Market Overview

| Study Period | 2020 - 2031 |

|---|---|

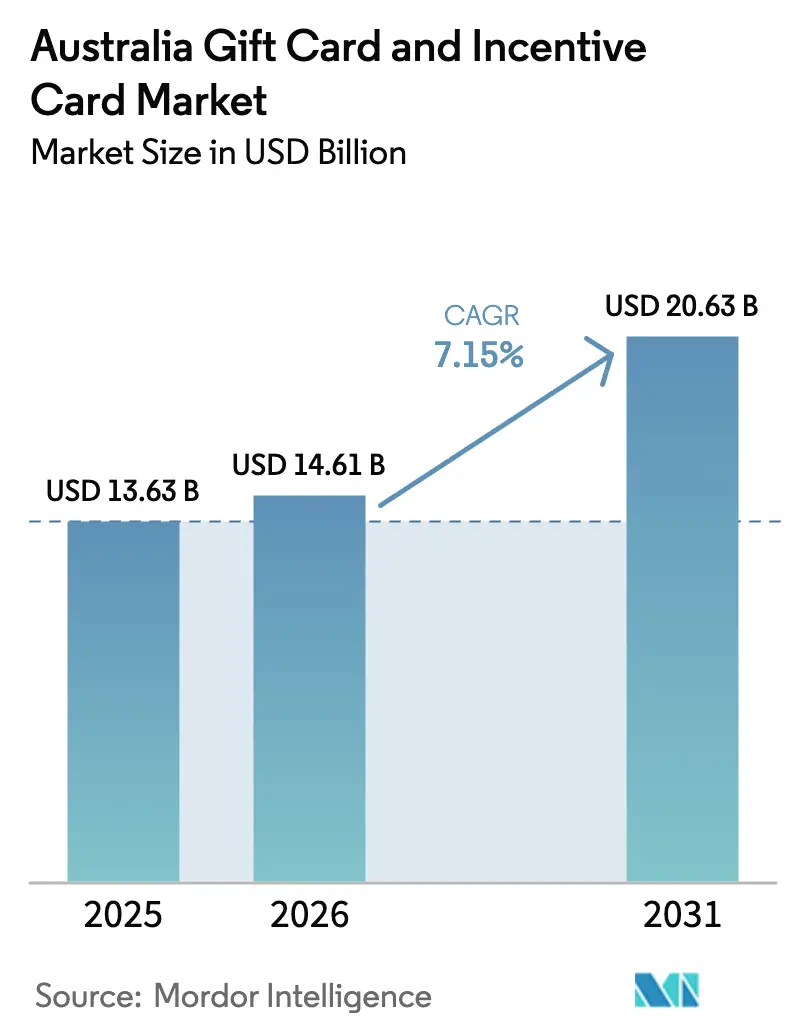

| Base Year Market Size (2025) | USD 13.63 Billion |

| Market Size (2026) | USD 14.61 Billion |

| Market Size (2031) | USD 20.63 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Largest Market | Latin America |

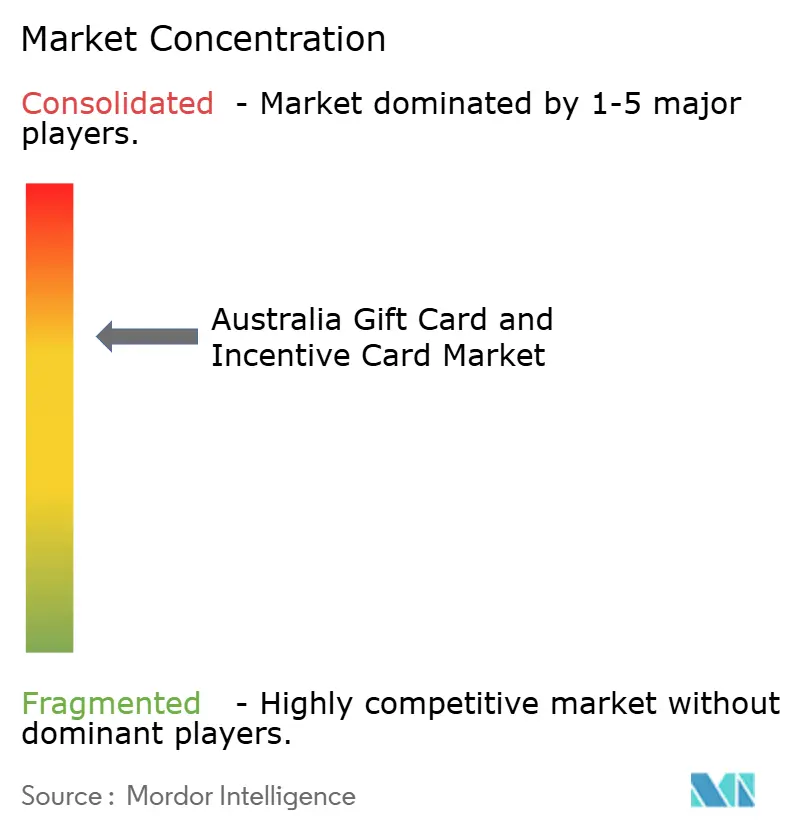

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The Australia Gift Card and Incentive Card market size was valued at USD 13.63 billion in 2025 and estimated to grow from USD 14.61 billion in 2026 to reach USD 20.63 billion by 2031, at a CAGR of 7.15% during the forecast period (2026-2031). The expansion is fueled by rapid digitization of corporate incentive programs, integration of prepaid rails into embedded-finance stacks, and rising demand for real-time analytics that prove the return on incentive spending. Corporate buyers increasingly substitute physical merchandise with API-integrated e-gift cards, enabling granular tracking of redemption behavior and cost-efficient distribution across multiple jurisdictions. Parallel growth in open-loop prepaid cards for gig-economy payouts extends the addressable base, while government stimulus transfers over prepaid rails reinforce the product’s public-sector relevance. Adoption also benefits from the interoperability of gift cards with mobile wallets, allowing instant issuance and seamless redemption inside consumer super-apps. Despite the positive outlook, issuers face higher fraud-management costs, interchange fee pressures, and new breakage-reserve rules that compress legacy revenue pools. Nonetheless, sustained investment in compliance, tokenization, and artificial-intelligence fraud tools positions the leading participants to capture incremental volumes and protect margins in the medium term.

Key Report Takeaways

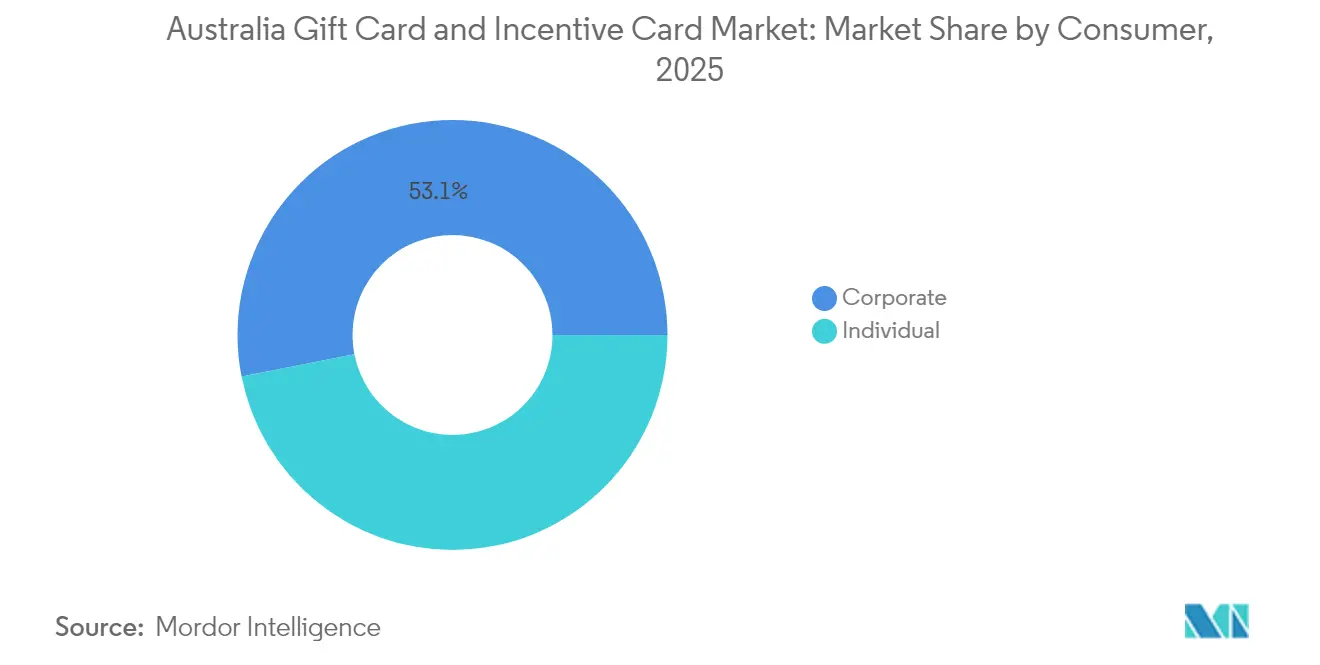

- By consumer, the corporate segment led with 53.10% of the Australian Gift Card and Incentive Card market share in 2025 and is forecast to expand at a 12.85% CAGR to 2031.

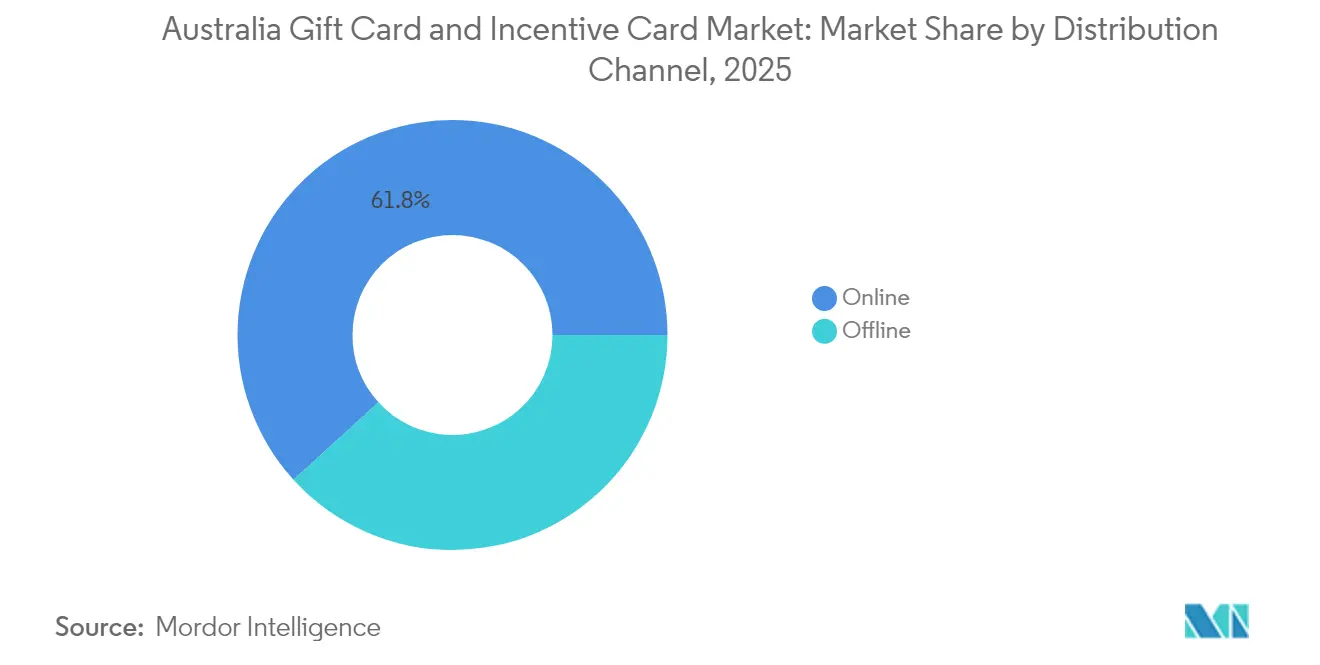

- By distribution channel, online captured 61.75% of the Australian Gift Card and Incentive Card market size in 2025 and is advancing at a 16.05% CAGR through 2031.

- By product, e-gift cards accounted for 69.10% of the Australian Gift Card and Incentive Card market size in 2025 and are growing at a 18.85% CAGR to 2031.

- By geography, New South Wales held 31.40% of the Australian Gift Card and Incentive Card market share in 2025, while Tasmania is recording the highest forecast CAGR at 11.95% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitisation of B2B incentives | +1.2% | National, with early adoption in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Rising employee experience budgets post-pandemic | +1.5% | National, concentrated in major corporate centers | Short term (≤ 2 years) |

| Integration of gift cards into super-app ecosystems | +0.8% | APAC spillover, strongest in Melbourne, Sydney | Long term (≥ 4 years) |

| Open-loop prepaid adoption for gig-economy payouts | +0.6% | National, with concentration in urban delivery markets | Medium term (2-4 years) |

| Government stimulus disbursement via prepaid rails | +0.4% | National, coordinated through federal and state programs | Short term (≤ 2 years) |

| ESG-linked consumer reward programmes | +0.3% | National, led by corporate sustainability initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitization of B2B Incentives

Corporate Australia’s pivot from physical merchandise to API-enabled digital rewards now defines how firms manage employee recognition, supplier payments, and customer acquisition. Prezzee disclosed USD 2.18 billion (AUD 3.4 billion) in card sales alongside 178% revenue growth, signaling keen enterprise appetite for instant, trackable incentives. Human-resources platforms integrate gift-card APIs directly into performance suites, triggering real-time delivery upon completion of defined tasks or milestones. Executives value the transparent redemption data that enables granular ROI calculations, while finance teams favor the simplified reconciliation workflows relative to traditional procurement. Supplier-relationship managers employ digital cards as spot bonuses for early delivery or quality compliance, broadening use cases beyond employees. Marketing departments run influencer campaigns where redemptions serve as conversion proxies, turning gift-card data into actionable customer-journey insights. These cumulative effects elevate digital incentives from peripheral perks to strategic levers that shape workforce engagement and partner ecosystems.

Rising Employee Experience Budgets Post-Pandemic

Australian companies lifted employee-experience allocations by 40%-60% after 2024, channeling sizable portions into wellness stipends, remote-work allowances, and retention bonuses via gift cards. Tight labor markets compel employers to differentiate value propositions without permanently inflating wage bills; prepaid incentives provide a flexible, tax-advantageous mechanism that resonates with staff. Medibank’s Live Better platform illustrates the trend by rewarding 823,000+ members through health-oriented gift card redemptions. Finance leaders welcome the budgetary control inherent in fixed-denomination digital cards, while HR appreciates the morale lift tied to immediate, personalized rewards. Technology integrations ensure frictionless distribution, eliminating manual request forms that once delayed employee benefits. Analytics dashboards report redemption velocity and category preferences, enabling data-driven refinement of benefit policies. This institutionalization of gift-card stipends cements prepaid instruments as enduring fixtures of the future workplace.

Integration of Gift Cards into Super-App Ecosystems

Australia’s fintech landscape increasingly mirrors Asian super-apps where multipurpose wallets host ride-booking, food delivery, and financial services. Within these platforms, gift cards function as interoperable value tokens transferable across service verticals, amplifying their utility beyond single-merchant redemption [1]Australian Competition and Consumer Commission, “Payment Surcharges,” accc.gov.au. . Expatriates purchase Australian gift cards abroad, enabling cross-border gifting and low-cost remittance corridors that bypass legacy wire networks. Loyalty operators embed gift-card APIs to convert points to spendable value within super-apps, lifting redemption rates while capturing customer-journey data. Merchants gain incremental reach as cards circulate in closed-loop ecosystems that aggregate consumer demand. Developers exploit programmable features such as category spend limits to craft context-aware incentives tied to location or time, further embedding gift cards into daily routines. These dynamics broaden the Australian Gift Card and Incentive Card market as super-apps scale nationwide.

Open-Loop Prepaid Adoption for Gig-Economy Payouts

Delivery and rideshare platforms increasingly rely on Visa- or Mastercard-branded gift cards to compensate contractors for performance bonuses, referral rewards, and peak-hour surges[2]DoorDash, “DoorDash Australia,” doordash.com. . This strategy circumvents complex payroll onboarding while granting recipients immediate spending flexibility across Australia’s retail network. Seasonal spikes in delivery demand create transient workforces that traditional bank-account onboarding cannot economically support. Open-loop prepaid cards also operate as acquisition levers, with gig companies issuing small-value sign-on bonuses to attract new drivers. Push-to-card APIs enable same-day disbursement, which enhances contractor liquidity and platform loyalty. Issuers glean data on end-merchant spending that informs targeted promotions, fostering deeper engagement loops. As gig platforms disseminate across secondary cities, open-loop gift cards anchor inclusive financial access where conventional banking penetration is shallow.

Government Stimulus Disbursement via Prepaid Rails

Federal and state authorities deploy prepaid cards to expedite economic-relief payments and targeted stimulus packages, recognizing the speed and fiscal traceability advantages over paper checks[3]Reserve Bank of Australia, “Review of Retail Payments Regulation,” rba.gov.au. . Pre-loaded cards ensure funds flow to intended recipients without requiring bank accounts, aiding financially vulnerable households. Real-time monitoring tools alert agencies to suspicious patterns, satisfying anti-money-laundering mandates while reducing administrative leakage. Partnerships with supermarkets and pharmacy chains broaden acceptance footprints, enabling beneficiaries to purchase essential goods close to home. Digital issuance cuts program-deployment timelines from months to weeks, strengthening policy responsiveness. Moreover, unspent balances flow back to the treasury after mandated durations, enhancing fiscal stewardship. Such deployment normalizes prepaid infrastructure inside public-sector payment architecture, indirectly bolstering commercial adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chargeback and fraud exposure in card-not-present transactions | -0.9% | National, concentrated in high-volume online redemption markets | Short term (≤ 2 years) |

| High breakage liability under revised ASIC guidelines | -0.7% | National, affecting all licensed gift card issuers | Medium term (2-4 years) |

| Rising interchange and scheme fees squeezing margins | -1.0% | National, with greater impact on low-margin retail issuers | Medium term (2–4 years) |

| Saturation of retail closed-loop cards | -0.8% | Urban centers with high retailer density and mature programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chargeback and Fraud Exposure in Card-Not-Present Transactions

Digital gift card rails attract sophisticated fraud rings that exploit rapid activation and irreversible redemptions, leaving issuers to absorb chargeback costs. Bulk corporate purchases heighten vulnerability because streamlined KYC processes can inadvertently lower authentication barriers. Card-not-present fraud rates for prepaid products run 3-5× higher than conventional cards, prompting expensive investments in AI-driven anomaly detection. Merchants face authorization holds that impede cash flow, while consumers risk delayed benefit receipt during dispute investigations. Regulatory mandates under ASIC’s ePayments Code require robust remediation protocols, increasing operational overhead for compliance. Reputation damage compounds financial losses when high-profile breaches undermine confidence in digital incentives. Persistent threat evolution forces continuous platform upgrades, eroding small issuers’ margins and potentially accelerating industry consolidation.

High Breakage Liability Under Revised ASIC Guidelines

ASIC’s 3-year minimum expiry and tightened fee rules diminish breakage income that once underwrote a substantial portion of program economics[4]Australian Securities and Investments Commission, “Regulatory Resources – Payment Systems,” asic.gov.au.. Issuers must now maintain enlarged balance-sheet provisions for unredeemed value, thereby raising capital-intensity and depressing returns on equity. Retailers reluctant to pay higher merchant service fees may scale back gift-card promotions, curbing sales volumes. Smaller fintech entrants lacking deep capital reserves struggle to comply, tilting competitive advantage toward well-capitalized incumbents. Accounting complexities increase as firms shift from recognition of immediate revenue toward deferred liability treatment, complicating investor communications. To offset lost breakage, issuers re-engineer products to generate interchange revenue or premium analytics services, but monetization lags regulatory cost escalation in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consumer: Corporate Dominance Drives Market Evolution

Corporate buyers controlled 53.10% of Australia Gift Card and Incentive Card market size in 2025, reflecting a decisive swing in incentive strategy that favors digital cards over legacy merchandise rewards. Enterprise procurement teams cite tax efficiency, denomination flexibility, and seamless API integration as leading drivers of adoption, resulting in a projected 12.85% CAGR through 2031 that outpaces individual-consumer growth. HR leaders bundle gift cards into wellness stipends, retention bonuses, and recognition programs that generate quantifiable engagement metrics. Finance departments, meanwhile, appreciate the straightforward reconciliation of prepaid instruments, which eliminates vendor-invoice clutter and reduces audit complexity. Analytics dashboards render redemption behavior by region, department, and demographic, enabling iterative program design that optimizes ROI. In contrast, individual consumers, holding 46.90% share, confront discretionary-spend pressures amid rising living-cost indices, nudging gifting behavior toward experiential vouchers rather than retail-centric cards.

Corporate segment expansion accelerates innovation in issuance platforms, with enterprise clients demanding role-based user access, SSO compatibility, and automated tax reporting workflows. Vendors respond with white-label portals that embed directly into procurement suites, shortening deployment cycles from months to days. Dynamic denomination engines allow managers to tailor reward value to performance tiers without revisiting contract terms, enhancing program agility. Multi-currency functionality supports cross-border teams in New Zealand and Singapore, broadening the regional influence of Australian-issued incentives. Compliance modules incorporate AML screening and GST mapping, simplifying governance in regulated industries such as financial services and healthcare. The spillover benefits include reduced paper-based processes, lower carbon footprints, and heightened transparency attributes that position corporate gift-card programs as best-practice benchmarks for digital remuneration.

By Distribution Channel: Digital Transformation Accelerates

Online channels captured 61.75% of the Australian Gift Card and Incentive Card market size in 2025, propelled by enterprise bulk-purchase portals and consumer appetite for instant gratification. Robust 16.05% CAGR to 2031 stems from scalable cloud infrastructure that automates issuance, reduces per-unit fulfillment costs, and provides audit-grade transaction logs. Mobile-wallet integrations push redemption experiences directly to smartphones, bypassing physical logistics and elevating customer satisfaction scores. API connectivity with ERP platforms means corporate buyers can link incentives to sales performance dashboards in real time. Fraud-management rules engines within digital storefronts apply velocity filters and device-fingerprinting, mitigating card-not-present risks that historically hampered online expansion. Personalized landing pages support cause-marketing campaigns, where consumers send gift cards tied to charity donations, broadening engagement. The Australian Gift Card and Incentive Card market, therefore, benefits from the virtuous loop of speed, data richness, and operating expense reduction offered by digital channels.

Offline distribution retains a 38.25% share, sustained by supermarket chains, convenience stores, and post-office kiosks that cater to demographics favoring tangible cards or lacking digital payment credentials. Woolworths and Coles leverage extensive brick-and-mortar networks to position card kiosks in high-traffic aisles, capturing impulse purchasers during routine grocery trips. Retailers cross-promote with loyalty programs, granting bonus points for in-store gift-card purchases that in turn drive repeat footfall. Hybrid fulfillment models gain traction: consumers order online and collect sealed gift-card packs at customer-service desks within hours, merging digital convenience with physical assurance. Merchants monetize end-cap real estate by renting shelf space to issuers seeking brand visibility, creating ancillary revenue streams. Yet rising real-estate costs, shrinkage risks, and sustainability imperatives gradually erode the offline channel’s relative profitability. Consequently, retailers accelerate digital-wallet tie-ins to meet evolving shopper expectations, ensuring channel coexistence rather than displacement.

By Product: E-Gift Cards Reshape Market Dynamics

EGift cards dominated the Australian Gift Card and Incentive Card market in 2025, capturing 69.10% of the total market share and establishing themselves as the standard for immediacy, flexibility, and data-driven incentive design. Both corporate demand for streamlined, automated delivery and consumer preference for smartphone-native, digital experiences drive their popularity. A projected CAGR of 18.85% through 2031 reflects the sustained growth momentum of this format. Businesses increasingly view gift cards as strategic engagement tools rather than simple rewards. Digital formats eliminate plastic production and logistics, aligning with corporate ESG mandates and reducing unit costs. Issuers layer conditional logic onto codes, such as merchant category limitations or staggered activation dates, enabling sophisticated, regulatory-compliant payouts. Real-time tracking of email or SMS delivery confirms receipt, while reminder notifications spur redemption and minimize dormant balances. Retail partners value the ability to offer variable-value cards without physical SKU proliferation, streamlining inventory management. The Australian Gift Card and Incentive Card market thus increasingly orients product roadmaps around digital-first architectures that support continuous innovation.

Physical cards, holding 30.90% share, remain relevant for ceremonial gifting occasions, point-of-sale upsells, and consumers lacking reliable digital identities Customized packaging, metallic foils, and tactile finishes provide an experiential premium that some employers favor for milestone awards Retailers bundle physical gift cards with complementary products such as confectionery or greeting cards to drive basket-size growth However, environmental concerns over PVC waste and surging courier fees sharpen cost scrutiny, prompting issuers to experiment with recyclable substrates and biodegradable inks Dual-path hybrid cards that store a QR-code link to a digital balance attempt to merge tangibility with mobile convenience Over the forecast horizon, physical share is projected to decline gradually but persist as a niche anchored in high-touch gifting rituals.

Geography Analysis

New South Wales accounted for 31.40% of Australia Gift Card and Incentive Card market share in 2025, reflecting Sydney’s dense concentration of Fortune 500 regional headquarters and advanced fintech ecosystem. High average disposable incomes and sophisticated shopper loyalty schemes reinforce sustained B2C purchases, while large enterprise clusters generate sizable B2B volumes. The state government’s tech-friendly regulatory stance and digital-identity pilots further accelerate prepaid adoption in public-sector programs. Victoria followed with 25.60% share, leveraging Melbourne’s robust professional-services base and vibrant startup community that pilots API-driven gift-card innovations. Retail density along Bourke Street Mall and plentiful co-working hubs facilitate both consumer and corporate uptake, while universities deploy prepaid cards for student disbursements, adding incremental demand. Queensland held 17.40% share, buoyed by Brisbane’s post-pandemic tourism rebound and event-driven spending linked to upcoming international sporting fixtures.

Western Australia and South Australia jointly contributed 17.20% share, with mining and energy firms issuing cards to reward remote-site employees and contractor suppliers. Strong fly-in-fly-out workforces value gift cards redeemable nationwide, supporting financial inclusivity in isolated regions. Tasmania, albeit small in absolute terms, leads growth at 11.95% CAGR to 2031, propelled by government-mandated gaming pre-commitment systems that rely on prepaid cards for harm-minimization. The Australian Capital Territory leverages federal-government procurement programs to issue prepaid incentives for community initiatives, while the Northern Territory explores prepaid disbursements within indigenous-economic-development schemes. Geographic disparities in regulatory incentives, broadband penetration, and retail-network maturity shape distinct adoption curves, but national interoperability ensures that cardholders enjoy consistent redemption experiences across state borders.

Competitive Landscape

The Australia Gift Card and Incentive Card market shows moderate concentration, with the top five providers holding a significant majority of the market. Blackhawk Network leads the space, followed by strong competition from Prezzee and InComm Payments. Market leaders wield scale advantages in compliance staffing, issuer-processing capacity, and merchant-network breadth, allowing them to absorb ASIC’s heightened breakage-reserve requirements more comfortably than smaller rivals. Vertical integration deepens moats: supermarkets such as Woolworths and Coles extend from physical distribution into digital issuance via proprietary apps, thereby enclosing consumers within closed-loop ecosystems. Technology specialists double down on artificial-intelligence fraud suites that differentiate platform security, while merchant analytics dashboards open new revenue streams through upsell recommendations. API-first disruptors position themselves as white-label issuance engines powering banks, HR platforms, and loyalty programs that lack in-house prepaid capabilities.

Cross-border virtual gift cards emerge as a contested space as tourism revives and foreign consumers seek to preload spending before arrival. Incumbents pilot multi-currency cards with dynamic FX conversion, but nimble fintech entrants leverage blockchain tokenization to expedite settlement and lower costs. ESG-linked incentives offer adjacent battlegrounds where providers bundle carbon-offset certificates alongside standard denominations, appealing to corporates with net-zero ambitions. Strategic partnerships proliferate: Blackhawk Network’s acquisition of Tango Card deepened its B2B suite, while Aevi’s alliance with Paydock created omnichannel orchestration that broadens redemption endpoints. Consolidation continues as Lesaka Technologies absorbed Adumo to scale payment infrastructure, signaling investor appetite for synergistic platform roll-ups.

Regulatory compliance remains a key differentiator; operators with seasoned legal teams navigate AML/CTF Amendment Act 2024 reporting burdens more effectively, offering assurance to risk-averse enterprise buyers. Meanwhile, platform extensibility matters: vendors providing SDKs and sandbox testing environments attract developers eager to embed incentive flows into super-apps, gig portals, and e-commerce plugins. Data-privacy credentials influence public-sector tenders, with ISO 27001 certifications and local data-center footprints acting as gating factors. As competition intensifies, pricing war potential is tempered by high fixed compliance costs, anchoring a rational economic environment where value-added services, not discounting, decide market-share shifts.

Australia Gift Card And Incentive Card Industry Leaders

Blackhawk Network

Prezzee

InComm Payments

Edge Loyalty (Village Roadshow)

TCN – The Card Network

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Qantas announced comprehensive Frequent Flyer program changes effective August 2025, including up to 20% increases in Classic Flight Reward redemption costs and expanded partner airline access, reshaping corporate incentive program economics for companies using Qantas Points as employee rewards.

- October 2024: Aevi partnered with Paydock to deliver unified omnichannel payment orchestration, combining in-store and e-commerce capabilities that enable retailers to accept online payment methods in face-to-face environments, potentially expanding gift card redemption options across physical and digital channels.

- August 2024: Woolworths Group reported 9.8 million active Australian Everyday Rewards members with 137% growth in Everyday Extra paid subscribers, highlighting the scale of loyalty program infrastructure that supports gift card distribution and targeted incentive delivery across Australia's largest grocery network.

- May 2024: Lesaka Technologies announced acquisition of payments platform Adumo with backing from institutional investors Apis and ARC, signaling continued consolidation in Australia's payments infrastructure sector and potential expansion of gift card processing capabilities.

Australia Gift Card And Incentive Card Market Report Scope

A gift card is a prepaid debit card loaded with funds for future use, which can be used to make purchases and other financial transactions. A complete background analysis of the market, which includes a market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report. Australia Gift Card and Incentive Card Market is segmented by Consumer (Individual and Corporate (Small scale, Mid-tier, and Large enterprise)), by distribution channel (Online and offline), and by product (e-gift card and physical card). The report offers market size and forecasts for Australia Gift Card and Incentive Card Market in value (USD Million) for all the above segments.

By Consumer

| Individual | |

| Corporate | Small Scale |

| Mid-tier | |

| Large Enterprise |

By Distribution Channel

| Online |

| Offline |

By Product

| E-Gift Card |

| Physical Card |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Australian Capital Territory |

| Northern Territory |

| By Consumer | Individual | |

| Corporate | Small Scale | |

| Mid-tier | ||

| Large Enterprise | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Product | E-Gift Card | |

| Physical Card | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| South Australia | ||

| Tasmania | ||

| Australian Capital Territory | ||

| Northern Territory | ||

Key Questions Answered in the Report

How large is the Australia Gift Card and Incentive Card market in 2026?

The market is valued at USD 14.61 billion in 2026 and is on track to reach USD 20.63 billion by 2031, reflecting a 7.15% CAGR.

Which segment represents the largest share by consumer type?

Corporate buyers represent 53.10% of total value and are growing at 12.85% CAGR, highlighting their pivotal role in market expansion.

What drives the rapid rise of e-gift cards?

Instant digital delivery, reduced logistics costs, and integration with mobile wallets have propelled e-gift cards to 69.10% share with a 18.85% growth rate.

Which Australian state leads in gift-card adoption?

New South Wales leads with 31.40% share, benefiting from Sydney’s dense corporate presence and advanced fintech ecosystem.

What is the primary regulatory challenge facing issuers?

ASIC’s tighter breakage-reserve rules extend expiry periods and compel higher balance-sheet provisions, squeezing traditional breakage revenue streams.

Page last updated on: