Automotive LiDAR Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 32.09% CAGR |

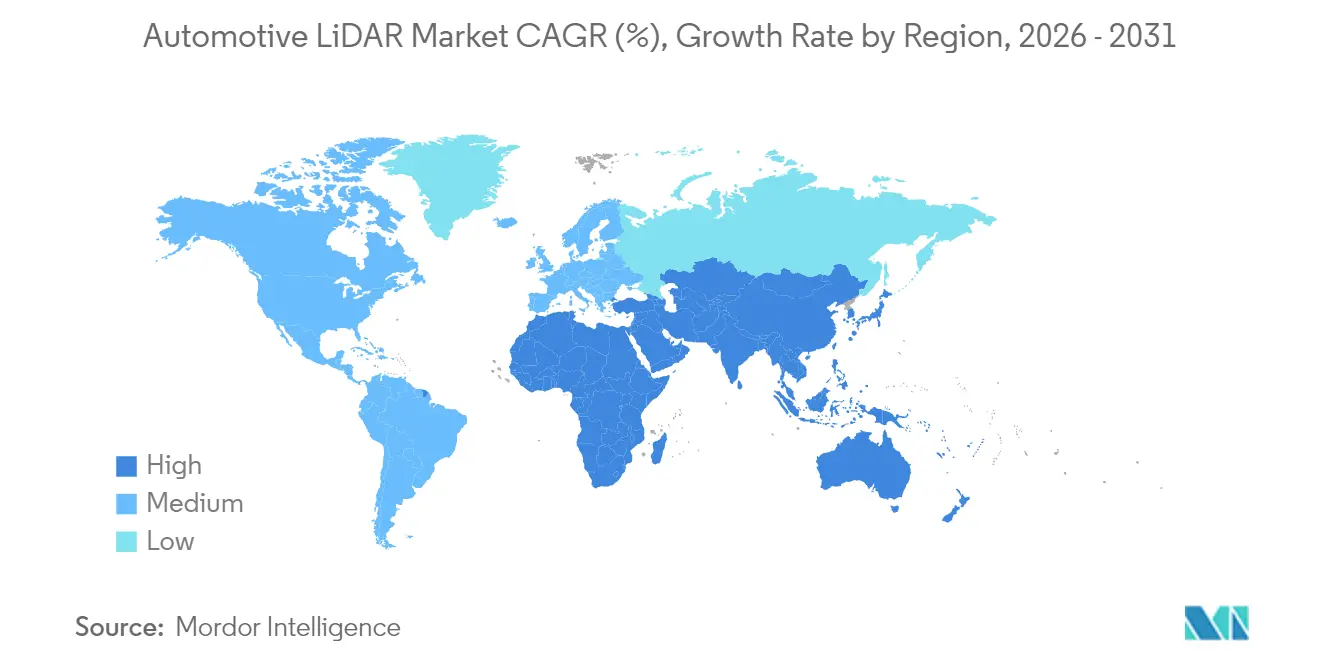

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive LiDAR Market Analysis by Mordor Intelligence

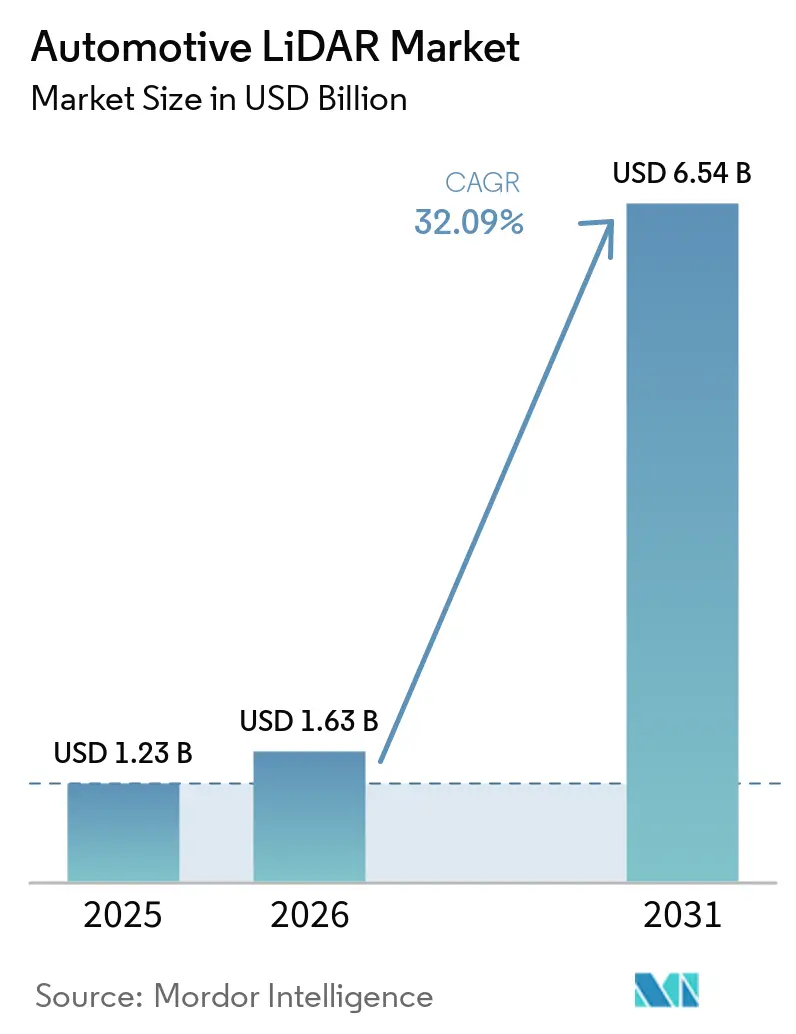

The automotive LiDAR market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 6.54 billion by 2031, at a CAGR of 32.09% during the forecast period (2026-2031). Rising demand for Level 3 and above automated driving, falling sensor prices, and tightening perception-focused safety rules are accelerating volume growth. Chinese original-equipment manufacturers (OEMs) currently account for the highest installation density, and tier-1 suppliers are entering multiyear supply programs that bring production‐grade sensors into mainstream vehicle platforms. Breakthroughs in frequency-modulated continuous-wave (FMCW) architectures now enable a 400-meter range at Class 1 eye-safety limits, positioning the technology as the leading candidate for highway autonomy. Partnerships between hardware vendors and cloud software stacks are reshaping traditional supply chains, while regional subsidies and new assessment protocols make high-resolution perception a basic requirement for premium and, increasingly, mid-priced vehicles.

Key Report Takeaways

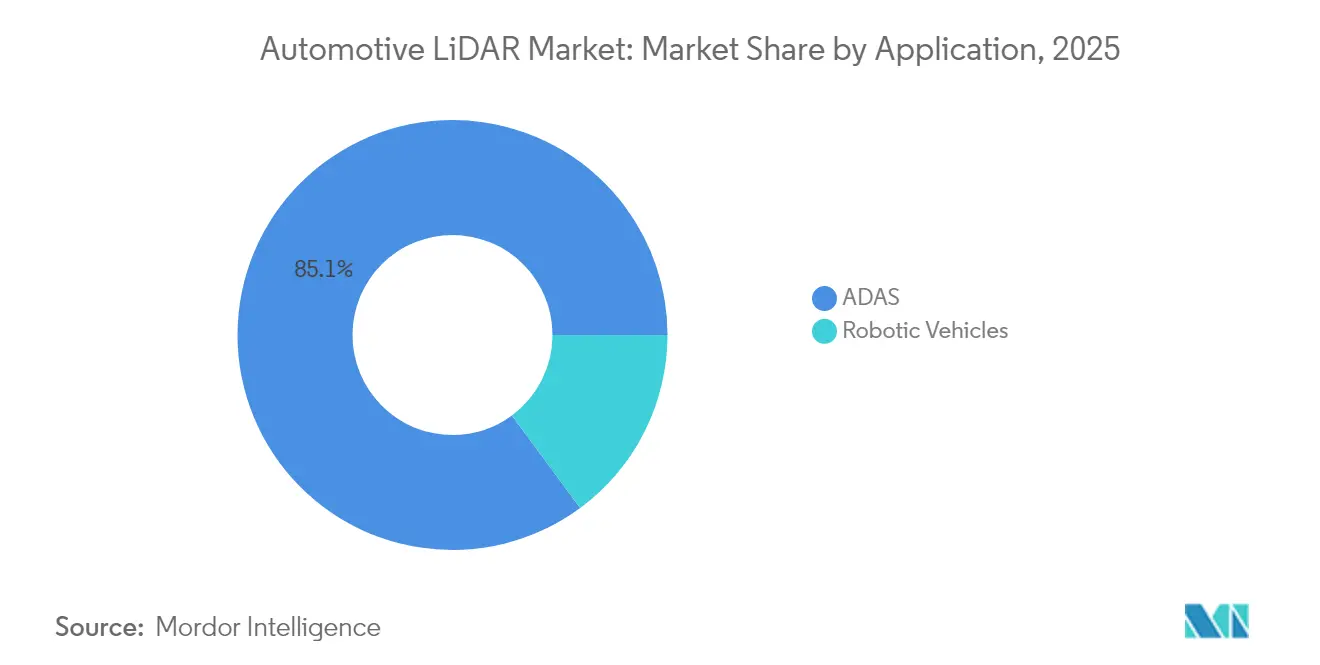

- ADAS, by application, held a dominant 85.12% share of the automotive LiDAR market in 2025, with projections indicating a robust expansion rate of 37.88% CAGR through 2031.

- By technology type, mechanical/spinning LiDAR systems led with 62.15% of the market share in 2025, while the FMCW segment is projected to expand at a 47.46% CAGR through 2031.

- By vehicle type, passenger cars held 77.65% of the automotive LiDAR market share in 2025, and are expected to grow at a 31.1% CAGR by 2031.

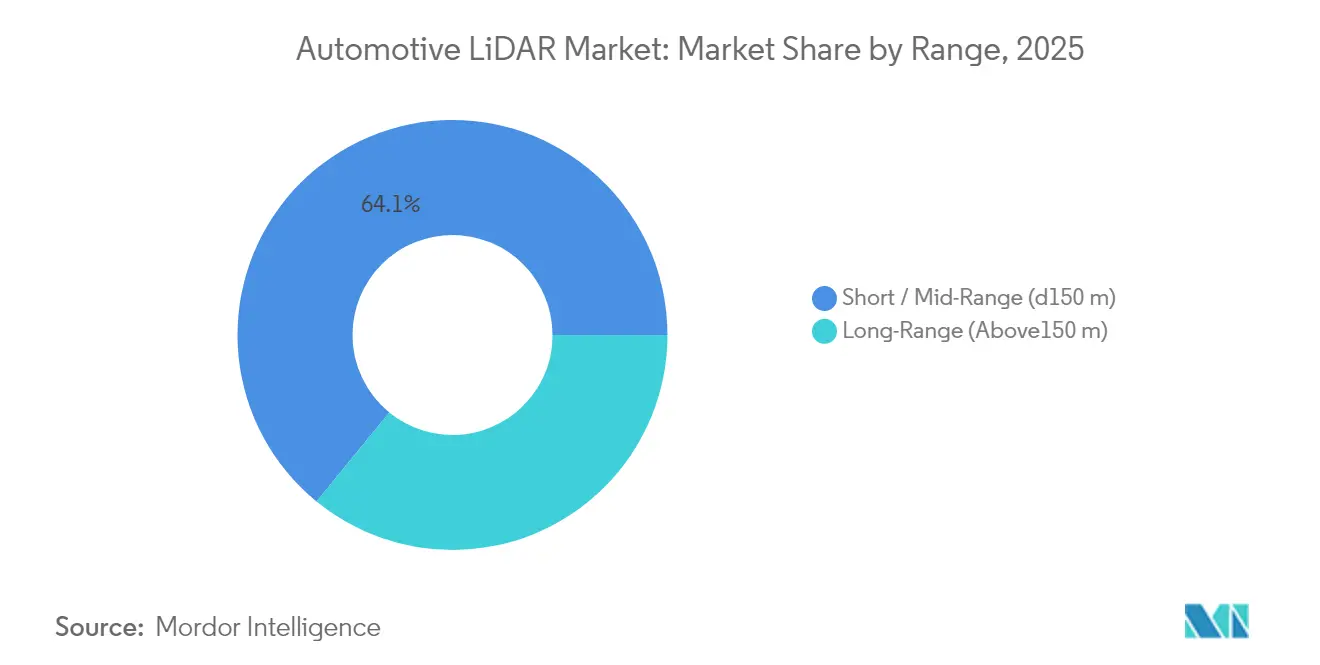

- By range, short and mid-range units (Up to 150 m) captured 64.10% of the market size in 2025, while the long-range (above 150 m) segment is expected to expand at a 32.4% CAGR.

- By installation position, roof-mounted modules led with 38.62% of the automotive LiDAR market share in 2025, whereas headlamp-integrated modules are expected to grow at a 35.1% CAGR.

- By geography, Asia-Pacific commanded 41.75% of 2025 revenue, and the region, excluding Japan, is projected to register the fastest 25.9% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive LiDAR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mid-Priced Vehicle Adoption | +8.5% | Global, with strongest impact in China and Europe | Medium term (2-4 years) |

| FMCW Lidar Sensor Breakthroughs | +6.6% | Global, led by North America and China | Long term (≥ 4 years) |

| Autonomy Ratings Mandating Higher-Resolution | +6.5% | Europe, China, with spillover to other regions | Short term (≤ 2 years) |

| Deals Between Tier-1s and Cloud AV Stacks | +4.8% | Global, concentrated in major automotive markets | Medium term (2-4 years) |

| L3-Ready Sensor Suite Subsidies | +3.9% | China, with competitive pressure globally | Short term (≤ 2 years) |

| Highway Lidar Subscription Monetization | +2.7% | North America, Europe, premium segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid ASP Decline Unlocking Mid-Priced Vehicle Adoption

Average selling prices for solid-state units fell more than 30% between 2023 and 2025, bringing fully automotive-qualified flash sensors below USD 400. Cost reduction stems from silicon photonics integration, wafer-level optics, and back-end test automation, enabling installation on premium compact cars instead of only luxury flagships. PreAct Technologies and several Chinese fabs report six-figure monthly output volumes, illustrating economies of scale. The downward price curve broadens the total addressable automotive LiDAR market by enabling optional packages at sub-USD 1,500 price points for consumers. A greater installed base further drives learning effects that compress cost over the medium term.

Early-stage FMCW Sensor Breakthroughs

FMCW architectures emit continuous low-power light and use coherent detection to measure both distance and radial velocity. Aurora Innovation’s FirstLight sensor shows reliable detection of 10% reflectivity objects at 400 meters, a critical requirement for highway speeds. Because FMCW separates each unit’s frequency chirp, crosstalk is virtually eliminated in dense traffic, and immunity to solar interference improves all-weather uptime. OEM roadmaps indicate FMCW deployment on 2027-model premium vehicles in North America and China, with production tooling already underway at several OSAT partners. These advances suggest FMCW will command an outsized share of incremental revenue growth in the automotive LiDAR market through the forecast period.

UNECE R157 and China NCAP 2026 Autonomy Mandates

China’s NCAP 2026 adds dedicated scoring for autonomous functions, creating direct commercial incentives for higher sensor counts. Together, these rules reduce technology uncertainty and push LiDAR-equipped models into volume production ahead of earlier expectations, especially among Chinese and European brands. Testing organizations such as TÜV SÜD report a sharp increase in ALKS homologation projects as OEMs race to achieve compliance.

Mass-Production Deals Between Tier-1s and Cloud AV Stacks

Mobileye’s Drive platform integrates up to nine InnovizTwo sensors per vehicle under a long-term manufacturing agreement, showcasing a shift toward tightly coupled hardware-software stacks. Tier-1s gain access to perception algorithms and over-the-air (OTA) update pathways, while cloud providers secure automotive-grade supply continuity. Such alliances compress development cycles and distribute liability, accelerating sensor adoption across multiple brands. Similar frameworks are emerging between Aeva and Daimler Truck, Valeo and Amazon Zoox, and RoboSense with several Chinese EV startups, each adding momentum to the automotive LiDAR market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Eye-Safety (IEC 60825-1) Rules | -4.8% | Global, with stricter enforcement in Europe and North America | Long term (≥ 4 years) |

| Radar/Camera Fusion Roadmaps | -4.3% | Global, particularly in emerging markets and entry-level segments | Medium term (2-4 years) |

| 1,550 Nm Gaas VCSELs' Export Scrutiny | -3.8% | US-China trade corridors, affecting global supply chains | Medium term (2-4 years) |

| Beam-Steering MEMS Reliability Concerns | -2.9% | Global, affecting all MEMS-based LiDAR systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Eye-Safety Limits on Peak Power

IEC 60825-1 Class 1 rules cap maximum permissible exposure, limiting optical power for long-range roof units. Vendors, therefore, rely on larger receiver apertures, avalanche photodiodes, and advanced signal processing rather than raw transmit power[1]"LiDAR Safety Standards and Exposure Limits - QuantumLABS." QuantumLABS, Accessed April 17, 2025. q-labs.ai.. While safety guarantees protect public health, design latitude narrows and drives up cost for precision optics and thermal management. These engineering trade-offs slow the rollout of ultra-long-range products and marginally dampen the automotive LiDAR market growth outlook.

Radar/Camera Fusion Roadmaps

OEM cost-down programs demonstrate that high-resolution radar combined with machine-vision cameras can meet regulatory minimums for many assist features. When LiDAR adds USD 600–1,000 to the bill of materials, brands targeting sub-USD 25,000 price bands often postpone adoption. Component suppliers estimate that the global attach rate in A- and B-segment vehicles may stay below 15% until at least 2028. While technology learning curves should eventually close cost gaps, price-sensitive tiers remain a near-term brake on automotive LiDAR market penetration, particularly in South America, India, and parts of Southeast Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Level 5 systems stimulate long-run upside

In 2025, ADAS accounted for 85.12% of the Automotive LiDAR Market, reflecting its mainstream adoption. Additionally, ADAS is the fastest-growing segment, with a 37.88% CAGR, driven by city-level permits and ride-hailing fleet orders. ADAS Level 3 and Level 4 programs bridge the gap: German premium OEMs already ship production Level 3 highway pilots, and Chinese mobility companies operate supervised Level 4 services in over 10 metropolitan areas. Higher autonomy levels require multiple sensors, redundancy, and full-stack validation, raising average content per vehicle and powering the next wave of the market size expansion.

Scaling to full autonomy shifts value from hardware to continuous OTA upgrades. Subscription models for highway self-driving add revenue streams that justify higher sensor bills, and data collected by Level 5 fleets feeds iterative perception improvements. As these platforms mature, they reinforce a virtuous cycle: wider data coverage supports safer algorithms, in turn unlocking permits for broader operations. This flywheel underpins bullish long-range forecasts despite early-stage volumes.

By Technology Type: FMCW disrupts mechanical incumbency

In 2025, mechanical spinning units captured 62.15% of the revenue share in the Automotive LiDAR Market, due to their proven field performance, comprehensive 360-degree coverage, and established manufacturing lines. Yet their moving parts create reliability concerns for a 10-year automotive design life, and form-factor constraints complicate stylistic integration. Solid-state approaches, including MEMS beam steering, optical phased arrays, and flash topologies, step in with fully sealed modules and lower cost trajectories. Within this solid-state cohort, FMCW is the breakout sub-category, projected at 47.46% CAGR and expected to reach double-digit share before 2031.

Valeo continues to iterate its second-generation Scala hybrid scanner, while Luminar brings high-channel-count pulsed time-of-flight into series production. Huawei and Hesai invest heavily in 905-nm pulsed and 1,550-nm FMCW pipelines, seeking to hedge technology bets across different vehicle classes. This pluralistic landscape ensures that no single architecture dominates all use cases, even as FMCW captures the performance leadership narrative.

By Vehicle Type: Commercial fleets move from pilot to scale

In 2025, passenger cars commanded a dominant 77.65% share of the market, with projections indicating a robust growth rate of 31.1% CAGR. Premium electric vehicles, especially in China and Europe, now ship with roof or grille LiDAR as baseline hardware. OTA feature unlocks generate post-sale revenues, reinforcing adoption. Fleet operators value operational savings and regulatory compliance, prioritizing durability over retail price. Daimler Truck’s selection of Aeva’s 4D FMCW exemplifies this focus.

As logistics providers commit to autonomous corridors, each Class 8 tractor may carry three or more roof-edge or bumper sensors for redundant forward coverage. These high-volume, high-spec deployments lift average selling prices despite ongoing cost compression in passenger segments, adding a stabilizing factor to the automotive LiDAR market.

By Range: Long-range capability gains momentum

In 2025, early implementations of Automotive LiDAR saw short and mid-range units (up to 150 m) commanding a dominant 64.10% market share. Urban ADAS features such as automated braking and traffic jam pilots rely on these sensors. However, UNECE R157 compliance and North American highway pilot rollouts are shifting procurement toward long-range units. Long-range devices already post a 32.4% CAGR, and their automotive LiDAR market share is projected to increase significantly by 2031 as 150–300 meter detection becomes compulsory for speeds above 100 km/h.

Manufacturers respond with multi-range portfolios: a narrow-FOV long-range sensor pairs with two wide-FOV short-range modules, optimizing cost and performance. FMCW’s coherent gain supports this segmentation because a single photonics platform can be tuned for different range profiles without changing the underlying laser wafer process.

By Installation Position: Design integration reshapes demand

In 2025, roof-mounted sensors, prized for unobstructed 360-degree views, captured a 38.62% share of the Automotive LiDAR Market. Yet, high profile and aerodynamic drag conflict with styling objectives. Automakers therefore migrate to headlamp, grille, and bumper placements. Luminar’s Halo demonstrates a fully enclosed unit behind the windshield, eliminating protrusions. This trend spurs new optical designs that tolerate glare, vibration, and temperature extremes when embedded in body panels, driving additional R&D spend.

Consequently, the installation position spectrum is fragmenting. Some premium models retain roof pods for 360-degree redundancy, while mass-market trims opt for concealed forward sensors supplemented by high-definition radar for lateral coverage. This variety keeps the Automotive LiDAR market open to multiple form factors and supplier strategies.

Geography Analysis

In 2025, the Automotive LiDAR Market saw Asia-Pacific commanding a dominant revenue share of 41.75%, with China as the epicenter of sensor deployment. Provincial subsidies worth up to CNY 10,000 per L3-ready vehicle, extended through 2027, increase penetration of battery electric SUVs and sedans. Domestic supply chains spanning wafer fab to final assembly compress cost and shorten lead times, reinforcing regional dominance. South Korea and Singapore add pilot zones and smart-highway projects, further expanding regional demand. The market in Asia-Pacific is forecast to grow at a 25.9% CAGR, the highest across all regions.

Autonomous trucking corridors linking Texas, Arizona, and California, and consumer appetite for hands-free highway assist, push a 23.2% CAGR. Aurora, Ouster, and Aeva operate domestic facilities that reduce import reliance, while U.S. export control on certain 1,550 nm VCSEL epitaxy encourages local alternative suppliers. Canada’s winter testing grounds add niche demand for all-weather FMCW products.

Europe follows with a 20.4% CAGR, reflecting advanced regulation and conservative consumer uptake. UNECE-based rules originate in Europe, but national type-approval processes remain stringent, slowing high-volume delivery. However, German, Swedish, and French premium brands install multi-LiDAR configurations to meet L3 highway pilot requirements, making the region an influential technology trendsetter. Smaller yet notable opportunities arise in the Gulf Cooperation Council, where smart-city mega-projects embed autonomous shuttles into new urban designs. Africa and Latin America post CAGRs of 21.3% and 19.6% respectively on lower bases, driven by mining haulage automation and public-sector fleet modernization.

Competitive Landscape

Hesai leads the automotive LiDAR market, closely followed by Huawei HI-XG and RoboSense. Valeo retains a niche with its Scala series, while Luminar commands a significant share across European premium contracts.

Competitive strategies focus on vertical integration, cost leadership, and differentiated architectures. Chinese suppliers leverage large domestic EV customer bases to reach annual run-rates above 500,000 units, gaining cost advantages. Western startups emphasize FMCW intellectual property, velocity data, and long-range performance to secure premium contracts. Joint ventures between tier-1s and cloud providers—Mobileye-Innoviz, Daimler-Aeva, illustrate growing alliances that pool hardware and algorithm expertise for end-to-end autonomy solutions.

Hesai invested in a wafer-to-module plant that doubles output capacity, signaling expectations for sustained growth. Meanwhile, suppliers diversify into adjacent markets, industrial robots, construction machinery, and smart infrastructure, to hedge automotive cyclicality. Overall, technological pluralism persists, but scale requirements favor players with manufacturing depth and software ecosystems.

Automotive LiDAR Industry Leaders

-

Hesai Technology

-

Valeo SA

-

Luminar Technologies Inc.

-

Huawei Technologies Co., Ltd.

-

RoboSense Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Innoviz Technologies partnered with Fabrinet to mass-produce InnovizTwo, with Fabrinet’s Thailand facility passing OEM audits for automotive-grade standards.

- January 2025: Aeva and Wideye showcased the first in-cabin FMCW 4D LiDAR behind the windshield, combining long-range sensing with streamlined vehicle styling.

- December 2024: Aurora Innovation opened a 78,000 sq ft research facility in Bozeman, Montana, to refine its FirstLight technology and support 2025 autonomous trucking rollout in Texas.

Global Automotive LiDAR Market Report Scope

LIDAR - sometimes called time of flight (ToF), laser scanners or laser radar - is a sensing method that detects objects and maps their distances. The technology works by illuminating a target with an optical pulse and measuring the characteristics of the reflected return signal. The width of the optical pulse can range from a few nanoseconds to several microseconds. The study analyses the application of LiDAR in automotive industry. It provides a in-depth analysis of the application along with the extent of development and adoption in various geographies.

| Robotic Vehicles | |

| ADAS | Level 2+ / 2++ |

| Level 3 / 4 | |

| Level 5 |

| Mechanical/Spinning |

| Solid-State (MEMS, Flash) |

| FMCW |

| Passenger Cars |

| Commercial Vehicles |

| Short / Mid-Range (Up to 150 m) |

| Long-Range (Above 150 m) |

| Roof-Mounted |

| Grille / Bumper |

| Headlamp-Integrated |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Robotic Vehicles | |

| ADAS | Level 2+ / 2++ | |

| Level 3 / 4 | ||

| Level 5 | ||

| By Technology Type | Mechanical/Spinning | |

| Solid-State (MEMS, Flash) | ||

| FMCW | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Range | Short / Mid-Range (Up to 150 m) | |

| Long-Range (Above 150 m) | ||

| By Installation Position | Roof-Mounted | |

| Grille / Bumper | ||

| Headlamp-Integrated | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Automotive LiDAR market?

The Automotive LiDAR market was valued at USD 1.63 billion in 2026 and is projected to grow at a 32.09% CAGR to USD 6.54 billion by 2031.

Which region leads global demand?

Asia-Pacific holds 41.75% of target market revenue due to China’s aggressive autonomous-vehicle policies and local manufacturing ecosystems.

Why is FMCW technology gaining traction?

FMCW simultaneously measures distance and velocity, avoids crosstalk, and delivers 400 meter range at Class 1 eye safety, driving the fastest segment growth at 47.46% CAGR.

How do regulations influence adoption?

UNECE R157 in Europe and China NCAP 2026 both require higher-resolution perception, effectively pushing LiDAR into Level 3 and above production vehicles.

What challenges limit LiDAR penetration in entry-level cars?

Strict eye-safety power limits and cheaper radar-camera sensor fusion keep added hardware costs high, slowing adoption in vehicles priced below USD 25,000.

Page last updated on: