in 2026 is estimated at USD 10.75 billion, growing from 2025 value of USD 10.23 billion with 2031 projections showing USD 13.74 billion, growing at 5.04% CAGR over 2026-2031. This trajectory reflects escalating upgrades to water and wastewater networks, power plant cooling loops, and oil pipeline booster stations across both mature and emerging economies. Competitive positioning increasingly hinges on variable-speed technology that lowers lifetime operating costs, while digital monitoring platforms help utilities trim unplanned downtime. Rapid urbanization in the Asia-Pacific amplifies flood-control spending, whereas North American operators channel capital into modernizing crude-oil corridors subject to stricter reliability standards. Supply chain risk for high-alloy components remains a watch point, yet manufacturers are partially offsetting price volatility through backward integration and regionalized sourcing.

Key Report Takeaways

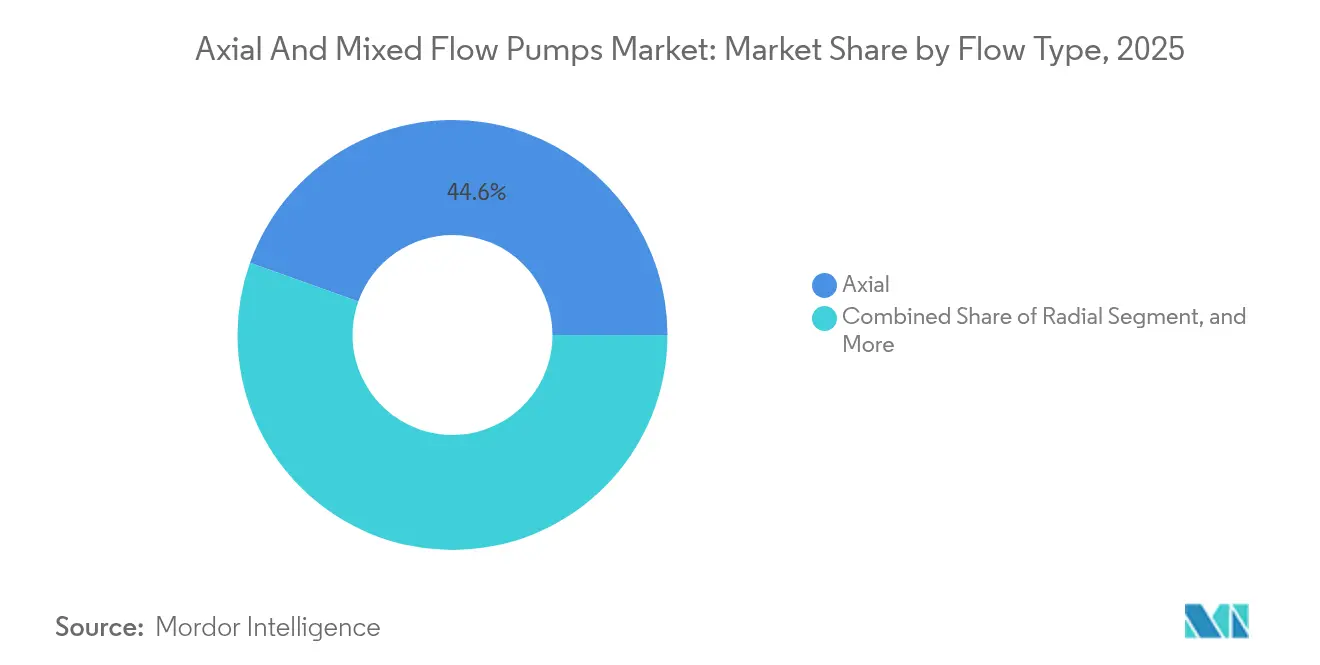

- By flow type, mixed flow pumps are expected to advance at a 6.78% CAGR through 2031, while axial flow designs are projected to retain a 44.55% revenue share in 2025.

- By number of stages, multi-stage units recorded the fastest 6.9% CAGR, whereas single-stage models held 60.74% of the 2025 demand.

- By installation orientation, vertical arrangements captured 69.12% of 2025 sales, while horizontal systems grew at a 5.96% CAGR.

- By end-user industry, power generation logged a 5.28% CAGR, as water and wastewater accounted for 33.12% of 2025 consumption.

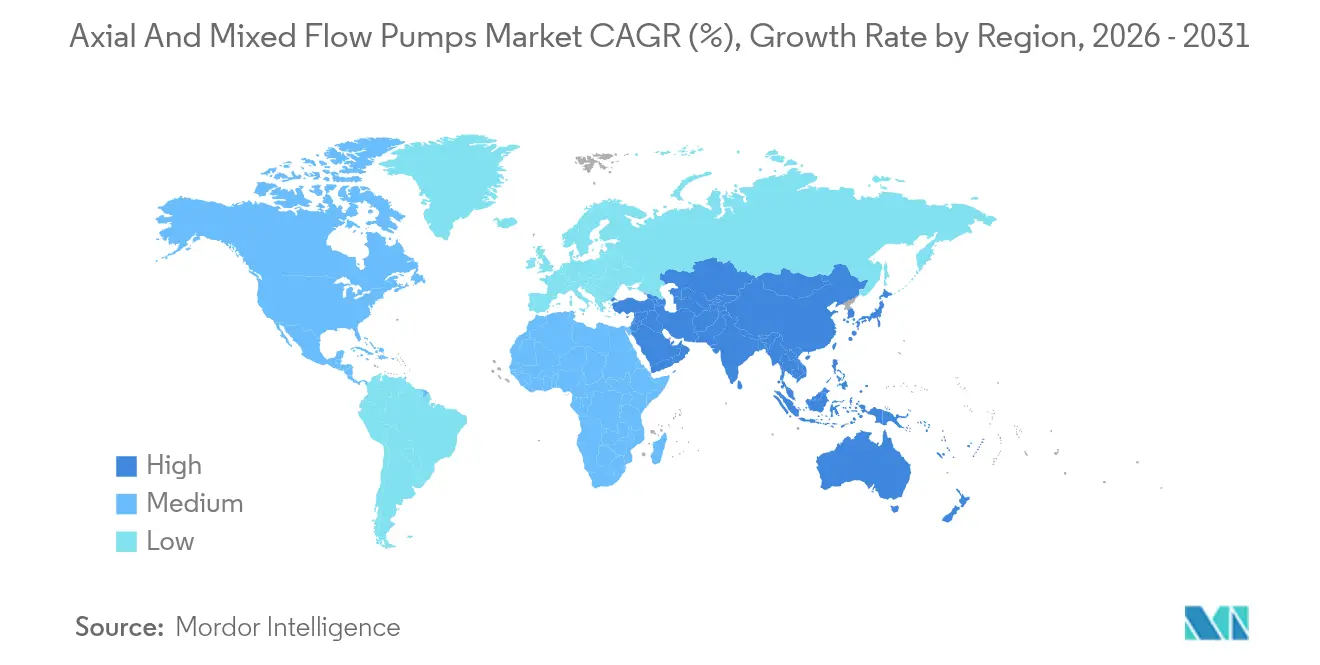

- By geography, the Asia-Pacific region commanded 43.52% of 2025 revenues and exhibited a top 5.78% CAGR trajectory to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Axial And Mixed Flow Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of municipal water and wastewater infrastructure | +1.8% | Global, early gains in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Increasing investments in oil and gas midstream projects | +1.2% | North America and Middle East core, spill-over to South America | Short term (≤ 2 years) |

| Accelerated urban flood control and irrigation schemes | +1.0% | Asia-Pacific core, spill-over to Africa | Medium term (2-4 years) |

| Adoption of variable speed drive axial pumps for wave energy converters | +0.4% | Global coastal regions, early gains in Europe and Australia | Long term (≥ 4 years) |

| Surging demand for seawater source heat pump systems | +0.3% | Global coastal cities, concentrated in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rise of modular pump stations for data center liquid cooling loops | +0.4% | Global, early gains in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Municipal Water and Wastewater Infrastructure

Spending on water supply and treatment upgrades is increasing as aging pipes and treatment facilities reach the end of their lifespan, while emerging nations scale up their capacity to support growing urban populations. Projects such as Singapore’s NEWater expansion rely on large-bore axial flow pumps to manage high-volume seawater intakes efficiently.[1]International Organization for Standardization, “ISO 14046 Environmental Management—Water Footprint,” iso.org Variable-speed drives trim energy consumption by 15-25%, a decisive benefit for utilities facing carbon-reduction mandates. The government stimulus exceeding USD 200 billion in the Asia-Pacific region during 2024 is translating directly into tender pipelines for high-capacity units. Manufacturers that can bundle pumps, motors, and digital monitoring platforms are best positioned to capture repeat orders as utilities adopt lifecycle-service contracts.

Increasing Investments in Oil and Gas Midstream Projects

North American operators invested USD 15 billion in 2024 pipeline upgrades, culminating in the USD 34 billion Trans Mountain expansion, which specified axial flow pump stations rated for use in mountainous terrain. Compliance with API 610 encourages buyers to opt for robust designs that maintain a mean-time-between-failure of over 60,000 hours.[2]American Petroleum Institute, “API Standard 610,” api.org Latin American shale programs, typified by Argentina’s Vaca Muerta, require similar pumping systems to move 500,000 barrels per day. High throughput and tight uptime targets continue to favor axial configurations over centrifugal alternatives in these midstream links.

Accelerated Urban Flood Control and Irrigation Schemes in Asia-Pacific

Intensifying rainfall events are spurring megacity drainage programs, which feature stations equipped with axial pumps sized for more than 200 m³/s, as seen in Tokyo’s underground flood tunnels.[3]Tokyo Metropolitan Government, “Flood Control in Tokyo,” metro.tokyo.lg.jp India’s Jal Jeevan Mission allocates USD 50 billion for rural water supply, promoting the adoption of mixed flow in canal rehabilitation. Governments pair hardware upgrades with IoT telemetry that modulates pump speed in real-time, curbing energy use during dry seasons and preventing overflow during storms.

Adoption of Variable Speed Drive Axial Pumps for Wave Energy Converters

Demonstration plants in Scotland and Australia utilize axial pumps to regulate seawater movement within oscillating water column devices, thereby enhancing conversion efficiency across varying wave heights. IEC 62600 guidelines recommend corrosion-resistant alloys and magnetic bearings, which reduce maintenance visits in harsh marine environments. Although niche today, cumulative installations along European and Asia-Pacific coastlines point to emerging long-term demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance limitations with high-viscosity fluids | -0.8% | Global, concentrated in chemicals and pharmaceuticals | Short term (≤ 2 years) |

| Rising prevalence of alternative inline propeller pump designs | -0.6% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Supply chain disruptions for high-alloy stainless steel components | -0.4% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Escalating energy efficiency regulations increasing compliance costs | -0.3% | Europe and North America core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Limitations with High-Viscosity Fluids

When viscosity exceeds 100 cP, axial and mixed flow pumps lose up to 30% of their efficiency, prompting chemical producers to opt for magnetic-drive centrifugal models that maintain output across a broader range of fluid properties. Pharmaceutical plants tied to FDA Part 11 cleaning codes further retreat from axial designs due to sanitization complexities. Until new impeller geometries or drive technologies reverse efficiency penalties, penetration in viscous-fluid verticals will lag core water and energy markets.

Rising Prevalence of Alternative Inline Propeller Pump Designs

Inline propeller pumps reduce footprint and civil works costs by 20-40%, making them attractive for retrofits where constructing deep sumps is impractical. European utilities pioneering these systems point to easier above-ground maintenance and faster installation. Manufacturers of axial and mixed-flow equipment must therefore defend their share by coupling efficiency gains with life-cycle service contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flow Type: Mixed Flow Drives Innovation

The axial and mixed flow pumps market size for mixed flow configurations is growing rapidly as users seek efficiency across a range of heads. Mixed flow products recorded a 6.78% CAGR through 2031, although axial designs still controlled 44.55% of 2025 revenues. Cooling-water circuits in gas and nuclear plants are increasingly opting for mixed-flow units that maintain hydraulic stability over a range of 5 m to 15 m heads. Operators report energy savings of up to 8% against pure axial alternatives when load swings are frequent. Continued R&D into variable-pitch impellers and composite casings aims to further narrow cost gaps, reinforcing the mixed flow growth arc.

Robust municipal flood-control deployments also illustrate the migration of technology. Tokyo’s new underground reservoirs utilized mixed-flow pumps to accommodate fluctuating stormwater levels, demonstrating steady throughput even as suction heads changed dramatically. Standardization under ISO 9906 test procedures builds buyer confidence by validating performance across broader duty points, thereby accelerating the adoption of mixed flow in both greenfield and retrofit packages.

By Number of Stages: Multi-Stage Systems Gain Momentum

Single-stage assemblies dominated the axial and mixed flow pumps market share, accounting for 60.74% in 2025, which is favored for simplicity in low-head water treatment and irrigation applications. Yet multi-stage lines expanded at a 6.9% CAGR, propelled by rising head requirements at nuclear stations that now target 50–100 m discharge pressures. Multi-stage designs also anchor pipeline booster stations, where elevation changes strain the limits of single-stage designs. Manufacturers mitigate higher capital costs by modularizing casings, allowing operators to add stages as demand grows without the need to reinstall entire units.

The Trans Mountain project integrated multi-stage axial pumps in its mid-line stations to offset mountain passes, demonstrating favorable lifecycle economics under heavy-oil duty cycles. Predictive analytics, combined with pressure sensors, alerts technicians to stage-imbalance drift before vibration escalates, supporting higher availability targets within critical energy corridors.

By Installation Orientation: Vertical Dominance Continues

Vertical pumps accounted for 69.12% of 2025 sales, thanks to their compact footprints that suit tight municipal vaults. Submerging motors underwater cuts airborne noise and frees surface area for other treatment equipment. Nonetheless, horizontal builds advanced at a 5.96% CAGR as industrial campuses favored above-grade access for faster inspection cycles. Data centers deploying liquid cooling loops illustrate the shift; horizontally mounted skids slide out for maintenance without disrupting server halls.

Oil pipelines reflect this trend; surface-mounted booster stations along desert routes simplify maintenance and minimize confined-space hazards. Saudi Arabia’s NEOM desalination works specified horizontal axial pumps for modular plant blocks, where cranes lift out entire skid assemblies for overhaul. Occupational safety legislation also encourages owners to adopt lay-flat layouts when worker entry into deep, wet pits is avoidable.

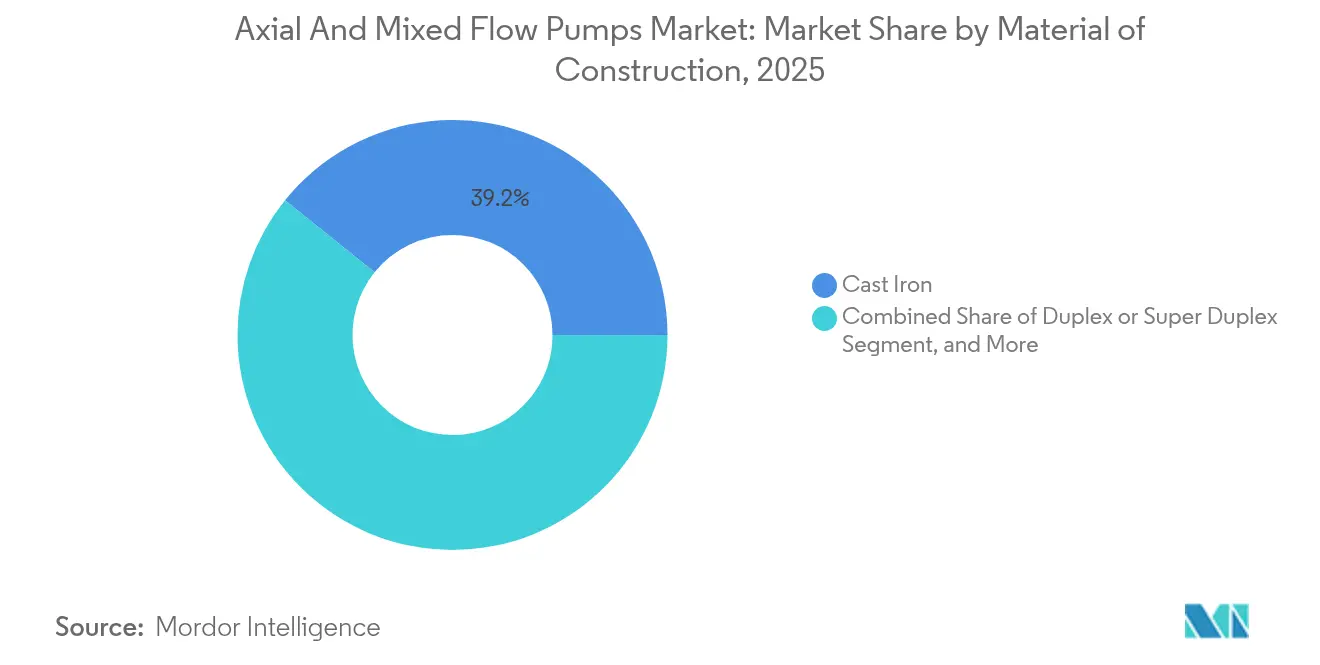

By Material of Construction: Stainless Steel Gains Ground

Cast-iron casings retained 39.22% of the 2025 volume on cost merit for freshwater service, whereas stainless steel grades climbed at a 5.59% CAGR amid the spread of seawater and corrosive industrial duties. The axial and mixed flow pumps market size for duplex stainless pumps benefited from offshore oil and desalination capex that demands 25% chromium alloys to curb pitting. Nickel price swings increased 316L cost by 25% in 2024, but operators tolerated premiums given that replacement expenses topped USD 1 million per unplanned outage.

OEMs respond by dual-sourcing billets and machining near end-markets to buffer logistics disruptions. Some also experiment with ceramic liners in high-sand river intakes to cut abrasion, further expanding the material palette beyond classic ferrous metallurgy.

By End-User Industry: Power Generation Accelerates

Water and wastewater schemes captured 33.12% of the 2025 demand and remain the anchor customer group; however, power generation is positioned as the fastest ascender, with a 5.28% CAGR. Utilities modernizing their nuclear fleets are adopting axial cooling-water pumps capable of moving more than 100,000 m³/h continuously. Renewable-heavy grids echo this need for flexible flow control in pumped-storage hydro and solar thermal storage loops. Meanwhile, chemical plants continue redirecting viscous streams toward centrifugal designs, moderating their growth contribution.

Construction projects in Southeast Asia utilize temporary axial dewatering packages to expedite basement excavation during the monsoon months. Mining operators specify duplex casings and hard-faced impellers to handle abrasive tailings water, representing a niche yet technically demanding slice that rewards specialized vendors.

Geography Analysis

The Asia-Pacific region retained 43.52% of 2025 expenditures and is pacing forward at a 5.78% CAGR as megacities strengthen flood protection, rural districts expand potable water networks, and industrial corridors equip energy megaprojects. China has earmarked USD 50 billion for drainage tunnels that integrate high-capacity axial sets, while India’s Jal Jeevan Mission channels pump orders to over 2,000 regional contractors. Southeast Asian nations, led by Vietnam and the Philippines, secured multilateral funding that bundles variable-speed drives with smart telemetry to meet efficiency targets.

North America holds an entrenched share through oil-pipeline refurbishments and municipal rehabilitations that address aging infrastructure. The axial and mixed flow pumps market share in this region benefits from API-compliant builds, which are demanded by publicly traded pipeline operators that cannot risk environmental penalties. U.S. water utilities face USD 625 billion of capital replacements over two decades, ensuring a recurring order funnel even as federal funding cycles fluctuate. Europe prioritizes energy efficiency and carbon budgets. Utilities are adopting IE5 motors, paired with digital twins that simulate flooding scenarios before hardware installation, a practice reinforced by EU taxonomy rules. Coastal cities from Spain to Denmark trial seawater-source heat pumps, each requiring corrosion-resistant axial units. Meanwhile, demand in the Middle East and Africa escalates through desalination and petrochemical expansions, with megaprojects such as NEOM validating premium stainless duplex materials. South America, although smaller, is experiencing steady growth from mining and onshore LNG developments that rely on axial booster pumps to transport process water over challenging terrain.

Competitive Landscape

The axial and mixed flow pumps market is moderately consolidated, with a cadre of global manufacturers holding notable project portfolios yet leaving room for regional specialists. Top companies bundle hydraulics, electric motors, and PLC-based controls into turnkey packages, raising the technical threshold for new entrants. Xylem’s USD 7.5 billion purchase of Evoqua broadened its treatment and pumping lineup, allowing municipal bidders to source complete systems from a single vendor. KSB’s USD 150 million expansion in Pune bolsters domestic capacity to serve Indian irrigation tenders without import delays. Sulzer’s USD 75 million NEOM award underscores deep-water expertise and material science leadership.

Technology rivalry now centers on energy-efficiency curves and predictive analytics. OEMs embed vibration sensors and cloud apps that alert crews to early bearing wear, targeting a 40% cut in unplanned downtime. Magnetic bearings that eliminate oil-based lubrication are gaining traction for wave-energy and remote-pipeline duties, promising 20-year design lives with scant maintenance. Platform vendors also form alliances with engineering, procurement, and construction contractors, securing influence at the specification stage where pump footprints, motor ratings, and civil works budgets are finalized.

Regional challengers still thrive by customizing packages for niche codes or offering rapid onsite service. Chinese suppliers, backed by joint ventures with companies like Flowserve, deliver price-competitive units into Belt and Road pipeline corridors. European mid-tier firms capture retrofits by packaging inline propeller alternatives that slot into existing shafts. Despite intensified consolidation, differentiated hydraulic modeling, field support, and material specialization create diverse pathways for both incumbents and newcomers.

Axial And Mixed Flow Pumps Industry Leaders

Xylem Inc.

Franklin Electric Co., Inc.

Sulzer Ltd

Kubota Corporation

Pentair plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Grundfos launched an AI-enabled predictive maintenance platform developed with Microsoft Azure, allowing municipal utilities to forecast bearing wear in axial and mixed flow pumps up to 60 days before vibration thresholds are exceeded.

- July 2025: Sulzer opened an additive-manufacturing facility in Texas dedicated to 3-meter titanium impellers for multi-stage axial pumps, reducing production lead times by 40% and enabling rapid spare-part delivery for North American pipeline operators.

- April 2025: ANDRITZ introduced a super-duplex stainless steel mixed flow pump series rated for 700,000 m³ per day seawater intake, extending mean time between overhauls to 10 years in high-chloride environments.

- January 2025: Xylem commissioned the first fully digital axial flow pump station under Singapore’s NEWater expansion, integrating edge analytics that cut energy use by 18% versus the previous fixed-speed installation.

Global Axial And Mixed Flow Pumps Market Report Scope

Axial flow pumps are of the propeller type, in which the rotation of the impeller forces the water forward axially and do not strictly qualify as centrifugal pumps. At the same time, mixed flow pumps act partly by centrifugal action and partly by propeller action, with the impeller blades being twisted to some degree.

The Axial And Mixed Flow Pumps Market Report is Segmented by Flow Type (Axial, Radial, Mixed), Number of Stages (Single Stage, and Multi Stage), Installation Orientation (Vertical, and Horizontal), Material of Construction (Cast Iron, Stainless Steel, and More), End-User Industry (Oil and Gas, Water and Wastewater, Power Generation, Chemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Axial |

| Radial |

| Mixed |

| Single Stage |

| Multi Stage |

| Vertical |

| Horizontal |

| Cast Iron |

| Stainless Steel |

| Duplex or Super Duplex |

| Other Material of Construction |

| Oil and Gas |

| Water and Wastewater |

| Power Generation |

| Chemicals |

| Food and Beverage |

| Pharmaceuticals |

| Metals and Mining |

| Construction |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Flow Type | Axial | ||

| Radial | |||

| Mixed | |||

| By Number of Stages | Single Stage | ||

| Multi Stage | |||

| By Installation Orientation | Vertical | ||

| Horizontal | |||

| By Material of Construction | Cast Iron | ||

| Stainless Steel | |||

| Duplex or Super Duplex | |||

| Other Material of Construction | |||

| By End-User Industry | Oil and Gas | ||

| Water and Wastewater | |||

| Power Generation | |||

| Chemicals | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Metals and Mining | |||

| Construction | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the axial and mixed flow pumps market in 2026?

The market reached USD 10.75 billion in 2026 and is projected to climb to USD 13.74 billion by 2031.

Which region leads current demand for axial and mixed flow pumps?

Asia-Pacific holds 43.52% of global 2025 revenues, driven by major water and flood-control projects.

What is the fastest-growing end-user segment for these pumps?

Power generation shows the highest 5.28% CAGR because nuclear and renewable facilities require larger cooling-water capacities.

Why are mixed flow pumps gaining popularity?

Mixed flow designs maintain higher efficiency across variable head conditions, making them ideal for power-plant cooling and urban flood-control systems.

What technologies are improving pump reliability?

Variable-speed drives, IoT-based predictive maintenance, and magnetic bearings all extend service life while cutting energy use.

How are energy regulations impacting pump selection?

Stricter efficiency rules are pushing utilities to choose variable-speed axial pumps that meet IE5 motor classes and reduce operating costs.

Page last updated on: