High-end Inertial Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.5 Billion |

| Market Size (2031) | USD 7.4 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

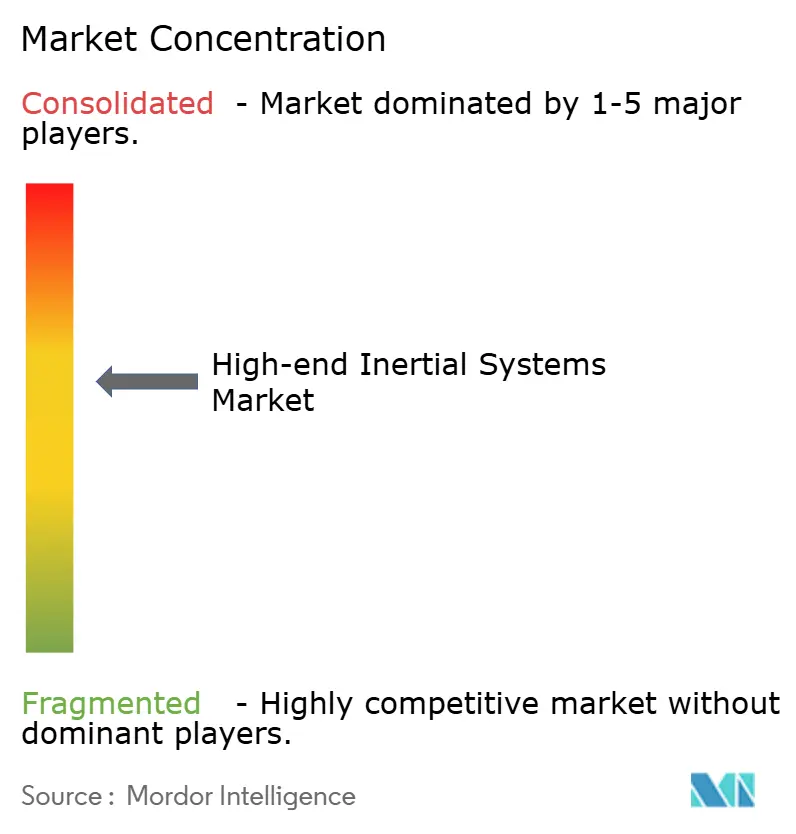

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-end Inertial Systems Market Analysis by Mordor Intelligence

The high-end inertial systems market size is expected to grow from USD 5.18 billion in 2025 to USD 5.5 billion in 2026 and is forecast to reach USD 7.4 billion by 2031 at 6.13% CAGR over 2026-2031. Digital transformation in defense, energy, and industrial automation is shifting demand from legacy ring-laser gyroscopes toward quantum-ready sensors and compact fiber-optic or MEMS-based units, even as multi-year procurement contracts in North America and Europe moderate annual revenue expansion. The uptake of software-defined Kalman-filter stacks that fuse inertial data with vision or lidar inputs is growing, carving out a recurring licensing stream for vendors and raising switching costs for integrators. GNSS-denied navigation mandates in aviation and underground mining, alongside offshore wind vessel requirements for real-time motion compensation, are broadening applications beyond defense. Meanwhile, export control regimes continue to restrict strategic-grade sales to non-allied nations, creating parallel domestic supply chains in China, India, and South Korea. Component lead-time uncertainty, particularly for specialty optical fiber and single-crystal quartz, remains a capacity-planning risk; however, ongoing MEMS scaling and photonic-chip gyroscope R&D point to cost curves that favor wider commercial adoption by the end of the decade.

Key Report Takeaways

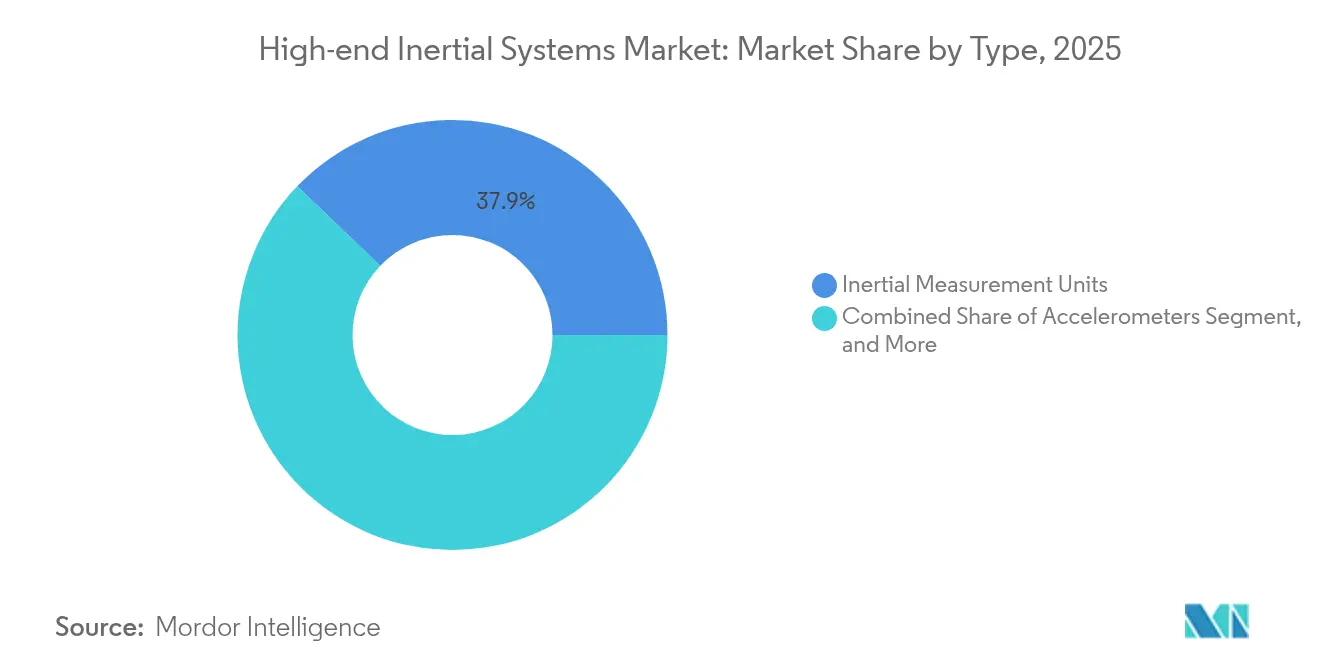

- By type, inertial measurement units held 37.85% of the 2025 revenue of the high-end inertial systems market, whereas attitude and heading reference systems are projected to log the fastest 8.28% CAGR through 2031.

- By component, Sensors commanded 42.15% of the 2025 component revenue in the high-end inertial systems market, while software and algorithms are projected to post the fastest growth pace of 8.37% over the forecast period.

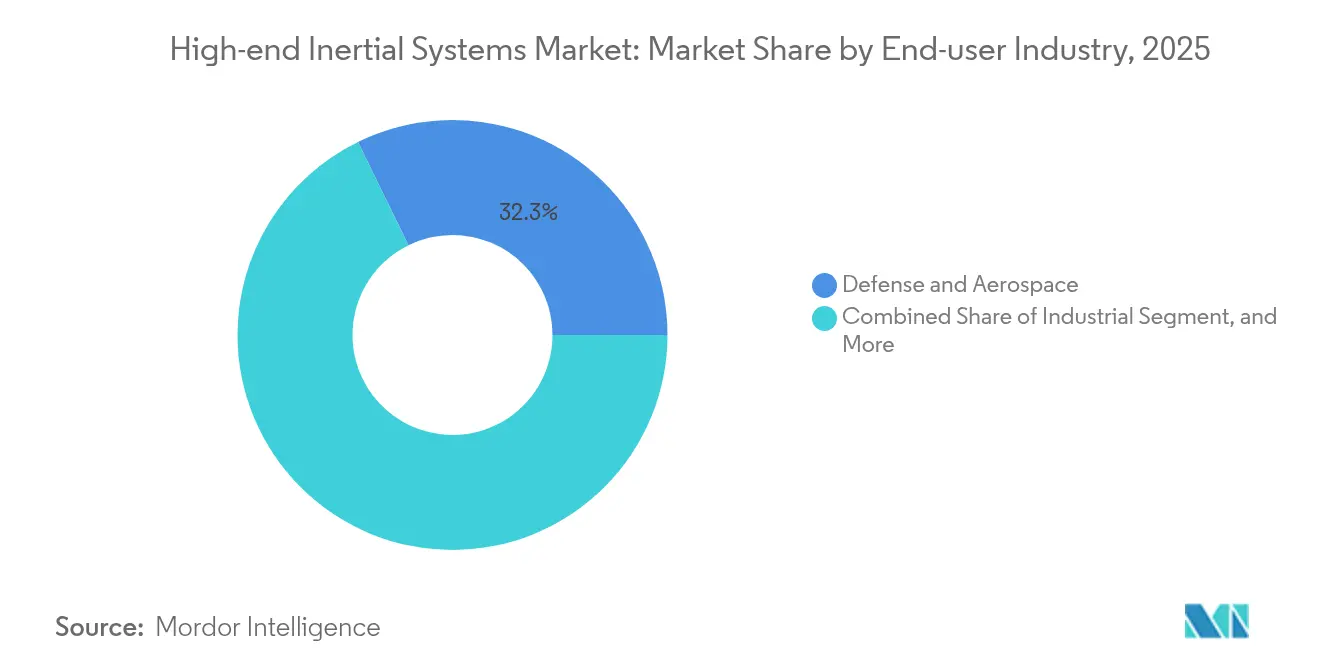

- By end-user industry, the Defense and aerospace sector accounted for 32.25% of the 2025 spending in the high-end inertial systems market, while the industrial segment is expected to expand at a 8.74% CAGR, driven by underground GNSS-denied vehicle deployments.

- By navigation grade, Strategic-grade platforms captured 33.55% of 2025 sales of the high-end inertial systems market; industrial-grade units will advance at a 7.62% CAGR as robotics and IoT devices trade some accuracy for lower cost.

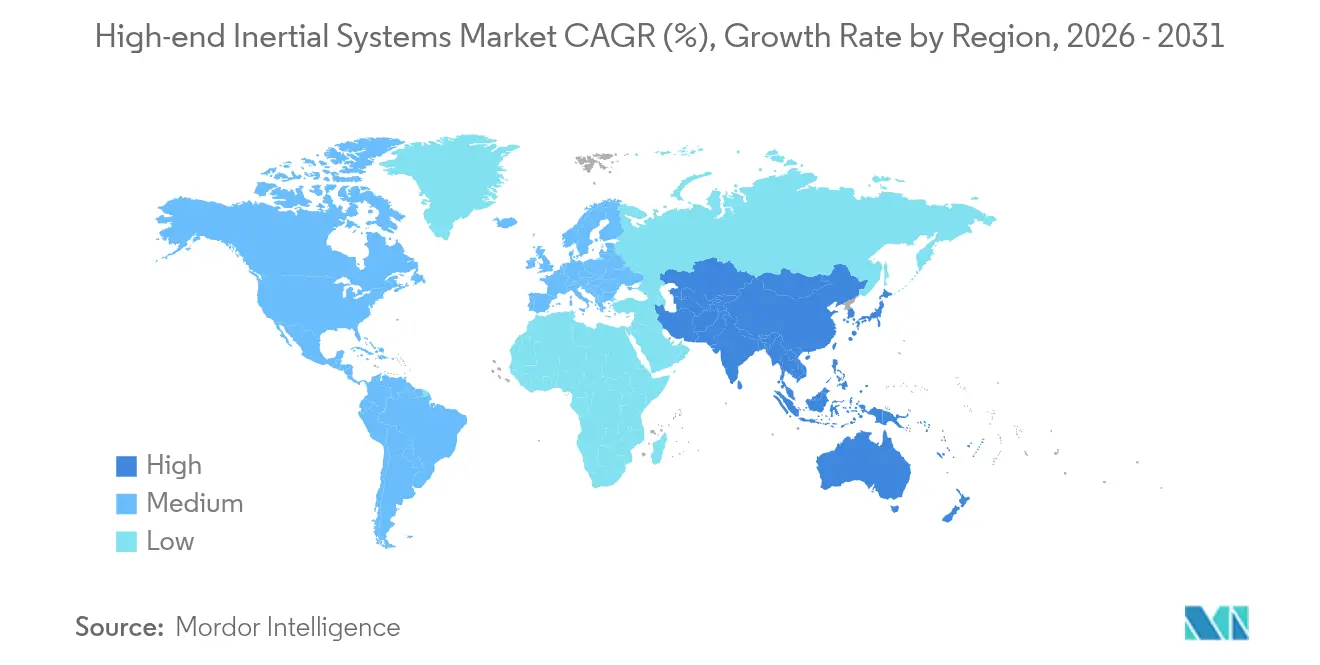

- By geography, North America led the 2025 high-end inertial systems market with 37.65% of the revenue, but the Asia Pacific is poised for the highest 8.21% CAGR, supported by BeiDou-independent navigation programs and automotive ADAS demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-end Inertial Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of UAVs and autonomous vehicles | +1.3% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Defense modernization budgets for inertial navigation | +1.1% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Advancements in MEMS manufacturing reducing SWaP | +0.9% | Global, led by Asia Pacific fabrication hubs | Short term (≤ 2 years) |

| Increasing demand for GNSS-denied navigation in aerospace | +0.8% | North America, Europe, select Asia Pacific markets | Medium term (2-4 years) |

| Emergence of quantum-enhanced inertial sensors | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Integration with fiber-optic gyros in offshore wind installation vessels | +0.6% | Europe, Asia Pacific coastal markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of UAVs And Autonomous Vehicles

Rising UAV fleet sizes and autonomous-system deployments compel operators to adopt tactical-grade IMUs that minimize drift below 1°/h, allowing missions to continue during GPS jamming. U.S. Special Operations Command forecast procurement of more than 1,200 Group-3 UAVs between 2024 and 2029, embedding a steady base of high-rate IMU demand.[1]U.S. Special Operations Command, “Group-3 UAV Acquisition Forecast,” socom.mil In mining and agriculture, visual-inertial odometry integrates IMU outputs with stereo-camera feeds, reducing cumulative position error to under 0.5% of the distance traveled while keeping the unit price below USD 5,000. Local processing of fused data eliminates latency associated with cloud offloading, prompting sensor makers to co-develop on-board Kalman filters that satisfy safety-critical response requirements. This momentum supports the broader penetration of high-end inertial systems in the civilian sector without diluting the strategic-grade backlog.

Defense Modernization Budgets For Inertial Navigation

Pentagon allocations rose in fiscal 2024, exemplified by a USD 99 million award to Honeywell for the Distributed Anti-Jam GPS System that pairs tactical-grade IMUs with anti-jam receivers. Similar upgrade cycles in European navies are replacing 1990s-era fiber-optic gyros with newer tactical-grade INS, cutting per-unit costs by roughly 30% and extending platform life. The U.S. Army’s Mounted Assured Positioning, Navigation and Timing architecture blends LN-251 fiber-optic gyros with encrypted GPS to harden vehicles against electronic attack, solidifying recurring revenue for Tier-1 primes but raising certification barriers for entrants. These contracts anchor the high-end inertial systems market even when commercial demand fluctuates.

Advancements In MEMS Manufacturing Reducing SWaP

MEMS gyroscope bias instability now dips below 0.1°/h, edging closer to fiber-optic performance while consuming under 1 mW in idle modes, as seen in Bosch Sensortec’s BMI323 released in 2024. Silicon-carbide bulk acoustic wave designs withstand temperatures of up to 300 °C, enabling hypersonic weapon guidance where shock and temperature extremes defeat conventional sensors. Cost per axis has fallen below USD 10 in high-volume automotive lines, bringing tactical-grade capability within reach of industrial robots, AGVs, and warehouse drones. This cost-curve pressure is forcing fiber-optic incumbents to layer value through proprietary calibration or application-specific analytics, reshaping the competitive landscape within the high-end inertial systems market.

Increasing Demand For GNSS-Denied Navigation In Aerospace

Recurring satellite outages and jamming episodes, recorded several times per year according to FAA RNP guidance, are prompting airlines to retrofit inertial reference units on their narrow-body fleets.[2]Federal Aviation Administration, “RNP Procedures Guidance,” faa.gov Honeywell’s HG9900 IMU, already line-fit on 737 MAX, maintains 1 NM/hour accuracy without GPS updates, satisfying ICAO Annex 10 backup navigation rules. Parallel defense research invested USD 45.5 million in 2024 to field cold-atom interferometry sensors that promise absolute position fixes independent of satellites. Although still in the early stages, such quantum-based units underscore a technology roadmap that bolsters the high-end inertial systems market against concerns over GNSS vulnerability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial procurement and calibration costs | -0.8% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Complex system integration challenges in multi-sensor fusion | -0.6% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Supply-chain vulnerabilities for specialty inertial-grade quartz and optical fibers | -0.5% | Global, with acute impact in Asia Pacific | Short term (≤ 2 years) |

| Regulatory export controls limiting high-performance IMU shipments | -0.4% | Global, concentrated in North America and Europe exports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Procurement And Calibration Costs

Strategic-grade inertial navigation systems priced above USD 500,000 require six-axis thermal calibration, which can add 20% to the purchase cost and extend lead times by more than 18 months.[3]Honeywell International, “Inertial Navigation Unit Pricing and Calibration Data,” honeywell.com Tactical-grade IMUs still require factory cycles spanning 72 hours, pushing smaller industrial buyers to postpone adoption in favor of GNSS-only modules under USD 1,000. Leasing and calibration-as-a-service schemes remain immature, forcing end users to amortize capital expenses over decade-long refresh cycles that exceed consumer-hardware timelines, constraining near-term penetration of the high-end inertial systems market.

Complex System Integration Challenges In Multi-Sensor Fusion

Real-time fusion of inertial, lidar, radar, and vision data involves tuning covariance matrices that balance filter responsiveness against oscillation, a task extending development schedules by months. The U.S. Army’s Integrated Visual Augmentation System experienced delays in 2024 after sensor-fusion latency exceeded its 20-ms headset threshold, illustrating how IMU integration issues can cascade into program setbacks. While open-source stacks such as ROS lower barriers, platform-specific calibration parameters remain proprietary, locking OEMs into single-vendor supply at exactly the point they seek cost diversity. This complexity slows scaling for new entrants within the high-end inertial systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: IMUs Retain Scale, AHRS Accelerate

Inertial measurement units contributed 37.85% of 2025 revenue, underscoring their centrality to the high-end inertial systems market size for multi-domain navigation platforms. Their modular architecture pairs tri-axis accelerometers and gyroscopes with external processors, allowing OEMs to tailor performance-to-cost ratios across aerospace and industrial robots. Attitude and heading reference systems are set to clock an 8.28% CAGR, mainly because offshore-wind installation vessels demand heading accuracy within 0.5°, where integrated magnetometers outperform standalone IMUs. This performance uptick underlines how incremental sensor fusion is driving segment substitution rather than pure additive spend.

IMUs benefit from broader design-win opportunities in UAVs and missiles; yet AHRS gains traction in marine and mining equipment seeking plug-and-play pitch-roll solutions. Fiber-optic or MEMS gyros, when combined with fluxgate or solid-state compasses, enable AHRS to replace more expensive INS units on price-sensitive platforms. Quantum-interferometry prototypes, such as Northrop Grumman’s LR-500, which achieved 0.001°/h bias stability in 2024, remain in laboratories; however, miniaturization roadmaps suggest disruptive competition within the high-end inertial systems market before 2030.

By Component: Sensors Dominate, Software Monetizes

Sensor hardware accounted for 42.15% of component revenue in 2025, reflecting the capital-intensive nature of clean-room MEMS wafering and fiber-coil winding, which influences the cost structure across the high-end inertial systems market share. However, software and algorithms are expected to record an 8.37% CAGR as customers pay licensing fees for adaptive Kalman-filter libraries and AI-enhanced error modeling. Vendors increasingly bundle middleware with hardware to secure pull-through revenue and lock customers into their calibration frameworks.

Processors, typically ARM Cortex-M7 or DSP cores, account for roughly 9% of the bill-of-materials value but ensure deterministic loop times of less than 1 ms, which is necessary for suppressing IMU shot noise. Mechanical frames made of titanium or carbon fiber stave off vibration-induced errors, which are critical for military and offshore applications. Meanwhile, power-supply modules designed for 9-36 V rails broaden cross-platform integration, helping to expand the total addressable spend within the high-end inertial systems market.

By End-user Industry: Defense Leads, Industrial Outpaces

Defense and aerospace comprised 32.25% of 2025 outlays, with the U.S. Navy’s WSN-7 ring-laser gyroscope refresh highlighting ongoing strategic-grade demand. The industrial vertical, however, will rise at a 8.74% CAGR, as miners, drillers, and heavy-equipment OEMs automate assets that operate in areas where GNSS is absent or unreliable. Rio Tinto’s Pilbara mines, for example, fused lidar and tactical-grade IMUs to unlock 24-hour autonomous haulage across 1,500 km of roads. Such case studies illustrate how performance once reserved for defense migrates down-market, enlarging the high-end inertial systems market.

Marine and subsea users deploy fiber-optic gyros for dynamic positioning to prevent collisions with subsea pipelines, while automotive OEMs embed low-cost MEMS IMUs in ADAS modules priced under USD 20. These cross-sector synergies blur historic boundaries, pushing suppliers toward tiered product lines spanning sub-USD 500 industrial units to USD 500,000 strategic navigation suites.

By Navigation Grade: Strategic Retains Value, Industrial Scales

Strategic-grade platforms captured 33.55% of 2025 sales, driven by submarine and ICBM programs that require drift below 0.01°/h and radiation-hardening to 100 krad. Navigation-grade systems serve the commercial aviation and surface-ship niches, while tactical-grade units cater to UAVs and land vehicles.

Industrial-grade devices are expected to post a 7.62% CAGR as MEMS cost curves drive prices below USD 1,000, making them more attractive for autonomous forklifts, warehouse AMRs, and construction equipment. Export-control thresholds that ban sub-0.5°/h bias stability to non-allies effectively segment the high-end inertial systems market into controlled and commercial tiers.

Geography Analysis

North America generated 37.65% of 2025 revenue as Pentagon funding of USD 1.2 billion flowed into inertial upgrades across air, land, and sea platforms. Honeywell’s Clearwater and Northrop Grumman’s Woodland Hills plants dominate strategic-grade output, with Canadian Arctic programs spurring demand for −55 °C-rated IMUs. Mexico’s Querétaro cluster assembles tactical-grade sensors that qualify for USMCA duty benefits yet remain subject to ITAR re-export rules, illustrating the interdependence of supply chains within the high-end inertial systems market.

Asia Pacific is predicted to log an 8.21% CAGR through 2031, propelled by BeiDou-denied backup systems, Japanese destroyer retrofits worth over USD 100 million, and India’s Make-in-India defense offsets. Hanwha’s domestic IMU for the K2 tank and Australian mining fleets, which utilize more than 2,000 IMUs annually, reflect the regional appetite for both strategic resilience and industrial automation. Taiwan and South Korea’s semiconductor fabs offer MEMS volume capacity, positioning the region to capture a larger share of sensor hardware as unit shipments rise.

Europe, the Middle East, and Africa supply the remainder of the high-end inertial systems market. European offshore wind projects, such as Ørsted’s Hornsea 2, employ fiber-optic gyros for dynamic positioning, sustaining a high-margin marine niche. Middle Eastern demand centers around UCAV tactical-grade imports, while South African underground platinum mining highlights industrial-grade opportunities in GNSS-denied environments. The region also faces supply-chain constraints for optical fiber produced in Germany and France, which could potentially lengthen lead times for fiber-optic units.

Regulatory Landscape

High-end inertial systems are governed by dual-use export-control frameworks that restrict transfers of high-performance inertial sensors and navigation assemblies, particularly when they meet controlled performance thresholds for military and space applications. In the European Union, Council Regulation (EC) No 428/2009 (Dual-Use List, Annex I Category 7) provides the basis for licensing and classification for inertial sensors and navigation equipment. Hong Kong also maintains aligned strategic-trade controls through its Import and Export (Strategic Commodities) Regulations, including a July 2025 revision that retained civil aircraft exemption criteria for certain inertial measurement systems.

Civil aviation use is shaped by safety and approval requirements, including FAA Part 121 provisions (Appendix G) linked to operational acceptance of inertial navigation systems. For defense users, Department of Defense Instruction (DoDI) 4650.06 sets expectations for PNT governance and interoperability, which can affect cybersecurity, assurance, and integration requirements for inertial subsystems. Public-sector procurement activity is also a practical gatekeeper for underwater and maritime inertial solutions, including the US Naval Surface Warfare Center Carderock Division March 2026 procurement for Exail PHINS COMPACT units for hydrodynamic testing and DARPA's May 2026 PINPOINT research notice focused on GPS-independent inertial navigation advances.

Value Chain Analysis

The value chain starts with upstream materials and components that shape both cost and lead-time risk, including inertial-grade quartz, specialty optical fiber/coils for fiber-optic gyroscopes, and MEMS wafers supported by packaging and test services. Manufacturing covers sensor fabrication (MEMS and fiber-optic gyroscopes), precision mechanical frames, embedded processing boards, and factory calibration plus environmental testing. Downstream, firmware and higher-level software (error models and Kalman-filter stacks) increasingly differentiate system performance and can support recurring licensing revenue. OEMs and integrators then embed IMUs, INS, and AHRS into platforms spanning defense and aerospace, industrial automation and robotics, marine and subsea, mining and drilling, and automotive ADAS.

A structural shift is underway from heavily outsourced chains toward vertical integration, aimed at securing sensitive components and reducing delivery windows that can extend to 12 to 18 months in complex global sourcing models. Companies referenced for in-house production and calibration include Advanced Navigation, Fiber Optical Solution, and Cielo Inertial Solutions, with specialized contributors such as Memsense, iNGage, and LITEF supporting defense and industrial programs. This integration push is also tied to export-control and security requirements that favor controlled manufacturing and traceability for higher-grade navigation products.

Competitive Landscape

Market concentration is moderate; the five largest vendors, Honeywell, Northrop Grumman, Safran, Thales, and Collins Aerospace, hold roughly 55% of strategic-grade revenue but only 30% of tactical-grade volume, evidencing a bifurcated structure. Honeywell vertically integrates quartz resonator fabrication, whereas Northrop Grumman controls fiber-coil winding, securing sensitive nodes in their supply chains. Disruptors like VectorNav and Silicon Sensing leverage commercial MEMS paired with proprietary software to deliver tactical-grade performance under USD 5,000, eroding price floors.

Quantum-enhanced and photonic-chip gyroscopes represent white-space avenues. Northrop Grumman’s 2024 CMOS-compatible silicon-photonic gyroscope patent could chop unit pricing from USD 50,000 to under USD 5,000 within five years.[4]U.S. Patent and Trademark Office, “Silicon-Photonic Gyroscope Patent US20240118234A1,” uspto.gov Start-ups AOSense and M Squared Lasers collectively raised USD 80 million to commercialize cold-atom interferometry sensors for underwater vehicles and subterranean mining. Established players counter by acquiring sensor-fusion software firms, as Honeywell did in 2024, to reinforce system-level differentiation inside the high-end inertial systems market.

High-end Inertial Systems Industry Leaders

Honeywell International Inc.

Northrop Grumman Corporation

Safran S.A.

Thales S.A.

Collins Aerospace (Raytheon Technologies Corp.)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An actionable opportunity centers on GNSS-denied navigation solutions that pair high-end inertial sensing with resilient PNT architectures for unmanned and contested operations. Recent product moves in 2026 reflect efforts to widen adoption by reducing integration friction and SWaP constraints. Honeywell introduced the commercially available HGuide i700 near-navigation-grade MEMS IMU as a no-license-required option (March 2026) and expanded embedded GNSS/INS through the Kestrel solution using an HG3900 MEMS IMU and M-code receiver (June 2026). VectorNav's March 2026 Tactical Series upgrades with high-G ranges target demand from fast-maneuvering platforms that require robust inertial data under extreme dynamics.

Industrial capacity and sovereign supply-chain initiatives also create room for suppliers that can scale output without losing performance. Safran's announced EUR 120 million investment at its Montlucon facility to increase hemispherical resonator gyroscope output from 10,000 to 30,000 units annually by 2032 links manufacturing expansion to GPS-independent navigation sensor demand. On applications, maritime and littoral missions are drawing purpose-built solutions, including Exail's June 2026 introduction of the Advans Vega SL inertial navigation system for amphibious operations across GNSS-limited environments. Across these changes, vendors that combine hardware with validated calibration workflows and software-defined fusion stacks stand to perform better where qualification cycles are long and multi-sensor integration is complex.

Recent Industry Developments

- July 2026: Thales announced a binding agreement to acquire Exail Technologies, expanding its position in inertial navigation and maritime robotics. The combination is designed to strengthen a European supply base for high-end navigation and subsea autonomy programs, while increasing competitive pressure on standalone specialists in defense and marine inertial systems.

- April 2026: Northrop Grumman delivered the first production unit of its LN-351 EGI-M navigation system, designed to provide M-Code GPS with blended navigation assurance for contested environments. Transitioning from development to production supports platform-level fielding schedules and reinforces demand for integrated EGI architectures that pair resilient GPS with high-end inertial sensors.

- March 2024: Honeywell announced plans to acquire Civitanavi Systems to expand autonomous operations offerings in aerospace and deepen its European footprint. The transaction adds inertial and stabilization know-how and broadens Honeywell's ability to offer integrated navigation and control solutions across defense and commercial programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers high end inertial systems used to sense motion and support navigation, positioning, and stabilization in platforms where accuracy and reliability requirements are high, and the outputs are sold as systems or integrated subsystems.

Scope exclusions: We exclude low cost consumer grade motion sensors and basic MEMS parts that are sold mainly for smartphones, wearables, and simple IoT devices.

Segmentation Overview

- By Type

- Inertial Measurement Units

- Inertial Navigation Systems

- Accelerometers

- Gyroscopes

- Attitude and Heading Reference Systems

- Others

- By Component

- Sensors

- Processors (DSP and Micro-controllers)

- Software and Algorithms

- Mechanical Frames

- Power Supplies

- Others

- By End-user Industry

- Defense and Aerospace

- Industrial

- Marine and Sub-sea

- Mining and Drilling

- Automotive

- Other End-user Industries

- By Navigation Grade

- Strategic Grade

- Navigation Grade

- Tactical Grade

- Industrial Grade

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand pool and to set guardrails around platform deliveries, modernization cycles, and procurement timing. We relied on public sources such as defense budget and procurement documents, aviation and maritime regulators, and official trade statistics to understand where high accuracy inertial solutions are being pulled into programs.

To convert that context into model inputs, we also reviewed sources such as customs and import export releases, patent publications, and peer reviewed aerospace and navigation journals for technology direction (for example, ring laser and fiber optic gyro adoption, and software algorithm improvements). Company annual reports, investor presentations, and credible industry press were used to cross check product mix and exposure by end use. In a few cases, paid subscriptions that aggregate company financials, contracts and tenders, and shipment level trade signals were used to confirm timelines and pricing bands. These examples are not exhaustive, and other public and paid sources were consulted for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets bought as a high end system versus a component, and how pricing changes by navigation grade and qualification level. We spoke with stakeholders across defense and aerospace programs, industrial users, and marine and subsea integrators, then checked assumptions by region so the final model is not driven by one geography's procurement cycle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 16% | APAC: 45% |

| Mid tier: 44% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 17% | Managers: 44% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs demand using platform production and delivery signals, then applies fit rates for where high accuracy inertial functions are required, followed by an adjustment for retrofit and upgrade cycles in long life fleets. Once the demand pool is formed, revenue is calculated using typical system level pricing by navigation grade and by end use, and then it is checked against a selective bottom-up approximation built from sampled supplier shipments, channel feedback, and average selling price ranges.

Inputs used in the model include, for example, defense and aerospace procurement timing, aircraft and naval platform deliveries, modernization and mid life upgrade cadence, navigation grade mix (strategic, navigation, tactical, and industrial), and shifts toward software driven sensor fusion that can change system content. Where a bottom-up check has gaps, they are handled through conservative penetration assumptions that are then revisited during expert calls so the totals remain realistic.

For forecasting, scenario analysis was used because program starts can shift with budgets and export controls, and the impact is not always smooth year to year. The scenarios are built around platform production outlook, retrofit intensity, and price progression, and then they are reconciled back to what interviewees consider a plausible procurement path by region and end use.

Data Validation & Update Cycle

Outputs are triangulated against independent signals like platform deliveries, procurement disclosures, and trade flows, and then variances are reviewed to confirm whether the driver is a real market shift or a modeling artifact. When a number appears off, we re-check the grade mix, pricing bands, and retrofit share, and follow up with contributors if the mismatch persists.

Before sign-off, the model and assumptions go through multi step analyst review so arithmetic, unit handling, and currency timing are consistent. Reports are refreshed annually, with interim updates when material events occur, and a final fresh pass is completed close to delivery so clients receive the latest updated view.

Mordor Intelligence's High End Inertial Systems Market Size Versus Other Published Estimates

Published numbers for this market often vary because each publisher draws the line differently between full inertial navigation systems, standalone sensors, and adjacent navigation electronics, and they also use different timing for defense procurement and retrofit waves.

Low cost consumer grade MEMS motion sensors sit outside Mordor Intelligence's scope for this market, and that single exclusion typically explains why some wider sensor studies show much larger totals for the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.18 B (2025) | |

| Global Consultancy A | USD 10.12 B (2025) | Often combines high end systems with a broader set of inertial sensors, and it can count component level revenue in parallel with system revenue, which raises the total versus a system-led view. |

| Industry Publisher B | USD 4.92 B (2024) | Uses a different base year and may lean more on conservative adoption for upgrade programs, and it can treat navigation grade and geophysical use cases as separate buckets that reduce the counted system pool. |

The spread in the table comes mainly from what is treated as a complete system versus a sensor component, and from how retrofit cycles are timed in the forecast. By keeping the inputs tied to platform demand signals, grade mix, and repeatable pricing logic, the estimate stays transparent and easier to reproduce when assumptions need to be stress tested.

Key Questions Answered in the Report

What is the projected value of the high-end inertial systems market by 2031?

The market is forecast to reach USD 7.4 billion by 2031, growing at a 6.13% CAGR.

Which segment will register the fastest growth through 2031?

Attitude and heading reference systems are expected to post the quickest 8.28% CAGR.

How will Asia Pacific perform compared with other regions?

Asia Pacific is set to expand at an 8.21% CAGR, outpacing all other regions on the back of BeiDou-independent navigation and ADAS demand.

Why are quantum sensors relevant to future inertial navigation?

Quantum-enhanced gyroscopes promise bias stability below 0.001°/h, enabling accurate navigation for long durations without GNSS signals.

What restrains wider adoption in industrial applications?

High upfront procurement and calibration costs, along with complex multi-sensor fusion integration, deter smaller industrial users.

Which companies dominate strategic-grade supply?

Honeywell, Northrop Grumman, Safran, Thales, and Collins Aerospace collectively account for most strategic-grade revenue.

Page last updated on: